Australia Hemodialysis Market Size, Share, Trends and Forecast by Segment, Modality, End-User, and Region, 2026-2034

Australia Hemodialysis Market Overview:

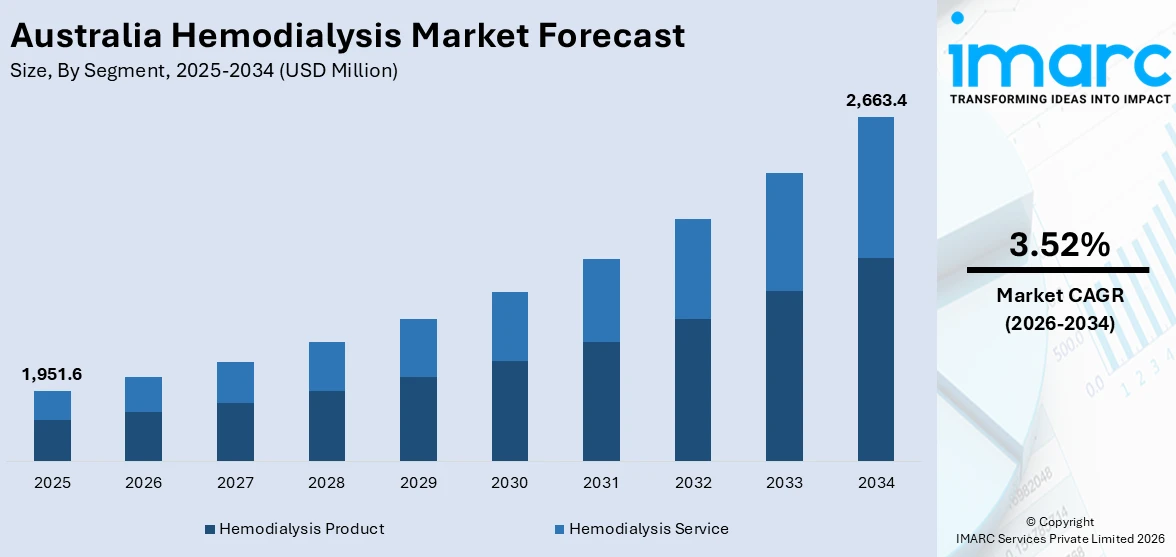

The Australia hemodialysis market size reached USD 1,951.6 Million in 2025. Looking forward, the market is expected to reach USD 2,663.4 Million by 2034, exhibiting a growth rate (CAGR) of 3.52% during 2026-2034. The rising chronic kidney disease and end‑stage renal disease (ESRD) prevalence linked to aging, diabetes and hypertension, a rapid shift toward technologically advanced, home‑based dialysis systems, favorable reimbursement policies, and growing number of dialysis clinics are the key factors propelling the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1,951.6 Million |

| Market Forecast in 2034 | USD 2,663.4 Million |

| Market Growth Rate 2026-2034 | 3.52% |

Key Trends of Australia Hemodialysis Market:

Surging Prevalence of CKD and ESRD Driven by Diabetes, Hypertension and Aging

Australia is experiencing a marked increase in chronic kidney disease (CKD) and end-stage renal disease (ESRD) driven by demographic and health factors. In 2022, some 15,518 patients underwent kidney replacement therapy, of whom 82% received hemodialysis. Diabetes mellitus, the principal etiological factor, accounts for nearly 40% of kidney failures, with hypertension a close second. The highest incidence occurs among individuals aged 75 to 84, who commonly present multiple comorbidities necessitating frequent or intensive dialysis. Reflecting this burden, 1,117 Australians per million population were on dialysis in 2022, underscoring significant pressure on renal services. This persistent trend compels both public and private healthcare providers to rapidly expand dialysis infrastructure, augment specialist staffing, and elevate service capacity, thereby intensifying demand for hemodialysis machines, consumables, and integrated support systems to meet evolving patient needs.

To get more information on this market Request Sample

Shift Toward Home-Based Hemodialysis Supported by Reimbursement & Tech Innovation

Australia is undergoing a strategic shift from center-based to home hemodialysis (HHD), underpinned by cost efficiencies, government subsidy frameworks, and enhanced patient convenience. Federal and state programs provide funding differentials of up to AUD 30,000 per patient per annum and cover additional home utility expenses to encourage uptake. Leading dialysis platforms, including the Fresenius 4008S and Gambro AK95, have been optimized for self-administered overnight regimens, yielding superior solute clearance and fluid management. These combined structural and financial measures have alleviated pressure on in-center facilities and elevated patient quality of life, establishing HHD as a sustainable growth trajectory. The synergy of fiscal incentives and demonstrable clinical outcomes is driving accelerated adoption among healthcare providers and patients nationwide.

