Australia Bus Market Size, Share, Trends and Forecast by Type, Fuel Type, Seat Capacity, Application, and Region, 2026-2034

Australia Bus Market Summary:

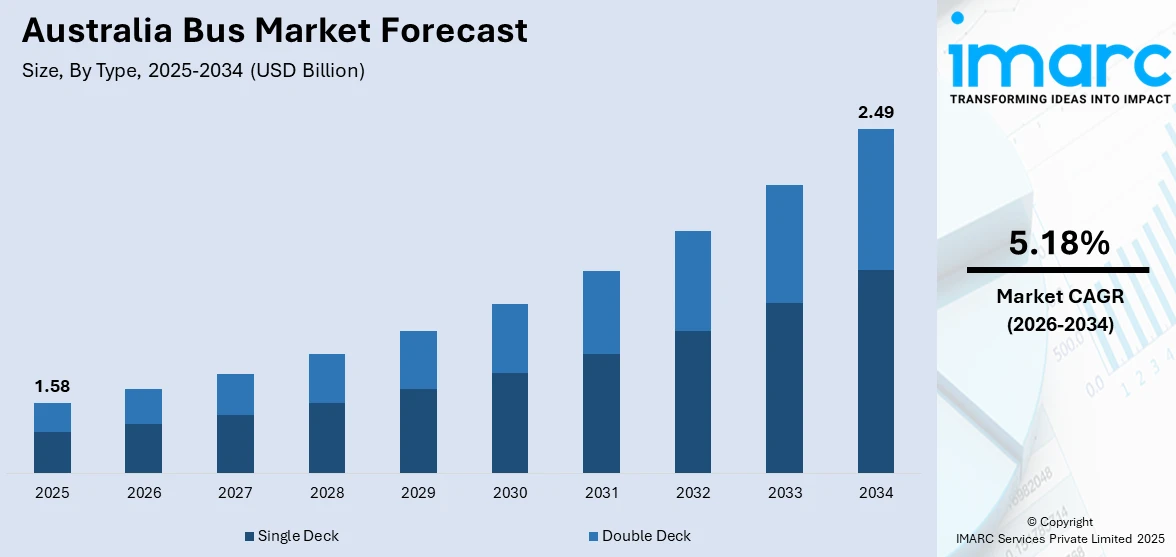

The Australia bus market size was valued at USD 1.58 Billion in 2025 and is projected to reach USD 2.49 Billion by 2034, growing at a compound annual growth rate of 5.18% from 2026-2034.

The Australia bus market is witnessing sustained growth, driven by rising public transportation demand, rapid urban population growth, and significant government investments in sustainable mobility solutions. Increasing emphasis on fleet modernization, school transport requirements, and tourism sector expansion are further propelling the market growth. The transition toward zero-emission technologies, supported by stringent emission regulations and electrification initiatives, is reshaping procurement priorities across metropolitan and regional transit networks. These converging factors are strengthening the competitive landscape and positioning Australia as a key market for next-generation bus technologies and sustainable urban mobility solutions.

Key Takeaways and Insights:

- By Type: Single deck dominates the market with a share of 74% in 2025, driven by its versatility in urban transit operations, cost-effectiveness in fleet procurement, and suitability for diverse route configurations across metropolitan and regional networks.

- By Fuel Type: Diesel leads the market with a share of 60% in 2025, reflecting the established infrastructure, operational reliability, and competitive total cost of ownership that continue to support diesel fleet operations across public and private transport sectors.

- By Seat Capacity: 31-50 seats represent the largest segment with a market share of 44% in 2025, representing the optimal balance between passenger capacity and operational flexibility for standard urban transit and intercity coach applications throughout Australia.

