Australia Silicon Wafer Market Size, Share, Trends and Forecast by Wafer Size, Type, Application, End Use, and Region, 2026-2034

Australia Silicon Wafer Market Summary:

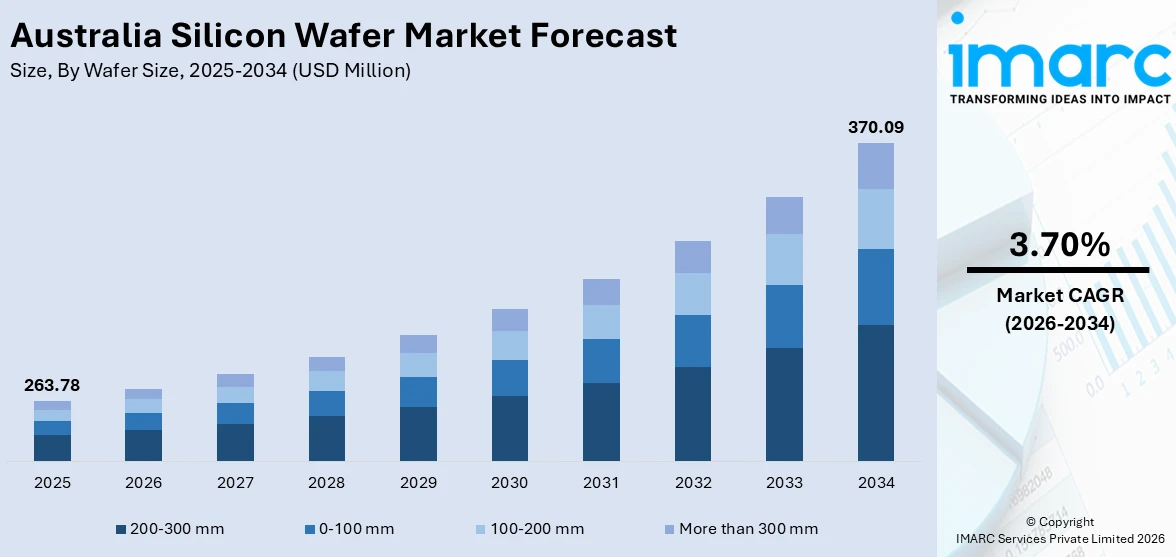

The Australia silicon wafer market size was valued at USD 263.78 Million in 2025 and is projected to reach USD 370.09 Million by 2034, growing at a compound annual growth rate of 3.70% from 2026-2034.

The Australia silicon wafer market is gaining strong momentum as the nation accelerates its renewable energy ambitions and expands its digital infrastructure. Rising demand for photovoltaic cells in solar power installations, the growing semiconductor demand across consumer electronics and telecommunications, and government-backed investments in domestic manufacturing are positively influencing the market. The convergence of clean energy policy commitments and technology sector growth is creating diverse and sustained end-use demand, strengthening the Australia silicon wafer market share across multiple high-growth industries.

Key Takeaways and Insights:

- By Wafer Size: 200-300 mm dominates the market with a share of 42.5% in 2025, driven by its superior efficiency in semiconductor fabrication and its compatibility with high-volume solar cell manufacturing processes.

- By Type: P-type leads the market with a share of 72.5% in 2025, supported by its compatibility with PERC solar cell technology and widespread use across integrated circuits, power electronics, and consumer device applications.

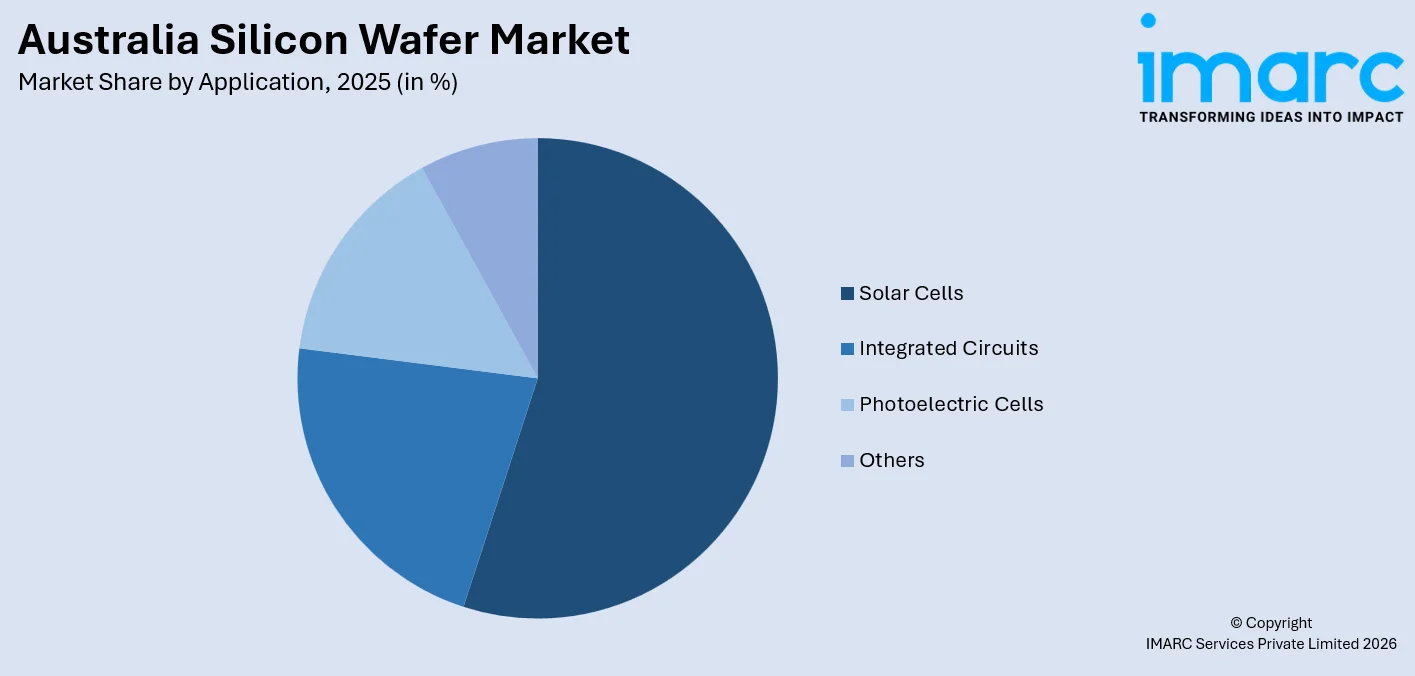

- By Application: Solar cells represent the largest segment with a market share of 52.8% in 2025, reflecting Australia's rapid photovoltaic capacity expansion across residential, commercial, and utility-scale solar projects nationwide.

- By End Use: Consumer electronics dominate the market with a share of 32.5% in 2025, underpinned by strong adoption of smartphones, wearables, IoT devices, and 5G-enabled technologies across the Australian market.

- By Region: Western Australia leads the market with a share of 38.5% in 2025, owing to robust renewable energy expansion, critical minerals processing activity, and the growing solar infrastructure investments across the state.

- Key Players: The Australia silicon wafer market features an evolving competitive landscape, with international suppliers currently dominating supply while emerging domestic manufacturers position themselves to capture the growing demand from the nation's expanding solar and semiconductor industries.

To get more information on this market Request Sample

The Australia silicon wafer market continues to grow as the country increasingly prioritizes renewable energy infrastructure and the development of a sovereign semiconductor supply chain. Rising investments in clean energy projects, particularly solar photovoltaics, are driving the demand for high-purity silicon wafers, which are essential components in solar cells. In 2024, Australia’s clean energy sector recorded $12.7 billion in investment, including $9 billion allocated to large-scale generation projects, highlighting the scale of infrastructure expansion. These developments are encouraging domestic wafer production and technology adoption to meet growing demand from solar, electronics, and semiconductor industries. Government-backed initiatives promoting energy security, sustainable manufacturing, and local production capabilities further strengthen the market growth. Additionally, the focus on high-quality, durable wafers supports innovation in both industrial and renewable energy applications, ensuring Australia can meet the increasing technological and environmental requirements.

Australia Silicon Wafer Market Trends:

Expansion of Renewable Energy Infrastructure

The increasing deployment of renewable energy technologies, particularly solar photovoltaics, is boosting the demand for high-quality silicon wafers in Australia. Solar cells require pure, durable wafers to efficiently convert sunlight into electricity, and large-scale solar farms and distributed installations are driving higher wafer usage. Government policies supporting clean energy, energy security, and domestic manufacturing further reinforce this trend, encouraging continuous improvements in wafer quality and production efficiency. Reflecting these developments, in 2025, Australian manufacturer Halocell Energy launched perovskite-based PV modules designed for low-light conditions targeting indoor and IoT applications. Produced in New South Wales using recyclable materials, the modules exemplify the growth of domestic solar manufacturing and the alignment of industry innovation with government-backed initiatives, supporting long-term expansion of the silicon wafer market.

Government Initiatives and Support

Government programs promoting high-tech manufacturing and semiconductor capabilities are driving growth in Australia’s silicon wafer market by encouraging local production, innovation, and workforce development. Policies providing grants, funding, and incentives strengthen domestic supply chains and reduce dependence on imported wafers. In 2024, the Government of Australia, through ARENA, launched the AUD 1 billion Solar Sunshot program to boost domestic solar PV manufacturing. The initiative targeted the full solar supply chain, including polysilicon, silicon ingots, wafers, cells, and modules, aiming to enhance local production capacity and create high-value jobs. By supporting private investment and commercialization of advanced solar technologies, the program reinforced infrastructure and capabilities for high-quality wafer production, fostering long-term growth and enhancing Australia’s position in the global solar and semiconductor markets.

Rising Demand in Semiconductor Manufacturing

The rapid growth of Australia’s semiconductor sector is a key factor driving demand for high-quality silicon wafers. As electronics, computing, and telecommunications industries expand, manufacturers require wafers with precise specifications and minimal defects to support increasingly complex integrated circuit designs. This trend is encouraging wafer producers to enhance production capacity and adopt advanced manufacturing technologies. Reflecting the sector’s growth, the Australia semiconductor market reached a size of USD 14.8 billion in 2025, according to the IMARC Group. Domestic efforts to strengthen semiconductor fabrication capabilities further amplify wafer consumption, ensuring that suppliers can meet the performance, reliability, and scalability requirements of modern electronic and computing applications. This sustained expansion underlines the critical role of wafers in supporting Australia’s high-tech industrial growth.

Market Outlook 2026-2034:

The Australia silicon wafer market demonstrates solid revenue growth potential throughout the forecast period, driven by increasing demand for semiconductors across consumer electronics, automotive, and renewable energy applications. The market generated a revenue of USD 263.78 Million in 2025 and is projected to reach a revenue of USD 370.09 Million by 2034, growing at a compound annual growth rate of 3.70% from 2026-2034. Strong government support for domestic semiconductor production and increasing integration of chips in industrial automation are further contributing to sustained demand for silicon wafers.

Australia Silicon Wafer Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Wafer Size |

200-300 mm |

42.5% |

|

Type |

P-type |

72.5% |

|

Application |

Solar Cells |

52.8% |

|

End Use |

Consumer Electronics |

32.5% |

|

Region |

Western Australia |

38.5% |

Wafer Size Insights:

- 0-100 mm

- 100-200 mm

- 200-300 mm

- More than 300 mm

200-300 mm dominates with a market share of 42.5% of the total Australia silicon wafer market in 2025.

The 200–300 mm leads the market due to its widespread use in advanced semiconductor manufacturing and compatibility with high-volume production requirements. These wafers support efficient fabrication of integrated circuits used across consumer electronics, automotive systems, and industrial applications. Its ability to enable higher chip yields per wafer and improved cost efficiency makes it a preferred choice among manufacturers. Increasing demand for miniaturized and high-performance electronic components is further driving adoption, reinforcing its dominance in supporting scalable semiconductor production across Australia.

The 200–300 mm segment continues to strengthen its position in the market because of ongoing advancements in fabrication technologies and the growing investments in semiconductor infrastructure. Manufacturers are prioritizing this wafer size to meet evolving requirements for precision, performance, and production efficiency. The segment benefits from established processing standards and compatibility with modern fabrication equipment, enabling consistent output quality. Rising integration of semiconductor devices across sectors, such as renewable energy, telecommunications, and automation is supporting sustained demand, ensuring it remains central to Australia’s semiconductor manufacturing expansion.

Type Insights:

- N-type

- P-type

P-type leads with a market share of 72.5% of the total Australia silicon wafer market in 2025.

P-type dominates the market owing to its extensive application in solar cells and semiconductor devices. This segment benefits from its cost-effectiveness, stable performance, and compatibility with established manufacturing processes. It is widely used in photovoltaic applications, where it supports efficient energy conversion and large-scale deployment. Its material properties enable consistent electrical performance, making it suitable for various industrial and electronic uses. The growing demand for renewable energy solutions and increased semiconductor consumption are supporting its continued dominance, ensuring it remains a key contributor to wafer production and application across Australia.

The dominance of P-type is also driven by the ongoing demand from solar and electronics industries. This segment is preferred for its reliability, ease of processing, and suitability for mass production environments. It aligns well with current manufacturing infrastructure, allowing producers to maintain efficiency and output consistency. Rising investments in clean energy and electronic device manufacturing are further supporting its growth. Its ability to meet performance requirements while maintaining cost advantages ensures it remains highly competitive, reinforcing its role in supporting the expansion of Australia’s semiconductor and renewable energy sectors.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Solar Cells

- Integrated Circuits

- Photoelectric Cells

- Others

The solar cells exhibit a clear dominance with a 52.8% share of the total Australia silicon wafer market in 2025.

Solar cells are the leading segment in the market attributed to the growing focus on renewable energy generation and widespread adoption of solar power systems across residential, commercial, and utility sectors. Silicon wafers serve as a core component in photovoltaic cell manufacturing, enabling efficient energy conversion and long-term performance. Increasing deployment of rooftop solar installations and large-scale solar farms is driving consistent demand for high-quality wafers. Supportive government policies, clean energy targets, and rising awareness regarding carbon emission reduction are further encouraging solar capacity expansion, strengthening the dominance of solar cells within the application landscape across Australia.

Solar cells continue to maintain their leading position as advancements in photovoltaic technology improve efficiency and durability of silicon-based modules. Manufacturers are focusing on enhancing wafer quality, reducing material losses, and optimizing production processes to meet growing demand. Integration of advanced cell architectures and improved energy conversion techniques is supporting higher output from solar installations. Expanding investments in renewable infrastructure and grid integration are also contributing to sustained demand for silicon wafers. As energy transition efforts accelerate, solar cells are expected to remain the primary application segment, supported by consistent innovation and increasing reliance on solar energy solutions across Australia.

End Use Insights:

- Consumer Electronics

- Automotive

- Industrial

- Telecommunications

- Others

The consumer electronics dominates with a market share of 32.5% of the total Australia silicon wafer market in 2025.

Consumer electronics represent the largest segment because of the strong demand for advanced electronic devices and continuous product innovation. Silicon wafers are widely used in the manufacturing of semiconductors that power smartphones, laptops, tablets, and wearable devices. The growing individual reliance on digital technologies and connected devices is driving the demand for high-performance components. Increasing penetration of smart devices and rising adoption of compact, energy-efficient electronics are further supporting wafer consumption. Manufacturers are focusing on improving chip performance and miniaturization, which requires high-quality wafers, reinforcing the dominance of consumer electronics within the end use landscape across Australia.

Consumer electronics continue to hold a leading position as technological advancements drive the development of faster, smaller, and more efficient semiconductor devices. Companies are investing in next-generation chip technologies to support features such as artificial intelligence, high-speed connectivity, and enhanced processing capabilities. The rising popularity of smart home devices, gaming systems, and personal electronics is further increasing demand for semiconductor components. Continuous upgrades and shorter product replacement cycles are also contributing to sustained wafer usage. As digitalization expands across daily life, consumer electronics remain the primary end use segment, supported by ongoing innovation and strong consumer demand in Australia.

Regional Insights:

- Australian Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Western Australia leads with a market share of 38.5% of the total Australia silicon wafer market in 2025.

Western Australia holds the biggest market share driven by its strong presence in mining and raw material processing activities that support the semiconductor value chain. The region is rich in essential minerals such as silica, which is a key input for silicon wafer production. Well-established mining infrastructure and access to high-purity raw materials provide a stable supply base for upstream processing. Additionally, favorable regulatory support and industrial development initiatives encourage investments in material processing and related technologies. The presence of export-oriented industries further strengthens the region’s position, enabling efficient supply of processed materials to both domestic and international semiconductor markets.

Western Australia continues to strengthen its position as a leading silicon production hub due to ongoing investments in resource extraction and processing technologies that enhance material quality and production efficiency. Companies are optimizing supply chains and purification processes to meet growing demand from semiconductor, electronics, and solar industries. Reflecting this focus on sustainable production, in 2025, Western Australia’s Simcoa Operations received $39.8 million in federal funding to expand its Wellesley facility and eliminate coal from silicon production. The investment is expected to reduce emissions by 89%, support low-carbon silicon for solar panels, and maintain domestic manufacturing capacity, reinforcing the region’s industrial ecosystem, supporting local jobs, and enhancing Australia’s role in the global renewable energy and electronics supply chains.

Market Dynamics:

Growth Drivers:

Why is the Australia Silicon Wafer Market Growing?

Technological Advancements in Wafer Fabrication

Innovations in wafer manufacturing processes, including improvements in crystal growth, slicing precision, and surface treatment, are impelling the market growth. Enhanced wafer quality, uniformity, and reduced defect rates increase yield for semiconductor and solar applications, making investment in advanced wafers more attractive. The push for smaller, faster, and more energy-efficient electronic devices necessitates wafers with superior electrical and thermal properties. Continuous research and development (R&D) in materials engineering and process automation support these advancements, driving adoption by manufacturers and encouraging higher production volumes, which collectively contribute to the growth of the silicon wafer market.

Rising Demand for Miniaturized and Energy-Efficient Chips

The ongoing shift toward miniaturization in electronics drives the demand for wafers capable of supporting smaller, more powerful chips. Reduced feature sizes in integrated circuits require wafers with exceptionally low defect rates, high uniformity, and advanced material properties. Energy efficiency requirements in consumer and industrial electronics add pressure for wafers that optimize power consumption and heat dissipation. This convergence of miniaturization and energy performance stimulates wafer producers to enhance manufacturing processes, upgrade facilities, and innovate materials. As a result, demand for advanced silicon wafers continues to rise, sustaining growth across multiple high-tech industries in Australia.

Adoption of Advanced Packaging Technologies

The increasing implementation of advanced semiconductor packaging solutions, such as 3D ICs and system-in-package designs, is driving the demand for high-quality silicon wafers. These technologies require wafers with precise dimensions, minimal warpage, and high surface uniformity to ensure proper stacking and interconnection of chips. As manufacturers aim to deliver smaller, faster, and more efficient devices, the need for wafers capable of supporting complex packaging architectures grows. This trend encourages wafer producers to invest in process optimization and material improvements, directly supporting the market growth and fostering innovation in wafer design and fabrication.

Market Restraints:

What Challenges the Australia Silicon Wafer Market is Facing?

Heavy Import Dependency on Chinese Wafer Production

Australia silicon wafer market is constrained by heavy reliance on imports, creating exposure to external supply chain disruptions. Limited domestic production capacity reduces control over pricing, availability, and lead times for critical semiconductor materials. Any instability in global trade flows or supplier concentration can affect consistent supply for local manufacturers. This dependency increases procurement risks, impacts production planning, and restricts the development of a stable and self-sufficient semiconductor ecosystem.

High Capital Requirements for Domestic Wafer Fabrication

Australia silicon wafer market faces challenges due to the high capital intensity required to establish domestic manufacturing facilities. Significant investment is needed for advanced equipment, controlled production environments, and skilled workforce development. These financial barriers limit new market entrants and slow the expansion of local production capabilities. As a result, progress toward building a competitive and self-reliant semiconductor supply chain remains constrained across the country.

Technical Expertise and Skilled Labor Shortages

Australia’s silicon wafer market is constrained by a limited availability of highly specialized technical expertise required for advanced semiconductor manufacturing processes. Gaps in skills related to crystal growth, materials engineering, and precision fabrication reduce operational efficiency and innovation capacity. Dependence on international talent increases costs and delays project execution, while extended training timelines hinder the rapid development of a skilled domestic workforce needed to support industry growth.

Competitive Landscape:

The Australia silicon wafer market features a competitive landscape largely dominated by international suppliers, with most demand fulfilled through import channels and distributor networks. Domestic production capacity is still developing, with increasing efforts to establish local manufacturing capabilities. Competition is primarily based on product quality, wafer specifications, consistency, and supply reliability. Market dynamics are gradually shifting as government support and industry investments encourage new entrants into both solar-grade and semiconductor-grade wafer production, strengthening the local ecosystem. This transition is expected to enhance supply security, improve competitiveness, and reduce dependence on external sources while supporting the growth of a more resilient and diversified domestic market.

Recent Developments:

- March 2026: The Australian government has granted Major Project Status to Stellar PV for its planned 2 GW polysilicon ingot and wafer facility near Townsville, Queensland. The AUD 400 million project will produce silicon ingots and wafers, supporting a domestic solar supply chain and global market needs. With pre-feasibility studies confirming technical and commercial viability, Stellar PV aims to begin production by late 2028.

- August 2025: Stellar PV has received a AUD 4.7 Million grant from ARENA to conduct a feasibility study for a 2 GW polysilicon ingot and wafer manufacturing facility near Townsville, Queensland. The plant will produce high-purity silicon ingots using the Czochralski method and convert them into silicon wafers, supporting a domestic solar supply chain. This project aimed to strengthen Australia’s renewable energy manufacturing capabilities and provide low-carbon, globally competitive solar components.

Australia Silicon Wafer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Wafer Sizes Covered | 0 - 100 mm, 100 - 200 mm, 200 - 300 mm, More than 300 mm |

| Types Covered | N-type, P-type |

| Applications Covered | Solar Cells, Integrated Circuits, Photoelectric Cells, Others |

| End Uses Covered | Consumer Electronics, Automotive, Industrial, Telecommunications, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Silicon Wafer Market Report

The Australia silicon wafer market size was valued at USD 263.78 Million in 2025.

The Australia silicon wafer market is expected to grow at a compound annual growth rate of 3.70% from 2026-2034 to reach USD 370.09 Million by 2034.

The 200-300 mm dominates the Australia silicon wafer market with 42.5% revenue share in 2025, owing to its superior manufacturing efficiency in both semiconductor chip fabrication and high-efficiency solar photovoltaic cell production.

Key factors driving the Australia silicon wafer market include government programs promoting high-tech manufacturing and semiconductor capabilities, which encourage local production, innovation, and workforce development. For example, in 2024, ARENA’s AUD 1?billion Solar Sunshot program targeted the full solar supply chain, including wafers, to boost domestic production and create high-value jobs.

Major challenges include strong reliance on imported silicon wafers, creating supply chain risks and limited control over availability. High capital investment requirements restrict the development of domestic manufacturing capacity. Additionally, a shortage of skilled professionals in advanced semiconductor production processes constrains industry growth and slows the establishment of a self-sufficient local ecosystem.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)