Australia Grocery Retail Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region 2026-2034

Australia Grocery Retail Market Size, Share, Trends & Forecast (2026-2034)

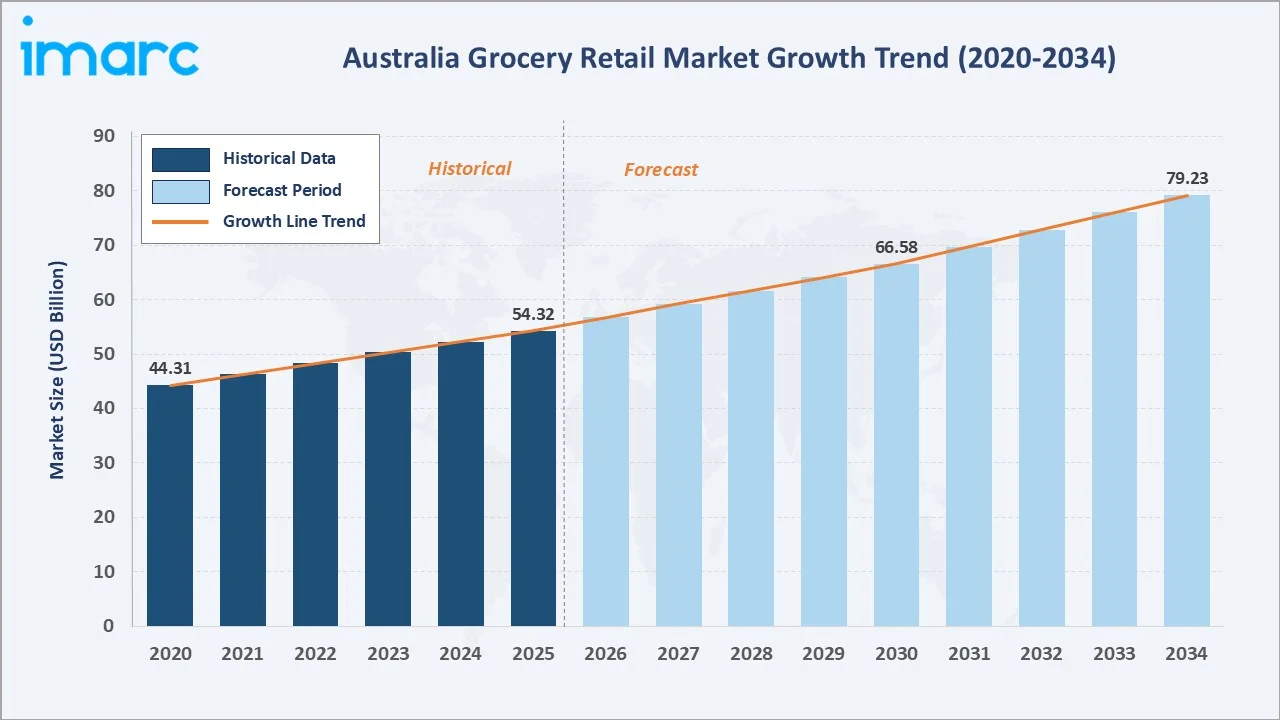

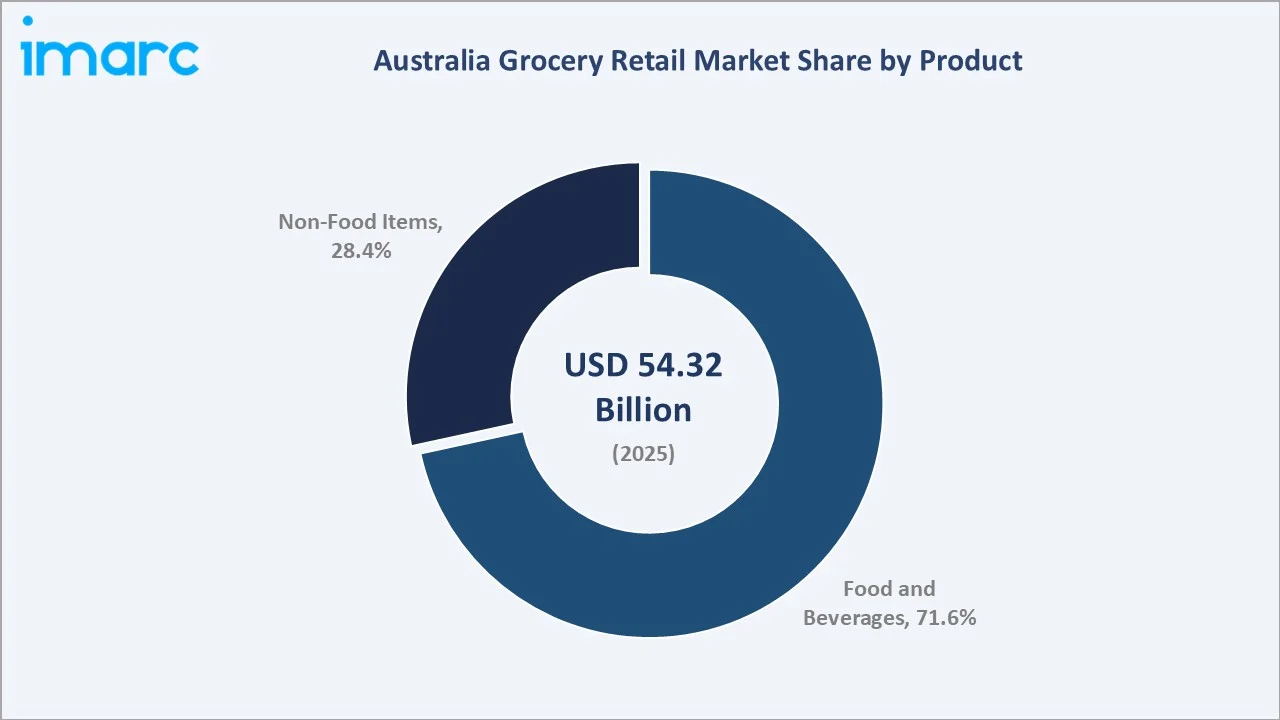

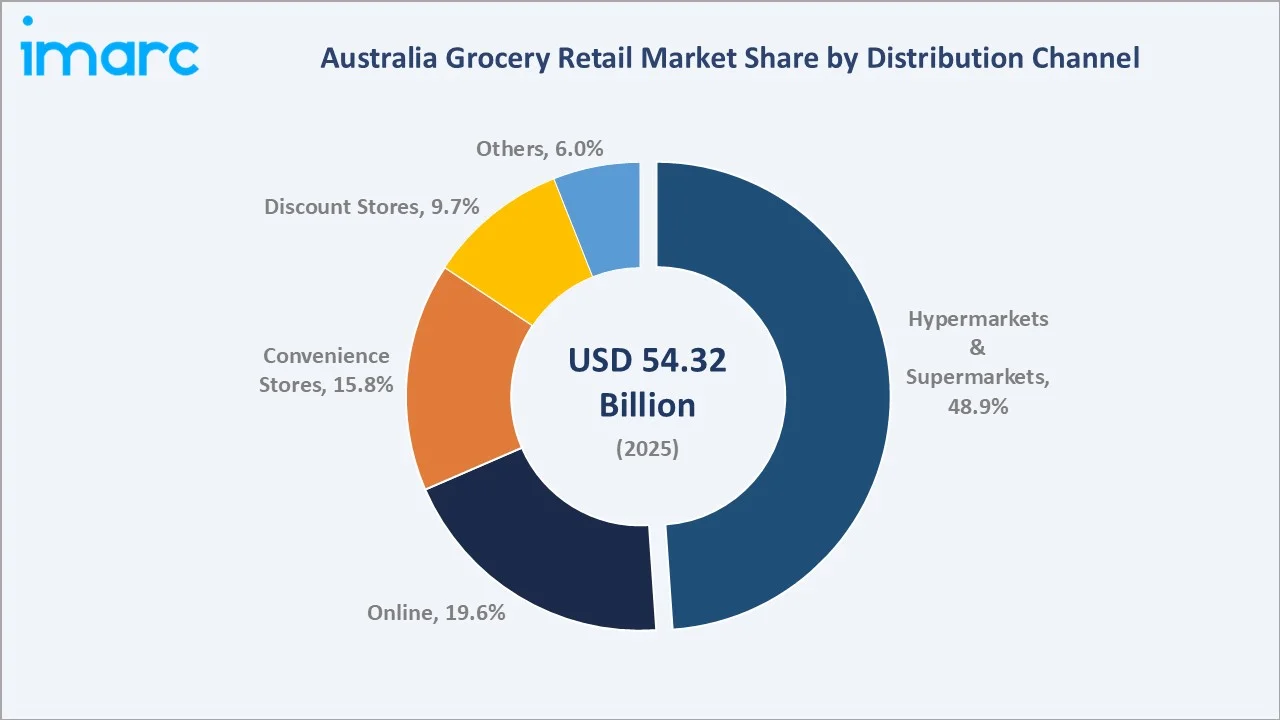

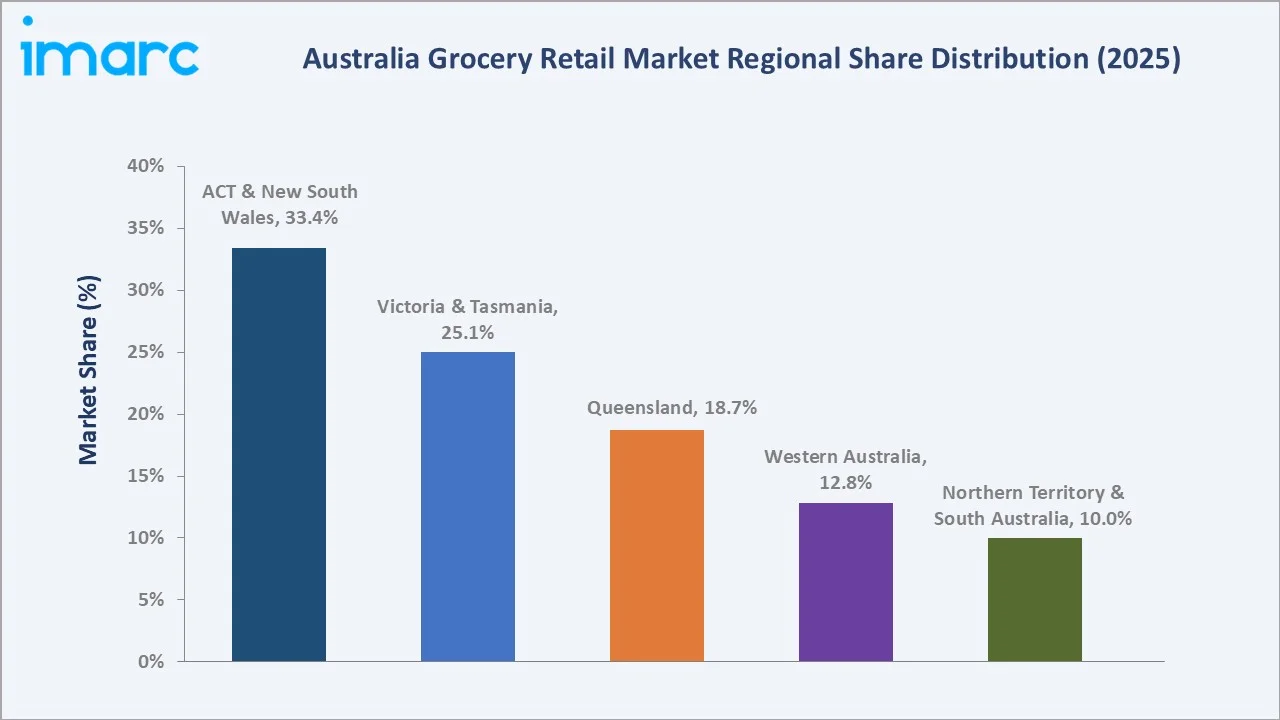

The Australia grocery retail market reached USD 54.32 Billion in 2025 and is projected to reach USD 79.23 Billion by 2034, growing at a CAGR of 4.16% during 2026-2034. Australia's population growth, with 27.7 million people by September 2025, driven by record net overseas migration, the Woolworths-Coles duopoly's private label expansion, the accelerating online grocery channel, and consumer premiumization in health and wellness food categories, collectively anchors the market growth. Food and beverages dominate at 71.6%. Hypermarkets and supermarkets lead the distribution channel at 48.9%. Australia Capital Territory & New South Wales commands 33.4% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 54.32 Billion |

