Australia Electric Vehicle Market Size, Share, Trends and Forecast by Vehicle Type, Price Category, Propulsion Type, and Region, 2026-2034

Australia Electric Vehicle Market Size, Share, Trends & Forecast (2026-2034)

The Australia electric vehicle market reached USD 21.06 Billion in 2025 and is projected to reach USD 221.02 Billion by 2034, growing at a CAGR of 28.80% during 2026-2034. Rising adoption of electric vehicles by businesses to meet sustainability objectives, growing mass production improving affordability, rapid expansion of charging infrastructure, and the implementation of the New Vehicle Efficiency Standard are the key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 21.06 Billion |

|

Forecast Market Size (2034) |

USD 221.02 Billion |

|

CAGR (2026-2034) |

28.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Segment (Vehicle Type) |

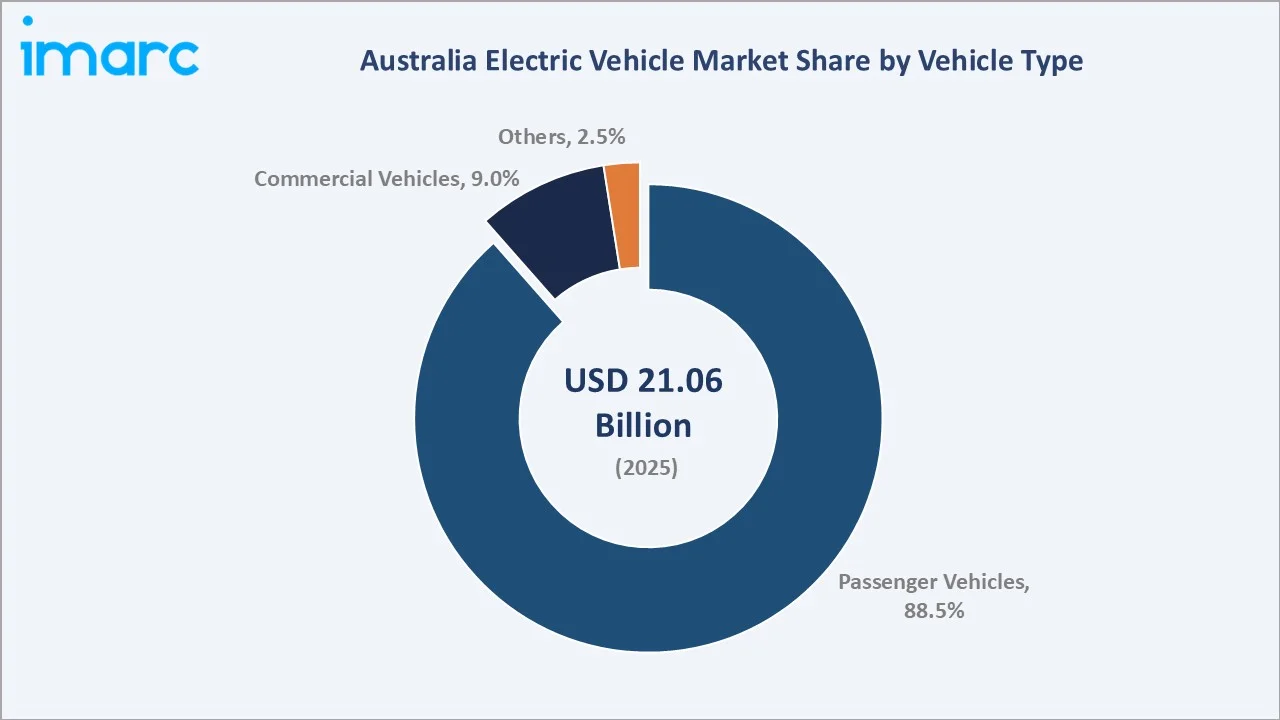

Passenger Vehicles (88.5% share, 2025) |

|

Largest Segment (Price Category) |

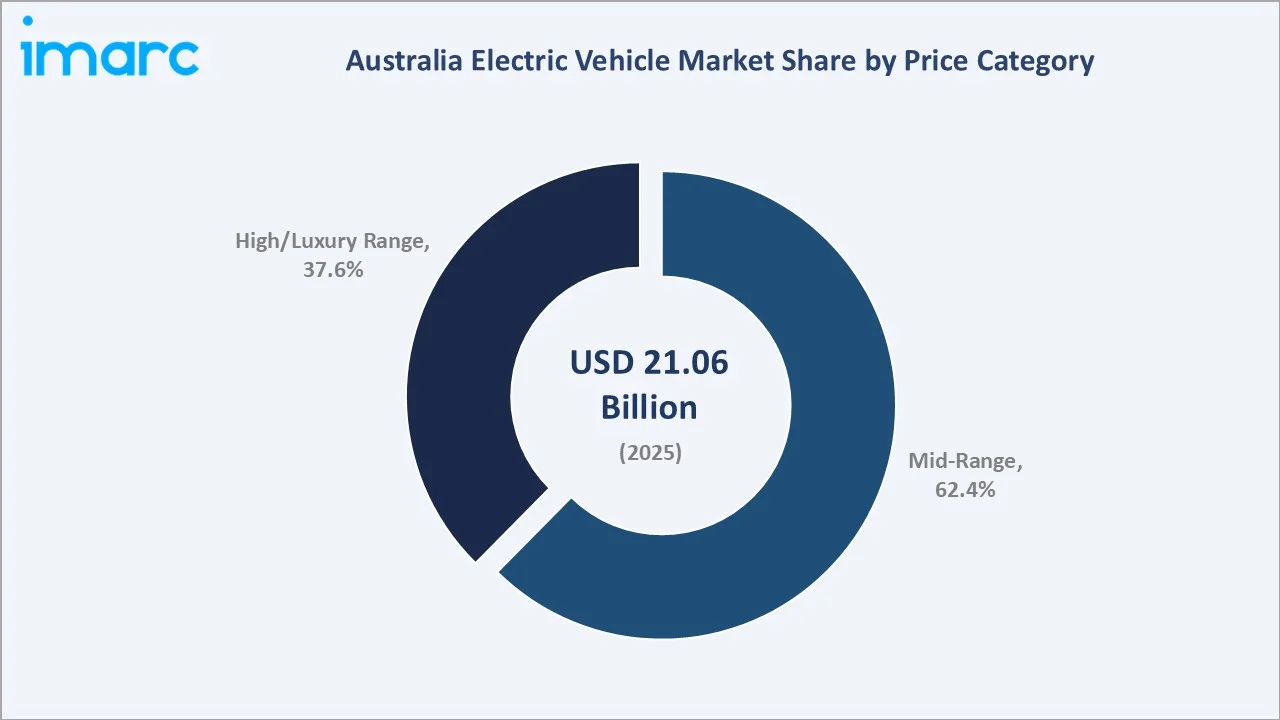

Mid-Range (62.4% share, 2025) |

|

Leading Region |

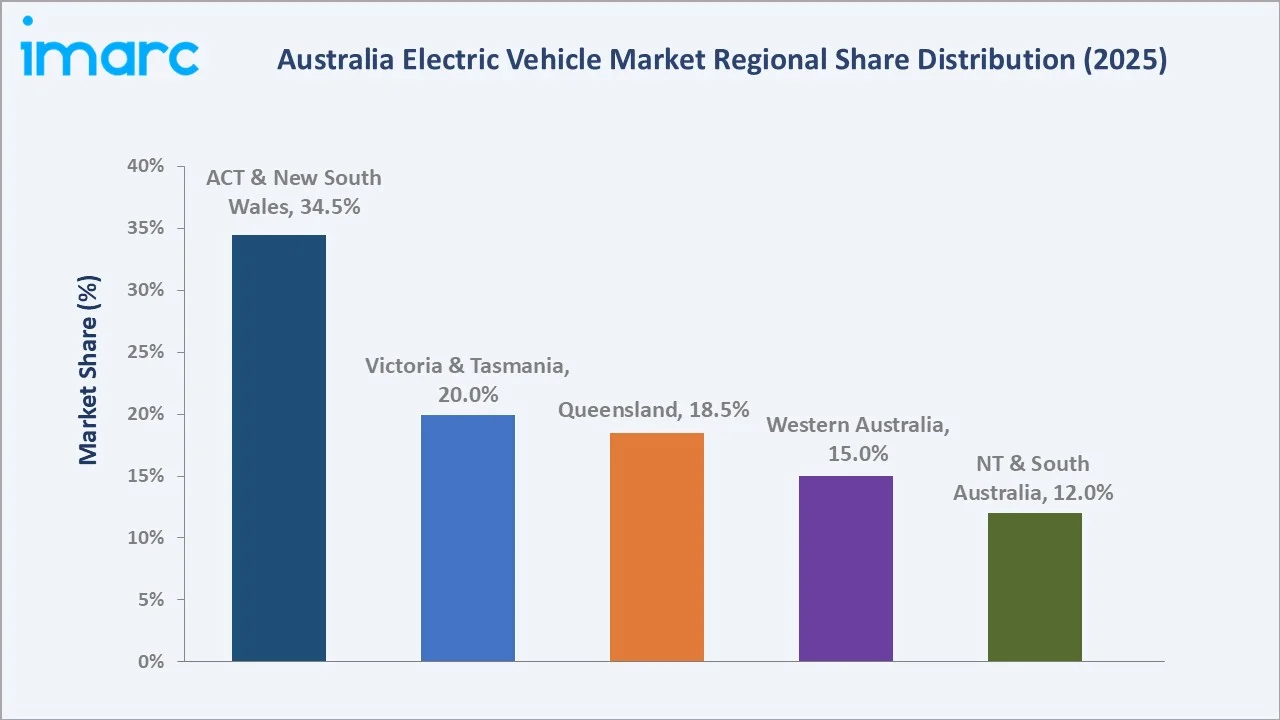

Australia Capital Territory & New South Wales (34.5% share, 2025) |

|

Fastest Growing Region |

Queensland |

Passenger vehicles dominate the market with an 88.5% share in 2025, driven by strong consumer demand for electric SUVs and hatchbacks. Mid-Range vehicles lead price categories at 62.4%, supported by government incentives and affordability improvements. Australia now has over 454,000 electric vehicles in its national fleet, with 153 EV models available to buyers, including 94 battery electric vehicles and 59 plug-in hybrids, reflecting the market's rapid transition toward sustainable transportation.

To get more information on this market, Request Sample

With vehicle segments spanning battery electric vehicles, hybrid electric vehicles, and plug-in hybrids across passenger and commercial applications, the market is expected to continue expanding, supported by advancements in battery technology, fleet electrification commitments, and sustained government investment in charging infrastructure across urban, highway, and regional areas throughout Australia.

Executive Summary

The Australia electric vehicle market is on a sustained and accelerating growth trajectory, underpinned by progressive government policy, rapidly expanding charging infrastructure, advancing battery technology, and a decisive shift in consumer and corporate purchasing behavior toward sustainable mobility. The market reached USD 21.06 Billion in 2025 and is forecast to surpass USD 221.02 Billion by 2034, reflecting an exceptional CAGR of 28.80% over the forecast period.

ACT & New South Wales leads with a 34.5% revenue share in 2025, supported by comprehensive government rebate programs, stamp duty exemptions, and the most extensive public charging network in Australia. Victoria & Tasmania follows at 20.0%, with Queensland (18.5%), Western Australia (15.0%), and the Northern Territory & South Australia (12.0%) rounding out the national market, each supported by distinct state-level incentive frameworks.

