Australia Metal Coatings Market Size, Share, Trends and Forecast by Resin Type, Process, Technology, End Use Industry, and Region, 2026-2034

Australia Metal Coatings Market Summary:

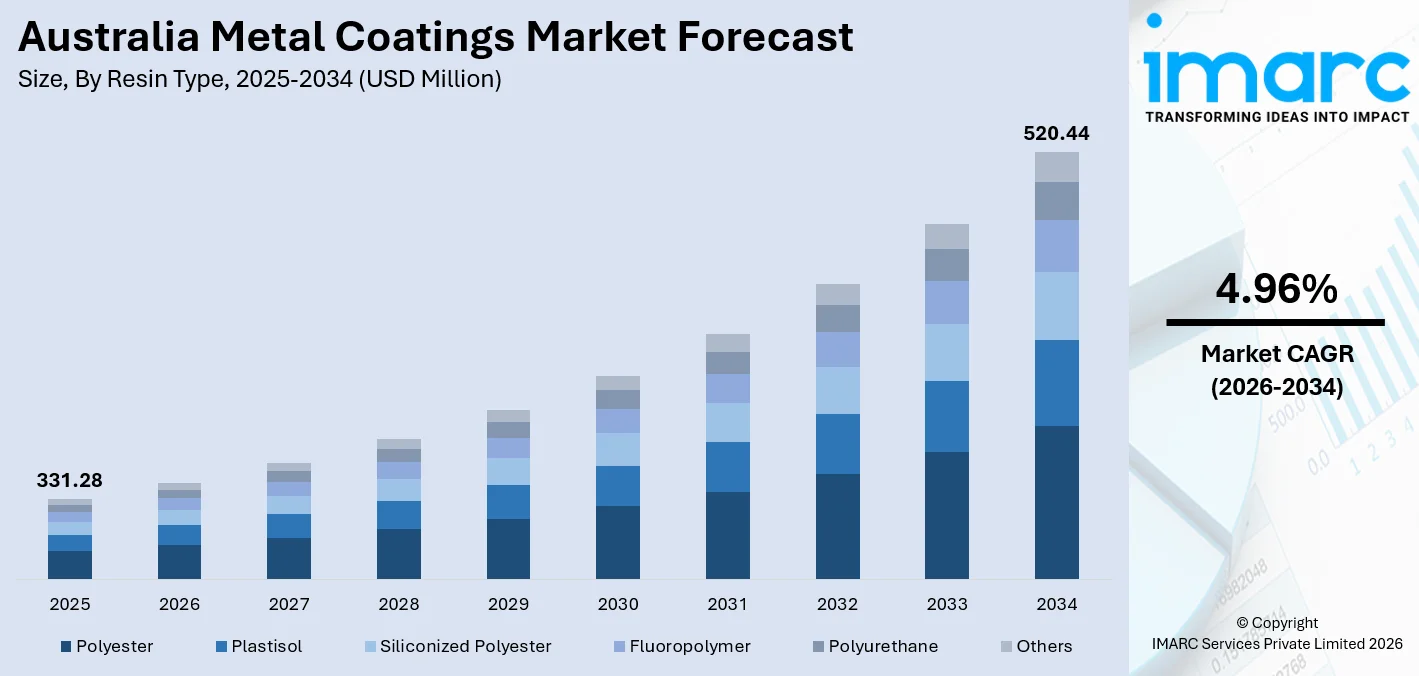

The Australia metal coatings market size was valued at USD 331.28 Million in 2025 and is projected to reach USD 520.44 Million by 2034, growing at a compound annual growth rate of 4.96% from 2026-2034.

The Australia metal coatings market is gaining strong momentum as the construction and mining sectors accelerate infrastructure development and demand corrosion-resistant solutions for long-term asset protection. Heightened environmental awareness is steering manufacturers toward low-volatile organic compound (VOC) formulations and water-based technologies, while advancements in nanotechnology and material science are enabling coating systems with self-healing, temperature-responsive, and extreme-condition-resistant properties. Tightening regulatory standards and the expanding renewable energy sector are reinforcing demand for high-performance metal coatings across diverse industrial applications, ultimately driving sustained growth in Australia metal coatings market share.