|

Forecast Market Size (2034) |

USD 79.23 Billion |

|

CAGR (2026-2034) |

4.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product |

Food & Beverages (71.6%, 2025) |

|

Dominant Distribution Channel |

Hypermarkets & Supermarkets (48.9%, 2025) |

|

Leading Region |

ACT & NSW (33.4%, 2025) |

The market expanded from USD 44.31 Billion in 2020 to USD 54.32 Billion in 2025, anchored at USD 66.58 Billion in 2030, and forecast to reach USD 79.23 Billion by 2034. COVID-19 was the grocery market's most consequential demand catalyst. Lockdown-driven at-home cooking, pantry stockpiling, and avoidance of food service created incremental grocery revenue during 2020-2021 that permanently elevated Australia's grocery baseline demand.

To get more information on this market, Request Sample

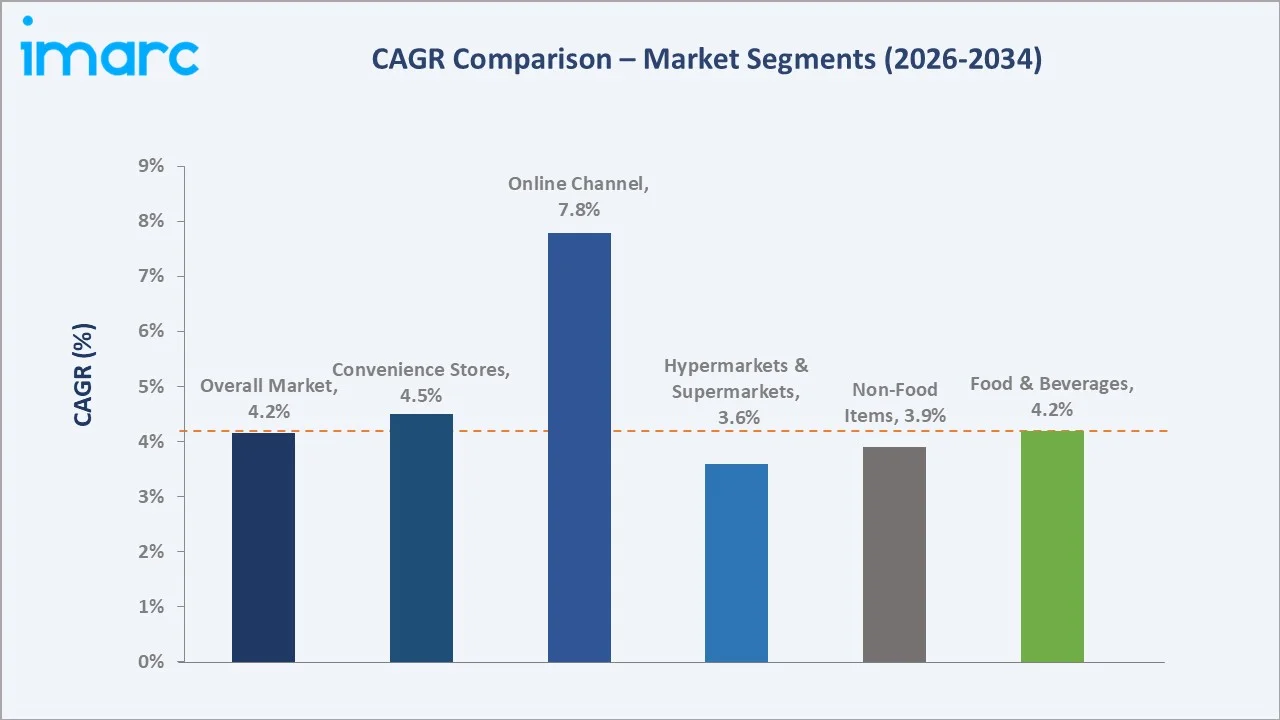

Online grows fastest at ~7.8% CAGR as Amazon Fresh grocery expansion in Sydney and Melbourne collectively builds the infrastructure enabling same-day delivery at competitive economics. Non-food Items at ~3.9% CAGR is sustained by convenience purchasing of household products and personal care at supermarkets, where non-food gross margins (25-35%) exceed food margins (20-28%), incentivizing retailers to expand the non-food category range.

Executive Summary

The Australia grocery retail market reached USD 54.32 Billion in 2025, representing one of the world's most concentrated grocery retail markets in a developed economy. Woolworths Group and Coles Group together command approximately 65-70% of Australia's organized grocery retail market, a duopoly concentration that is among the highest for any G20 economy's food retail sector. The market is projected to reach USD 79.23 Billion by 2034 at 4.16% CAGR.

Food and beverages at 71.6% encompass all consumable food categories from fresh produce, meat, and dairy through packaged and processed food, frozen meals, snacks, confectionery, and beverages. Hypermarkets and supermarkets at 48.9% reflect the established dominance of Australia's full-service supermarket format. ACT and NSW at 33.4% leads through Sydney's concentration of Australia's highest-income households and highest grocery expenditure density.

Key Market Insights

|

Insight |

Data |

|

Dominant Product |

Food & Beverages - 71.6% share (2025) |

|

Dominant Distribution Channel |

Hypermarkets & Supermarkets - 48.9% market share (2025) |

|

Leading Region |

ACT & NSW - 33.4% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Food and beverages at 71.6% anchored by Australia's full-service supermarket model where fresh food, packaged grocery, and beverages drive weekly shopping missions: Australia's grocery shopping behavior is concentrated in weekly full-shop occasions averaging AUD 170-200 per household visit at Woolworths and Coles, with fresh food (produce, meat, dairy) typically constituting 40-45% of basket value, the highest fresh food basket proportion of any English-speaking grocery market.

- Hypermarkets and supermarkets at 48.9% sustaining dominance through store network scale, private label margin, and loyalty ecosystem advantages: Despite online grocery growing at 7.8% CAGR, the physical supermarket format maintains near-50% channel share because Australian grocery shopping behavior prioritizes fresh food selection, impulse purchasing, and convenience of immediate access to all grocery categories in a single location.

- ACT and NSW at 33.4% through Sydney's population concentration, high household income, and grocery spending intensity: Sydney's 5.3 million metropolitan population as of 2024 represents 20%+ of Australia's total population but generates 25%+ of total national grocery spending, a per-capita grocery expenditure premium reflecting Sydney's above-average household incomes, multicultural population's elevated fresh and specialty food spend, and Sydney's higher cost-of-living creating higher absolute food prices even at equivalent volumes.

Australia Grocery Retail Market Overview

Australia's grocery retail market encompasses all organized and informal retail channels selling food, beverages, and household non-food consumables to Australian consumers. The market spans full-service supermarkets, discount grocery stores, convenience stores, warehouse clubs, specialty food retailers, and online grocery. Australia's 27 million+ population, universal smartphone ownership, and progressive online shopping culture create a grocery retail market where multichannel shopping is the norm for 60%+ of households.

The ecosystem integrates Australian agricultural producers, food processors and FMCG manufacturers, grocery wholesale and distribution, retail operators across formats and channels, digital technology providers, loyalty and data analytics platforms, and regulators.

Market Dynamics

To evaluate market opportunities, Request Sample

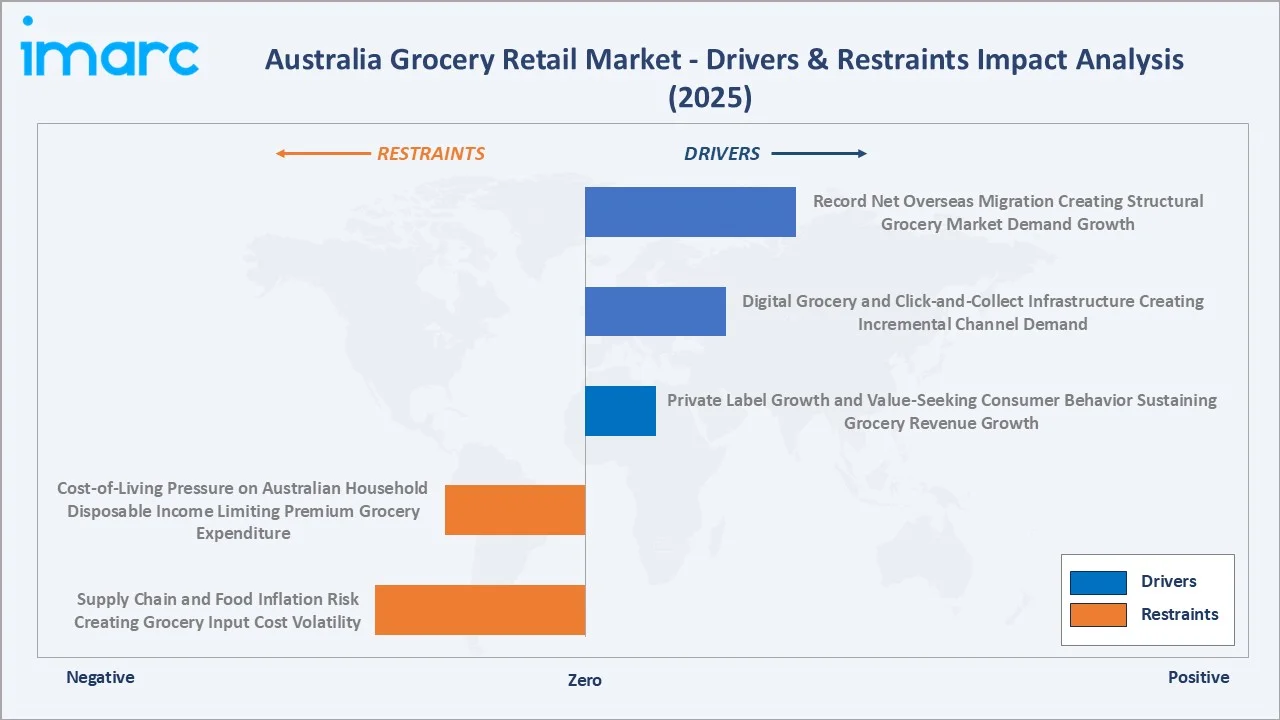

Market Drivers

- Record Net Overseas Migration Creating Structural Grocery Market Demand Growth: Australia experienced record net overseas migration of 446,000 in 2023-24, adding new grocery consumers over two years. This migration wave has been structurally beneficial for grocery retail in ways beyond simple population addition: migrant households typically maintain higher cooking frequency, higher fresh food spending, and specific category demand that mainstream supermarkets have responded to with expanded multicultural food sections.

- Digital Grocery and Click-and-Collect Infrastructure Creating Incremental Channel Demand: Australia's online grocery market is benefiting from both infrastructure investment and behavioral normalization following COVID-19's forced adoption.

- Private Label Growth and Value-Seeking Consumer Behavior Sustaining Grocery Revenue Growth: Australia's grocery private label market growth, driven by both retailer investment in private label quality and range, and consumer willingness to substitute from branded to store-owned product in response to food inflation.

Market Restraints

- Cost-of-Living Pressure on Australian Household Disposable Income Limiting Premium Grocery Expenditure: Australia's interest rate cycle created significant mortgage payment increases for 40%+ of Australian homeowners with variable rate mortgages, reducing household disposable income and driving trade-down behavior in grocery shopping. This trade-down manifested as increased private label substitution, reduced frequency of premium and specialty grocery purchases, and a measurable shift from full-service supermarket shopping toward ALDI's discount format.

- Supply Chain and Food Inflation Risk Creating Grocery Input Cost Volatility: Australia's grocery supply chain faces structural food inflation risks from climate change impacts, global commodity price volatility, and domestic agricultural labor shortages.

Market Opportunities

- Meal Kit and Ready-to-Cook Grocery Integration Creating New Revenue Streams: Australia's meal kit market and Woolworths and Coles' integration of recipe cards and pre-portioned ingredient kits within supermarket aisles represent a grocery format innovation that is increasing grocery basket values for participating households. Supermarket meal kit sections command premium pricing versus individual ingredient shopping while increasing fresh food attachment to grocery visits. Integrating meal planning apps with direct-to-cart product linking is creating personalized grocery experiences that increase basket size through algorithmic meal planning suggestions.

- Private Label Premium Tier Expansion Creating Brand-Level Profitability at Lower Marketing Cost: The success of Woolworths' Macro Wholefoods Market, Coles' Finest premium range, and ALDI's premium Specially Selected range demonstrates that Australian consumers will pay premium prices for private label products perceived as superior quality, natural, or ethical. This private label premiumization creates brand-equivalent revenues without the brand marketing investments that FMCG companies invest annually.

Market Challenges

- ACCC Grocery Market Inquiry and Political Price Regulation Risk: The ACCC's 2024 Supermarkets Inquiry created the most significant regulatory risk for Australia's grocery retail industry. The inquiry's recommendations represent a regulatory intervention that could structurally alter profitability for Australia's two dominant grocery retailers.

- Amazon Fresh Australia Potential Market Entry at Scale Creating Disruptive Online Grocery Competition: Amazon Fresh’s potential large-scale entry into Australia could intensify price competition and accelerate online grocery adoption. Its strong logistics, data-driven pricing, and delivery capabilities may pressure established retailers like Woolworths and Coles, disrupting margins and customer loyalty in the grocery retail market.

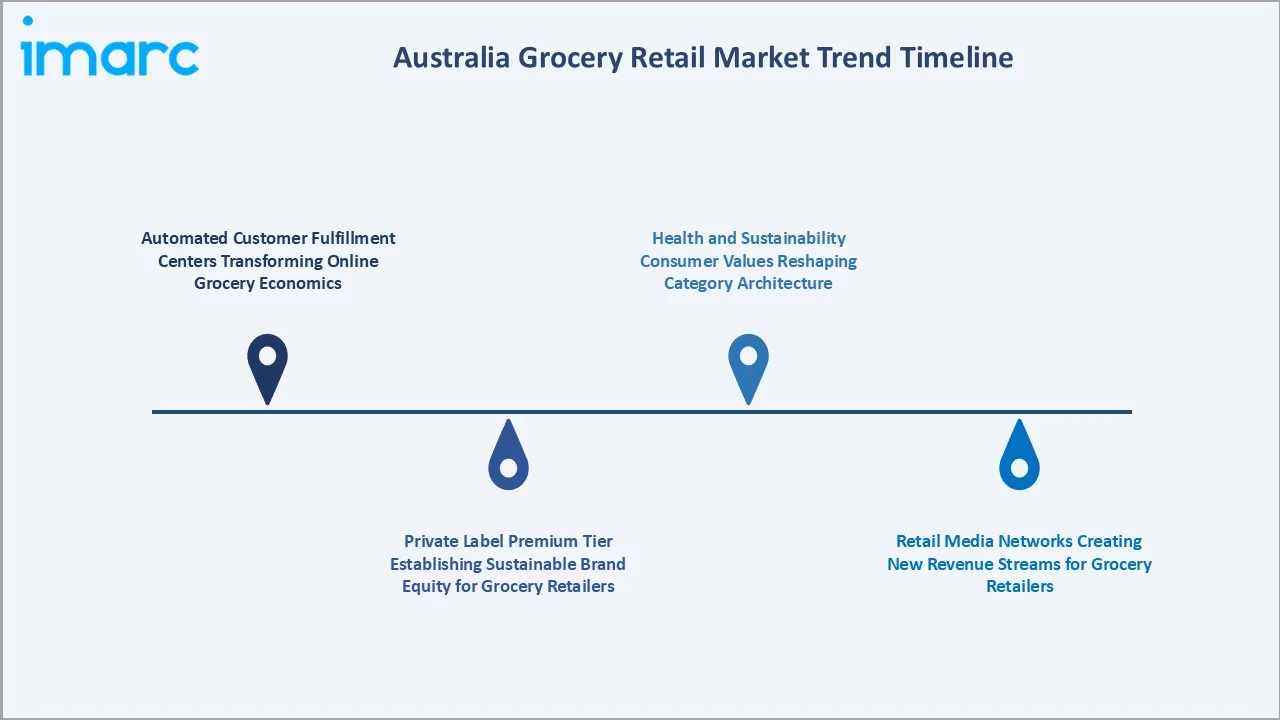

Emerging Market Trends

1. Automated Customer Fulfillment Centers Transforming Online Grocery Economics

Automated customer fulfillment centers are becoming an emerging trend as retailers seek to improve the economics of online grocery delivery. By using automation for picking, packing, and order processing, these centers reduce labour costs, improve accuracy, and speed up fulfillment. This enables supermarkets to handle growing online demand more profitably while offering faster and more reliable delivery services.

2. Private Label Premium Tier Establishing Sustainable Brand Equity for Grocery Retailers

Private label premium tiers are emerging as retailers move beyond basic value products to offer higher quality, differentiated ranges. These premium private labels help supermarkets build stronger brand loyalty, improve margins, and compete with national brands. By focusing on quality, sustainability, and unique product positioning, retailers can create long-term brand equity among value-conscious yet quality-seeking consumers.

3. Retail Media Networks Creating New Revenue Streams for Grocery Retailers

Retail media networks are emerging as supermarkets use their customer data, digital platforms, and in-store assets to sell targeted advertising to brands. This creates a high-margin revenue stream beyond traditional grocery sales. It also helps suppliers reach shoppers more effectively at the point of purchase, strengthening retailer-brand partnerships.

4. Health and Sustainability Consumer Values Reshaping Category Architecture

Health and sustainability values are reshaping category architecture as consumers increasingly prefer organic, plant-based, low-sugar, locally sourced, and eco-friendly products. Retailers are reorganizing shelves, private labels, and online categories around wellness and responsible consumption. This trend helps supermarkets capture premium demand while aligning with evolving shopper expectations.

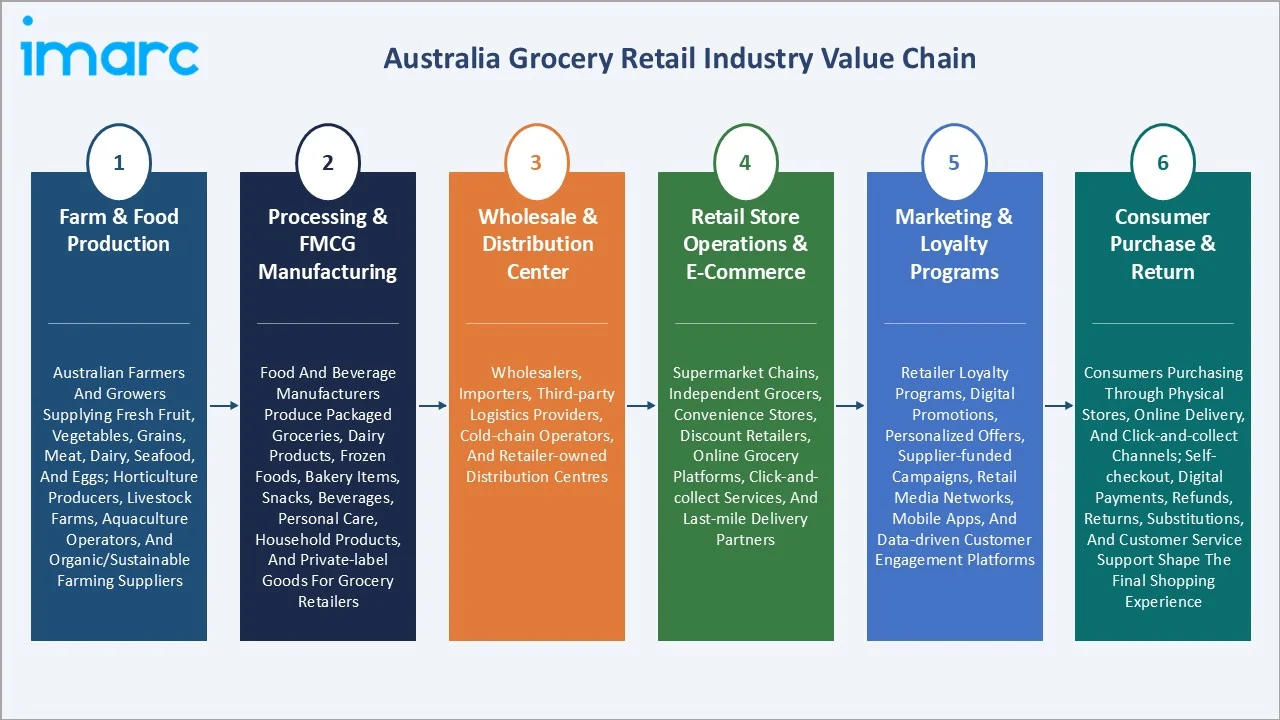

Industry Value Chain Analysis

Australia's grocery retail value chain integrates farm and food production, food processing and FMCG manufacturing, wholesale and distribution center logistics, retail store and e-commerce operations, marketing and loyalty programs, and consumer purchase and return. Full-service supermarket gross margins average 24-28%, convenience stores 28-35%, discount stores 18-22%, and online grocery 20-26%.

|

Stage |

Key Participants |

|

Farm & Food Production |

Australian farmers and growers supplying fresh fruit, vegetables, grains, meat, dairy, seafood, and eggs; horticulture producers, livestock farms, aquaculture operators, and organic/sustainable farming suppliers. |

|

Processing & FMCG Manufacturing |

Food and beverage manufacturers produce packaged groceries, dairy products, frozen foods, bakery items, snacks, beverages, personal care, household products, and private-label goods for grocery retailers. |

|

Wholesale & Distribution Center |

Wholesalers, importers, third-party logistics providers, cold-chain operators, and retailer-owned distribution centres. |

|

Retail Store Operations & E-Commerce |

Supermarket chains, independent grocers, convenience stores, discount retailers, online grocery platforms, click-and-collect services, and last-mile delivery partners. |

|

Marketing & Loyalty Programs |

Retailer loyalty programs, digital promotions, personalized offers, supplier-funded campaigns, retail media networks, mobile apps, and data-driven customer engagement platforms. |

|

Consumer Purchase & Return |

Consumers purchasing through physical stores, online delivery, and click-and-collect channels; self-checkout, digital payments, refunds, returns, substitutions, and customer service support shape the final shopping experience. |

The marketing and loyalty program tier is Australia's grocery value chain's most commercially innovative element. The first-party data advantage from loyalty programs is estimated to be worth AUD 500 Million-1 Billion in annual retail media and product development value for Woolworths and Coles combined, representing a competitive moat that ALDI cannot easily replicate.

Technology Landscape in the Australia Grocery Retail Industry

Automated Fulfillment and Robotics

In June 2025, Woolworths and KNAPP achieved a major milestone in their long-standing partnership with the launch of Woolworths’ first fully automated Central Fulfillment Centre (CFC) in Western Sydney. These automated systems are the physical infrastructure enabling Australia's online grocery market's economics to improve sufficiently for profitable delivery at competitive consumer prices, a prerequisite for sustained online grocery market share growth beyond the 20% penetration ceiling that expensive manual fulfillment would otherwise impose.

Loyalty Data Analytics and Personalization

Loyalty data analytics and personalization enable retailers to use shopper data for targeted promotions, product recommendations, and customized offers. These tools help supermarkets improve customer retention, basket size, and campaign effectiveness. As competition increases, AI-driven loyalty platforms and digital apps are becoming central to building stronger customer relationships.

Self-Checkout and Frictionless Retail Technology

Self-checkout and frictionless retail technology are reducing checkout time and improving store efficiency. Tools such as scan-and-go apps, smart carts, and digital payments help retailers lower labour pressure while improving customer convenience. These technologies also generate shopper data that supports better store planning, inventory management, and personalized engagement.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Food and Beverages |

71.6% |

2025 |

|

Distribution Channel |

Hypermarkets and Supermarkets |

48.9% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

33.4% |

2025 |

By Product

Food and beverages lead at 71.6% market share (2025). Australia's food and beverages grocery segment spans fresh food, dairy products, packaged and ambient grocery, frozen food, confectionery and snacks, and beverages.

To access detailed market analysis, Request Sample

Non-food items at 28.4% encompasses household cleaning, personal care, baby and infant, pet food, health supplements, and stationery and paper categories. Non-food's higher gross margin profile makes it disproportionately important to grocery retailers' overall profitability.

By Distribution Channel

Hypermarkets and supermarkets lead at 48.9% market share (2025). Australia's full-service supermarket format remains the dominant grocery channel through its combination of convenience, range, fresh food quality, and value.

Online at 19.6% grows fastest at ~7.8% CAGR, the channel's growth is accelerating relative to the pre-pandemic trajectory as CFC infrastructure investment reduces delivery costs and improves product availability. Convenience stores at 15.8% serves impulse and top-up grocery purchases. Discount stores at 9.7%. Others at 6.0% encompasses farmers' markets, specialty food retailers, petrol station mini-marts, and pharmacy-based grocery sections.

Regional Market Insights

|

Region |

Share (2025) |

Key Grocery Retail Growth Drivers & Characteristics |

|

ACT & New South Wales |

33.4% |

Supported by high population density, strong urban grocery demand, and mature supermarket infrastructure. |

|

Victoria & Tasmania |

25.1% |

Benefit from Melbourne’s large consumer base, diverse food culture, and strong demand for fresh, premium, multicultural, and health-focused grocery products. |

|

Queensland |

18.7% |

Supported by population growth, expanding suburban communities, and increasing demand across both metro and regional areas. |

|

Western Australia |

12.8% |

Shaped by concentrated urban demand, dispersed regional communities, and the need for efficient supply-chain and cold-chain infrastructure. |

|

Northern Territory & South Australia |

10.0% |

These markets are smaller but important, with demand driven by established urban centres, regional communities, and remote-area grocery access needs. |

ACT and NSW's 33.4% market leadership reflects Sydney's extraordinary grocery market intensity. Woolworths' top-10 highest-revenue stores nationally are concentrated in Sydney metropolitan locations. This innovation concentration creates a self-reinforcing cycle where format improvements developed for Sydney's demanding consumers progressively improve grocery value propositions for Australian consumers nationally.

Victoria and Tasmania's 25.1% reflect Melbourne's unique grocery competitive intensity, including Australia's highest concentration of premium and specialty grocery retailers. Queensland's 18.7% is growing fastest by CAGR, driven by population migration. Western Australia's 12.8% features Australia's most isolated major grocery market by geography. NT and SA's combined 10.0% includes South Australia's distinctively competitive independent grocery sector and the Northern Territory's unique remote community grocery supply challenges.

Competitive Landscape

Australia's grocery retail market is one of the world's most concentrated, with Woolworths Group and Coles Group together commanding approximately 65-70% of organized grocery retail revenues. This duopoly concentration has been sustained by Australia's geographic distances, the two major retailers' complementary network density, and their integrated loyalty, supply chain, and private label advantages.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

Woolworths Group Limited |

Woolworths Supermarkets, Milkrun, healthylife |

Market Leader |

Woolworths Group is one of Australia’s largest retailers with a wide-reaching store network and eCommerce business, anchored in the strength of its cornerstone Food business. |

|

Coles Group |

Coles Supermarkets, Coles Online |

Market Leader |

Coles is one of Australia’s leading retailers, with an extensive footprint nationally. |

|

Metcash Limited |

IGA, Foodland |

Strong Challenger |

Metcash has the widest retail distribution network in Australia, servicing Independent Retailers in all corners of Australia. |

|

AUR |

FoodWorks, FoodStore |

Established Player |

The AUR Board is made up of independent retailers and highly qualified retail industry experts. |

The ACCC's 2024 Supermarkets Inquiry has created a competitive dynamic where both major retailers are under regulatory and political pressure to moderate price increases, invest in private label affordability, and improve promotional transparency.

Key Company Profiles

Woolworths Group Limited

Woolworths Group is one of Australia’s largest retailers with a wide-reaching store network and eCommerce business, anchored in the strength of its cornerstone Food business.

- Brands: Woolworths Supermarkets, Milkrun, and healthylife, among others.

- Recent Developments: In March 2026, Woolworths switched on a $20 million high-tech "eStore" in St Mary's, doubling online delivery capacity for thousands of families across Western Sydney.

- Strategic Focus: Strengthening value, fresh food differentiation, digital/online capabilities, loyalty-led personalization, and supply-chain efficiency in Australia’s grocery retail market.

Coles Group

Coles Group is Australia's second-largest grocery retailer, operating Coles supermarkets and Coles Online grocery delivery.

- Brands: Coles supermarkets and Coles Online.

- Recent Developments: In October 2025, Coles became the first major Australian retailer to implement ChatGPT Enterprise at scale through its partnership with OpenAI, enabling employees to leverage advanced AI tools while exploring innovative ways to improve customer experience.

- Strategic Focus: Focuses on value-driven pricing, digital transformation, supply-chain automation, private-label expansion, and personalized customer engagement to strengthen its position in Australia’s grocery retail market.

Market Concentration Analysis

Australia's grocery retail market is one of the world's most concentrated among developed economies. Woolworths Group (37-38% market share) and Coles Group (29-31% market share) together command approximately 66-69% of Australia's organized grocery retail, a combined share that exceeds the UK, USA, and most comparable Western grocery markets. This concentration has been sustained by Australia's geographic isolation, the two majors' scale advantages in supply chain, private label, loyalty data, and retail media, and Australia's historically limited regulatory intervention in grocery market structure.

The ACCC's 2024 Supermarkets Inquiry marks a potential structural inflection point, the first serious regulatory consideration of whether Woolworths and Coles' market power should be structurally addressed rather than merely monitored. While structural remedies are unlikely in the short term, the inquiry's recommendations create a more adversarial regulatory environment for margin expansion by the two majors, effectively acting as a regulatory constraint on the duopoly's pricing power.

Investment & Growth Opportunities

Fastest Growing Segments

Online grocery channel (~7.8% CAGR), premium private label (18-22% CAGR within private label), plant-based food subcategory (25%+ CAGR), retail media (25-35% CAGR), health supplement grocery integration (8-12% CAGR), and convenience meal kit grocery (15-18% CAGR) represent Australia's highest-growth grocery retail investment vectors.

