Australia Engineering Plastics Market Size, Share, Trends and Forecast by Type, Performance Parameter, Application, and Region, 2026-2034

Australia Engineering Plastics Market Size, Share, Trends & Forecast (2026-2034)

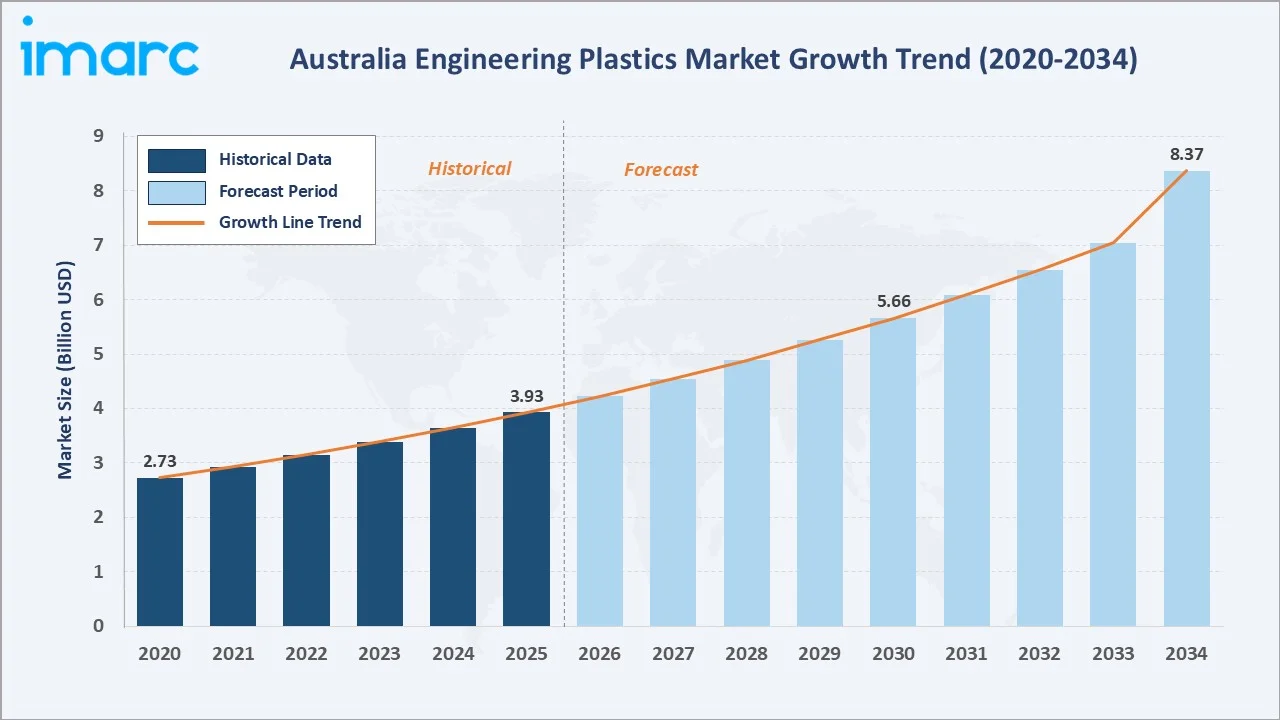

The Australia engineering plastics market reached USD 3.93 Billion in 2025 and is projected to reach USD 8.37 Billion by 2034, growing at a CAGR of 7.58% during 2026-2034. Market growth is driven by expanding demand from automotive lightweighting, electrical & electronics manufacturing, construction infrastructure, and medical device applications.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.93 Billion |

|

Forecast Market Size (2034) |

USD 8.37 Billion |

|

CAGR (2026-2034) |

7.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

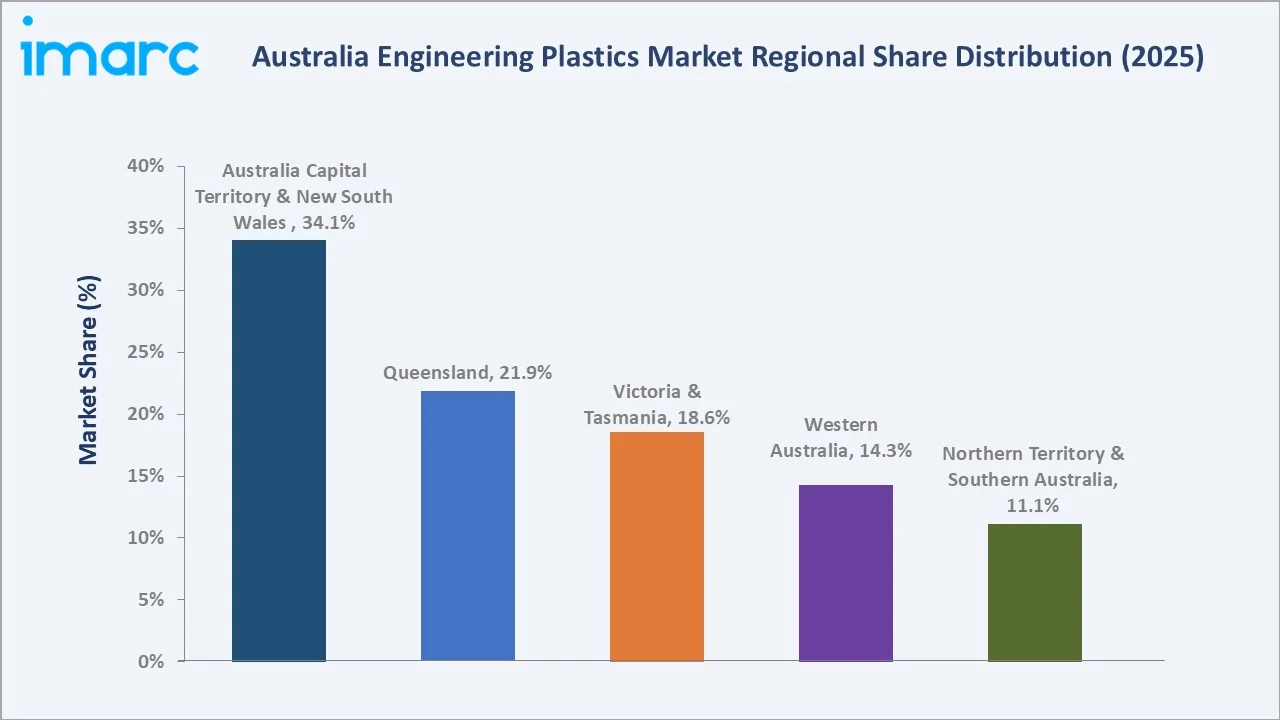

Australia Capital Territory & New South Wales’s 34.1% dominance reflects Sydney's concentration of automotive OEMs, electronics manufacturers, and medical device companies requiring engineering plastics, along with Canberra's defense and aerospace sector procurement.

To get more information on this market, Request Sample

The market's 7.58% CAGR reflects the compounding demand from multiple industrial sectors simultaneously transitioning toward higher-performance materials. Automotive electrification requires thermally stable, high-dielectric-strength engineering plastics for battery housings and EV drivetrain components, while 5G infrastructure rollout and data center construction are driving demand for flame-retardant polycarbonate and high-performance fluoropolymers.

Executive Summary

The Australia engineering plastics market is on a consistent growth trajectory driven by the convergence of automotive lightweighting, electronics expansion, construction investment, and the transition to high-performance sustainable materials. From USD 3.93 Billion in 2025, the market will reach USD 8.37 Billion by 2034, creating USD 4.44 Billion in incremental value at a 7.58% CAGR.

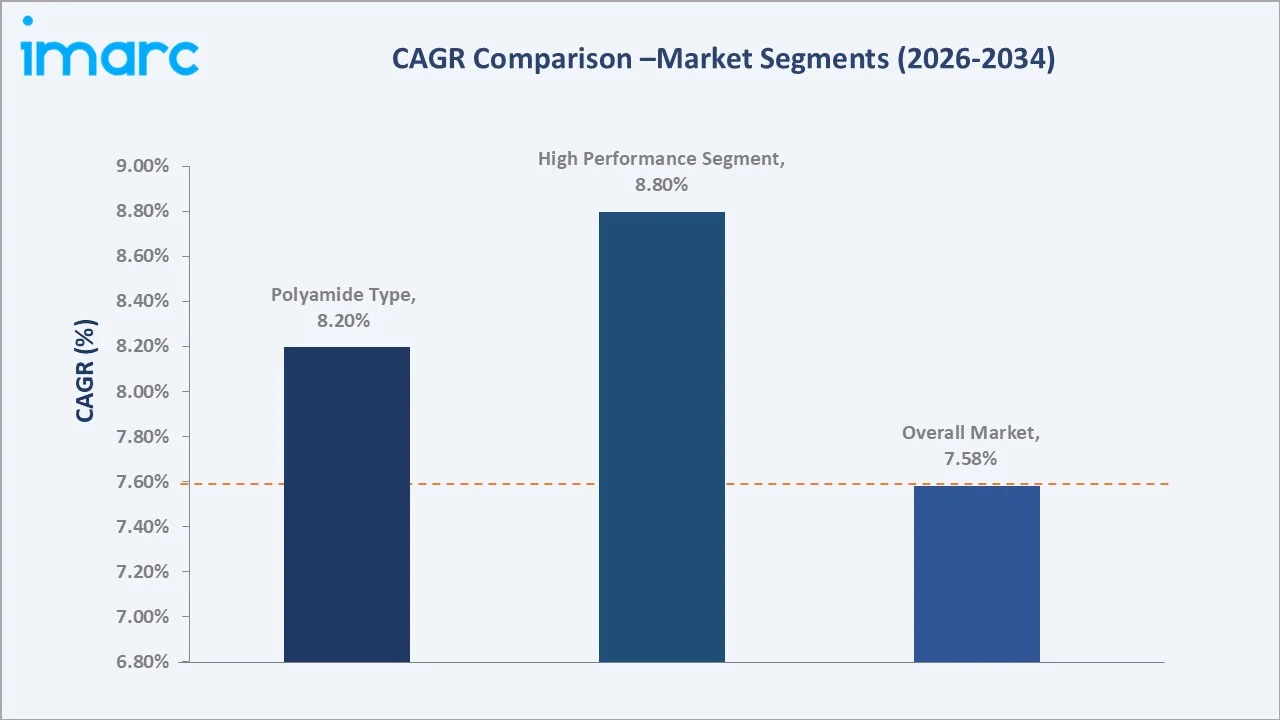

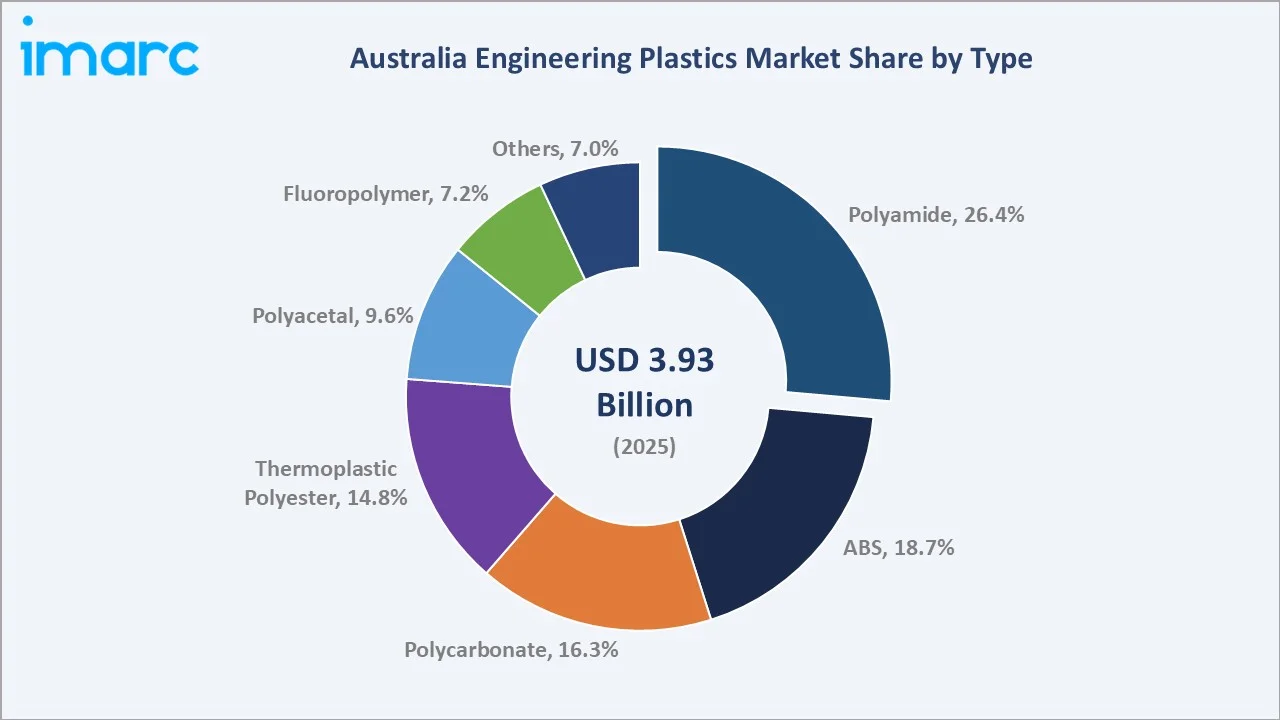

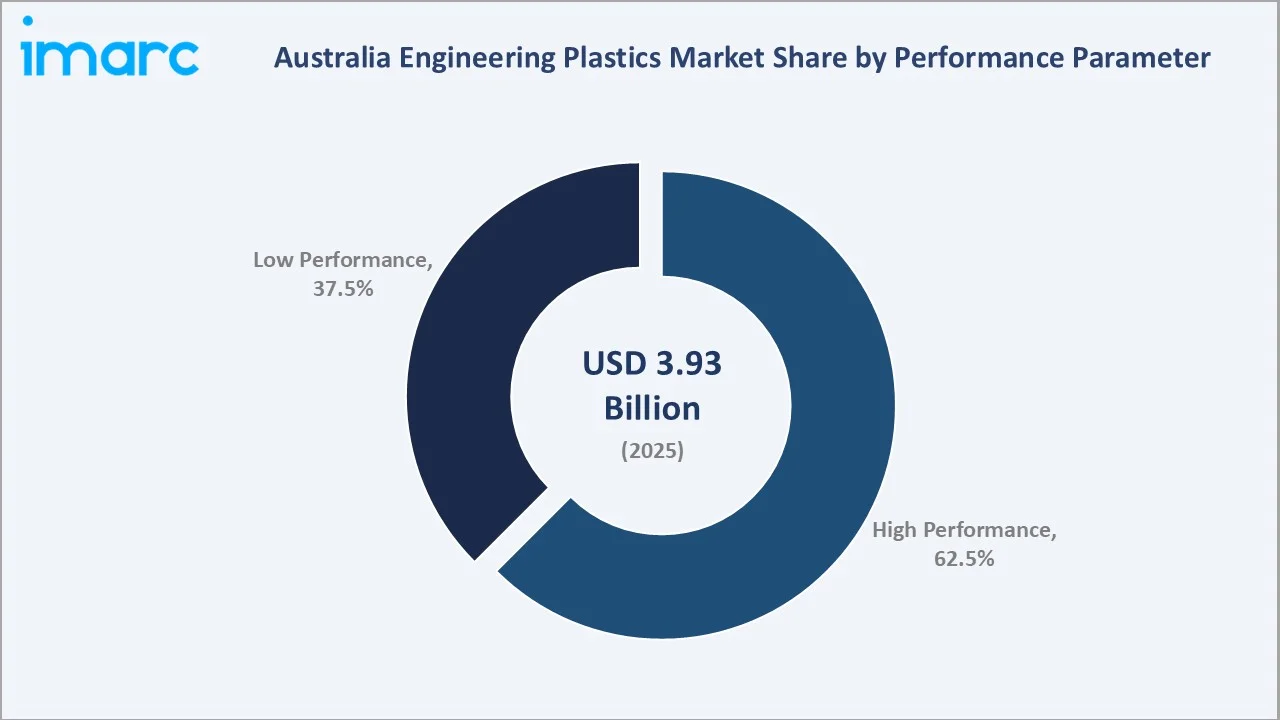

Polyamide leads the type segment at 26.4% in 2025, driven by its combination of mechanical strength, chemical resistance, and thermal stability that makes it the polymer of choice for automotive structural parts, industrial connectors, and consumer durable applications. High performance grades command 62.5% of the performance parameter segment, reflecting the growing proportion of engineering plastic consumption driven by demanding technical specifications in EV, aerospace, and medical device applications.

Key players, including BASF, XRG Group, Arkema, and Mitsubishi Chemical Group Corporation, supply the Australian market through import-based distribution networks supported by local technical application development teams, competing on material grade breadth, regulatory compliance certification, lead time reliability, and application engineering support services.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Polyamide – 26.4% share (2025) |

|

Fastest Growing Type |

Fluoropolymer – high growth driven by chemical and semiconductor demand |

|

Largest Performance Segment |

High Performance – 62.5% share (2025) |

|

Fastest Growing Performance |

High Performance – ~8.80% CAGR (2026-2034) |

|

Leading Region |

Australia Capital Territory & New South Wales – 34.1% share (2025) |

|

Top Companies |

BASF, XRG Group, Arkema, and Mitsubishi Chemical Group Corporation |

Key Analytical Observations:

- Polyamide at 26.4% (2025) dominates the type segment due to its exceptional balance of properties across multiple performance dimensions, tensile strength up to 80-95 MPa, continuous use temperature up to 160-180°C for PA46, and inherent lubricity reducing wear in moving parts without external lubrication.

- High performance grades command 62.5% of the Australian engineering plastics market in 2025. This above-average proportion reflects Australia's industrial mix, which skews toward technically demanding applications in mining equipment, defense components, aerospace parts, and medical devices that require materials exceeding the performance envelope of standard commodity polymers.

- ABS (Acrylonitrile Butadiene Styrene) at 18.7% is the second-largest type segment, driven by consumer electronics, automotive interior trims, and 3D printing feedstock demand. Australia's growing industrial 3D printing sector is generating new demand for engineering-grade ABS and ABS blend filaments for direct manufacturing of functional parts in aerospace and defense applications.

- The Australia Capital Territory & New South Wales region's 34.1% (2025) leadership reflects Sydney's industrial manufacturing concentration, including automotive component suppliers in Western Sydney, electronics manufacturing in the Greater Sydney technology corridor, and medical device manufacturers across NSW.

Australia Engineering Plastics Market Overview

Engineering plastics are a class of high-performance polymeric materials engineered to deliver mechanical, thermal, chemical, and electrical properties that exceed those of commodity plastics (polyethylene, polypropylene, PVC).

They include polyamides (PA), ABS, polycarbonate (PC), thermoplastic polyesters (PET, PBT), polyacetals (POM), fluoropolymers (PTFE, PVDF, FEP), and specialty high-performance resins (PEEK, PPS, PSU). In Australia, engineering plastics are consumed across automotive, electrical & electronics, construction, industrial machinery, aerospace, medical devices, and consumer goods sectors.

Australia is predominantly an importer of engineering plastics, with limited domestic polymer synthesis capacity. The supply chain is characterized by global chemical companies supplying through Australian distributors who provide technical support, customized blending, and short-lead-time local inventory for Australian fabricators.

The fabrication and part manufacturing stage, injection molding, extrusion, machining, and 3D printing of engineering plastic components, represents the primary domestic industrial value-add layer.

Market Dynamics

To evaluate market opportunities, Request Sample

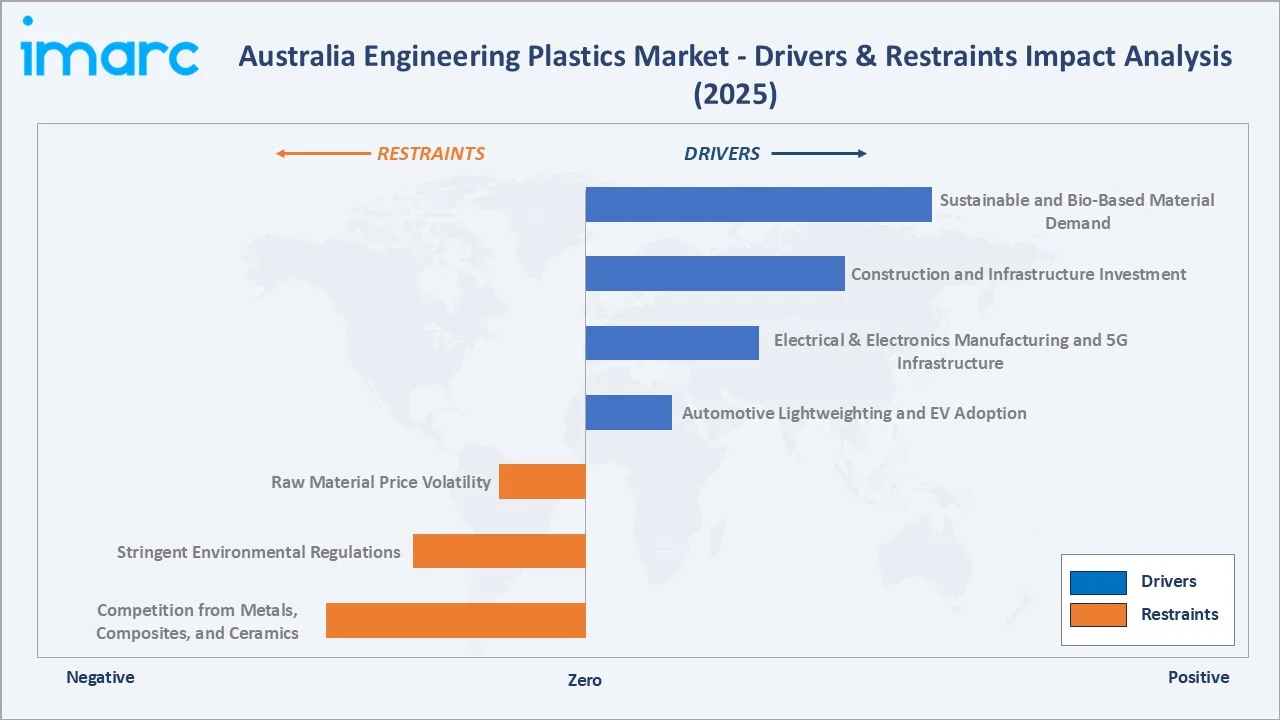

Market Drivers

- Automotive Lightweighting and EV Adoption: Australia's transition to electric vehicles is generating demand for engineering plastics in battery modules, motor housings, high-voltage connectors, charging infrastructure, and structural brackets.

- Electrical & Electronics Manufacturing and 5G Infrastructure: Australia's 5G network rollout requires engineering plastics for antenna housings, circuit board substrates, and cable management systems.

- Construction and Infrastructure Investment: Australia's housing affordability crisis is driving record residential construction activity, while the federal government's infrastructure investment program is creating demand for engineering plastics in plumbing fittings, electrical conduit and fittings, structural brackets, and facade cladding systems.

- Sustainable and Bio-Based Material Demand: Australian industrial buyers are increasingly requiring sustainable material options to meet Scope 3 emissions commitments. Bio-based polyamides, recycled-content ABS and PC, and bio-derived PLA engineering blends are growing at premium price points.

Market Restraints

- Raw Material Price Volatility: Engineering plastics pricing is directly linked to petrochemical feedstock costs. Global oil price swings of 20–30% translate into polymer price fluctuations of 15–25%, creating procurement uncertainty for Australian fabricators who operate on long-term contracts with their end-customer OEMs but are exposed to spot pricing risk on polymer inputs.

- Stringent Environmental Regulations: Australia's National Plastics Plan, Chemical Innovations Taskforce, and state-level EPR regulations are increasing compliance requirements for engineering plastic formulations, particularly regarding fluorinated compounds, brominated flame retardants, and heavy metal stabilizers.

- Competition from Metals, Composites, and Ceramics: In high-performance applications such as aerospace structural components, industrial pump housings, and mining wear parts, engineering plastics compete directly with aluminum alloys, carbon fiber composites, and ceramic materials.

Market Opportunities

- Additive Manufacturing and 3D Printing Feedstocks: Australia's industrial 3D printing sector is growing at 15%+ annually, creating new demand for engineering-grade filaments, powder bed fusion materials, and photopolymer resins from engineering plastic precursors.

- Mining Equipment Applications: Australia's mining sector is the world's largest consumer of many commodities by per-GDP measure. Mining equipment manufacturers and operators are replacing steel wear liners, UHMWPE chutes, and metal bearings with engineering plastics in applications where weight reduction, corrosion resistance, and reduced maintenance frequency justify the material substitution economics.

Market Challenges

- Skilled Technical Specification Workforce: Engineering plastic selection for Australian industrial applications requires materials engineers capable of specifying polymer grade, fill content, and processing parameters for each application. The shortage of materials engineers and polymer processing technicians in the Australian labor market constrains new application development cycles.

- Supply Chain Lead Time Dependency: As a predominantly import-dependent market for primary engineering plastics, Australia is exposed to long supply chain lead times, typically 8–16 weeks for specialty grades from European and Asian suppliers. Supply disruptions can cause extended material shortages that force fabricators to substitute alternative grades, disrupting quality systems and requiring recertification of components in regulated industries.

Emerging Market Trends

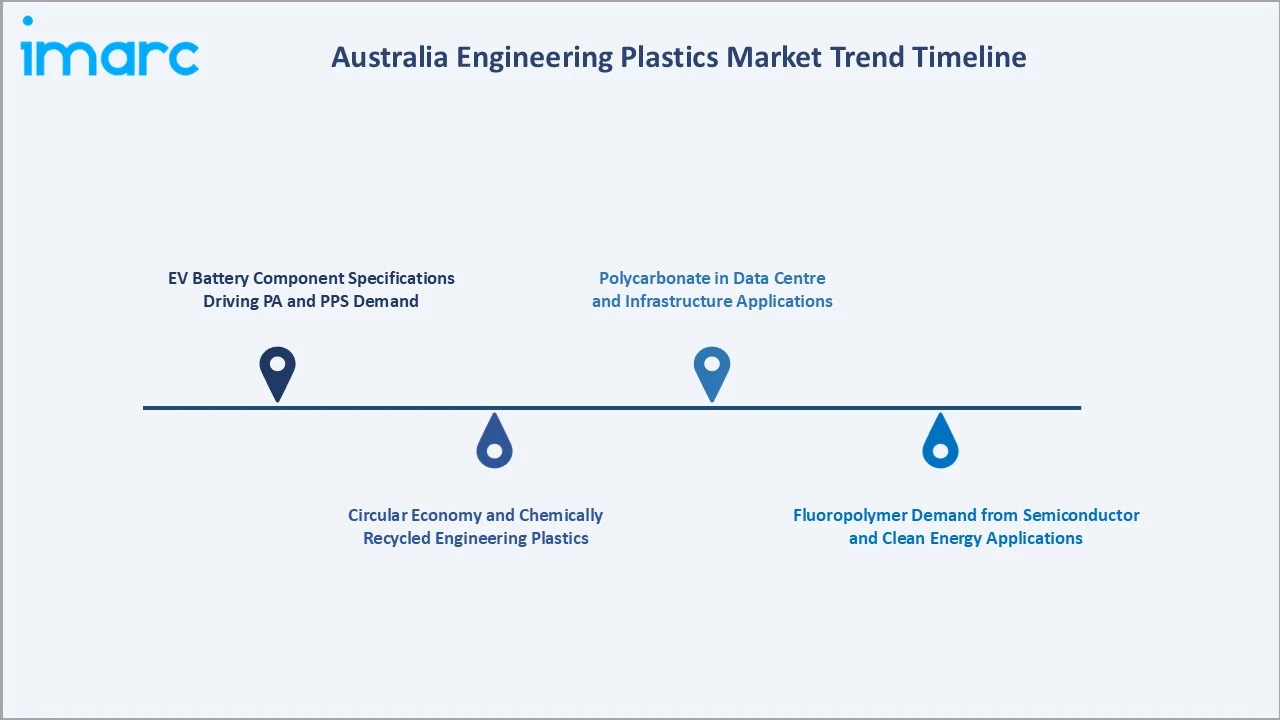

1. EV Battery Component Specifications Driving PA and PPS Demand

Australia's accelerating EV adoption, from 10% of new car sales in 2025 to projected 50%+ by 2030, is establishing engineering plastics as critical EV supply chain materials. PA6, PA66-GF30, and PPS are specified for high-voltage connector housings, battery cell holders, and motor end-shields in Australian EV assembly and component manufacturing operations.

2. Circular Economy and Chemically Recycled Engineering Plastics

Covestro's Makrolon RE and Arkema's Rilsan PA11 are gaining adoption among Australian automotive and consumer goods OEMs seeking to close their polymer supply chain loops. Samsara Eco's enzyme-based PET recycling platform, developed in Australia, represents a domestic contribution to engineering plastic circularity.

3. Fluoropolymer Demand from Semiconductor and Clean Energy Applications

Australia's nascent semiconductor manufacturing ambitions, supported by the National Reconstruction Fund, and expanding clean hydrogen infrastructure are creating new demand for PTFE and PVDF in ultra-pure chemical handling, fuel cell membrane precursors, and electrolysis equipment components. The Chemours Company's Teflon PTFE and Arkema's Kynar PVDF are the primary specifications for these applications, commanding significant price premiums over commodity engineering plastics.

4. Polycarbonate in Data Centre and Infrastructure Applications

Australia is emerging as an Asia-Pacific hub for sovereign AI infrastructure, supported by major investments including OpenAI’s planned AUD 7 billion Sydney AI campus, AWS’s AUD 20 billion expansion, and Project Southgate’s 1.6 GW NVIDIA-powered capacity. This is driving consistent demand for polycarbonate enclosures, structural glazing, and LED lighting diffusers.

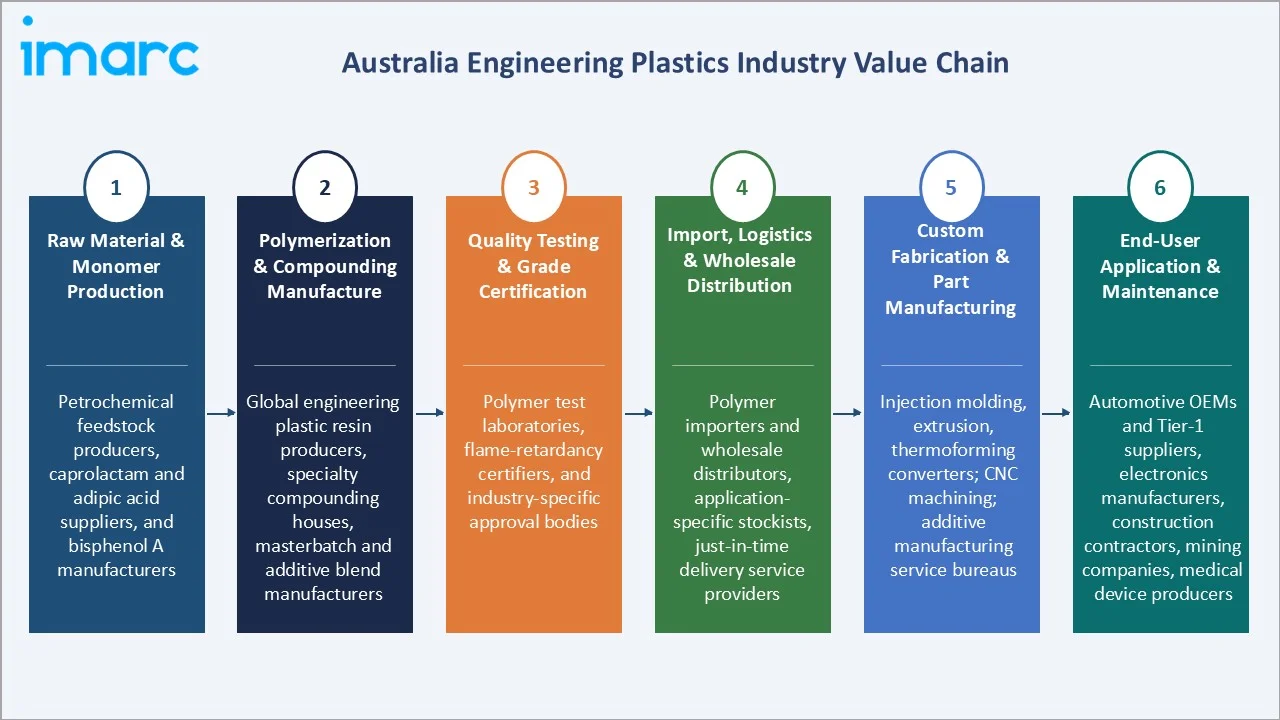

Industry Value Chain Analysis

Australia's engineering plastics value chain is primarily import-driven at the resin stage, with domestic value creation concentrated in distribution, compounding, and component fabrication stages.

|

Stage |

Key Players / Examples |

|

Raw Material & Monomer Production |

Petrochemical feedstock producers, caprolactam and adipic acid suppliers, and bisphenol A manufacturers |

|

Polymerization & Compounding Manufacture |

Global engineering plastic resin producers, specialty compounding houses, masterbatch and additive blend manufacturers |

|

Quality Testing & Grade Certification |

Polymer test laboratories, flame-retardancy certifiers, and industry-specific approval bodies |

|

Import, Logistics & Wholesale Distribution |

Polymer importers and wholesale distributors, application-specific stockists, just-in-time delivery service providers |

|

Custom Fabrication & Part Manufacturing |

Injection molding, extrusion, thermoforming converters; CNC machining; additive manufacturing service bureaus |

|

End-User Application & Maintenance |

Automotive OEMs and Tier-1 suppliers, electronics manufacturers, construction contractors, mining companies, medical device producers |

Technology Landscape in the Australia Engineering Plastics Industry

Polyamide (PA) Technology

Modern PA compounding incorporates glass fiber, carbon fiber, mineral fill, and flame retardant additives to create application-specific grades. BASF's Ultramid and Celanese’s Zytel are the dominant platforms in the Australian market, with glass-filled grades predominating in structural applications.

Polycarbonate (PC) Technology

Polycarbonate at 16.3% serves transparent, impact-resistant, and flame-retardant applications. Produced from bisphenol A and phosgene via interfacial polymerization, PC offers transparency, impact strength 30× higher than glass, and UL94 V-0 flame retardancy in specialty grades.

Fluoropolymer Technology

Fluoropolymers at 7.2% represent the highest value-per-kilogram engineering plastic segment. PTFE, PVDF, ETFE, and FEP offer unmatched chemical inertness, thermal stability, and electrical insulation across all frequency ranges. In Australia, fluoropolymers are specified for chemical processing equipment, semiconductor ultra-pure fluid handling, offshore oil & gas seals, and medical implantable device components.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Polyamide |

26.4% |

2025 |

|

Performance Parameter |

High Performance |

62.5% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

34.1% |

2025 |

By Type

Polyamide leads the type segment at 26.4% in 2025. Its dominance reflects the broadest application range of any single engineering plastic family, from automotive under-bonnet components and industrial gears to food-contact conveyor systems and sporting goods.

To access detailed market analysis, Request Sample

PA's combination of processability, recyclability, and potential for bio-based variants makes it central to both current performance demands and future sustainability strategies of Australian industrial OEMs.

ABS at 18.7% serves consumer electronics, automotive interior, and 3D printing applications. Polycarbonate at 16.3% dominates transparent and flame-retardant structural applications. Thermoplastic polyester at 14.8% serves electrical connector and automotive electronic housing applications.

By Performance Parameter

High performance grades command a 62.5% market share in 2025. These grades include glass or carbon fiber-reinforced polyamides, flame-retardant polycarbonate, high-heat PPS, specialty fluoropolymers, and aerospace/medical-grade PEEK compounds.

Australia's industrial mix, weighted toward mining equipment, defense components, aerospace parts, and medical devices, drives above-average high performance grade consumption compared to manufacturing-intensive economies where standard grades constitute a larger proportion of total engineering plastic use.

Low performance grades at 37.5% serve construction fittings, consumer goods, agricultural equipment, and general industrial applications where standard mechanical properties at competitive pricing are the primary specification driver.

Regional Market Insights

Australia Capital Territory & New South Wales leads with a 34.1% market share in 2025. Sydney's industrial base, including automotive component suppliers in Western Sydney, the largest electronics manufacturing cluster in Australia, and a significant medical device manufacturing sector, creates diverse, multi-sector engineering plastic demand.

Victoria & Tasmania's 18.6% share is anchored by Melbourne's transition from traditional automotive manufacturing to EV component and advanced materials production. Western Australia's 14.3% share reflects the mining sector's significant engineering plastic consumption, in applications from UHMWPE chute liners to PA gear components and fluoropolymer chemical seals at major mine sites.

|

Region |

Share (2025) |

Key Growth Drivers |

|

ACT & New South Wales |

34.1% |

Largest industrial manufacturing concentration, large automotive component suppliers and medical device OEMs, large defense procurement base |

|

Queensland |

21.9% |

Mining equipment manufacturing, growing automotive parts supply, high construction activity, growing manufacturing diversification |

|

Victoria & Tasmania |

18.6% |

Automotive heritage sector transitioning to EV components, advanced manufacturing industry base, polymer processing facilities, high construction activity |

|

Western Australia |

14.3% |

Mining industry engineering plastic consumption, resources sector equipment manufacturing, oil & gas chemical processing applications |

|

Northern Territory & Southern Australia |

11.1% |

Adelaide's defense manufacturing hub, automotive industry legacy, rising mining and resources sector demand |

Competitive Landscape

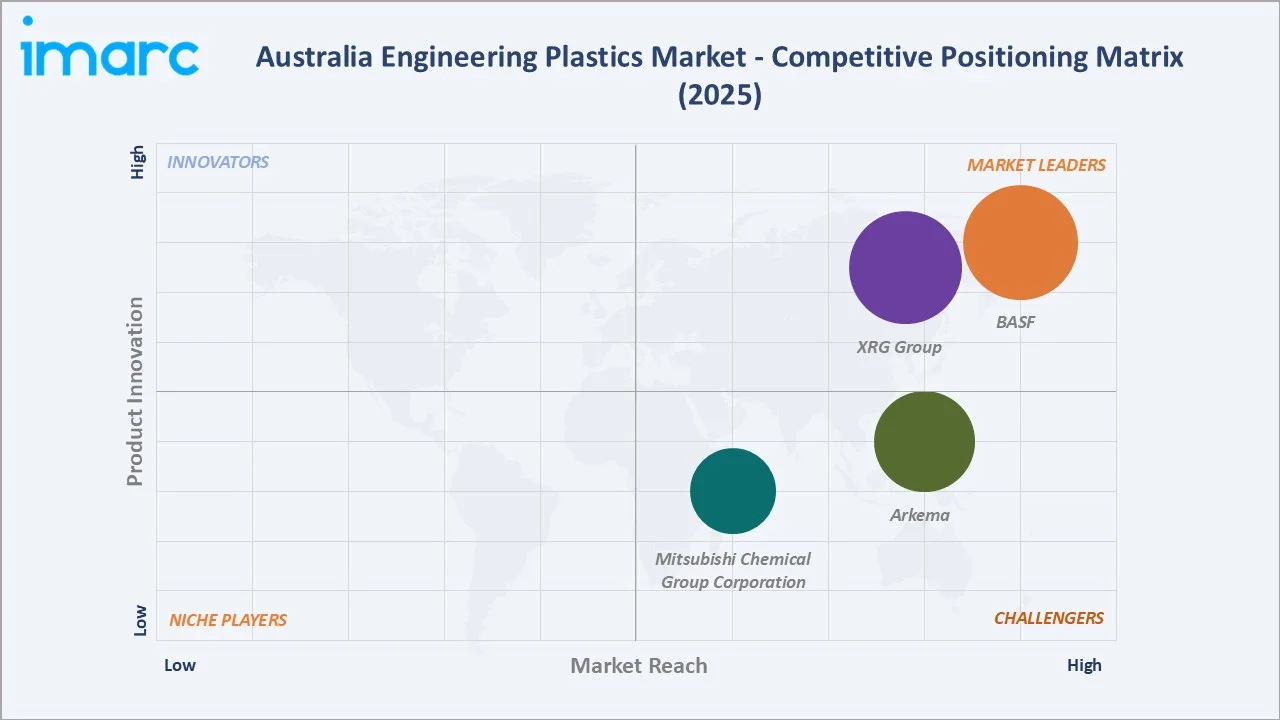

The Australia engineering plastics market is moderately consolidated at the resin supply level. BASF and XRG Group collectively hold an estimated 45–55% of the Australian market by revenue.

|

Company Name |

Brand |

Market Position |

Core Strength |

|

BASF |

Ultradur, Ultraform, Ultramid, Ultrason |

Market Leader |

Broadest engineering plastic grade portfolio with a strong focus on EV-ready and sustainability-oriented material innovations |

|

XRG Group |

Apec, Bayblend Makroblend, Makrolon, Makrofol, Desmopan TPU |

Market Leader |

Polycarbonate system leadership with strong positioning in data center, construction, and sustainable application segments |

|

Arkema |

Kynar, Pebax, Rilsan, Kepstan, Orgasol, Rilsamid |

Strong Challenger |

Bio-based polyamide expertise, fluoropolymer chemical resistance capabilities, and a high-performance specialty resin platform |

|

Mitsubishi Chemical Group Corporation |

RCH, Borotron, Acetron/Ertacetal, Altron, Ertalyte, Flextron, Nylatron/ Ertalon, TIVAR, Proteus |

Challenger |

Diversified engineering plastic compound portfolio for precision mechanical applications, with established supply capabilities for electronics and automotive OEMs |

The players are leveraging their global manufacturing scale, breadth of approved grades, and established relationships with major Australian distributors including Ixom and Dotmar Engineering Plastics.

Key Company Profiles

BASF

BASF is the global market leader in engineering plastics and the broadest-portfolio supplier to the Australian market. BASF's Materials division supplies Ultramid polyamides, Ultraform POM, Ultrason, and Ultradur PBT through its distribution partnership in Australia.

- Product Portfolio: Ultramid PA6 and PA66, Ultramid Advanced N, Ultraform N2320 POM (precision mechanical parts), Ultrason, and Ultradur PBT.

- Recent Developments: In September 2025, Porsche, BASF, and BEST completed a pilot project that chemically recycled mixed end-of-life vehicle waste into new high-performance plastic for steering wheels. The project supports circular automotive production by recovering plastics that cannot be mechanically recycled.

- Strategic Focus: EV powertrain and battery system grade development, bio-based and sustainable polymer portfolio expansion, digital customer specification tools, and co-engineering programs with Australian automotive Tier-1 suppliers.

XRG Group

XRG Group’s subsidiary Covestro AG is one of the world's leading polycarbonate producers and a major supplier of engineering thermoplastics to the Australian market.

- Product Portfolio: Makrolon PC, Apec high-heat PC, Desmopan TPU, Bayblend, and Makroblend.

- Strategic Focus: Circular economy PC leadership, data center construction polycarbonate market expansion, healthcare-grade PC product development, and bio-based PC precursor R&D program for post-2030 product launches.

Market Concentration Analysis

The Australia engineering plastics market is moderately consolidated at the supplier level, with BASF and XRG Group collectively holding approximately 45–55% of market revenue. The top suppliers account for approximately 65–70%, consistent with engineering plastic market concentration across most developed economies.

The Australian market's moderate consolidation creates a competitive dynamic where global tier-1 suppliers compete on technical grade differentiation and application engineering support, while regional distributors compete on price, lead time, and stock availability. The emergence of bio-based and circular economy grades is opening new competitive dimensions that reward innovation differentiation over commodity price competition.

Investment & Growth Opportunities

Fastest Growing Segments

High performance grades (~8.80% CAGR), fluoropolymers for semiconductor and clean energy applications, bio-based and recycled-content engineering plastics, and additive manufacturing feedstock grades represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental market of approximately USD 3.5 Billion by 2034.

Emerging Market Expansion

Australia's expanding defense manufacturing base, with submarine and surface vessel programs requiring specialty engineering plastics, and the growing medical device manufacturing sector both represent high-value emerging demand pockets. The Australia–UK AUKUS submarine program alone is expected to generate multi-decade demand for PEEK, PPS, and specialty fluoropolymers in hull fittings, electronic system housings, and propulsion component applications.

Venture and Institutional Investment Trends

- Bio-based polymer company Samsara Eco attracted AUD 54 Million in Series A funding in 2022 for its enzyme-based PET depolymerization technology, with potential to extend to engineering PBT and PA recycling, representing Australian venture investment in the circular engineering plastics value chain.

- Global engineering plastic compounders BASF and Covestro are investing in dedicated Asia-Pacific technical application centers that serve Australian customers with local application testing, which reduces the technical risk for Australian OEMs adopting new engineering plastic grades and accelerates the material specification process.

Future Market Outlook (2026-2034)

The Australia engineering plastics market is positioned for sustained growth through 2034, reaching USD 8.37 Billion from USD 3.93 Billion in 2025, representing total incremental value of USD 4.44 Billion at a 7.58% CAGR. Growth will be driven by Australia's EV supply chain development, data center construction, defense manufacturing investment, and the continuing transition from metal to polymer in industrial applications.

High performance grades will grow their market share from 62.5% in 2025 to an estimated 67–68% by 2034, reflecting the increasing proportion of demand from EV, aerospace, and medical device applications requiring materials beyond the performance envelope of standard commodity grades.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 75 industry participants in 2024–2025, including engineering plastic distributors, injection molding fabricators, OEM procurement managers, polymer compounders, and materials engineers across Australia's major industrial sectors. Expert input validated market sizing, grade adoption trends, and regional demand dynamics.

Secondary Research

Secondary research encompassed supplier annual reports, Australian Bureau of Statistics manufacturing data, Plastics Industry Association of Australia sector reports, ISO and ASTM polymer standards documentation, CSIRO advanced materials research publications, and trade publications including Australian Manufacturing Technology, Materials Australia, and Plastics News Asia.

Forecasting Models

Market size estimations used bottom-up forecasting incorporating Australian manufacturing output by sector, polymer consumption intensity per sector, average polymer price trajectories, grade mix evolution assumptions, and identified supply chain investment commitments. A base-case CAGR of 7.58% reflects validated consensus against distributor order forecasts and OEM procurement plans through 2027.

Australia Engineering Plastics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Polyamide, ABS, Thermoplastic Polyester, Polycarbonate, Polyacetal, Fluoropolymer, Others |

| Performance Parameters Covered | High Performance, Low Performance |

| Applications Covered | Packaging, Building and Construction, Electrical and Electronics, Automotive, Consumer Products, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | BASF, XRG Group, Arkema, Mitsubishi Chemical Group Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia engineering plastics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia engineering plastics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia engineering plastics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Engineering Plastics Market Report

The market reached USD 3.93 Billion in 2025 and is projected to reach USD 8.37 Billion by 2034 at a 7.58% CAGR.

Australia Capital Territory & New South Wales leads with a 34.1% share in 2025, driven by Sydney's manufacturing concentration and defense procurement in Canberra.

Polyamide leads with a 26.4% share in 2025, valued for its combination of mechanical strength, chemical resistance, and thermal stability across automotive, industrial, and consumer applications.

High performance grades dominate at 62.5% in 2025, reflecting Australia's industrial mix weighted toward EV, mining, defense, and medical applications requiring premium specifications.

BASF, XRG Group, Arkema, and Mitsubishi Chemical Group Corporation, are some of the major suppliers in the market.

Automotive EV lightweighting, electrical & electronics demand, construction investment, and sustainable/bio-based material adoption are the primary drivers.

Raw material price volatility, environmental regulations, competition from metals and composites, and supply chain lead time dependency are key challenges.

Fluoropolymers are fastest growing, driven by semiconductor, clean energy, and offshore applications requiring exceptional chemical and thermal resistance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)