Australia Smartwatch Market Size, Share, Trends and Forecast by Product, Operating System, Application, Distribution Channel, and Region, 2026-2034

Australia Smartwatch Market Summary:

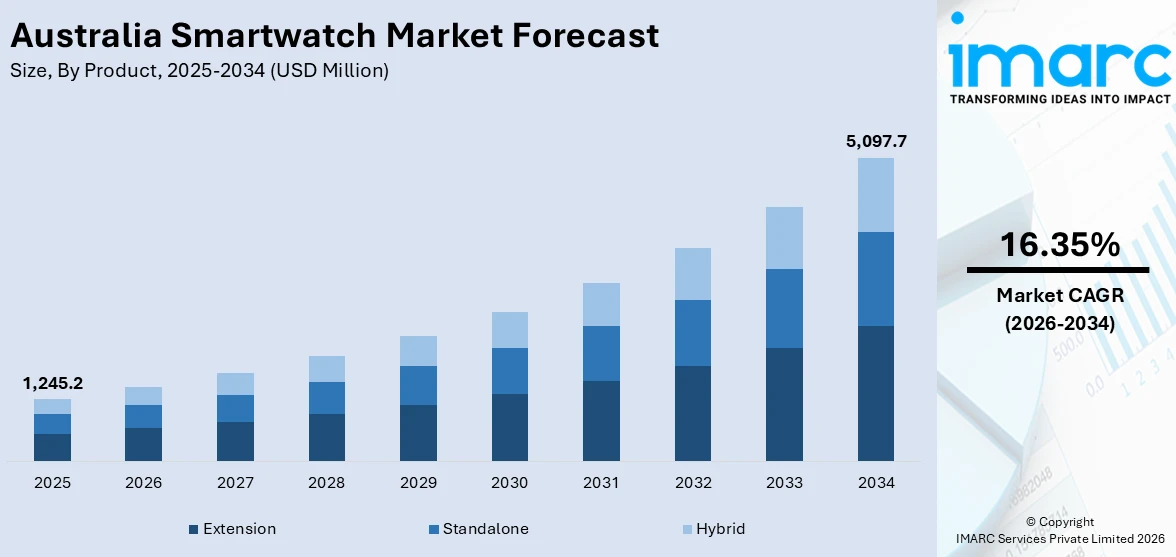

The Australia smartwatch market size was valued at USD 1,245.2 Million in 2025 and is projected to reach USD 5,097.7 Million by 2034, growing at a compound annual growth rate of 16.35% from 2026-2034.

The Australia smartwatch market is experiencing robust expansion fuelled by rising health consciousness, growing fitness awareness, and increasing integration of wearable technology into daily routines. Advancements in sensor capabilities, seamless smartphone connectivity, and evolving consumer preferences for multifunctional devices are strengthening adoption. Expanding digital health ecosystems, supportive government initiatives, and broader retail accessibility are further reinforcing the Australia smartwatch market share.

Key Takeaways and Insights:

- By Product: Extension dominates the market with a share of 55.5% in 2025, owing to the seamless pairing capabilities with smartphones, superior notification management, and advanced health-monitoring features that make extension smartwatches the preferred choice among Australian consumers seeking integrated digital experiences.

- By Operating System: WatchOS leads the market with a share of 48.5% in 2025, reflecting strong consumer loyalty toward the Apple ecosystem, supported by exclusive health features, intuitive interface design, and deep integration with iPhones that drive consistent purchasing patterns across Australian metropolitan areas.

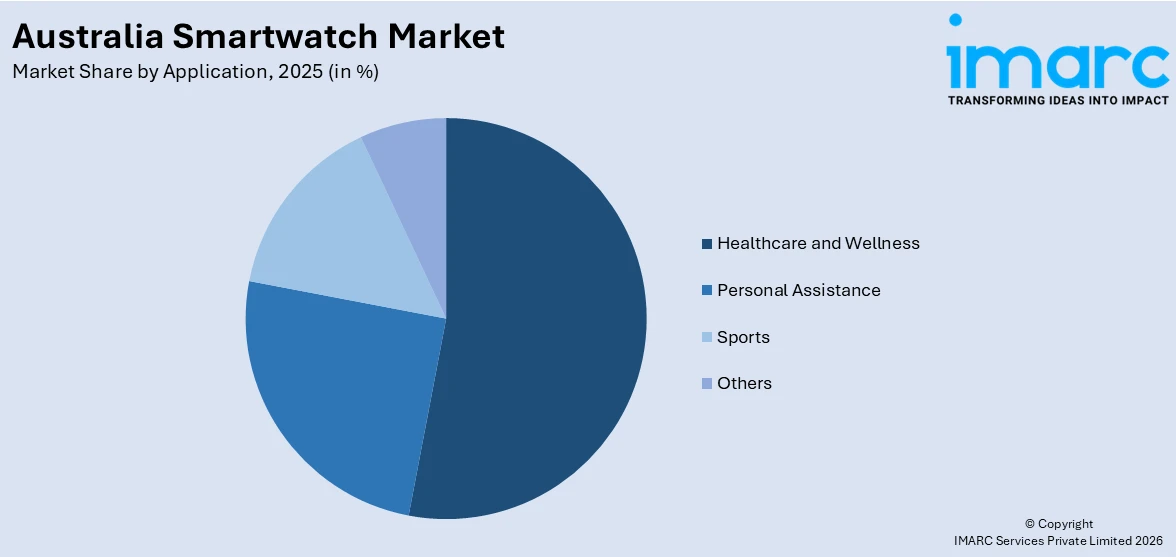

- By Application: Healthcare and wellness represent the biggest segment with a market share of 52.5% in 2025, driven by growing consumer demand for real-time health monitoring capabilities including heart rate tracking, sleep analysis, blood oxygen measurement, and electrocardiogram functionality that support preventive care approaches.

- By Distribution Channel: Offline stores exhibits clear dominance in the market with a share of 58.5% in 2025, as Australian consumers continue to value hands-on product evaluation, personalised in-store assistance, and immediate purchase fulfilment when investing in premium wearable technology devices.

- By Region: Australia Capital Territory & New South Wales is the largest region with 34.8% share in 2025, driven by the concentration of tech-savvy populations in Sydney, higher disposable incomes, robust retail infrastructure, and strong digital health awareness fuelling smartwatch adoption across the region.

- Key Players: Key players drive the Australia smartwatch market by expanding product portfolios, advancing sensor technologies, enhancing health-monitoring capabilities, and strengthening retail and online distribution. Their investments in research and development, brand partnerships, and ecosystem integration boost consumer awareness, accelerate adoption, and ensure consistent product availability across diverse segments.

To get more information on this market Request Sample

The Australia smartwatch market is advancing rapidly as consumers, healthcare providers, and technology companies embrace connected wearable solutions for health management, fitness tracking, and lifestyle enhancement. A major catalyst shaping this growth is the country’s increasing emphasis on preventive healthcare and digital wellness, which supports the long-term viability of smartwatch adoption. For instance, in January 2025, Garmin announced the expansion of its ECG App to customers in Australia with compatible smartwatches including the Venu 3 Series and fēnix 8 Series, marking its first smartwatch feature categorised as a medical device in the country. This regulatory milestone underscores the growing convergence of consumer wearables with clinical-grade health capabilities. Policy support through the National Digital Health Strategy 2023–2028, expanding retail accessibility, and rising interest in personalised fitness insights are contributing to a more favourable environment for smartwatch adoption. These dynamics are positioning the Australia smartwatch market for sustained and meaningful expansion throughout the forecast period.

Australia Smartwatch Market Trends:

Rising demand for advanced health-monitoring wearables

Australian consumers are increasingly adopting smartwatches as preventive health tools rather than simple activity trackers, seeking advanced capabilities such as electrocardiogram monitoring, blood oxygen measurement, and sleep apnea detection. This shift is aligning with broader policy initiatives that are broadening Medicare coverage for chronic care management. For instance, in September 2024, Apple launched the Watch Series 10 in Australia featuring sleep apnea notifications, faster charging, and enhanced water depth sensing, reinforcing the transition toward clinically relevant wearable features that support the Australia smartwatch market growth.

Integration with digital ecosystems and smart home platforms

Smartwatches in Australia are evolving from standalone fitness devices into central components of interconnected digital ecosystems, offering seamless integration with smartphones, home automation systems, and Internet of Things platforms. Consumers increasingly demand the convenience of managing multiple connected devices through a single wearable interface, from controlling smart lighting and thermostats to receiving real-time security alerts. The growing availability of voice-controlled assistants, contactless payment capabilities, and cross-platform synchronisation is reinforcing the role of smartwatches as essential digital hubs within connected Australian households and workplaces.

Growing personalisation and lifestyle-driven wearable design

Australian consumers are increasingly favouring smartwatches that blend advanced functionality with personal style and customisation. Manufacturers are responding by offering interchangeable bands, customisable watch faces, and user-optimised applications that span fitness tracking, professional productivity, and entertainment. This trend toward personalised wearable experiences is strengthening consumer loyalty and broadening the appeal of smartwatches beyond traditional technology enthusiasts. The rising emphasis on fashion-forward designs, premium material options, and tailored wellness interfaces is enabling brands to capture diverse consumer preferences across age groups and lifestyle segments.

Market Outlook 2026-2034:

Australia’s smartwatch market is positioned for sustained advancement, underpinned by policy continuity, expanding health ecosystems, and rising consumer interest in connected wellness solutions. The market generated a revenue of USD 1,245.2 Million in 2025 and is projected to reach a revenue of USD 5,097.7 Million by 2034, growing at a compound annual growth rate of 16.35% from 2026-2034. Increasing adoption of AI-powered health analytics, broader integration of clinical-grade sensors in consumer devices, and growing enterprise demand for workplace safety wearables are expected to open new revenue streams. Expanding 5G and eSIM connectivity, coupled with government support through the National Digital Health Strategy and Medicare-linked health programs, will further accelerate penetration. The convergence of fashion-forward designs with advanced health capabilities is broadening the consumer base across demographics, while competitive pricing strategies and flexible payment plans continue to improve accessibility. These factors collectively position the Australian market for a more competitive, mature, and innovation-driven wearable technology landscape throughout the forecast period.

Australia Smartwatch Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Extension |

55.5% |

|

Operating System |

WatchOS |

48.5% |

|

Application |

Healthcare and Wellness |

52.5% |

|

Distribution Channel |

Offline Stores |

58.5% |

|

Region |

Australia Capital Territory & New South Wales |

34.8% |

Product Insights:

- Extension

- Standalone

- Hybrid

Extension dominates with a market share of 55.5% of the total Australia smartwatch market in 2025.

Extension smartwatches have established themselves as the backbone of Australia's wearable technology landscape by offering seamless connectivity with smartphones, enabling users to access notifications, calls, messaging, and application controls directly from their wrist. The growing smartphone penetration across Australian households, combined with consumer preference for devices that enhance rather than replace their existing mobile experience, has propelled extension smartwatch demand. The convenience of real-time synchronisation, intuitive interface design, and cross-platform compatibility continues to position extension smartwatches as the preferred choice among Australian consumers seeking integrated digital experiences.

The extension segment's continued leadership is further strengthened by the depth of ecosystem integration offered by leading manufacturers, where smartwatches function as natural extensions of smartphone capabilities. Australian consumers increasingly value the ability to manage health data, conduct contactless payments, and control smart home devices through a unified wearable interface tethered to their smartphones. The expanding availability of eSIM support among Australian carriers is further enhancing the versatility of extension smartwatches by enabling cellular connectivity without requiring a separate mobile plan.

Operating System Insights:

- WatchOS

- Android

- Others

WatchOS leads with a share of 48.5% of the total Australia smartwatch market in 2025.

WatchOS maintains a commanding presence in the Australian smartwatch market, benefiting from the strong brand loyalty and deeply integrated ecosystem cultivated across the country. The operating system's proprietary health features, including advanced electrocardiogram monitoring, blood oxygen tracking, fall detection, and sleep apnea notifications, have positioned it as a trusted platform for health-conscious consumers. The intuitive user interface, consistent software refinement, and exclusive application availability further reinforce WatchOS as the preferred operating system among Australian smartwatch buyers seeking reliability, security, and seamless device interoperability.

The continued evolution of WatchOS through annual software updates has reinforced its competitive advantage by introducing features such as adaptive workout tracking, personalised health insights, and enhanced voice assistant integration. Australian consumers benefit from seamless compatibility between WatchOS devices and the broader connected ecosystem including smartphones, tablets, laptops, and wireless earbuds. The regular introduction of refined training load tracking, overnight health metrics, and customisable activity monitoring capabilities continues to deepen user engagement and support sustained market leadership across diverse consumer demographics throughout Australia.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Personal Assistance

- Healthcare and Wellness

- Sports

- Others

Healthcare and wellness represent the largest segment, accounting for 52.5% of the total Australia smartwatch market in 2025.

Given the country's increasing emphasis on proactive health management and preventative care, the healthcare and wellness application category has become the main source of income in the Australian smartwatch market. Smartwatches are being used more and more by Australian consumers to measure vital signs, manage chronic diseases, and access real-time health analytics that supplement clinical consultations. Consumer wearables are evolving into useful health management tools that close the gap between professional medical oversight and personal wellness tracking thanks to the incorporation of clinical-grade sensors that can identify irregular heart rhythms, track respiratory patterns, and evaluate sleep quality.

The integration of consumer wearables with healthcare applications is accelerating due to institutional acceptance and government support. National digital health regulations and expanding telehealth frameworks are promoting an environment where smartwatches serve as gateways to interconnected health ecosystems. Further aligning smartwatch health aspects with official healthcare pathways, the expansion of public healthcare coverage for chronic care management is promoting adoption among older populations and those with long-term disorders. These developments support the notion that smartwatches are mostly used for wellness and healthcare, which is driving up demand in Australia.

Distribution Channel Insights:

- Online Stores

- Offline Stores

Offline stores hold the largest share at 58.5% of the total Australia smartwatch market in 2025.

Due to consumer preferences for in-store personalized coaching, hands-on product inspection, and instant fulfillment when buying high-end wearables, offline retail channels continue to dominate distribution in the Australian smartwatch industry. Along with large electronics retailers, flagship brand stores are important touchpoints where customers can evaluate comfort, compare features, and get professional advice. The tactile aspect of smartwatch purchases, where factors like band fit, display quality, and interface responsiveness affect decisions, keeps physical retail spaces relevant as the main means of distribution in both metropolitan and regional Australian markets.

The experiential element of smartwatch purchasing, where customers frequently try to evaluate wearable comfort and design aesthetics before committing to a purchase, further supports the robustness of offline distribution. Through trade-in programs that encourage upgrades, live demonstrations, and designated wearable technology zones, retailers are improving in-store experiences. Furthermore, a wider range of consumers in Australian metropolitan and regional centers may now afford expensive smartwatches because to the availability of flexible payment plans like buy-now-pay-later alternatives at physical retailers.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represents the leading segment with a 34.8% share of the total Australia smartwatch market in 2025.

With Sydney as Australia's largest metropolitan center, as well as the concentration of tech-savvy consumers, corporate offices, and upscale retail infrastructure, New South Wales and the Australian Capital Territory lead the regional smartwatch market. Strong internet literacy, greater average disposable incomes, and an established network of flagship stores and electronics merchants all help the region's adoption of smartwatches. The region's wide range of consumer groups consistently demand cutting-edge wearable technology due to the region's sizable urban professional workforce and deeply embedded fitness and wellness culture.

The existence of important government agencies in the ACT, which promote the implementation of digital health policies and the need for wearable technology in the public sector, further solidifies the region's leadership. A favorable demand environment for high-end smartwatches with cutting-edge health-monitoring functions is created by Sydney's thriving exercise culture and rising health consciousness among metropolitan professionals. New South Wales and ACT are emerging as Australia's leading hubs for linked health wearable adoption due to the growth of telehealth services and the growing incorporation of wearable health data into clinical workflows.

Market Dynamics:

Growth Drivers:

Why is the Australia Smartwatch Market Growing?

Increasing consumer focus on preventive healthcare and wellness monitoring

The adoption of smartwatches throughout Australia is being fundamentally accelerated by the country's increasing emphasis on preventive health management. Customers are looking for wearable devices that offer ongoing insights into critical health metrics including heart rate variability, blood oxygen saturation, sleep quality, and stress levels as they move away from reactive healthcare techniques and toward proactive wellness monitoring. Australian urban and suburban populations are experiencing a wider cultural shift toward fitness awareness and holistic well-being, which is intensifying this behavioral change. Supportive government regulations and institutional approvals that encourage the incorporation of wearable technology into healthcare delivery frameworks are further solidifying the match between consumer health priorities and smartwatch capabilities. The line separating leisure gadgets from medical instruments is getting thinner as clinical-grade functions like sleep apnea diagnosis, irregular heart rhythm alarms, and ECG monitoring become commonplace in consumer smartwatches. Consumer trust in smartwatches as authentic wellness management tools is being strengthened by the increasing acknowledgement of wearable-generated health data by insurers and medical experts, which is propelling steady market expansion across all consumer categories in Australia.

Expanding digital connectivity and ecosystem integration

Strong demand dynamics are being created by smartwatches' increasing integration into Australia's larger digital environment as users look for unified platforms for entertainment, productivity, and communication. These days, smartwatches serve as crucial hubs in networks that include cloud-based apps, smart home appliances, automobile systems, and smartphones. Wearables are evolving from basic accessories into essential daily companions that improve convenience and efficiency in a variety of spheres of life as a result of this convergence. Through the extension of eSIM support, next-generation network coverage, and companion data plans that allow smartwatches to connect independently, Australian telecom companies are significantly contributing to the acceleration of this trend. Consumer reliance on smartwatches as central digital hubs is being strengthened by the expanding availability of contactless payment features, integrated navigation capabilities, and voice-activated smart assistant functionality. These features contribute to both new user acquisition and upgrade cycles. Long-term market demand is being strengthened by the rising integration of smartwatches into Australian customers' everyday digital workflows as cross-platform compatibility improves and manufacturers expand their relationships with software developers and service providers.

Supportive regulatory environment and government digital health initiatives

By supporting the use of wearable technology in healthcare delivery and preventive care, Australia's regulatory environment and government health initiatives are laying the groundwork for the growth of the smartwatch market. Both consumer adoption and institutional purchases of linked health devices are being encouraged by policies that acknowledge wearable-generated health data as an adjunct to clinician evaluations. In order to create a policy climate that facilitates the integration of wearable technology across public and private health systems, national digital health policies prioritize connected, person-centered, and data-driven healthcare. The way health authorities are categorizing health-oriented wearables is changing in tandem with these regulatory initiatives, giving manufacturers more precise guidelines for where to place devices with clinical features. Smartwatch health features are being more integrated into formal healthcare pathways as public healthcare coverage for chronic care management expands, encouraging adoption among older and health-vulnerable populations. The Australian smartwatch market is anticipated to gain from increased institutional confidence, broader reimbursement pathways, and deeper integration into national health monitoring ecosystems as regulatory frameworks continue to develop and acknowledge the role of consumer wearables in supporting clinical outcomes.

Market Restraints:

What Challenges the Australia Smartwatch Market is Facing?

High price sensitivity among mainstream consumers

The high cost of sophisticated smartwatches continues to be a major obstacle to their wider adoption in Australia, especially among consumers who are price conscious and may consider feature-rich wearables to be luxuries rather than necessities. Leading manufacturers' flagship models are expensive, making them inaccessible to younger consumers, students, and those with lower incomes. Affordability issues have been somewhat resolved by buy-now-pay-later programs and promotional discounts, but some prospective customers are discouraged from entering the market by the ongoing costs of premium subscriptions, cellular connectivity plans, and accessory purchases, which raise the overall cost of ownership.

Data privacy and security concerns

Some Australian consumer sectors are hesitant to adopt smartwatches due to growing knowledge of the data privacy dangers connected with continuous biometric monitoring. Concerns over data storage, third-party sharing, and potential breaches are raised by the sensitive health data that smartwatches gather, such as heart rate patterns, sleep patterns, location tracking, and physiological parameters. Manufacturers trying to strike a balance between innovation, compliance, and consumer trust have additional challenges due to the changing regulatory environment, which includes the Therapeutic Goods Administration's examination of health-related marketing claims and the larger debate around AI governance in healthcare.

Limited differentiation and upgrade fatigue

As Australian consumers see declining returns on new model purchases, the incremental nature of smartwatch updates year over year is slowing replacement cycles. Existing smartwatch customers may put off upgrading for several product cycles because each iteration offers only slight enhancements in display brightness, battery life, or sensor quality rather than revolutionary feature additions. The endurance of contemporary products, which frequently retain performance relevance for several years, adds to this upgrade fatigue by making it less urgent for customers to purchase newer models.

Competitive Landscape:

Global technology manufacturers are vying for market share in Australia's smartwatch market by expanding their ecosystems, developing new products, and forming strategic retail alliances. To set themselves apart from the competition, businesses are investing in the creation of sophisticated health-monitoring devices, analytics driven by AI, and customized user experiences. Expanding distribution networks, adaptable pricing policies, and partnerships with telecom companies and healthcare providers all contribute to increased competition. Premium customization choices, sustainability-focused designs, and locally relevant product features are helping market participants target specific consumer niches. Because of this, manufacturers are always improving their tactics to increase brand loyalty, speed up product uptake, and profit from Australia's growing trend for connected wearable health and lifestyle technology.

Australia Smartwatch Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Extension, Standalone, Hybrid |

| Operating Systems Covered | WatchOS, Android, Others |

| Applications Covered | Personal Assistance, Healthcare and Wellness, Sports, Others |

| Distribution Channels Covered | Online Stores, Offline Stores |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Smartwatch Market Report

The Australia smartwatch market size was valued at USD 1,245.2 Million in 2025.

The Australia smartwatch market is expected to grow at a compound annual growth rate of 16.35% from 2026-2034 to reach USD 5,097.7 Million by 2034.

Extension dominated the market with a share of 55.5%, driven by seamless smartphone integration, advanced notification management, and growing consumer preference for connected wearable devices that complement existing mobile ecosystems across Australian metropolitan and regional markets.

Key factors driving the Australia smartwatch market include increasing consumer health consciousness, expanding digital health infrastructure, supportive government initiatives, growing ecosystem integration, advancing sensor technologies, and rising demand for personalised fitness and wellness monitoring capabilities.

Major challenges include high premium device pricing, data privacy and security concerns, limited year-over-year differentiation, consumer upgrade fatigue, regulatory complexity around health claims, and accessibility barriers in regional and rural areas.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)