Australia Biosimilar Market Size, Share, Trends and Forecast by Molecule, Manufacturing Type, Indication, and Region, 2026-2034

Australia Biosimilar Market Summary:

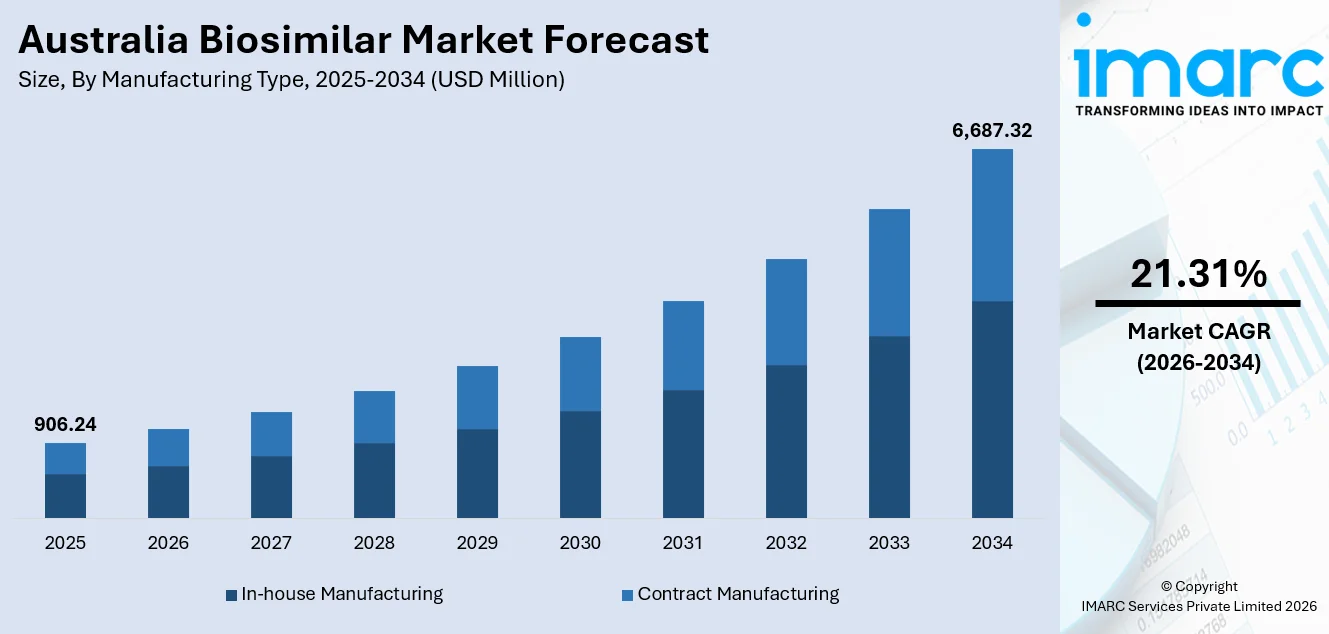

The Australia biosimilar market size was valued at USD 906.24 Million in 2025 and is projected to reach USD 6,687.32 Million by 2034, growing at a compound annual growth rate of 21.31% from 2026-2034.

The Australia biosimilar market is experiencing growth as the nation embraces cost-effective biologic alternatives to address escalating healthcare expenditures and rising chronic disease prevalence. Supportive government frameworks, expanding Pharmaceutical Benefits Scheme listings, and the growing clinical confidence in biosimilar therapies are collectively strengthening adoption across therapeutic categories. Advancements in biomanufacturing capabilities, increasing patent expirations of major reference biologics, and proactive regulatory reforms by the Therapeutic Goods Administration are accelerating market maturity, positioning Australia as a leading biosimilar destination in the Asia-Pacific region.

Key Takeaways and Insights:

- By Molecule: Adalimumab dominates the market with a share of 22.5% in 2025, driven by extensive Pharmaceutical Benefits Scheme (PBS)-listed biosimilar brands, widespread prescribing across autoimmune indications, and growing clinician acceptance of cost-effective biologic alternatives for chronic inflammatory conditions.

