Australia Cold Chain Market Size, Share, Trends and Forecast by Type, Temperature Range, Application, and Region, 2026-2034

Australia Cold Chain Market Overview:

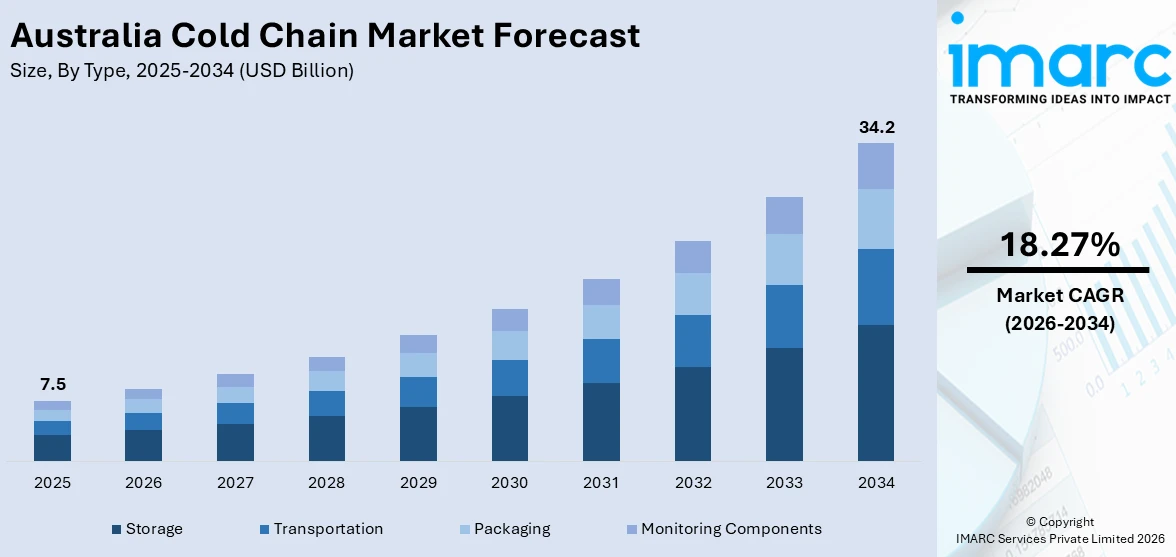

The Australia cold chain market size reached USD 7.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 34.2 Billion by 2034, exhibiting a growth rate (CAGR) of 18.27% during 2026-2034. Rising demand for fresh and frozen food, expanding pharmaceutical logistics, stricter food safety regulations, increased e-commerce grocery sales, improved cold storage infrastructure, and advancements in temperature-controlled transport and tracking technologies across the supply chain are some of the factors propelling the Australia cold chain market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 7.5 Billion |

| Market Forecast in 2034 | USD 34.2 Billion |

| Market Growth Rate 2026-2034 | 18.27% |

Australia Cold Chain Market Trends:

Rising Investment and Expansion in Temperature-Controlled Logistics

Australia is witnessing rising interest in temperature-controlled logistics, influenced by global momentum in refrigerated transport and storage services. The sector is being reshaped by increasing consumer reliance on perishable food delivery, pharmaceutical distribution, and export-grade fresh produce. With international markets expanding rapidly and projections showing a threefold increase in valuation, domestic logistics players are investing in advanced infrastructure, including energy-efficient cold storage units, GPS-enabled reefer trucks, and real-time temperature monitoring systems. This shift is not just geared toward keeping pace with international demand but also aligning with stringent quality and safety regulations. Additionally, partnerships between logistics operators and retail chains are intensifying to streamline last-mile cold deliveries, especially in urban and remote regions. The overall outlook suggests significant upgrades in capabilities and coverage, supported by rising cross-border trade, evolving consumer preferences, and policy-driven improvements in food and health supply chain reliability.

To get more information on this market Request Sample

Sustainable Packaging Gains Ground in Cold Chain Sector

The Australia cold chain market demand is increasingly moving toward sustainable packaging solutions to reduce environmental impact. Traditional materials like expanded polystyrene are being replaced with recyclable and compostable alternatives such as fiberboard and wool insulation. These solutions are capable of maintaining critical temperature ranges, particularly for pharmaceuticals during high-heat summer conditions. The shift reflects a broader industry effort to align logistics practices with eco-conscious goals, minimize non-recyclable waste, and enhance operational sustainability. Emphasis is now on solutions that balance temperature control, performance reliability, and environmental responsibility across short-distance and time-sensitive shipment needs. For example, in September 2024, Merck introduced eco-friendly insulation for cold-chain shipments in Australia, replacing expanded polystyrene with fiberboard and wool-based materials from Planet Protector Packaging. The switch eliminates 3.6 tons of non-recyclable waste annually. Designed to maintain 2°C to 8°C for one-day pharma shipments in Australian summer conditions, the new packaging supports Merck’s SMASH Packaging strategy aimed at improving sustainability across its supply chain.

Growth Drivers of Australia Cold Chain Market:

Surging Demand for Pharmaceutical and Biologic Cold Chain Services

The pharmaceutical sector's expansion, particularly in vaccine manufacturing, biotechnology products, and temperature-sensitive medications, is a primary driver of the Australia cold chain market growth. The establishment of advanced pharmaceutical manufacturing facilities, including mRNA vaccine production sites, has intensified the need for ultra-cold storage capabilities and GDP-compliant transport solutions. Regulatory requirements mandate strict temperature control throughout the supply chain to preserve drug efficacy and patient safety. Australia's role as a regional pharmaceutical hub for the Asia-Pacific region further amplifies cold chain demand, with increasing exports of vaccines, blood products, and biologics requiring specialized refrigerated logistics. Healthcare providers are investing in dedicated cold chain infrastructure to support clinical trials, personalized medicine, and emergency medical supply distribution. The growing complexity of pharmaceutical products, including cell and gene therapies requiring storage at -80°C or lower, is pushing cold chain operators to upgrade their facilities with cutting-edge refrigeration technologies and continuous monitoring systems to meet evolving industry standards.

Robust Growth in E-Commerce Grocery Sales and Online Food Delivery

The dramatic rise in online grocery shopping and food delivery services across Australia is fundamentally reshaping cold chain logistics requirements. Major supermarket chains and online grocery platforms are establishing sophisticated distribution networks with temperature-controlled fulfilment centers to handle growing order volumes. Consumer preferences for fresh produce, chilled meals, frozen foods, and premium seafood delivered to their doorsteps are driving investments in refrigerated last-mile delivery fleets and insulated packaging solutions. The convenience factor, coupled with expanded product selections and improved delivery reliability, is encouraging more Australians to shift from traditional in-store shopping to online platforms. This transition requires cold chain providers to develop flexible, scalable operations capable of managing variable order sizes, multiple temperature zones, and tight delivery windows. Meal kit services and subscription-based fresh food boxes are further contributing to demand, necessitating innovative cold chain solutions that maintain product quality across diverse geographic locations, from metropolitan areas to regional communities, throughout the delivery journey.

Strengthening Food Safety Regulations and Quality Standards

Increasingly stringent food safety regulations imposed by government authorities are compelling businesses across the food supply chain to invest in robust cold chain infrastructure and compliance systems. Food Standards Australia New Zealand (FSANZ) has implemented comprehensive guidelines governing the temperature control of perishable foods during production, storage, transportation, and retail display. These regulations require detailed record-keeping, temperature monitoring, and traceability measures to prevent foodborne illnesses and ensure consumer protection. Businesses face significant penalties for non-compliance, including product recalls, legal liabilities, and reputational damage, creating strong incentives to adopt best-practice cold chain solutions. The Australian Food and Grocery Council's cold chain guidelines emphasize end-to-end temperature management across multi-party supply chains. Retailers, wholesalers, and foodservice operators are implementing advanced monitoring technologies and staff training programs to meet regulatory requirements. Export-oriented producers must also comply with international quality certifications and destination country regulations, necessitating investment in certified cold storage facilities, refrigerated transport equipment, and comprehensive quality assurance systems that support Australia's reputation for premium food products in global markets.

Opportunities of Australia Cold Chain Market:

Expanding Agricultural Export Markets Requiring Specialized Cold Chain Solutions

Australia's reputation as a leading exporter of premium agricultural products, including beef, lamb, seafood, dairy, fruits, and wine, presents significant opportunities for cold chain service providers. Growing demand from Asian markets, particularly China, Japan, South Korea, and Southeast Asian nations, is driving the need for sophisticated temperature-controlled logistics connecting Australian farms and processing facilities to international ports and airports. Free trade agreements are opening new export corridors, enabling Australian producers to access lucrative markets for high-value perishables. However, capitalizing on these opportunities requires investment in specialized cold chain infrastructure capable of maintaining product quality across long-distance international shipments. This includes pre-cooling facilities near production sites, refrigerated container fleets, cold storage at port facilities, and coordination with international logistics partners. The growing middle class in Asian countries is driving demand for premium imported foods, creating sustained growth potential for Australian exporters. Cold chain providers that can offer integrated export logistics solutions—combining storage, transport, customs clearance, and quality certification—are well-positioned to capture market share in this expanding segment.

Integration of Renewable Energy and Green Technologies in Cold Chain Operations

As per the Australia cold chain market analysis, the cold chain industry's high energy consumption creates substantial opportunities for companies to differentiate themselves through sustainable practices and green technology adoption. Installing solar panels on warehouse roofs, implementing energy-efficient refrigeration systems, and utilizing natural refrigerants with lower global warming potential can significantly reduce operational costs and environmental impact. Government incentives and corporate sustainability commitments are driving investment in electric refrigerated vehicles, hydrogen fuel cell trucks, and alternative fuel technologies for Austrlaia cold chain transport market. Carbon reporting requirements and customer preferences for environmentally responsible suppliers are creating competitive advantages for early adopters of green logistics solutions. Cold storage facilities incorporating advanced insulation materials, LED lighting, high-speed doors, and heat recovery systems can achieve substantial energy savings while maintaining temperature integrity. Smart building management systems optimize refrigeration loads based on storage patterns and external conditions. Cold chain operators that successfully balance sustainability goals with operational performance can attract environmentally conscious customers, reduce long-term operating costs, and position themselves favorably as regulations around emissions and energy efficiency continue to tighten across Australia's logistics sector.

Development of Regional Cold Chain Networks Supporting Remote Communities

Australia's vast geography and dispersed population create unique opportunities for cold chain operators to develop specialized regional logistics networks serving remote and rural communities. These areas face significant challenges in accessing fresh, high-quality perishable foods due to distance from major distribution centers and limited local cold storage infrastructure. Establishing strategically located regional cold storage hubs, supported by refrigerated transport links to both capital cities and remote townships, can improve food security and product availability in underserved markets. Government initiatives supporting regional development and infrastructure investment may provide funding opportunities for cold chain expansion into these areas. Regional cold chains also support local agricultural producers by providing access to broader markets and enabling value-added processing closer to farm gates. Indigenous communities, mining operations, tourism destinations, and healthcare facilities in remote locations all require reliable cold chain services for food supplies, medical provisions, and vaccines. Cold chain providers developing expertise in regional logistics, including coordination of multi-modal transport (road, rail, air, and sea), flexible service models, and partnerships with local businesses, can build sustainable competitive advantages in this specialized market segment.

Australia Cold Chain Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on type, temperature range, and application.

Type Insights:

- Storage

- Facilities/Services

- Refrigerated Warehouse

- Cold Room

- Equipment

- Blast Freezer

- Walk-in Cooler and Freezer

- Deep Freezer

- Others

- Facilities/Services

- Transportation

- By Mode

- Road

- Sea

- Rail

- Air

- By Offering

- Refrigerated Vehicles

- Refrigerated Containers

- By Mode

- Packaging

- Crates

- Insulated Containers and Boxes

- Large (32 to 66 liters)

- Medium (21 to 29 liters)

- Small (10 to 17 liters)

- X-small (3 to 8 liters)

- Petite (0.9 to 2.7 liters)

- Cold Chain Bags/Vaccine Bags

- Ice Packs

- Others

- Monitoring Components

- Hardware

- Sensors

- RFID Devices

- Telematics

- Networking Devices

- Others

- Software

- On-premises

- Cloud-based

- Hardware

The report has provided a detailed breakup and analysis of the market based on the type. This includes storage [facilities/services (refrigerated warehouse and cold room), equipment (blast freezer, walk-in cooler and freezer, deep freezer, and others)], transportation [by mode (road, sea, rail, and air), by offering (refrigerated vehicles and refrigerated containers)], packaging [crates, insulate containers and boxes (large (32 to 66 liters), medium (21 to 29 liters), small (10 to 17 liters), x-small (3 to 8 liters), petite (0.9 to 2.7 liters), cold chain bags/vaccine bags, ice packs, and others], and monitoring components [hardware (sensors, RFID devices, telematics, networking devices, and others) and software (on-premises and cloud-based)].

Temperature Range Insights:

- Chilled (0°C to 15°C)

- Frozen (-18°C to -25°C)

- Deep-frozen (Below -25°C)

A detailed breakup and analysis of the market based on the temperature range have also been provided in the report. This includes chilled (0°C to 15°C), frozen (-18°C to -25°C), and deep-frozen (below -25°C).

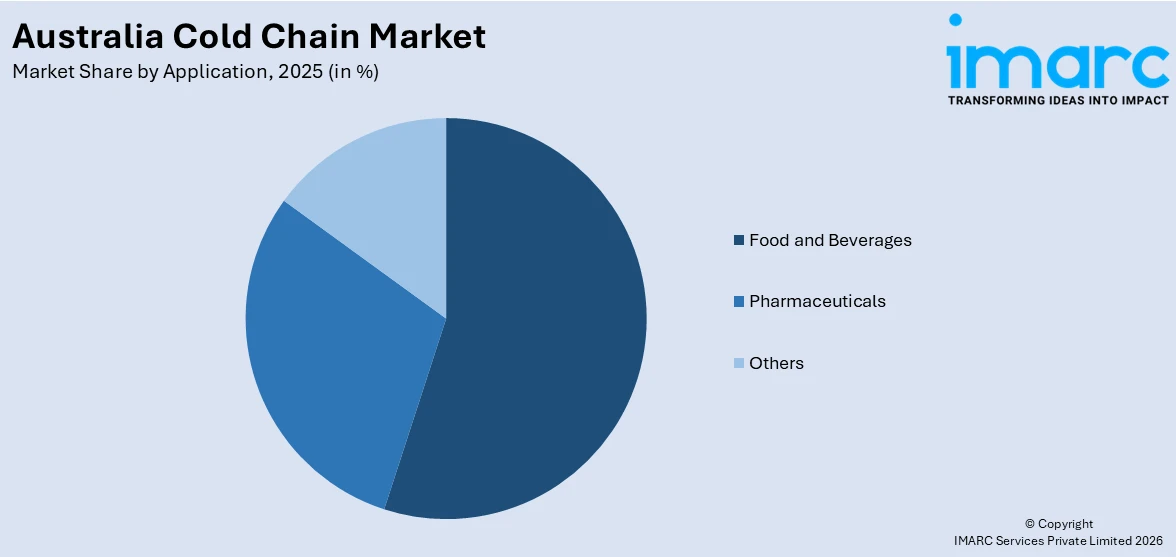

Application Insights:

Access the comprehensive market breakdown Request Sample

- Food and Beverages

- Fruits and Vegetables

- Fruit Pulp and Concentrates

- Dairy Products

- Milk

- Butter

- Cheese

- Ice Cream

- Others

- Fish, Meat, and Seafood

- Processed Food

- Bakery and Confectionary

- Others

- Pharmaceuticals

- Vaccines

- Blood Banking

- Others

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes food and beverages [fruits and vegetables, fruit pulp and concentrates, dairy products (milk, butter, cheese, ice cream, and others), fish, meat, and seafood, processed food, bakery and confectionary, and others], pharmaceuticals (vaccines, blood banking, and others), and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Cold Chain Market News:

- In April 2025, Cold Chain Technologies launched the CCT Tower Elite, a reusable 1600L pallet shipper featuring multi-temperature control and IoT-enabled tracking. This innovation enhanced the secure transport of temperature-sensitive goods in Australia, improving delivery reliability and supporting the growth of advanced cold chain logistics.

- In April 2025, China Eastern Air Logistics introduced a new portfolio in Adelaide focused on boosting exports of temperature-sensitive goods like rock lobster, salmon, and cherries. As part of this, an MoU was signed between its cold chain division and Ferguson Australia to strengthen end-to-end cold chain services. The initiative aims to support South Australia’s premium seafood and produce exports with reliable, temperature-controlled logistics connecting to international markets.

Australia Cold Chain Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

|

Temperature Ranges Covered |

|

| Applications Covered |

|

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia cold chain market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia cold chain market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia cold chain industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Cold Chain Market Report

The Australia cold chain market was valued at USD 7.5 Billion in 2025.

The Australia cold chain market is projected to exhibit a CAGR of 18.27% during 2026-2034.

The Australia cold chain market is projected to reach a value of USD 34.2 Billion by 2034.

The key market trends include accelerated adoption of IoT-enabled monitoring technologies providing real-time visibility across temperature-controlled supply chains. Expansion of automated, high-capacity cold storage infrastructure with advanced racking systems and multi-temperature zones is also transforming warehousing capabilities.

The Australia cold chain market drivers include surging pharmaceutical and biologic cold chain requirements from expanding vaccine manufacturing and biotechnology sectors. Rising consumer expectations for product freshness and quality are further compelling retailers and foodservice operators to invest in advanced refrigerated cold chain solutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)