Key Takeaways and Insights:

- By Resin Type: Polyester leads the market with a share of 32.5% in 2025, owing to its cost-effectiveness, excellent weathering resistance, and broad compatibility with various metal substrates used across construction and industrial applications in Australia.

- By Process: Coil coating dominates the market with a share of 48.5% in 2025, reflecting its efficiency advantages in pre-finishing large metal volumes for roofing, cladding, and building envelope systems supplied across Australia's construction sector.

- By Technology: Liquid coating represents the largest segment with a market share of 58.5% in 2025, underpinned by its versatility, ease of application, and suitability for complex geometries across industrial, construction, and transport applications.

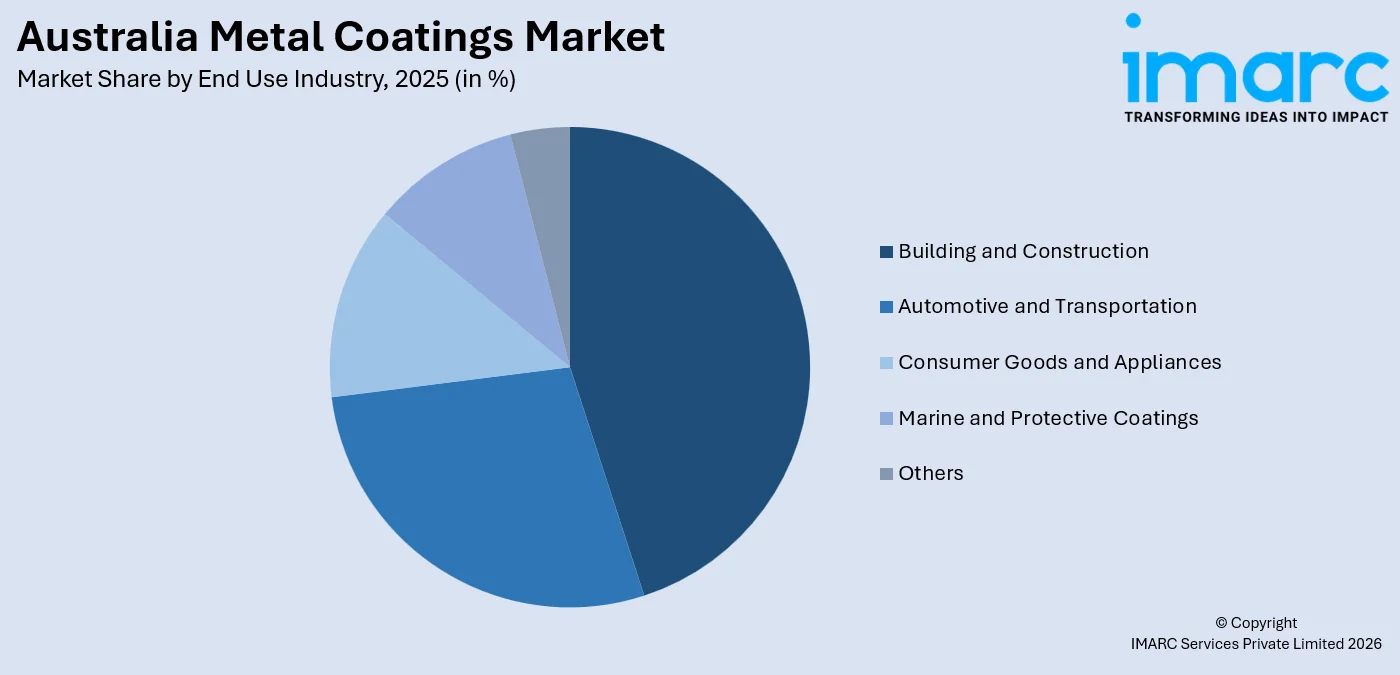

- By End Use Industry: Building and construction dominate the market with a share of 42.5% in 2025, driven by Australia's record infrastructure pipeline and strong residential and non-residential construction activity generating substantial demand for protective and decorative metal finishes.

