Australia Buy Now Pay Later Market Size, Share, Trends and Forecast by Channel, Enterprise Size, End Use, and Region, 2026-2034

Australia Buy Now Pay Later Market Size and Share:

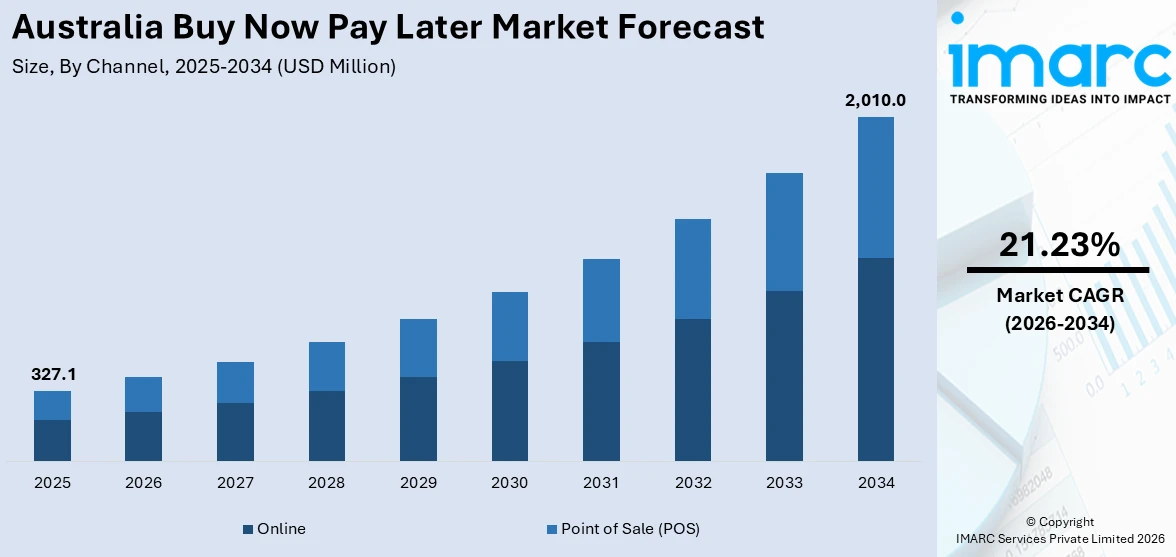

The Australia buy now pay later market size reached USD 327.1 Million in 2025. Looking forward, the market is expected to reach USD 2,010.0 Million by 2034, exhibiting a growth rate (CAGR) of 21.23% during 2026-2034. The high smartphone penetration, widespread e-commerce adoption, growing millennial and Gen Z consumer base, increasing demand for flexible payment solutions, growing retailer partnerships, strong digital infrastructure, and rising financial awareness are driving the growth of the market in Australia.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 327.1 Million |

| Market Forecast in 2034 | USD 2,010.0 Million |

| Market Growth Rate 2026-2034 | 21.23% |

Key Trends of Australia Buy Now Pay Later Market:

Increased Smartphone Penetration Driving Mobile BNPL Usage

Australia’s high smartphone penetration is a critical factor propelling the Australia buy now pay later market growth. With over 90% of Australians owning a smartphone, consumers are increasingly managing their finances, purchases, and digital wallets through mobile applications. Buy now pay later (BNPL) providers are capitalizing on this trend by designing mobile-first platforms that offer instant credit approvals, seamless integration with shopping apps, and real-time transaction tracking. The convenience of accessing BNPL services directly through smartphones is especially attractive to digitally native demographics, particularly Millennials and Gen Z users. Apart from this, mobile apps also support the development of value-added services such as push notifications for repayments, spending limits, and personalized offers based on usage behavior. These features contribute to better user engagement and repeat transactions. Also, BNPL firms are integrating their services with mobile payment ecosystems like Apple Pay and Google Pay to ensure a frictionless checkout experience. This mobile-centric growth is pushing retailers to optimize their online storefronts for compatibility with BNPL solutions embedded within smartphone environments.