- By Manufacturing Type: In-house manufacturing leads the market with a share of 62.5% in 2025, reflecting the preference of established pharmaceutical companies to maintain quality control, protect proprietary processes, and ensure consistent supply of complex biosimilar products.

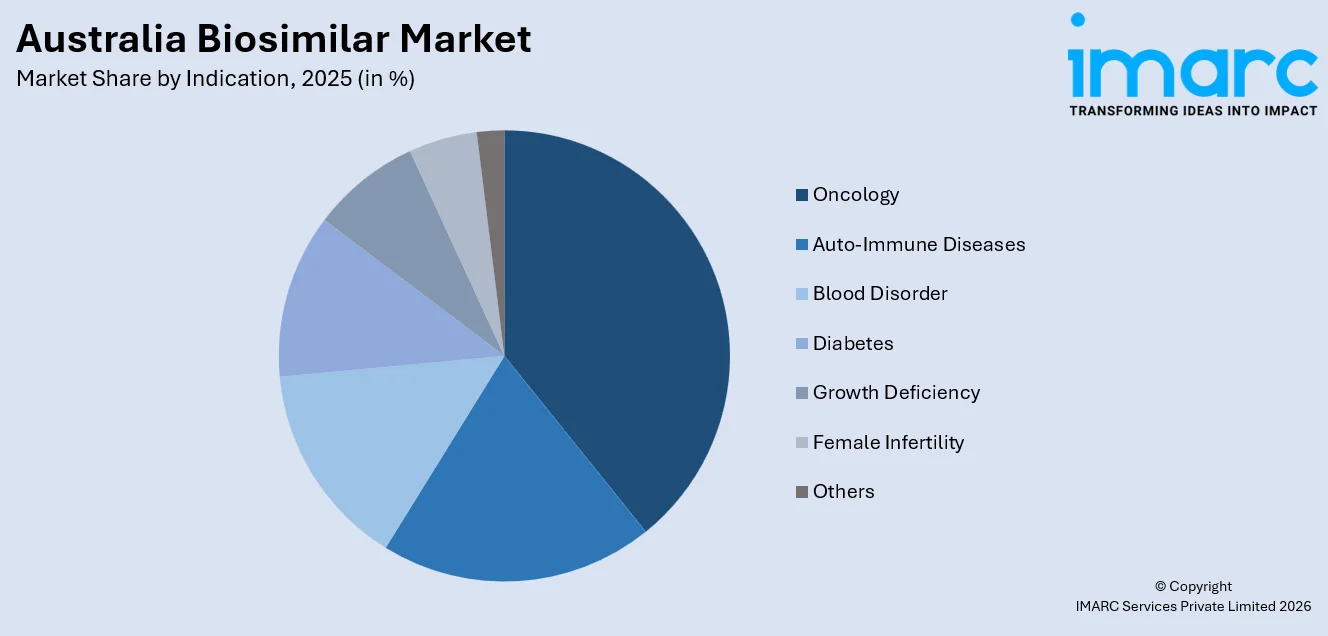

- By Indication: Oncology represents the largest segment with a market share of 38.5% in 2025, underpinned by the rising cancer burden across the Australian population, growing availability of oncology biosimilars such as trastuzumab and bevacizumab, and their PBS subsidization for hospital-administered cancer therapies.

- By Region: Australia Capital Territory & New South Wales dominate the market with a share of 32.5% in 2025, owing to the concentrated healthcare infrastructure, major teaching hospitals, higher specialist density, and advanced pharmaceutical distribution networks serving the region.

- Key Players: The Australia biosimilar market is highly competitive, with leading global biosimilar developers expanding product portfolios, securing TGA approvals, pursuing PBS listings, and forming strategic distribution partnerships to capture market share across oncology, immunology, and chronic disease therapeutic segments.

To get more information on this market Request Sample

The Australia biosimilar market is progressing steadily as regulatory refinement, physician education, and cost-containment priorities collectively support a structured shift from originator biologics to competitively priced biosimilar therapies. Strengthened evaluation pathways and growing clinical familiarity are reducing adoption barriers in complex treatment areas. This momentum was reinforced in 2025 when the Therapeutic Goods Administration approved Sandoz’s Tyruko® as the first natalizumab biosimilar in Australia, referencing Biogen’s Tysabri®. The 300mg/15mL intravenous infusion was indicated for relapsing remitting multiple sclerosis to delay disability progression and reduce relapse frequency, marking entry into a highly specialized neurology segment. Such approvals demonstrate regulatory confidence in biosimilar comparability standards and expand therapeutic competition beyond traditional high-volume categories. As more specialty biologics face exclusivity expiry, continued regulatory endorsement and clinical uptake are expected to deepen biosimilar penetration across advanced disease areas within Australia’s healthcare system.

Australia Biosimilar Market Trends:

Expansion into New Specialty Therapeutic Segments

Broadening biosimilar penetration into additional high-value specialty segments is a crucial trend impelling the market growth in Australia. Regulatory and reimbursement endorsements in complex therapy areas are strengthening competitive depth and widening treatment access. In 2025, the Pharmaceutical Benefits Advisory Committee recommended PBS listing for three Celltrion biosimilars: Eydenzelt® (aflibercept), Stoboclo®/Osenvelt® (denosumab), and Avtozma® (tocilizumab). Eydenzelt® became the first aflibercept biosimilar approved in Australia, while Avtozma® represented the first and only tocilizumab biosimilar approved and recommended for listing. Entry into ophthalmology, bone health, and immunology increases therapeutic coverage, stimulates price competition in specialist markets, and supports sustained expansion of Australia’s biosimilar portfolio.

Strengthened Reimbursement Support and Substitution Policies

Enhanced government reimbursement measures are playing a central role in accelerating biosimilar adoption across Australia. Expanded listing within the Pharmaceutical Benefits Scheme improves patient access while reinforcing cost-containment objectives in high-expenditure therapeutic areas. For instance, in 2024, the scheme listed 30 biosimilar brands across 12 active ingredients, with 18 designated as ‘a’ flagged to permit pharmacy-level substitution and activate statutory price reductions of up to 25% following the first biosimilar entry. These structured pricing and substitution mechanisms create immediate competitive pressure on originator biologics, encourage prescribing shifts, and deliver measurable savings to the public healthcare system. Such policy-backed incentives provide a stable demand environment, supporting sustained biosimilar market growth.

Rise of Domestic Biomanufacturing Infrastructure

Strengthening local biomanufacturing capacity is emerging as a significant factor propelling the growth of the Australia biosimilar market. Enhanced domestic production capabilities reduce reliance on imported biologics and improve supply chain resilience, supporting timely market entry of complex therapies. For example, in 2025, Queensland’s Deputy Premier unveiled ENTRI, an Australian-first on-demand cGMP biomanufacturing facility in Woolloongabba backed by more than AU$ 100 million in investment. The facility planned to provide advanced cleanrooms and manufacturing infrastructure to help biotech and medtech companies scale clinical-stage production locally. By bridging manufacturing gaps and accelerating translation from research to commercial supply, such infrastructure strengthens Australia’s ability to support biosimilar development, regulatory approval readiness, and long-term market expansion.

Market Outlook 2026-2034:

The Australia biosimilar market demonstrates exceptional growth potential throughout the forecast period, driven by accelerating patent expirations of major biologic therapies and increasing pressure to contain healthcare expenditure. As exclusivity periods lapse, opportunities expand for cost-effective alternatives to enter high-value therapeutic segments, including oncology, immunology, and endocrinology. The market generated a revenue of USD 906.24 Million in 2025 and is projected to reach a revenue of USD 6,687.32 Million by 2034, growing at a compound annual growth rate of 21.31% from 2026-2034.

Australia Biosimilar Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Molecule |

Adalimumab |

22.5% |

|

Manufacturing Type |

In-house Manufacturing |

62.5% |

|

Indication |

Oncology |

38.5% |

|

Region |

Australia Capital Territory & New South Wales |

32.5% |

Molecule Insights:

- Infliximab

- Insulin Glargine

- Epoetin Alfa

- Etanercept

- Filgrastim

- Somatropin

- Rituximab

- Follitropin Alfa

- Adalimumab

- Pegfilgrastim

- Trastuzumab

- Bevacizumab

- Others

Adalimumab leads with a share of 22.5% of the total Australia biosimilar market in 2025.

Adalimumab represents the largest segment driven by its wide therapeutic use across autoimmune conditions, such as rheumatoid arthritis, psoriasis, Crohn’s disease, and ulcerative colitis. The reference biologic recorded strong prescription volumes for years, creating a substantial patient base eligible for biosimilar transition. Once patent protections eased, multiple biosimilar versions entered the market, intensifying competition and improving affordability. Australia’s reimbursement system supports substitution of cost-effective alternatives, encouraging hospitals and specialists to adopt adalimumab biosimilars. High treatment duration and chronic disease management further sustain recurring demand. These factors collectively position adalimumab as the highest volume molecule segment in the biosimilar market.

Another reason for adalimumab’s dominance is the structured switching programs implemented across public health systems. Clear regulatory guidance confirming therapeutic comparability has supported clinician-led transitions toward cost-effective alternatives, while competitive hospital tendering has accelerated uptake of lower-priced variants. This structured market environment continues to evolve. In 2025, the PBAC published its March 2026 agenda including reimbursement consideration for adalimumab biosimilars Amgevita and Yuflyma, alongside other immunology products. Ongoing PBS review and listing decisions strengthen competitive access conditions, sustain high prescription volumes, and reinforce adalimumab’s dominant biosimilar share.

Manufacturing Type Insights:

- In-house Manufacturing

- Contract Manufacturing

In-house manufacturing exhibits a clear dominance with a 62.5 share of the total Australia biosimilar market in 2025.

In-house manufacturing holds the biggest market share because of the high level of quality control and regulatory compliance required for biologic products. Biosimilars involve complex cell culture processes, strict sterility standards, and detailed comparability studies, which encourage companies to maintain direct oversight of production. Operating internal facilities allows manufacturers to safeguard intellectual property, manage supply continuity, and meet Therapeutic Goods Administration requirements efficiently. Local production capabilities also reduce dependency on overseas contract facilities and minimize supply disruptions. This direct control over critical processes supports consistent product quality and strengthens market positioning for established pharmaceutical companies.

Another factor supporting in-house manufacturing dominance is the long-term cost advantage associated with scaled operations. Large pharmaceutical firms investing in dedicated biologics plants can optimize production volumes and reduce per-unit costs over time. Internal research and development teams can closely coordinate with manufacturing units to streamline formulation adjustments and regulatory documentation. Maintaining production within controlled facilities also enables faster response to market demand and tender requirements from public hospitals. As biosimilar competition intensifies, companies prefer integrated production models that protect margins and ensure reliability. These operational efficiencies reinforce in-house manufacturing as the leading approach in Australia’s biosimilar market.

Indication Insights:

Access the comprehensive market breakdown Request Sample

- Auto-Immune Diseases

- Blood Disorder

- Diabetes

- Oncology

- Growth Deficiency

- Female Infertility

- Others

Oncology dominates with a share of 38.5% of the total Australia biosimilar market in 2025.

Oncology leads the market owing to the high prevalence of cancer and the significant cost burden associated with biologic therapies. Treatments for breast cancer, colorectal cancer, lung cancer, and hematological malignancies often rely on expensive monoclonal antibodies and supportive care biologics. Biosimilars offer comparable clinical outcomes at lower prices, making them attractive to public and private healthcare systems managing rising oncology expenditure. Australia’s PBS encourages cost-effective alternatives, accelerating uptake in hospital oncology departments. Large treatment volumes and long therapy durations further increase demand. These factors collectively position oncology as the largest indication segment within the biosimilar market.

Another reason for oncology’s dominance is the strong presence of hospital-based infusion centers where biologics are routinely administered. Oncologists are increasingly familiar with biosimilar data supported by rigorous regulatory evaluation, strengthening prescribing confidence. Competitive tendering processes within public hospitals favor lower-cost biosimilar options for widely used cancer drugs. The growing cancer screening programs also contribute to earlier diagnosis and higher treatment initiation rates. Pharmaceutical companies prioritize oncology biosimilar launches due to the substantial revenue potential tied to established reference biologics. Sustained patient inflow and institutional procurement systems ensure steady volume demand, reinforcing oncology’s leading share in Australia’s biosimilar market.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australian Capital Territory and New South Wales lead with a share of 32.5% of the total Australia biosimilar market in 2025.

Australian Capital Territory and New South Wales dominate the market due to their concentration of major hospitals, research institutions, and specialist treatment centers. Sydney and Canberra host large patient populations requiring biologic therapies across oncology, autoimmune, and chronic disease segments. Higher healthcare expenditure and advanced clinical infrastructure support faster adoption of cost-effective biosimilar alternatives. Physicians in these regions are generally early adopters of new therapeutic options supported by strong regulatory oversight. Public hospital procurement systems also encourage the use of biosimilars to manage pharmaceutical budgets efficiently. This combination of demand scale and institutional readiness drives leading regional market share.

Another factor supporting their dominance is the presence of leading pharmaceutical distributors and policy-driven reimbursement frameworks. New South Wales operates one of the largest public health networks in the country, creating substantial volume-based purchasing opportunities. Education initiatives aimed at clinicians and patients have improved confidence in biosimilar safety and efficacy. The Australian Capital Territory benefits from coordinated healthcare administration and streamlined policy implementation due to its smaller geographic size. Strong collaboration between healthcare providers and regulatory authorities further accelerates market penetration. These structural advantages ensure sustained biosimilar uptake across hospitals and specialty clinics, reinforcing regional leadership within Australia’s biosimilar market.

Market Dynamics:

Growth Drivers:

Why is the Australia Biosimilar Market Growing?

Advancements in Biomanufacturing and Supply Reliability

Advancements in biologics manufacturing technologies are strengthening the growth trajectory of the Australia biosimilar market by improving production efficiency and supply reliability. The adoption of scaled manufacturing platforms, refined upstream and downstream processing techniques, and enhanced quality assurance systems is reducing per-unit costs while maintaining stringent regulatory standards. Greater process control minimizes batch-to-batch variability, supporting consistent therapeutic performance. Reliable supply is critical in hospital and long-term treatment settings where interruptions can affect patient outcomes. Investment in resilient production networks and diversified raw material sourcing further mitigates disruption risks. Improved operational stability enhances purchaser confidence, facilitates multi-year procurement contracts, and reinforces the commercial credibility of biosimilar manufacturers.

Rising Chronic Disease Burden and Aging Population Demographics

Australia’s biosimilar market is supported by the rising prevalence of chronic and age-related diseases that require sustained biologic therapy, creating long-term demand for cost-effective treatment alternatives. Conditions such as cancer, autoimmune disorders, diabetes, and hematologic diseases are increasingly common, placing continued pressure on pharmaceutical expenditure. Demographic trends reinforce this trajectory. The Centre for Population’s 2025 Population Statement notes that the national median age is projected to reach 40 years within the next decade and increase further to 43.7 years by 2065–66, reflecting steady population ageing. An older population is more likely to require complex biologic interventions over extended durations, strengthening the economic rationale for biosimilar substitution. As treatment volumes expand, affordable alternatives are becoming central to maintaining healthcare system sustainability.

Strengthening Clinical Confidence Through Long-Term Real-World Evidence

Accumulating long-term clinical data is reinforcing physician confidence in biosimilar safety and effectiveness, supporting wider adoption across chronic disease management. Robust real-world evidence addressing persistence, immunogenicity, and treatment outcomes reduces hesitation associated with switching stable patients from originator biologics. In 2025, findings from Australia’s SAME study demonstrated that patients with inflammatory bowel disease who transitioned from originator infliximab to biosimilar CT-P13 maintained comparable treatment persistence over four years, with similar rates of disease worsening, adverse events, antibody development, and discontinuation. Such longitudinal evidence provides reassurance regarding nonmedical switching practices, strengthens institutional prescribing guidelines, and promotes broader integration of biosimilars within specialist therapeutic pathways.

Market Restraints:

What Challenges the Australia Biosimilar Market is Facing?