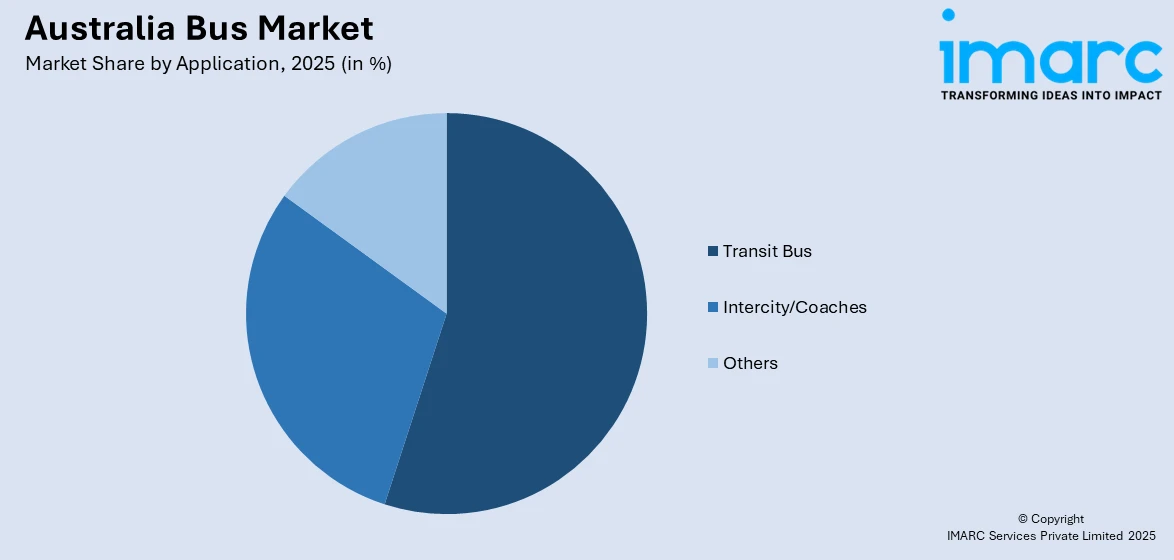

- By Application: Transit bus dominates the market with a share of 65% in 2025, underlining the critical role of scheduled public transportation services in addressing urban mobility challenges and supporting daily commuter requirements across Australian cities.

- By Region: Australia Capital Territory & New South Wales leads the market with a share of 30% in 2025, owing to high urbanization levels, strong public transport usage, early adoption of electric buses, and sustained government funding for fleet modernization and zero-emission transport initiatives

. - Key Players: The Australia bus market exhibits competitive intensity, with multinational manufacturers competing alongside domestic producers across technology segments. Companies are focusing on electrification capabilities, local manufacturing content, and strategic partnerships to strengthen market positioning.

To get more information on this market Request Sample

The Australia bus market is advancing as urban population growth, policy backed public transport investment, and fleet decarbonization priorities continue to shape demand. Governments rely on buses for congestion management, regional connectivity, and rapid service deployment, while long term funding frameworks support fleet renewal and infrastructure upgrades. Electrification, hydrogen adoption, and digital systems are influencing procurement decisions as operators focus on compliance, reliability, and operating cost control. Replacement of ageing fleets, expansion of regional and tourism focused services, and greater private sector participation under contract models further contribute to the market growth. Industry coordination and technology visibility also play a role in sustaining investment activity. In 2025, BusNSW confirmed it will host the 2026 Australasian Bus and Coach Expo at Sydney Showgrounds, scheduled for 15–16 July 2026, highlighting new vehicles, technologies, and zero emission transport solutions, reinforcing confidence, accelerating adoption, and supporting continued growth across the national bus ecosystem.

Australia Bus Market Trends:

Local Assembly Partnerships

The Australia bus market growth is supported by partnerships that combine global manufacturing scale with domestic assembly and skills development. Local completion facilities reduce delivery lead times, improve aftersales support, and align procurement with national industry objectives. In 2024, Yutong announced a partnership with Australia’s Vehicle Dealers International (VDI) to assemble electric buses in Queensland. Partially assembled buses were shipped from China and completed at VDI’s Brisbane facility, beginning with the Yutong E12 series. The arrangement included technical training and engineering services, strengthening domestic capability while supporting low emission transport goals and sustained fleet investment.

Expansion of Manufacturer Presence and Aftermarket Support

Growth in the market is reinforced by manufacturers expanding local operations alongside new product launches. Strong aftersales support, parts availability, and proximity to operators improve fleet reliability and lower lifecycle costs, encouraging procurement decisions. In 2024, BYD announced the launch of two new electric bus models for Australia, the B70 low floor midibus and the BC12B1 metropolitan city bus, tailored to local route and operator needs. The company also confirmed the expansion of its Australian footprint through a new Dandenong facility to support parts distribution and service coverage, strengthening buyer confidence and accelerating electric bus adoption.

