Australia Application Processor Market Size, Share, Trends and Forecast by Device Type, Core Type, and Region, 2026-2034

Australia Application Processor Market Summary:

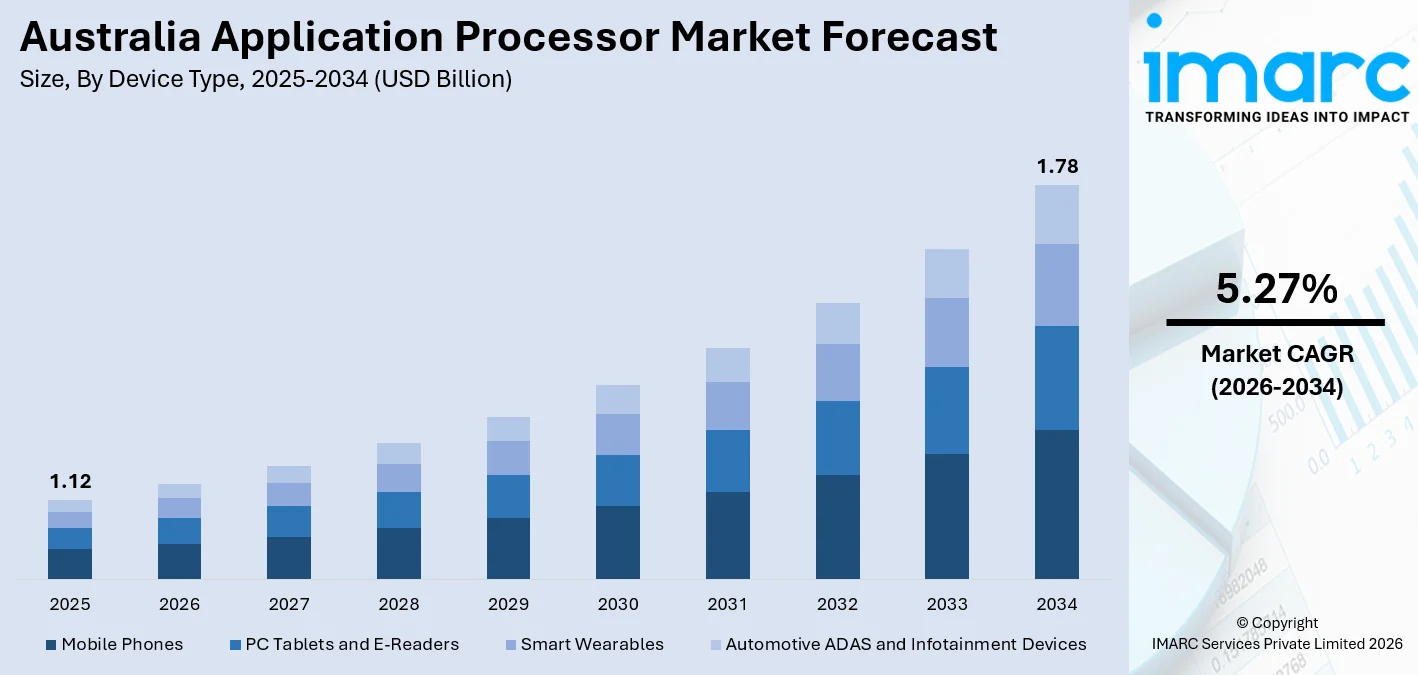

The Australia application processor market size was valued at USD 1.12 Billion in 2025 and is projected to reach USD 1.78 Billion by 2034, growing at a compound annual growth rate of 5.27% from 2026-2034.

The Australia application processor market is expanding steadily, driven by the rapid proliferation of smart devices, nationwide 5G deployment, and the growing integration of artificial intelligence at the edge. Rising consumer demand for premium smartphones and next-generation wearables is intensifying the need for high-performance processing solutions. The automotive sector is also emerging as a significant demand driver, with increasing adoption of advanced driver-assistance systems and in-vehicle infotainment platforms. Additionally, the expanding internet of things ecosystem across healthcare, industrial, and smart-home applications continues to fuel processor innovation. These interconnected dynamics are collectively shaping the Australia application processor market share.

Key Takeaways and Insights:

- By Device Type: Mobile phones dominate the market with a share of 40% in 2025, driven by persistent consumer upgrades to 5G-capable flagship handsets, deepening smartphone penetration in both urban and regional communities, and strong retail demand for AI-powered features including real-time language processing and enhanced computational photography.

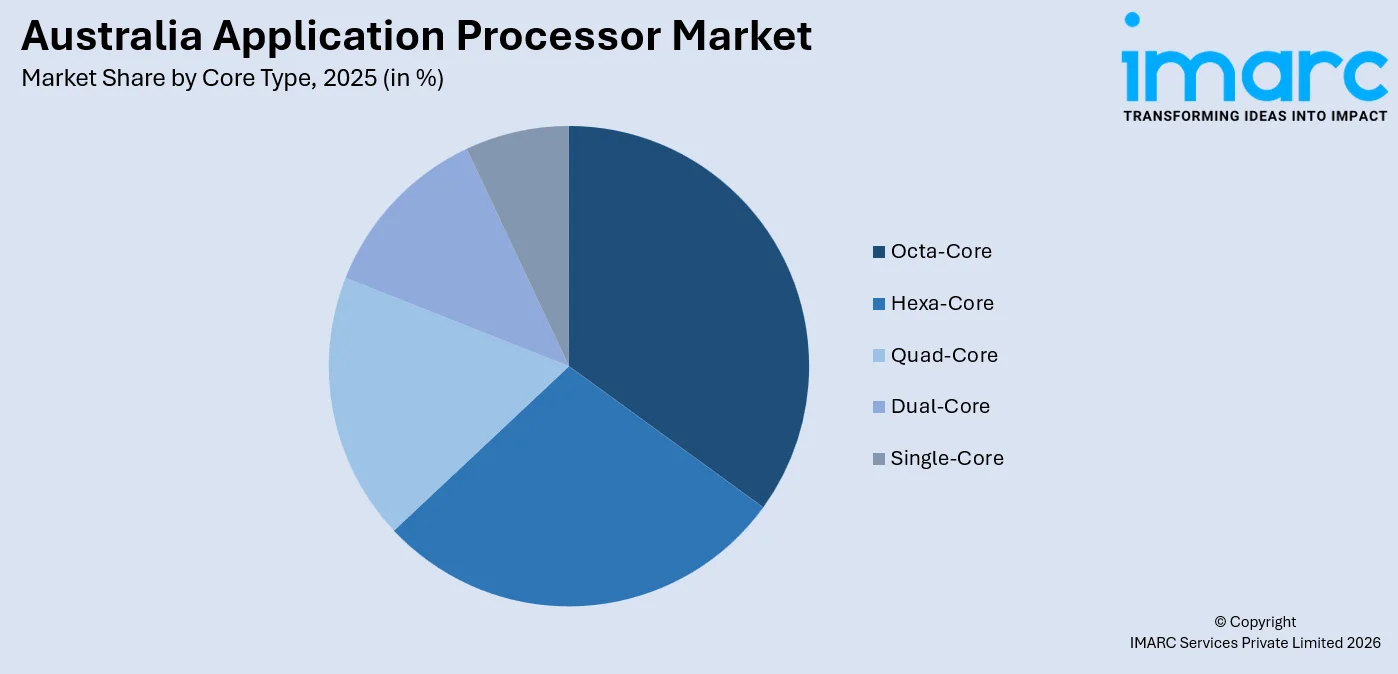

- By Core Type: Octa-core leads the market with a share of 35% in 2025, reflecting widespread preference among device manufacturers for processors that deliver optimised multitasking performance, improved power management, and seamless support for demanding applications such as mobile gaming, high-resolution streaming, and AI-enabled functions.

- Key Players: Key players in the Australia application processor market advance growth by launching AI-integrated, energy-efficient processor architectures, investing in 5G-optimised chip designs, and forging strategic partnerships with device manufacturers. Their focus on localised innovation and edge computing capabilities strengthens competitive positioning across consumer and industrial segments.

To get more information on this market Request Sample

The Australia application processor market is undergoing significant transformation, driven by the convergence of mobile connectivity, artificial intelligence, and a rapidly expanding device ecosystem. The nationwide rollout of next-generation network infrastructure has created fertile ground for advanced processor architectures capable of supporting higher data throughput and lower latency requirements across modern mobile applications. Simultaneously, growing consumer preference for premium smartphones, smart wearables, and connected automotive platforms is intensifying demand for sophisticated processing solutions that deliver enhanced performance, energy efficiency, and on-device intelligence. Enterprise digitisation across healthcare, industrial automation, and transportation sectors is further broadening the addressable market beyond traditional consumer electronics. This confluence of infrastructure investment, consumer premiumisation, and multi-sector IoT adoption signals a maturing market where processor demand is being shaped by both technological advancement and evolving end-user expectations across diverse application segments.

Australia Application Processor Market Trends:

Rising Integration of On-Device Artificial Intelligence:

Application processors in Australia are increasingly incorporating dedicated neural processing units that enable advanced on-device AI workloads without cloud dependency. This architectural shift supports privacy-sensitive applications across healthcare diagnostics, augmented reality, and biometric authentication. In January 2025, Samsung launched the Galaxy S25 series in Australia, powered by the Snapdragon 8 Elite chip featuring dedicated AI acceleration hardware, enabling real-time task management and AI-driven voice assistance directly on the device, exemplifying the industry-wide pivot toward embedded intelligence in premium consumer electronics.

Acceleration of 5G-Optimised Processor Architectures:

The progressive rollout of 5G networks across Australian metropolitan and regional corridors is compelling semiconductor manufacturers to redesign application processor architectures for improved connectivity performance. Processors are now integrating advanced baseband modems alongside multi-core CPU clusters to handle high-bandwidth cloud gaming, telehealth services, and enterprise mobility. In February 2025, Telstra announced an AUD 800 million infrastructure investment programme spanning four years, signalling sustained commitment to advanced connectivity that directly stimulates demand for 5G-compatible processing solutions in both consumer and industrial device categories.

Expansion of Application Processors Into Automotive and Wearable Segments:

Beyond smartphones, application processors are rapidly penetrating the automotive advanced driver-assistance systems segment and smart wearables market in Australia. Vehicle manufacturers are deploying increasingly sophisticated infotainment and safety computing platforms, while consumer demand for smartwatches and fitness-tracking devices continues to expand. In October 2024, Bosch and Tenstorrent partnered to standardise chiplet-based automotive processors, targeting lower-cost, AI-capable compute across cockpit, ADAS, and connectivity systems, a development with direct relevance to the Australian automotive technology supply chain and its growing demand for high-performance embedded processors.

Market Outlook 2026-2034:

The application processor market in Australia has tremendous scope to grow in the forecast period due to increasing smartphone penetration rates, rising enterprise Internet of Things adoption rates, and increasing investment in 5G infrastructure. The increasing demand for application processors in premium smartphone users, health monitoring device manufacturers, and automotive electronics designers will help to diversify revenue streams and reduce dependence on any one device category. The increasing miniaturization of semiconductor nodes and the increasing adoption of heterogeneous computing architectures with CPUs, GPUs, and Neural Processing Units will help application processor manufacturers to serve a wider range of application requirements in terms of performance and power efficiency. The emerging application processor market in health monitoring wearables, autonomous vehicle platforms, and edge-AI industrial systems is expected to add to the diversification in application processor market growth in Australia during the forecast period. The market generated a revenue of USD 1.12 Billion in 2025 and is projected to reach a revenue of USD 1.78 Billion by 2034, growing at a compound annual growth rate of 5.27% from 2026-2034.

