Australia Meat Processing Market Size, Share, Trends and Forecast by Product, Equipment, Meat, Mode of Operation, and Region, 2026-2034

Australia Meat Processing Market Summary:

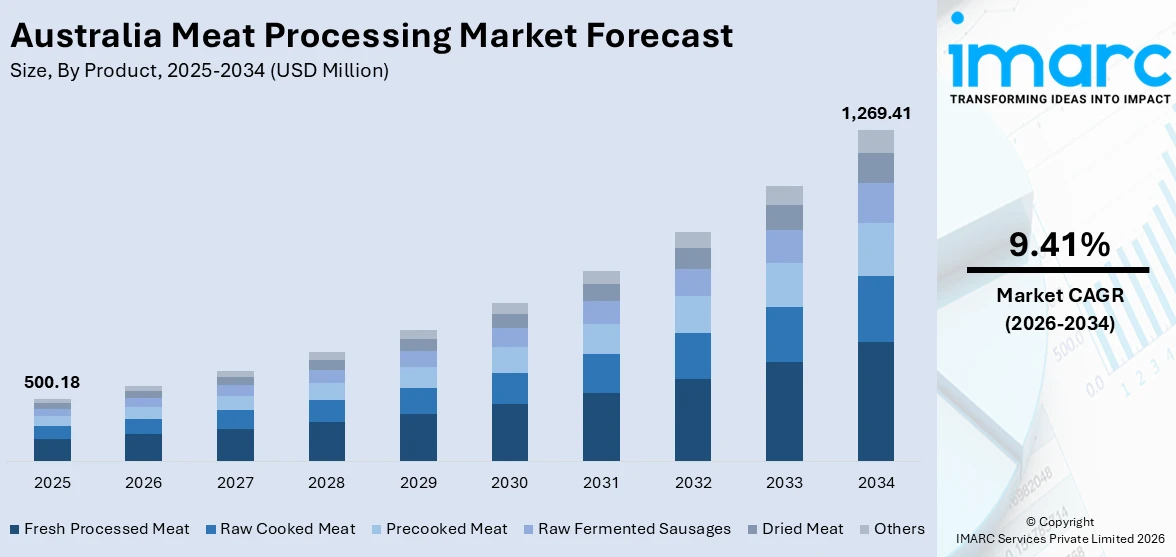

The Australia meat processing market size was valued at USD 500.18 Million in 2025 and is projected to reach USD 1,269.41 Million by 2034, growing at a compound annual growth rate of 9.41% from 2026-2034.

The Australia meat processing market is experiencing sustained growth, as domestic protein consumption increases and export demand strengthens across key international destinations. Rapid adoption of automation, technological innovations in processing equipment, and expanding cold chain infrastructure are enhancing operational efficiency and product quality across the supply chain. Growing consumer preferences for convenient, minimally processed, and premium meat products are accelerating product diversification.

Key Takeaways and Insights:

- By Product: Fresh processed meat dominates the market with a share of 38.5% in 2025, owing to rising consumer preference for minimally processed, convenient, and ready-to-cook products that align with evolving dietary habits across urban and regional Australian households.

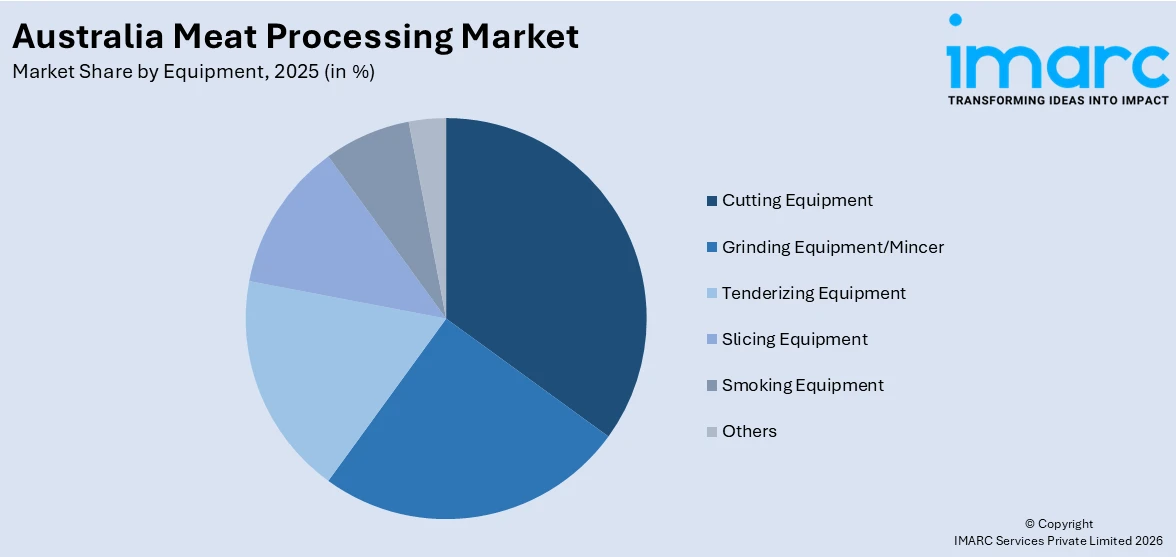

- By Equipment: Cutting equipment leads the market with a share of 32.5% in 2025. This dominance is driven by its critical role in high-throughput deboning, portioning, and precision cutting operations that are essential for export-grade and value-added meat processing.

- By Meat: Beef prevails the market with a share of 42.5% in 2025, reflecting Australia's position as one of the world's leading beef producers and exporters, with strong domestic and international demand sustaining robust processing volumes across the supply chain.

- By Mode of Operation: Automatic represents the leading segment with a share of 58.5% in 2025, driven by rising labor costs, increasing processing capacity requirements, and the need for consistent product quality and food safety compliance across processing facilities.

- By Region: Australia Capital Territory & New South Wales comprises the largest region with 32.5% share in 2025, driven by its proximity to major livestock farming areas, well-developed processing infrastructure, and strategic access to key export logistics and domestic consumption centers.

- Key Players: Key players drive the Australia meat processing market through capacity expansion, adoption of advanced automation systems, and strengthening of global distribution networks. Investments in food safety compliance, sustainable processing practices, and value-added product development are helping companies boost operational efficiency, expand market access, and meet evolving domestic and international consumer expectations.

To get more information on this market Request Sample

The Australia meat processing market is underpinned by a robust agricultural foundation, a resilient export ecosystem, and accelerating investment in modern processing infrastructure. In 2024, Australia shipped 2.24 Million Tons of red meat to 104 nations, marking the highest quantity of red meat exported to date. Growing domestic protein consumption alongside strong international demand for premium, quality-assured Australian red meat is prompting processors to expand capacity, modernize equipment, and adopt automation-led production models across the supply chain. The increasing shift towards convenience-oriented, value-added products, such as marinated cuts, pre-seasoned offerings, and ready-to-cook items, is reshaping product development across retail and foodservice channels. Sustained government support through food safety frameworks, bilateral trade agreements, and industry innovation programs is helping processors maintain competitive positioning in demanding global markets. Technological upgrades in cold chain logistics, digital traceability systems, and precision cutting equipment are enabling facilities to meet increasingly stringent quality and sustainability standards from major importing nations.

Australia Meat Processing Market Trends:

Accelerating Adoption of Automation and Robotics

The integration of automated robotics, artificial intelligence (AI), and machine vision systems across the Australia meat processing sector is reshaping facility operations and production capabilities. Processors are deploying robotic cutting, deboning, and packaging lines to address persistent labor shortages in regional areas, improve throughput consistency, and reduce reliance on physically demanding manual tasks. These technologies enable precise, repeatable processing outcomes while enhancing hygiene compliance and food safety standards, contributing to Australia meat processing market growth in alignment with the increasing demands of export-oriented production.

Expansion of Premium and Value-Added Meat Products

Consumer demand for premium, specialty, and value-added meat products is intensifying across both domestic retail and export channels, creating new product development opportunities for Australian processors. The growing appetite for grass-fed, grain-fed, Wagyu, halal-certified, and organic varieties reflects a broader premiumization trend driven by health and wellness awareness, ethical sourcing preferences, and rising disposable incomes. As per IMARC Group, the Australia health and wellness market is set to attain USD 205.8 Billion by 2034.

Growing Focus on Sustainability and Environmental Responsibility

Environmental sustainability is becoming an increasingly central consideration in the Australia meat processing sector as processors face rising expectations from consumers, investors, and regulatory authorities. Facilities are investing in renewable energy integration, water recycling systems, biogas generation from processing waste, and carbon footprint reduction programs. Export markets, particularly in Europe and North America, are applying greater scrutiny to the environmental credentials of their meat suppliers, incentivizing Australian processors to adopt certified sustainable practices and develop transparent reporting mechanisms that demonstrate measurable progress toward environmental and animal welfare benchmarks throughout the supply chain.

Market Outlook 2026-2034:

The Australia meat processing market is positioned for a robust and sustained growth trajectory, propelled by the convergence of strengthening export demand, modernizing processing infrastructure, and evolving domestic consumption patterns. As producers and processors continue to adapt to changing market conditions, investment in high-capacity automation, energy-efficient systems, and advanced packaging technologies is expected to intensify throughout the forecast period. The market generated a revenue of USD 500.18 Million in 2025 and is projected to reach a revenue of USD 1,269.41 Million by 2034, growing at a compound annual growth rate of 9.41% from 2026-2034. Rising emphasis on traceability, food safety standards, and value-added meat products is further shaping competitive strategies and driving long-term market expansion.

Australia Meat Processing Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Fresh Processed Meat |

38.5% |

|

Equipment |

Cutting Equipment |

32.5% |

|

Meat |

Beef |

42.5% |

|

Mode of Operation |

Automatic |

58.5% |

|

Region |

Australia Capital Territory & New South Wales |

32.5% |

Product Insights:

- Raw Cooked Meat

- Precooked Meat

- Fresh Processed Meat

- Raw Fermented Sausages

- Dried Meat

- Others

Fresh processed meat dominates with a market share of 38.5% of the total Australia meat processing market in 2025.

Fresh processed meat includes a broad variety of minimally processed items that give customers the ease of less preparation while maintaining natural flavor and nutritional value, such as sausages, burger patties, marinated cuts, and seasoned ready-to-cook foods. Health-conscious Australian customers are steadily moving towards diets high in protein and low in processed foods, which supports this segment’s expansion. The growing need for quick meal options that fit hectic schedules without sacrificing quality or freshness lends more credence to this.

The fast expansion of the foodservice industry, where restaurants, quick-service restaurants (QSRs), and meal kit providers demand consistent, high-quality, pre-cut portions, further solidifies the dominance of fresh processed meat in Australia's processing landscape. Fresh processed meat is becoming more competitive in both retail and export markets, owing to advancements in modified-atmosphere and vacuum packaging, which increase shelf life while maintaining flavor integrity. The segment's consumer base is developing as a result of the growing trend toward premium and ethically sourced products.

Equipment Insights:

Access the comprehensive market breakdown Request Sample

- Grinding Equipment/Mincer

- Tenderizing Equipment

- Cutting Equipment

- Slicing Equipment

- Smoking Equipment

- Others

Cutting equipment leads with a share of 32.5% of the total Australia meat processing market in 2025.

Cutting equipment encompasses a wide variety of machinery used for deboning, portioning, and precise trimming in beef, lamb, and pork processing operations, such as band saws, circular saws, water-jet cutters, and AI-guided robotic cutting systems. Its dominance illustrates how crucial precise, fast cutting aids in preserving product yield, eliminating waste, and fulfilling strict export-grade requirements. Its significance in contemporary meat processing lines is further reinforced by its capacity to manage high processing volumes with reliable accuracy.

Australia's meat processing facilities are transforming, due to the use of advanced robotics and computer vision-guided cutting systems, which allow for reliable, high-throughput processes with less reliance on manual labor. Automated cutting machines using machine learning (ML) algorithms and three-dimensional scanning capabilities can adjust to changes in animal size and carcass structure, greatly increasing production and accuracy while reducing worker repetitive strain injuries. Processors are investing in next-generation cutting systems that combine speed, hygiene compliance, and flexible cutting profiles to effectively meet a variety of global market needs, as export volumes continue to climb and buyer criteria become more demanding.

Meat Insights:

- Beef

- Pork

- Mutton

- Others

Beef exhibits a clear dominance with a 42.5% share of the total Australia meat processing market in 2025.

Beef forms the cornerstone of the Australia meat processing industry, with the country consistently ranked among the world’s leading beef producers and exporters. The vast cattle herd, diverse processing capacity across eastern and northern Australia, and strong domestic consumption underpin sustained beef processing volumes throughout the year. According to the United States Department of Agriculture Foreign Agricultural Service, Australian beef production increased by 14% from 2023 levels in 2024, reaching near-record volumes and reinforcing the sector’s capacity to meet both expanding domestic consumption and surging export demand.

The premium beef category is experiencing accelerating growth as both domestic consumers and international buyers increasingly favor grain-fed, grass-fed, and Wagyu varieties for their superior marbling, flavor profiles, and perceived health benefits. Processors are investing in advanced grading systems, blockchain-enabled traceability platforms, and halal-certified processing lines to address the nuanced preferences of export markets across Asia and the Middle East. Strong feedlot capacity across Queensland and New South Wales continues to support consistent year-round supply of high-quality grain-fed beef, enabling processors to maintain stable production schedules and fulfill premium export contracts with leading global retail and foodservice partners.

Mode of Operation Insights:

- Manual

- Semi-Automatic

- Automatic

Automatic prevails the market with a 58.5% share of the total Australia meat processing market in 2025.

Automatic encompasses integrated robotic cutting, deboning, packaging, and palletizing operations that enable high-throughput, consistent, and hygiene-compliant meat processing with minimal manual intervention. Its widespread adoption in Australia is driven by rising labor costs, persistent workforce shortages in regional processing facilities, and the operational imperative to scale production in line with surging export demand. Automatic systems also enhance operational consistency by reducing human error and ensuring standardized processing outcomes across large production volumes.

The transition to automatic operations is also propelled by the growing emphasis on traceability, food safety compliance, and export accreditation requirements. Automated systems embedded with digital sensors, machine vision cameras, and real-time monitoring software enable processors to maintain precise temperature control, consistent cut specifications, and complete lot-level traceability from slaughter through to final packaging. Australia’s leading processing facilities are deploying next-generation robotics and AI-guided systems to address complex deboning, trimming, and carcass grading tasks, improving operational efficiency and worker safety while ensuring rigorous compliance with the stringent quality and regulatory requirements of international export markets.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represents the leading segment with a 32.5% share of the total Australia meat processing market in 2025.

The Australian Capital Territory & New South Wales constitute the single largest regional market in Australia’s meat processing industry, anchored by a concentration of major processing facilities, extensive logistics infrastructure, and proximity to Australia’s largest domestic consumer markets. Sydney and surrounding metropolitan areas serve as critical distribution hubs for both domestic supply chains and export-oriented cold chain operations, connecting processing plants to major international shipping ports. This strong connectivity enables efficient movement of perishable products across both domestic and global markets.

The region’s market dominance is further reinforced by its well-developed agricultural hinterland, which supports consistent livestock supply from diverse production zones across New South Wales. Beef and sheep processing operations are particularly prominent, with the state’s processing facilities collectively capable of handling significant daily throughput volumes across multiple product categories including primal cuts, offal, and value-added prepared products. The Australian Capital Territory’s proximity to key regulatory bodies, research institutions, and government agencies provides New South Wales-based processors with favorable access to compliance support, export accreditation services, and industry development programs that facilitate continued market access expansion across domestic and international channels.

Market Dynamics:

Growth Drivers:

Why is the Australia Meat Processing Market Growing?

Rising Domestic Protein Demand and Shifting Consumer Preferences

The sustained growth in domestic protein consumption constitutes a foundational driver of the Australia meat processing market. Australian consumers are increasingly adopting high-protein dietary frameworks driven by broader health, fitness, and wellness trends, which are elevating demand across a diverse spectrum of processed, minimally processed, and value-added meat products throughout retail, foodservice, and digital commerce channels. The shift towards convenience-oriented purchasing is particularly significant, as the rapid growth of dual-income households, urbanization, and time-poor lifestyles accelerates demand for pre-seasoned, marinated, and ready-to-cook formats that deliver premium quality with minimal preparation burden. In 2024, in New South Wales, for couple families with dual incomes, the median income for families with children was USD 3,282, while for those without children, it was USD 2,954. The expanding foodservice sector, encompassing QSRs, full-service dining outlets, hotel catering, and meal delivery platforms, is simultaneously generating sustained wholesale demand for precisely portioned, hygienically processed meat inputs of uniform quality. Processors are responding by investing in flexible, multi-product lines capable of addressing the increasingly segmented consumer market, including premiumization trends, grass-fed and organic options, halal-certified products, and culturally specific specialty meats.

Strong Export Demand and Expanding Global Market Access

The Australia meat processing sector is significantly propelled by robust and growing international demand, particularly from high-value markets in Asia, the Middle East, and North America. Australia’s well-established global reputation for producing safe, high-quality, sustainably raised red meat gives its processors a competitive premium that is reinforced by comprehensive food safety accreditation systems and animal welfare standards recognized by importing nations. The extensive network of bilateral and multilateral free trade agreements covering key export destinations continues to reduce tariff barriers and streamline market access, enabling Australian processors to compete effectively against other major exporting nations. The geopolitical and supply dynamics of international beef trade, including shifts in competitive supply from other major exporters, are creating expanded market opportunities that Australian processors are positioned to capitalize upon. Investments in cold chain logistics, advanced packaging technologies for extended shelf life, and digital traceability systems are improving the export-readiness of Australian products, supporting higher-value product categories in premium retail and foodservice segments internationally.

Technological Advancements and Modernization of Processing Infrastructure

Technological innovations and infrastructure modernization represent a powerful structural growth driver for the Australia meat processing market. The accelerating deployment of automated processing systems, robotics, AI-guided quality control, and advanced packaging technologies is enabling processing facilities to achieve significant improvements in throughput efficiency, product consistency, and operational cost management. These investments are particularly critical in an environment of rising labor costs and persistent workforce challenges in regional processing locations, where automation offers a sustainable pathway to maintaining and expanding production capacity. The Australian government has demonstrated sustained commitment to supporting food processing innovation, with approvals granted for major new facilities incorporating renewable energy systems and advanced processing technologies. This ongoing technological transformation is also enhancing export competitiveness by enabling processors to meet stringent international quality, traceability, and sustainability standards more effectively.

Market Restraints:

What Challenges the Australia Meat Processing Market is Facing?

Persistent Workforce Shortages and Labor Cost Pressures

Labor availability represents one of the most significant structural challenges facing the Australia meat processing sector. Regional processing facilities frequently encounter difficulties attracting and retaining sufficient skilled workers, as the physically demanding nature of the work, geographic remoteness of many facilities, and competition from other industries constrain workforce supply. Elevated labor costs driven by wage growth and workforce scarcity are compressing operating margins, particularly for smaller processors.

Environmental Compliance and Sustainability Cost Burden

Mounting regulatory and stakeholder expectations around environmental performance are creating significant cost pressures for the Australia meat processing industry. Processing facilities are substantial consumers of water and energy, and they generate considerable volumes of organic waste and wastewater that require careful treatment and management. Compliance with evolving environmental regulations, including requirements related to greenhouse gas emissions, effluent management, and waste reduction, demands continuous capital investment in infrastructure upgrades.

Exposure to Trade Policy Uncertainty and Market Access Risks

Australia’s heavy reliance on export markets for a substantial share of processed meat revenue creates inherent vulnerability to shifts in trade policy, tariff regimes, and geopolitical dynamics. Changes in market access conditions, the imposition of trade restrictions, or disruptions to diplomatic relationships with key importing nations can rapidly affect the commercial viability of export-oriented processing operations. Biosecurity risks, including the potential introduction of animal disease outbreaks, pose additional threats to market access by triggering import suspensions from critical trading partners.

Competitive Landscape:

The Australia meat processing market exhibits moderate-to-high concentration, with a small number of large, vertically integrated processors operating extensive multi-site facilities, alongside a broader base of regional and specialty processors. Competitive differentiation is increasingly driven by product quality, export accreditation, sustainability credentials, automation investment, and the breadth of branded product portfolios. Leading processors are channeling profits from record export performance back into facility expansions, renewable energy integration, and workforce development programs. Strategic partnerships with international retail and foodservice buyers are strengthening long-term supply relationships, while investments in digital traceability and food safety systems are reinforcing export market credentials across premium destinations globally.

Australia Meat Processing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Raw Cooked Meat, Precooked Meat, Fresh Processed Meat, Raw Fermented Sausages, Dried Meat, Others |

| Equipments Covered | Grinding Equipment/Mincer, Tenderizing Equipment, Cutting Equipment, Slicing Equipment, Smoking Equipment, Others |

| Meats Covered | Beef, Pork, Mutton, Others |

| Mode of Operations Covered | Manual, Semi-Automatic, Automatic |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Meat Processing Market Report

The Australia meat processing market size was valued at USD 500.18 Million in 2025.

The Australia meat processing market is expected to grow at a compound annual growth rate of 9.41% from 2026-2034 to reach USD 1,269.41 Million by 2034.

Fresh processed meat dominated the market with a share of 38.5%, driven by strong consumer preference for minimally processed, convenient, and protein-rich products that align with health-conscious and time-efficient modern lifestyles across Australian households.

Key factors driving the Australia meat processing market include rising domestic protein demand, robust global export growth supported by free trade agreements, accelerating adoption of automation and precision processing technologies, and strong government investment in food safety and processing infrastructure.

Major challenges include persistent labor shortages in regional processing facilities, rising operational and wage costs, increasing regulatory and compliance requirements around environmental sustainability, and the high capital expenditure required to implement advanced automated processing systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)