To get more information on this market Request Sample

Growth in E-Commerce Transactions Accelerating BNPL Adoption

The rapid expansion of e-commerce sector in Australia is a significant factor augmenting Australia buy now pay later market share. Online retail sales have been increasing in recent years, fueled by changing consumer behavior, convenience, and the shift to digital channels. According to an industry report, e-commerce market in Australia is expected to reach USD 1,568.60 Billion by 2033, exhibiting a CAGR of 12.70% from 2025-2033. This robust digital retail expansion is directly contributing to the growing BNPL adoption, as more consumers turn to flexible payment options during online purchases. BNPL services are now firmly embedded in the online checkout process, frequently appearing alongside credit card and PayPal options, which makes them a familiar and accessible choice for shoppers. In addition to this, retailers across categories are integrating BNPL platforms to offer flexible financing options at the point of sale. The integration is mutually beneficial: merchants experience increased sales volumes and reduced cart abandonment, while BNPL firms gain access to a broader consumer base. Seasonal sales, online-only deals, and promotional campaigns also push consumers toward short-term financing tools, reinforcing BNPL’s role in the online shopping journey. As e-commerce grows, BNPL adoption continues to scale alongside it, which is enhancing Australia buy now pay later market outlook.

Growth Factors of Australia Buy Now Pay Later Market:

High Digital Adoption and Consumer Comfort with Fintech Platforms

The highly developed digital infrastructure of Australia and consumer receptiveness to new technology have strongly contributed to the expansion of the Buy Now Pay Later (BNPL) market. Australians are among the region's earliest adopters of fintech products, having a high level of smartphone penetration and comfort with online payments. This has made it an ideal place for BNPL suppliers to flourish. Platforms that provide interest-free instalment facilities have resonated strongly with younger Australians who prefer flexible expenditure to conventional credit frameworks. With an increasing number of shoppers seeking easy, on-the-spot purchasing channels, BNPL has become a part of both online and point-of-sale transactions. This behavior change, along with the tech-first Australian consumer lifestyle, continues to enable fast adoption and growth in an increasing number of retail categories.

Transition Away from Historical Credit and Banking Preferences

One of the key drivers contributing to the Australia buy now pay later market demand is the waning popularity of traditional credit products, particularly among Gen Z and millennials. Credit cards are seen with suspicion by many younger consumers, mainly due to their interest charges, intricate fee schedules, and opacity. BNPL products, on the other hand, have clear-cut repayment schedules and zero-interest timeframes, which are more comfortable and better understood. Australia's banking industry, though solid, has suffered criticism in recent years on questions of trust and customer service, prompting consumers to seek out alternative forms of payment. Increasing financial independence among young consumers and the need to stay away from long-term debt add further weight to BNPL. This cultural and age-based transformation of attitudes towards personal finance is particularly robust in Australia, where debt-conscious consumers actively are reconfiguring the way payment and credit solutions are utilized. Consequently, BNPL platforms exist as more consumer-friendly options that resonate with today's financial values.

Retail Integration and Support from Domestic Brands

Australian retailers have been instrumental in growing the BNPL market by quickly adopting the services into both online and physical sales channels. Top local brands in fashion, household goods, electronics, and even supermarkets now make BNPL an everyday payment choice. Such ubiquitous availability has helped make BNPL a simple and familiar aspect of the shopping experience for many Australians. In addition, Australian consumers are employing BNPL to increase the average order value and drive impulse buying by reducing the upfront cost for them. Australian BNPL providers, like those that started from Australia, have adapted their platforms for use in the domestic market by emphasizing simplicity, quick approvals, and easy integration into e-commerce platforms. Seasonal sale days such as Boxing Day or Click Frenzy also experience surges in BNPL usage, solidifying its place within the local retail landscape. The co-operative steam between retailers and BNPL providers remains to fuel deepened market penetration.

Opportunities of Australia Buy Now Pay Later Market:

Expansion into Underserved Categories and Daily Expenditures

According to the Australia buy now pay later market analysis, one of the most compelling opportunities in the region is its expansion from the mainstream retail segments. Fashion, electronics, and lifestyle products have been among the first to adopt BNPL services, and there is interest in embedding BNPL in daily expenditure categories like groceries, utilities, healthcare, and education. Australian shoppers have become more willing to employ instalment payment choices on ordinary purchases, particularly amid economic uncertainty. The trend permits BNPL players to expand customer bases as well as usage frequency. In regional Australia, where access to alternative payment facilities might be limited, pushing BNPL services into supermarkets and local service providers provides an avenue for financial inclusion. This under-leveraged segment has the potential to generate significant volume growth and long-term loyalty if services are customized to meet different spending behaviors and income levels prevalent in different Australian communities.

Capitalizing on Small and Medium Enterprise (SME) Partnerships

Australia's thriving small business environment presents another major opportunity for BNPL growth. While big retailers have embraced BNPL services in broad numbers, there is still a huge opportunity to grow within the SME space. Independent stores, local services firms, and regional enterprises are seeking increasingly how to compete with chains, and integration of BNPL can provide them with a competitive advantage. Through facilitating installment payments, the companies can capture budget-constrained and younger consumers who value flexibility in their finances. For BNPL providers, making cheap and easy-to-implement solutions available for SMEs increases their merchant base and extends their footprint in local economies. Furthermore, collaboration with Australian origin fintech accelerators and locally born platforms can assist BNPL providers in customizing products for small businesses with considerations around compliance, user-friendliness, and local support. With SMEs serving as key drivers of employment in Australia's economy and regional economic growth, their uptake of BNPL is a significant potential to firm up market share by way of inclusive, bottom-up development strategies.

Integration with Super Apps and Financial Wellness Tools

Another significant opportunity for the Australia BNPL market is integrating it with larger digital ecosystems, such as super apps and financial health platforms. As more consumers are aware of their financial health, they increasingly look for more than just tools that allow them to spend but also allow them to budget, monitor expenses, and save better. Australian BNPL providers can take advantage of this trend by integrating their service within apps that provide multi-purpose assistance—such as mobile banking, investment monitoring, and customized financial advice. Australia's fintech industry is extremely innovative, and partnerships between digital finance tools and BNPL platforms can increase user interaction while adding to the image of BNPL as a responsible form of credit. Furthermore, developing reward systems, loyalty rewards, or learning capabilities within BNPL apps can assist with overspending issues as well as enable regular use. This opens differentiation opportunities in a crowded market, providing more utility to technologically inclined Australian consumers who expect convenience, transparency, and control over their financial experience.

Challenges of Australia Buy Now Pay Later Market:

Regulatory Scrutiny and the Pressure for Consumer Protection

The biggest threat to the Buy Now Pay Later (BNPL) industry in Australia is the increasing level of regulatory oversight. Australian financial authorities and consumer groups have increasingly raised concerns about the risk of consumer over-indebtedness from BNPL products, especially among young users who do not have the benefit of conventional credit experience. In contrast to credit cards and personal loans, BNPL services have, to a significant extent, existed outside mainstream credit, escaping more stringent responsible lending requirements. Yet, with growing demands for bringing BNPL under the same regulation, particularly in the wake of public scrutiny and reports calling for enhanced consumer protections, something is sure to give. For providers, this shift in regulation may translate into higher costs of compliance, stricter approval processes, and restrictions on marketing BNPL products. While regulation will improve long-term trust, it will also limit the flexibility that has facilitated fast growth for BNPL platforms. Innovation balanced with prudent lending standards will be key to the sector's further development in Australia.

Increasing Competition and Market Saturation

The BNPL market in Australia, previously dominated by a handful of local pioneers, is increasingly experiencing strong competition both from local players and foreign players. Large fintech brands, international e-commerce sites, and even legacy banks began to introduce BNPL offerings, resulting in a crowded market. The increase in providers has resulted in market fragmentation, competition on price, and rising customer acquisition expenses. Smaller or younger players find it difficult to be distinct, particularly when larger platforms can pay less or collaborate with well-known merchants. In addition, the consumer market is getting increasingly discerning, frequently opting for BNPL products in-built in their go-to shopping apps or with integrated rewards. As the market matures, growth can slow, and it can become increasingly challenging for new participants to take hold or for smaller players to remain profitable. For Australia, where fintech innovation is strong but market size is proportionally small, saturation may result in consolidation, with only the most resilient and diversified suppliers holding a competitive advantage.

Consumer Behavior Changes and Economic Volatility

A second Australian BNPL market challenge is remaining responsive to changing consumer behavior influenced by economic uncertainty and inflationary stress. Although BNPL expanded aggressively in times of consumer optimism and retail growth, unstable economic conditions could have a major impact on consumer spend. As the cost-of-living increases in Australia, particularly within metropolitan areas such as Sydney and Melbourne, discretionary spend can fall, affecting most active sectors in which BNPL operates namely fashion, travel, and lifestyle goods. They might become more prudent with their money, reducing their dependence on instalment-based credit or switching to more conventional forms of credit that provide more extensive use. And public opinion regarding BNPL can change based on coverage in the media and anecdotal experience—especially if tales of financial distress due to excessive usage are reported. Providers need to respond to these issues by improving transparency, providing budgeting tools, and encouraging responsible use to build trust. Understanding and predicting changes in consumer opinion is most important for long-term viability in the Australian financial sector.

Australia Buy Now Pay Later Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on channel, enterprise size, and end use.

Channel Insights:

- Online

- Point of Sale (POS)

The report has provided a detailed breakup and analysis of the market based on the channel. This includes online and point of sale (POS).

Enterprise Size Insights:

- Large Enterprises

- Small and Medium Enterprises

A detailed breakup and analysis of the market based on the enterprise size have also been provided in the report. This includes large enterprises and small and medium enterprises.

End Use Insights:

