Australia Green Tea Market Size, Share, Trends and Forecast by Type, Flavor, Distribution Channel, and Region, 2026-2034

Australia Green Tea Market Summary:

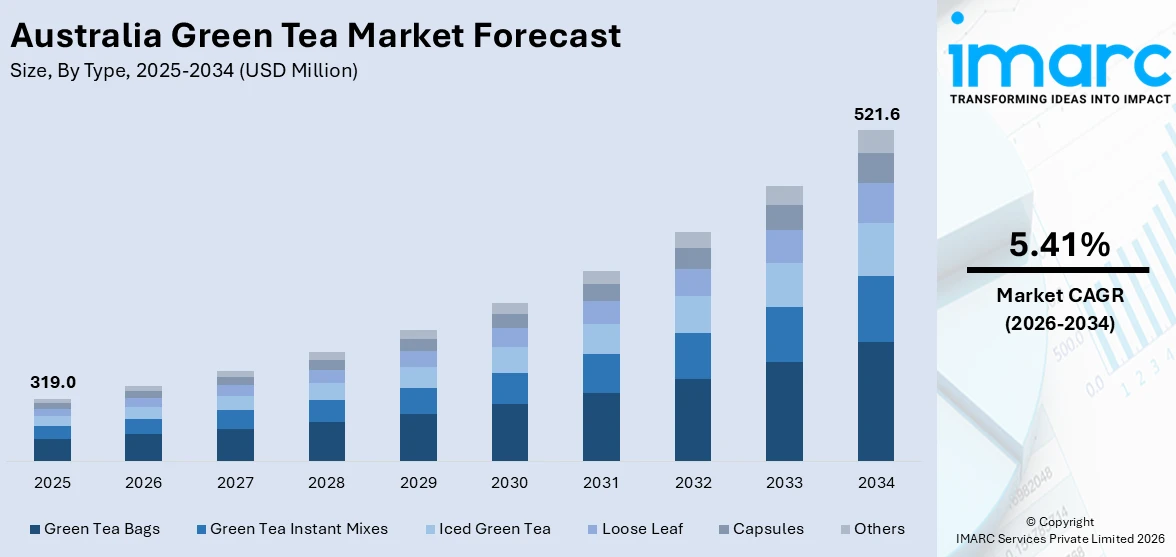

The Australia green tea market size was valued at USD 319.0 Million in 2025 and is projected to reach USD 521.6 Million by 2034, growing at a compound annual growth rate of 5.41% from 2026-2034.

Growing consumer awareness of the wellness advantages of green tea across a range of consumer groups, as well as a demand for natural and antioxidant-rich beverages, are driving the market's strong expansion in Australia. Trends toward premiumization, creative product designs, and the incorporation of beneficial ingredients are expanding the market. The market share of green tea in Australia is being further strengthened by increasing retail availability, bolstering e-commerce platforms, and incorporating multicultural dietary trends.

Key Takeaways and Insights:

- By Type: Green tea bags dominate the market with a share of 45.9% in 2025, owing to their affordability, brewing convenience, and widespread availability across supermarkets and online platforms. Growing consumer demand for quick, mess-free tea preparation is fueling the market expansion.

- By Flavor: Lemon leads the market with a share of 24.7% in 2025. This dominance is driven by the widespread preference for citrus-infused beverages that complement green tea’s natural taste, enhanced vitamin C perception, and strong retail positioning across flavored tea categories.

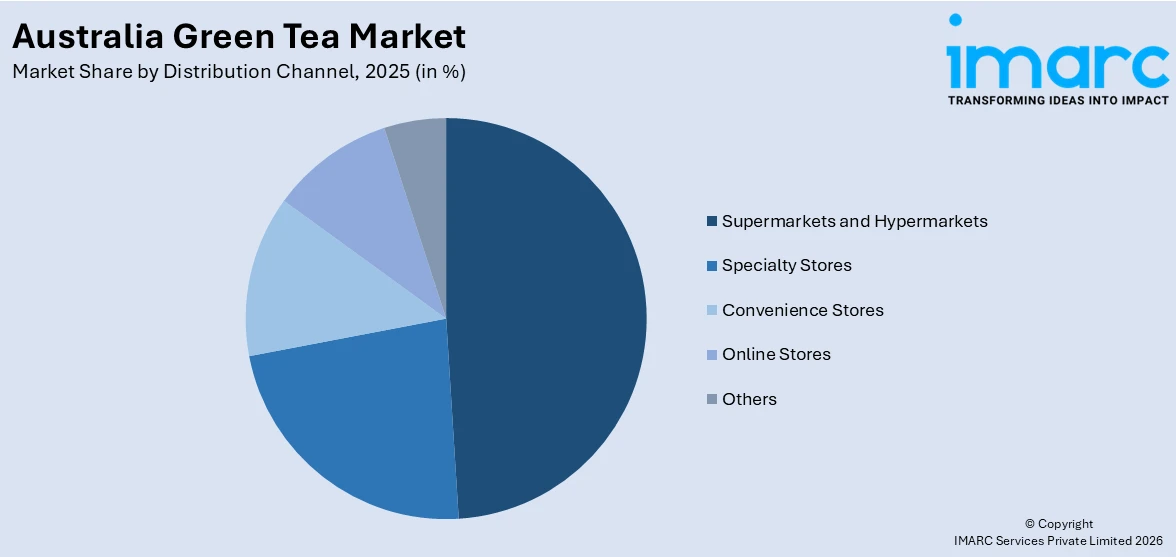

- By Distribution Channel: Supermarkets and hypermarkets represent the biggest segment with a market share of 49.2% in 2025, reflecting Australian consumers’ continued reliance on large-format retail outlets for routine grocery shopping, where extensive tea brand assortments and promotional offers drive purchase decisions.

- By Region: Australia Capital Territory & New South Wales is the largest region with 35.6% share in 2025, driven by the concentration of Australia’s most populous metropolitan area in Sydney, higher disposable incomes, and a culturally diverse population with strong affinity for health-oriented beverages.

- Key Players: In order to foster brand loyalty and meet the growing demand from health-conscious consumers, major players in the Australian green tea market diversify their product portfolios, launch high-end and functional varieties, bolster retail and digital distribution, and invest in innovative packaging and sustainable sourcing.

To get more information on this market Request Sample

As health-conscious consumers increasingly choose natural, antioxidant-rich beverages over fizzy and sugar-laden ones, the green tea market in Australia is expanding. Consumption of green tea is expanding across demographic groups as more people become aware of its advantages, which include improved cognitive function, cardiovascular health, and metabolism support. Australia's growing inclination for functional and wellness-focused beverages is a major factor propelling this expansion. The fundamental demand for healthier beverage options is being reinforced by consumers' growing emphasis on nutrition and ingredient transparency when making food and beverage purchases. The increased emphasis on health is sustaining demand for green tea in both conventional and novel forms, including matcha mixes, ready-to-drink varieties, and capsule-based products. The market landscape is becoming increasingly diversified due to tendencies toward premiumization, the introduction of sustainably packaged and ethically sourced goods, and the widespread use of flavored green teas. Growing multicultural influences, quick e-commerce acceptance, and strengthened retail infrastructure all support the growth of the Australian green tea market, setting it up for long-term growth in both urban and rural locations.

Australia Green Tea Market Trends:

Rising Demand for Matcha and Premium Green Tea Variants

Premium green tea kinds, especially those infused with matcha, are becoming more and more popular among Australian consumers due to their high antioxidant content and adaptability in both drinking and culinary applications. A larger consumer tendency for artisanal, single-origin, and functional tea experiences that command higher price points and promote brand differentiation is reflected in this premiumization trend. In response, producers are broadening their offerings with unique blends that merge conventional brewing techniques with contemporary wellness messaging, satisfying discriminating customers looking for superior quality and genuine tea experiences.

Expansion of Sustainable and Ethically Sourced Tea Products

Australian customers are actively looking for tea products that are supported by environmental certifications and ethical supply chain processes, making sustainability and ethical sourcing defining considerations in their purchasing decisions. Consumer trust in the expanding Australian green tea sector is being reinforced by clean-label positioning, transparent ingredient listings, and environmentally friendly packaging. In order to match their product offers with the growing environmental consciousness of Australian customers in both mainstream and premium market segments, manufacturers are giving priority to biodegradable and plastic-free packaging materials in addition to collaborations with certified sustainable tea plantations.

Growth of Digital Retail and Direct-to-Consumer Tea Channels

E-commerce is rapidly transforming how Australians discover and purchase green tea, with online platforms offering broader selections, subscription models, and personalized recommendations. As per Australia Post’s 2025 Annual eCommerce Report, Australian households spent AUD 69 Billion on online shopping, representing a 12% increase from the previous year, with grocery and beverage categories among the fastest-growing segments. Tea brands are leveraging digital storefronts, social media marketing, and direct-to-consumer models to reach health-focused consumers beyond traditional retail footprints.

Market Outlook 2026-2034:

The market for green tea in Australia is expected to increase steadily due to rising health consciousness, growing retail infrastructure, and ongoing product innovation in both established and new formats. Manufacturers are introducing a variety of product lines, including matcha mixes, flavored infusions, and ready-to-drink choices, as consumer preferences shift toward functional beverages that combine convenience and wellness advantages. The market generated a revenue of USD 319.0 Million in 2025 and is projected to reach a revenue of USD 521.6 Million by 2034, growing at a compound annual growth rate of 5.41% from 2026-2034. It is anticipated that new revenue streams would be generated by the influence of multicultural eating practices, premiumization trends that emphasize organic and sustainably sourced products, and growing e-commerce penetration. In addition to increasing demand for ceremonial-grade and specialty teas, strengthening alliances between tea companies and hospitality channels will further boost market momentum and solidify Australia's standing as one of the Asia-Pacific region's leading green tea markets.

Australia Green Tea Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Green Tea Bags |

45.9% |

|

Flavor |

Lemon |

24.7% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

49.2% |

|

Region |

Australia Capital Territory & New South Wales |

35.6% |

Type Insights:

- Green Tea Bags

- Green Tea Instant Mixes

- Iced Green Tea

- Loose Leaf

- Capsules

- Others

Green tea bags dominate with a market share of 45.9% of the total Australia green tea market in 2025.

Due to its unparalleled convenience, reliable brewing, and affordable prices that appeal to a wide range of consumers across all age groups, green tea bags continue to be the most popular format in Australia. They are perfect for consumption at home or at work because of their single-serve shape, which streamlines preparation and minimizes waste. The format's lengthy shelf life and mobility contribute to its popularity in retail channels. In order to meet the increased demand from consumers for convenient yet health-conscious beverage options across both mainstream and premium market segments, manufacturers are continuing to expand their tea bag offerings with a variety of green tea blends and wellness-focused formulations.

Green tea bags are widely accessible in supermarkets, convenience stores, and internet marketplaces, guaranteeing steady customer access regardless of location. Innovations in product design, such as tea bags made of compostable and biodegradable materials, are tackling environmental issues while preserving the convenience that makes the market unique. In order to bridge the gap between loose leaf quality and tea bag convenience, brands are also launching high-end pyramid-style bags that enable broader leaf expansion and deeper absorption. The segment's appeal to customers who care about the environment is being strengthened by the ongoing evolution in packaging design and material sources.

Flavor Insights:

- Lemon

- Aloe Vera

- Cinnamon

- Vanilla

- Wild Berry

- Jasmin

- Basil

- Others

Lemon leads the market with a share of 24.7% of the total Australia green tea market in 2025.

Due to its pleasant citrus flavor that balances the inherent vegetal notes of green tea and is thought to have immune-boosting and detoxifying properties, lemon-flavored green tea has the biggest market share among flavor categories. Australian consumers who are looking for tasty yet healthful beverages find that the combination of lemon and green tea is very appealing. Seasonal attractiveness and consumption occasions are expanded by its adaptability in both hot and iced recipes. Lemon green tea's standing as a top option in the flavored wellness beverage market is being reinforced by consumers' increasing preference for naturally flavored drinks over those with artificial sweeteners.

The popularity of lemon green tea is further supported by its prominent placement in major Australian retail chains, where it regularly holds premium shelf space in the flavored tea section. Both seasoned tea drinkers and novices moving away from sugary drinks will find the flavor profile appealing, making it an approachable entry point to the wider green tea market. By using cold-brew-compatible formats, vitamin C fortification, and organic lemon extracts, brands are advancing in this market. Lemon green tea's naturally low-sugar content fits in nicely with Australian consumers' changing dietary tastes, which place a higher value on beverage choices that are nutritionally transparent.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Others

Supermarkets and hypermarkets represent the largest segment, accounting for 49.2% of the total Australia green tea market in 2025.

In Australia, supermarkets and hypermarkets continue to be the main distribution channels for green tea because of their wide store networks, diverse product offerings, and aggressive price policies that encourage foot traffic from customers. Green tea items are given a large amount of shelf space by major retail chains, which sell both private-label and mainstream brands. Customers' propensity for buying green tea from these large-format retail establishments is reinforced by the ease of one-stop grocery shopping, frequent marketing campaigns, and loyalty benefits. The channel's market leadership is further reinforced by the ongoing development of grocery retail infrastructure in urban and regional areas.

Supermarkets and hypermarkets' intentional focus on health and wellness product aisles, where green tea is prominently displayed among other functional beverages and natural products, further reinforces their dominance. In an effort to appeal to the expanding market of technologically savvy customers, these merchants are progressively incorporating digital shopping features, such as click-and-collect services and online delivery platforms. Seasonal displays, in-store promotions, and sample occasions offer more touchpoints for customer interaction and brand exposure. Leading Australian grocery operators' growing omnichannel initiatives are enhancing the link between in-store experiences and online convenience, increasing the availability of green tea across the country.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales holds the largest share at 35.6% of the total Australia green tea market in 2025.

Because of the large population and high concentration of health-conscious consumers in the Greater Sydney metropolitan area, the Australia Capital Territory and New South Wales together constitute the largest regional market for green tea. Strong ethnic populations, especially sizable Asian-Australian communities with long-standing tea-drinking customs that inherently increase green tea consumption, are advantageous to the area. Market penetration is also supported by rising average disposable incomes, a well-established retail infrastructure with large supermarket chains, specialized tea merchants, and a flourishing café culture. Both mainstream and premium green tea uptake are facilitated by the region's high rate of urbanization and diverse consumer base.

Major tea manufacturers emphasize product introductions and marketing efforts inside the New South Wales market, bolstering the region's supremacy as Australia's main commercial and cultural powerhouse. Green tea and matcha-based products have been adopted as main menu items by Sydney's and Canberra's burgeoning café and hotel industries, further increasing consumption beyond conventional home-brewed formats. Sales of premium and specialized green tea are supported by the concentration of health food stores, organic merchants, and wellness-oriented businesses, which adds more distribution touchpoints. The area's closeness to domestic tea-growing regions offers logistical benefits that improve supply chain effectiveness and local market accessibility.

Market Dynamics:

Growth Drivers:

Why is the Australia Green Tea Market Growing?

Escalating Health Consciousness and Shift Toward Natural Beverages

Preventive health and wellness are becoming more and more important to Australians, which is causing a fundamental change in beverage consumption habits away from sugar-filled fizzy drinks and toward natural, useful substitutes. Green tea has become a popular option for health-conscious customers of all ages due to its high antioxidant content, metabolism-supporting catechins, and cardiovascular wellness qualities. This change is especially noticeable among Generation Z and millennials, who show a higher readiness to spend money on goods that support their lifestyle and health goals. The fundamental need for health-conscious beverages like green tea is being reinforced by consumers' growing emphasis on nutrition and ingredient transparency when making food and beverage purchases. Low-calorie, naturally based beverages are becoming more and more popular among consumers due to the rising prevalence of lifestyle-related health issues including diabetes and obesity. A more knowledgeable consumer base that actively seeks out items with clear health credentials is being created by government-led health programs encouraging lower sugar intake and more nutritional literacy. Green tea is well-positioned in this changing environment thanks to its well-established reputation as a clean-label, lightly processed beverage.

Product Innovation and Diversification Across Formats

Continuous product innovation is a critical driver of the Australia green tea market, as manufacturers introduce diverse formats, flavours, and functional enhancements to capture broader consumer segments. The market has expanded well beyond traditional tea bags to include matcha powders, ready-to-drink bottles, capsule-compatible formats, cold-brew variants, and green tea-infused food products. These innovations address evolving consumer preferences for convenience, portability, and experiential variety. Flavour innovation is also expanding the market by introducing botanical, fruit-infused, and spice-blended green tea varieties that appeal to consumers seeking novel taste experiences. The incorporation of functional ingredients such as vitamins, collagen, and adaptogens into green tea formulations is creating new product categories that bridge the gap between traditional tea and modern functional beverages. This diversification strengthens market resilience and attracts previously untapped consumer demographics, enabling brands to differentiate their offerings and establish stronger competitive positioning across both mainstream and premium market tiers.