Passenger vehicles command the dominant segment at 88.5% in 2025, reflecting the primacy of consumer-facing EV adoption. The Mid-range price category leads at 62.4%, demonstrating mainstream market penetration driven by increasingly competitive pricing from global and Chinese automakers. Battery electric vehicle sales exceeded 100,000 units for the first time in 2025, reaching 103,269 deliveries, marking a critical inflection point in the Australia electric vehicle market growth.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Vehicle Type) |

Passenger Vehicles – 88.5% share (2025) |

|

Largest Segment (Price Category) |

Mid-Range – 62.4% share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales – 34.5% revenue share (2025) |

|

Fastest Growing Region |

Queensland (government ZEV targets + charging investment) |

|

Top Companies |

Tesla, BYD Company Ltd, MG MOTOR, Hyundai Motor Company, Kia Corporation |

|

Key Milestone |

BEV sales exceeded 100,000 units for the first time in 2025 (103,269 deliveries) |

Key Analytical Observations Supporting the Above Data:

- Passenger Vehicles account for 88.5% of the Australian electric vehicle market in 2025, driven by strong consumer preference for electric SUVs and hatchbacks, government fringe benefits tax exemptions, and expanding model diversity from global automakers.

- Mid-range vehicles lead the price category segment at 62.4% (2025), attracting eco-conscious families and daily commuters with competitive features, extended driving ranges, and accessibility supported by government subsidies and tax benefits.

- Australia Capital Territory & New South Wales holds 34.5% of the Australian EV market in 2025, supported by progressive state government policies, fast-charging locations reaching 1,272 sites nationwide, and more than 800 high-powered charging plugs installed.

- Battery electric vehicle sales crossed the 100,000-unit milestone in 2025 at 103,269 deliveries, a 13.1% increase year-on-year, with BEVs now representing 8.3% of all new vehicle deliveries in Australia.

Australia Electric Vehicle Market Overview

Electric vehicles encompass passenger cars, commercial vehicles, and specialty vehicles powered fully or partially by electric motors, drawing energy from onboard battery packs. The Australian electric vehicle market ecosystem spans raw material and battery cell suppliers, vehicle manufacturers and importers, charging infrastructure operators, software and fleet management providers, government policy bodies, and end consumers across private, corporate, and public sector segments. Australia's transition from early EV adoption to mainstream acceptance has accelerated markedly, supported by a converging set of policy, economic, and technological drivers.

The introduction of Australia's New Vehicle Efficiency Standard has catalyzed supply-side change, requiring manufacturers to meet fleet-wide emissions targets and incentivizing the introduction of more diverse and affordable low-emission models to the Australian market. Complementing this regulatory framework, the national fleet now encompasses 153 EV models, providing consumers with unprecedented choice across price points, body styles, and propulsion technologies.

Market Dynamics

To evaluate market opportunities, Request Sample

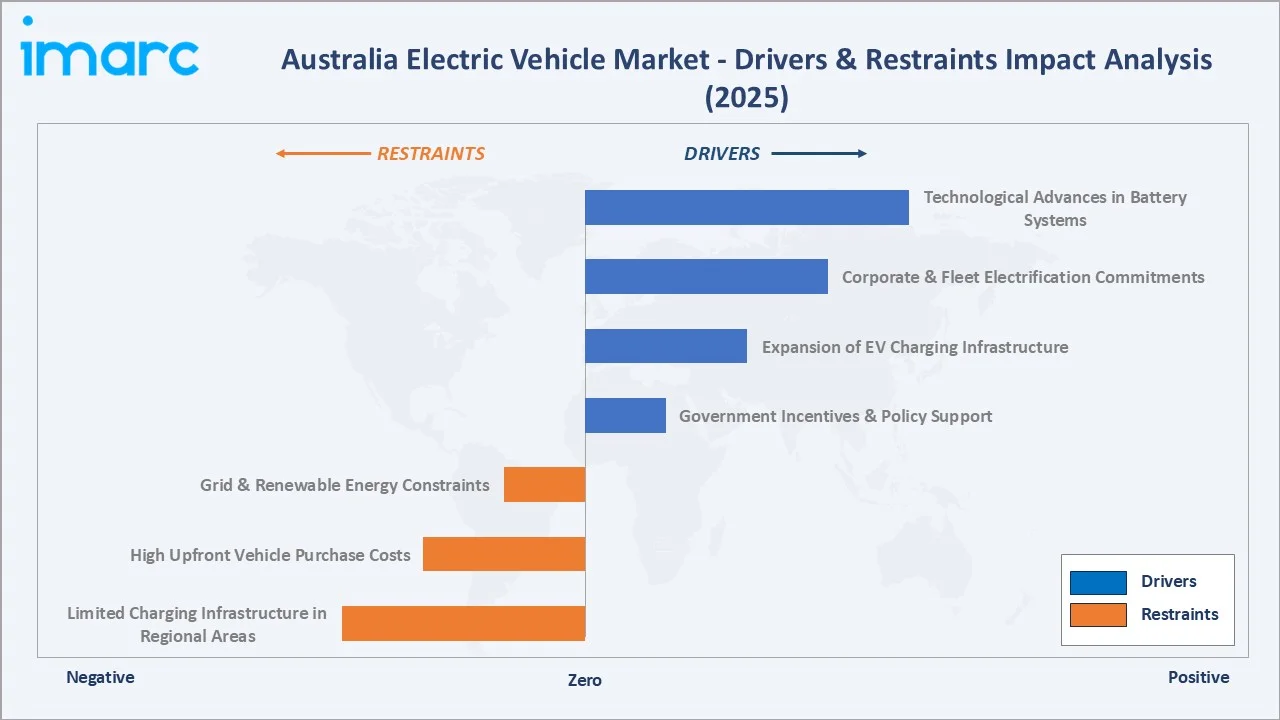

Market Drivers

- Government Incentives and Policy Support: Federal and state government incentives have materially reduced the total cost of electric vehicle ownership for both individual and corporate buyers. The New Vehicle Efficiency Standard passed by Australian Parliament is projected to deliver over AUD 95 billion in fuel savings and reduce carbon dioxide emissions by approximately 321 million tons by 2050.

- Expansion of EV Charging Infrastructure: Australia had 1,272 fast-charging locations with over 3,436 plugs by mid-2025, representing approximately 20% growth year-on-year. The Australian Government announced a AUD 40 million investment in September 2025 to expand kerbside and fast-charging infrastructure across suburbs and regional communities.

- Corporate and Fleet Electrification Commitments: Major logistics, car rental, utilities, and rideshare operators are leading the transition through bulk procurement, dedicated leasing models, and fleet charging infrastructure. IKEA Australia significantly scaled its zero-emission delivery efforts, with over 76% of customer deliveries completed using zero-emission vehicles as of August 2025, and is progressing toward its 90% zero-emission delivery target.

- Technological Advances in Battery Systems: Continuous improvements in battery energy density, charging speed, and cycle life are extending driving ranges, reducing charging times, and lowering per-kWh production costs, making electric vehicles increasingly competitive with conventional ICE vehicles across price segments.

Market Restraints

- Limited Charging Infrastructure in Regional Areas: Despite urban progress, charging infrastructure in rural and remote Australia remains substantially underdeveloped, creating range anxiety for buyers outside metropolitan centers and constraining EV adoption among a significant proportion of the population living in regional areas.

- High Upfront Vehicle Purchase Costs: Despite falling battery costs and government incentives, electric vehicles still carry a significant price premium over comparable ICE vehicles, particularly at entry-level price points, limiting first-time buyer accessibility among lower-income consumer segments.

- Grid and Renewable Energy Constraints: The rapid scaling of EV charging demand creates grid stability challenges in regions where renewable energy capacity has not yet caught up, requiring coordinated investment in grid upgrades alongside EV infrastructure expansion.

Market Opportunities

- Second-Hand EV Market Development: Fleet electrification by corporations and government agencies is creating a growing supply of late-model used electric vehicles, enabling lower-cost entry for private buyers and expanding the total addressable market beyond new vehicle purchasers.

- Vehicle-to-Grid Integration: Australia's high renewable energy penetration and household solar adoption create favorable conditions for vehicle-to-grid technology, enabling EV owners to generate revenue through grid services while supporting national energy system stability.

- Commercial Vehicle Electrification: The commercial vehicle segment, currently at 9.0% of the EV market, represents a high-growth opportunity as logistics, construction, and public transport operators accelerate fleet transitions in response to emissions regulations and fuel cost pressures.

Market Challenges

- Supply Chain Concentration Risk: Australia's EV market relies heavily on imported vehicles and battery components, creating exposure to global supply chain disruptions, currency fluctuations, and geopolitical risks affecting key manufacturing hubs in China, South Korea, and Japan.

- Consumer Education and Awareness Gaps: Despite growing adoption, significant misconceptions persist among Australian consumers regarding charging infrastructure availability, battery longevity, cold weather performance, and total cost of ownership, requiring sustained industry and government communication investment.

Emerging Market Trends

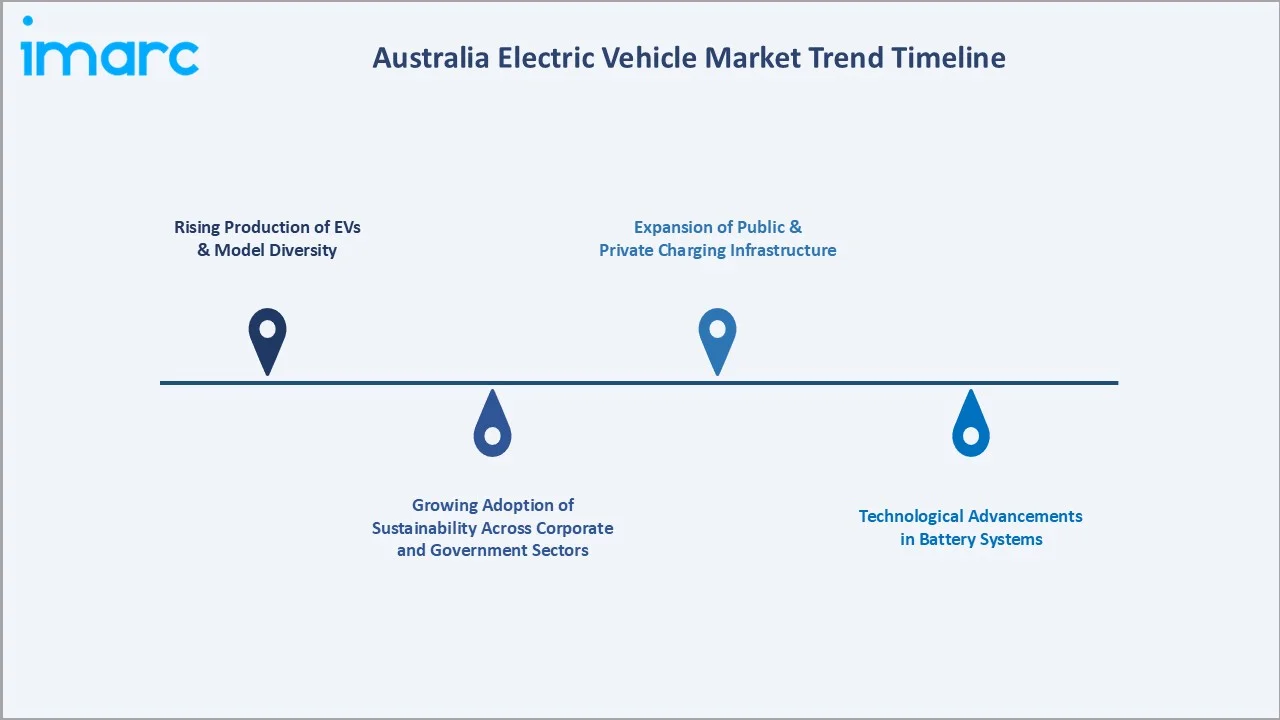

1. Rising Production of EVs and Model Diversity

Expanded manufacturing capacity from global automakers and Chinese brands has broadened model lineups from compact city cars to larger utility-style vehicles, with 153 EV models available in Australia by 2025. The Tesla Model Y maintained its position as Australia's best-selling electric vehicle in 2025 with 22,239 units delivered, demonstrating strong consumer preference for practical electric SUVs that combine range, technology, and value, reinforcing the Australian electric vehicle market trends toward mainstream adoption.

2. Growing Adoption of Sustainability Across Corporate and Government Sectors

Government agencies at the federal and state levels are accelerating this shift through policies promoting renewable energy integration and zero-emission transport mandates. The New Vehicle Efficiency Standard is projected to deliver cumulative fuel cost savings exceeding AUD 95 billion while cutting carbon dioxide emissions by approximately 321 million tons by 2050. This regulatory commitment is reinforcing corporate procurement decisions and creating sustained structural demand for electric vehicles across the fleet segment.

3. Technological Advancements in Battery Systems

Improvements in battery design are extending driving ranges beyond 500 kilometers on a single charge for premium models, while rapid-charging capability is reducing recharge times to under 30 minutes at DC fast chargers. The integration of bidirectional charging capabilities allows vehicles to operate as mobile energy storage units, supporting household energy management and grid stability, a particularly compelling proposition in Australia's high solar-penetration energy environment.

4. Expansion of Public and Private Charging Infrastructure

Australia had 1,272 fast-charging locations with over 3,436 plugs by mid-2025, representing approximately 20% annual growth. Western Australia completed its Electric Vehicle Highway connecting Perth to regional areas including Kalgoorlie, Geraldton, and Albany, with charging stations at intervals matching typical electric vehicle ranges.

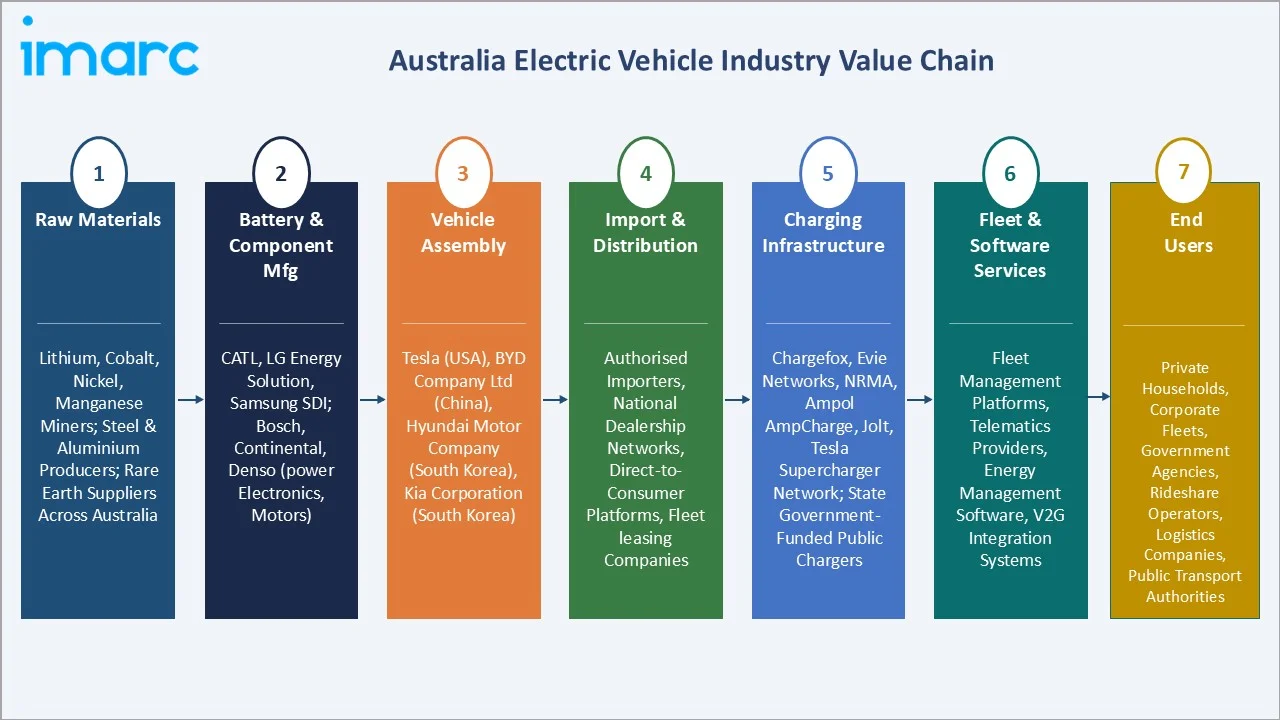

Industry Value Chain Analysis

The Australia electric vehicle value chain spans global raw material extraction through end-consumer operation, with each stage involving specialized operators whose performance directly influences vehicle availability, pricing, and ownership experience. Australia's market is predominantly import-dependent at the vehicle level, creating a value chain that intersects global supply networks with growing domestic charging and service infrastructure.

|

Stage |

Key Participants / Examples |

|

Raw Materials |

Lithium, cobalt, nickel, manganese miners; steel and aluminum producers; rare earth element suppliers across Australia |

|

Battery & Component Mfg |

CATL, LG Energy Solution, Samsung SDI (cells); Bosch, Continental, Denso (power electronics, motors) |

|

Vehicle Assembly |

Tesla (USA), BYD Company Ltd (China), Hyundai Motor Company (South Korea), Kia Corporation (South Korea) |

|

Import & Distribution |

Authorized importers, national dealership networks, online direct-to-consumer sales platforms, fleet leasing companies |

|

Charging Infrastructure |

Chargefox, Evie Networks, NRMA, Ampol AmpCharge, Jolt, Tesla Supercharger Network; state government-funded public chargers |

|

Fleet & Software Services |

Fleet management platforms, telematics providers, energy management software, V2G integration systems |

|

End Users |

Private households, corporate fleets, government agencies, rideshare operators, logistics companies, public transport authorities |

Technology Landscape in the Australia Electric Vehicle Industry

Advanced Battery Technology

Lithium-iron-phosphate (LFP) batteries are gaining market share in mid-range vehicles due to their superior safety profile, longer cycle life, and declining cost structure, while nickel-manganese-cobalt (NMC) chemistry continues to dominate in premium long-range applications. Solid-state battery development, expected to reach commercial viability by 2028–2030, promises further step-changes in energy density, charging speed, and thermal safety.

Vehicle-to-Grid and Smart Charging Technology

V2G-capable vehicles can provide grid stabilization services and household energy storage, creating revenue streams for owners while supporting the integration of variable renewable energy. Several Australian state governments are actively trialing V2G programs, with the ACT government leading a large-scale V2G pilot in Canberra, positioning Australia as a global leader in bidirectional EV technology deployment.

Connected and Autonomous Vehicle Integration

Australian EV manufacturers and technology companies are progressively integrating over-the-air software update capabilities, advanced driver assistance systems, and vehicle connectivity platforms into their offerings. These technologies enhance the ownership experience through continuous feature improvements and enable real-time fleet management for corporate operators. The development of autonomous driving capabilities, while still in early commercial stages in Australia, is creating long-term opportunities at the intersection of electrification and mobility-as-a-service business models.

Recycling and Second-Life Battery Technology

As Australia's EV fleet ages, battery recycling and second-life applications are emerging as critical technology domains. Second-life battery systems, where retired EV batteries with remaining capacity are redeployed as stationary storage, are gaining commercial traction alongside purpose-built battery recycling facilities. Several companies are developing Australian recycling infrastructure to capture the economic value of end-of-life battery materials, supporting circular economy objectives and reducing supply chain dependence on primary raw material extraction.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Type | Passenger Vehicles | 88.5% | 2025 |

| Price Category | Mid-Range | 62.4% | 2025 |

| Propulsion Type | Battery Electric Vehicle | 70.2% | 2025 |

| Region | Australia Capital Territory & New South Wales | 34.5% | 2025 |

By Vehicle Type

Passenger Vehicles dominate the vehicle type segment with an 88.5% share in 2025, equivalent to approximately USD 18.64 Billion in market value. This commanding position reflects the primacy of consumer-facing EV adoption in Australia, driven by government incentives specifically targeting private vehicle ownership, the availability of 94 battery electric vehicle models, and strong consumer preference for electric SUVs and hatchbacks.

To access detailed market analysis, Request Sample

Commercial Vehicles represent 9.0% of the market, with adoption concentrated in urban delivery vans, utility vehicles for infrastructure services, and light commercial vehicles operated by government agencies and logistics companies. The segment is growing as fleet operators calculate favorable total cost of ownership metrics for commercial EVs over 5–7 year operational cycles.

By Price Category

Mid-Range vehicles lead the price category segment with a 62.4% share in 2025. This segment's dominance reflects the successful democratization of EV technology, with vehicles in the AUD 45,000–AUD 80,000 price band offering competitive features including 400–600 km driving ranges, advanced safety systems, and modern infotainment platforms at price points increasingly supported by government subsidies.

High/Luxury Range vehicles account for 37.6% of the market, a substantial share reflecting Australia's relatively affluent early adopter base and the premium positioning of the market's dominant brand. Tesla's Model Y and Model 3 lineup spans the boundary between mid-range and luxury segments, while German premium automakers, including BMW, Mercedes-Benz, Audi, and Porsche, maintain strong representation among high-income buyers seeking premium electric options with established brand heritage.

Regional Market Insights

Australia Capital Territory & New South Wales (34.5%, 2025) lead Australia's EV market as the most advanced states for electric vehicle policy, infrastructure, and adoption. New South Wales maintains the nation's largest charging network with 357 total locations, and the AUD 5.9 million regional grant announced in November 2025 extends this leadership into regional areas.

|

Region |

Share (2025) |

Key Growth Drivers |

Infrastructure Status |

Key Incentives |

|

ACT & New South Wales |

34.5% |

Progressive govt policy; large corporate fleets; urban density |

357 charging locations; AUD 5.9M regional expansion grant (Nov 2025) |

Zero-interest EV loans; stamp duty exemption; registration discount |

|

Victoria & Tasmania |

20.0% |

ZEV targets; public transport electrification; strong urban EV demand |

Dense urban charging network; expanding regional corridors |

EV stamp duty waiver; government fleet electrification mandate |

|

Queensland |

18.5% |

State ZEV strategy; tourism EVs; growing fleet adoption |

Gold Coast and Brisbane charging expansion; highway corridors |

AUD 3,000 EV rebate; stamp duty concession for new EVs |

|

Western Australia |

15.0% |

EV Highway completion; mining sector EVs; state net-zero targets |

EV Highway connecting Perth to Kalgoorlie, Geraldton, Albany |

EV rebate program; discounted registration fees |

|

NT & South Australia |

12.0% |

Growing renewables integration; state fleet targets; regional tourism |

Developing infrastructure; SA focused on corridor charging |

SA EV subsidy; NT emerging policy framework |

Victoria & Tasmania (20.0%) is supported by the Victorian government's zero-emission vehicle targets and strong public transport electrification commitments, including a mandate to electrify the entire government fleet. Queensland (18.5%) is accelerating EV adoption through its state ZEV strategy and AUD 3,000 purchase rebate, with Brisbane and the Gold Coast emerging as particularly active EV markets.

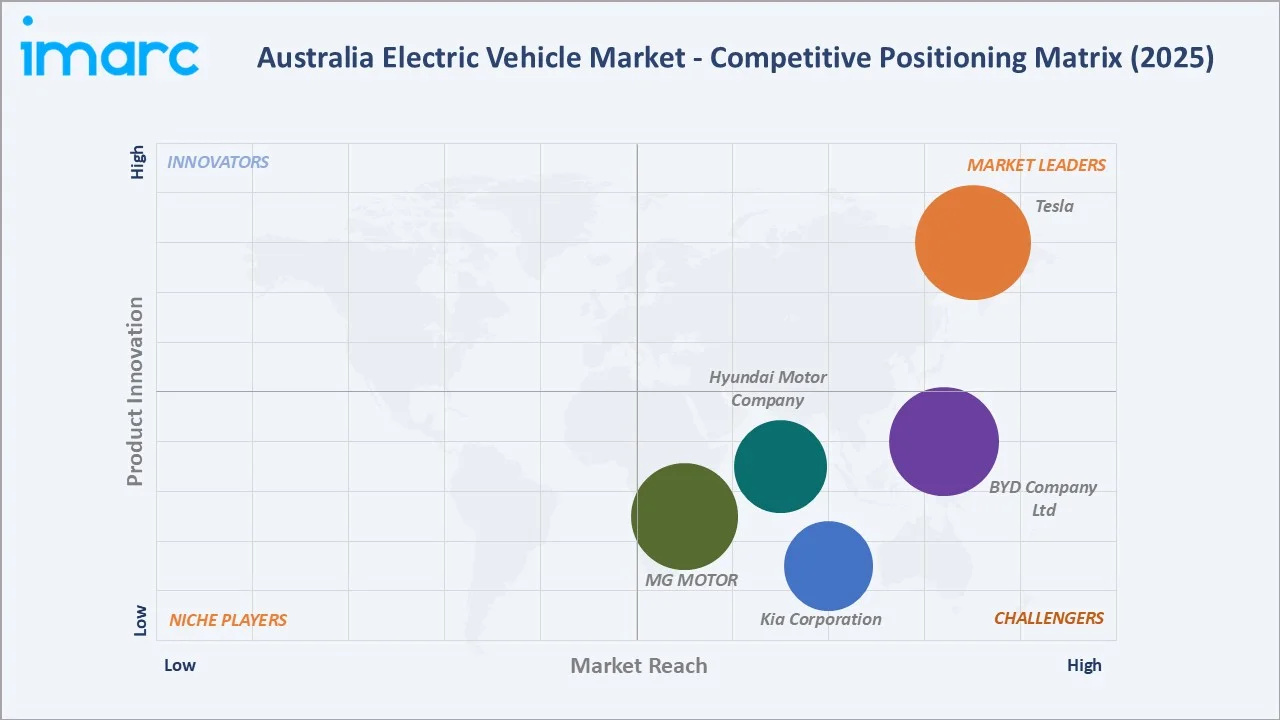

Competitive Landscape

The Australia electric vehicle market exhibits intensifying competitive dynamics, with multinational automakers, established Japanese brands, and rapidly expanding Chinese manufacturers competing across all price segments. The market structure is moderately concentrated at the premium tier, while the mid-range and entry-level segments are increasingly contested by a growing number of Chinese brands offering feature-rich vehicles at competitive price points.

|

Company |

Key Models |

Market Position |

Core Strength |

|

Tesla |

Model Y, Model 3 |

Market Leader |

Australia's #1 EV brand; Model Y best-seller with 22,239 units in 2025; proprietary Supercharger network advantage |

|

BYD Company Ltd |

Atto 3, Seal, Dolphin, Sealion 6, Shark 6, Sealion 7 |

Strong Challenger |

Rapid Australian market expansion; vertically integrated battery supply; competitive pricing across multiple segments |

|

MG MOTOR |

MG4, MGS5 EV, MG4 XPOWER, Cyberster, MG IM5, MG IM6 |

Challenger |

Value-oriented market positioning; strong dealer network; popular entry-level EV models for first-time buyers |

|

Hyundai Motor Company |

IONIQ 5, IONIQ 9, Kona Electric, INSTER, ELEXIO, IONIQ 5 N, MIGHTY Electric |

Challenger |

Premium EV technology with 800V ultra-fast charging; strong brand trust and established dealer service network |

|

Kia Corporation |

EV5, EV3, EV9, EV6, EV4 Sedan |

Challenger |

Award-winning design; competitive pricing; strong SUV lineup appealing to Australian family buyers |

The competitive landscape is being reshaped by the accelerating entry of Chinese EV brands, which are leveraging manufacturing scale and vertically integrated battery supply chains to offer vehicles at prices that challenge established players. Simultaneously, traditional European and Korean automakers are rapidly expanding their EV model lineups to defend market share.

Key Company Profiles

Tesla

Tesla, headquartered in Austin, Texas, is Australia's dominant electric vehicle brand, maintaining market leadership through its comprehensive product lineup, proprietary Supercharger network, and direct-to-consumer sales model.

- Product Portfolio: Model Y, Model 3

- Recent Developments: In March 2026, Tesla announced its plans to build its largest Supercharger station in Australia with more than 25 high‑power stalls that will surpass the current 20‑stall location in Goulburn, NSW.

- Strategic Focus: Supercharger network expansion to third-party vehicles; Model Y refresh driving volume growth; Full Self-Driving capability expansion; V2G integration with the Australian residential solar market.

BYD Company Ltd

BYD Company Ltd, which operates in Australia as BYD Australia Pty Ltd, is the world's largest EV manufacturer and Australia's fastest-growing EV brand, leveraging its vertically integrated battery manufacturing capability and extensive model range to rapidly expand market presence.

- Product Portfolio: Atto 3, Seal, Dolphin, Sealion 6, Shark 6, Sealion 7

- Recent Developments: In April 2026, BYD expanded its presence in the Australian utility vehicle segment with the expansion of its Shark 6 range, including a trade-focused cab-chassis variant and a new performance-oriented flagship designed to broaden the appeal of its Dual Mode (DM) plug-in hybrid ute platform.

- Strategic Focus: Expansion beyond urban centers into regional markets; Shark ute market penetration; competitive pricing strategy leveraging cell-to-body battery integration; growing aftersales service network.

MG Motor

MG Motor, a brand of SAIC Motor Corporation headquartered in Shanghai, China, has established a strong presence in the Australian EV market through its value-oriented positioning and broad dealership distribution.

- Product Portfolio: MG4, MG S5 EV, MG4 Long Range 77, MG4 XPOWER, Cyberster, MG IM5 MG IM6

- Recent Developments: In August 2025, MG Motor Australia broadened its small electric vehicle lineup by introducing a second version of the MG 4 EV, a more affordable front‑wheel‑drive hatch that will sit below the existing rear‑ and all‑wheel‑drive models in the range.

- Strategic Focus: Value market leadership; dealer network expansion into regional areas; fleet sales growth with a competitive total cost of ownership proposition; product range expansion into higher segments.

Market Concentration Analysis

The Australia electric vehicle market exhibits moderate-to-high concentration at the sales volume level, with Tesla maintaining clear market leadership and the top five brands collectively accounting for approximately 65–70% of new EV deliveries in 2025. However, the rapid entry of Chinese brands and the accelerating model introductions from established automakers are progressively fragmenting market share, increasing competitive intensity across all price segments.

Brand concentration is highest in the premium segment, where Tesla's Supercharger network advantage and brand loyalty create meaningful switching barriers. The mid-range and entry-level segments are experiencing the most rapid fragmentation, with multiple Chinese brands, including BYD, MG, GWM Ora, and Chery, all competing aggressively through competitive pricing, feature richness, and expanding dealer coverage.

Investment & Growth Opportunities

Fastest Growing Segments

Commercial vehicle electrification (estimated CAGR above 35%), electric utes targeting Australia's dominant ute market segment, and EV charging-as-a-service infrastructure represent the three highest-growth investment opportunities in the Australian EV ecosystem through 2034. Together, these opportunity areas address a total addressable market of approximately USD 45 billion by 2030, driven by converging fleet electrification commitments, government mandates, and consumer demand for EV variants across all major vehicle body types.

Infrastructure Investment Opportunities

Australia's charging infrastructure deficit, particularly in regional and rural areas, represents a multi-billion-dollar investment opportunity for infrastructure operators, energy companies, and strategic co-investors. The Australian Government's AUD 40 million infrastructure commitment is intended to catalyze substantially larger private sector co-investment, with favorable economics available for DC fast-charging operators in high-traffic corridors.

Venture and Institutional Investment Trends

- Key investment themes include battery recycling and second-life battery systems, V2G software and hardware platforms, EV fleet management technology, and regional charging infrastructure operators.

- Private equity interest is targeting EV charging network operators, fleet leasing companies building dedicated EV products, and software providers enabling smart charging and energy management integration.

- Impact capital is increasingly available for projects that combine EV infrastructure deployment with renewable energy integration, particularly in regional and remote communities with high diesel dependency and strong solar resources.

Future Market Outlook (2026-2034)

The Australia electric vehicle market is positioned for exceptional, sustained growth through 2034. From a base of USD 21.06 Billion in 2025, the market is projected to reach USD 221.02 Billion by 2034, representing total incremental value creation of USD 199.96 Billion over the forecast decade at a CAGR of 28.80%.

The convergence of regulatory pressure from New Vehicle Efficiency Standards, expanding model availability across all price and vehicle-type segments, rapid infrastructure scaling, and accelerating corporate and government fleet commitments creates a self-reinforcing growth dynamic. Manufacturers that achieve competitive pricing in the AUD 35,000–50,000 price bracket, build reliable national service networks, and demonstrate compatibility with Australia's high-solar residential energy environment will capture a disproportionate share of the volume growth anticipated through 2034.

Australia's unique energy market characteristics, including very high residential solar penetration, a national grid undergoing rapid decarbonization, and some of the world's largest lithium reserves, position the country as a globally significant node in the long-term electric vehicle ecosystem. The Australia electric vehicle market trends toward domestically powered, solar-integrated vehicle operation represent a compelling long-term value proposition that will continue attracting consumer, corporate, and investor interest throughout the forecast period.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 100 industry participants during 2024–2025, including EV brand representatives, dealership operators, fleet managers, charging infrastructure operators, government policy officials, and automotive industry analysts across New South Wales, Victoria, Queensland, and Western Australia.

Secondary Research

Secondary research encompassed systematic review of Federal Chamber of Automotive Industries sales data, Electric Vehicle Council Australia reports, state government EV strategy documents, company annual reports, Australian government policy publications, and trade press covering the automotive and energy sectors. Over 180 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches incorporating EV sales data, vehicle fleet projections, government policy commitments, charging infrastructure deployment rates, and battery cost trajectory analyses. A base-case CAGR of 28.80% reflects consensus estimates validated against reported national EV sales data and industry body forecasts.

Australia Electric Vehicle Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles, Others |

| Price Categories Covered | Mid-Range, High/Luxury Range |

| Propulsion Types Covered | Battery Electric Vehicle, Hybrid Electric Vehicle, Plug-In Hybrid Electric Vehicle |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Tesla, BYD Company Ltd, MG MOTOR, Hyundai Motor Company, Kia Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Electric Vehicle Market Report

The Australia electric vehicle market reached USD 21.06 Billion in 2025. It is projected to reach USD 221.02 Billion by 2034.

The Australia electric vehicle market is expected to grow at a CAGR of 28.80% during the forecast period from 2026 to 2034, driven by strong policy support, expanding infrastructure, and accelerating consumer and corporate adoption.

Australia Capital Territory & New South Wales lead with a 34.5% revenue share in 2025, supported by progressive government incentives, Australia's most extensive public charging network, and high levels of corporate and government fleet electrification activity centered on Sydney and Canberra.

Passenger vehicles dominate with an 88.5% share in 2025, driven by strong consumer demand for electric SUVs and hatchbacks, fringe benefits tax exemptions, and expanding model diversity from global automakers including Tesla, BYD Company Ltd, MG, Hyundai, and Kia.

Mid-Range vehicles lead with a 62.4% share in 2025, reflecting successful mainstream market penetration supported by government subsidies, increasing model competition from Chinese automakers, and growing consumer acceptance of electric vehicle total cost of ownership benefits.

Key players in the market include Tesla, BYD Company Ltd, MG MOTOR, Hyundai Motor Company, Kia Corporation, and others, among other global automakers, are competing across the passenger, commercial, and premium EV segments.

Australia had 1,272 fast-charging locations with over 3,436 plugs by mid-2025, representing approximately 20% annual growth. The Australian Government's AUD 40 million infrastructure investment under its Net Zero Plan and state-level grants are progressively eliminating range anxiety as a barrier to EV adoption, particularly in regional and remote areas.

Key challenges include limited charging infrastructure in rural and remote areas, the persistent price premium of EVs over comparable ICE vehicles, grid stability concerns from rapid charging demand growth, supply chain concentration risk in imported vehicles and battery components, and ongoing consumer education gaps around EV ownership.

Significant opportunities exist in regional and highway EV charging infrastructure, commercial and fleet vehicle electrification, vehicle-to-grid technology integration, battery recycling and second-life systems, EV fleet management software, and electric ute vehicles targeting Australia's dominant ute market segment. The market is projected to create USD 199.96 Billion in incremental value between 2025 and 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)