Australia Modular Construction Market Size, Share, Trends and Forecast by Type, Module Type, Material, End Use, and Region, 2026-2034

Australia Modular Construction Market Size & Forecast 2026-2034

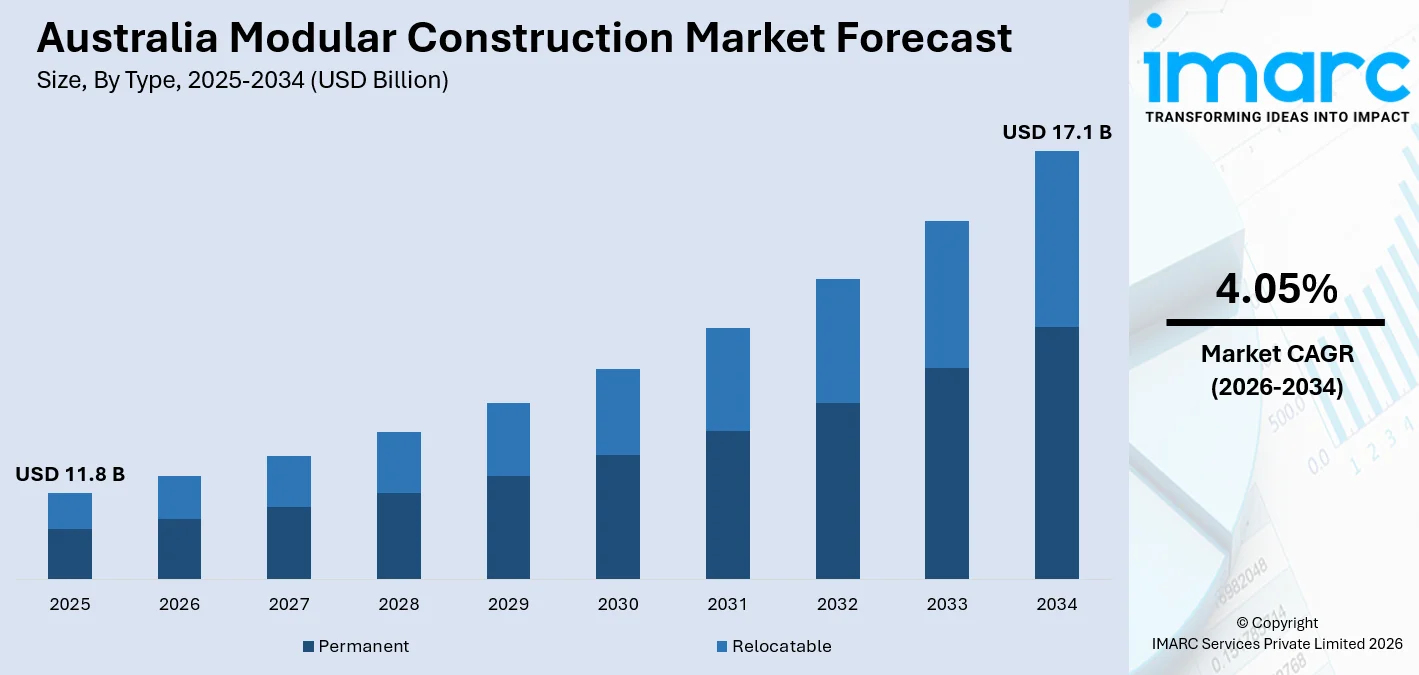

The Australia modular construction market was valued at USD 11.8 Billion in 2025 and is expected to grow to USD 17.1 Billion by 2034 at a CAGR of 4.05% during the forecast period from 2026-2034. This is because of the increasing demand for fast, efficient, and environmentally friendly building techniques. In 2025, the Australian Government pledged over AUD 32 billion to its Housing Australia Future Fund and other related housing programs, thus boosting the adoption of prefabricated and modular constructions to address the Australian housing shortage.

