Australia Online Grocery Market Size, Share, Trends and Forecast by Product Type, Business Model, Platform, Purchase Type, and Region 2026-2034

Australia Online Grocery Market Size & Forecast 2026-2034

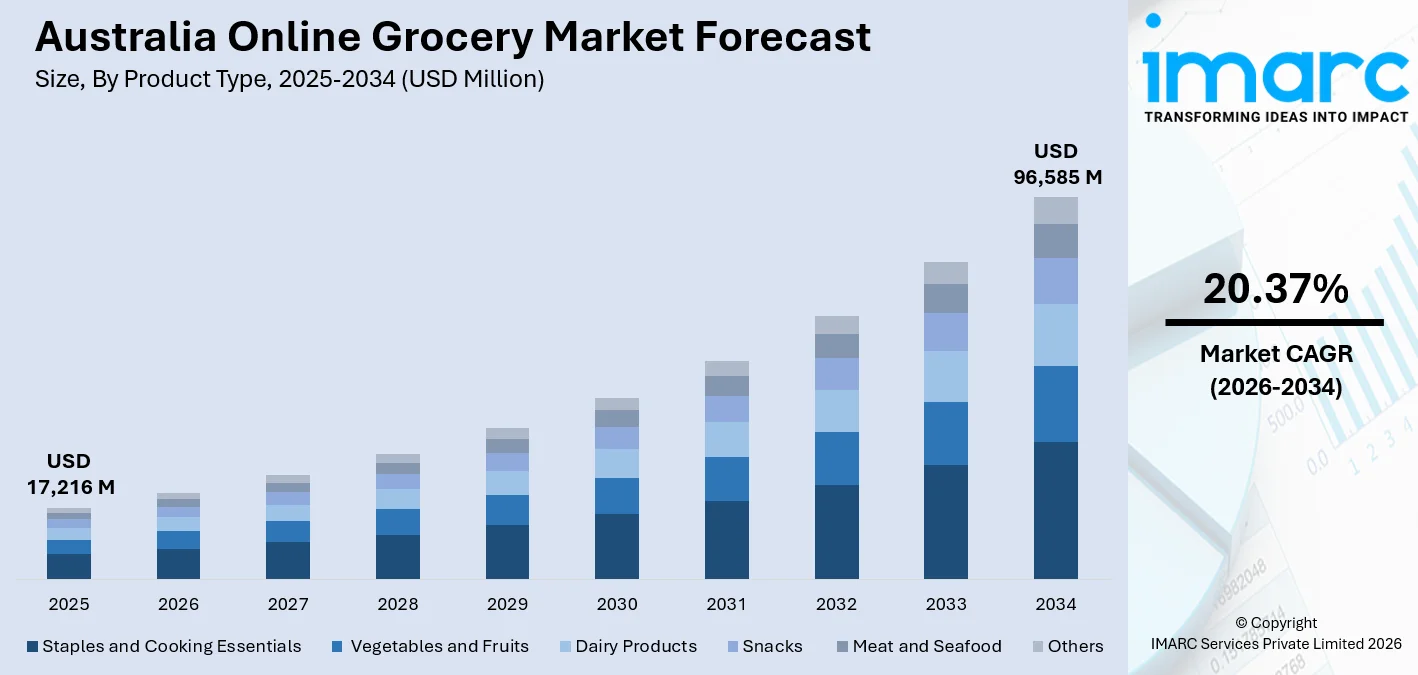

The Australia online grocery market size stood at USD 17,216 Million in 2025 and is projected to hit USD 96,585 Million by 2034, advancing at a CAGR of 20.37% through 2026-2034. A predominantly mobile-oriented consumer base continued capital deployment into automated fulfilment infrastructure across Sydney and Melbourne, and the broad-based adoption of application-driven grocery procurement are collectively transforming the way Australian households manage their essential purchasing. Woolworths Group’s online food sales exceeded AU$ 9.1 billion in FY2025 alone, a figure that reflects not merely the scale of digital channel growth, but the velocity at which consumer engagement is transitioning from physical retail environments to digital platforms, helping consolidate the Australia online grocery market share.

To get more information on this market Request Sample

Australia Online Grocery Industry Analysis Key Insights

- Staples and cooking essentials account for 25.8% by product type in 2025, representing the category’s most enduring structural position within the channel. This segment’s dominance is grounded in habitual replenishment behavior, as households consistently restock foundational items such as rice, cooking oil, and pasta on a recurring basis, which explains why no discretionary category has meaningfully displaced it from the leading position

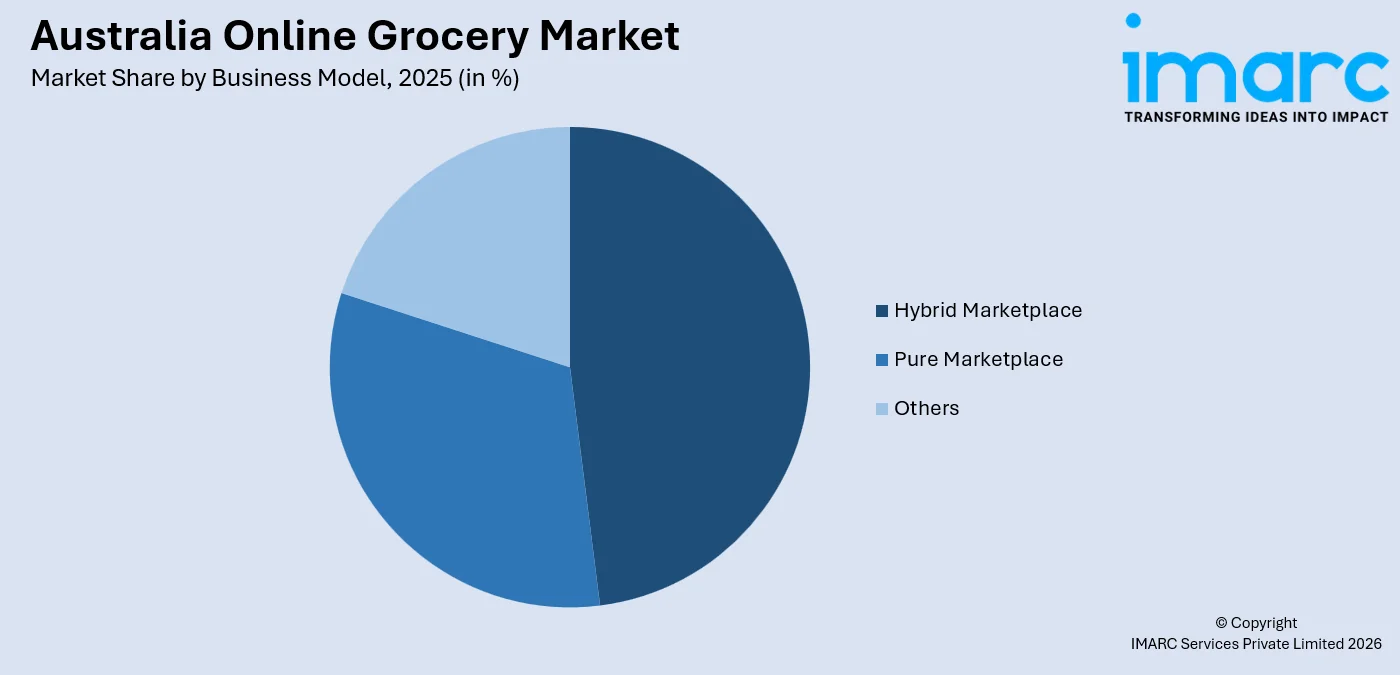

. - Hybrid marketplace controls 47.2% of the business model in 2025; with nearly half of the market having converged on this dual-architecture format, wherein first-party inventory and third-party seller listings coexist within a unified platform environment. This configuration affords consumers access to a broader product range, while enabling platform operators to achieve meaningful margin diversification structural advantage that pure-play online models have consistently struggled to replicate at comparable scale.

- App-based platforms own 62.4% of the platform in 2025, representing a decisive market position that reflects the depth of mobile integration within Australian consumer behavior. With more than nine in ten Australians carrying smartphones, and with supermarket applications offering personalized promotional content alongside streamlined reordering functionality, the web-based grocery experience has increasingly become a secondary channel preference.