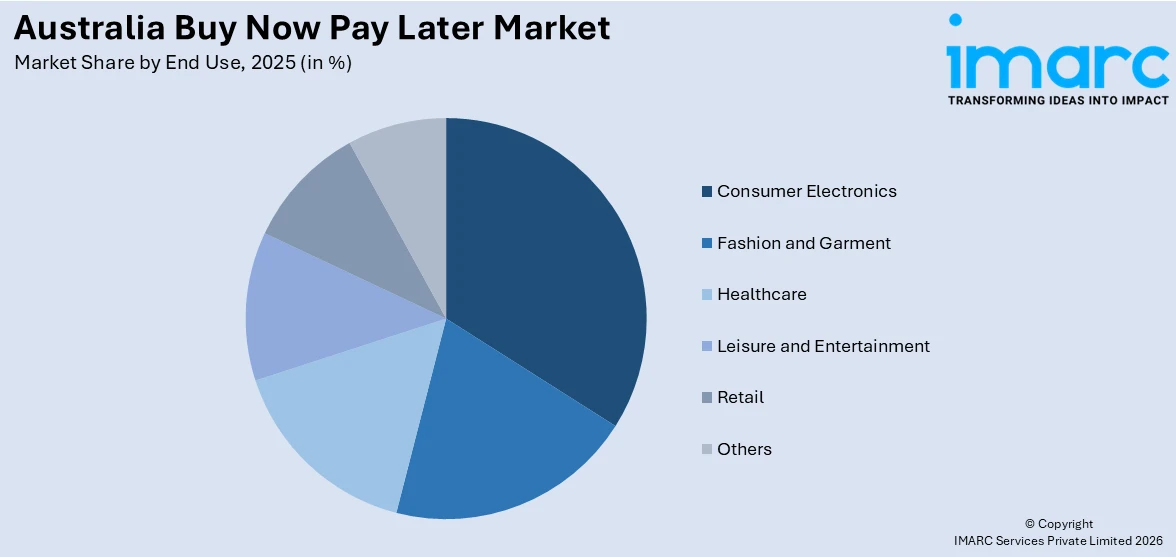

Access the comprehensive market breakdown Request Sample

- Consumer Electronics

- Fashion and Garment

- Healthcare

- Leisure and Entertainment

- Retail

- Others

The report has provided a detailed breakup and analysis of the market based on the end use. This includes consumer electronics, fashion and garment, healthcare, leisure and entertainment, retail, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided, including:

- Afterpay Australia Pty Ltd

- Commonwealth Bank of Australia

- humm BNPL Pty Ltd

- Klarna Australia Pty Ltd

- National Australia Bank Limited

- Quest Payment Systems Pty. Ltd.

- Sezzle

- Zip Co Limited

Australia Buy Now Pay Later Market News:

- The Australian Securities and Investments Commission (ASIC) announced that effective June 10, 2025, Buy Now Pay Later (BNPL) providers must hold an Australian credit license under new legislation extending the National Credit Code to BNPL contracts. Providers are required to apply for a license, have their application accepted by ASIC, and become members of the Australian Financial Complaints Authority by the specified deadline.

- On May 8, 2025, Regulatory Guide 281 (RG 281), published by the Australian Securities and Investments Commission (ASIC), provided comprehensive guidelines for providers of low-cost credit (LCC) agreements, which include most Buy Now Pay Later (BNPL) services. Beginning on June 10, 2025, these providers will be subject to the changes made to the National Consumer Credit Protection Act 2009 (Cth) (National Credit Act) by the Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Act 2024 (Cth). The new system applies to all LCC agreements signed before, on, or after June 10, 2025.

- On February 7, 2025, ASIC announced a consultation on its proposed guidance for low-cost credit contract (LCCC) providers, which includes most Buy Now Pay Later (BNPL) products. An exposure draft of the related National Consumer Credit Protection Amendment (Low Cost Credit) Regulations 2025 ("Draft BNPL Regulations") was made available for consultation by ASIC on February 5, 2025.

Australia Buy Now Pay Later Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Channels Covered | Online, Point of Sale (POS) |

| Enterprise Sizes Covered | Large Enterprises, Small and Medium Enterprises |

| End Uses Covered | Consumer Electronics, Fashion and Garment, Healthcare, Leisure and Entertainment, Retail, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Afterpay Australia Pty Ltd, Commonwealth Bank of Australia, humm BNPL Pty Ltd, Klarna Australia Pty Ltd, National Australia Bank Limited, Quest Payment Systems Pty. Ltd., Sezzle, Zip Co Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia buy now pay later market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia buy now pay later market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia buy now pay later industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Buy Now Pay Later Market Report

The Australia buy now pay later market was valued at USD 327.1 Million in 2025.

The Australia buy now pay later market is projected to exhibit a CAGR of 21.23% during 2026-2034.

The Australia buy now pay later market is expected to reach a value of USD 2,010.0 Million by 2034.

The primary key trend of the Australia buy now pay later market is the transformation of BNPL sector with greater embedding in e-commerce, mobile wallets, and in-store point-of-sale systems. Growth in subscription-based BNPL, as well as tailored credit limits, is a testament to a movement toward financial flexibility. Greater emphasis on responsible lending and regulatory adherence is also facilitating innovation.

Australia's BNPL sector is boosted by digital adoption that is extremely high, consumers' preference for payment flexibility, and reduced use of conventional credit cards. Robust e-commerce growth and backing from the country's big retailers also contribute significantly to demand. Younger generations and digitally savvy consumers continue to adopt BNPL due to convenience, control over budget, and interest-free installment advantages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)