Australia Thermal Processing Equipment Market Size, Share, Trends and Forecast by Equipment Type, Process Type, Heating Source, Automation Level, End-Use Industry, and Region, 2026-2034

Australia Thermal Processing Equipment Market Summary:

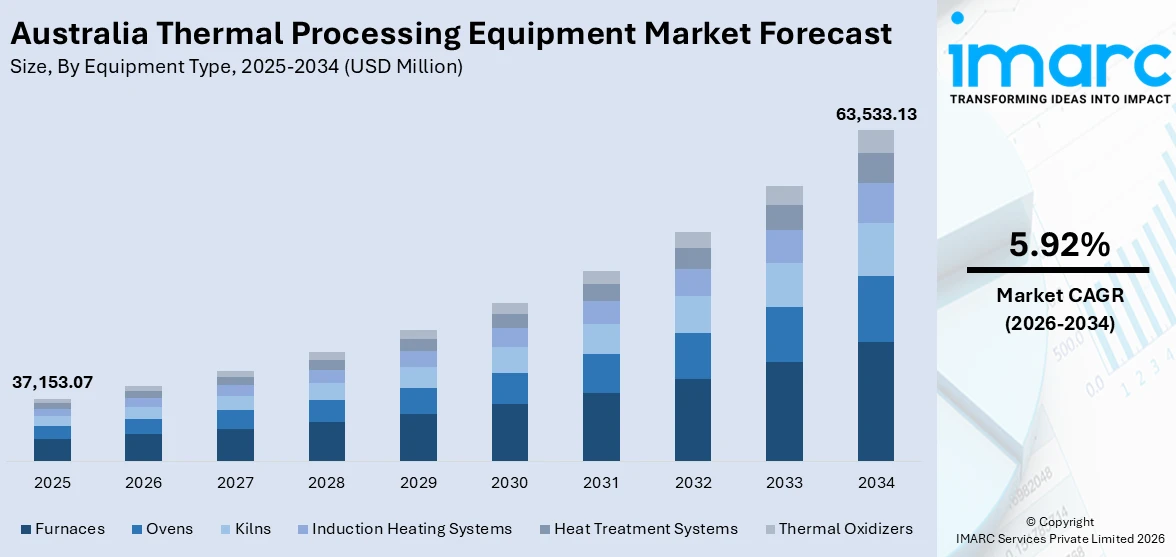

The Australia thermal processing equipment market size was valued at USD 37,153.07 Million in 2025 and is projected to reach USD 63,533.13 Million by 2034, growing at a compound annual growth rate of 5.92% from 2026-2034.

As the country's manufacturing, mining, and metals processing industries rapidly modernize, the market for thermal processing equipment in Australia is growing steadily. The need for sophisticated furnaces, kilns, and heat treatment systems is increasing as a result of increased focus on energy transition, operational efficiency, and sustainable manufacturing practices. Growing automation and government-supported decarbonization programs are changing the thermal processing environment and bolstering Australia's market dominance in thermal processing equipment.

Key Takeaways and Insights:

- By Equipment Type: Furnaces dominate the market with a share of 32.5% in 2025, driven by escalating demand for high-capacity heating solutions across metals smelting, mineral refining, and advanced manufacturing operations throughout Australia.

- By Process Type: Heat treatment leads the market with a share of 28.5% in 2025, owing to extensive requirements for hardening, tempering, and stress-relieving processes in automotive, aerospace, and mining equipment manufacturing sectors.

- By Heating Source: Electric thermal processing holds the biggest share at 42.5% in 2025, reflecting Australia's accelerating electrification of industrial operations and growing integration of renewable energy into thermal processing systems.

- By Automation Level: Fully automated systems account for the majority segment with 48.5% in 2025, supported by persistent labor shortages in manufacturing and mining that are accelerating adoption of smart, digitally controlled thermal processing equipment.

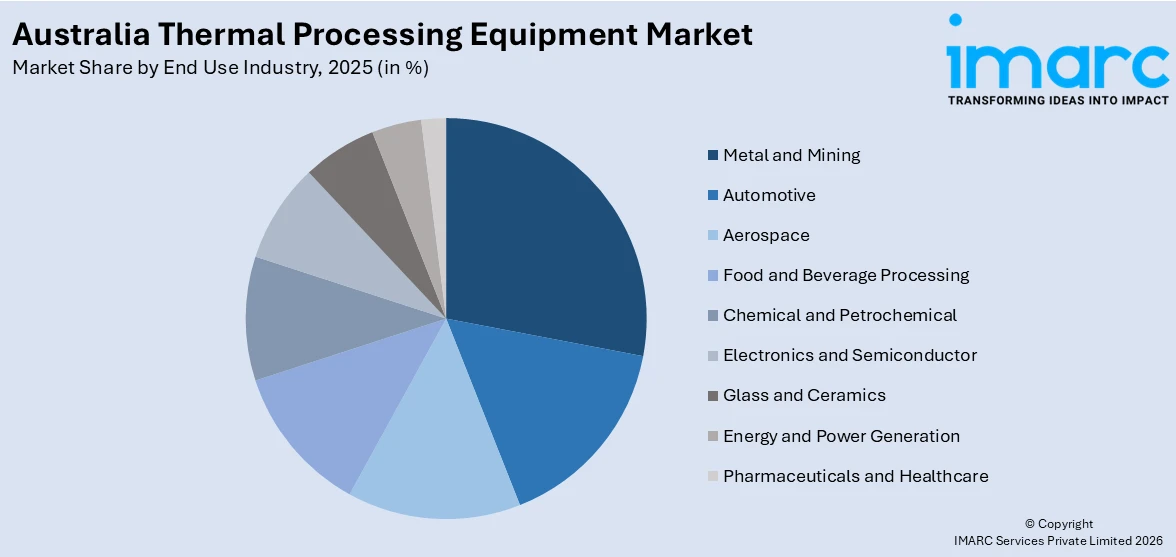

- By End Use Industry: Metal and mining represents the leading segment with 28.5% in 2025, driven by the robust expansion of Australia's mineral extraction and processing activities across iron ore, gold, copper, and critical minerals.

- By Region: Western Australia is the largest region with 35.5% share in 2025, underpinned by the state's dominant position in iron ore, gold, and critical minerals production requiring extensive thermal processing infrastructure.

- Key Players: In order to provide comprehensive thermal solutions, leading players in the Australian thermal processing equipment market are fortifying their positions through strategic alliances, automation capabilities expansion, and investments in energy-efficient furnace designs.

To get more information on this market Request Sample

As the country's industrial sector goes through a period of persistent transition driven by mining growth, manufacturing modernization, and renewable energy integration, the market for thermal processing equipment in Australia is growing significantly. Sophisticated furnaces, kilns, induction heating systems, and heat treatment equipment are still needed in the nation's resource-rich economy to support advanced component manufacture, metal refining, and mineral processing. Persistent skilled labor shortages in key industrial sectors are driving operators to invest in intelligent, digitally controlled equipment that lessens reliance on human interaction, accelerating the trend toward automated and energy-efficient thermal systems. Investment in cutting-edge thermal processing technology is being further stimulated by government programs aimed at enhancing local manufacturing capabilities and decarbonizing heavy industrial processes. Additionally, the spectrum of applications for thermal processing equipment is growing due to the increased demand for semiconductor-grade materials, green steel production, and important mineral processing. Australia is becoming a more significant market for next-generation thermal processing technologies and solutions due to the increased focus on downstream value addition and environmentally friendly production practices.

Australia Thermal Processing Equipment Market Trends:

Accelerating Transition Toward Electrified and Low-Emission Thermal Systems

As decarbonization requirements increase, Australia's industrial sector is moving more and more away from coal-based and gas-fired thermal systems and toward electric and hybrid alternatives. Electric furnaces and heat treatment systems powered by renewable energy sources are being integrated by manufacturers to lower operating emissions while preserving process efficiency. Electric thermal processing is becoming more practical and affordable for heavy industrial applications as clean electricity from solar, wind, and hydropower sources become more widely available. Cleaner thermal processing methods are being adopted nationwide by the mining, metals, food processing, and chemical manufacturing sectors thanks to government incentives, carbon reduction requirements, and changing sustainability standards.

Integration of Industry 4.0 and Smart Automation in Thermal Processing

Thermal processing processes throughout Australia are changing as a result of the use of digital twin technology, AI-driven process control, and Industrial Internet of Things sensors. Real-time monitoring, predictive maintenance, and optimized energy use in furnaces and kilns are made possible by smart automation. These cutting-edge features enable operators to reduce unscheduled downtime, maintain constant heat profiles across production cycles, and identify equipment anomalies before breakdowns occur. As processors look to increase throughput, lower defect rates, and improve energy efficiency in heat-intensive manufacturing environments, such as metals processing, ceramics production, and advanced component fabrication, this trend is bolstering the growth of the Australian thermal processing equipment market.

Rising Demand for Advanced Thermal Equipment in Critical Minerals Processing

The need for specialist thermal processing equipment, especially high-temperature furnaces, sintering systems, and calcination units necessary for the processing of rare earth and lithium, is being driven by Australia's critical minerals policy. Advanced thermal systems that can handle complicated mineral compositions and achieve accurate temperature profiles are becoming increasingly necessary due to the nation's growing pipeline of vital minerals projects. Precision thermal processing equipment is finding new uses as a result of investments in downstream value-adding operations like rare earth refining and battery material manufacture. This increased emphasis on domestic mineral beneficiation is supporting the country's ongoing acquisition of advanced thermal technology.

Market Outlook 2026-2034:

Australia's thermal processing equipment market is positioned for sustained expansion as industrial modernisation, mining sector growth, and clean energy transitions converge to drive equipment demand. The market generated a revenue of USD 37,153.07 Million in 2025 and is projected to reach a revenue of USD 63,533.13 Million by 2034, growing at a compound annual growth rate of 5.92% from 2026-2034. Continued investment in critical minerals processing, green steel initiatives, and energy-efficient manufacturing is expected to sustain procurement of advanced furnaces, kilns, and automated heat treatment systems. The nation's commitment to achieving net-zero emissions by 2050, coupled with the Future Made in Australia agenda, will encourage ongoing replacement of legacy thermal equipment with electrified and digitally controlled alternatives, further strengthening market revenue trajectories across the forecast period.

Australia Thermal Processing Equipment Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Equipment Type |

Furnaces |

32.5% |

|

Process Type |

Heat Treatment |

28.5% |

|

Heating Source |

Electric Thermal Processing |

42.5% |

|

Automation Level |

Fully Automated Systems |

48.5% |

|

End Use Industry |

Metal and Mining |

28.5% |

|

Region |

Western Australia |

35.5% |

Equipment Type Insights:

- Furnaces

- Ovens

- Kilns

- Induction Heating Systems

- Heat Treatment Systems

- Thermal Oxidizers

Furnaces dominate with a market share of 32.5% of the total Australia thermal processing equipment market in 2025.

Furnaces remain the most widely deployed category of thermal processing equipment in Australia, serving critical functions across metals smelting, mineral processing, and advanced manufacturing operations. The segment's dominance reflects the country's extensive mining sector, which requires high-temperature heating solutions for iron ore processing, gold refining, and copper smelting. Industrial furnaces are being progressively upgraded to incorporate electric heating elements and automated temperature control systems, improving energy efficiency and process consistency. The growing emphasis on sustainable production methods is encouraging operators to replace conventional combustion-based furnaces with electrified alternatives that align with national decarbonization objectives across heavy industry.

Growing demand for precision metallurgical processing and advanced material heat treatment is further reinforcing furnace procurement across the country. Manufacturers in the automotive, aerospace, and electronics sectors rely on vacuum furnaces, induction furnaces, and batch furnaces to achieve exacting thermal profiles required for high-performance components. The emergence of green steel production initiatives, utilizing electric arc furnaces and direct reduced iron technology, is creating a new category of demand. These transformative developments in low-emission ironmaking and steel recycling are driving significant interest in next-generation furnace technologies across Australia's industrial landscape.

Process Type Insights:

- Heat Treatment

- Annealing

- Hardening and Tempering

- Sintering

- Drying and Curing

- Calcination

Heat treatment leads with a share of 28.5% of the total Australia thermal processing equipment market in 2025.

Heat treatment processes constitute the largest process type segment in Australia's thermal processing equipment market, reflecting widespread industrial requirements for improving the mechanical properties, durability, and performance of metal components. The process is essential across mining equipment manufacturing, automotive part production, and aerospace component fabrication, where treated metals must withstand extreme operational stresses. Australia's expanding resource extraction activities, particularly in iron ore, gold, and copper, generate continuous demand for heat-treated drill bits, crusher components, and wear-resistant parts. Investment in WA's mining and petroleum industries totaled AUD 33 Billion in 2024-25, underscoring the scale of industrial activity driving heat treatment requirements.

Modern heat treatment operations in Australia increasingly employ computer-controlled atmosphere furnaces, vacuum systems, and induction heating equipment to achieve precise metallurgical outcomes. The automotive and aerospace industries demand tightly controlled thermal cycles for aluminum alloys, titanium components, and high-strength steels that require specific hardness, tensile strength, and fatigue resistance characteristics. Ongoing advancements in sensor-based monitoring and data analytics are enabling more efficient heat treatment cycles, reducing energy consumption and improving throughput. These technological improvements are encouraging manufacturers to upgrade legacy equipment and invest in next-generation heat treatment systems optimized for both performance and sustainability.

Heating Source Insights:

- Electric Thermal Processing

- Gas-Fired Systems

- Infrared and Microwave Heating

- Induction Heating

Electric thermal processing is the largest segment, accounting for 42.5% of the total Australia thermal processing equipment market in 2025.

Electric thermal processing equipment has established clear dominance in Australia's heating source landscape, driven by the nation's accelerating industrial electrification and expanding renewable energy integration. Electric furnaces, ovens, and induction systems offer precise temperature control, lower emissions, and compatibility with renewable power grids, making them increasingly preferred over gas-fired alternatives. Australia's renewable energy generation accounted for approximately 40% of total electricity output according to the 2024 Clean Energy Council study, providing a robust clean power foundation for electric thermal processing operations. This growing availability of affordable renewable electricity is encouraging industrial operators to transition toward electrically heated systems for both economic and environmental advantages.

The adoption of electric thermal processing is being further propelled by government decarbonization mandates and industry sustainability commitments across major end-use sectors. Mining companies, metals processors, and food manufacturers are investing in electric kilns, resistance furnaces, and induction heating systems to reduce Scope 1 emissions and comply with the Safeguard Mechanism requirements. The emergence of electro-thermal energy storage technologies, such as MGA Thermal's patented block system that converts renewable electricity into stored heat for industrial dispatch, is creating novel pathways for integrating electric thermal processing with variable renewable generation sources across the country.

Automation Level Insights:

- Manual Thermal Processing Equipment

- Semi-Automated Systems

- Fully Automated Systems

Fully automated systems hold the largest share at 48.5% of the total Australia thermal processing equipment market in 2025.

Fully automated thermal processing systems represent the leading automation level segment in Australia, reflecting the country's strong emphasis on smart manufacturing and operational efficiency. Persistent skilled labour shortages across manufacturing and mining sectors are compelling operators to adopt automated furnaces, kilns, and heat treatment lines equipped with programmable logic controllers, robotic handling systems, and real-time process monitoring. The growing difficulty of recruiting qualified technicians for high-temperature industrial environments is making automation not merely a preference but an operational necessity for maintaining consistent production schedules and output quality across thermally intensive industries throughout the country.

The integration of Industry 4.0 technologies into thermal processing equipment is expanding rapidly, with digital twins, artificial intelligence-driven process optimization, and predictive maintenance capabilities becoming standard features in new installations. Fully automated systems minimize human exposure to high-temperature environments, reduce process variability, and enable continuous operation with minimal intervention. The broader momentum toward smart manufacturing across Australia's industrial base is reinforcing demand for fully integrated, digitally controlled thermal processing solutions across sectors ranging from metals processing and food manufacturing to pharmaceuticals and electronics fabrication nationwide.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Aerospace

- Metal and Mining

- Food and Beverage Processing

- Chemical and Petrochemical

- Electronics and Semiconductor

- Glass and Ceramics

- Energy and Power Generation

- Pharmaceuticals and Healthcare

Metal and mining represents the leading segment with a 28.5% share of the total Australia thermal processing equipment market in 2025.

The metal and mining sector accounts for the largest end-use share in Australia's thermal processing equipment market, driven by the country's position as a globally significant producer of iron ore, gold, copper, lithium, and rare earth minerals. Thermal processing equipment, including smelting furnaces, calcination kilns, and sintering systems, is fundamental to mineral beneficiation and metals refining operations across the country. The sheer scale of Australia's resource extraction activities, spanning established commodities and emerging critical minerals, creates a sustained and diversified base of demand for high-capacity thermal processing infrastructure across both brownfield upgrades and greenfield project developments.

The expansion of critical minerals processing and green metals production is creating new layers of demand for specialized thermal equipment in Australia's mining sector. Companies are investing in advanced furnace and kiln technologies to support downstream processing of lithium, rare earths, and battery materials, moving beyond traditional bulk commodity extraction. The increasing focus on domestic processing capabilities, supported by national strategies encouraging value-adding mineral beneficiation, is fostering a favorable environment for sustained procurement of sophisticated thermal processing equipment. Strategic partnerships between miners and technology providers are further strengthening the pipeline of thermal equipment investment opportunities.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Western Australia exhibits a clear dominance with a 35.5% share of the total Australia thermal processing equipment market in 2025.

Western Australia is the undisputed leader in Australia's thermal processing equipment market, commanding the largest regional share due to its concentration of iron ore, gold, lithium, and rare earth mining and processing operations. The state's resources sector consistently attracts the largest portion of national mining investment, sustaining demand for high-capacity furnaces, smelting equipment, and heat treatment systems essential for mineral beneficiation and metals refining. Western Australia's dominant position in both traditional commodity production and emerging critical minerals development creates an exceptionally broad and diversified base of thermal processing requirements that extends across exploration, extraction, processing, and refining stages.

The emergence of green steel and low-emission metals processing initiatives is further strengthening Western Australia's thermal processing equipment market. Major collaborative projects involving leading mining companies and steelmakers are advancing electric smelting furnace and direct reduced iron technologies within the state, underscoring the region's leadership in next-generation thermal processing innovation. Additionally, green steel recycling facilities utilizing electric arc furnace technology are progressing through approval and construction phases, reinforcing the state's commitment to advanced thermal processing infrastructure. These transformative developments are positioning Western Australia as a focal point for innovative thermal equipment deployment and long-term industrial investment.

Market Dynamics:

Growth Drivers:

Why is the Australia Thermal Processing Equipment Market Growing?

Expanding Mining and Mineral Processing Activities

Australia's mining sector continues to be a primary growth engine for thermal processing equipment demand, with the country maintaining its position as the world's largest iron ore producer and a leading supplier of gold, copper, lithium, and rare earth minerals. The resource extraction and processing cycle requires extensive thermal infrastructure, including blast furnaces, smelting systems, calcination kilns, and heat treatment equipment for both upstream mineral processing and downstream metals refining. The robust investment pipeline across Australia's mining industry is sustaining equipment procurement cycles and encouraging upgrades to higher-capacity, more efficient thermal systems. The diversification of mining activities toward critical minerals and battery materials is creating incremental demand for specialized thermal processing equipment suited to complex mineral compositions. The steady expansion in project development across both established commodities and emerging mineral categories is directly translating into increased procurement of furnaces, kilns, and automated heat treatment systems required for new processing facilities across the country.

Government-Led Industrial Decarbonization and Electrification Programs

Federal and state government initiatives aimed at reducing industrial emissions are catalyzing significant investment in advanced, energy-efficient thermal processing equipment across Australia. Policy frameworks encouraging domestic manufacturing capabilities and clean energy integration are driving heavy industries to adopt electrified manufacturing technologies, including electric furnaces, induction heating systems, and thermal energy storage solutions. These measures are accelerating the replacement of legacy gas-fired and coal-based thermal equipment with cleaner alternatives, driving a new cycle of capital expenditure in the thermal processing equipment market. Complementary regional funding programs are providing targeted financial support for emissions reduction at heavy industrial facilities, including kiln upgrades, furnace electrification, and alternative fuel integration projects. These investments demonstrate the direct linkage between decarbonization policy and thermal processing equipment demand, as industries upgrade their heating infrastructure to meet evolving regulatory requirements and national sustainability objectives.

Persistent Labor Shortages Accelerating Automation Adoption

Chronic skilled labor shortages across Australia's manufacturing and mining sectors are compelling industrial operators to invest heavily in automated thermal processing equipment. The country's manufacturing sector faces a significant and growing workforce gap, creating an imperative for robotic handling, computer-controlled furnaces, and fully automated heat treatment lines that can operate with minimal human intervention. This workforce constraint is particularly acute in remote mining regions where thermal processing facilities operate continuously, making automated systems essential for maintaining production schedules and operational reliability. The convergence of labor market pressures with advancing automation technologies is producing a structural shift toward higher-specification thermal processing equipment. Industrial operators are increasingly specifying fully automated furnaces, smart kilns with integrated sensor networks, and artificial intelligence-driven process optimization platforms when replacing or expanding thermal processing capacity, reinforcing sustained demand for advanced, digitally controlled thermal processing solutions across all major end-use sectors.

Market Restraints:

What Challenges the Australia Thermal Processing Equipment Market is Facing?

High Capital Investment Requirements for Advanced Equipment

The acquisition and installation of modern thermal processing equipment, particularly fully automated electric furnaces and smart kiln systems, requires substantial upfront capital expenditure that can deter investment, especially among small and medium-sized enterprises. Advanced vacuum furnaces, induction heating systems, and automated heat treatment lines carry significantly higher purchase prices compared to conventional alternatives. Additionally, the costs of facility modifications, electrical infrastructure upgrades, and integration with existing production systems further increase total deployment expenses, creating financial barriers that slow the pace of equipment modernization across segments of Australia's industrial base.

Supply Chain Vulnerabilities and Long Lead Times

Australia's geographic isolation and dependence on imported thermal processing equipment components expose the market to supply chain disruptions and extended delivery timelines. Many specialized furnace components, advanced refractories, and precision control systems are manufactured overseas, making procurement susceptible to shipping delays, trade policy changes, and global manufacturing bottlenecks. These logistical challenges can delay project commissioning schedules and increase costs for industrial operators, particularly in remote mining regions where timely equipment availability is critical for maintaining production continuity and meeting contractual obligations.

Stringent Environmental and Regulatory Compliance Burden

Increasingly rigorous environmental regulations and emissions reporting requirements are adding complexity and cost to thermal processing equipment operations in Australia. Industrial operators must navigate overlapping federal and state regulatory frameworks, including the Safeguard Mechanism and climate-related financial disclosure mandates. Compliance with evolving emissions standards may require costly equipment retrofits, additional monitoring infrastructure, and process modifications that increase operational overhead. For smaller operators with limited resources, meeting these regulatory demands while maintaining competitive production economics presents a persistent challenge that can constrain equipment investment decisions.

Competitive Landscape:

The Australia thermal processing equipment market features a competitive landscape characterized by the presence of both established global manufacturers and specialized regional suppliers. Competition is driven by technological innovation, energy efficiency performance, and the ability to deliver customized solutions tailored to specific industrial applications. Market participants are investing in research and development to advance electric furnace designs, improve automation integration, and enhance thermal efficiency across their product portfolios. Strategic collaborations between equipment manufacturers, mining companies, and technology providers are intensifying as industries seek integrated thermal processing solutions. After-sales service capabilities, spare parts availability, and technical support networks also play critical roles in competitive positioning across Australia's geographically dispersed industrial base.

Australia Thermal Processing Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered | Furnaces, Ovens, Kilns, Induction Heating Systems, Heat Treatment Systems, Thermal Oxidizers |

| Process Types Covered | Heat Treatment, Annealing, Hardening and Tempering, Sintering, Drying and Curing, Calcination |

| Heating Sources Covered | Electric Thermal Processing, Gas-Fired Systems, Infrared and Microwave Heating, Induction Heating |

| Automation Levels Covered | Manual Thermal Processing Equipment, Semi-Automated Systems, Fully Automated Systems |

| End Use Industries Covered | Automotive, Aerospace, Metal and Mining, Food and Beverage Processing, Chemical and Petrochemical, Electronics and Semiconductor, Glass and Ceramics, Energy and Power Generation, Pharmaceuticals and Healthcare |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Thermal Processing Equipment Market Report

The Australia thermal processing equipment market size was valued at USD 37,153.07 Million in 2025.

The Australia thermal processing equipment market is expected to grow at a compound annual growth rate of 5.92% from 2026-2034 to reach USD 63,533.13 Million by 2034.

Furnaces dominated the market with a share of 32.5%, driven by their essential role in metals smelting, mineral processing, and advanced manufacturing operations across Australia's resource-intensive industrial sectors.

Key factors driving the Australia thermal processing equipment market include expanding mining and mineral processing activities, government-led industrial decarbonization programs, persistent labor shortages accelerating automation adoption, and growing critical minerals processing investment.

Major challenges include high capital investment requirements for advanced equipment, supply chain vulnerabilities and long lead times for imported components, stringent environmental compliance requirements, and the complexity of integrating new thermal systems with legacy industrial infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)