Australia Hydrogen Energy Storage Market Size, Share, Trends and Forecast by Storage Form, Technology, Application, End User, and Region, 2026-2034

Australia Hydrogen Energy Storage Market Overview:

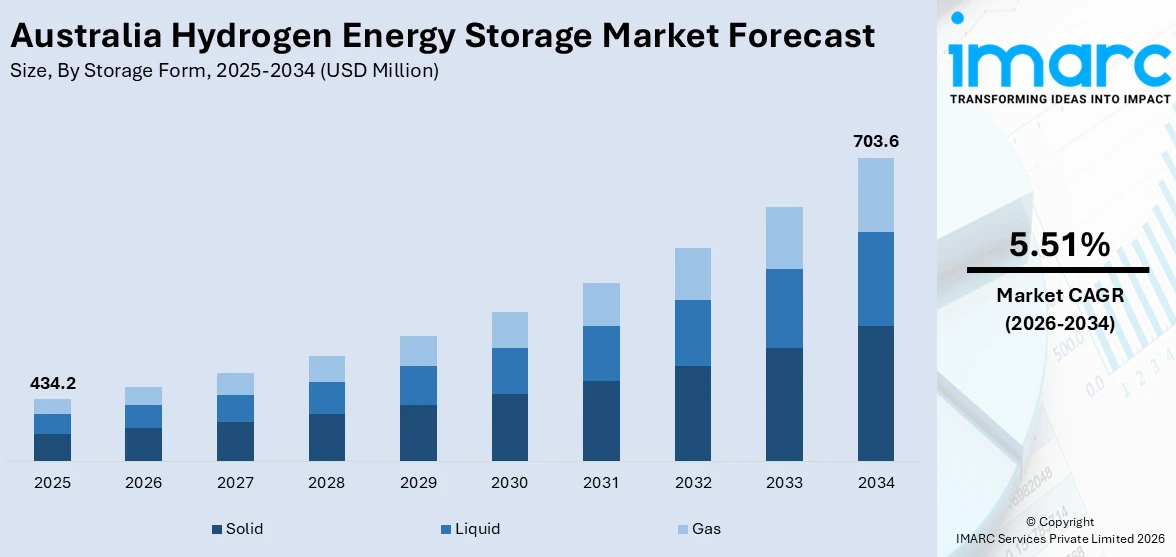

The Australia hydrogen energy storage market size reached USD 434.2 Million in 2025. Looking forward, the market is expected to reach USD 703.6 Million by 2034, exhibiting a growth rate (CAGR) of 5.51% during 2026-2034. The market is driven by growing investments in renewable energy, government support for decarbonization, and the country’s potential as a hydrogen exporter. The integration of hydrogen with solar and wind projects, especially in remote and off-grid areas, is enhancing storage adoption. In addition to this, the rising demand for clean energy, the development of hydrogen hubs, and the increasing focus on energy security are important factors augmenting Australia hydrogen energy storage market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 434.2 Million |

| Market Forecast in 2034 | USD 703.6 Million |

| Market Growth Rate (2026-2034) | 5.51% |

Key Trends of Australia Hydrogen Energy Storage Market:

Expansion of Renewable-Integrated Hydrogen Projects

Australia is witnessing a significant rise in renewable energy projects that are coupled with hydrogen production and storage systems. With vast solar and wind resources, regions like Western Australia, Queensland, and South Australia are increasingly becoming hubs for integrated renewable hydrogen initiatives. In addition to this, projects such as the Asian Renewable Energy Hub and the Western Green Energy Hub aim to produce green hydrogen at scale using solar and wind energy, with on-site storage playing a critical role in balancing intermittent power generation and ensuring continuous hydrogen supply. These integrated systems enhance grid stability and offer a pathway for decarbonizing hard-to-abate sectors, including mining, transport, and heavy industry. Additionally, strong government support through initiatives like the Australian Renewable Energy Agency (ARENA) and Clean Energy Finance Corporation (CEFC) is providing funding for pilot-scale and commercial-scale renewable hydrogen projects. For instance, the government is legislating the Hydrogen Production Tax Incentive. The incentive will pay USD 2 for each kilogram of qualified renewable hydrogen produced for up to ten years, from July 1, 2027, to June 30, 2040. This trend is establishing a scalable infrastructure model that positions hydrogen as a fuel and as a critical energy storage vector aligned with Australia’s broader clean energy transition goals.

To get more information on this market Request Sample

Development of Hydrogen Export Infrastructure with Storage Capabilities

Australia is actively positioning itself as a global hydrogen exporter, particularly targeting energy-deficient countries in Asia such as Japan and South Korea. According to the Australian Renewable Energy Agency (ARENA), demand for hydrogen exports from Australia might exceed three million tons by 2040, contributing AUD10 billion per year to the economy. Moreover, significant investments are directed toward building integrated storage and transportation systems to meet the expected export demand. Hydrogen storage technologies, including compressed gas storage, liquefied hydrogen, and ammonia-based storage, are deployed at port facilities to facilitate large-scale shipment. Additionally, there is growing collaboration between Australian agencies and international stakeholders to standardize safety, quality, and storage protocols for export-ready hydrogen. This, in turn, is contributing to Australia hydrogen energy storage market growth. Apart from this, projects like the Hydrogen Energy Supply Chain (HESC) in Victoria and the Port of Gladstone’s hydrogen hub illustrate how storage solutions are tailored to match export formats and long-haul logistics requirements. These projects often incorporate buffer storage to manage supply fluctuations and ensure continuous loading capabilities for maritime transport. The growing export-oriented infrastructure reinforces the role of hydrogen storage for domestic energy management and as a critical enabler of Australia’s participation in the global hydrogen economy.

Growth Drivers of Australia Hydrogen Energy Storage Market:

Decarbonization of Industrial and Energy Sectors

Australia's pledge to decarbonize its industrial and energy sectors is a key impetus for growth in its hydrogen energy storage market. As industries like steel production, mining, and heavy transport come under growing pressure to cut emissions, hydrogen presents a viable and scalable alternative to fossil fuels. These industries are energy-intensive and tend to be located in areas that lack grid access or have poor-quality grids. Hydrogen energy storage can feed power systems off-grid, power industrial processes, and serve as backup energy solutions without causing greenhouse gas emissions. Mining, specifically, is looking into hydrogen-fueled equipment and storage-centric energy systems to deliver sustainability targets without sacrificing productivity. Moreover, the shift toward renewables for the national electricity grid needs complementary storage for dealing with variability and demand. Hydrogen fills this function by storing surplus renewable energy and providing it again when there is a need, and thus, becoming a valuable instrument in Australia's drive toward a lower-carbon economy.

Strategic Export Potential and Regional Trade Partnerships

Australia's geographical proximity to leading Asian economies as well as its status as a low-risk energy exporter is a principal driver for the growth of its hydrogen energy storage market. Japan, South Korea, and Singapore are engaged in actively investing in hydrogen technologies and have set up strategic alliances with Australia to tie up long-term hydrogen supply. This makes Australia a domestic consumer of hydrogen and a potential export center in the future, with the need for large-scale energy storage facilities to meet supply and demand. Hydrogen energy storage allows producers to balance production, control export timetables, and maintain consistent quality and supply assurance, which are key considerations in global trade. Further, hydrogen shipping infrastructure development, including liquefaction and port facilities, is also driving storage demand. With Australia's shift toward new energy exports such as coal and gas to hydrogen, the demand for efficient and scalable energy storage technology becomes central to enabling it to play a part in the changing regional energy ecosystem.

Government Policies and Industry-Led Hydrogen Initiatives

Industrial cooperation and government support are major forces driving the growth of Australia's hydrogen energy storage market. National and state hydrogen strategies have set the stage for regulatory incentives, financing mechanisms, and pilot programs focused on fast-tracking the hydrogen economy. States like Queensland and South Australia have initiated dedicated hydrogen hubs with production, storage, and distribution infrastructure. These projects sometimes entail partnerships between public agencies, energy firms, and research institutions to bring about new storage technologies and showcase commerciality. Additionally, hydrogen is viewed to assist decarbonization of hard-to-abate industries such as transport, mining, and heavy industry, building multi-sectoral demand that further stimulates innovation in storage. Grants and investment incentives have also attracted private firms into the hydrogen market, thus promoting competition and technological development. With government and industry converging on long-term sustainability targets, the drive for hydrogen energy storage is getting even stronger throughout the Australian market.

Opportunities of Australia Hydrogen Energy Storage Market:

Leveraging Renewable Energy Surplus for Domestic Storage

Australia enjoys a richness of solar and wind resources, notably in isolated and sparsely populated areas like Western Australia and South Australia. These regions tend to produce renewable energy than can be utilized by the grid instantly, resulting in curtailment or wasted capacity. Hydrogen energy storage represents a major opportunity to harvest and store this excess energy in the form of hydrogen for future use. Stored hydrogen can be used to provide electricity at peak demand periods, maintain grid stability, and minimize fossil fuel dependence. As utility-scale solar and wind farms are becoming heavily invested in, hydrogen storage is a strategic facilitator for a more flexible and robust energy system. It also creates opportunity for decentralized energy networks in remote towns, enabling independence in energy and backing Australia's long-term climate ambitions. Excess renewable energy can be converted into hydrogen and in doing so, the nation can leverage its natural resources to the maximum and develop a sound domestic storage system.

Establishing a Hydrogen Export and Bunkering Hub

As per the Australia hydrogen energy storage market analysis, the closeness of the region to key Asia-Pacific economies uniquely positions it to become a future export leader in hydrogen. Yet before hydrogen can be exported overseas, particularly in liquid form or as ammonia, it will need to be safely stored at scale. This presents a large opportunity for investment in Australia in large-scale hydrogen storage facilities around major ports like Darwin, Port Kembla, and Gladstone. These ports are being established as possible hydrogen export terminals and have the potential to become international refueling or bunkering nodes for ships powered by hydrogen. This would fund Australia's export plans and be consistent with the global shipping industry's move toward cleaner energy. In addition, the establishment of these hydrogen storage facilities creates engineering, construction, maintenance, and logistics downstream opportunities. It also has regional economic dividends, especially for regions moving away from fossil fuel-based economies. As international demand for green hydrogen increases, Australia's strategic position, export experience, and robust maritime infrastructure provide it with a competitive advantage in this new sector.

Industrial Decarbonization and Off-Grid Storage Solutions

Australia's energy-intensive industry sectors, such as mining, cement, and chemical manufacturing, are major energy users, typically based in off-grid or on-the-periphery-of-grid areas. Hydrogen energy storage provides the chance to revolutionize decarbonizing these industries while improving energy security and reliability. For example, remote mining operations in Western Australia or Queensland can use hydrogen generated on-site from renewables, then stored and converted back into electricity or used directly for fueling equipment. This reduces the need for diesel transport and lowers both emissions and fuel costs. Additionally, industrial clusters looking to meet sustainability goals are exploring hydrogen as a clean feedstock and energy source, requiring advanced storage solutions for continuous operations. The flexibility of hydrogen storage to serve both power and industrial process needs gives it a unique advantage over other forms of storage. As industry and government increasingly focus on zero-emissions production, hydrogen storage stands out as a critical enabler of Australia’s clean industrial future.

Government Support of Australia Hydrogen Energy Storage Market:

National Hydrogen Strategy and Long-Term Policy Vision

The Australian government has taken a proactive approach to developing its hydrogen industry, including hydrogen energy storage, through the establishment of a comprehensive National Hydrogen Strategy. By integrating hydrogen technology across industries like transportation, energy, and heavy industry, this strategy sets a long-term goal for Australia to become a significant worldwide leader in clean hydrogen. It mentions energy storage as the key driver of this shift, offering funding, regulation, and infrastructure planning to make hydrogen an energy carrier that works. It is one of the distinctive features of this policy that it aims to tap Australia's natural renewable energy resources like solar and wind potential, to produce green hydrogen, which is stored and consumed within Australia or exported. The national plan also assists the establishment of clean hydrogen certification schemes that meet quality standards while stimulating private investment in storage technologies for hydrogen in line with decarbonization trends globally, which further contributes to the growth of Australia hydrogen energy storage market demand.

State Government Investment in Hydrogen Hubs and Storage Infrastructure

State governments in Australia are taking the lead in driving hydrogen energy storage development by investing in specific hydrogen hubs and state-level policy implementations. Regions like South Australia, Queensland, and Western Australia have set up or are setting up multi-million-dollar hydrogen hubs with storage infrastructure as a central element. Hubs are strategically placed in areas with high quality renewable resources and proximity to transport and export facilities. Hubs are innovation hubs for generating, storing, and exporting hydrogen, often including government agencies, energy players, and research institutions. State assistance involves direct funding, access to land, expedited permitting, and collaboration with universities to spur technological innovation in storage systems. The programs are designed to boost local economies and form clean energy jobs, and to prove commercial-scale viability of hydrogen storage. By designing assistance according to regional strengths and industrial necessities, state governments are creating a decentralized yet integrated system for scaling up hydrogen storage nationwide.

Funding Initiatives and Research Incentives

Support from the government for hydrogen energy storage in Australia goes beyond policy into significant monetary support in the form of research grants, industry incentives, and public-private partnerships. Pilot programs, feasibility studies, and new storage technologies have been made possible in large part by organizations such as the Clean Energy Finance Corporation and ARENA (Australian Renewable Energy Agency). These include funding hydrogen compression, liquefaction, underground storage, and mobile storage systems. The administration also encourages innovation by programs that facilitate partnerships between universities, research institutions, and industry stakeholders to create safer, efficient, and affordable storage technology. Remote and off-grid uses are specifically targeted in funding, demonstrating the significance of hydrogen energy storage in enabling energy access for remote communities and industries. Moreover, procurement policies are in development to give precedence to clean hydrogen and its related infrastructure in government projects. This layered support structure ensures that Australia remains at the forefront of global hydrogen development, with energy storage positioned as a key pillar.

Challenges of Australia Hydrogen Energy Storage Market:

High Infrastructure Costs and Investment Barriers

One of the most significant challenges facing Australia’s hydrogen energy storage market is the high cost associated with developing the necessary infrastructure. Building hydrogen storage systems, especially those involving compression, liquefaction, or underground storage, requires substantial capital investment. In Australia, where renewable energy generation facilities are far away from industry and port locations, the expense of setting up integrated transport and storage networks is higher. Furthermore, as hydrogen storage is an ongoing technology development, economies of scale are restricted, and prices remain high. Although government pilots and grants assist in covering some of the up-front costs, private sector investment is still tentative with undefined return on investment and long payback periods for technology. This is especially true in Western Australia and Northern Territory off-grid regions, where logistical and operational issues further make infrastructure rollout difficult. Removing these financial impediments is critical to upscaling hydrogen storage and supporting the wider hydrogen economy in Australia.

Technical and Safety Challenges of Hydrogen Storage

Hydrogen, though a promising clean energy carrier, has specific technical and safety issues associated with its storage. Its low energy density necessitates either high-pressure compression, cryogenic liquefaction, or chemical storage—all processes involving complex technologies and rigorous safety measures. The regulatory mechanism for hydrogen storage in Australia is yet to be developed, which can prolong project approval timelines and lead to uncertainty for investors. Storage facilities need to be able to handle the extreme temperature fluctuations prevalent in Australia's outback, especially in desert or coastal environments. Additionally, today's Australian industrial workforce possesses little experience working with hydrogen-specific safety standards, so there is a need for extensive upskilling and reskilling. The flammability of hydrogen and the requirement for leak-free storage and transport also create issues, particularly if storage units are placed close to urban areas or critical infrastructure. These technical challenges, in addition to sparse real-world operating experience, delay deployment and necessitate extensive testing and standardization to establish confidence in the technology's reliability and security.

Uncertain Demand and Market Development Pathways

The other major challenge in Australia's hydrogen energy storage market is the uncertainty of clearly defined demand pathways. Although hydrogen is regarded as a future energy carrier of importance, at present it has limited application in Australia, and hence making large-scale storage investment without strong offtake agreements become problematic. The steel, transport, and electricity sectors are still at the nascent stage of adopting hydrogen, and most planned projects remain in the feasibility or pilot stage. This uncertainty impacts investor confidence and complicates long-term planning for storage facilities. Moreover, Australia's energy market is state fragmented with its own hydrogen roadmap and different levels of advancement, which can lead to inadequate national coordination. Without unified demand signals and standardized frameworks, storage developers are at risk of underutilization. To meet this, the creation of stable, long-term policy regimes and assured end-use markets will be pivotal in driving the hydrogen storage industry forward.

Australia Hydrogen Energy Storage Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on storage form, technology, application, and end user.

Storage Form Insights:

- Solid

- Liquid

- Gas

The report has provided a detailed breakup and analysis of the market based on the storage form. This includes solid, liquid, and gas.

Technology Insights:

- Compression

- Liquefaction

- Material Based

A detailed breakup and analysis of the market based on the technology have also been provided in the report. This includes compression, liquefaction, and material based.

Application Insights:

Access the comprehensive market breakdown Request Sample

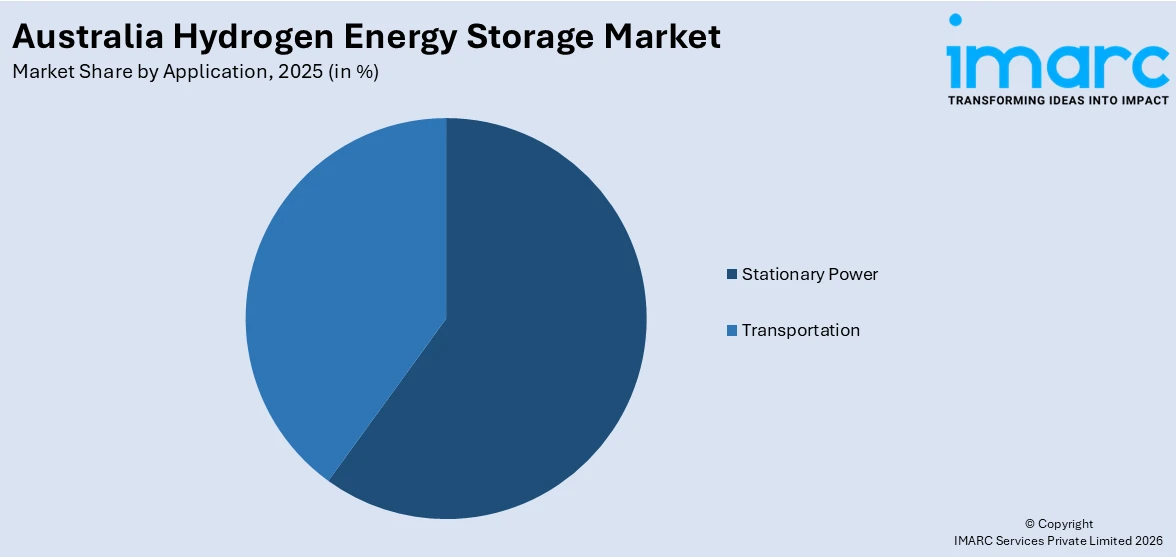

- Stationary Power

- Transportation

The report has provided a detailed breakup and analysis of the market based on the application. This includes stationary power and transportation.

End User Insights:

- Utilities

- Industrial

- Commercial

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes utilities, industrial, and commercial.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Hydrogen Energy Storage Market News:

- On March 22, 2024, The Australian Renewable Energy Agency (ARENA) has invested $2 million in Lochard Energy's H2RESTORE project, launching an 18-month feasibility study for large-scale hydrogen production and underground storage in Victoria's Ottway Basin. The study aims to assess the technical and economic viability of repurposing existing underground gas reservoirs to store hydrogen generated via electrolysis using surplus energy from the National Electricity Market (NEM), thereby providing long-duration, seasonal energy storage to enhance grid reliability. This initiative represents Australia's first exploration into underground hydrogen storage.

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Storage forms Covered | Solid, Liquid, Gas |

| Technologies Covered | Compression, Liquefaction, Material Based |

| Applications Covered | Stationary Power, Transportation |

| End Users Covered | Utilities, Industrial, Commercial |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia hydrogen energy storage market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia hydrogen energy storage market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia hydrogen energy storage industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Hydrogen Energy Storage Market Report

The Australia hydrogen energy storage market was valued at USD 434.2 Million in 2025.

The Australia hydrogen energy storage market is projected to exhibit a CAGR of 5.51% during 2026-2034.

The Australia hydrogen energy storage market is expected to reach a value of USD 703.6 Million by 2034.

The Australia hydrogen energy storage market is witnessing trends like increased investment in green hydrogen hubs, development of large-scale underground and liquefied hydrogen storage, and integration with renewable energy projects. Collaboration between government and industry, along with export-focused infrastructure, is shaping a more resilient and future-ready hydrogen storage ecosystem.

The Australia hydrogen energy storage market is driven by the nation’s push for decarbonization, abundant renewable energy resources, and strong government support. Strategic export potential to Asia and the need for reliable storage solutions to stabilize renewable energy supply further accelerate investment and innovation in hydrogen-based storage technologies across the country.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)