Emerging Market Opportunities

Australia's multicultural premium grocery segment is among the market's most underserved opportunities. The Asian grocery specialty store segment serves an addressable market of Asian-background Australian households spending AUD 3,500-5,000 annually on specialty Asian groceries that mainstream Woolworths and Coles only partially address. Organized grocery retailers developing credible Asian specialty grocery ranges can capture premium category share in Australia's fastest-growing grocery demographic segment.

Investment Themes

- Online grocery infrastructure investment for competitive fulfillment economics: Retailers investing in automated fulfillment infrastructure by 2027-2028 will achieve same-day delivery economics competitive with in-store shopping prices.

- Private label premiumization for health and sustainability positioning: The premium private label tier represents the highest-margin, fastest-growing segment within grocery private label. Retailers and private label developers investing in premium private label quality, transparent sourcing, and sustainable packaging can build brand equity commanding 20-35% price premiums versus standard private label at gross margins 12-18 percentage points above branded equivalents in the same category.

Future Market Outlook (2026-2034)

The Australia grocery retail market is projected to grow from USD 54.32 Billion in 2025 to USD 79.23 Billion by 2034, delivering a 4.16% CAGR and 46% market expansion over the forecast period. The market's anchor value of USD 66.58 Billion in 2030 represents an Australian grocery industry where online grocery has crossed 25% of total channel share as Woolworths' and Coles' automated CFCs deliver competitive same-day delivery economics, private label penetration in supermarkets, and Australia's population, creating an enlarged consumer base from sustained migration inflows.

Three structural forces define Australia's grocery retail market growth through 2034 with high confidence: Australia's population growth through sustained net overseas migration inflows, adding 4-5 million new grocery consumers who collectively contribute AUD 18-22 Billion in cumulative incremental grocery spend; food and grocery inflation normalizing to 2.5-3.5% annually after the 2022-2024 spike, sustaining revenue growth above volume growth through pricing even as volume growth is supported by population expansion; and the online grocery channel's structural shift from supplement to core shopping channel as automated fulfillment economics and behavioral normalization compound to push online penetration toward 28-30% of total grocery by 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Grocery Category Directors and Strategy executives; Metcash independent retail support team executives; IGA store owners and managers in NSW, VIC, and QLD; Harris Farm Markets and Drakes Supermarkets senior management; ACCC Grocery Market Inquiry consumer research data access; Roy Morgan Research grocery panel data; Woolworths' and Coles' team executives discussing online grocery technology strategy; and consumer focus groups with grocery shoppers across 5 Australian state markets.

Secondary Research

Secondary research encompassed Woolworths Group and Coles Group annual reports (FY2022-FY2025); Metcash annual reports (FY2022-FY2025); ACCC Supermarkets Inquiry 2024 interim and final reports; Australian Bureau of Statistics (ABS) Household Expenditure Survey and Retail Trade Survey monthly data; IBISWorld Australian Supermarkets and Grocery Stores industry report 2025; Roy Morgan Consumer Grocery Preference Surveys 2025; IRI Australia scan data grocery category reports; Euromonitor International Australia packaged food and grocery retail data 2025; private label market analysis reports; and individual state retail trade association reports. Over 70 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up product and distribution channel models calibrated against ABS Retail Trade monthly series (grocery-relevant categories), Woolworths and Coles combined publicly disclosed food and everyday needs revenues, and Metcash disclosed food wholesale revenues. Key inputs include ABS population projection scenarios, Roy Morgan weekly grocery spend panel data by channel and format, food CPI forecasts from RBA and independent economic research, and online grocery penetration growth modeling based on automated CFC capacity expansion timelines from Woolworths' and Coles' capital expenditure guidance.

Australia Grocery Retail Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Distribution Channels Covered | Hypermarkets and Supermarkets, Convenience Stores, Discount Stores, Online, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Woolworths Group Limited, Coles Group, Metcash Limited, AUR, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia grocery retail market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia grocery retail market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the Australia grocery retail industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Grocery Retail Market Report

The Australia grocery retail market reached USD 54.32 Billion in 2025, driven by Australia's 27 million+ population generating high annual household grocery spend, the Woolworths-Coles duopoly's 65-70% organized market share, record migration-driven population growth adding new grocery consumers, and post-COVID normalization sustaining elevated at-home food consumption versus pre-pandemic food service participation rates.

The market grows at 4.16% CAGR during 2026-2034, reaching USD 79.23 Billion by 2034, driven by sustained net overseas migration expanding the consumer base, online grocery infrastructure investment enabling competitive delivery economics, food inflation normalization contributing pricing-driven revenue growth, private label premiumization expanding average basket values, and Australia's population.

Food and beverages lead at 71.6% through the centrality of fresh food, packaged grocery, and beverages to Australia's weekly household shopping occasion.

Hypermarkets and supermarkets lead at 48.9% through Woolworths' and Coles' store network.

ACT and NSW lead at 33.4%, anchored by Sydney's 5.3 million metropolitan population and Australia's highest average household grocery expenditure. NSW is also Australia's primary grocery retail format innovation testbed, where new concepts are piloted before national rollout.

Leading companies include Woolworths Group Limited, Coles Group, Metcash Limited, and AUR, among others.

The market is projected to reach approximately USD 66.58 Billion by 2030, with online grocery crossing 25% channel share as automated CFCs achieve delivery price parity with in-store shopping, private label penetration crossing 32% of supermarket revenues, and Australia's population growth.

Online grocery grew from 3% of grocery sales pre-COVID to approximately 20% by 2025, driven by Woolworths, Coles Online, and Amazon Fresh. Online grocery's structural advantage is compelling enough that online penetration will continue growing toward 28-30% by 2034 as delivery economics improve from automated fulfillment investment.

Three priority opportunities: online grocery infrastructure investment in automated fulfillment enabling price-competitive same-day delivery; premium private label development in health, sustainability, and provenance categories commanding 20-35% price premiums with 12-18 percentage point gross margin advantages versus branded equivalents; and convenience format development in Australia's densifying urban apartment markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)