To get more information on this market Request Sample

Australia Modular Construction Industry Analysis- Key Insights

- Permanent leads type at 54.0% in 2025 - the durability and long-term cost advantages of permanent modular structures make them the preferred choice for commercial, residential, and institutional applications across Australia.

- Four sided leads module type at 29.0% in 2025 - fully enclosed four-sided modules offer superior structural integrity and thermal performance, making them dominant for multi-story residential and commercial modular builds.

- Steel leads material at 42.0% in 2025 - steel's high strength-to-weight ratio, design flexibility, and compatibility with multi-story modular construction solidify its position as the leading structural material in the Australian market.

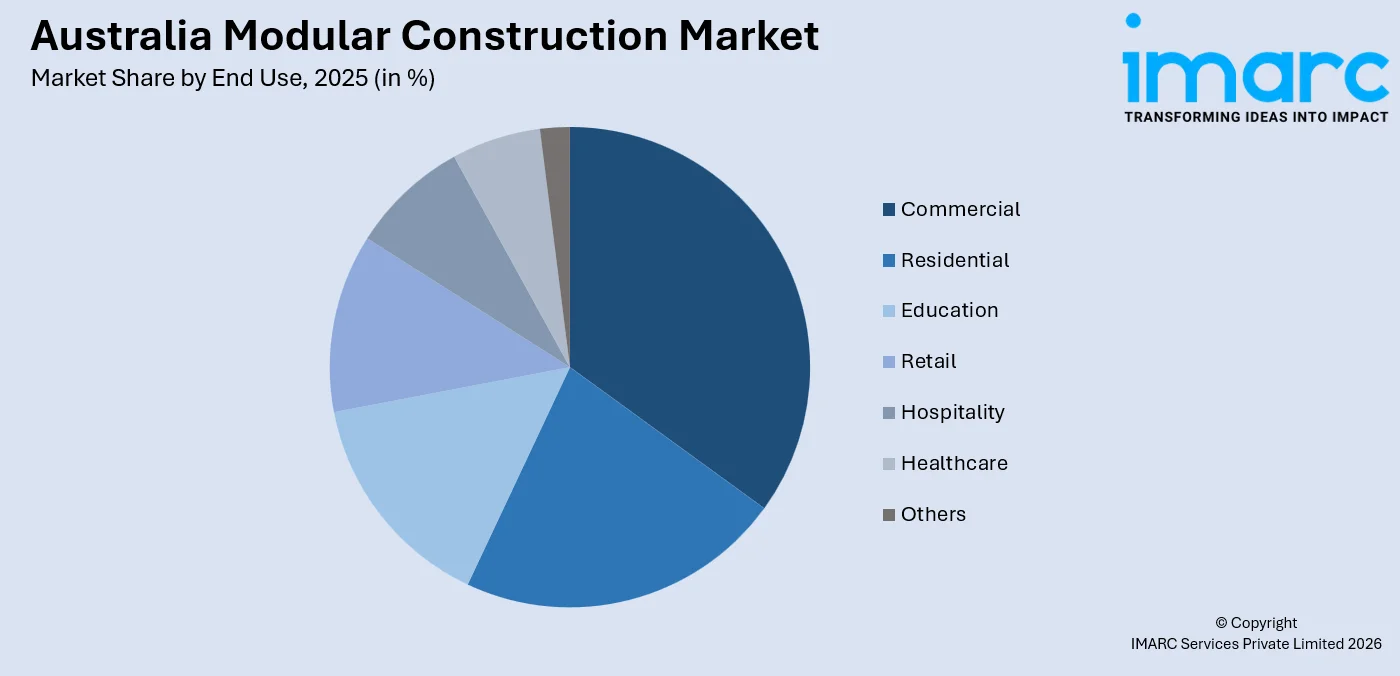

- Commercial leads end use at 32.0% in 2025 - robust demand for modular offices, retail fit-outs, and hospitality facilities is driving strong commercial sector uptake of modular construction across Australian urban centres.

- Australia Capital Territory & New South Wales leads regionally at 36.0% in 2025 - the concentration of major infrastructure projects, strong housing demand, and a well-established construction ecosystem in NSW and ACT anchor the region's leading market position.

Australia Modular Construction Market Trends and Dynamic 2026

Market Trends

Government housing programs are accelerating modular construction adoption

Australia's escalating housing affordability crisis has prompted unprecedented government investment in alternative construction methods, with modular building emerging as a key delivery mechanism. Federal and state governments are actively incorporating modular procurement into their housing programs to reduce build times and lower per-unit costs. In 2020, the Victorian Government launched its Big Housing Build initiative with dedicated funding allocations for modular social housing, reinforcing policy-led demand across the sector.

Sustainability mandates and green building codes are reshaping modular design standards

Australia's environmental regulations through the National Construction Code's 2022 and 2025 updates have encouraged modular manufacturers to opt for low-carbon materials, green design strategies, and circular construction practices. Modular building companies are now incorporating cross-laminated timber, recycled steel, and passive house strategies into their product offerings to achieve 7-star NatHERS ratings. Fleetwood Australia and Hickory Group, two of the industry leaders, have stepped up investments in sustainable module configurations to match procurement requirements from institutions.

- Digital Engineering Integration: Increased usage of digital twin technology and BIM, which helps improve precision in modular construction, manufacture, and assembly coordination.

- Hybrid Construction Approaches: Increased demand for hybrid construction methods, which incorporate both modular volumetric construction systems and traditional construction methods, particularly in mixed-use developments.

- Remote and Resource Sector Demand: Increased demand for modular construction solutions in remote mining, energy, and defence sectors, which require self-contained accommodation solutions.

- Healthcare and Aged Care Expansion: Expansion of modular healthcare facilities, as well as aged care facilities, driven by ageing population statistics and government-funded aged care infrastructure programs undertaken by state governments.

Growth Drivers

Chronic housing shortage and affordable housing policy investment

Australia's undersupplied housing stock, particularly in its major metropolitan markets, continues to drive demand for modular and prefabricated building as a faster method of delivery. The National Housing Accord aims to achieve 1.2 million homes in the next five years from July 2024 to June 2029. This is a huge volume requirement that traditional building methods alone are unable to achieve. The capacity for faster delivery by reducing build times by significantly over traditional building methods makes modular building a vital component in the Australian Government's drive for housing delivery and subsequent long-term market growth.

Strong commercial and infrastructure sector pipeline

Australia has a healthy construction pipeline of commercial building projects, such as office parks, retail precincts, hotels, and educational facilities, which are consistently requiring modular solutions with shorter delivery periods and minimized site disturbance. The federal government has committed to a ten-year, over AUD 120 billion infrastructure investment program, with significant funding allocated towards schools, hospitals, and community infrastructure projects, many of which are now incorporating modular solutions as part of their delivery strategy. Permanent modular construction is being utilized by commercial developers to fast-track time to revenue for hotel, student accommodation, and build-to-rent projects.

- Labour Market Constraints: The increasing cost competitiveness of factory-built modular construction, which requires fewer site workers, is driven by the skilled labour market constraints in the traditional construction market.

- Cost Efficiency Imperatives: The increase in cost of holding land in urban areas is driving developers to seek faster construction periods to reduce holding costs, which aligns with the cost advantages of modular construction’s accelerated delivery model.

- Institutional Investment Flows: The increased institutional investment flows in build-to-rent and social housing are driving demand for repeatable modular construction products.

- Defence Infrastructure Programs: The extension of Australia’s defence infrastructure investment program under the AUKUS agreement is driving demand for modular construction for remote bases, training facilities, and temporary accommodation.

Market Restraints

High costs of manufacturing and transporting modules: The capital cost of setting up modular manufacturing facilities, as well as the cost of transporting large modules to remote locations, remains high and affects profitability for businesses in Australia.

Planning and regulatory fragmentation: The lack of a unified regulatory framework for the certification of modular buildings at a national level leads to regulatory complexities in meeting building codes and obtaining regulatory approvals in Australia. There are also inconsistencies in state building codes, local council planning requirements, and off-site construction requirements for modular buildings.