- By Region: Australia Capital Territory & New South Wales leads the market with a share of 34.8% in 2025, reflecting the concentration of major construction projects, manufacturing activity, and industrial facilities in and around Sydney and Canberra.

- Key Players: The Australia metal coatings market is highly competitive, with leading manufacturers and specialty coating suppliers focused on expanding eco-friendly and low-VOC product lines, strengthening distribution networks across key industrial and construction hubs, and investing in advanced formulation technologies to deliver high-performance, regulatory-compliant solutions that sustain competitive advantage across the market.

To get more information on this market Request Sample

The Australia metal coatings market is advancing steadily, driven by the convergence of infrastructure expansion, environmental regulation, and material innovation. Sustained public and private investment in transport, utilities, and building projects is generating consistent demand for protective and decorative metal coatings across key industries. For instance, in October 2025, BASF Coatings expanded its distribution partnership with Wholesale Paint Group in South Australia to supply its Glasurit and baslac automotive refinish coating products, strengthening local availability of advanced coating technologies for industrial and automotive applications. Tightening VOC emission standards enforced by state environmental authorities are encouraging manufacturers to develop and commercialize waterborne and low-solvent formulations. At the same time, growing investments in renewable energy infrastructure, including solar, wind, and energy storage projects, are opening new end-use segments for corrosion-resistant and UV-stable metal coatings in challenging outdoor environments across Australia.

Australia Metal Coatings Market Trends:

Accelerating Shift Toward Low-VOC and Waterborne Formulations

Australia's progressive environmental regulations are compelling metal coatings manufacturers to replace solvent-based systems with low-VOC and waterborne alternatives. State-level emission standards for surface coatings have tightened steadily, driving industrial users across construction, manufacturing, and mining to adopt cleaner product portfolios. In January 2025, AkzoNobel launched its Interpon D Futura powder coatings collection in Australia and New Zealand, offering solvent-free architectural coatings with Environmental Product Declaration (EPD) certification and long-term durability designed to support sustainable construction practices. This regulatory shift is reshaping manufacturer research and development priorities, accelerating the commercialization of sustainable formulations, and positioning eco-friendly coatings as a central driver of Australia metal coatings market growth across diverse end-use applications.

Rising Adoption of Nanotechnology-Enhanced and Smart Coatings

Advances in material science are enabling the commercial development of next-generation metal coatings with self-healing, anti-microbial, and stimuli-responsive properties. These coatings are gaining traction in high-value applications including aerospace, marine infrastructure, and precision manufacturing, where minimizing maintenance intervals and extending asset lifespan deliver measurable cost benefits. For instance, in November 2025, Sparc Technologies partnered with Dulux Australia to apply a graphene-enhanced protective coating system at the Cape Jaffa Lighthouse in South Australia, demonstrating the real-world use of advanced graphene additives designed to improve corrosion resistance in harsh coastal environments. Growing academic and industry investment in functional coating technologies tailored for harsh Australian conditions is reinforcing demand for advanced performance solutions across industrial and infrastructure segments.

Expanding Demand Driven by Renewable Energy Infrastructure

Australia's accelerating transition to renewable energy is generating sustained demand for specialized metal coatings with exceptional UV resistance, corrosion protection, and long-term durability in remote and coastal environments. Solar photovoltaic installations, wind turbines, and battery energy storage systems require protective coatings on structural steel and metallic components exposed to extreme outdoor conditions. According to reports, in September 2025, the Western Australian Government supported a $5.31 million project by RCR Mining Technologies to expand local manufacturing of wind-turbine components at its Bunbury facility, including transition flanges used at the base of wind towers, strengthening Australia’s renewable energy supply chain. This emerging end-use segment is creating new growth opportunities for coatings manufacturers as green infrastructure investment expands across multiple states.

Market Outlook 2026-2034:

The Australia metal coatings market is poised for steady growth over the forecast period, supported by ongoing infrastructure development, accelerating urbanization, and the expanding renewable energy transition requiring durable protective coating solutions. Construction activity across key states will sustain demand for high-performance architectural and industrial finishes, while continued innovation in eco-friendly waterborne systems, nanotechnology-enhanced formulations, and advanced self-healing coatings will redefine competitive differentiation. Regulatory pressure on VOC emissions will further accelerate the adoption of sustainable coating solutions, reinforcing long-term market expansion across diverse industrial and commercial end-use segments. The market generated a revenue of USD 331.28 Million in 2025 and is projected to reach a revenue of USD 520.44 Million by 2034, growing at a compound annual growth rate of 4.96% from 2026-2034.

Australia Metal Coatings Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Resin Type |

Polyester |

32.5% |

|

Process |

Coil Coating |

48.5% |

|

Technology |

Liquid Coating |

58.5% |

|

End Use Industry |

Building and Construction |

42.5% |

|

Region |

Australia Capital Territory & New South Wales |

34.8% |

Resin Type Insights:

- Polyester

- Plastisol

- Siliconized Polyester

- Fluoropolymer

- Polyurethane

- Others

The polyester dominates with a market share of 32.5% of the total Australia metal coatings market in 2025.

Polyester resin coatings occupy the leading position due to their optimal balance of cost efficiency, UV durability, and broad compatibility across a wide range of metallic substrates. These coatings are extensively used in pre-coating applications for roofing panels, wall cladding, and structural components, where consistent weathering performance across Australia's diverse climatic zones is essential. Their wide compatibility with coil coating lines and cost advantage over premium fluoropolymer alternatives make polyester the preferred resin for high-volume architectural metal finishing.

The chemistry's proven durability and economic value directly address building material industry requirements for reliable performance at competitive pricing across standard architectural exposures. In construction applications, polyester-based systems deliver long-term corrosion and UV protection, a critical requirement for commercial and industrial projects in coastal and high-humidity environments. Ongoing resin technology advancements and pigment selection improvements continue to strengthen polyester performance characteristics, reinforcing its position as the central component of comprehensive metal coatings portfolios across Australia.

Process Insights:

- Coil Coating

- Extrusion Coating

- Hot-Dip Galvanizing

The coil coating leads with a share of 48.5% of the total Australia metal coatings market in 2025.

Coil coating's dominant position reflects its fundamental efficiency advantages for high-volume metal pre-finishing prior to fabrication. The continuous, automated process applies uniform primer and topcoat layers to steel and aluminium strips, enabling building product manufacturers to deliver consistently finished roofing, wall panels, and cladding components without the delays and variability of post-fabrication painting. Australia's growing pipeline of non-residential and infrastructure construction projects is sustaining strong demand for coil-coated metal products meeting stringent performance and aesthetic specifications.

Pre-coated metals produced through coil coating processes offer measurable lifecycle cost advantages, including reduced on-site labour, lower maintenance requirements, and longer protective warranties compared to field-applied alternatives. Building owners and developers increasingly specify factory-finished coil-coated products to standardize quality and compress project timelines. The process's compatibility with polyester, siliconized polyester, and fluoropolymer coating chemistries further extends its utility across a broad spectrum of architectural and industrial metal finishing applications throughout Australia.

Technology Insights:

- Liquid Coating

- Powder Coating

The liquid coating dominates with a market share of 58.5% of the total Australia metal coatings market in 2025.

Liquid coating technology commands the largest share due to its versatility in covering complex geometries, irregular surfaces, and large structural components across construction, automotive, and marine applications. Waterborne liquid coatings have particularly benefited from tightening environmental regulations, as manufacturers reformulate product lines to meet state-level VOC emission standards without compromising protective performance. Multi-coat liquid systems combining corrosion-inhibiting primers with durable topcoats provide comprehensive surface protection for metallic assets exposed to coastal salt spray, industrial chemicals, and elevated UV radiation.

The technology's adaptability to both spray and brush application methods makes it suitable for on-site maintenance and new construction applications alike, giving it broad relevance across diverse end-use industries. Continued investment in waterborne and high-solids liquid formulations is enabling performance parity with solvent-based systems at significantly reduced environmental impact. As regulatory pressure on VOC emissions intensifies, liquid coating technology is expected to maintain its dominant position while progressively shifting toward cleaner, more sustainable formulation platforms across the Australian market.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Building and Construction

- Automotive and Transportation

- Consumer Goods and Appliances

- Marine and Protective Coatings

- Others

The building and construction lead with a share of 42.5% of the total Australia metal coatings market in 2025.

The building and construction sector's leading position is underpinned by Australia's sustained investment in residential, commercial, and public infrastructure development. Both the public and private sectors are channeling significant resources into transport infrastructure, social housing, healthcare facilities, and energy transmission projects, all requiring protective and decorative metal coatings to extend the lifespan of structural steel, aluminium cladding, and roofing systems. The sector's demand for coatings with long-term corrosion and weathering performance is reinforcing the use of premium polyester and fluoropolymer formulations in pre-painted metal building components.

Construction activity across major urban centres and regional growth corridors is generating consistent procurement of coil-coated roofing, pre-finished cladding, and structural steel coatings. Non-residential and infrastructure segments are recovering strongly following a period of elevated input costs, with project pipelines extending across New South Wales, Queensland, and Western Australia sustaining above-trend volumes. The sector's requirements for both aesthetic appeal and long-term protective durability make it the most value-intensive end-use segment for high-performance metal coatings across Australia.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales exhibits a clear dominance with a 34.8% share of the total Australia metal coatings market in 2025.

New South Wales and the Australian Capital Territory represent the largest regional market, anchored by Sydney's position as Australia's principal economic and industrial hub and Canberra's role as a centre for government-funded infrastructure. The region hosts the highest concentration of commercial construction activity, manufacturing facilities, and major infrastructure projects in the country. Strong demand for protective and decorative metal coatings is generated across transport, utilities, and building sectors, with coastal exposure and urban density driving requirements for durable, corrosion-resistant coating systems.

Sustained public investment in transport infrastructure, social housing, and energy transmission is reinforcing demand for pre-coated metals and industrial coating solutions across New South Wales and the ACT. The region's dense industrial base and active construction project pipeline create consistent procurement volumes for both coil-coated architectural products and site-applied protective coating systems. New South Wales has also emerged as a focal point for renewable energy transmission infrastructure, further broadening the end-use base for high-performance metal coatings across the state and surrounding territories.

Market Dynamics:

Growth Drivers:

Why is the Australia Metal Coatings Market Growing?

Record Infrastructure Investment and Construction Activity

Australia's sustained investment in infrastructure is a primary structural driver of metal coatings demand. Ongoing public and private sector commitment to transport, utilities, social housing, and healthcare facilities is generating consistent procurement of coated structural steel, pre-painted roofing, and architectural cladding products. For instance, in June 2024, the New South Wales government approved the modernization of BlueScope Steel ’s Plate Mill at the Port Kembla Steelworks, a major project aimed at increasing steel production capacity to supply infrastructure, renewable energy, and defence sectors across Australia. State governments across New South Wales, Queensland, and Victoria are advancing substantial construction programs, sustaining above-trend demand for both architectural and protective metal coatings throughout the forecast period.

Expansion of Renewable Energy and Mining Sectors

Australia's accelerating renewable energy transition is creating a growing demand stream for metal coatings with superior UV resistance, anti-corrosion performance, and long-term structural integrity. Investment in utility-scale solar farms, wind projects, and high-voltage transmission infrastructure requires durable coatings for steel towers, substations, and cable trays in harsh outdoor environments. For instance, the Australian Energy Market Operator released its Integrated System Plan outlining major transmission expansion projects, including new high-voltage lines and renewable energy zones across multiple states to support large-scale wind and solar deployment. The mining sector further sustains demand for protective coatings on processing equipment, pipelines, and storage tanks exposed to abrasive and chemically aggressive operating conditions.

Technological Innovation in Eco-Friendly and High-Performance Coatings

Innovation in coating formulations is expanding the addressable market and improving the value proposition for Australian industrial users. The commercialization of waterborne, low-VOC, and UV-curable technologies enables manufacturers to meet tightening environmental regulations while maintaining protective performance. The Australian Paint Approval Scheme, overseen by government authorities with technical support from CSIRO, sets strict testing and certification standards for coatings used on bridges, fuel tanks, buildings, and industrial infrastructure to ensure durability and corrosion protection. Advances in nanotechnology are enabling self-healing, anti-microbial, and temperature-responsive coatings that reduce maintenance frequency and extend asset lifespans in corrosive environments, reinforcing long-term competitiveness across construction, mining, and renewable energy end-use segments.

Market Restraints:

What Challenges the Australia Metal Coatings Market is Facing?

Volatility in Raw Material and Input Costs

Metal coatings manufacturers rely heavily on petroleum-derived resins, solvents, and pigments whose prices fluctuate in line with global crude oil markets and chemical supply chains. Input cost volatility compresses manufacturer margins and creates pricing uncertainty across the supply chain, intensifying buyer pressure on coatings suppliers to absorb cost increases. This unpredictability poses ongoing challenges for production planning, contract pricing, and profitability across the industry.

Stringent and Evolving VOC Regulatory Requirements

While environmental regulation is a long-term market driver, the pace and cost of compliance reformulation present near-term operational challenges for coatings manufacturers. Meeting state-specific and national VOC emission thresholds requires significant ongoing research and development investment to reformulate established solvent-based product lines without compromising protective performance. Smaller regional manufacturers face disproportionate compliance burdens, potentially consolidating market share toward larger players capable of absorbing reformulation costs at scale.

Intense Competition and Market Consolidation Pressure

The Australia metal coatings industry operates in a highly competitive environment, with global multinationals leveraging integrated supply chains and broad product portfolios to compete aggressively on price and technical performance. Ongoing consolidation among major manufacturers is reducing the competitive space for independent operators and placing sustained downward pressure on margins. Smaller domestic players face increasing difficulty differentiating their offerings against well-resourced international competitors across key industrial and construction segments.

Competitive Landscape:

The Australia metal coatings market is characterized by a competitive blend of global multinationals and regionally focused players competing on product performance, sustainability credentials, and distribution reach. Leading manufacturers are actively investing in low-VOC product development, expanding eco-certified coating ranges, and strengthening technical service capabilities to meet tightening regulatory requirements and evolving customer specifications. Strategic partnerships, acquisitions, and technology licensing agreements are shaping competitive positioning across the market. New entrants with specialized nano-coating and functional coating technologies are increasingly targeting premium industrial and renewable energy segments, intensifying competition and driving further innovation throughout the industry.

Recent Developments:

- In August 2025, AkzoNobel inaugurated a new Automotive Training Centre in Port Melbourne, Australia to support body shops and technicians using advanced automotive coatings. The facility provides training on modern refinishing technologies, color matching, and sustainable coating solutions, strengthening the company’s technical service network in the region.

Australia Metal Coatings Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Resin Types Covered | Polyester, Plastisol, Siliconized Polyester, Fluoropolymer, Polyurethane, Others |

| Processes Covered | Coil Coating, Extrusion Coating, Hot-Dip Galvanizing |

| Technologies Covered | Liquid Coating, Powder Coating |

| End Use Industries Covered | Building and Construction, Automotive and Transportation, Consumer Goods and Appliances, Marine and Protective Coating, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Metal Coatings Market Report

The Australia metal coatings market size was valued at USD 331.28 Million in 2025.

The Australia metal coatings market is expected to grow at a compound annual growth rate of 4.96% from 2026-2034 to reach USD 520.44 Million by 2034.

Coil coating, holding the largest segment share of 48.5%, is critical to Australia's metal coatings market, enabling high-efficiency pre-finishing of steel and aluminium for roofing, cladding, and architectural building products supplied across the construction sector.

Key factors driving the Australia metal coatings market include expansion of renewable energy and mining sector demand, tightening environmental regulations accelerating adoption of eco-friendly waterborne coatings, and ongoing technological innovation in nanotechnology-enhanced and high-performance protective coating formulations.

Major challenges include volatility in petroleum-derived raw material costs, the compliance burden of evolving VOC emission regulations requiring ongoing product reformulation investment, and intense competitive pressure from global multinationals consolidating market share through strategic acquisitions across Australia's coatings sector.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)