Emergence of Hydrogen Technology and Alternative Zero Emission Pathways

The rise of zero emission technologies beyond battery electric platforms is a crucial factor impelling the market growth. Hydrogen fuel cell buses offer advantages for longer routes and high utilization services, broadening decarbonization options for operators. In 2024, Australian bus bodybuilder Volgren rolled out its first hydrogen powered bus in partnership with Northern Ireland’s Wrightbus, integrating Wrightbus’s hydrogen fuel cell chassis into a locally built vehicle. This milestone expanded Volgren’s zero emission portfolio and demonstrated technical readiness for hydrogen adoption, encouraging public authorities to consider diversified clean energy fleets and supporting continued investment in next generation buses.

Market Outlook 2026-2034:

The Australia bus market demonstrates robust revenue growth potential throughout the forecast period, underpinned by sustained government investment in public transportation infrastructure and irreversible trends of fleet electrification. The market generated a revenue of USD 1.58 Billion in 2025 and is projected to reach a revenue of USD 2.49 Billion by 2034, growing at a compound annual growth rate of 5.18% from 2026-2034. This growth trajectory reflects increasing procurement of zero-emission vehicles, modernization of aging diesel fleets, and expansion of transit services to accommodate urban population growth across major metropolitan regions.

Australia Bus Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Single Deck |

74% |

|

Fuel Type |

Diesel |

60% |

|

Seat Capacity |

31-50 Seats |

44% |

|

Application |

Transit Bus |

65% |

|

Region |

Australia Capital Territory & New South Wales |

30% |

Type Insights:

- Single Deck

- Double Deck

Single deck dominates with a market share of 74% of the total Australia bus market in 2025.

Single deck holds the biggest market share due to its operational flexibility and suitability across diverse route structures. Its design supports efficient movement in urban, suburban, and regional networks without requiring specialized infrastructure. Capacity levels are well aligned with typical passenger volumes, enabling balanced load management and service frequency. Lower acquisition and maintenance requirements support cost control for operators. Maneuverability and ease of deployment further enhance route coverage. These functional advantages make single deck a practical and scalable solution across a wide range of public and private transport operations nationwide.

Another reason for this dominance lies in operational efficiency and long-term fleet management considerations. Single deck offers simplified maintenance processes, standardized parts usage, and reduced downtime compared to larger configurations. Driver training and operational integration are more straightforward, supporting workforce flexibility. Fuel efficiency and compatibility with alternative powertrains strengthen their viability under evolving transport policies. Fleet renewal cycles also favor models with proven performance and adaptability. These combined economic and operational benefits reinforce the sustained preference for single deck buses within the market across varied service environments.

Fuel Type Insights:

- Diesel

- Electric and Hybrid

- Others

Diesel leads with a market share of 60% of the total Australia bus market in 2025.

Diesel represents the largest segment because of its established reliability, widespread availability, and compatibility with existing fleet operations. The fuel supports consistent performance across varied operating conditions and duty cycles, ensuring dependable service continuity. Refueling infrastructure is extensive and integrated into transport networks, reducing operational disruption. Diesel engines offer predictable torque delivery suited to frequent stop-start operations. Cost certainty in maintenance practices and mature service ecosystems further support sustained usage. These factors collectively maintain diesel’s strong position within the bus fuel landscape.

Another driver of diesel dominance is its alignment with long-term fleet planning and asset utilization strategies. Operators benefit from standardized maintenance regimes, readily available technical expertise, and proven engine durability. Lifecycle costs remain competitive due to economies of scale in parts and servicing. Operational familiarity reduces transition risks and training requirements. Fleet replacement timelines also favor continuity where infrastructure and performance benchmarks are well understood. These operational and economic considerations continue to reinforce diesel as the preferred fuel type within the market.

Seat Capacity Insights:

- 15-30 Seats

- 31-50 Seats

- More than 50 Seats

31-50 seats exhibit a clear dominance with a 44% share of the total Australia bus market in 2025.

31–50 seats dominate the market owing to their balanced alignment between passenger volume and operational efficiency. This capacity range supports effective service delivery across routes with moderate demand while maintaining optimal occupancy levels. Vehicle size within this segment allows flexibility in scheduling and route deployment without compromising comfort or accessibility. Cost efficiency in acquisition, fuel usage, and maintenance further strengthens adoption. These buses provide sufficient capacity for peak periods while avoiding underutilization, reinforcing their preference across diverse transport operations nationwide.