- One-time accounts for 65.7% of purchase type in 2025. This indicates that most online grocery shoppers preferred to make independent, one‑off transactions rather than opting for recurring or subscription‑based services, reflecting a tendency among Australian consumers to shop as needs arise rather than committing to regular delivery plans. The prevalence of one‑time purchases underscores the importance of flexibility and convenience in the market, as shoppers increasingly seek to order groceries online without long‑term commitments, driven by busy lifestyles and the ease of browsing digital platforms for individual orders.

- Australia Capital Territory & New South Wales leads regionally at 34.5% in 2025, reflecting the compounding advantages conferred by Sydney’s population density and the concentration of automated fulfilment infrastructure within this region. While New South Wales maintains a structural lead, the margin relative to Victoria is progressively narrowing as Melbourne’s dark store network and Customer Fulfilment Centre development continues to advance through 2025 and the years ahead.

Australia Online Grocery Market Trends and Dynamic 2026

Market Trends

Mobile-first grocery procurement has transitioned from an emerging trend to the established behavioral norm.

What originally emerged as a pandemic-era convenience measure has since crystallized into a permanent behavioral pattern. Australian consumers now hold clear expectations that their preferred supermarket application will retain their purchasing preferences, surface contextually relevant promotional offers, and provide delivery confirmation within defined two-hour windows—often before their morning routines have concluded. Woolworths’ Everyday Rewards program recorded 10.2 million active members as of February 2025, representing more than half of the nation’s adult population, which positions loyalty-integrated application engagement as the most consequential customer retention mechanism currently operating within the market.

Purpose-built dark stores and automated Customer Fulfilment Centers are fundamentally reconfiguring the economics of grocery delivery operations.

Leading Australia edible grocery market retailers are systematically reducing their cost-per-order through a strategically deployed network of purpose-engineered fulfilment nodes, spanning large-scale suburban Customer Fulfilment Centers through to compact urban micro-warehouses. The commissioning of Coles’ Witron-powered automated facility in Truganina, Victoria, in November 2024, unlocked capacity for tens of thousands of automated daily order picks at a substantially reduced operational cost relative to conventional in-store fulfilment methods. Capital committed to such infrastructure effectively converts delivery from a cost-center function into a sustainable competitive differentiator, positioning it as essential to preserving growth momentum in Australia’s online grocery sector following the initial acceleration of digital channel adoption.

Environmental responsibility is evolving from brand-level messaging into quantifiable operational commitment across logistics networks.

For an extended period, sustainability in grocery retail was largely confined to the adoption of recyclable packaging materials. This baseline is changing in a very real and palpable way. In March 2025, Amazon Australia’s Melbourne sort center became the first facility in Australia to earn a zero-carbon certification. The company is striving to more fully integrate electric vehicles into its logistics networks. The above path indicates that sustainability is beginning to inform last-mile logistics strategies and raise the bar for competition within the industry. These rising standards are increasingly being incorporated into procurement strategies and are influencing the buying habits of eco-conscious urban consumers within Australia’s online grocery market.

- Subscription Delivery Pass Expansion: In an effort to increase purchase frequency and combat platform churn, both Woolworths and Coles are actively pursuing conversion strategies that aim to convert one-off buyers into loyal delivery pass subscribers.

- AI-Driven Basket Personalization: Advanced product recommendation engines are leveraging machine learning capabilities to surface contextually appropriate items at the most relevant junctures within the consumer purchasing journey.

- Quick Commerce (Q-Commerce) Emergence: Within the metropolitan regions of Sydney and Melbourne, on-demand grocery delivery within a sub-two-hour window is moving from a high-end service proposition to an expected service proposition within the overall service fulfillment mix.

- Voice and Smart Home Commerce: Time-constrained metropolitan living is showing early signs of adoption with smart speaker-enabled grocery reorder features, further expanding the potential user touchpoints beyond screen-based interfaces.

Growth Drivers

Australia’s digital infrastructure is particularly well-suited to sustaining high-frequency online grocery engagement across the population.

Very few markets globally present the confluence of near-universal broadband connectivity, high rates of smartphone ownership, and a mature digitized payments infrastructure that characterizes the Australian environment. As of February 2026, the country counted 25.94 million active internet users equivalent to 96.7% of the population, with mobile sessions outnumbering desktop across every retail category. This foundational capability does not merely facilitate online grocery participation; it systematically removes the friction points that have historically impeded digital channel adoption among older and less technologically engaged demographic groups.

Capital investment directed toward fulfilment automation is materially expanding delivery capacity across the national network.

The strategic commitment by Australia’s two dominant grocery retailers to robotics-driven fulfilment carries implications that extend well beyond the immediate operational context. Woolworths Group’s commitment to its Moorebank Customer Fulfilment Centre in Sydney confirmed in June 2025 targets processing over 60,000 online orders per week from a single site. Processing capacity of this magnitude fundamentally reconfigures the unit economics of online grocery operations and provides the quantitative foundation for the sustained positive Australia online grocery market forecast.

The premium placed on time efficiency by Australian consumers positions online grocery as one of the most direct expressions of this behavioral priority.

The prevalence of dual income families has also lengthened urban commute times, while the rapid normalization of flexible work arrangements has helped to raise the importance of convenience as a genuinely material economic factor for Australian consumers. Australia Post's 2025 Annual eCommerce Report found that Australians had spent a historic $69 billion on online purchases in 2024, with food and beverages being a major category that accounted for $13.6 billion of those online expenditures.

- Frictionless Digital Payments: The widespread integration of digital wallet solutions, contactless payment functionality, and buy-now-pay-later platforms has effectively eliminated the checkout-related hesitation that previously impeded new consumer conversion to online grocery channels.

- Post-Pandemic Behavioral Lock-In: A significant proportion of Australian consumers who first engaged with online grocery services during COVID-related restrictions did not subsequently revert to exclusively in-store purchasing behaviors, resulting in a retained customer base that continues to demonstrate increasing order frequency and expanded basket values over time.

- Millennial and Gen Z Household Formation: As digitally native generational cohorts assume primary household purchasing responsibilities, application-first retail engagement becomes the expected default rather than an alternative approach. This generational transition provides a durable long-term structural tailwind for the continued expansion of online grocery channels.

- Cold-Chain Technology Maturation: Ongoing advancements in insulated packaging solutions and temperature-controlled vehicle fleets have rendered fresh produce and chilled product categories viable at meaningful scale through digital channels, thereby unlocking access to the highest-margin product segments for online channel development.

Market Restraints

Delivery economics that do not yet pencil out beyond metro zones: In a market environment where physical supermarkets retain strong accessibility, last-mile grocery delivery continues to impose significant operational costs, while consumers demonstrate persistent resistance to absorbing meaningful delivery fee charges. Even the most well-capitalized operators encounter considerable difficulty in substantiating the commercial rationale for regular home delivery services beyond established metropolitan catchment areas, which materially constrains both network expansion timelines and near-term profitability improvement trajectories.

Fresh produce trust remains a stubborn conversion barrier: A considerable segment of Australian consumers, particularly those who habitually prepare meals from fresh ingredients, retain a meaningful degree of reluctance to delegate produce selection to an unfamiliar picker. Adoption within the highest-frequency grocery product categories continues to be moderated by qualitative concerns that advanced personalization technologies have not yet fully resolved, including substitution policy transparency, uncertainty regarding product freshness standards, and the absence of direct sensory evaluation at the point of selection.

Regional and rural Australia is structurally underserved: The majority of regional, rural, and remote communities across Australia lack access to the competitive online grocery infrastructure that metropolitan consumers regard as standard, including same-day fulfilment options, comprehensive product assortment, and price-competitive delivery terms. Inadequate broadband coverage, cost-prohibitive delivery distances, and insufficient cold-chain network development collectively produce a bifurcated market structure that constrains meaningful national channel penetration and limits access to the benefits of digital grocery procurement for a substantial portion of the Australian population.