Growth Drivers of Australia Hemodialysis Market:

Aging Population and Increased Long-Term Renal Care Demand

The fast-increasing aging population in Australia is one of the major growth drivers for the hemodialysis market since elderly people are more likely to develop the chronic conditions that result in kidney failure. As life expectancy rises and complications related to age become more prevalent, the healthcare sector is increasingly witnessing elderly patients in need of long-term renal care. This demographic trend has increased pressure on dialysis service capacity in both public and private sectors. To address this, medical professionals are increasing the volume of dialysis chairs, enhancing accessibility in aged care facilities, and making investments in technology appropriate for geriatric patients. The elderly patients also tend to need more personalized and continuous treatment, leading to increased demand for dialysis equipment promoting patient comfort, safety, and user-friendliness. As this trend persists, healthcare planners are giving increasing priority to dialysis facilities in parts of the country with greater aging populations, so that treatment capacity keeps up with demand driven by demographics.

Government Health Support and Subsidized Treatment Access

Australia's publicly funded health system, Medicare, is an important factor in fueling the development of the hemodialysis market by making access to subsidized or fully subsidized dialysis treatment available to most citizens. The government acknowledges dialysis as an essential life-sustaining treatment and categorizes it under essential health services, enabling patients to access it at no to minimal direct cost. There is also increasing policy focus on decentralizing care, which enables patients to be treated using dialysis outside the conventional hospital environment, for example, in a community clinic or at home. Rural and remote health programs also facilitate the extension of dialysis services to geographically disadvantaged areas. Government funding has also helped provide training programs, supply chain assistance, and the incorporation of new dialysis technologies into public health facilities. This government support guarantees patient access and encourages private sector investment, as medical equipment manufacturers and healthcare providers have a stable and growing market base.

Raising Private Sector Involvement and Technological Progress

Australia's hemodialysis market is growing through increased private sector participation and technological developments. Private dialysis operators are coming into the market with new facilities and mobile units, particularly where there is unmet need or overextended public systems. These operators tend to bring in the latest equipment and individualized care models, attracting patients looking for convenience and excellence. Technological innovation, including smaller hemodialysis machines, digital monitoring systems, and automated treatment settings, is also changing the delivery of dialysis. These innovations are facilitating quicker setup times, enhanced patient outcomes, and data tracking for clinicians. Additionally, Australia's focus on digital health integration allows for the utilization of networked dialysis solutions that can be monitored remotely, improving safety and efficiency. As the private sector continues to partner with public health systems and experiment with new delivery models, the overall market is growing, providing greater options and better experiences for patients receiving dialysis treatment.

Opportunities of Australia Hemodialysis Market:

Expansion of Services in Rural and Indigenous Communities

Australia's geography and scattered population present enormous opportunities for expanding hemodialysis services in rural, remote, and Indigenous communities. These areas tend to have restricted access to specialist services and are underprovided by conventional hospital-based dialysis units. Therefore, there is intense need for home dialysis units, satellite clinics, and home dialysis programs specific to regional requirements. Government incentives and Indigenous health plans are becoming oriented toward enhancing chronic kidney disease outcomes in these areas, and they motivate healthcare providers to create localized dialysis services. For the private sector, this offers an opportunity to open new facilities or collaborate with public health agencies to provide community-based dialysis treatment. In regions such as the Northern Territory and portions of Western Australia, the excessive burden of kidney disease among Indigenous populations intensifies the urgency as well as market demand. By providing culturally sensitive, accessible treatment modalities, clinicians can satisfy an unmet need and support enhanced healthcare equity nationally.

Home-Based and Portable Dialysis Technology Innovation

With increased Australians desiring flexibility and self-management of chronic illness, home-based hemodialysis is increasingly in demand, presenting strong opportunity for manufacturers and service providers. Home dialysis enables patients to preserve their way of life, save travel costs, and receive treatment in a comfortable environment, making it particularly popular among people in remote locations or with limited mobility. This has paved the way for the production and sale of small, easy-to-use, and networked dialysis machines that are easily operable with minimal doctor supervision. Firms that innovate in home-based portable systems, water-saving equipment, and telehealth-facilitated care platforms are poised to take advantage of this expanding demand. National health policies in Australia are becoming progressively supportive of home care models, and public health budgets are shifting to fund home installation and patient education. Increasing awareness and advances in technology, the home dialysis segment offers a principal growth path in the overall Australian hemodialysis market.

Integration of Digital Health and Remote Monitoring

According to the Australia hemodialysis market analysis, robust digital health foundation and investment in the growth of telemedicine create a special setting in which remote monitoring can be integrated into hemodialysis care. With so many patients residing at distances from nephrology centers, the potential to monitor dialysis sessions and patient health information remotely presents the potential to enhance outcomes and simplify care. Firms that are working on dialysis machines with real-time data transmission, artificial intelligence-based diagnostics, or remote diagnostic functionality are in a good position to take advantage of this trend. Australia's investments in national health data platforms and digital medical records also provide an environment where these technologies can be adapted and scaled quickly. Clinicians benefit through remote monitoring by enabling timely intervention, medication titration, and better adherence monitoring. For patients, it provides reassurance and continuity. This convergence of digital innovation and healthcare demand offers a forward-looking opportunity for the hemodialysis market in Australia, especially as the sector moves toward more patient-centric and tech-enabled treatment models.

Challenges of Australia Hemodialysis Market:

Geographic Barriers and Access Disparities

One of the most persistent challenges in the Australian hemodialysis market is the difficulty in providing equitable access to dialysis services across the country’s vast and sparsely populated regions. Numerous remote and rural communities, particularly in the Northern Territory, Western Australia, and some Queensland regions, experience severe obstacles in receiving frequent dialysis treatment. These areas are without permanent dialysis centers, and patients are forced to travel extensive distances or even move totally to receive treatment within city centers. Such displacements trigger emotional, cultural, and economic distress, especially among Indigenous Australians who are over-represented in kidney disease. Inadequate specialist staffing, infrastructure constraints, and logistical challenges add to the difficulty of projecting services in these regions. Although home-based care and mobile dialysis units are yielding positive results, mainstreaming such solutions across broad and distant terrains is a daunting challenge. Closing this urban–rural gap is essential to guaranteeing universal access and enhancing national dialysis outcomes.

Workforce Shortages and Specialist Training Gaps

Australia is experiencing a lack of trained nephrologists, dialysis nurses, and renal technicians directly affecting the capacity and quality of hemodialysis services. The issue is extreme in rural and remote areas, where healthcare facilities regularly experience difficulties in recruiting and retaining trained staff. The specialized nature of dialysis therapy ensures that general medical practitioners regularly are not qualified to deal with those in need of prolonged renal replacement treatment. On top of this, the scarcity of training courses and career paths specially designed for renal care limits the development of a sustainable labor force. The ageing healthcare staff also puts extra pressure on already stretched teams, while burnout and elevated turnover undermine continuity of care. Without a steady supply of trained staff, the growth of dialysis services, particularly newer models such as home-based treatment, could be hampered. Filling this labor shortage through education, incentives, and local training centers is critical to the long-term sustainability of the Australia hemodialysis market demand.

High Operating Expenses and Systems Sustainability

Providing hemodialysis therapy in Australia is intensive and involves high operating expenses, such as staff, consumables, water, and electricity. These are compounded in rural locations, where transport and infrastructure costs are higher, and where economies of scale are less attainable. Although the public healthcare system subsidizes a large part of the costs of dialysis, growing demand for the service threatens long-term financial viability. The transition to home-based dialysis, though financially sound in the longer term, entails upfront spending on patient education, home adaptation, and the installation of equipment, which are costs not fully covered by subsidy programs. In addition, regular maintenance and constant technical support to machines can be stressing for both private and public providers. When healthcare budgets are constrained and demand increases for dialysis, coming up with efficient and scalable solutions that balance quality of care with costs is an urgent issue. These economic pressures may hinder future innovation and expansion of services if properly addressed.

Australia Hemodialysis Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the region/country level for 2026-2034. Our report has categorized the market based on segment, modality, and end-user.

Segment Insights:

- Hemodialysis Product

- Machines

- Dialyzers

- Others

- Hemodialysis Service

- In-center Services

- Home Services

The report has provided a detailed breakup and analysis of the market based on the segment. This includes hemodialysis product (machines, dialyzers, and others) and hemodialysis service (in-center services and home services).