Expanding Retail Infrastructure and E-Commerce Penetration

The expansion and modernization of retail channels across Australia is significantly enhancing green tea accessibility and driving market growth. Major supermarket chains continue to allocate dedicated shelf space for health and wellness beverages, positioning green tea as a core category within their product assortments. Simultaneously, the rapid growth of e-commerce is creating new pathways for consumer acquisition, with online platforms offering broader product selections, subscription models, and personalized recommendations that encourage repeat purchases. Grocery categories remain among the fastest-growing e-commerce segments, reflecting the increasing consumer preference for digital convenience in everyday purchasing. Specialty tea retailers, health food stores, and direct-to-consumer brands are also contributing to market expansion by offering curated green tea selections and premium products that complement mainstream retail offerings. The integration of omnichannel strategies, where retailers seamlessly connect physical stores with digital platforms through click-and-collect and same-day delivery services, is enhancing consumer convenience and broadening market reach across urban and regional areas.

Market Restraints:

What Challenges the Australia Green Tea Market is Facing?

Strong Competition from Established Coffee Culture

Australia’s deeply entrenched coffee culture presents a significant competitive barrier for the green tea market, as coffee remains the dominant hot beverage choice across both residential and out-of-home consumption settings. The country’s sophisticated café ecosystem and consumer loyalty to specialty coffee create strong substitution resistance, limiting green tea’s ability to capture a larger share of the overall hot beverages market despite growing health awareness among Australian consumers.

Price Sensitivity Toward Premium and Organic Variants

Premium and organic green tea products carry higher price points compared to conventional tea and coffee options, limiting their adoption among cost-conscious consumers. Australia’s ongoing cost-of-living pressures are amplifying price sensitivity, particularly among younger demographics and households with constrained budgets. This affordability gap between premium green tea offerings and mainstream beverage alternatives can slow the premiumization trajectory and restrict market penetration in price-sensitive consumer segments.

Limited Domestic Production and Import Dependency

Australia’s green tea market is predominantly reliant on imports from key producing countries, exposing the supply chain to currency fluctuations, international trade disruptions, and rising logistics costs. Domestic tea production remains geographically concentrated and limited in scale, constraining the availability of locally grown green tea varieties. This import dependency increases vulnerability to external supply chain shocks and can lead to price volatility that affects both manufacturers and consumers.

Competitive Landscape:

The Australia green tea market features a competitive landscape characterized by the presence of established multinational tea companies alongside growing domestic and specialty brands. Market participants are competing through product innovation, premiumization strategies, sustainability commitments, and expanded distribution networks. Companies are differentiating through functional ingredient integration, organic certifications, and ethically sourced supply chains to appeal to increasingly discerning consumers. Strategic investments in digital marketing, e-commerce channels, and partnerships with foodservice operators are reshaping competitive dynamics. Private-label offerings from major retailers are intensifying price competition, while niche brands leverage artisanal quality and unique flavor profiles to capture premium market segments, fostering a dynamic and evolving competitive environment.

Australia Green Tea Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Green Tea Bags, Green Tea Instant Mixes, Iced Green Tea, Loose Leaf, Capsules, Others |

| Flavours Covered | Lemon, Aloe Vera, Cinnamon, Vanilla, Wild Berry, Jasmin, Basil, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request |

Frequently Asked Questions About the Australia Green Tea Market Report

The Australia green tea market size was valued at USD 319.0 Million in 2025.

The Australia green tea market is expected to grow at a compound annual growth rate of 5.41% from 2026-2034 to reach USD 521.6 Million by 2034.

Green tea bags dominated the market with a share of 45.9%, driven by their unmatched convenience, consistent brewing quality, competitive pricing, portability, and widespread availability across supermarket, convenience, and online retail channels in Australia.

Key factors driving the Australia green tea market include rising health consciousness, growing demand for natural and antioxidant-rich beverages, product innovation across multiple formats, expanding retail and e-commerce infrastructure, premiumization trends, and increasing multicultural dietary influences.

Major challenges include strong competition from Australia’s established coffee culture, price sensitivity toward premium and organic variants amid cost-of-living pressures, limited domestic tea production capacity, import dependency exposing the supply chain to external disruptions, and the need for sustained consumer education efforts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)