Another contributing factor is the suitability of the 31–50 seat segment for fleet standardization and long-term planning. Operators benefit from consistent vehicle specifications that simplify procurement and maintenance processes. This capacity class supports regulatory compliance, safety standards, and accessibility requirements without complex design modifications. In addition, maneuverability remains manageable across varied road networks, enhancing operational reliability. The segment also aligns well with staffing efficiency and service frequency planning.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Transit Bus

- Intercity/Coaches

- Others

Transit bus dominates with a market share of 65% of the total Australia bus market in 2025.

Transit bus leads the market, as it plays a central role in scheduled passenger transport and network-based mobility systems. This vehicle is designed for high-frequency operations, efficient boarding, and consistent route coverage. Its configuration supports accessibility requirements, passenger flow management, and operational reliability. Integration with urban and regional transport planning strengthens demand, as transit services form the backbone of public mobility. High utilization rates and continuous service requirements drive sustained fleet deployment, reinforcing the prominence of transit bus across the national bus market.

Another factor supporting this dominance is the alignment of transit bus with policy objectives focused on mass transport efficiency and service continuity. Operators prioritize applications that enable predictable demand patterns and stable revenue structures. Transit bus is optimized for durability and frequent operation, reducing lifecycle disruptions. Moreover, standardized specifications simplify fleet management and procurement. Compatibility with evolving emissions standards and powertrain transitions further enhances long-term relevance. In 2025, Adelaide introduced the first two of 60 new battery-electric transit buses as part of its public transport electrification program. Supplied by Scania with Volgren bodies, the buses operated on regular Adelaide Metro routes, replacing ageing diesel vehicles.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory and New South Wales lead with a market share of 30% of the total Australia bus market in 2025.

Australia Capital Territory and New South Wales dominate the market, driven by their high concentration of transport networks and sustained investment in public mobility systems. Strong population density and extensive commuter movement create consistent demand for bus services. Regional planning frameworks emphasize integrated transport solutions, supporting large-scale fleet deployment. Funding stability and long-term infrastructure programs further strengthen market size. The presence of mature procurement systems and centralized transport authorities enables efficient fleet expansion and renewal, reinforcing regional dominance within the national bus market.

Another contributing factor is the advanced operational environment supporting high service frequency and network coverage. Structured route planning, coordinated scheduling, and strong governance frameworks enhance efficiency and utilization levels. Regulatory alignment and policy continuity further reduce operational uncertainty. For instance, in 2025, the NSW Government announced the purchase of 151 new battery electric buses as part of its push toward a zero-emission public transport fleet. This move supported the long-term plan to transition over 8,000 diesel and gas buses across NSW to zero-emission vehicles while improving air quality and passenger comfort.

Market Dynamics:

Growth Drivers:

Why is the Australia Bus Market Growing?

Service Innovation to Support Tourism and Urban Accessibility

Expansion of targeted bus services designed around local travel needs is contributing to the market growth in Australia. Transport authorities increasingly use buses to manage congestion in high demand recreational and tourist areas while improving public access. In 2025, the WA state government launched a free Surf CAT bus service linking Scarborough Beach with Stirling Train Station. The service was introduced to reduce parking pressure, improve beach accessibility, and support tourism. Modified buses with dedicated surfboard storage highlight how service customization can drive additional fleet requirements and reinforce the role of buses in supporting local economic activity.

Product Diversification and Customizable Electric Platforms

The expansion of electric bus offerings beyond traditional urban transit applications is propelling the market growth. Manufacturers are addressing varied operational needs across school, charter, and specialist segments through adaptable vehicle platforms. In 2025, Volvo Bus Australia unveiled its BZR Electric coach platform, extending zero emissions technology into longer range and non-urban services. The platform allowed operators to customize battery capacity, interior layout, and body configuration while integrating advanced safety systems. This flexibility lowers adoption barriers for diverse operators, encourages fleet electrification across multiple use cases, and drives broader demand for next generation buses in the Australian market.