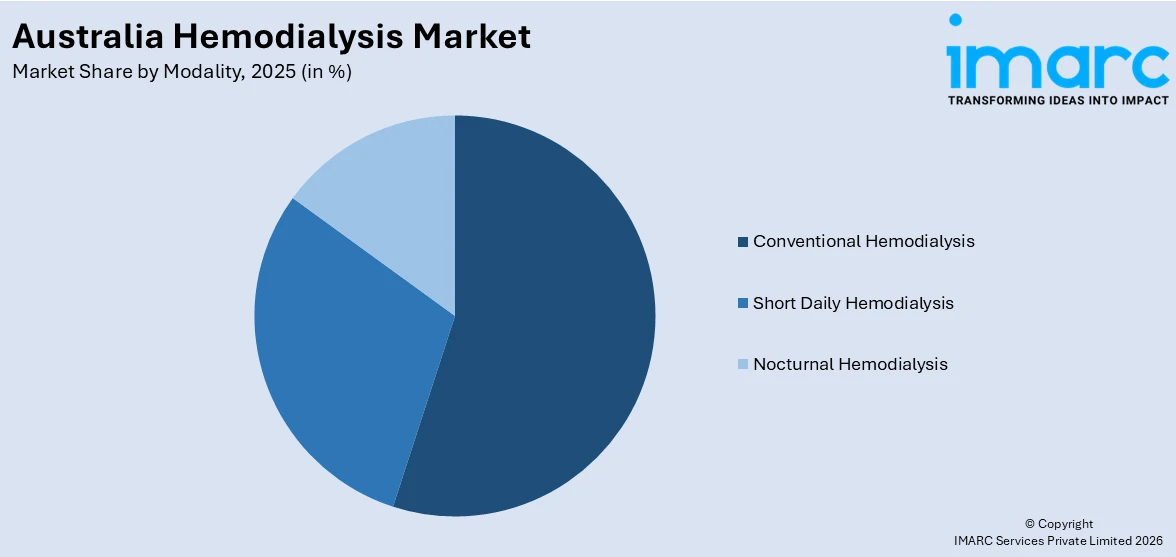

Modality Insights:

Access the comprehensive market breakdown Request Sample

- Conventional Hemodialysis

- Short Daily Hemodialysis

- Nocturnal Hemodialysis

A detailed breakup and analysis of the market based on the modality have also been provided in the report. This includes conventional hemodialysis, short daily hemodialysis, and nocturnal hemodialysis.

End-User Insights:

- Hospitals

- Independent Dialysis Centers

- Others

The report has provided a detailed breakup and analysis of the market based on the end-user. This includes hospitals, independent dialysis centers, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Hemodialysis Market News:

- April 2025: The Government of New South Wales awarded AUD 5.2 million to expand renal dialysis services in South‑West Sydney, including a new unit at Camden Hospital and upgrades at Campbelltown, Bowral, and Liverpool Hospitals. The funding will acquire specialist equipment and repurpose space, enabling around 120 extra hemodialysis sessions weekly.

- March 2025: The Yeppoon Satellite Renal Dialysis Unit officially opened at Capricorn Coast Hospital, offering new hemodialysis stations. The AUD 10.37 million facility eliminates the need for patients to travel to Rockhampton for life-sustaining blood filtration treatment three times weekly.

- February 2025: WA Country Health Service inaugurated a four-chair renal dialysis unit at Karratha Health Campus. The AUD 2.3 million facility begins with four chairs, scaling up to serve 16 patients weekly, thereby bringing treatment on-country for West Pilbara residents.

- June 2024: Mornington Island Hospital unveiled a new six‑station hemodialysis unit, allowing remote patients to undergo lifesaving blood‑filtration treatment on‑Country. The facility supports both independent and nurse‑assisted dialysis, enhancing continuity of care, cultural connection, and patient well-being by enabling regular treatment alongside family and community.

Australia Hemodialysis Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered |

|

| Modalities Covered | Conventional Hemodialysis, Short Daily Hemodialysis, Nocturnal Hemodialysis |

| End-Users Covered | Hospitals, Independent Dialysis Centers, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia hemodialysis market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia hemodialysis market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia hemodialysis industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Hemodialysis Market Report

The Australia hemodialysis market was valued at USD 1,951.6 Million in 2025.

The Australia hemodialysis market is projected to exhibit a CAGR of 3.52% during 2026-2034.

The Australia hemodialysis market is expected to reach a value of USD 2,663.4 Million by 2034.

Key trends in Australia hemodialysis market include the shift toward home-based dialysis treatments, adoption of portable and user-friendly machines, and integration of telehealth for remote patient monitoring. There is also growing investment in public-private partnerships to expand dialysis infrastructure and improve access in regional and Indigenous communities.

The Australia hemodialysis market is driven by the rising prevalence of chronic kidney disease, an aging population, and increased awareness about renal care. Expanding access to dialysis services in rural areas, advancements in dialysis technology, and supportive government healthcare policies also contribute to the growing demand for hemodialysis treatment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)