Clinician Hesitancy and Limited Biosimilar Prescribing Confidence

Despite growing regulatory approvals, some clinicians remain hesitant to prescribe biosimilars, particularly regarding non-medical switching of stable patients from originator biologics. Concerns about immunogenicity, indication extrapolation, and interchangeability continue to constrain broader prescribing adoption, limiting the pace at which biosimilar uptake translates into meaningful market share gains across certain therapeutic specialties.

Complex Regulatory and Reimbursement Pathways Delaying Market Access

The multi-step pathway from TGA approval through PBAC recommendation to PBS listing creates extended timelines that delay biosimilar market access and commercial launch. The sequential regulatory and reimbursement process can add substantial lead times before approved biosimilars become available to patients, reducing the competitive advantage of early approval and potentially discouraging biosimilar developers from prioritizing the Australian market.

Originator Defensive Strategies Constraining Biosimilar Market Penetration

Originator biologic manufacturers are employing sophisticated competitive strategies to defend market share, including launching authorized biosimilars, securing additional brand registrations, and offering rebate arrangements that diminish the pricing advantage of independent biosimilar competitors. These defensive measures create additional commercial barriers that can slow biosimilar uptake despite regulatory approval and PBS listing.

Competitive Landscape:

The Australia biosimilar market exhibits intensifying competitive dynamics as global biosimilar developers accelerate product registrations and PBS listing strategies to capture market share across therapeutic categories. Competition is shaped by portfolio breadth, manufacturing capabilities, distribution partnerships, and pricing strategies aligned with PBS reimbursement frameworks. Companies are increasingly differentiating through advanced formulation development, including high-concentration delivery devices and patient-friendly administration formats. Strategic partnerships between international biosimilar manufacturers and Australian distributors are strengthening market access and supply chain reliability. The competitive landscape continues to evolve as new therapeutic categories open for biosimilar competition, expanding market opportunities beyond established molecules.

Recent Developments:

- September 2025: Celltrion launched Steqeyma® (ustekinumab) and Omlyclo® (omalizumab) biosimilars in Australia, following a licensing agreement with Arrotex for local commercialization. Both products were PBS-listed on August 1, 2025, with Steqeyma® becoming the first ustekinumab biosimilar listed and Omlyclo® the only approved omalizumab biosimilar in the country. The launches expanded treatment options as additional presentations of Omlyclo® received TGA approval in August 2025.

- July 2025: Biocon Biologics launched Nepexto, its etanercept biosimilar for autoimmune diseases, in Australia through partner Generic Health. The product is a biosimilar to Amgen’s Enbrel and is indicated for conditions including rheumatoid arthritis, psoriasis, and ankylosing spondylitis. The launch strengthens Biocon Biologics’ presence in regulated markets as it plans further global expansion of the brand.

Australia Biosimilar Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Molecules Covered | Infliximab, Insulin Glargine, Epoetin Alfa, Etanercept, Filgrastim, Somatropin, Rituximab, Follitropin Alfa, Adalimumab, Pegfilgrastim, Trastuzumab, Bevacizumab, Others |

| Indications Covered | In-house Manufacturing, Contract Manufacturing |

| Manufacturing Types Covered | Auto-Immune Diseases, Blood Disorder, Diabetes, Oncology, Growth Deficiency, Female Infertility, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Biosimilar Market Report

The Australia biosimilar market size was valued at USD 906.24 Million in 2025.

The Australia biosimilar market is expected to grow at a compound annual growth rate of 21.31% from 2026-2034 to reach USD 6,687.32 Million by 2034.

Adalimumab holds the largest revenue share of 22.5% in 2025, driven by extensive PBS-listed biosimilar brands, widespread prescribing across autoimmune indications, and growing clinical acceptance of biosimilar alternatives for chronic inflammatory conditions.

Key factors driving the Australia biosimilar market include expansion of domestic biomanufacturing capacity to reduce import dependence and improve supply resilience. In 2025, Queensland unveiled ENTRI, a AU$ 100 million on-demand cGMP facility in Woolloongabba supporting local clinical-stage production and commercial readiness.

Major challenges include clinician hesitancy regarding biosimilar switching, complex multi-step regulatory and reimbursement pathways delaying market access, originator defensive competitive strategies, limited real-world adoption data, and patient perception barriers that constrain broader biosimilar uptake.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)