Perception issues for consumers and developers: The ongoing perception issues for some segments of developers and consumers regarding the quality, flexibility, and resale values of modular buildings continue to act as barriers to market adoption of modular buildings in Australia. These perception issues are driven by historical preferences for traditional construction in high-end residential and commercial buildings.

Australia Modular Construction Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Permanent | 54.0% | 2025 |

| Module Type | Four Sided | 29.0% | 2025 |

| Material | Steel | 42.0% | 2025 |

| End Use | Commercial | 32.0% | 2025 |

| Region | Australia Capital Territory & New South Wales | 36.0% | 2025 |

Type Insights

Permanent- 54.0% Market Share (2025) | Leading Type

Permanent modular construction accounts for a majority share in the Australian market due to a strong appetite for permanent modular solutions from commercial developers, government housing initiatives, and institutional clients who require long-life buildings with a complete lifespan expectancy. Permanent modules provide the same planning approval benefits as conventional buildings while offering considerable benefits during the construction phase. Hickory Group and Lendlease Modular, prominent operators in Australia, have utilized permanent volumetric construction for multi-storey residential and hospitality facilities in Melbourne and Sydney cities.

|

Segment Breakdown Permanent (54.0%) · Relocatable |

Module Type Insights

Four Sided- 29.0% Market Share (2025) | Leading Module Type

Four-sided modules are dominant in the Australian market, driven by their structural completeness, thermal and acoustic performance, and ability to be stacked in multi-storey configurations for residential and commercial sectors. The fully enclosed module type also assists in achieving maximum factory completion, which in turn facilitates a greater level of fit-out, such as bathroom pods, kitchen installations, and mechanical services, to be completed in a factory-controlled environment. This is particularly beneficial in Australia, where construction environments are subject to diverse climatic conditions.

|

Segment Breakdown Four Sided (29.0%) · Open Sided · Partially Open Sided · Mixed Modules and Floor Cassettes · Modules Supported by a Primary Structure · Others |

Material Insights

Steel- 42.0% Market Share (2025) | Leading Material

Steel is the dominant material for structural purposes in the modular construction industry in Australia, with its high strength-to-weight ratio, flexibility in design, and successful in-service performance in volumetric multi-story applications contributing to its popularity. Its ability to accommodate factory production methods, including precise cutting and welding technology, is allowing for high standards of repeatability and quality control in modular construction products. In addition, the increasing availability of recycled steel and galvanized steel is providing a further boost to the alignment of steel modular construction with the increasing green building standards in Australia.

|

Segment Breakdown Steel (42.0%) · Concrete · Wood · Plastic · Others |

End Use Insights

Access the comprehensive market breakdown Request Sample

Commercial- 32.0% Market Share (2025) | Leading End Use

The commercial sector is the dominant sector in the Australian modular construction industry and includes offices, retail spaces, hospitality spaces, and mixed-use developments where the benefits of faster programme delivery and minimal disruption to the surrounding occupied areas are highly valued. Commercial clients are increasingly specifying the use of modular construction for build-to-rent apartment buildings, hotel and serviced apartment projects, and office spaces where the need for time-to-revenue generation makes the cost premium associated with off-site construction viable. In 2024, Marriott International completed several modular hotel projects across Asia-Pacific, citing programme savings of up to eight months compared to conventional construction.

|

Segment Breakdown Commercial (32.0%) · Residential · Education · Retail · Hospitality · Healthcare · Others |

Regional Insights

Australia Capital Territory & New South Wales- 36.0% Market Share (2025) | Leading Region

New South Wales and the Australian Capital Territory collectively represent the largest regional market for modular construction in Australia, driven by the concentration of major infrastructure investment, strong population growth, and Sydney's position as the country's primary commercial construction market. The NSW Government's Social and Affordable Housing programs and the Canberra-based Commonwealth Government's infrastructure pipeline are generating significant procurement volumes for modular solutions. Sydney's high land costs and dense urban environment further incentivise modular construction's reduced on-site footprint and accelerated delivery model.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

36.0%

|

|

Key States

|

NSW, ACT (Canberra) |

|

Major Growth Drivers

|

Government housing programs, commercial construction pipeline, high urban density, infrastructure investment |

|

Outlook

|

Largest and most active modular construction market in Australia |

|

Segment Breakdown Australia Capital Territory & New South Wales (36.0%) · Victoria & Tasmania · Queensland · Northern Territory & Southern Australia · Western Australia |

Victoria & Tasmania:

Victoria is the second-largest modular construction market in Australia, supported by Melbourne's strong residential development pipeline and the Victorian Government's Big Housing Build program, which is actively deploying modular construction to deliver social and affordable housing at scale. Tasmania's growing tourism infrastructure investment is creating emerging demand for modular hospitality and accommodation facilities.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Melbourne, Geelong, Hobart |

|

Major Growth Drivers

|

Social housing programs, residential growth, tourism infrastructure, manufacturing capability |

|

Outlook

|

High-growth market supported by government procurement |

Queensland:

Queensland's modular construction market is expanding rapidly, driven by strong population growth in South East Queensland, the 2032 Brisbane Olympics infrastructure pipeline, and significant resource sector accommodation demand in regional Queensland mining and energy precincts. The state's warm climate and dispersed settlement pattern create strong demand for relocatable and permanent modular facilities.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Brisbane, Gold Coast, Townsville, Mackay |

|

Major Growth Drivers

|

Olympics 2032 infrastructure, resource sector accommodation, population growth, healthcare expansion |

|

Outlook

|

Fast-growing market with major event and resource sector catalysts |

Northern Territory & Southern Australia:

The Northern Territory's remote geography and defence infrastructure investment under the AUKUS agreement create strong structural demand for modular construction. South Australia's growing defence and renewable energy sectors, combined with Adelaide's residential housing demand, are supporting market expansion in the region.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Darwin, Adelaide, remote mining and defence sites |

|

Major Growth Drivers

|

Defence infrastructure, remote accommodation, renewable energy projects, housing affordability |

|

Outlook

|

Defence and resources-driven growth |

Western Australia:

Western Australia's modular construction market is anchored by the state's large resource sector, which requires high volumes of relocatable and permanent modular accommodation in remote Pilbara, Kimberley, and goldfields locations. Perth's strong residential market and the state government's social housing investment are contributing to growth in the permanent modular segment.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Perth, Pilbara region, Goldfields, Kimberley |

|

Major Growth Drivers

|

Mining accommodation, resource project infrastructure, residential housing, government programs |

|

Outlook

|

Resource sector-anchored with growing residential demand |

Market Outlook 2026-2034

What is the future outlook of the Australia modular construction market?

The Australia modular construction market is expected to sustain steady revenue growth through 2034.

The Australian modular construction industry is set to sustain its growth trajectory over the forecast period from 2026 to 2034, with the market being driven by underlying structural trends such as the chronic undersupply of housing, rising infrastructure investment pipeline, and increased government policy support for modular construction methods. The Australian modular construction industry will witness rising technology and quality standards with the advancement of information technologies in building information modeling, automation in the fabrication of modules, and the development of superior quality modular connections systems, which will sustain the cost competitiveness of the industry over the forecast period. The convergence of labor markets, environmental pressures, and institutional capital flows into the residential and commercial property sectors will sustain the market penetration of the Australian modular construction industry across all states and territories through the forecast period to 2034.

Australia Modular Construction Market: Leading Key Players

The Australian market for modular construction comprises a competitive landscape of specialized manufacturers, large construction companies with specialized modular businesses, and new technology-centric companies. The key players in this market are enhancing their market positions by investing in manufacturing capacity, design innovation, winning government contracts, and forging partnerships with institutional developers and housing associations.

| Company | Leading Brands | Highlights |

|---|---|---|

| Hickory Group | Hickory Modular | Pioneer in high-rise modular construction; delivered Australia's first tall modular residential building in Melbourne |

| Modscape | Modscape | Award-winning modular design specialist; strong focus on bespoke residential and hospitality modular projects |

| Fleetwood Australia | Fleetwood, Moduline | Leading provider of modular buildings for education, mining, and government sectors across Australia |

Some of the other major players in the market include Lendlease, Ausco Modular, Quickbuilt, Moduline, Portable Buildings Australia, etc.

Latest Development & News

- In December 2025, Hickory announced partnering with Build Home, in launching their brand-new state-of-the-art facade manufacturing precinct in China, a very significant milestone in our longstanding partnership relationship. This new precinct is set to supercharge Hickory’s facade manufacturing capabilities, not only making buildings better but also making them more affordable for our customers, thereby speeding up much-needed projects in Australia. This precinct is 44,000 m² in area, includes a state-of-the-art manufacturing facility with the latest in robotics and fabrication technology, and a 10-storey office tower housing an international talent pool focused on facade manufacturing and delivery.

- In May 2025, the Australian Government's National Housing Supply and Affordability Council released its State of the Housing System report, recommending accelerated adoption of modular and prefabricated construction methods to address the national shortfall and reduce construction timelines for social and affordable housing projects.

- In February 2025, an application was lodged with the NSW Government for a $1.5 billion build-to-rent development in the inner west Sydney suburb of Marrickville. If approved, almost 1,200 homes, including 115 affordable homes, will be constructed on the site of the former timber yard, which will add to the demand for modular building.

Australia Modular Construction Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Permanent, Relocatable |

| Module Types Covered | Four Sided, Open Sided, Partially Open Sided, Mixed Modules and Floor Cassettes, Modules Supported by a Primary Structure, Others |

| Materials Covered | Steel, Concrete, Wood, Plastic, Others |

| End Uses Covered | Residential, Commercial, Education, Retail, Hospitality, Healthcare, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia modular construction market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia modular construction market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia modular construction industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Modular Construction Market Report

The Australia modular construction market was valued at USD 11.8 Billion in 2025.

The Australia modular construction market is anticipated to reach a value of USD 17.1 Billion by 2034.

Permanent dominates the market with a share of 54.0%, driven by strong demand from government housing programs, commercial developers, and institutional clients seeking durable, long-lifecycle modular structures with full building code compliance.

Steel commands the market with a share of 42.0%, reflecting its superior structural performance, compatibility with factory fabrication processes, and suitability for multi-storey modular construction across residential and commercial applications.

Some of the major players in the Australia modular construction market include Hickory Group, Modscape, Fleetwood Australia, Lendlease, Ausco Modular, Quickbuilt, Moduline, Portable Buildings Australia, and several other regional and national manufacturers and contractors.

Key trends include the government-mandated acceleration of modular housing delivery to address Australia's housing shortage, increasing integration of BIM and digital manufacturing technologies, growing adoption of sustainable materials and low-carbon module designs aligned with NCC 2025 energy standards, and the expansion of high-rise modular construction techniques for urban residential and commercial applications.

Australia Capital Territory & New South Wales currently leads the Australia modular construction market, accounting for a share of 36.0%. The region benefits from concentrated infrastructure investment, strong commercial construction activity, government housing program funding, and the presence of major modular contractors across Sydney and Canberra.

Growth is driven by the National Housing Accord's ambitious housing delivery targets, escalating construction labour shortages making factory manufacturing increasingly cost-competitive, strong government procurement of modular social and affordable housing, a robust commercial infrastructure pipeline across all states, and rising institutional investor appetite for build-to-rent assets constructed using modular methods.

Challenges include high capital costs associated with establishing and maintaining modular manufacturing facilities, fragmented state-based building regulation creating compliance complexity, ongoing consumer and developer perception gaps regarding modular building quality and resale value, and logistical constraints around the transportation of oversized modules to remote and constrained urban sites.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)