Government Policy and Public Transport Investment

Public transport policy in Australia continues to position buses as central to integrated mobility systems, supported by sustained federal and state funding for service expansion, fleet renewal, and operational efficiency. Buses align closely with policy goals linked to congestion management, inclusion, and regional access, while offering faster deployment and lower capital requirements than fixed infrastructure. This policy commitment is reinforced through tangible infrastructure investment. For example, in 2025, the ACT Government opened Australia’s largest electric bus depot at Woden, capable of housing up to 100 electric buses with advanced charging and future solar integration. Such initiatives strengthen regulatory certainty, encourage operator investment, and underpin long term growth across the national bus market.

Market Restraints:

What Challenges the Australia Bus Market is Facing?

High Capital Costs for Electric Bus Procurement

Battery-electric buses involve significantly higher upfront costs than conventional diesel models, creating procurement hurdles for fleet operators planning large-scale transitions. Even though long-term operating savings arise from lower fuel usage and reduced maintenance needs, the initial capital outlay places pressure on budgets. This financial strain is more pronounced for smaller operators, often resulting in phased purchases or delayed electrification plans.

Charging Infrastructure Development Requirements

The shift toward electric bus fleets demands substantial capital investment in charging infrastructure and depot modernization, going well beyond the cost of vehicle procurement. Fleet operators must undertake depot upgrades that include grid reinforcement, transformer installation, energy management systems, and large-scale charger deployment. These infrastructure projects often require lengthy planning, regulatory approvals, and construction timelines, which can delay implementation and create temporary gaps in fleet replacement and service continuity.

Skilled Workforce Shortages in Bus Operations

The bus industry continues to face structural challenges in attracting and retaining qualified drivers and skilled maintenance technicians, placing pressure on daily operations. Persistent driver shortages reduce route coverage, disrupt schedules, and limit service frequency, especially during peak demand periods. Additionally, the shift toward electric buses requires specialized technical knowledge, forcing fleet operators to invest in retraining programs, safety protocols, and higher workforce development costs.

Competitive Landscape:

The Australia bus market shows strong competitive intensity, with multinational manufacturers and domestic producers competing across varied technology segments, operating models, and price bands. European OEMs position themselves at the premium end, focusing on advanced safety systems, superior build quality, and low-emission technologies, while Asian manufacturers compete on cost efficiency, faster delivery timelines, and scalable production. Local players add value through customization and after-sales support. Competitive differentiation is increasingly driven by electrification capabilities, battery technology partnerships, total cost of ownership, and access to reliable charging infrastructure as public and private operators accelerate zero-emission fleet procurement.

Recent Developments:

- January 2026: Autobus Australia announced the upcoming launch of TRUBUS, Australia’s first integrated, purpose-built off-road 4×4 bus designed specifically for mining conditions. Built on a Scania 4×4 chassis with capacity for more than 40 seated passengers and features suited to rough mine-site terrain.

- July 2025: FlixBus announced plans to launch long-distance coach services along Australia’s East Coast. The initial network aimed to connect major cities, including Sydney, Melbourne, and Brisbane, using Flix’s tech-driven partnership model with local operators. The move marked Flix’s formal entry into the Australian intercity coach market, focusing on digital booking, connectivity, and scalable route expansion.

Australia Bus Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Single Deck, Double Deck |

| Fuel Types Covered | Diesel, Electric and Hybrid, Others |

| Seat Capacities Covered | 15-30 Seats, 31-50 Seats, More than 50 Seats |

| Applications Covered | Transit Bus, Intercity/Coaches, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Bus Market Report

The Australia bus market size was valued at USD 1.58 Billion in 2025.

The Australia bus market is expected to grow at a compound annual growth rate of 5.18% from 2026-2034 to reach USD 2.49 Billion by 2034.

Single deck dominates the market with 74% share in 2025, driven by their operational versatility, cost-effectiveness, and suitability for diverse urban transit and regional transportation applications across Australia.

Key factors driving the Australia bus market include partnerships linking global manufacturing with local assembly and workforce development. In 2024, Yutong partnered with Vehicle Dealers International to complete electric buses in Brisbane, improving delivery timelines, aftersales support, technical capability, and alignment with Australia’s low emission public transport objectives.

Major challenges include high capital costs for electric bus procurement, charging infrastructure development requirements, skilled workforce shortages affecting driver availability, long lead times for depot conversions, and the complexity of coordinating fleet electrification with service continuity requirements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade