Australia Carbon Credit Market Size, Share, Trends and Forecast by Type, Project Type, End-Use, and Region 2026-2034

Australia Carbon Credit Market Size & Forecast 2026-2034

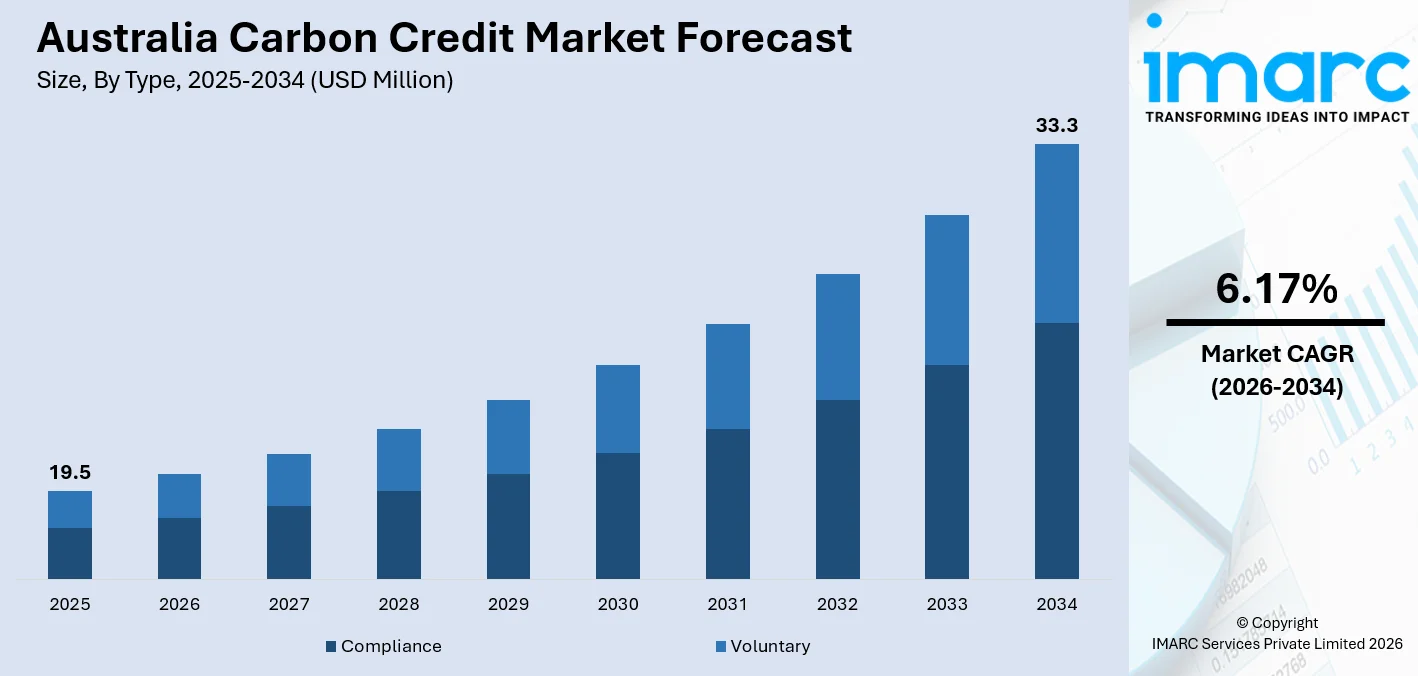

Australia carbon credit market size reached USD 19.5 Million in 2025 and is projected to reach USD 33.3 Million by 2034, growing at a CAGR of 6.17% from 2026-2034. The market is growing owing to the reformed Safeguard Mechanism, which now mandates annual emissions baseline reductions across large industrial facilities in Australia's highest-emitting sectors. In 2025, total ACCU issuances reached a record 21.64 million units, a 15% year-on-year increase from 18.78 million in 2024, reflecting the structural compliance demand surge and proliferating land-based supply projects underpinning Australia's carbon credit market share.

To get more information on this market Request Sample

Australia Carbon Credit Industry Analysis - Key Insights

- Compliance commands 62.3% of the market by type in 2025 the Safeguard Mechanism's mandatory declining baselines for large emitters have structurally embedded compliance as the dominant demand channel, with voluntary purchase accounting for the balance of the market.

- Removal/sequestration projects lead project type at 48.6% in 2025 HIR and soil carbon projects in NSW, Queensland, and WA rangelands dominate supply, reflecting Australia's vast land resources and the diversity of approved ACCU methodologies for the land sector.

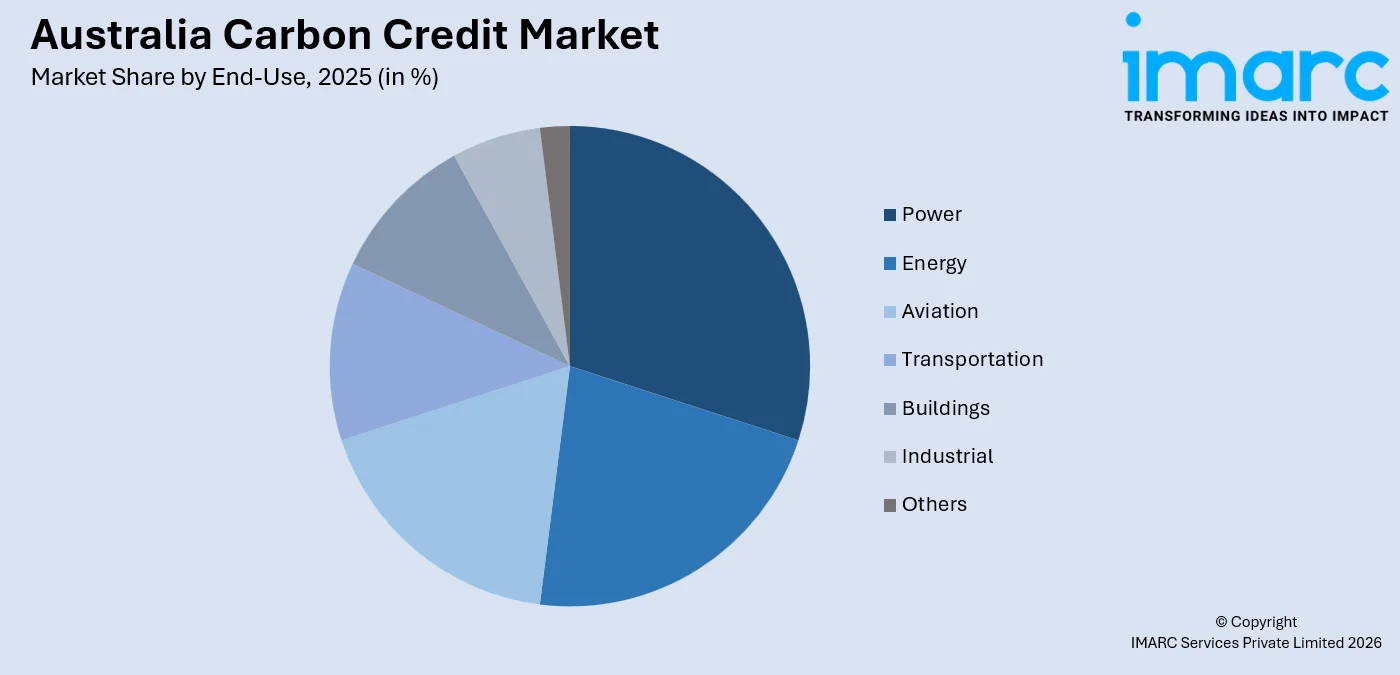

- Power dominates end-use at 28.4% in 2025 grid-connected generation facilities face direct compliance obligations under the Safeguard Mechanism's electricity sectoral baseline, and the sector's accelerating coal exit is simultaneously reshaping its net ACCU demand profile.

- Australia Capital Territory & New South Wales leads regionally at 34.2% in 2025 Sydney's concentration of ACCU market infrastructure, legal advisory services, and the proximity of northwest NSW rangelands to major HIR project corridors anchors this region as the market's commercial and supply hub.

Australia Carbon Credit Market Trends and Dynamic 2026

Market Trends

Digital Registry Infrastructure and Market Transparency

In December 2023, the Clean Energy Regulator signed a contract with Trovio Group to develop the new Unit and Certificate Register. Australia carbon credit market is being transformed by investments in digital measurement, reporting, and verification infrastructure that strengthen ACCU integrity and traceability. Registry upgrades were deployed in three stages between May and July 2025, adding crediting period dates, permanence period start dates, and voluntary project proponent disclosures.

Institutional Capital Entering the Carbon Farming Sector

The Clean Energy Finance Corporation and La Caisse jointly launched the AUD 250 million Meldora agricultural and carbon platform in September 2025. This platform acquired a 15,000-hectare property in Central Queensland for environmental plantings under the ACCU scheme. There is a large-scale institutional investment drive that is redefining the carbon farming sector in Australia. Sovereign wealth funds, superannuation funds, and corporate investors are entering long-term ACCU offtake agreements.

Nature-Based Supply Expansion Across the Land Sector

GreenCollar established an AUD 100 million (~USD 64.9 million) fund to create Environmental Plantings (EP) Australian Carbon Credit Unit (ACCU) projects. The projects will be designed to support the financing and registration of nature-based carbon sequestration projects in early 2026. Regeneration projects like human-induced regeneration, soil carbon sequestration, and savanna fire management are expanding.

- Corporate Offtake Structures: Long-term supply agreements between key industrial players and ACCU project developers are locking in multi-year credit pipelines, mitigating price risk, and driving new project registrations.

- Indigenous Land Participation: The vast rangelands of Aboriginal people are producing ACCUs via endorsed savanna fire management, providing both environmental and cultural co-benefits while also providing an economic outcome.

- New ACCU Method Development: DCCEEW is actively consulting on new landfill gas and savanna fire management methods, with integrated farm and land management and proponent-led methods also in development to diversify the supply base.

- ESG Reporting Pressure: Mandatory climate risk disclosure requirements are compelling listed companies to formalize their ACCU procurement strategies and report verified carbon offset positions to shareholders.

Growth Drivers

Reformed Safeguard Mechanism Creating Structural Compliance Demand

The reformed Safeguard Mechanism applies mandatory 4.9% annual baseline decline rates to Australia's 215 largest emitters by 2030, creating a structural and growing floor of ACCU demand. In FY2024, the first full compliance year, 142 facilities incurred a combined liability of 9.2 Mt CO₂-e above their assigned baselines, collectively surrendering 7.1 million ACCUs and 1.4 million Safeguard Mechanism Credits to the Clean Energy Regulator.

Corporate Net-Zero Commitments and ESG Reporting Pressure

Australia's major corporations are embedding ACCU procurement into long-term climate strategies, spurred by investor scrutiny, ESG reporting mandates, and the introduction of mandatory climate risk disclosures for listed companies. In August 2024, Qantas, Rio Tinto, and BHP each committed as foundation investors to the Silva Carbon Origination Fund, collectively providing AUD 80 million toward a fund targeting AUD 250 million to originate high-integrity nature-based ACCUs.

- International Trade Alignment: Australia's ACCUs are internationally recognized, enabling export-oriented sectors such as mining and agriculture to leverage credits for carbon border adjustment mechanism readiness in key trading partner markets.

- Financial Sector Participation: Banks, superannuation funds, and specialist carbon funds are structuring ACCU-backed financial products and offtake arrangements, increasing secondary market liquidity and improving long-term price discovery.

- Land Use Diversification Income: Landholders across rangelands, agricultural zones, and coastal areas are integrating carbon farming projects with existing production systems, creating complementary revenue streams that incentivize long-term participation.

Market Restraints

Integrity and additionality concerns in land-based methods: Challenges about human-induced regeneration methods generating permanent carbon sequestration continue to create scientific debate and regulatory scrutiny. Inconsistencies between credited abatement and measurable vegetation outcomes weaken market confidence, constrain voluntary buyer willingness to pay premium prices, and expose the broader ACCU scheme to reputational risks.

Price volatility and supply-demand imbalances: The ACCU market faces structural uncertainty arising from policy cycles, regulatory changes, and uneven project development timelines. These dynamics create significant price fluctuations that complicate long-term project finance planning for new market entrants, particularly smaller landholders and independent project developers.

Regulatory complexity and access barriers for smaller participants: Navigating the technical and administrative requirements for ACCU project registration and CER reporting creates high barriers to entry for smaller landholders in remote areas. The complexity of approved method selection disproportionately disadvantages independent developers relative to large aggregators.

Australia Carbon Credit Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Compliance | 62.3% | 2025 |

| Project Type | Removal/Sequestration Projects | 48.6% | 2025 |

| End-Use | Power | 28.4% | 2025 |

| Region | Australia Capital Territory & New South Wales | 34.2% | 2025 |

Type Insights

Compliance - 62.3% market share (2025) | Leading Type

Compliance-grade ACCUs are driven by the Safeguard Mechanism's mandatory framework covering large emitters across the oil and gas, mining, manufacturing, and heavy industrial sectors, which must keep covered emissions below declining annual baselines or surrender ACCUs. The Clean Energy Regulator's cost containment mechanism is indexed annually to the consumer price index plus 2%, with the 2025–26 price set at USD 82.68 per ACCU. It is providing a regulated compliance floor that underpins structural demand growth through 2030 and beyond.

|

Segment Breakdown Compliance (62.3%) · Voluntary |

Project Type Insights

Removal/Sequestration Projects - 48.6% market share (2025) | Leading Project Type

Removal/sequestration projects include the removal or sequestration of CO₂ from the atmosphere by nature-based solutions like reforestation/afforestation and soil carbon sequestration. This also includes human-induced regeneration (HIR), which involves the regeneration of degraded lands by natural means, and savanna fire management, which helps reduce emissions from early-season fires in Northern Australia.

|

Segment Breakdown Removal/Sequestration Projects (48.6) - Nature-based & Technology-based · Avoidance/Reduction Projects |

End-Use Insights

Access the comprehensive market breakdown Request Sample

Power - 28.4% market share (2025) | Leading End-Use

The power sector's leading position in ACCU end-use reflects both the sector's historically significant emissions and its pivotal role in Australia's clean energy transition. In Q1 2025, renewable energy in the National Electricity Market averaged a record 43% of total generation, signaling accelerating coal displacement and a structural shift in the sector's net ACCU demand dynamics as coal retires and renewables scale.

|

Segment Breakdown Power (28.4%) · Energy · Aviation · Transportation · Buildings · Industrial · Others |

Regional Insights

Australia Capital Territory & New South Wales - 34.2% market share (2025) | Leading Region

Australia Capital Territory & New South Wales anchored Australia carbon credit market through Sydney's concentration of ACCU market infrastructure, legal and financial advisory services, and the headquarters of major project developers and corporate buyers. The northwest NSW rangelands host the highest density of human-induced regeneration projects in the country, exemplifying the commercial viability of agricultural carbon integration.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

34.2%

|

|

Key States

|

New South Wales, Australian Capital Territory |

|

Major Growth Drivers

|

HIR project density, corporate and financial headquarters, soil carbon innovation, Sydney carbon trading hub |

|

Outlook

|

Sustained regional leadership in compliance and voluntary markets |

|

Regional Breakdown Australia Capital Territory & New South Wales (34.2%) · Victoria & Tasmania · Queensland · Northern Territory & Southern Australia · Western Australia |

Victoria & Tasmania:

Victoria and Tasmania represent a high-value market anchored by significant Safeguard Mechanism compliance obligations from industrial emitters in the aluminum smelting, steel, chemicals, and cement sectors, concentrated in the Melbourne-Geelong corridor and the Latrobe Valley. Melbourne's status as Australia's second-largest corporate hub generates substantive voluntary ACCU procurement from companies meeting ESG disclosure requirements.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Victoria, Tasmania |

|

Major Growth Drivers

|

Industrial compliance demand, Melbourne corporate headquarters, Tasmanian forest sequestration opportunities, superannuation fund investment |

|

Outlook

|

Steady compliance-driven demand growth |

Queensland:

Queensland's carbon credit market is among the most diverse in Australia, combining savanna fire management ACCUs from the state's tropical north, soil carbon and HIR projects in the western rangelands, and industrial compliance demand from its large minerals, liquefied natural gas, and resources sector. The state has committed to reducing emissions by 75% below 2005 levels by 2035, providing a clear policy mandate for accelerated land-based carbon project development.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Queensland |

|

Major Growth Drivers

|

Savanna fire management supply, agri-carbon integration, resource sector compliance, 75% state emissions reduction target by 2035 |

|

Outlook

|

High-growth land sector supply region |

Northern Territory & Southern Australia:

The Northern Territory is Australia's most significant source of savanna fire management ACCUs, with Indigenous communities and station owners operating fire management projects across vast tropical rangelands using endorsed early dry-season burning methodologies. Savanna fire management methods accounted for 1.59 million ACCUs nationally in 2025, representing 7.3% of total annual issuances, with the Northern Territory contributing the dominant share of these credits.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Northern Territory, South Australia |

|

Major Growth Drivers

|

Indigenous savanna fire management, NT rangeland scale, SA environmental plantings pipeline, government land sector program support |

|

Outlook

|

Growing Indigenous-led ACCU project pipeline |

Western Australia:

Western Australia is home to some of Australia's largest industrial emitters under the Safeguard Mechanism, including major liquefied natural gas export facilities and iron ore operations that generate substantial ACCU compliance demand. The state also produces a significant land-based ACCU supply from its extensive rangelands. This combination of high demand and supply positions Western Australia as a key player in Australia’s carbon market, offering opportunities for both emission reductions and ACCU generation.

|

Metric

|

Details

|

|---|---|

|

Major Growth Drivers

|

LNG sector compliance demand, rangeland-scale nature-based projects, energy efficiency technology ACCU generation, resource sector decarbonization investment |

|

Outlook

|

Major dual supply-and-demand state anchoring national ACCU volumes |

Market Outlook 2026-2034

What is the future outlook of Australia carbon credit market?

Australia carbon credit market is expected to sustain steady revenue growth through 2034

Australia's carbon credit market is positioned for sustained expansion through 2034, underpinned by the Safeguard Mechanism's progressively tightening baselines and the broadening of institutional capital into land-based carbon projects. Digital MRV improvements, the maturation of methodology frameworks for soil carbon and savanna fire management, and the anticipated launch of the Australian Carbon Exchange will collectively expand supply quality and market liquidity.

Australia Carbon Credit Market - Leading Key Players

Australia's carbon credit market features a competitive landscape of specialized environmental market developers, land management companies, energy sector participants, and financial intermediaries that collectively shape ACCU supply, pricing, and market integrity. Leading players differentiate through proprietary project methodologies, large-scale land portfolios, institutional capital partnerships, and established compliance relationships with major Safeguard-covered industrial emitters across Australia's highest-emitting sectors.

| Company | Leading Brands | Highlights |

|---|---|---|

| GreenCollar Group (TerraCarbon) | Nature-based ACCUs, Reef Credits, NaturePlus | Australia's largest land-based ACCU developer; 46.3 million ACCUs delivered by January 2026; launched AUD 100 million EP ACCU reforestation fund in November 2025 |

| AgriProve Pty Ltd | Soil carbon ACCUs (Agriprove methodology) | Pioneer in scientifically validated soil carbon sequestration; operates projects across Queensland, NSW, and South Australia; developer of proprietary measurement technology for soil carbon quantification |

| LMS Energy Pty Ltd | Landfill gas ACCUs | Australia's largest landfill gas ACCU operator; led national ACCU issuances in multiple months of 2025; sustained producer of waste-method credits across metropolitan landfill sites |

Some existing key players in the market are Greenfleet Australia, Xpansiv, Corporate Carbon Group of Companies, Clean Earth Capital, South Pole (Australia), Carbon Neutral, Climate Impact Partners, APA Group, and Santos Limited, etc.

Latest Development & News

- In November 2025, Santos achieved a record carbon credit allocation at its Moomba carbon capture and storage project, receiving 614,133 Australian Carbon Credit Units from the Clean Energy Regulator for verified emissions reductions achieved between September 2024 and March 2025. The allocation underscores the scaling role of technology-based carbon removal projects in Australia's compliance-grade ACCU supply and validates the commercial case for industrial CCS under the ACCU Scheme.

- In November 2025, GreenCollar launched a new AUD 100 million (~USD 64.9 million) Environmental Plantings ACCU fund targeting institutional investors, with the fund's close targeted for Q1 2026. Investors are entitled to distributions of ACCUs generated by the fund's reforestation portfolio in either carbon units or cash proceeds.

- In September 2025, Cibus Capital launched Cibus Carbon, a new Australian carbon credit fund targeting AUD 200–300 million (~USD 132 million) in commitments to develop planted carbon projects. This is aimed at generating approximately 11.25 million Australian Carbon Credit Units (ACCUs) over a 30‑year horizon. The fund will focus on mixed‑species tree plantings on selected sites, positioning Cibus to capitalize on rising compliance.

Australia Carbon Credit Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Compliance, Voluntary |

| Project Types Covered |

|

| End-Uses Covered | Power, Energy, Aviation, Transportation, Buildings, Industrial, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia carbon credit market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia carbon credit market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia carbon credit industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Carbon Credit Market Report

Australia carbon credit market reached USD 19.5 Million in 2025.

The Australia carbon credit market is anticipated to reach a value of USD 33.3 Million by 2034.

Compliance dominates the market with a share of 62.3% in 2025, driven by the Safeguard Mechanism's mandatory declining baselines for large industrial emitters that must purchase and surrender ACCUs to meet their annual compliance obligations.

Removal/sequestration projects - nature-based commands the market with a share of 48.6% in 2025, driven by Australia's vast rangelands, forests, and agricultural areas that are well-suited to HIR, soil carbon, and environmental plantings projects.

Power leads the market with a share of 28.4% in 2025, as grid-connected electricity generators face compliance obligations under the Safeguard Mechanism's sectoral baseline, while the sector's accelerating transition from coal to renewables reshapes its net ACCU demand profile.

New South Wales & Australia Capital Territory currently lead the market, accounting for a share of 34.2% in 2025. The region benefits from Sydney's concentration of ACCU market infrastructure, legal and financial advisory services, and the high density of HIR and soil carbon projects in northwest NSW rangelands that collectively underpin its dual supply and demand leadership.

Some of the major players in Australia carbon credit market include GreenCollar Group, AgriProve Pty Ltd, LMS Energy Pty Ltd, Greenfleet Australia, Xpansiv, Corporate Carbon Group of Companies, Clean Earth Capital, South Pole (Australia), Carbon Neutral, Climate Impact Partners, APA Group, and Santos Limited, etc.

Key trends shaping the market include the proliferation of digital MRV and blockchain-based registry platforms improving ACCU traceability, growing involvement of Indigenous communities in savanna fire management projects, and rising demand for premium environmental co-benefit credits from corporate ESG buyers.

Key growth factors include the Safeguard Mechanism's mandatory 4.9% annual baseline decline rate, creating compounding compliance demand, Australia's legislated 2030 and 2050 emissions targets anchoring long-term policy certainty, and the vast natural land resources suitable for sequestration projects.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)