Australia Application Processor Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Device Type |

Mobile Phones |

40% |

|

Core Type |

Octa-Core |

35% |

Device Type Insights:

- Mobile Phones

- PC Tablets and E-Readers

- Smart Wearables

- Automotive ADAS and Infotainment Devices

Mobile phones dominate with a share of 40% of the total Australia application processor market in 2025.

Mobile phones remain the primary demand engine for application processors in Australia, sustained by robust consumer appetite for flagship smartphones with advanced computational capabilities. The continued transition to 5G handsets necessitates processors equipped with integrated high-speed modems, multi-core CPU clusters, and dedicated AI acceleration engines. Australian consumers exhibit strong affinity for premium device categories, with manufacturers consistently upgrading silicon generations to support features such as computational photography, real-time language translation, and immersive gaming experiences. The replacement cycle dynamics, combined with evolving carrier subsidies tied to 5G plan adoption, ensure a reliable pipeline of device upgrades that anchor processor demand.

The integration of on-device AI capabilities within mobile processors represents a structural shift that is particularly pronounced in Australia's consumer electronics market. In January 2025, Samsung introduced the Galaxy S25 series powered by the Qualcomm Snapdragon 8 Elite, which includes a dedicated neural processing unit enabling advanced AI-driven functionalities such as contextual voice recognition and intelligent camera optimisation. This launch exemplifies the broader trend of processor manufacturers embedding AI cores as standard components in flagship mobile silicon, reinforcing the mobile phones segment's dominant position within Australia's application processor ecosystem throughout the forecast period.

Core Type Insights:

Access the comprehensive market breakdown Request Sample

- Octa-Core

- Hexa-Core

- Quad-Core

- Dual-Core

- Single-Core

Octa-core leads the market with a share of 35% of the total Australia application processor market in 2025.

Octa-core processors have established themselves as the preferred architecture across premium and mid-range device categories in Australia, delivering the parallel processing capability required for modern multitasking workloads. The eight-core configuration allows processor designers to implement heterogeneous arrangements that pair high-performance cores for computationally intensive tasks with efficiency cores for sustained, low-power operations. This architecture directly addresses the Australian consumer demand for smartphones and tablets that simultaneously support graphics-intensive gaming, high-resolution streaming, and AI-powered background processes without compromising battery longevity or device thermals.

The evolution of octa-core architecture is exemplified by the latest generation of flagship processors, which incorporate dedicated AI processing hardware alongside distinct performance and efficiency core clusters. This combination enables real-time natural language processing, advanced computational imaging, and low-latency gaming experiences that resonate strongly with Australia's technology-forward consumer segment. As device manufacturers continue to position octa-core silicon as the standard for flagship product tiers, deploying it across premium smartphones, high-performance tablets, and advanced wearable platforms, this segment's market leadership is expected to remain robust throughout the forecast period.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory and New South Wales collectively represent the largest regional segment within the Australia application processor market. The concentration of technology enterprises, financial services firms, and government institutions in Sydney and Canberra sustains substantial demand for advanced processing solutions across premium smartphones, enterprise mobile devices, and connected infrastructure platforms. High average consumer incomes in the Sydney metropolitan area support strong uptake of flagship handsets with cutting-edge processor technology. The region's robust startup and innovation ecosystem, particularly within Sydney's technology precincts, further drives demand for next-generation application processors across emerging IoT and edge-AI applications.

Victoria and Tasmania constitute a significant regional market anchored by Melbourne's role as Australia's second-largest commercial hub. Demand is supported by a diversified economic base spanning professional services, retail, and advanced manufacturing, which drives adoption of smart devices and embedded processing platforms across both consumer and enterprise segments.

Queensland represents a growing regional market driven by expanding urbanisation in Brisbane and the surrounding South-East Queensland corridor. Consumer electronics adoption is rising alongside infrastructure investments ahead of the 2032 Brisbane Olympic Games, with increased connectivity and smart city initiatives stimulating demand for advanced application processors across mobile and IoT device categories.

The Northern Territory and Southern Australia exhibit relatively smaller but strategically important market dynamics, characterised by demand for ruggedised and power-efficient processors in remote industrial and resource sector applications. Satellite and wireless connectivity expansion programmes are gradually enabling broader smart device adoption across geographically dispersed communities.

Western Australia's application processor market is shaped by the state's resource-intensive economy, where demand for industrial IoT processors and embedded computing solutions in mining and energy applications complements consumer electronics growth in the Perth metropolitan area. The state's geographic remoteness and specialised industrial requirements create distinct processor demand patterns differentiated from eastern seaboard markets.

Market Dynamics:

Growth Drivers:

Why is the Australia Application Processor Market Growing?

Nationwide 5G Network Expansion Driving Processor Demand

The progressive deployment of 5G infrastructure across Australia is fundamentally reshaping the application processor landscape by establishing demanding new performance benchmarks for mobile silicon. High-bandwidth, low-latency 5G connectivity necessitates processors equipped with advanced integrated modems, multi-core processing clusters, and energy-efficient architectures capable of sustaining continuous connectivity without compromising battery performance. Australian telecommunications providers have committed to extensive coverage programmes across metropolitan, suburban, and regional areas, progressively extending 5G access to a greater proportion of the population. This expanding coverage footprint is driving consumer and enterprise device upgrade cycles as users seek handsets and connected devices fully optimised for 5G capabilities. As 5G penetration deepens, processor manufacturers face intensifying demand for silicon architectures that can seamlessly support cloud gaming, real-time telehealth consultations, autonomous vehicle communications, and enterprise IoT connectivity, all of which rely on the concurrent processing performance that advanced application processors uniquely provide.

Growing Adoption of AI-Enabled Consumer and Industrial Devices

Artificial intelligence integration has evolved from a differentiating feature to a fundamental requirement across consumer electronics and industrial device categories in Australia. Application processors are now routinely expected to incorporate dedicated neural processing units that enable sophisticated on-device intelligence without reliance on latency-prone cloud inference pipelines. In the consumer segment, Australian users increasingly expect smartphones, wearables, and tablets to deliver personalised experiences through AI-driven photography enhancement, real-time translation, and context-aware voice assistance. In industrial and enterprise contexts, edge AI-enabled processors support predictive maintenance, remote asset monitoring, and autonomous quality inspection across mining, agriculture, and advanced manufacturing sectors. This type of indigenous innovation demonstrates that Australia's application processor ecosystem is not merely a consumer of imported silicon but an increasingly active contributor to global edge-AI processor development, broadening the market's domestic technology base and attracting further research investment.

Expanding IoT Ecosystem Across Healthcare, Automotive, and Smart Industry

The proliferation of internet of things applications across Australia's healthcare, automotive, and industrial sectors is creating a structurally diverse and resilient demand base for application processors beyond traditional consumer electronics. In healthcare, wearable biosignal monitoring devices and portable diagnostic tools require processors that combine precise real-time analytics with extremely low power consumption to support continuous patient monitoring over extended periods. The automotive sector is integrating increasingly sophisticated application processors into advanced driver-assistance systems, in-vehicle infotainment displays, and vehicle-to-everything communication modules as Australian automakers respond to evolving consumer and regulatory expectations. Industrial IoT deployments in remote monitoring, predictive maintenance, and smart energy management are further expanding the addressable market for application processors beyond conventional mobile device use cases. This multi-sector diversification strengthens market resilience and supports sustained volume demand for specialised processor solutions throughout the forecast period.

Market Restraints:

What Challenges the Australia Application Processor Market is Facing?

Global Semiconductor Supply Chain Vulnerabilities

The Australia application processor market remains exposed to disruptions in the global semiconductor supply chain, given the country's dependence on offshore fabrication from advanced foundries in Taiwan, South Korea, and the United States. Geopolitical tensions, manufacturing capacity constraints, and raw material shortages can cause procurement delays and price volatility that ripple through device manufacturers and ultimately affect the availability of advanced processors in the Australian market. Limited domestic fabrication infrastructure amplifies this vulnerability, constraining the ability of local device producers and technology companies to insulate themselves from external supply shocks.

High Cost of Premium Application Processors Limiting Mid-Market Penetration

The rapid advancement of processor technology, while driving performance improvements, simultaneously elevates the cost of cutting-edge silicon, creating price barriers that limit widespread adoption of high-performance processors in mid-market and value-segment devices. In Australia's comparatively small consumer electronics market, the economics of premium processor procurement can disproportionately affect device pricing, potentially deterring cost-sensitive consumer segments from upgrading to more capable handsets and wearables. These dynamic risks bifurcating the market between early adopters of advanced silicon and a broader consumer base that continues to utilise older processor generations with constrained AI and 5G capabilities.

Regulatory and Data Sovereignty Challenges in Edge-AI Deployments

The increasing deployment of AI-enabled application processors across healthcare, government, and financial services sectors in Australia raises complex regulatory questions around data sovereignty, algorithmic accountability, and cybersecurity compliance. Organisations deploying edge-AI processing solutions must navigate evolving legislative frameworks governing the storage and processing of sensitive personal and commercial data, which can extend procurement timelines and increase compliance costs. Uncertainty in regulatory requirements for AI-enabled devices may slow enterprise adoption rates and limit the pace at which advanced application processors penetrate high-value institutional market segments.

Competitive Landscape:

The Australia application processor marketplace has a concentrated competitive profile with a limited number of globally recognized semiconductor companies with advanced technology portfolios and distribution networks. The major players in the application processor marketplace in Australia are utilizing technology advancements in processor architecture, including multi-core processor technology, AI acceleration technology, and advanced fabrication technology, to maintain technology differentiation and premium price position. The competition in the application processor marketplace in Australia is increasing in terms of 5G modem technology integration, power consumption benchmarks, and developer support ecosystems. BrainChip Holdings, based in Australia, is a unique local player focusing on neuromorphic computing technology in edge-AI and industrial IoT segments. Technology partnerships between application processor and device manufacturers are considered major competitive factors in gaining design wins in consumer electronics and automotive segments.

Recent Developments:

- In November 2025, Sydney-based BrainChip Holdings announced AUD 37 Million capital raise to accelerate commercialisation of its Akida™ neuromorphic AI processor and fund development of next-generation edge-AI products, including generative AI platforms designed to run large language models on-device. The raise, fully underwritten at the institutional level, positions BrainChip to expand its hardware roadmap across aerospace, healthcare, smart home, and connected automotive applications.

- In February 2025, Samsung launched the Galaxy S25 series powered by the Snapdragon 8 Elite chip with advanced AI capabilities, with the devices made available in Australia from mid-February. The flagship smartphones feature dedicated neural processing units enabling on-device AI functions including real-time voice assistance and intelligent computational photography, marking a significant hardware upgrade cycle for the Australian premium smartphone segment.

Australia Application Processor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Device Types Covered | Mobile Phones, PC Tablets and E-Readers, Smart Wearables, Automotive ADAS and Infotainment Devices |

| Core Types Covered | Octa-Core, Hexa-Core, Quad-Core, Dual-Code, Single-Core |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Application Processor Market Report

The Australia application processor market size was valued at USD 1.12 Billion in 2025.

The Australia application processor market is expected to grow at a compound annual growth rate of 5.27% from 2026-2034 to reach USD 1.78 Billion by 2034.

Mobile phones dominated the market with a share of 40%, driven by strong consumer demand for 5G-capable smartphones and the integration of advanced AI processing capabilities within flagship handsets across Australia.

Key factors driving the Australia application processor market include nationwide 5G network expansion, growing adoption of AI-enabled consumer and industrial devices, and the proliferation of IoT applications across healthcare, automotive, and smart industry sectors.

Major challenges include global semiconductor supply chain vulnerabilities, high cost of premium processors limiting mid-market penetration, and evolving regulatory requirements around data sovereignty and AI compliance in enterprise deployments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)