Australia Seafood Market Size, Share, Trends, and Forecast by Type, Form, Distribution Channel, and Region, 2026-2034

Australia Seafood Market Size, Share, Trends & Forecast (2026-2034)

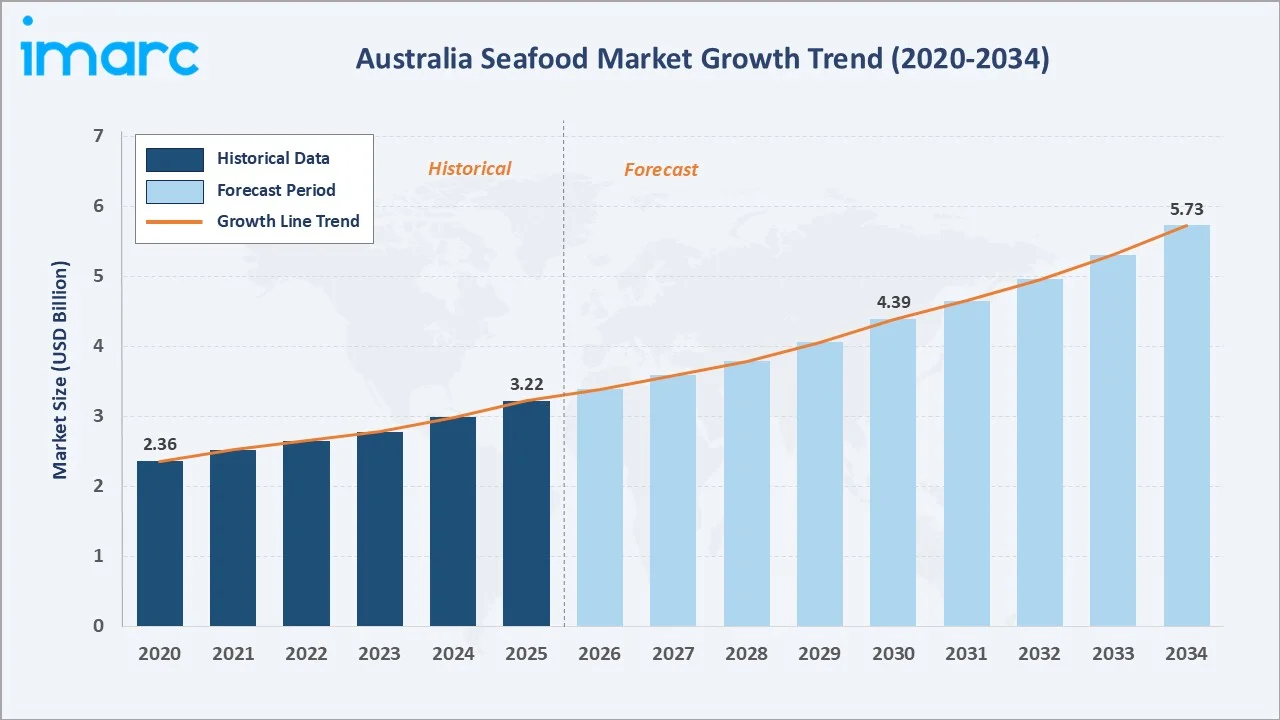

The Australia seafood market size reached USD 3.22 Billion in 2025 and is projected to reach USD 5.73 Billion by 2034, exhibiting a CAGR of 6.43% during 2026-2034. Rising health consciousness, expanding aquaculture infrastructure, and growing export demand are the primary growth forces shaping this market.

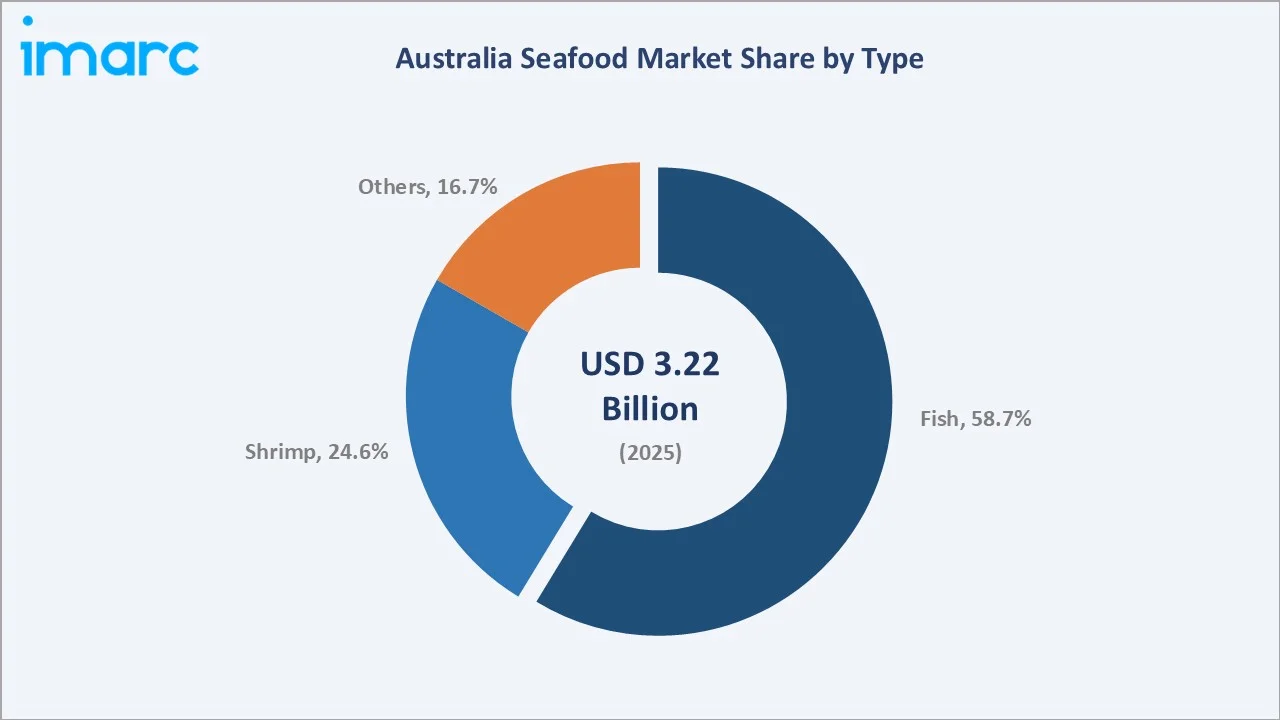

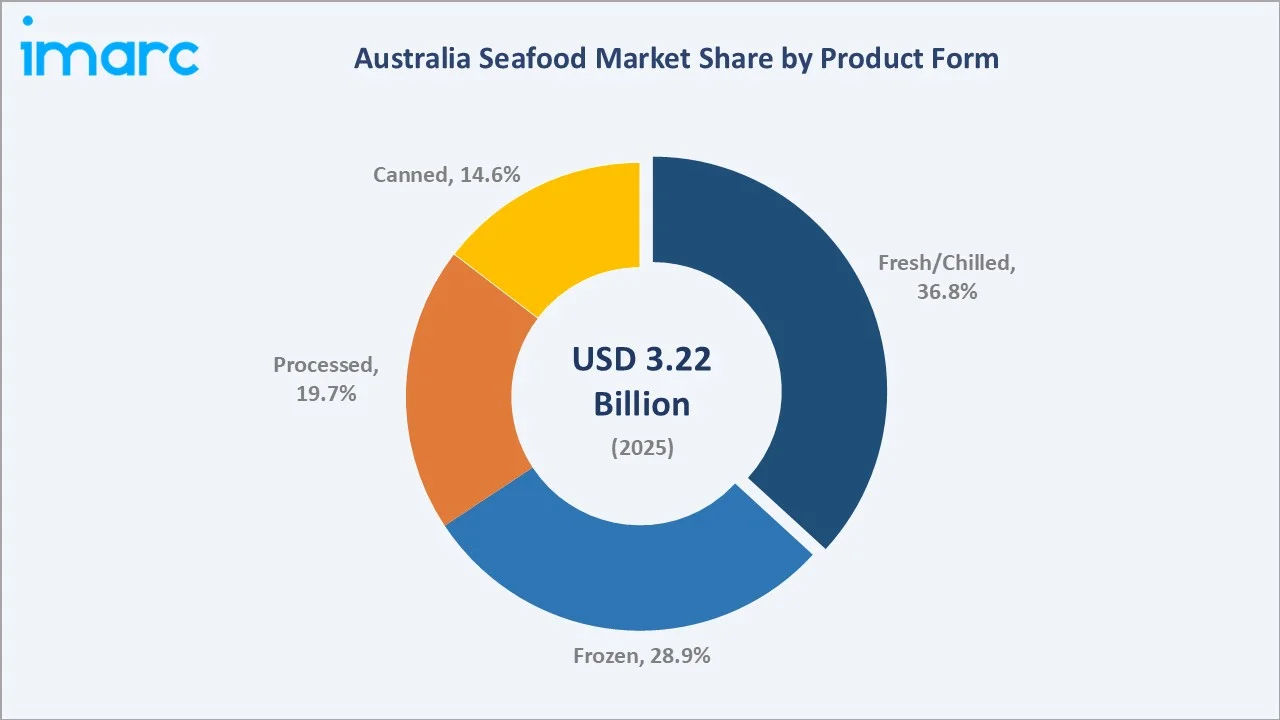

Fish leads the type segmentation at 58.7% in 2025, driven by widespread consumer preference for salmon, tuna, and barramundi. Fresh/Chilled commands 36.8% form share.

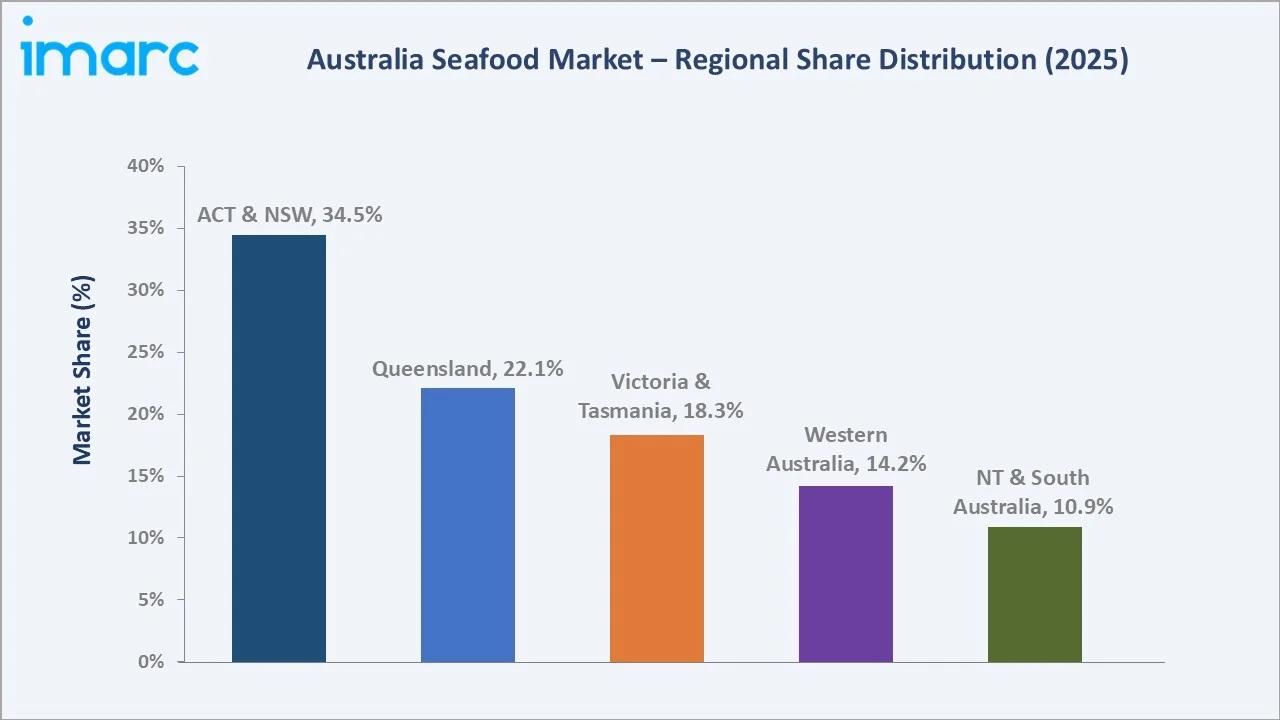

ACT & New South Wales dominates the regional landscape with a 34.5% share underpinned by large urban population centres and high per-capita seafood expenditure.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 3.22 Billion |

| Forecast Market Size (2034) | USD 5.73 Billion |

| CAGR (2026-2034) | 6.43% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Leading Type Segment | Fish (58.7% share, 2025) |

| Leading Form Segment | Fresh/Chilled (36.8% share, 2025) |

| Leading Region | ACT & New South Wales (34.5% share, 2025) |

The Australia seafood market growth from 2020 through 2034 reflects consistent demand driven by healthy eating trends and rising aquaculture output. The forecast to USD 5.73 Billion by 2034 captures accelerating export diversification, cold-chain modernisation, and growth in value-added seafood products across domestic and international channels.

To get more information on this market, Request Sample

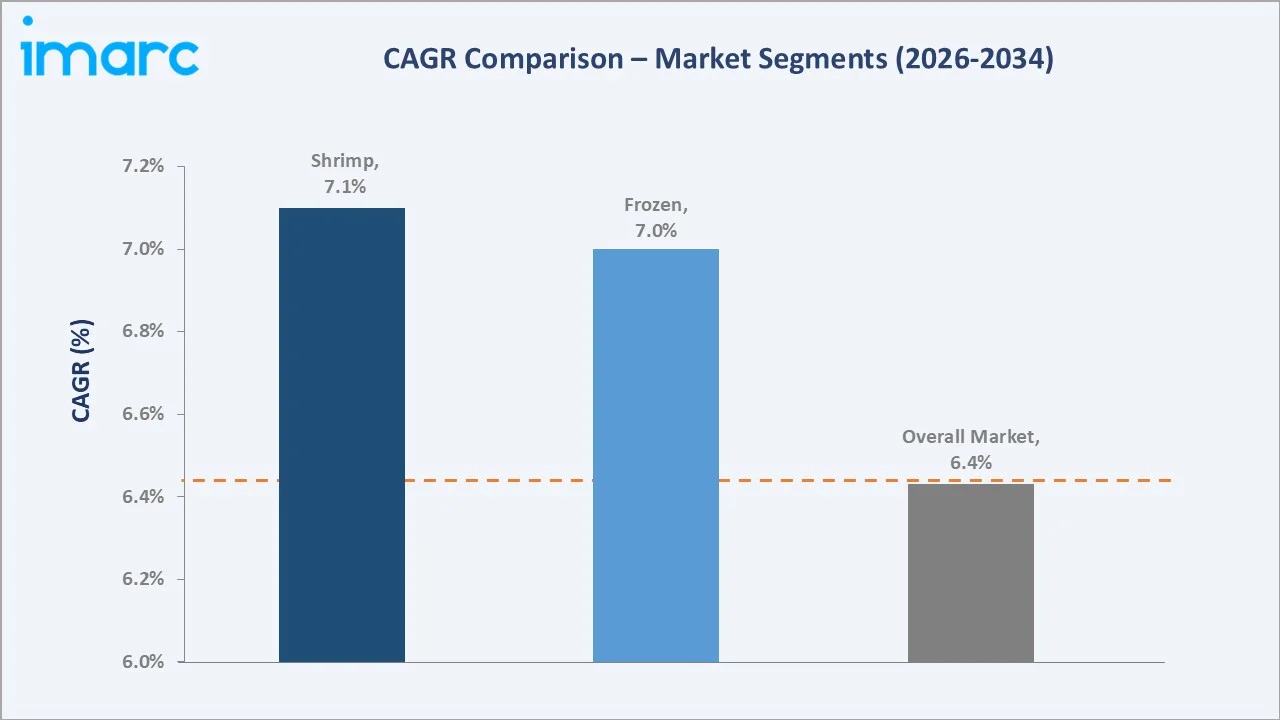

The CAGR trajectories across key type and form sub-segments highlight Shrimp at approximately 7.1% CAGR and Frozen at approximately 7.0% CAGR as the fastest-growing categories within the Australia seafood market through 2034.

Executive Summary

The Australia seafood market is on a sustained growth trajectory from USD 3.22 Billion in 2025 to USD 5.73 Billion by 2034. The market encompasses wild-caught fisheries, aquaculture operations, and seafood processing across domestic retail, food service, and export channels.

Fish leads type segmentation at 58.7% in 2025 owing to its widespread consumer appeal, nutritional profile, and diverse species availability. Shrimp (24.6%) drives premium retail and restaurant demand, while Others (16.7%) include crabs, oysters, lobsters, and abalone.

Fresh/Chilled commands 36.8% form share in 2025, driven by consumer preference for minimally processed premium seafood at retail fish counters and food service operators. Frozen (28.9%) addresses convenience demand; Processed (19.7%) and Canned (14.6%) serve pantry and export requirements.

ACT & New South Wales dominate at 34.5% in 2025, supported by Sydney Fish Market, high urban population density, and premium restaurant activity. Queensland follows at 22.1%, with significant prawn, barramundi, and reef fish production driving both local and export sales.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Type Segment | Fish – 58.7% share (2025) |

| Fastest-Growing Type | Shrimp – 7.1% CAGR (2026-2034) |

| Leading Form Segment | Fresh/Chilled – 36.8% share (2025) |

| Leading Region | ACT & New South Wales – 34.5% share (2025) |

| Second Largest Region | Queensland – 22.1% share (2025) |

| Top Companies | JBS Foods, Walker Seafoods Australia, and Seafarms Group |

- Fish at 58.7%: Fish commands 58.7% share because of diverse species availability, salmon, tuna, barramundi, and snapper, combined with strong nutritional positioning and well-established retail distribution networks across all Australian states.

- Fresh/Chilled at 36.8%: Fresh/Chilled captures 36.8% because rising foodservice expenditure and consumer willingness to pay a premium for minimally processed high-quality seafood support continued investment in cold-chain infrastructure across Australian retail and hospitality.

- ACT & NSW at 34.5%: ACT & New South Wales regional dominance reflects Sydney's position as the country's largest seafood trading hub, its dense urban consumer base, and its concentration of premium restaurant and institutional food service operators.

Australia Seafood Market Overview

The Australia seafood market encompasses wild-capture fisheries, marine and freshwater aquaculture, seafood processing, and cold-chain logistics serving domestic retail, food service, and international export markets. The market integrates fishers, aquaculture operators, processors, distributors, retailers, and regulatory bodies.

The ecosystem integrates government fisheries managers, certification bodies, cold-chain logistics providers, retail and food service channels, export trade partners, and consumer associations, all underpinned by the Department of Agriculture, Fisheries and Forestry (DAFF) and Food Standards Australia New Zealand (FSANZ).

Market Dynamics

To evaluate market opportunities, Request Sample

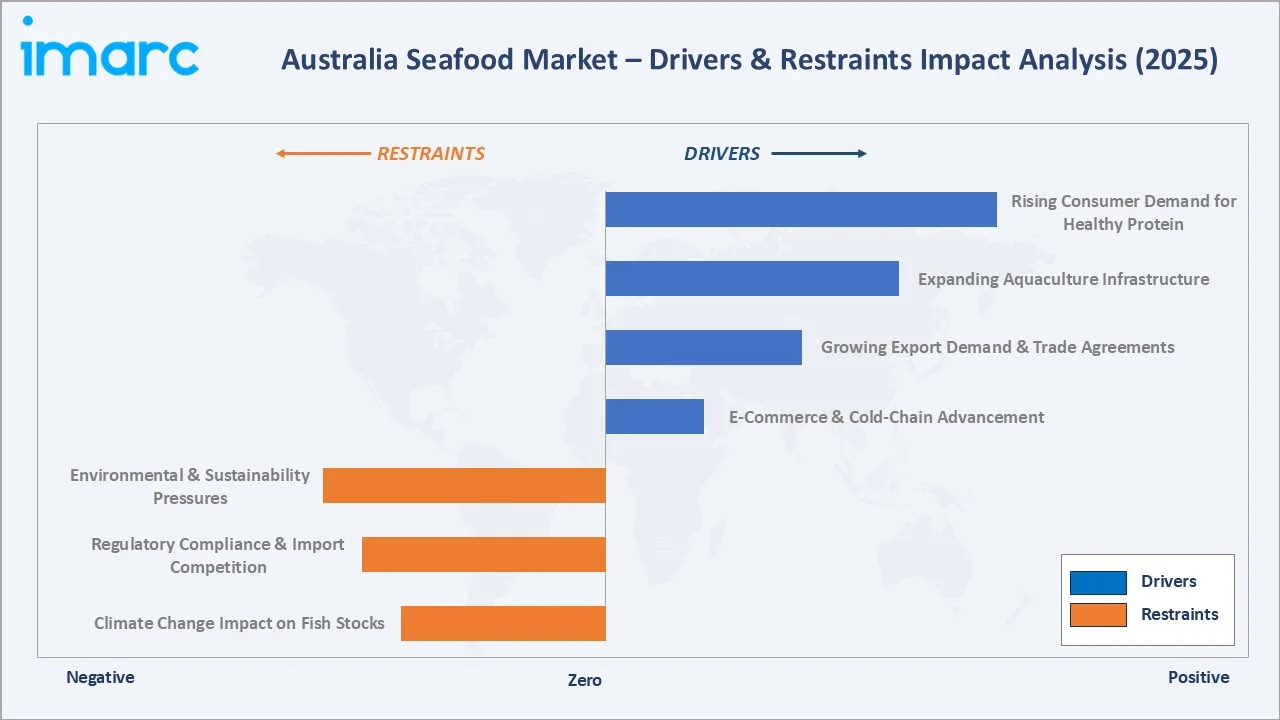

Market Drivers

- Rising Consumer Demand for Healthy Protein: Rising awareness of omega-3 fatty acids, lean protein benefits, and heart health advantages is driving per-capita seafood consumption higher. Health-conscious Australians increasingly substitute red meat with fish and shrimp, directly boosting retail and food service demand across all age demographics.

- Expanding Aquaculture Infrastructure: Government investment in land-based recirculating aquaculture systems (RAS), offshore cage aquaculture, and selective breeding programs is expanding domestic supply capacity. Salmon farming in Tasmania and barramundi aquaculture in Queensland is scaling rapidly to meet growing consumer and export demand.

- Growing Export Demand & Trade Agreements: Free trade agreements with Japan, South Korea, China, and ASEAN nations are lowering tariff barriers for Australian seafood exports. Premium lobster, abalone, southern bluefin tuna, and rock lobster command strong prices in Asian markets, driving investment in processing and export-grade cold-chain infrastructure.

- E-Commerce & Cold-Chain Advancement: Rapid growth in online grocery platforms, direct-to-consumer subscription seafood boxes, and improvements in last-mile refrigerated delivery are expanding the addressable market. Digital retail channels enable premium fresh seafood access in metropolitan and regional areas previously underserved by traditional fish retail.

Market Restraints

- Environmental & Sustainability Pressures: Tightening emissions regulations, marine protected area expansion, and consumer scrutiny of sustainability certifications are increasing compliance costs for wild-capture fisheries. Operators face higher documentation burdens, gear restrictions, and quota reductions, which constrain supply and increase raw material costs across the value chain.

- Regulatory Compliance & Import Competition: Strict FSANZ food safety regulations, biosecurity imports controls, and country-of-origin labelling requirements increase operational complexity for processors and importers. Simultaneously, low-cost Asian imported frozen seafood competes with domestically produced products in supermarket channels, compressing margins for local processors.

- Climate Change Impact on Fish Stocks: Marine heatwaves, ocean acidification, and irregular rainfall patterns adversely affect wild fishery biomass estimates and aquaculture yields. Climate variability increases supply unpredictability, elevates insurance and contingency costs, and threatens the long-term viability of temperature-sensitive aquaculture species.

Market Opportunities

- Premium Export Market Expansion: Growing Asian middle-class demand for premium Australian seafood, particularly southern bluefin tuna, rock lobster, abalone, and Pacific oysters, presents significant revenue opportunities. Direct online export channels and premium packaging innovations are enabling producers to capture higher-value consumer segments across key Asian markets.

- Value-Added Seafood Product Innovation: Australian consumers increasingly seek value-added, convenience-oriented seafood products such as marinated fillets, ready-to-cook meal kits, smoked varieties, and chef-inspired retail offerings, supporting investment in domestic processing capacity and creating margin-enhancement opportunities for seafood producers and retailers.

Market Challenges

- Declining Wild Fishery Access: Expanding marine protected areas and declining wild fish stock assessments in some regions are reducing access to traditional fishing grounds. Fisheries managers face difficult trade-offs between short-term industry needs and long-term ecosystem sustainability, creating supply uncertainty for processors reliant on wild-caught species.

- Labour Shortages in Processing & Aquaculture: Shortage of trained seafood processing workers, experienced aquaculture technicians, and qualified quality assurance personnel in regional locations constrain production capacity. Australia's geographic isolation and competitive labour market make seasonal workforce sourcing increasingly difficult for facilities outside major urban centres.

Emerging Market Trends

1. Health-Driven Seafood Consumption Growth

Post-pandemic health awareness has structurally elevated seafood demand. Nutritional positioning of omega-3-rich species and clean-label messaging are influencing purchasing decisions across retail and food service channels throughout Australia.

2. Sustainable Aquaculture and Certification Adoption

ASC, MSC, and BAP certification uptake is accelerating among Australian aquaculture and wild-catch operators. Certification provides export market access premiums and meets growing retailer requirements for verified sustainability credentials across major grocery chains.

3. Premiumisation and Value-Added Product Development

Australian seafood producers are investing in higher-margin value-added categories including ready-to-cook fillets, chilled meal kits, and smoked and marinated specialties. Retail innovation is expanding category premiumisation and improving producer margins.

4. Digital and Direct-to-Consumer Channel Expansion

Online subscription seafood boxes, farm-to-table direct sales, and digital marketplaces connecting fishers with consumers are disrupting traditional wholesale distribution. These channels enable price transparency, quality storytelling, and stronger producer margins.

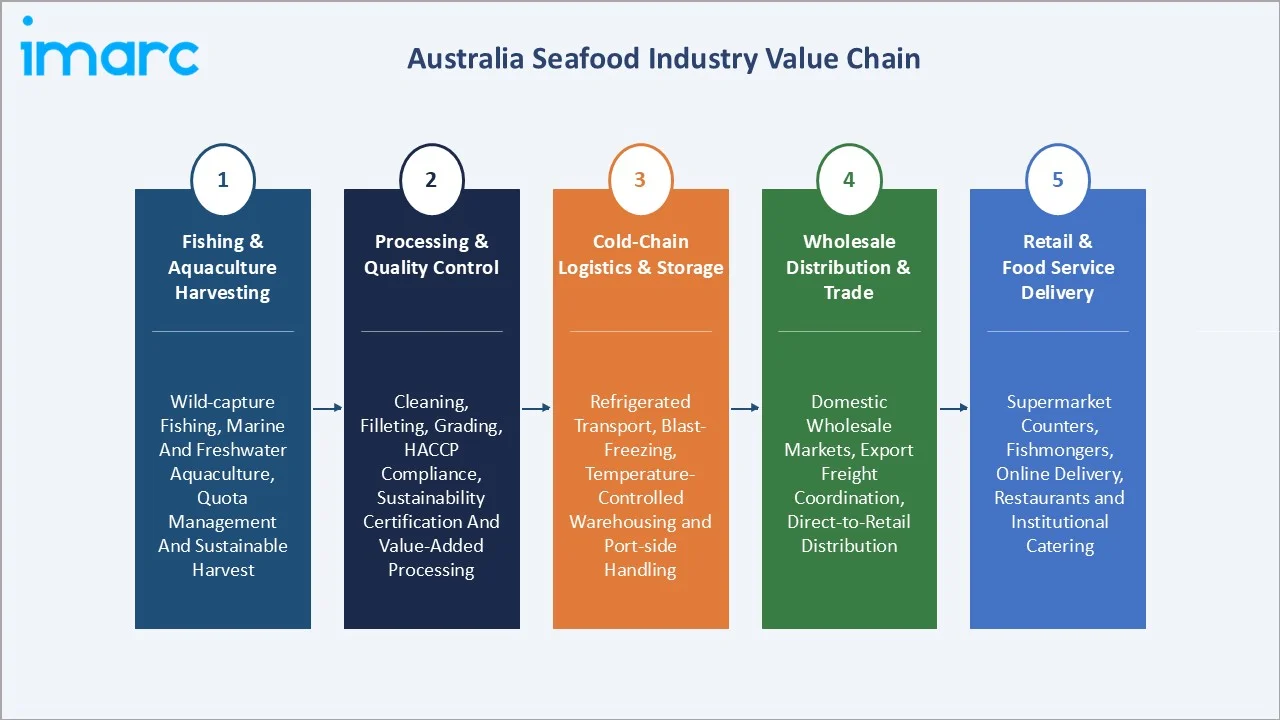

Industry Value Chain Analysis

The Australia seafood value chain spans five integrated stages from harvest through end-consumer delivery. Processing and quality control stages capture primary value through grading, filleting, and certification, while cold-chain logistics generate significant recurring service revenue across the supply network.

| Stage | Key Activities |

|---|---|

| Fishing & Aquaculture Harvesting | Wild-capture fishing, marine and freshwater aquaculture operations, sustainable quota management, and species-selective harvesting practices |

| Processing & Quality Control | Cleaning, filleting, grading, HACCP compliance, sustainability certification, and value-added product manufacturing |

| Cold-Chain Logistics & Storage | Refrigerated transport, blast-freezing, temperature-controlled warehousing, and port-side handling infrastructure |

| Wholesale Distribution & Trade | Domestic wholesale markets, export freight coordination, direct-to-retail distribution, and international trade partner management |

| Retail & Food Service Delivery | Supermarket seafood counters, specialty fishmongers, online delivery platforms, restaurants, and institutional food service operators |

Processing and quality control stages capture the highest value in the Australia seafood chain, requiring technical expertise in food safety compliance, sustainability certification, and product differentiation. After-sales cold-chain services and retail brand partnerships represent growing recurring revenue streams improving long-term producer and processor margins.

Technology Landscape in the Australia Seafood Industry

IoT-Enabled Cold-Chain Monitoring

Sensor-based temperature and humidity monitoring across refrigerated transport and storage is improving quality assurance. Real-time alerts enable proactive intervention, reducing waste and ensuring compliance with FSANZ and export market food safety standards.

Blockchain-Based Traceability Systems

Blockchain platforms are enabling end-to-end supply chain transparency, from harvest location to retail shelf. Consumer-facing QR codes providing species, catch method, and sustainability certification data are building trust and supporting premium pricing strategies.

Recirculating Aquaculture Systems (RAS) Technology

Advanced RAS enables land-based fish farming with precise water quality control, reduced disease risk, and year-round production. Investment in RAS for salmon, barramundi, and yellowtail kingfish is accelerating domestic supply independence and export capability.

AI-Powered Stock Assessment and Quota Management

Machine learning tools integrating sonar data, satellite imagery, and historical catch records are improving wild fishery biomass estimation. AI-assisted quota modelling supports sustainable harvest decisions while optimising catch allocation across licensed operators.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Fish | 58.7% | 2025 |

| Form | Fresh/Chilled | 36.8% | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Region | ACT & New South Wales | 34.5% | 2025 |

By Type

Fish commands a 58.7% majority share in 2025 owing to diverse species availability, strong nutritional profile, and broad consumer appeal across all demographic segments. Salmon, tuna, barramundi, snapper, and flathead are widely available through retail supermarkets, specialty fishmongers, and food service operators nationwide.

To access detailed market analysis, Request Sample

Shrimp (24.6%) commands the second-largest share driven by year-round retail demand, strong food service usage, and growing export demand from Asian markets. Others (16.7%) encompasses oysters, lobster, abalone, crab, and squid—high-value species sustaining premium export revenue and domestic specialty retail segments.

By Form

Fresh/Chilled dominates at 36.8% in 2025, driven by rising consumer preference for premium, minimally processed seafood across supermarket fish counters and specialty retailers. Cold-chain infrastructure investment and same-day delivery logistics are sustaining capital investment in fresh seafood handling facilities across metropolitan Australia.

Frozen (28.9%) addresses convenience-driven household demand and supports export logistics where temperature-controlled air freight is cost-prohibitive. Processed (19.7%) serves value-added product demand including smoked, marinated, and battered seafood categories. Canned (14.6%) covers ambient-stable products including tuna, salmon, and sardines.

Regional Market Insights

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| ACT & New South Wales | 34.5% | Largest seafood trading hub, high urban population density, premium food service concentration, and strong retail seafood expenditure |

| Queensland | 22.1% | Leading prawn aquaculture state, barramundi farming, reef fish harvesting, and strong domestic and Asian export market activity |

| Victoria & Tasmania | 18.3% | Salmon and oyster aquaculture dominance, southern bluefin tuna processing, and significant urban food service demand |

| Western Australia | 14.2% | Rock lobster and pearl oyster export leadership, significant wild-capture fisheries, and growing premium Asian export market demand |

| NT & Southern Australia | 10.9% | Barramundi aquaculture expansion, oyster production, and developing aquaculture investment in key coastal growing regions |

ACT & New South Wales' 34.5% market dominance in 2025 is driven by its position as the country's largest seafood trading hub, high urban density, premium restaurant activity, and superior cold-chain distribution infrastructure serving both retail and institutional food service customers across major metropolitan areas.

Queensland, at 22.1% in 2025, is anchored by prawn aquaculture, barramundi farming, and reef species harvesting. Victoria & Tasmania at 18.3% reflects dominance in salmon and oyster production. Western Australia at 14.2% leads in premium export species including rock lobster and pearl oyster, commanding strong values in Asian export markets.

Competitive Landscape

The Australia seafood market is moderately fragmented, with integrated aquaculture and processing companies, wild-capture specialist operators, and export-focused seafood businesses competing across domestic and international channels. Leading players leverage sustainability certification, cold-chain capabilities, and brand equity to maintain competitive advantage.

| Company Name | Key Products / Operations | Market Position | Strategic Focus |

|---|---|---|---|

| JBS Foods | Salmon products; Tasmania-based Salmon, Tasmania Salmon Caviar | Established | Operates through its brand, Huon Aquaculture. Advancing land-based aquaculture; leveraging JBS global distribution network |

| Walker Seafoods Australia | Yellowfin Tuna, Bigeye Tuna, Albacore Tuna, Striped Marlin | Established | Premium tuna product development for export; chef collaboration and value-added product innovation |

| Seafarms Group | Prawn Species | Emerging | Scaling large-scale tropical prawn aquaculture for domestic and Asian export market penetration |

Key players include JBS Foods, Walker Seafoods Australia, and Seafarms Group, among others.

Key Company Profiles

Walker Seafoods Australia

Walker Seafoods Australia is a leading tuna operator based in Australia, specialising in Eastern Tuna and Billfish Fishery (ETBF).

- Product Portfolio: Yellowfin tuna; Bigeye Tuna, Albacore Tuna, Striped Marlin, and others.

- Recent Developments: In August 2024, Walker Seafoods Australia announced a partnership with renowned chef Neil Perry to launch a new line of preserved local tuna for sale in Australian supermarkets, supporting sustainable seafood awareness.

- Strategic Focus: Walker Seafoods is focused on building premium domestic retail brand presence for Australian tuna through chef collaborations and value-added product innovation, while maintaining its strong Asian export position and advancing sustainability certification credentials.

JBS Foods

JBS Foods, which operates through Huon Aquaculture, is an integrated seafood company operating across farming, processing, and distribution of premium salmon and related seafood products in Australia. The company manages a fully integrated supply chain spanning aquaculture operations, value-added processing, and retail and export channels, supplying high-quality Tasmanian seafood products to domestic and international markets.

- Product Portfolio: Salmon products, Tasmania-based Salmon, Tasmania Salmon Caviar, and others.

- Strategic Focus: The company is focused on expanding production capacity, advancing sustainable farming practices, and enhancing its value-added product portfolio to meet growing consumer demand. It continues to strengthen its market position across domestic retail and key international export channels through ongoing investment in operational infrastructure and product innovation.

Market Concentration Analysis

The Australia seafood market is moderately fragmented at the production level, with leading integrated salmon aquaculture operators commanding significant category shares, while wild-catch and specialty aquaculture segments remain distributed across numerous smaller operators and regional fishing enterprises across all Australian states.

At the type level, Fish segment concentration is higher due to the scale economies available in salmon farming versus the fragmented nature of wild-catch operators. Geographic concentration in Tasmania for salmon, South Australia for tuna and kingfish, and Queensland for prawns creates specialised regional supply clusters that larger buyers must actively manage.

Investment & Growth Opportunities

Fastest-Growing Segments

Shrimp represents the highest-growth type segment through 2034 at approximately 7.1% CAGR, capturing rising retail and export demand. Frozen form leads form-segment growth at approximately 7.0% CAGR, driven by export logistics requirements and consumer convenience trends across Australian and Asian markets.

Emerging Investment Areas

Land-based RAS aquaculture, offshore cage farming, and value-added processing represent significant capital investment frontiers. Export market diversification into Southeast Asia and the Middle East presents growth opportunities for operators with sustainability certifications and premium product positioning.

Venture & Investment Trends

Private equity and strategic investors are increasing capital allocation to Australian aquaculture technology companies focused on RAS, selective breeding, and sustainable feed innovation. Government co-investment programs are catalysing private capital mobilisation across targeted aquaculture development precincts in Queensland and the Northern Territory.

Future Market Outlook (2026–2034)

The Australia seafood market is forecast to expand from USD 3.22 Billion in 2025 to USD 5.73 Billion by 2034 at a CAGR of 6.43%, driven by health-conscious consumer demand, aquaculture infrastructure expansion, rising export values, and premiumisation of retail and food service seafood categories across the forecast horizon.

Three structural forces will shape the market through 2034: aquaculture technology advancement will deliver supply scalability for salmon, prawns, and kingfish; export market premiumisation will drive investment in certification and value-added processing; and digital retail channel growth will reshape domestic distribution economics and enable direct producer-to-consumer value capture opportunities.

Research Methodology

Primary Research

Primary research encompassed structured interviews with aquaculture operators, seafood processors, export managers, retail category buyers, and regulatory specialists. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends across the Australia seafood market.

Secondary Research

Key secondary sources include DAFF fisheries production data, ABARES aquaculture output reports, industry association publications from Seafood Industry Australia (SIA), annual reports from key producers, trade publications, and market intelligence databases covering Australian food and beverage sectors.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating aquaculture production projections, export trade data, consumer expenditure trends, and regional economic growth scenarios. Base, optimistic, and conservative cases were modelled through the 2034 horizon.

Australia Seafood Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fish, Shrimp, Others |

| Forms Covered | Canned, Fresh/Chilled, Frozen, Processed |

| Distribution Channels Covered |

|

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | JBS Foods, Walker Seafoods Australia, Seafarms Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia seafood market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia seafood market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia seafood industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Seafood Market Report

The Australia seafood market reached USD 3.22 Billion in 2025, reflecting sustained demand driven by health-conscious consumers, expanding aquaculture output, and growing premium export demand across Asian and international markets.

The market is projected to reach USD 5.73 Billion by 2034, growing at a CAGR of 6.43% during 2026-2034, driven by aquaculture expansion, export premiumisation, and digital retail channel growth across domestic and international seafood markets.

Fish leads with a 58.7% share in 2025, driven by diverse species availability and broad consumer appeal. Shrimp at 24.6% is the fastest-growing type segment, supported by strong retail, food service, and export demand growth through the forecast period.

Fresh/Chilled commands the largest form share at 36.8% in 2025. Rising consumer preference for premium minimally processed seafood and cold-chain infrastructure investment are sustaining category leadership through the 2034 forecast horizon.

ACT & New South Wales dominates with a 34.5% share in 2025, underpinned by the country's largest seafood trading hub, high urban population density, and premium food service concentration. The region is expected to maintain leadership through the 2034 forecast period.

Key drivers include rising consumer demand for healthy protein, expanding aquaculture infrastructure, growing export demand via trade agreements, and e-commerce and cold-chain logistics advancement enabling broader geographic market access across Australia.

Major challenges include environmental and sustainability compliance pressures on wild-capture fisheries, import competition from low-cost Asian processed seafood, climate change impacts on fish stocks, and labour shortages in regional processing and aquaculture facilities.

Leading companies include JBS Foods, Walker Seafoods Australia, and Seafarms Group, among others.

Key emerging technologies include IoT-enabled cold-chain monitoring, blockchain-based traceability systems, advanced RAS land-based aquaculture, and AI-powered stock assessment and quota management tools improving both sustainable harvest decisions and operational efficiency across the value chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)