Australia Online Grocery Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Staples and Cooking Essentials | 25.8% | 2025 |

| Business Model | Hybrid Marketplace | 47.2% | 2025 |

| Platform | App-Based | 62.4% | 2025 |

| Purchase Type | One-Time | 65.7% | 2025 |

| Region | Australia Capital Territory & New South Wales | 34.5% | 2025 |

Product Type Insights

Staples and Cooking Essentials 25.8% market share (2025) | Leading Product Type

Pantry staples represent, by their fundamental nature, one of the most naturally suited categories for online grocery fulfillment: well-recognized product items, established brand preferences, minimal quality-assessment uncertainty, and a replenishment cycle that aligns seamlessly with scheduled delivery windows. Coles Group disclosed in June 2024 that pantry essentials recorded the highest frequency of repeat transactions on its online platform, reinforcing the consistent tendency among households to systematically restore necessities such as pasta and rice on a weekly basis.

Fresh produce, by contrast, presents a more substantive challenge to online adoption, one which the sector continues to address through deliberate investment. Retailers are committing significant resources to AI-assisted quality assessment tools and consumer-controlled substitution frameworks with the intention of addressing the residual psychological barriers to full-basket digital purchasing. In pursuit of reducing product-related service complaints and strengthening consumer confidence in fresh item ordering, Woolworths implemented an AI-enabled produce grading system at its Sydney fulfilment facility in March 2025 to support automated quality verification for home delivery orders.

|

Segment Breakdown Staples and Cooking Essentials (25.8%) · Vegetables and Fruits · Dairy Products · Snacks · Meat and Seafood · Others |

Business Model Insights

Access the comprehensive market breakdown Request Sample

Hybrid Marketplace 47.2% market share (2025) | Leading Business Model

The hybrid marketplace model has established its position as the preferred business architecture for Australian online grocery for a clearly identifiable reason: it enables comprehensive catalogue management without necessitating full merchant ownership of every product unit. By integrating proprietary inventory management with third-party vendor participation on a unified platform, operators such as Woolworths Everyday Market have achieved product ranges that would present significant logistical complexity to replicate through pure-play retail approaches. Through the progressive development of partnerships with independent vendors, Everyday Market meaningfully expanded its available online selection by end of 2024, establishing a diversified marketplace environment that encourages cross-category purchasing and deepens consumer engagement within the Woolworths network, while simultaneously raising switching costs for competing retailers.

|

Segment Breakdown Hybrid Marketplace (47.2 %) · Pure Marketplace · Others |

Platform Insights

App-Based 62.4% market share (2025) | Leading Platform

The 62.4% share commanded by app-based grocery platforms in Australia reflects the depth of mobile channel entrenchment within the market, a position that extends well beyond early adoption. Desktop-based grocery browsing has progressively receded as loyalty programs, push notification-driven engagement, and streamlined reorder functionality convert existing customers into consistently high-frequency revenue contributors. Smartphone penetration across Australia surpasses 95%, and grocery retailers have systematically embedded this audience into the foundational architecture of their digital engagement strategies. Coles’ redesigned mobile application, launched in January 2025, incorporated AI-powered basket recommendation capabilities alongside personalized aisle view functionality, features specifically developed to extend active session duration and support higher per-visit purchase conversion rates.

|

Segment Breakdown App-Based (62.4%) · Web-Based |

Purchase Type Insights

One-Time 65.7% market share (2025) | Leading Purchase Type

The 65.7% share held by one-time purchasing should not be interpreted as evidence of limited platform loyalty; rather, it is an accurate reflection of Australian consumers’ pronounced preference for exercising control over the timing and value of their grocery expenditure. Subscription-based grocery models are gaining measurable traction, yet securing customer commitment to a recurring order schedule requires an established level of confidence in fulfilment consistency, product availability reliability, and substitution quality standards that many consumers are still developing with their preferred platform. Australia Post’s 2025 Annual eCommerce Report showed that online shopping continued to grow in 2024, with 9.8 million Australian households making purchases and strong increases in key categories such as food and liquor, confirming that consumer demand and conversion in grocery and essentials remain important drivers of eCommerce volume growth.

|

Segment Breakdown One-Time (65.7%) · Subscription |

Regional Insights

Australia Capital Territory & New South Wales 34.5% market share (2025) | Leading Region

In numerous respects, the commercial development of online grocery in Australia has proceeded with Sydney as its primary reference point. The region’s population density extended average commute durations, high concentration of dual-income households, and substantial logistics infrastructure have collectively positioned it as the pre-eminent hub of the country’s digital grocery network. The co-location of both Woolworths’ Moorebank Customer Fulfilment Centre and Coles’ Smeaton Grange automated facility within the greater Sydney metropolitan basin places New South Wales in a class of its own with respect to delivery speed, operational throughput capacity, and cost efficiency at this stage of the market’s development.

The ACT’s contribution is more modest in terms of volume but carries meaningful value; Canberra’s substantial public sector employment base sustains above-average household income levels and a clearly expressed consumer preference for premium and convenience-focused retail formats. In January 2026, Amazon Fresh extended its delivery network to 80 additional Sydney suburbs, extending same-day coverage for both chilled and ambient product categories across the outer metropolitan ring and further consolidating New South Wales’ position as the most intensely competitive online grocery territory in the country.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

34.5%

|

|

Key States

|

New South Wales, Australian Capital Territory |

|

Major Growth Drivers

|

Automated fulfilment hub density, Amazon Fresh suburban expansion, high household digital adoption, above-average per capita grocery spending |

|

Outlook

|

National leadership sustained through 2034 delivery network deepening |

|

Regional Breakdown Australia Capital Territory & New South Wales (34.5%) · Victoria & Tasmania · Queensland · Northern Territory & Southern Australia · Western Australia |

Victoria & Tasmania:

Victoria and Tasmania represent the most credible form of competitive threat to New South Wales’ position as national leader, with this threat increasingly being underpinned by a significant reduction in the distance between these markets and the leading state. Victoria’s online food retail market is characterized by high logistics density in inner metropolitan areas and a consumer profile that has shown widespread adoption of online retail across a variety of product types. Tasmania’s online food retail market is smaller in scale but is benefiting from increased engagement with online retail driven by improved connectivity infrastructure and a tech-savvy consumer demographic in centers such as Hobart and Launceston. A significant step change in this region’s potential to meet demand was achieved in October 2024 with the opening of Coles’ Truganina Customer Fulfillment Centre in Melbourne’s western corridor, serving greater Melbourne and adjacent regional markets with its automated picking and next-day delivery model.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Victoria & Tasmania |

|

Major Growth Drivers

|

Truganina CFC capacity uplift, Melbourne inner suburban density, strong digital retail culture, rapid delivery adoption among young professionals |

|

Outlook

|

Strongest near-term challenger to NSW regional leadership |

Queensland:

Queensland’s online grocery growth story is principally concentrated within the Southeast Queensland corridor. The delivery speed and service standards that consumers in Sydney and Melbourne now regard baseline expectations are increasingly demanded by digitally engaged, rapidly urbanizing consumers across Brisbane, the Gold Coast, and the Sunshine Coast. Leading retailers are responding to this demand with targeted infrastructure investments. For example, in May 2025, Woolworths announced the development of its Heathwood Customer Fulfilment Centre in Brisbane, which will use Witron automation technology.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Queensland |

|

Major Growth Drivers

|

SEQ population growth corridor, Heathwood CFC commissioning, Gold Coast lifestyle demand, accelerating digital retail adoption among regional centers. |

|

Outlook

|

High-growth market underpinned by infrastructure investment and population surge |

Western Australia:

Perth occupies a distinctive position within the national online grocery landscape: a geographically isolated metropolitan center characterized by elevated household incomes attributable to the resources sector yet historically underserved by the fulfilment coverage that consumers in eastern-state markets have come to expect as standard. This position is changing. In February 2025, Coles launched an express delivery pilot in Perth’s northern suburbs, aiming to deliver priority grocery categories within 60 minutes. This initiative seeks to build rapid commerce credibility in a market where delivery capacity has not kept pace with consumer expectations.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Western Australia |

|

Major Growth Drivers

|

Mining-sector household income, Coles express delivery pilot, premium grocery appetite, underserved delivery market offering strong upside potential. |

|

Outlook

|

Premium-driven growth with significant untapped demand headroom |

Northern Territory & Southern Australia:

The Northern Territory and South Australian markets represent a sector in which the independent supermarket sector has a relatively larger presence, and the development of the online grocery sector is at an earlier stage of development than in established metropolitan markets. The online grocery sector is expanding beyond the two major supermarket chains, with Metcash’s IGA Shop Online service currently operating through 426 independent stores. In the Northern Territory, the challenges of distribution in remote communities and the geographic vastness of the territory may be impediments and opportunities for the development of the online grocery sector.

|

Metric

|

Details

|

|---|---|

|

Key States

|

South Australia, Tasmania, Northern Territory |

|

Major Growth Drivers

|

IGA network digitalization, Adelaide urban demand expansion, NBN broadband rollout, click-and-collect infrastructure investment in independent retail. |

|

Outlook

|

Emerging market with accelerating adoption as infrastructure gaps close |

Market Outlook (2026-2034)

What is the future outlook of the Australia Online Grocery market?

The Australia Online Grocery market is expected to sustain steady revenue growth through 2034.

The structural foundations supporting Australia’s online grocery market remain robust and show no indication of diminishing over the forecast horizon. The continuing evolution of the country’s already advanced digital infrastructure is manifesting through the progressive sophistication of fulfilment networks, the growing intelligence embedded within retail platforms, and the demonstrated willingness among major retailers to sustain near-term delivery cost pressures in the pursuit of long-term competitive positioning. The addressable consumer base for competitive online grocery services is expected to expand considerably as automated Customer Fulfilment Centers extend same-day delivery capability beyond the Sydney and Melbourne metropolitan areas into Brisbane, Perth, and ultimately regional centers. The convergence of increasing subscription model adoption, cold-chain logistics improvements that make full-basket fresh purchasing a viable digital channel proposition, and the ongoing transfer of primary household grocery decision-making to generations for whom online retail has always represented the standard approach collectively underpin a strongly constructive long-term market outlook.

Australia Online Grocery Market Leading Key Players

The competitive landscape in Australia’s online grocery market is concentrated in structure yet substantively contested in practice. Woolworths and Coles retain commanding positional advantages through the scale of their fulfilment infrastructure and the depth of their loyalty program ecosystems; however, the continued geographic expansion of Amazon Fresh’s footprint, ALDI’s disciplined value-pricing strategy, together with the Metcash-backed independent supermarket network, collectively ensures meaningful competitive discipline is maintained across the sector.

| Company | Leading Brands | Highlights |

|---|---|---|

| Woolworths Group Limited | Woolworths Supermarkets, Big W, Woolworths New Zealand, Everyday Rewards | Woolworths continues to strengthen its digital grocery ecosystem, with the Woolworths Online platform offering same-day and next-day delivery across major metropolitan areas, while Everyday Rewards remains a central driver of customer engagement and personalized offers. |

| Coles Group Limited | Coles Online, Coles Supermarkets, Liquor land | Truganina CFC opened in Melbourne in October 2024; redesigned mobile app with AI basket suggestions launched January 2025 |

| Amazon Australia | Amazon Fresh, Amazon Grocery | Extended Fresh delivery to 47 additional Sydney suburbs in December 2024; same-day coverage for chilled and ambient categories across metropolitan zones |

Some of the other key market players in the Australian online grocery market are ALDI Australia, Metcash Limited (IGA, Foodland, Drakes), and Harris Farm Markets.

Latest Development & News

- In February 2026, Woolworths Group obtained 100% renewable electricity for all its stores, distribution centers, BIG W locations, and support offices in Australia and New Zealand sourcing more than two-thirds of its power from wind, solar, and onsite generation systems capable of lighting over 17,000 homes and cutting operational emissions by more than 74% relative to past levels.

- In December 2025, Coles revealed a broadened partnership with Uber Eats to provide Australia’s most extensive on-demand grocery selection via the Uber Eats app, boosting available Coles items by more than 50% for quick delivery and offering customers additional options for digital grocery shopping through both Coles Online and Uber Eats.

- In March 2026, Amazon Australia announced a significant investment of AU$750 million in a new robotics-enabled fulfillment center located in Brisbane, spanning 150,000 m², aimed at handling over 125 million packages each year and generating over 1,000 jobs locally when fully operational (with another 2,000 jobs created during the construction phase).

Australia Online Grocery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Vegetables and Fruits, Dairy Products, Staples and Cooking Essentials, Snacks, Meat and Seafood, Others |

| Business Models Covered | Pure Marketplace, Hybrid Marketplace, Others |

| Platforms Covered | Web-Based, App-Based |

| Purchase Types Covered | One-Time, Subscription |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia online grocery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia online grocery market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia online grocery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Online Grocery Market Report

The Australia online grocery market was valued at USD 17,216 Million in 2025.

The Australia online grocery market is anticipated to reach a value of USD 96,585 Million by 2034.

Staples and cooking essentials dominate the market with a share of 25.8% in 2025. The category’s structural advantage comes from habitual replenishment cycles and strong compatibility with scheduled delivery, making it the most consistent revenue driver across all product type categories in Australia’s online grocery channel.

Hybrid marketplace dominates the market with a share of 47.2% in 2025. Its ability to combine first-party inventory with third-party seller participation on a unified platform delivers catalogue breadth and pricing diversity that pure-play or click-and-collect models are structurally unable to replicate at comparable scale.

App-based dominate the market with a share of 62.4% in 2025. Smartphone penetration exceeding 91% of the Australian population, combined with loyalty program integration and push-notification-driven re-engagement, makes mobile the primary and preferred interface for online grocery transactions across all demographic groups.

One-time purchases dominate the market with a share of 65.7% in 2025. Australian online grocery shoppers strongly favor transactional flexibility over subscription commitment, and while delivery pass models are growing, the on-demand segment continues to attract the majority of both new and returning digital grocery buyers.

Australia Capital Territory & New South Wales currently leads the Australia online grocery market, accounting for a share of 34.5% in 2025. Sydney’s metropolitan density, concentration of automated Customer Fulfilment Centers, and high per-capita household grocery spend collectively position the region as the most advanced and intensely competed online grocery market in the country.

Some of the major players in the Australia online grocery market include Woolworths Group Limited, Coles Group Limited, Amazon Australia Pty Ltd, ALDI Australia, Metcash Limited, Harris Farm Markets, etc.

The market is being shaped by several significant structural and behavioral developments, including: the accelerating deployment of purpose-built dark stores and Customer Fulfilment Centers that enable faster and more cost-effective urban delivery operations; increasing retailer investment in AI-driven personalization capabilities across mobile application platforms; the deepening integration of online grocery with meal planning and health-management tools; the geographic extension of rapid commerce, encompassing sub-two-hour delivery, from core metropolitan areas into outer suburban catchments; and the progressive digitalization of independent grocery retailers through platform investment and capability development programs.

Growth is being driven by the continued maturation of automated fulfilment infrastructure, which is systematically reducing cost-per-order for major grocery retailers; the enduring behavioral legacy of pandemic-era digital adoption among older consumer demographics; advancements in cold-chain logistics technology that render fresh and chilled categories viable for digital channel acquisition at meaningful scale; and the progressive assumption of primary household purchasing responsibilities by digitally native millennial and Generation Z consumers who regard application-based grocery procurement as the natural default channel.

Within a consumer environment characterized by strong resistance to delivery fee charges, the market continues to face structural last-mile profitability challenges, particularly in regions outside major metropolitan areas where the density economics required to support sustainable home delivery do not currently prevail. Adoption of full-basket digital purchasing among high-frequency fresh product consumers remains constrained by persistent barriers related to substitution trust and fresh produce quality assurance. The infrastructure gap between metropolitan and regional Australia continues to represent a significant structural limitation, while intensifying competitive pressure among Woolworths, Coles, and Amazon Fresh is sustaining elevated capital expenditure requirements on fulfilment infrastructure, which in turn constrains near-term sector-wide profitability improvement.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade