Australia Steel Market Size, Share, Trends and Forecast by Type, Product, Application, and Region, 2026-2034

Australia Steel Market Summary:

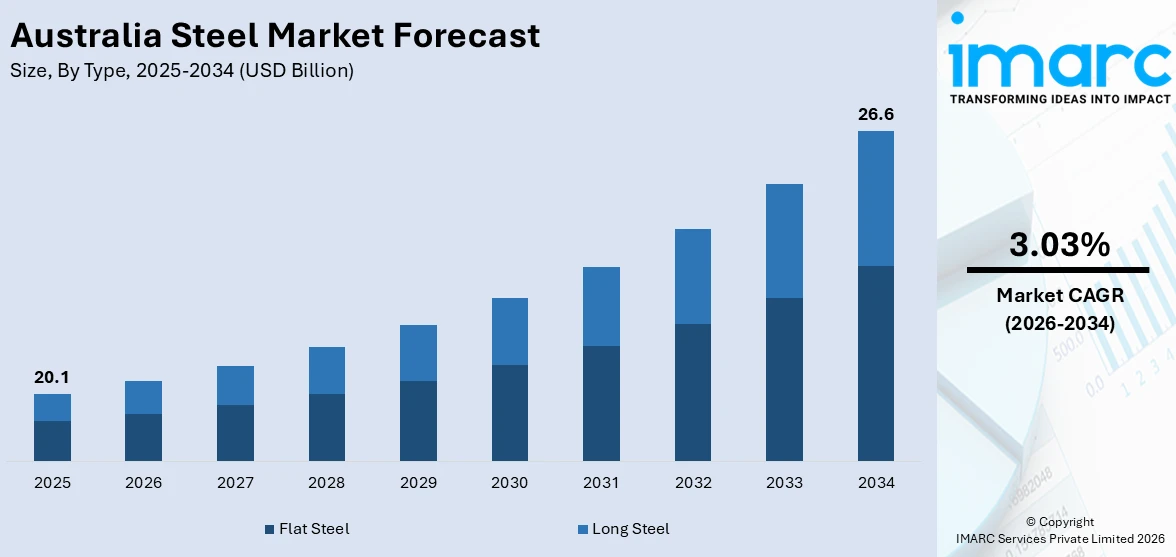

The Australia steel market size was valued at USD 20.1 Billion in 2025 and is projected to reach USD 26.6 Billion by 2034, growing at a compound annual growth rate of 3.03% during 2026-2034.

The Australia steel market is growing, underpinned by large-scale infrastructure investment, rising residential and commercial construction activity, and the accelerating transition to low-emission steelmaking technologies. The growing government expenditure on transportation networks, renewable energy installations, and defense modernization is reinforcing consistent steel demand. Domestic manufacturing initiatives, strategic export partnerships with Asia-Pacific economies, and increasing adoption of electric arc furnace and hydrogen-based production methods are collectively contributing to the Australia steel market share.

Key Takeaways and Insights:

- By Type: Flat steel dominates the market with a share of 52.4% in 2025, driven by its broad applications across construction, automotive manufacturing, and renewable energy infrastructure where high-strength, formable sheet and plate products are essential.

- By Product: Structural steel leads the market with a share of 34.2% in 2025, anchored by sustained demand from large-scale building and civil infrastructure projects across Australian cities and regional growth corridors where robust load-bearing frameworks are critical.

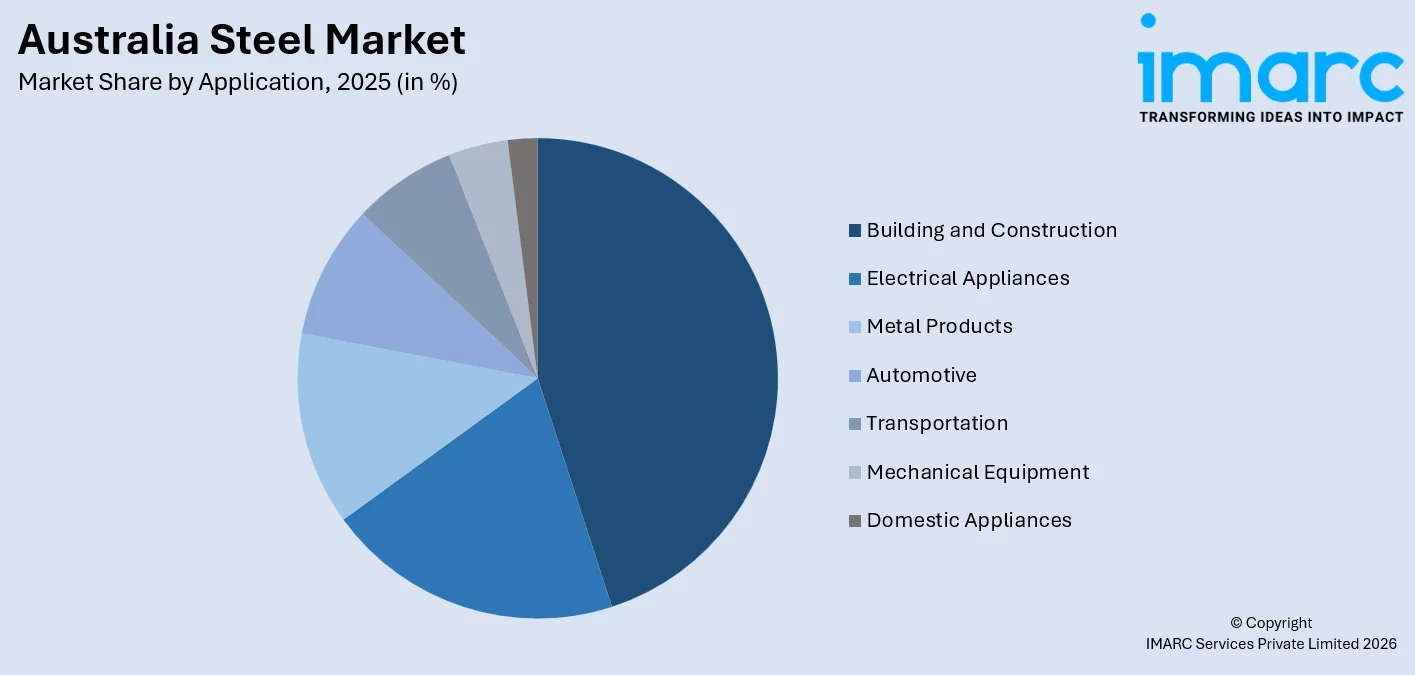

- By Application: Building and construction represents the largest segment with a market share of 42.3% in 2025, reflecting Australia's ongoing urban development, public infrastructure pipeline, and growing investment in residential and commercial building projects across major metropolitan regions.

- By Region: Australia Capital Territory & New South Wales dominates the market with a share of 32.1% in 2025, owing to Sydney's infrastructure expansion, major construction projects, and the concentration of industrial and manufacturing activity in the region.

- Key Players: The Australia steel market is competitively structured, with domestic producers and global steel majors competing across flat and long product categories, differentiated by sustainability credentials, production efficiency, and proximity to construction and infrastructure end markets. Some of the key players in the market include Australian Steel, BlueScope Steel Limited, Greensteel Australia, InfraBuild, LIBERTY Steel Group, Southern Steel Group, Swiss Steel Group, Vulcan Australia.

To get more information on this market Request Sample

The Australia steel market is gaining consistent momentum as infrastructure investment and decarbonization initiatives converge to reshape industry fundamentals. Rising government spending on transportation networks, renewable energy projects, and urban development is increasing demand for structural steel and related products across construction and industrial sectors. Furthermore, the industry is undergoing a transition toward low-carbon steel production as companies invest in cleaner technologies and energy-efficient manufacturing processes. Reflecting this shift, in 2024, Greensteel Australia partnered with Danieli to develop a 600,000-ton-per-year rolling mill in New South Wales powered entirely by green hydrogen. The facility utilized a hydrogen-fueled reheating furnace designed to eliminate fossil fuel use and significantly reduce emissions during steel production. Such investments highlight the growing focus on sustainable steel manufacturing while supporting domestic supply capabilities. The combination of infrastructure expansion, industrial modernization, and environmental transition continues to strengthen long-term demand for steel across Australia.

Australia Steel Market Trends:

Technological Advancements in Steel Processing and Fabrication

Technological innovation in steel manufacturing and processing is improving productivity and operational efficiency across the Australian steel industry. Steel producers are increasingly adopting advanced fabrication technologies, automation systems, and digital production management tools to enhance product quality and streamline manufacturing processes. Modern steel processing methods also enable the production of specialized steel grades designed to meet the evolving needs of construction, automotive, and industrial sectors. Reflecting this trend, in 2025, Greensteel Australia announced plans to invest $1.6 billion to build a new steel plant focused on low-carbon steel production. The facility planned to incorporate a direct reduced iron unit, electric arc furnaces, and advanced rolling mills supplied by Italy’s Danieli, demonstrating how modern manufacturing technologies are supporting innovation, efficiency improvements, and sustainable steel production in Australia.

Expansion of Renewable Energy Infrastructure Projects

Large renewable energy developments, including wind farms, solar power installations, and electricity transmission networks, require durable structural materials capable of supporting long-term energy production systems. Steel is widely used in wind turbine towers, transmission structures, and supporting frameworks due to its strength and reliability in large-scale infrastructure. Reflecting this growing demand, in 2025, the Australian Government announced a $500 million investment through the Future Made in Australia Innovation Fund to support domestic steelmaking and manufacturing capacity. Delivered through ARENA, the initiative focuses on strengthening local production of materials required for renewable energy infrastructure, including wind tower steel fabrication. Such policy support is encouraging industry expansion while reinforcing steel’s critical role in Australia’s renewable energy transition.

Government-Led Support for Green Iron and Domestic Supply Chain Security

Government-led initiatives aimed at strengthening domestic steel supply chains are emerging as an important trend shaping the Australia steel market. Policymakers are increasingly introducing financial support programs to secure the long-term viability of local steel production while ensuring that Australian iron ore remains competitive in a global market transitioning toward lower-emission manufacturing. These initiatives focus on supporting domestic processing capacity, stabilizing key production facilities, and promoting the development of green iron as a strategic industrial resource. Reflecting this trend, in 2025, Australia launched a A$1 billion Green Iron Fund to support low-carbon iron production and reinforce domestic steel supply chains. The package included an initial A$500 million allocation aimed at stabilizing the Whyalla steelworks in South Australia while supporting the broader transition toward sustainable steel production.

Market Outlook 2026-2034:

The Australia steel market is projected to experience growth during the forecast period, supported by rising infrastructure development, expansion of construction activities, and increasing demand from transportation and manufacturing sectors. Government investments in transportation networks, renewable energy infrastructure, and urban development projects are strengthening steel consumption across the country. The market generated a revenue of USD 20.1 Billion in 2025 and is projected to reach a revenue of USD 26.6 Billion by 2034, growing at a compound annual growth rate of 3.03% from 2026-2034.

Australia Steel Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Flat Steel |

52.4% |

|

Product |

Structural Steel |

34.2% |

|

Application |

Building and Construction |

42.3% |

|

Region |

Australia Capital Territory & New South Wales |

32.1% |

Type Insights:

- Flat Steel

- Long Steel

Flat steel dominates with a market share of 52.4% of the total Australia steel market in 2025.

Flat steel holds the biggest market share because of its extensive use across multiple industrial and commercial applications. Industries, such as construction, automotive manufacturing, infrastructure development, and machinery production, rely heavily on flat steel products, including Australia metal sheets market, plates, and coils. This material is widely used in building structures, roofing systems, pipelines, and industrial equipment due to its strength, durability, and adaptability in fabrication processes. The construction sector in particular drives large demand for flat steel as it is used in structural components, cladding, and reinforced building frameworks. Continuous infrastructure expansion and industrial development across Australia further strengthen the demand for flat steel products.

The automotive and manufacturing sectors also contribute significantly to the strong demand for flat steel in Australia. Flat steel is widely used in the production of vehicle bodies, appliance components, and heavy machinery due to its ability to be shaped, welded, and processed efficiently. Manufacturers prefer flat steel products for their consistency in thickness and surface quality, which supports precision engineering applications. In addition, flat steel is extensively utilized in shipbuilding, energy infrastructure, and transportation equipment. The increasing investment in infrastructure projects and the steady growth of manufacturing activities across the country continue to reinforce the leading share of flat steel in the market.

Product Insights:

- Structural Steel

- Prestressing Steel

- Bright Steel

- Welding Wire and Rod

- Iron Steel Wire

- Ropes

- Braids

Structural steel leads with a market share of 34.2% of the total Australia steel market in 2025.

Structural steel represents the largest segment due to its widespread use in construction, infrastructure, and large-scale engineering projects. It is widely utilized in building frameworks, bridges, industrial facilities, and commercial structures because of its high strength, durability, and load-bearing capacity. Structural steel products, such as beams, columns, and sections are essential components in modern construction projects that require stable and long-lasting structural support. The growing development of residential buildings, commercial complexes, and public infrastructure across Australia continues to drive the demand for structural steel. Its ability to support large structures while maintaining design flexibility makes it a preferred material for construction activities.

The expansion of transportation, defense, and industrial infrastructure across Australia is strengthening the demand for structural steel products due to their strength, durability, and suitability for large-scale construction projects. Structural steel is widely used in infrastructure such as transport facilities, industrial plants, and heavy equipment structures because it supports complex designs and high load-bearing requirements. Reflecting this demand, in 2025, Australia reported that more than 1,800 tons of structural steel were used to construct a major aircraft maintenance hangar in northern Adelaide, with over half sourced from Whyalla Steelworks. Continued infrastructure development and industrial investment are reinforcing the importance of structural steel across Australia’s construction and manufacturing sectors.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Building and Construction

- Electrical Appliances

- Metal Products

- Automotive

- Transportation

- Mechanical Equipment

- Domestic Appliances

Building and construction exhibits a clear dominance with a 42.3% share of the total Australia steel market in 2025.

Building and construction dominates the market driven by the extensive use of steel in residential, commercial, and infrastructure development projects across the country. Steel is widely used in structural frameworks, roofing systems, reinforcement bars, and cladding materials due to its strength, durability, and ability to support modern architectural designs. Construction companies rely on steel to build high-rise buildings, bridges, industrial facilities, and public infrastructure that require long-lasting and reliable structural support. The material’s flexibility in fabrication and installation also allows engineers and architects to design complex structures efficiently. Continuous urban development and population growth across major Australian cities continue to strengthen steel demand in construction activities.

The expansion of large infrastructure projects and rising government investment in transportation and urban development continue to strengthen steel demand across Australia’s construction sector. Steel is widely used in highways, rail networks, airports, and energy infrastructure due to its strength, durability, and suitability for heavy-load structural applications. Reflecting this momentum, in 2026, Sydney Metro West advanced into a major construction phase after authorities awarded approximately $7.7 billion in contracts covering stations, track systems, trains, and operations. The 24-km underground rail line connecting Parramatta with Sydney’s central business district highlights how major infrastructure programs are increasing the consumption of structural and reinforcement steel across Australia’s building and construction industry.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The Australia Capital Territory and New South Wales dominate with a market share of 32.1% of the total Australia steel market in 2025.

Australia Capital Territory and New South Wales lead the market attributed to the high concentration of construction, infrastructure development, and commercial projects across these areas. Major urban centers like Sydney and Canberra continue to experience strong demand for residential housing, commercial buildings, and public infrastructure, all of which require significant volumes of steel. Structural steel, reinforcement bars, and fabricated steel components are widely used in high-rise buildings, bridges, transportation systems, and institutional facilities. The ongoing expansion of urban infrastructure and population growth in these regions further increases the need for durable construction materials. As a result, steel consumption remains consistently high across major development projects.

Large-scale infrastructure development and industrial expansion in regions such as New South Wales and the Australian Capital Territory are strengthening steel demand across construction and manufacturing sectors. Government investment in transportation networks, public infrastructure, and industrial facilities requires substantial volumes of steel for structural reinforcement and long-term durability. Reflecting this trend, in 2024, Green Steel Australia contracted Danieli to build a 600,000-ton-per-year rolling mill in New South Wales for producing rebar and coil products. The project incorporated a hydrogen-powered reheating furnace and advanced automation technologies, highlighting the region’s role in supporting both infrastructure growth and sustainable steel production.

Market Dynamics:

Growth Drivers:

Why is the Australia Steel Market Growing?

Adoption of Sustainable and Low-Carbon Steel Production Technologies

Steel producers in Australia are increasingly investing in technologies that reduce carbon emissions and improve energy efficiency in manufacturing processes. The industry is gradually adopting cleaner production methods, greater recycling of steel scrap, and advanced low-emission technologies to align with evolving environmental regulations and sustainability goals. As governments and industries place greater emphasis on responsible manufacturing, demand for sustainable steel products is increasing across construction, infrastructure, and industrial sectors. Reflecting this transition, in 2025, BlueScope participated as a Gold Partner at the TRANSFORM 2025 sustainability conference hosted by the Green Building Council of Australia, which focused on strategies to decarbonize the steel industry. Such initiatives demonstrate how industry collaboration and sustainability commitments are accelerating modernization within steel production while strengthening the long-term competitiveness of Australia’s steel market.

Growing Collaboration Between Industry and Research Institutions

Collaboration between steel manufacturers and research institutions is becoming increasingly important in driving technological advancement across Australia’s steel sector. These partnerships support the development of innovative production methods, sustainable manufacturing technologies, and resource-efficient steelmaking processes. Joint research initiatives also enable knowledge exchange between industry experts and academic researchers, accelerating the commercialization of new technologies. Reflecting this trend, in 2024, Tata Steel and Monash University signed an agreement to establish a Centre for Innovation on Environment and Intelligent Manufacturing. The center focused on research areas, including decarbonization, resource recovery, and advanced manufacturing systems, supporting the development of next-generation steel production technologies while strengthening research cooperation within the industry.

Growth in Residential and Commercial Construction Activities

The expansion of residential housing developments and commercial building projects is strengthening the demand for steel products across Australia. Rapid urbanization, population growth, and increasing housing requirements are encouraging large-scale residential construction across metropolitan regions. Steel is widely used in building frameworks, reinforcement bars, roofing structures, and structural components due to its durability and versatility. Commercial real estate developments, including office complexes, retail centers, and mixed-use properties, also rely heavily on steel for construction. Developers prefer steel materials because they enable faster construction timelines and provide strong structural integrity. Continuous growth in real estate development is therefore supporting stable demand for steel products.

Market Restraints:

What Challenges the Australia Steel Market is Facing?

Import Competition Pressuring Domestic Fabricators and Producers

Australian steel fabricators and producers face increasing pressure from imported steel products entering the domestic market at competitive prices. This rising import presence is reducing the competitiveness of locally manufactured steel and tightening profit margins for domestic companies. As imported materials gain wider adoption across construction and manufacturing applications, local producers face growing challenges in maintaining stable demand and operational profitability.

Volatile Global Steel Prices and Supply Chain Disruptions

The Australian steel market continues to experience instability due to fluctuations in global steel prices and periodic supply chain disruptions. Changes in international trade dynamics and shifting demand patterns create uncertainty in steel procurement and pricing. These market conditions make cost planning more difficult for manufacturers and construction firms, increasing financial risks and operational challenges across the steel supply chain.

Labor Shortages and Skilled Workforce Constraints

Australia’s steel fabrication and construction sectors are experiencing increasing pressure from shortages of skilled labor across key operational roles. Limited availability of trained workers is affecting production capacity and delaying project timelines across the industry. As demand for steel products grows alongside infrastructure and construction development, workforce constraints are becoming a critical factor limiting operational expansion.

Competitive Landscape:

The Australia steel market features a competitive structure characterized by the presence of integrated domestic steel producers, specialized fabrication companies, and international material suppliers operating across different segments of the value chain. These participants compete by offering diverse steel product portfolios that serve construction, infrastructure, manufacturing, and industrial applications. Companies also differentiate through production capacity, processing capabilities, supply reliability, and regional distribution networks. Strong logistics and delivery capabilities enable suppliers to support large infrastructure and commercial construction projects across various states. In addition, sustainability initiatives, including lower-emission steel production methods and recycling practices, are becoming important competitive factors. Firms are also focusing on strengthening customer relationships, improving service responsiveness, and expanding fabrication capabilities to enhance their market positioning.

Some of the key players in the market include:

- Australian Steel

- BlueScope Steel Limited

- Greensteel Australia

- InfraBuild

- LIBERTY Steel Group

- Southern Steel Group

- Swiss Steel Group

- Vulcan Australia

Recent Developments:

- March 2026: Metal Logic acquired a 1,000-hectare site in Western Australia’s Pilbara region to deploy its modular clean steel smelting technology. The project aims to establish an initial one-million-ton-per-year facility capable of producing lower-emission steel while processing a wide range of iron ore grades. The initiative supports Australia’s push to develop domestic green steel production and create value-added processing near major mining regions.

- November 2025: The Western Australian government launched an Expression of Interest to encourage the use of locally produced green steel in major public infrastructure projects. The initiative aims to support domestic manufacturing, strengthen supply chains, and add value to Australia’s iron ore resources. Green steel could be used in projects such as railways, roads, hospitals, and energy infrastructure as part of the state’s “Made in WA” economic strategy.

Australia Steel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Flat Steel, Long Steel |

| Products Covered | Structural Steel, Prestressing Steel, Bright Steel, Welding Wire and Rod, Iron Steel Wire, Ropes, Braids |

| Applications Covered | Building and Construction, Electrical Appliances, Metal Products, Automotive, Transportation, Mechanical Equipment, Domestic Appliances |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Australian Steel, BlueScope Steel Limited, Greensteel Australia, InfraBuild, LIBERTY Steel Group, Southern Steel Group, Swiss Steel Group, Vulcan Australia, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Steel Market Report

The Australia steel market size was valued at USD 20.1 Billion in 2025.

The Australia steel market is expected to grow at a compound annual growth rate of 3.03% during 2026-2034 to reach USD 26.6 Billion by 2034.

Flat steel dominates with a revenue share of 52.4% in 2025, driven by broad demand across building and construction, automotive manufacturing, and renewable energy infrastructure applications requiring high-strength, formable steel products.

Key factors driving the Australia steel market include the rapid expansion of renewable energy infrastructure, which requires strong structural materials for wind turbines, solar installations, and transmission networks. In 2025, the Australian Government announced a $500 million investment through the Future Made in Australia Innovation Fund to support domestic steel manufacturing for renewable energy components.

Major challenges include low-cost import competition pressuring domestic fabricators, global steel price volatility and supply chain disruptions, and acute labor shortages threatening fabrication and construction capacity across Australian steel supply chains.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade