Australia Fuel Cell Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Australia Fuel Cell Market Overview:

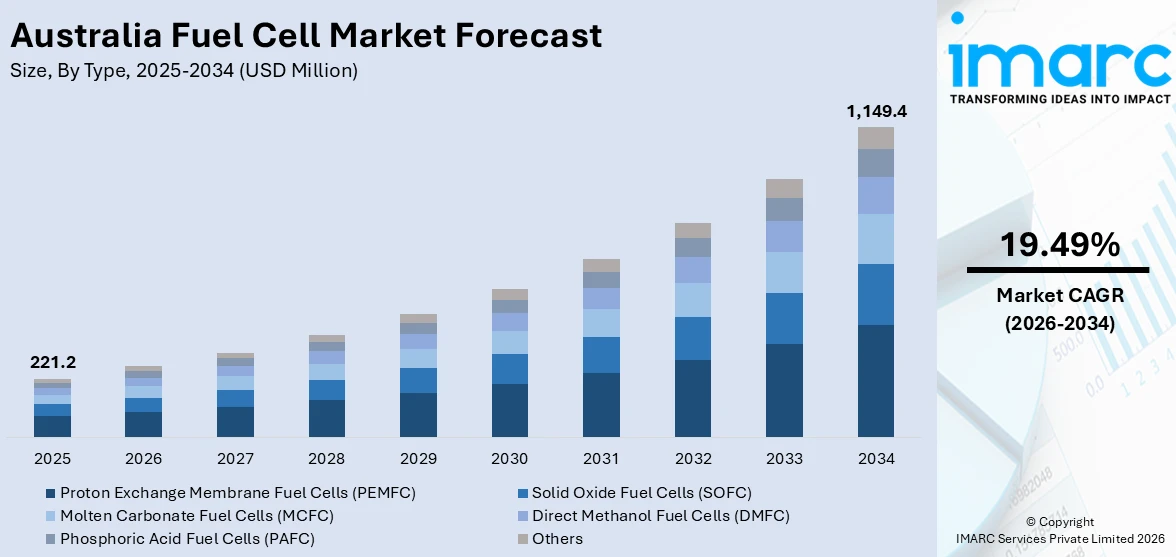

The Australia fuel cell market size reached USD 221.2 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,149.4 Million by 2034, exhibiting a growth rate (CAGR) of 19.49% during 2026-2034. The increasing demand for clean energy, government incentives promoting hydrogen technologies, growing investments in fuel cell research and development (R&D) activities, supportive infrastructure development, and growing adoption across transportation and stationary power sectors are some of the major factors facilitating market expansion.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 221.2 Million |

| Market Forecast in 2034 | USD 1,149.4 Million |

| Market Growth Rate 2026-2034 | 19.49% |

Australia Fuel Cell Market Trends:

Government Policy Support and National Hydrogen Strategy Implementation

The implementation of favorable initiatives is creating a positive Australia fuel cell market outlook. The government is allocating substantial funding through initiatives such as the Hydrogen Energy Supply Chain (HESC) project and the Australian Renewable Energy Agency (ARENA) to foster domestic fuel cell technology development. These policies not only promote infrastructure investment but also provide subsidies and incentives for private sector engagement in hydrogen and fuel cell research, production, and deployment. Federal and state-level programs, including those in New South Wales, Victoria, and Queensland, are advancing hydrogen mobility and industrial applications. The Clean Energy Finance Corporation (CEFC) also provides financial backing for clean hydrogen initiatives, indirectly boosting fuel cell system adoption. These policies align with Australia's broader emissions reduction commitments and decarbonization targets, helping to cultivate a favorable ecosystem for fuel cell technologies in power generation, heavy-duty transport, and off-grid applications across the country.

To get more information on this market Request Sample

Commercialization of Hydrogen Fuel Cell Vehicles and Refueling Infrastructure

Australia is witnessing early-stage commercialization of hydrogen-powered vehicles, particularly in fleet and heavy-duty transport segments. Automotive manufacturers are introducing fuel cell electric vehicles (FCEVs), primarily targeting government fleets and corporate entities. Besides this, trials in states such as Queensland and Victoria demonstrate a growing interest in deploying FCEVs as part of low-emission transport strategies. Furthermore, companies are investing in hydrogen refueling station development to support vehicle uptake, which is supporting Australia fuel cells market growth. According to an industry report, approximately there are 12 hydrogen refuelling stations either operational or under construction across Australia, highlighting the early stage of infrastructure development in the country’s fuel cell ecosystem. This limited availability poses a constraint to the widespread deployment of hydrogen fuel cell vehicles, particularly in the commercial and public transport sectors that require consistent and accessible refueling networks. However, the number of planned stations is gradually increasing through coordinated efforts by state governments, private sector collaborations, and federal funding schemes.

Growth in Stationary Fuel Cell Applications for Off-Grid and Backup Power

Stationary fuel cells are gaining traction in Australia, particularly for off-grid power supply, remote community electrification, and critical infrastructure backup. Fuel cells offer a compelling alternative to diesel generators by providing cleaner, quieter, and more efficient power generation. Companies are piloting proton exchange membrane (PEM) and solid oxide fuel cell (SOFC) systems for use in telecommunications, rural health centers, and isolated mining operations. Furthermore, concerns surrounding energy security and escalating electricity prices are reinforcing the demand for distributed generation technologies across Australia. According to an industry report, the average Australian household now incurs electricity expenses exceeding $ 300 per quarter, underscoring the growing financial burden on consumers. This trend is encouraging interest in alternative energy systems that offer both cost stability and energy independence. In this context, stationary fuel cell systems are being explored not only for remote and off-grid applications but also for residential and small commercial use, where consistent, low-emission power supply is a key requirement. These factors are significantly expanding the Australia fuel cell market share.

Australia Fuel Cell Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on type and application.

Type Insights:

- Proton Exchange Membrane Fuel Cells (PEMFC)

- Solid Oxide Fuel Cells (SOFC)

- Molten Carbonate Fuel Cells (MCFC)

- Direct Methanol Fuel Cells (DMFC)

- Phosphoric Acid Fuel Cells (PAFC)

- Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes proton exchange membrane fuel cells (PEMFC), solid oxide fuel cells (SOFC), molten carbonate fuel cells (MCFC), direct methanol fuel cells (DMFC), phosphoric acid fuel cells (PAFC), and others.

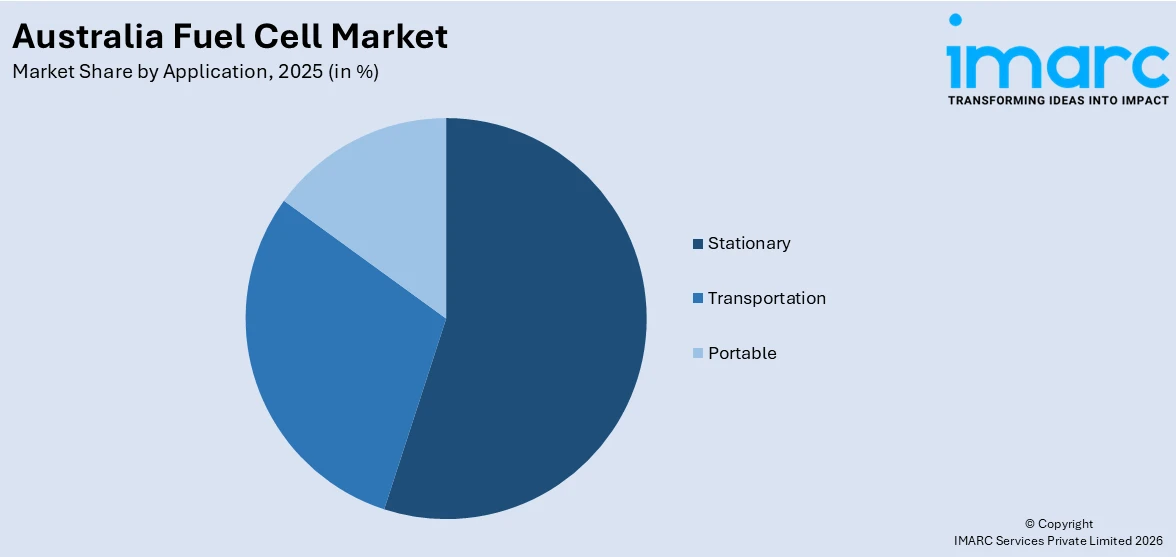

Application Insights:

Access the comprehensive market breakdown Request Sample

- Stationary

- Transportation

- Portable

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes stationary, transportation, and portable.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Fuel Cell Market News:

- On April 16, 2024, Toyota Australia announced the delivery of its first locally assembled EODev GEH2® hydrogen fuel cell stationary power generator to mining company Thiess. Manufactured at Toyota's Altona facility in Victoria, the 110kVA unit is part of a broader initiative to produce up to 100 generators over three years, targeting sectors such as mining, construction, and events. This collaboration underscores Toyota's commitment to advancing Australia's hydrogen economy and supporting industrial decarbonization efforts.

- On October 1, 2024, Deakin University inaugurated the Hycel Technology Hub at its Warrnambool campus in Southeast Victoria, marking Australia's first hydrogen fuel cell research and development (R&D) facility. The hub is designed to advance hydrogen technologies, focusing on fuel cells and associated infrastructure, thereby positioning Australia as a leader in the global hydrogen economy.

Australia Fuel Cell Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Proton Exchange Membrane Fuel Cells (PEMFC), Solid Oxide Fuel Cells (SOFC), Molten Carbonate Fuel Cells (MCFC), Direct Methanol Fuel Cells (DMFC), Phosphoric Acid Fuel Cells (PAFC), Others |

| Applications Covered | Stationary, Transportation, Portable |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia fuel cell market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia fuel cell market on the basis of type?

- What is the breakup of the Australia fuel cell market on the basis of application?

- What is the breakup of the Australia fuel cell market on the basis of region?

- What are the various stages in the value chain of the Australia fuel cell market?

- What are the key driving factors and challenges in the Australia fuel cell market?

- What is the structure of the Australia fuel cell market and who are the key players?

- What is the degree of competition in the Australia fuel cell market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia fuel cell market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia fuel cell market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia fuel cell industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)