Australia Private Equity Market Size, Share, Trends and Forecast by Fund Type and Region, 2026-2034

Australia Private Equity Market Size, Share, Trends & Forecast (2026-2034)

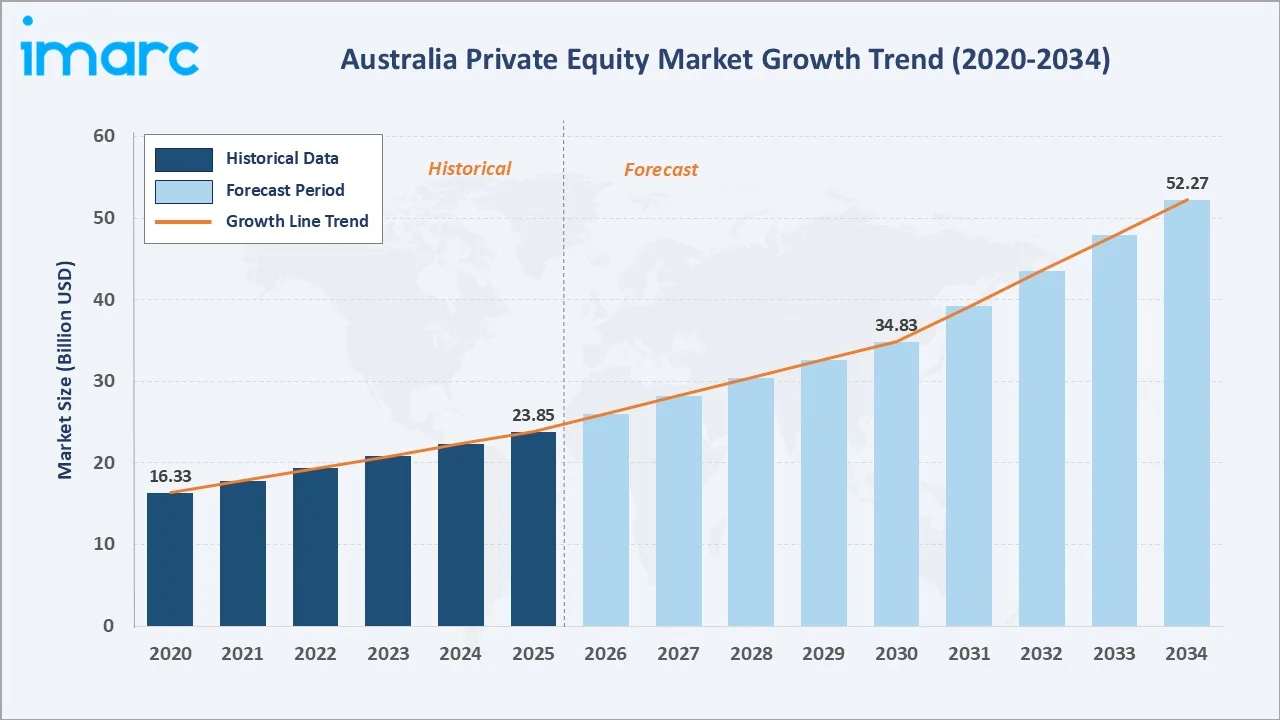

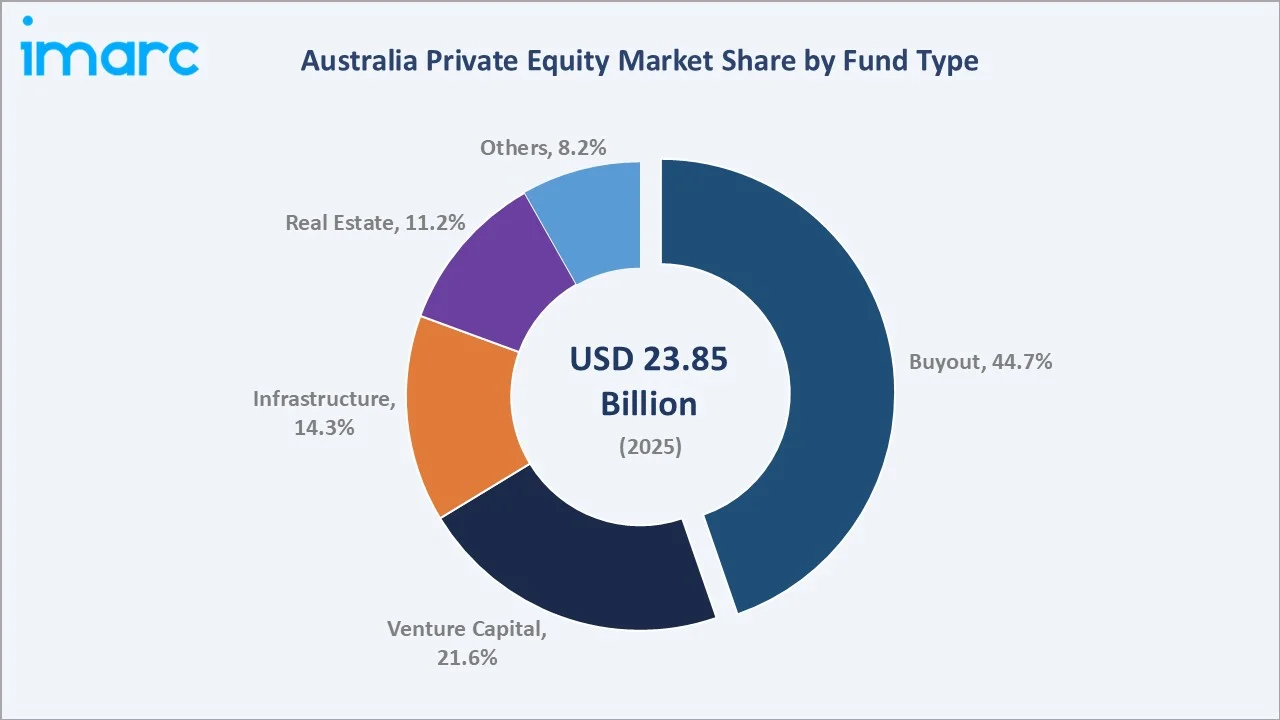

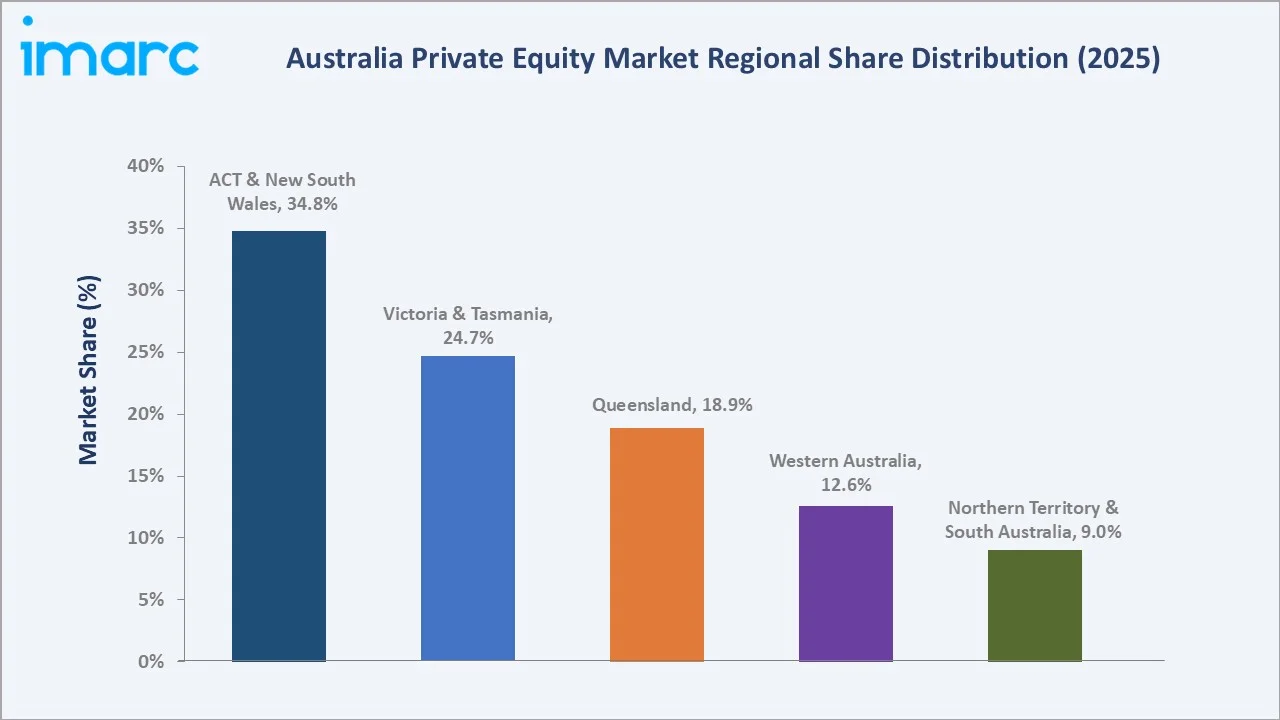

The Australia private equity market reached USD 23.85 Billion in 2025 and is projected to reach USD 52.27 Billion by 2034, growing at a CAGR of 7.87% during 2026-2034. Australia's AUD 4.5 Trillion superannuation sector, providing structurally deep LP capital, the maturing Australian technology startup ecosystem feeding VC and growth equity deal flow, accelerating infrastructure PE driven by Australia's 82% renewable electricity transition by 2030, the rate-cutting cycle improving leverage economics for buyout transactions, and Australia's positioning as the primary APAC PE hub for international fund managers, collectively anchor the market growth. Buyout dominates fund type at 44.7%. Australia Capital Territory & New South Wales commands 34.8% of market revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.85 Billion |

|

Forecast Market Size (2034) |

USD 52.27 Billion |

|

CAGR (2026-2034) |

7.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Fund Type |

Buyout (44.7%, 2025) |

|

Leading Region |

Australia Capital Territory & New South Wales (34.8%, 2025) |

The market expanded from USD 16.33 Billion in 2020 to USD 23.85 Billion in 2025, anchored at USD 34.83 Billion in 2030, and forecast to reach USD 52.27 Billion by 2034. COVID-19 initially compressed PE deal activity in 2020 before triggering the most active PE period in Australian history during 2021-2022, as abundant global liquidity, compressed interest rates enabling cheap LBO financing, and COVID-accelerated digital transformation created compelling PE thesis opportunities across technology, healthcare, and logistics, driving record Australian PE deal volumes.

To get more information on this market, Request Sample

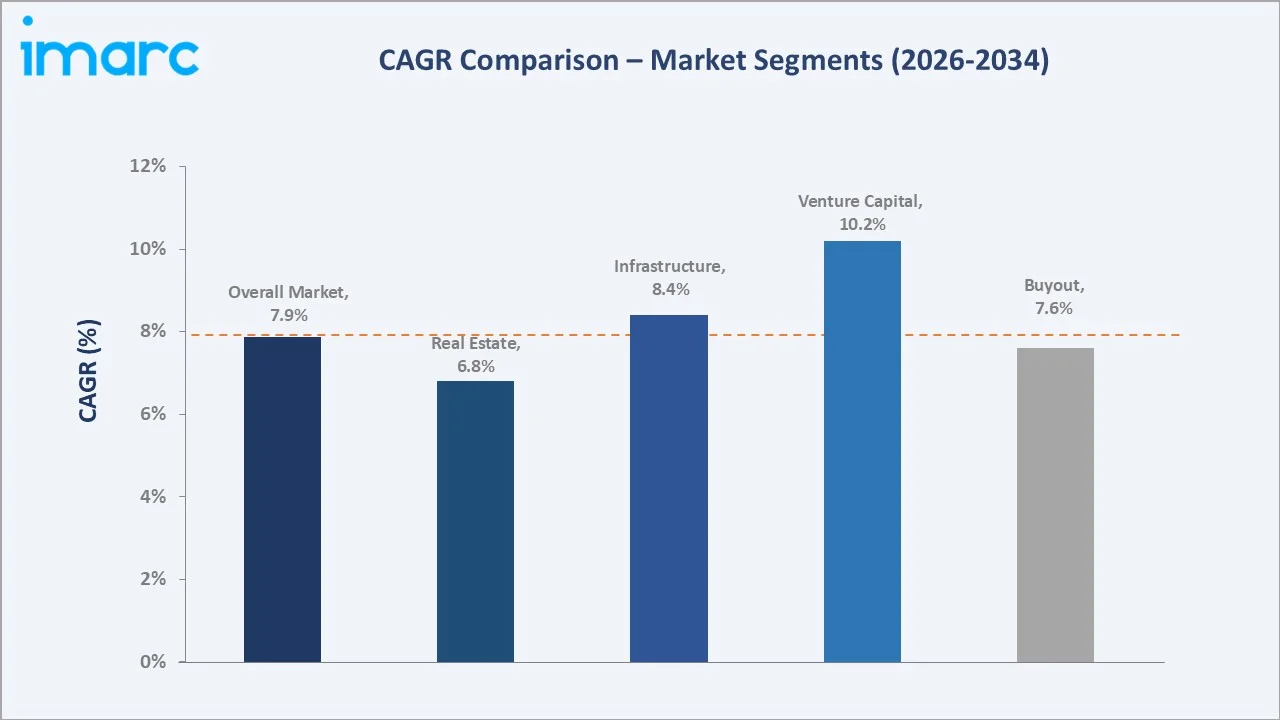

Venture capital grows fastest at ~10.2% CAGR as Australia's startup ecosystem matures beyond its origin companies toward a second-generation VC ecosystem where founder-turned-investors, deep specialist VC funds, and growing corporate venture arms are generating deal activity across software, fintech, climate tech, and deep technology. Infrastructure at ~8.4% CAGR reflects Australia's energy transition investment pipeline, creating long-duration infrastructure PE assets suited to superannuation fund mandates.

Executive Summary

The Australia private equity market reached USD 23.85 Billion in 2025, representing one of the Asia Pacific's largest PE markets and one of the world's most sophisticated PE ecosystems relative to its economy size. Australia's PE market is unique in the global context of alternative asset management. The market is projected to reach USD 52.27 Billion by 2034 at 7.87% CAGR.

Buyout at 44.7% dominates as Australia's core PE activity, driven by executing control acquisitions of established Australian businesses across healthcare, business services, technology services, and consumer sectors. ACT and NSW at 34.8% leads through Sydney's concentration of PE fund management offices, LP relationships with superannuation funds, and M&A advisory ecosystem.

Key Market Insights

|

Insight |

Data |

|

Dominant Fund Type |

Buyout - 44.7% AUM share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales - 34.8% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Buyout at 44.7% reflecting Australia's mature corporate PE ecosystem with compelling family business succession: Australia's buyout market is sustained by three deal sources that collectively provide consistent annual deal activity. First, family-owned Australian businesses at succession inflection points generate 40-50% of Australian mid-market buyout deal flow. Second, ASX-listed companies' take-private situations create large-cap buyout opportunities. Third, secondary PE transactions create deal volume as Australian PE portfolios reach exit horizon and are sold to subsequent PE owners at higher valuations reflecting operational improvements.

- ACT and NSW at 34.8% reflecting Sydney's established PE financial capital position with deal origination density, LP proximity, and exit market access: Sydney's primacy in Australian PE reflects its role as Australia's unambiguous financial capital, the ASX, Australia's largest investment banks, major superannuation fund investment offices, and the ecosystem of PE-supporting advisory firms create a self-reinforcing PE ecosystem density that NSW's geographic and financial capital position sustains.

Australia Private Equity Market Overview

Australia's private equity market encompasses all forms of alternative asset management investment in Australian companies and assets outside publicly traded markets, spanning leveraged buyout private equity, venture capital, growth equity, infrastructure PE, and private real estate PE. Australia's PE market connects an LP base of superannuation funds, family offices, insurance companies, and sovereign wealth funds to a GP community of domestic PE firms and global PE firms' Australian operations.

The ecosystem integrates institutional LP investors, global and domestic GP fund managers across buyout, venture capital, infrastructure, and real estate strategies, M&A advisory and investment banking firms originating deal mandates, commercial banks and debt capital markets providing leveraged acquisition financing, legal and accounting firms providing transaction services, and management consulting firms supporting portfolio value creation.

Market Dynamics

To evaluate market opportunities, Request Sample

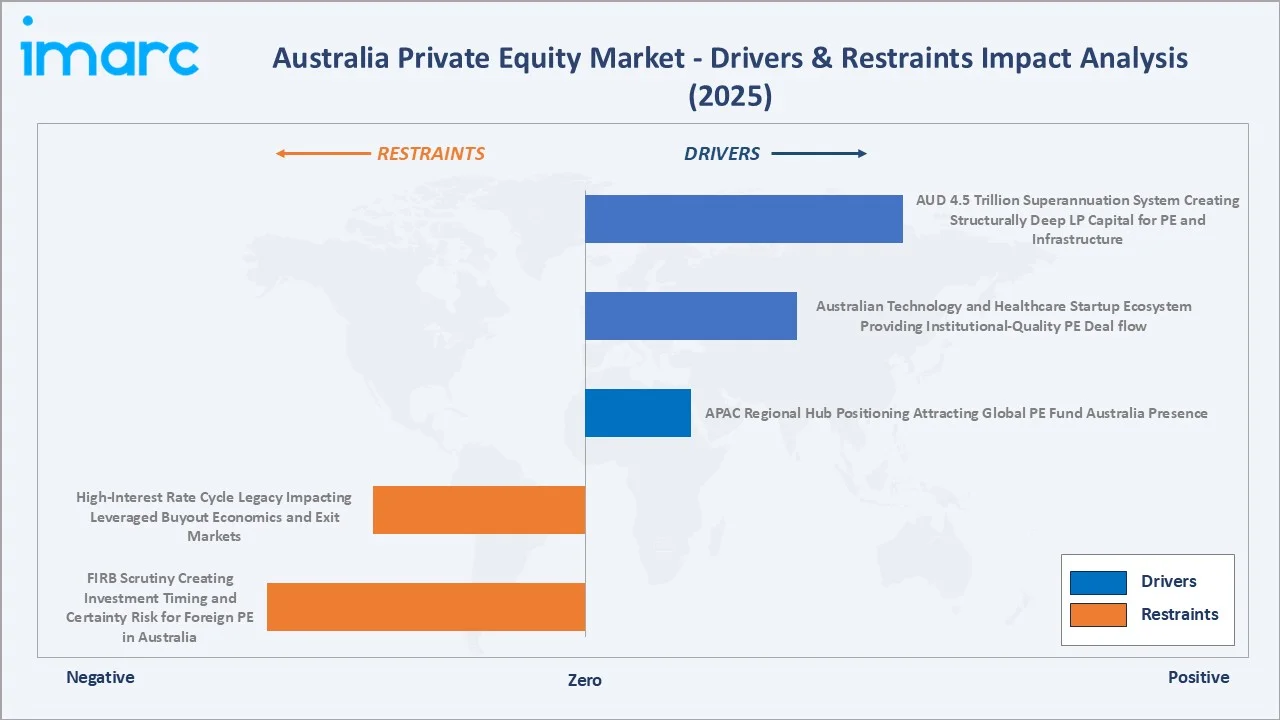

Market Drivers

- AUD 4.5 Trillion Superannuation System Creating Structurally Deep LP Capital for PE and Infrastructure: Australia's mandatory superannuation system has created the world's most disproportionately large pension pool relative to GDP, at AUD 4.5 Trillion in total superannuation assets. The growing allocation from super funds increases deal activity, supports larger transactions, and strengthens Australia’s attractiveness for domestic and global private equity firms.

- Australian Technology and Healthcare Startup Ecosystem Providing Institutional-Quality PE Deal flow: The maturation of Australia's technology startup ecosystem from angel-funded early stage to institutional VC scale has created a consistent pipeline of VC, growth equity, and eventual buyout deals that sustains Australian PE deal flow across multiple fund strategies. Healthcare PE benefits from Australia's $270.5 billion (2023–24) healthcare expenditure (10.1% of GDP), aging population increasing demand for private hospital, specialist medical, and aged care services, and the fragmentation of Australian healthcare services markets creating PE roll-up opportunities.

- APAC Regional Hub Positioning Attracting Global PE Fund Australia Presence: Australia's combination of English-language legal system, transparent regulatory framework, deep capital markets, skilled professional services workforce, and geographic proximity to Asian growth markets positions it as the preferred APAC PE investment hub for international PE funds seeking Asia Pacific exposure without the political risk of China or the corporate governance complexity of Southeast Asian markets.

Market Restraints

- High-Interest Rate Cycle Legacy Impacting Leveraged Buyout Economics and Exit Markets: The legacy impact of high interest rates is hampering the market by increasing borrowing costs and reducing the attractiveness of leveraged buyouts. Higher financing expenses, tighter credit conditions, and weaker valuation multiples are also slowing deal activity and delaying exit opportunities through IPOs and strategic sales.

- FIRB Scrutiny Creating Investment Timing and Certainty Risk for Foreign PE in Australia: FIRB scrutiny is increasing regulatory review timelines and creating uncertainty for foreign investors pursuing acquisitions. Stricter examination of sensitive sectors, national interest concerns, and transaction structures can delay approvals and reduce deal certainty. This environment may discourage cross-border PE activity and complicate large-scale investment execution in Australia.

Market Opportunities

- Energy Transition Infrastructure PE as Australia's Largest-Ever Single PE Investment Theme: Australia's transition from coal-fired baseload electricity to 82% renewable by 2030 requires AUD new generation, storage, transmission, and grid stability investment over the next 25 years, the largest infrastructure investment program in Australian history. For infrastructure PE, this creates a generational opportunity to own long-duration contracted revenue assets with inflation-linked returns that perfectly match superannuation fund liability durations.

- Healthcare Services Buyout Pipeline Driven by Aging Demographics and Private Sector Expansion: Healthcare services buyouts are creating a major opportunity due to the country’s aging population, rising healthcare demand, and expanding private healthcare infrastructure. Private equity firms are increasingly targeting hospitals, aged care, diagnostics, specialist clinics, and healthcare technology providers for scalable growth and recurring revenue potential. The sector also benefits from defensive demand characteristics and long-term demographic trends.

Market Challenges

- Australia-NZ VC Ecosystem Scale Constraints Versus Global Benchmarks: Despite significant maturation, Australia's VC ecosystem remains small relative to the economic opportunity. This relative under-penetration reflects lingering challenges, including insufficient corporate venture capital, limited deep tech VC capital, and talent constraints.

- PE Denominator Effect and Super Fund Portfolio Rebalancing Creating LP Capital Timing Uncertainty: When public equity markets decline significantly, superannuation fund total portfolios shrink in absolute value while PE and infrastructure assets maintain their book values, creating an optical overallocation to private markets versus target allocation percentages. This denominator effect temporarily constrains super fund PE commitment activity as LPs pause new commitments until public market valuations recover and portfolio allocation percentages normalize.

Emerging Market Trends

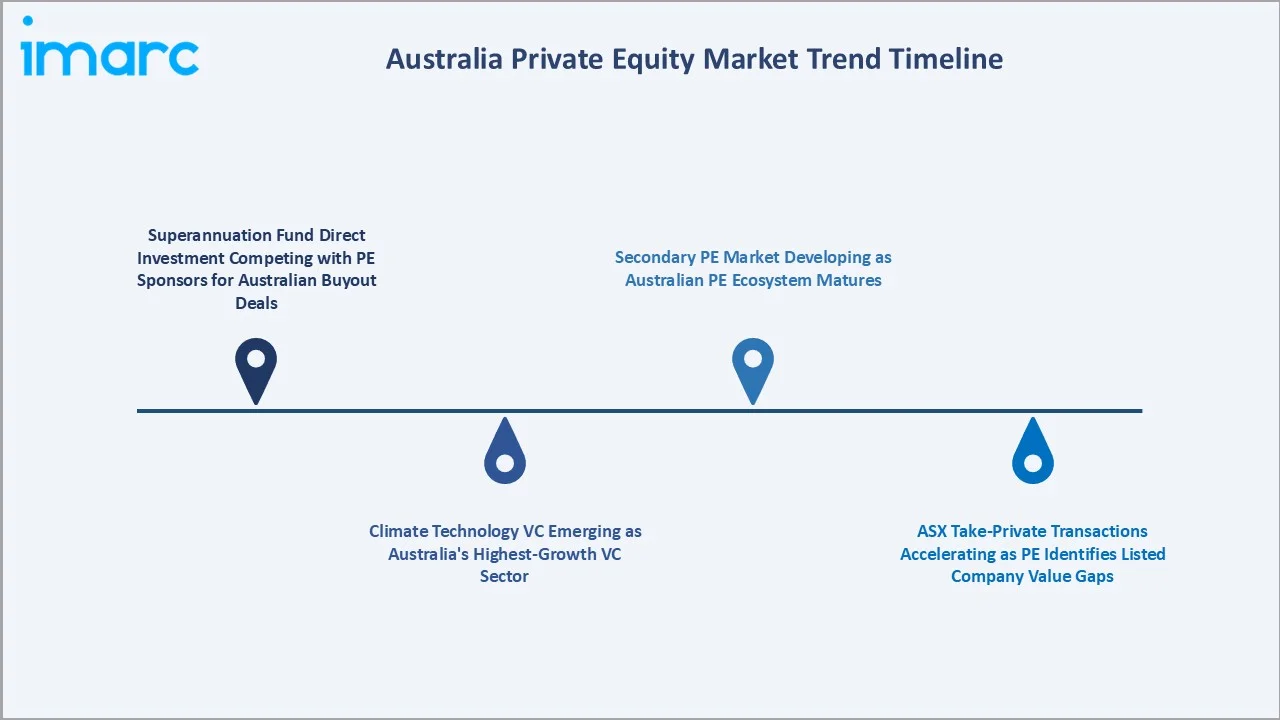

1. Superannuation Fund Direct Investment Competing with PE Sponsors for Australian Buyout Deals

Superannuation funds are increasingly emerging as direct competitors to private equity sponsors in Australian buyout deals by deploying large pools of long-term capital into private markets. These institutional investors are pursuing direct acquisitions and co-investment strategies to reduce fees and gain greater control over assets. This trend is intensifying competition for quality assets and reshaping deal structures across the Australian private equity market.

2. Climate Technology VC Emerging as Australia's Highest-Growth VC Sector

Climate technology venture capital is emerging as one of the fastest-growing trends, driven by increasing investment in clean energy, carbon reduction, battery storage, and sustainability-focused innovation. Strong government support, corporate decarbonization goals, and rising ESG-focused capital allocation are encouraging investors to back climate-tech startups and scalable green infrastructure opportunities.

3. ASX Take-Private Transactions Accelerating as PE Identifies Listed Company Value Gaps

Figures compiled by the Australian Financial Review from PitchBook data showed that Australian private equity exits increased by 62% last year across 56 transactions, including IPOs, buyouts, and trade sales. Major deals included Accel-KKR’s AUD 500 million acquisition of Phocas Software and United H2 Limited’s AUD 400 million purchase of GoZero. This rise in deal activity supports the trend of increasing ASX take-private transactions, as private equity firms identify undervalued listed companies and pursue acquisitions to unlock operational and valuation upside away from public market pressures.

4. Secondary PE Market Developing as Australian PE Ecosystem Matures

The secondary private equity market is emerging as the local PE ecosystem matures, and investors seek greater liquidity and portfolio flexibility. Growing demand for continuation funds, secondary buyouts, and stake sales is enabling investors to recycle capital more efficiently while extending asset holding periods. This trend is also attracting global secondary investors looking for exposure to established Australian private equity assets.

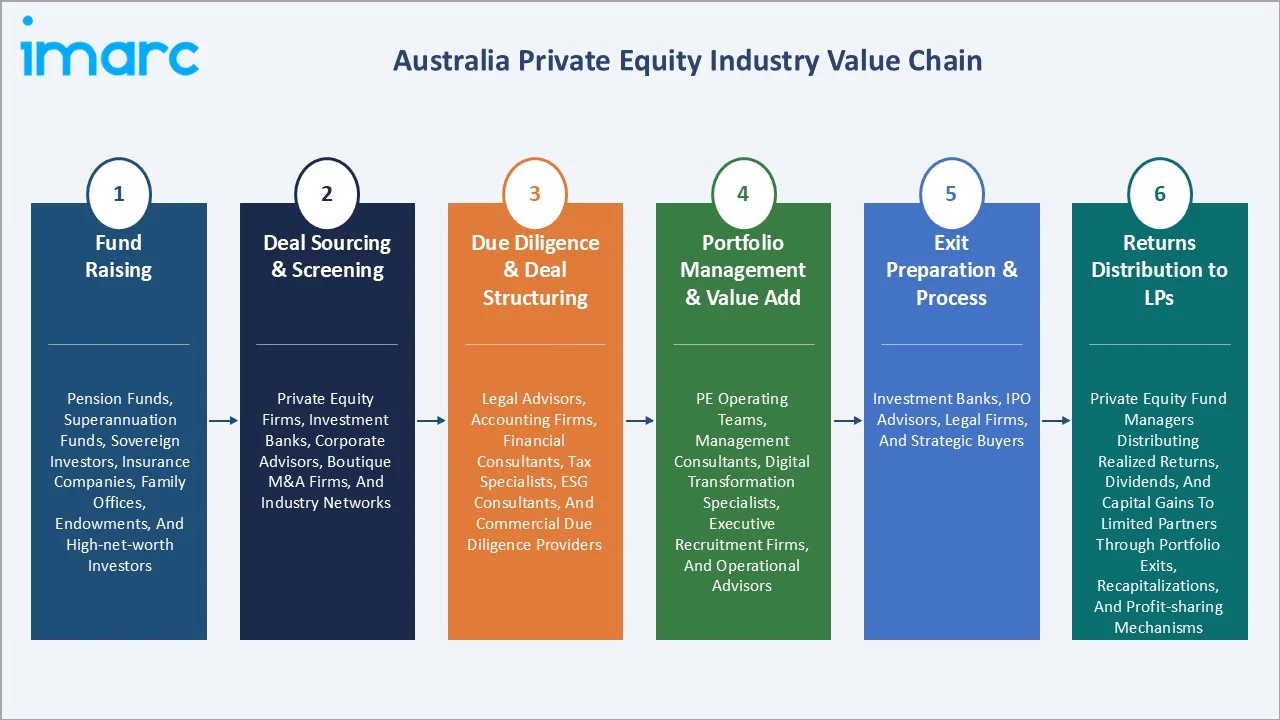

Industry Value Chain Analysis

Australia's private equity value chain integrates fund raising from institutional and high-net-worth LPs, deal sourcing and investment screening, due diligence and deal structuring, portfolio management and value creation, exit preparation and transaction execution, and returns distribution to LPs. PE fund managers earn management fees of 1.5-2% of committed capital annually, plus carried interest of 20% of profits above the 8% preferred return hurdle, creating commercial alignment between PE managers and LP investors that sustains Australia's PE institutional infrastructure.

|

Stage |

Key Participants |

|

Fund Raising |

Pension funds, superannuation funds, sovereign investors, insurance companies, family offices, endowments, and high-net-worth investors. |

|

Deal Sourcing & Screening |

Private equity firms, investment banks, corporate advisors, boutique M&A firms, and industry networks. |

|

Due Diligence & Deal Structuring |

Legal advisors, accounting firms, financial consultants, tax specialists, ESG consultants, and commercial due diligence providers. |

|

Portfolio Management & Value Add |

PE operating teams, management consultants, digital transformation specialists, executive recruitment firms, and operational advisors. |

|

Exit Preparation & Process |

Investment banks, IPO advisors, legal firms, and strategic buyers. |

|

Returns Distribution to LPs |

Private equity fund managers distributing realized returns, dividends, and capital gains to limited partners through portfolio exits, recapitalizations, and profit-sharing mechanisms. |

The portfolio management and value creation tier is Australian PE's most commercially differentiated element; the operational improvement and strategic repositioning capabilities that PE managers deploy at portfolio companies determine realized returns above market average public equity returns.

Technology Landscape in the Australia Private Equity Industry

PE Fund Administration and Portfolio Management Technology

PE fund administration and portfolio management technology are improving fund reporting, portfolio tracking, compliance management, and investor communication. Firms are increasingly adopting cloud-based platforms, AI-driven analytics, and automation tools to streamline operations and enhance decision-making. These technologies also support real-time performance monitoring, risk assessment, and greater transparency for limited partners and regulators.

Deal Sourcing and Pipeline Management Technology

Australian PE fund deal sourcing is being transformed by data analytics platforms that systematically identify potential acquisition targets matching GP investment criteria before formal sale processes launch. AI-enabled financial data extraction tools are increasingly used by Australian VC funds for automated portfolio company KPI monitoring and LP reporting generation.

Portfolio Company Value Creation Technology

Australian PE portfolio companies are benefiting from PE sponsor-commissioned digital transformation programs deploying cloud infrastructure, automation, and data analytics to improve operational efficiency and competitive positioning. Specifically: cloud migration programs, ERP modernization, CRM deployment, and digital marketing capability building.

ESG Monitoring and Reporting Technology

Australian PE funds are deploying ESG data management platforms to meet evolving LP reporting requirements and align with the Australian Treasury's proposed mandatory climate-related financial disclosure standards. In September 2024, Fuse Fleet introduced what it says is Australia’s first insurance-driven ESG reporting tool for fleets, employing Greater Than’s AI technology.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Fund Type |

Buyout |

44.7% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

34.8% |

2025 |

By Fund Type

Buyout leads at 44.7% market share (2025). Australia's buyout segment encompasses large-cap transactions, mid-market transactions, and lower mid-market transactions. Australian buyout activity is concentrated in healthcare services, business services, technology services, consumer, and industrials, with financial services and energy being the less common sectors due to regulatory complexity and commodity exposure, respectively.

To access detailed market analysis, Request Sample

Venture capital at 21.6% grows fastest at ~10.2% CAGR, driven by Australia's maturing startup ecosystem and growing international VC interest. Infrastructure at 14.3% grows at ~8.4% CAGR as energy transition deal volume accelerates. Real estate PE at 11.2% transitions from office/retail toward logistics, build-to-rent, and data center assets, growing at 6.8% CAGR. Others at 8.2% encompasses private credit, growth equity, and distressed debt.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

ACT & New South Wales |

34.8% |

Supported by a high concentration of financial institutions, corporate headquarters, investment banks, and professional advisory firms. |

|

Victoria & Tasmania |

24.7% |

Benefit from a diversified economy, strong business formation, and growing investment across healthcare, technology, consumer, and industrial sectors. |

|

Queensland |

18.9% |

Supported by population growth, infrastructure development, tourism, healthcare, and business expansion across metropolitan and regional areas. |

|

Western Australia |

12.6% |

Driven by mining, energy, infrastructure, and resource-linked industries, creating opportunities for private equity investment in industrial services and diversified regional businesses. |

|

Northern Territory & South Australia |

9.0% |

These regions have smaller but developing private equity markets, supported by defence, agriculture, renewable energy, infrastructure, and regional business investment. |

ACT and New South Wales at 34.8% anchors Australian PE through Sydney's financial capital functions. Victoria and Tasmania at 24.7% reflect Melbourne's PE deal activity in healthcare, consumer, and technology sectors alongside Tasmania's emerging renewable energy PE opportunity. Queensland at 18.9% captures resources-adjacent, tourism, and healthcare PE alongside growing VC deal activity.

Western Australia, at 12.6%, focuses on mining services, energy, agribusiness, and Perth-based PE. NT and South Australia at 9.0% encompasses defense, advanced manufacturing, and agribusiness PE alongside NT's remote infrastructure and critical minerals investment themes

Competitive Landscape

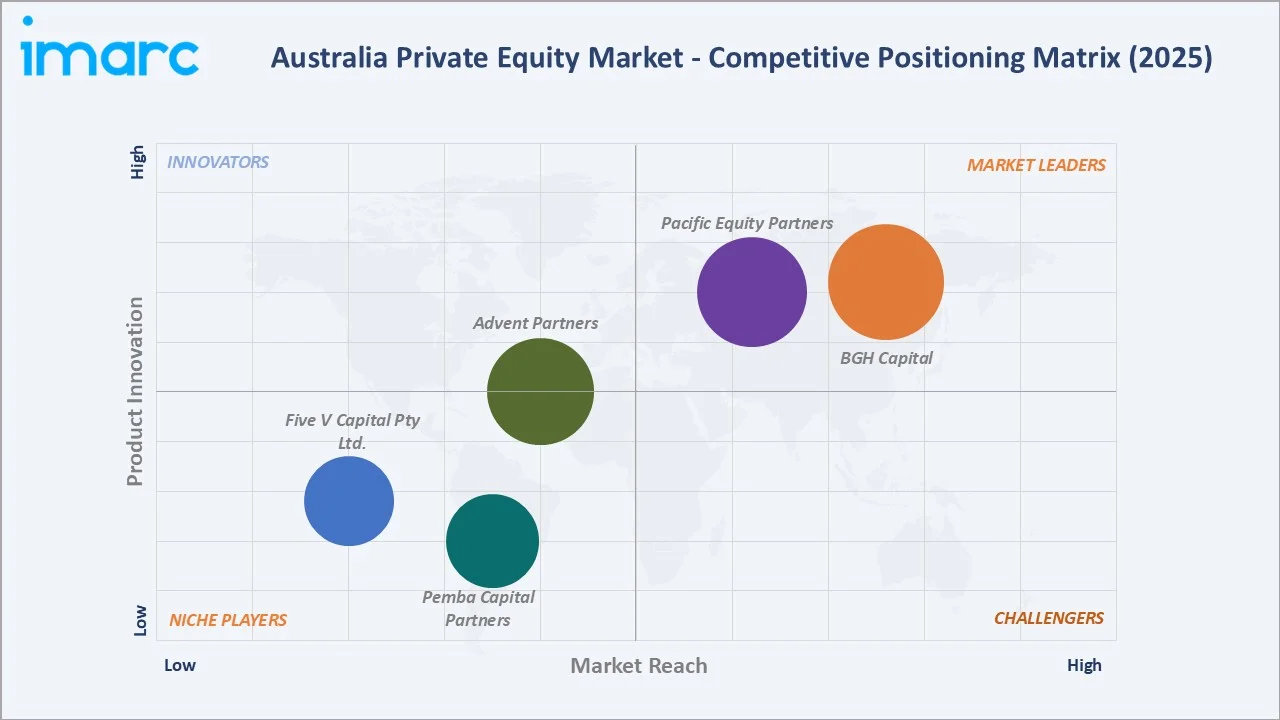

Australia's private equity competitive landscape features a distinctive two-tier structure: internationally headquartered global PE giants with Australian offices competing alongside Australian-domiciled PE funds of comparable deal capability. The global firms bring international deal networks, larger fund mandates, and global sector expertise; the domestic firms bring deeper local market relationships, Australian regulatory knowledge, and reputational capital with Australian sellers who prefer domestic PE sponsors for family business succession transactions.

|

Firm Name |

Key Sectors |

Market Position |

Core Strength |

|

BGH CAPITAL |

Healthcare & Aged Care, Consumer Products & Services, Financial Services, Business Services, Education, Technology, Media & Telecom, Leisure, Tourism & Hospitality, Industrials |

Market Leader |

BGH Capital is an independent private equity firm. BGH Capital invests in businesses in Australia with strong fundamentals and growing end markets. |

|

Pacific Equity Partners |

Industrial, Energy, Consumer products, Entertainment and ‘big data’/financial (All industries/sectors considered) |

Market Leader |

Pacific Equity Partners (PEP) is an Australia-based Private Markets Fund Manager. |

|

Advent Partners |

Business & financial services, Consumer, Healthcare, Industrial, Technology |

Established Player |

Advent Partners invests across five core sectors as they seek to source innovative deal opportunities and develop compelling businesses throughout Australia |

|

Pemba Capital Partners |

Technology, Healthcare, Business Services, Financial Services, Education |

Niche Player |

Pemba’s strategy focuses on attractive sub-segments and niches within five main sectors. |

|

Five V Capital Pty Ltd. |

Healthcare, Retail, Media, Consumer, Technology, Financial Services |

Niche Player |

With an unparalleled network across all sectors, geographies and stages of investment, Five V are not only aligned with the companies, but the team are among the biggest investors in the funds they manage. |

The competitive landscape's most significant 2020-2025trend was the emergence of BGH Capital as a credible alternative to global PE giants for large-cap Australian buyout transactions, demonstrating that locally-founded, Australia-focused PE funds could raise institutional LP capital and execute marquee transactions at a scale previously reserved for other Australian teams.

Key Company Profiles

BGH CAPITAL

BGH Capital is Australia's one of the largest domestically-founded mid-market buyout funds. BGH Capital invests in businesses in Australia and New Zealand with strong fundamentals and growing end markets. By partnering with management teams and business owners, BGH Capital seeks to generate attractive risk-adjusted returns.

- Key Sectors: Healthcare & Aged Care, Consumer Products & Services, Financial Services, Business Services, Education, Technology, Media & Telecom, Leisure, Tourism & Hospitality, Industrials.

- Strategic Focus: Focuses on large-scale buyouts, operational value creation, infrastructure-linked investments, and partnering with leading Australian and New Zealand businesses for long-term growth.

Pacific Equity Partners

Pacific Equity Partners is Australia's most experienced PE fund manager by continuous operating track record. PEP long-term investors include the world’s largest and most experienced investment institutions and sovereign wealth funds, as well as private wealth investors.

- Key Sectors: Industrial, Energy, Consumer products, Entertainment and ‘big data’/financial (All industries/sectors considered).

- Strategic Focus: Focuses on mid-to-large market buyouts, operational transformation, sector specialization, and long-term value creation across high-growth Australian and New Zealand businesses.

Market Concentration Analysis

Australia's private equity market exhibits moderate concentration at the fund manager level, with high concentration in specific fund type niches. In large-cap buyouts, BGH Capital and Pacific Equity Partners together execute 70-75% of transactions, reflecting the capital concentration required for large-scale LBO transactions and the relationship barriers to entry for new large-cap fund competitors. In the mid-market buyout, Advent Partners shares a more fragmented market with 15-20 active PE funds competing for quality deal flow.

Concentration in infrastructure PE is most extreme, reflecting the capital scale and operating expertise required for utility-scale infrastructure asset ownership. This concentration is commercially rational (infrastructure's long duration and operational complexity require deep sector expertise that few managers can develop) but creates commercial power to shape deal pricing in Australian infrastructure auctions.

Investment & Growth Opportunities

Highest Growth Investment Areas

Venture capital (~10.2% CAGR), energy transition infrastructure (~12-15% sub-sector CAGR), healthcare services buyout (~8-10% CAGR), logistics and data center real estate PE (~15-18% sub-sector CAGR), and climate technology VC (~25-30% from small base) represent Australia's highest-return PE investment vectors through 2034. Climate technology VC and energy transition infrastructure collectively represent Australia's most structurally differentiated PE opportunity relative to global competition. Australia's specific renewable energy resource advantage creates domestic deal flow that international PE funds cannot replicate through overseas portfolio strategies.

Emerging Investment Opportunities

Australia's critical minerals sector represents an emerging PE opportunity as global demand for EV battery materials and semiconductor raw materials transforms Australia's mining sector from commodity extraction to technology-adjacent critical resources. PE investments in critical minerals processing, advanced mining technology, and critical minerals logistics offer 15-25% IRR potential for PE investors who can navigate the political and ESG complexity of the Australian critical minerals investment landscape.

Investment Themes

- Energy transition infrastructure PE for superannuation fund mandates: Australia's renewable energy investment pipeline generates 25-35 year contracted revenue infrastructure assets that perfectly match superannuation fund 30-40 year liability management requirements. PE funds developing differentiated renewable energy project development capability can build proprietary deal flow pipelines competing for the most attractive renewable energy assets.

- Healthcare services buyout roll-up strategies targeting fragmented specialist medical sectors: Australian specialist medical services represent systematically fragmented markets with PE roll-up economics validated by existing transactions. PE funds acquiring 10-30 practices per year in a specialty, standardizing operations and technology, and expanding geographic coverage can achieve 3-5x invested capital returns within 5-7 year investment periods.

Future Market Outlook (2026-2034)

The Australia private equity market is projected to grow from USD 23.85 Billion in 2025 to USD 52.27 Billion by 2034, delivering a 7.87% CAGR over the forecast period. The market's anchor value of USD 34.83 Billion in 2030 represents a PE ecosystem where Australian superannuation funds have collectively deployed new PE commitments and BGH Capital's Fund III has completed its fundraising as Australia's first domestic PE fund raising, establishing domestic PE fund capability comparable to regional Asian PE leaders.

Three structural forces define Australia's private equity market growth through 2034 with high confidence: the superannuation system's continued asset accumulation sustaining LP capital availability that enables PE fund manager fundraising at growing fund sizes; Australia's energy transition infrastructure investment requirement creating the largest single PE investment pipeline in Australian history that will sustain emerging climate PE funds at historically high deployment rates; and the venture capital ecosystem's compound maturation creating progressively richer VC dealflow in technology, climate tech, and biotech that sustains Australia's VC CAGR above the overall PE market growth rate.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Managing Directors and Partners from BGH Capital, Pacific Equity Partners; LP investment professionals; M&A advisory directors from Macquarie Capital, Goldman Sachs Australia, and Greenhill Australia; legal advisors from Herbert Smith Freehills and Allens PE practices; and AVCAL (Australian Private Equity and Venture Capital Association) industry data and member survey analysis.

Secondary Research

Secondary research encompassed AVCAL Yearbook 2024-2025 PE and VC activity statistics; ASX-listed PE fund NTA and portfolio disclosures; annual reports and investor day presentations; ASIC and FIRB regulatory disclosure databases; Australia PE Market Update 2025; PitchBook APAC private equity deal data 2020-2025; Australian Bureau of Statistics Financial Accounts (superannuation assets data); RBA Financial Stability Review; APRA Superannuation Statistics; and individual fund manager press releases and investor communications. Over 70 secondary sources were reviewed.

Forecasting Models

Market size forecasts were developed using top-down and bottom-up models calibrated against AVCAL annual PE AUM data, Preqin Australia fund AUM tracking, individual GP AUM disclosures, and superannuation fund PE allocation commitment data (APRA quarterly statistics). Key forecast inputs include RBA cash rate projections (consensus economics), superannuation total asset growth projections (APRA long-run projections), PE fund type growth rate assumptions (CAGR differentiation by buyout, VC, infrastructure, and real estate based on secular demand drivers), and deal activity benchmarking versus GDP growth. Australian PE market size growth is calibrated against comparable market trajectories (Canada, Netherlands, Australia), adjusting for Australia's superannuation structural advantage and energy transition infrastructure tailwind.

Australia Private Equity Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fund Types Covered | Buyout, Venture Capital (VCs), Real Estate, Infrastructure, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | BGH CAPITAL, Pacific Equity Partners, Advent Partners, Pemba Capital Partners, Five V Capital Pty Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia private equity market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia private equity market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia private equity industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Private Equity Market Report

The Australia private equity market reached USD 23.85 Billion in 2025, driven by Australia's AUD 4.5 Trillion superannuation system providing structural LP capital depth, BGH Capital and Pacific Equity Partners' domestic buyout fund activity, infrastructure PE dominance, and the maturing Australian VC ecosystem.

The market grows at 7.87% CAGR during 2026-2034, reaching USD 52.27 Billion by 2034, driven by superannuation fund LP capital growth, energy transition infrastructure PE acceleration, VC ecosystem maturation, buyout activity recovering from the 2022-2024 rate-cycle compression, and international PE fund entries deepening Australian PE market liquidity.

Buyout leads at 44.7% through BGH Capital, Pacific Equity Partners, and Australian deal activity.

ACT and NSW lead at 34.8% through Sydney's concentration of PE fund management offices, M&A advisory origination, ASX exit market access, and LP relationships with superannuation fund investment teams.

Leading firms include BGH CAPITAL, Pacific Equity Partners, Advent Partners, Pemba Capital Partners, and Five V Capital Pty Ltd., among others.

The market is projected to reach approximately USD 34.83 Billion by 2030, with infrastructure PE deal volume potentially exceeding buyout deal volume for the first time as energy transition asset commissioning accelerates, BGH Capital's Fund III completes fundraising, and Australian VC producing its first domestically originated climate technology unicorn.

Australia's mandatory superannuation system creates AUD 4.5 Trillion in pension assets. Major super funds allocate 5-10% of total assets to PE and infrastructure. This structural LP capital pool is the single most important differentiator for Australia's PE market versus comparably sized economies, enabling PE fundraises domestically without requiring international LP marketing.

Australia's renewable energy investment pipeline through 2050 creates the largest infrastructure PE opportunity in Australian history. Long-duration (25-35 year) contracted revenue assets from wind, solar, and battery storage perfectly match superannuation fund liability management requirements.

Australian PE exits use three primary strategies: ASX IPO, trade sale to strategic buyers, and secondary PE sale.

Three priority opportunities: energy transition infrastructure PE, healthcare services roll-up buyout, and climate technology VC.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade