Australia Toys Market Size, Share, Trends and Forecast by Product Type, Age Group, Sales Channel, and Region, 2026-2034

Australia Toys Market Size, Share, Trends & Forecast (2026-2034)

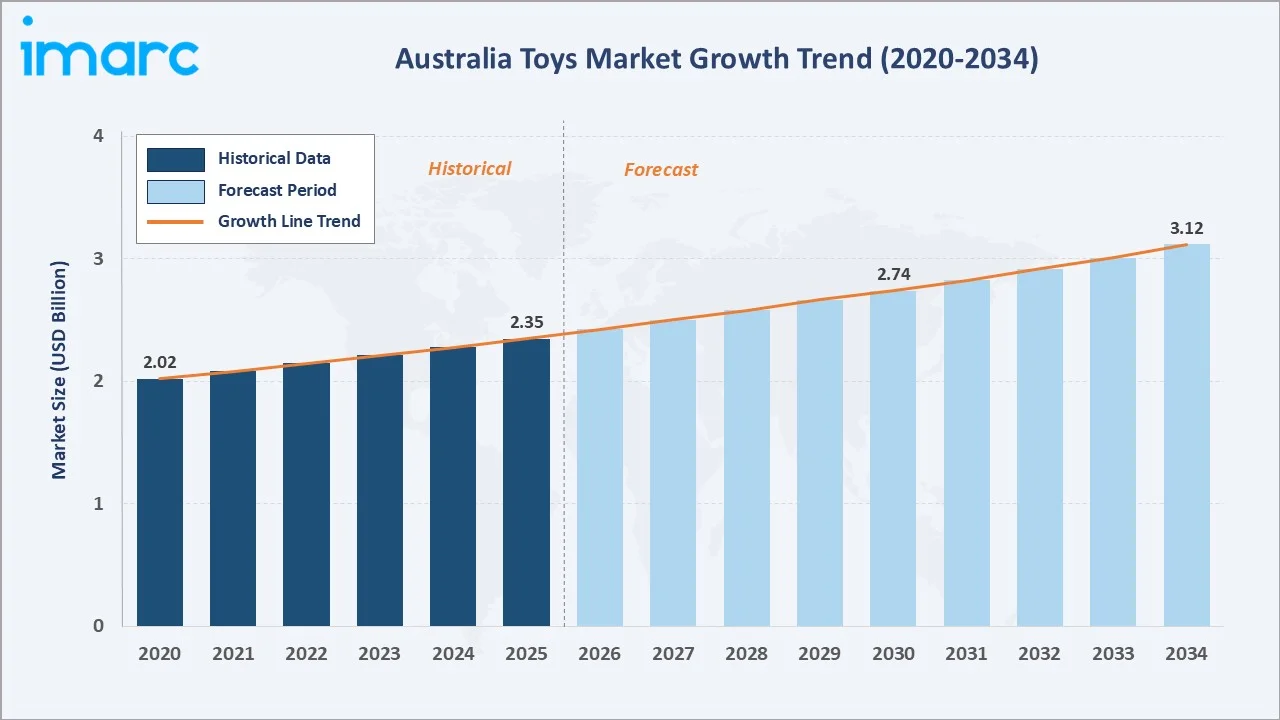

The Australia toys market size reached USD 2.35 Billion in 2025 and is projected to reach USD 3.12 Billion by 2034, exhibiting a CAGR of 3.10% during 2026-2034. Rising demand for STEM-based educational toys, surging popularity of licensed Australian franchises, and expanding e-commerce infrastructure are the primary forces driving market growth.

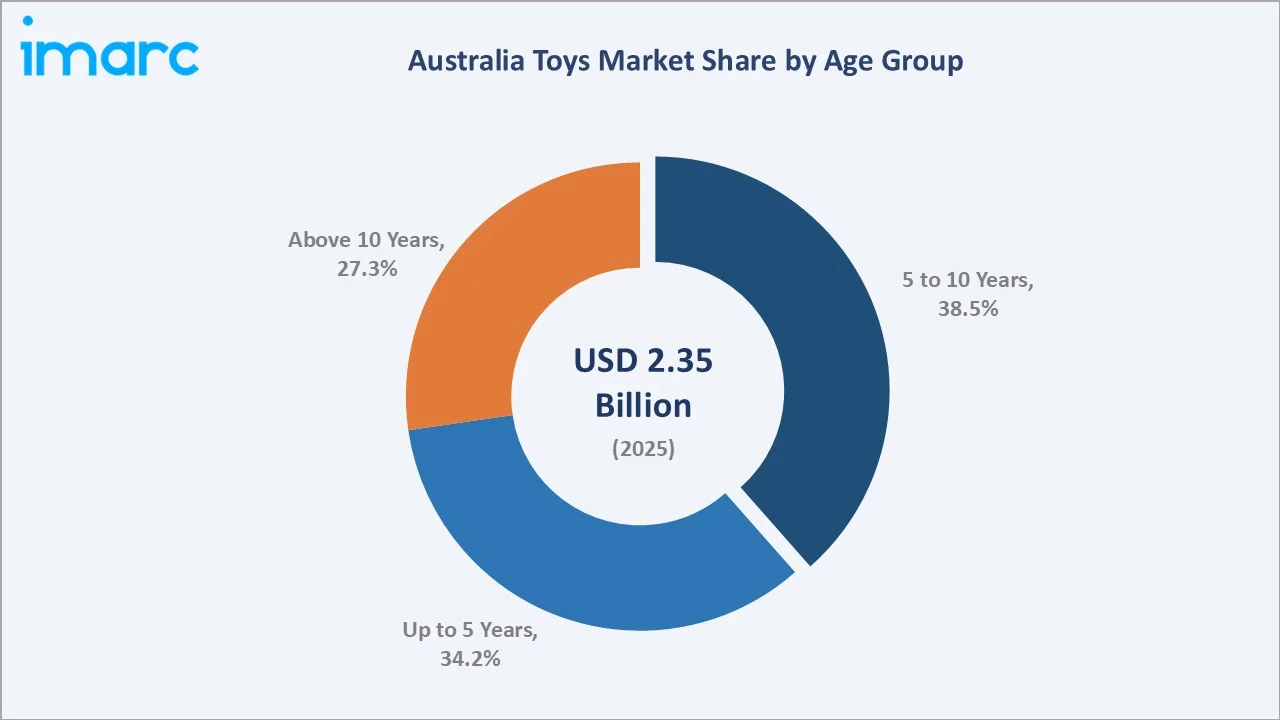

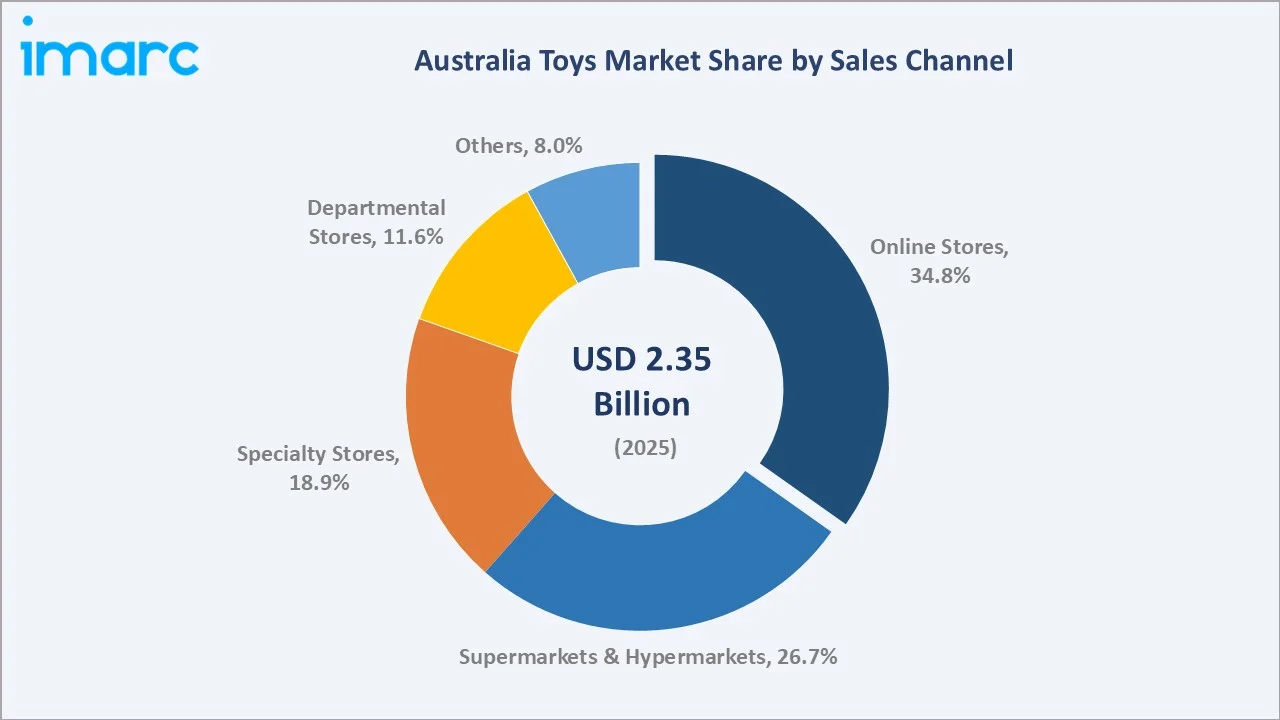

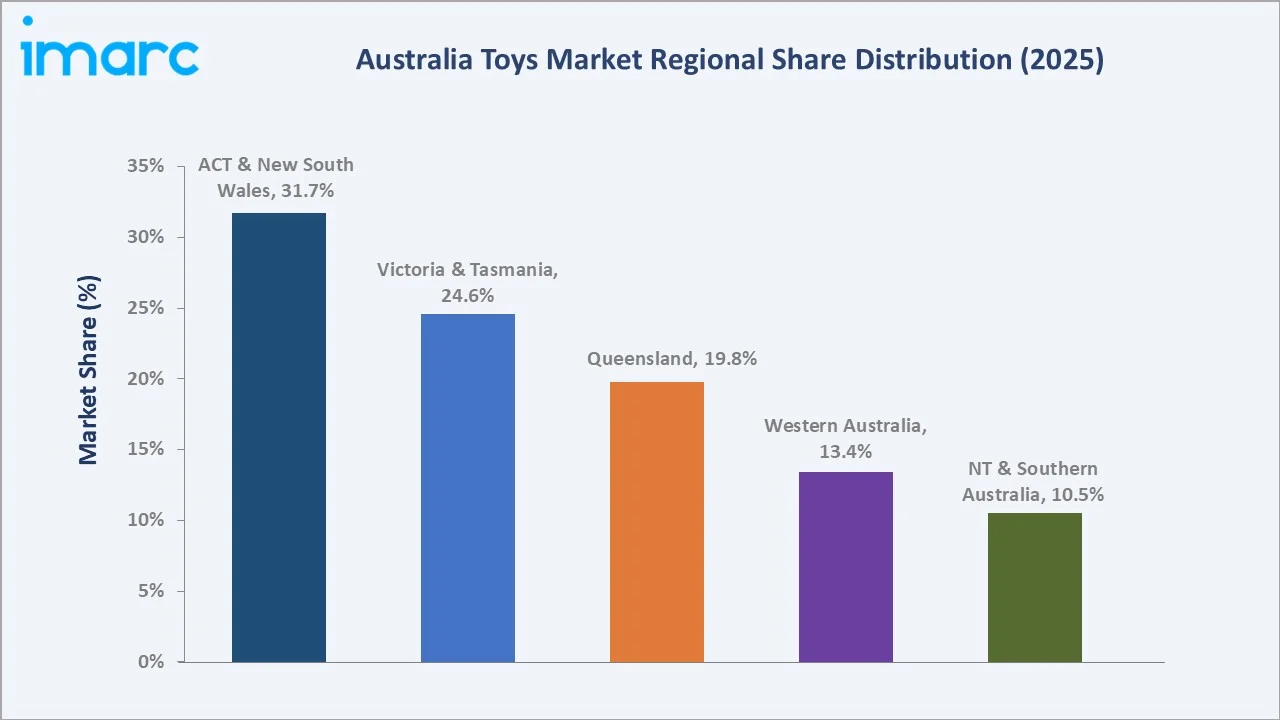

The 5 to 10 Years age group dominates the market at 38.5% in 2025, while online stores lead the sales channel mix at 34.8%. The Australia Capital Territory & New South Wales region commands a dominant 31.7% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.35 Billion |

|

Forecast Market Size (2034) |

USD 3.12 Billion |

|

CAGR (2026-2034) |

3.10% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Age Group |

5 to 10 Years (38.5% share, 2025) |

|

Second Age Group |

Up to 5 Years (34.2% share, 2025) |

|

Leading Sales Channel |

Online Stores (34.8%, 2025) |

|

Leading Region |

ACT & New South Wales (31.7%, 2025) |

The Australia toys market growth trajectory from 2020 through 2034, with historical expansion to USD 2.35 Billion in 2025, reflects consistent consumer demand, while the forecast to USD 3.12 Billion captures accelerating digital integration, STEM adoption, and omnichannel retail maturation across the country.

To get more information on this market, Request Sample

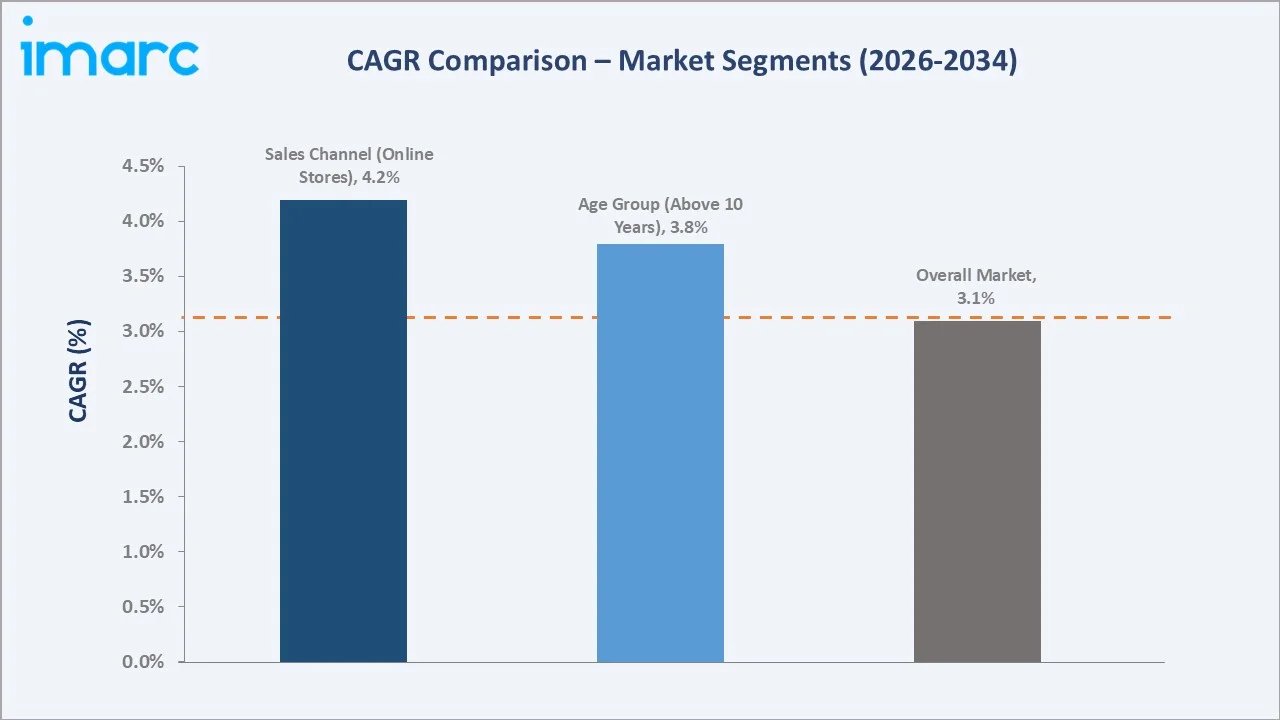

The CAGR trajectories across key age group, sales channel, and regional sub-segments, with online stores at ~4.2% CAGR and the Above 10 Years segment at ~3.8% CAGR, are the fastest-growing categories within the Australia toys market through 2034.

Executive Summary

The Australia toys market is on a sustained growth trajectory from USD 2.35 Billion in 2025 to USD 3.12 Billion by 2034. Toys, essential developmental and entertainment products spanning action figures, dolls, puzzles, board games, building blocks, and electronic devices, benefit from non-discretionary demand tied to child development priorities and parental investment in quality learning experiences.

The 5 to 10 Years age group dominates with a 38.5% share in 2025, owing to its broad product compatibility spanning educational, creative, and physical play categories. The Up to 5 Years segment (34.2%) commands strong demand driven by developmental toy spending among millennial parents. The Above 10 Years segment (27.3%) is the fastest-growing, fuelled by collectibles culture, STEM robotics kits, and digital-integrated toys targeting tweens and teens.

Online stores lead the sales channel mix at 34.8% in 2025, reflecting Australia's mature e-commerce infrastructure and the post-pandemic structural shift in toy purchasing behaviour.

The Australia Capital Territory & New South Wales region dominates at 31.7% in 2025, reflecting Australia's highest concentration of family households and retail infrastructure. Victoria & Tasmania follow at 24.6%, driven by Melbourne's status as a major retail hub and a growing child population.

Key Market Insights

|

Insight |

Data |

|

Leading Age Group |

5 to 10 Years – 38.5% share (2025) |

|

Second Age Group |

Up to 5 Years – 34.2% share (2025) |

|

Leading Sales Channel |

Online Stores – 34.8% share (2025) |

|

Second Sales Channel |

Supermarkets & Hypermarkets – 26.7% share (2025) |

|

Leading Region |

ACT & New South Wales – 31.7% share (2025) |

|

Second Largest Region |

Victoria & Tasmania – 24.6% share (2025) |

|

Top Companies |

Hasbro, Jazwares, LLC, Mattel, The LEGO Group, ZURU |

Key Analytical Observations Expanding on the Above Data:

- 5 to 10 Years Age Group: The 5 to 10 Years group dominates at 38.5% in 2025 because this age bracket represents the broadest product spectrum. Children in this range are developmentally suited to construction sets, board games, action figures, and STEM kits, creating multi-category buying patterns that sustain both volume and value uplift per transaction.

- Online Stores Channel: Online stores, with 34.8% in 2025, lead because Australian consumers have embraced digital retail for toy purchases across all demographics. Convenience, price comparison tools, broad SKU availability, and same-day delivery capabilities from major platforms drive this structural channel shift that continues to gain share.

- ACT & New South Wales Region: ACT & New South Wales dominance at 31.7% in 2025 reflects Sydney's role as Australia's most populous city with the highest household incomes, greatest retail density, and largest concentration of specialty toy retailers and department store toy sections in the country.

Australia Toys Market Overview

Toys are objects created for the purpose of play, amusement, and education, primarily designed for children but increasingly consumed by adults through collectible and nostalgia-driven categories. Product configurations are defined by age suitability, developmental purpose, material composition, and technology integration level, spanning traditional physical toys, digital-integrated smart toys, and educational STEM product lines.

The Australian toys ecosystem integrates global toy manufacturers, licensed IP owners, domestic distributors and importers, omnichannel retailers spanning specialty stores to hypermarkets, safety regulatory bodies including the Australian Competition and Consumer Commission (ACCC), and end-user consumers from newborn to adult.

Market Dynamics

To evaluate market opportunities, Request Sample

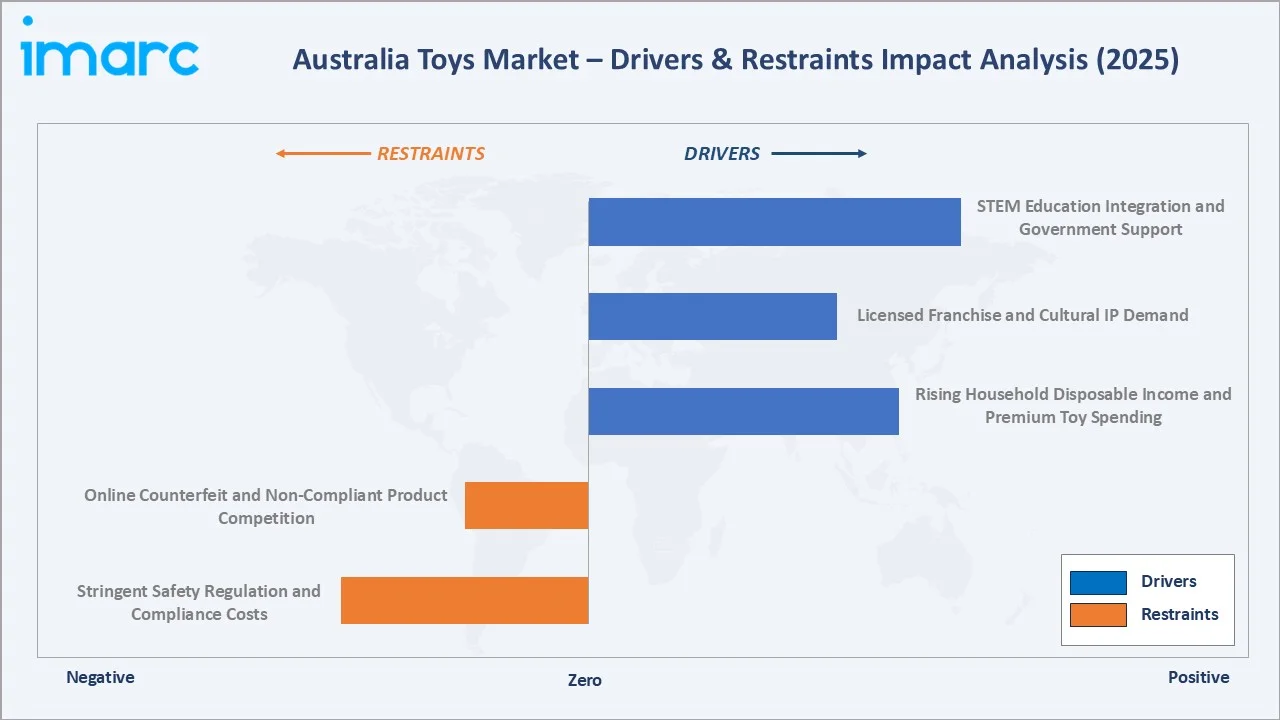

Market Drivers

- STEM Education Integration and Government Support: Australian schools and parents increasingly recognise the role of STEM-focused toys in preparing children for technology-driven careers. Federal and state government funding for STEM programs has amplified demand for coding kits, robotics sets, and science experiment toys, establishing educational toys as a key growth pillar sustaining above-market category expansion.

- Licensed Franchise and Cultural IP Demand: Australian-born franchises such as Bluey have achieved global recognition, generating substantial licensed toy sales across action figures, playsets, and plush categories. Strong IP licensing ecosystems around domestic and international content franchises sustain consistent demand cycles that are tightly aligned with new content releases across streaming and broadcast channels.

- Rising Household Disposable Income and Premium Toy Spending: Australia's rising household disposable income has supported increased per-unit spending on toys, with parents investing in higher-quality, more durable, and educationally validated products. Disposable income in Australia reported AUD 737,596 million in December 2025, representing a 1.4% increase over the preceding quarter, reinforcing consumer capacity for premium toy expenditure.

Market Restraints

- Stringent Safety Regulation and Compliance Costs: The ACCC enforces comprehensive product safety standards for toys sold in Australia, with penalties for non-compliance including button battery testing failures. Revised infant toy standards mandate additional choking-hazard assessments, increasing compliance with timelines and costs that disproportionately impact smaller importers and emerging brands.

- Online Counterfeit and Non-Compliant Product Competition: The growth of cross-border e-commerce has enabled proliferation of counterfeit and non-ACCC-compliant toys through online marketplaces, creating unfair pricing competition for compliant domestic and established international suppliers while simultaneously exposing consumers to safety risks.

Market Opportunities

- Eco-Friendly and Sustainable Toy Manufacturing: Rising consumer preference for environmentally responsible products is creating significant opportunity for toys manufactured using certified sustainable materials and minimal plastic packaging. Growing parental awareness of environmental impact is translating into measurable brand loyalty premiums for manufacturers that credibly communicate sustainability credentials.

- Adult Collectibles and Gaming Market Expansion: The growing collectibles culture among Gen Z and Millennials, driven by blind box formats, limited releases, and nostalgia-driven franchise revivals, is expanding the addressable market beyond children. Social media platforms accelerate awareness and demand cycles for collectible toy lines, creating recurring purchase behaviour.

Market Challenges

- Supply Chain Disruptions and Import Cost Pressures: Australia's high dependence on imported toys predominantly manufactured in China and Southeast Asia exposes the market to global supply chain disruptions, freight cost volatility, and currency exchange fluctuations that compress distributor and retailer margins while creating unpredictable inventory availability.

- Rapid Technology Shifts and Product Obsolescence: The accelerating pace of digital platform evolution and children's media consumption patterns creates risk of rapid product obsolescence for technology-integrated toys. Toys dependent on specific app ecosystems or hardware compatibility face shortened commercial lifecycles as underlying platforms evolve and consumer attention shifts.

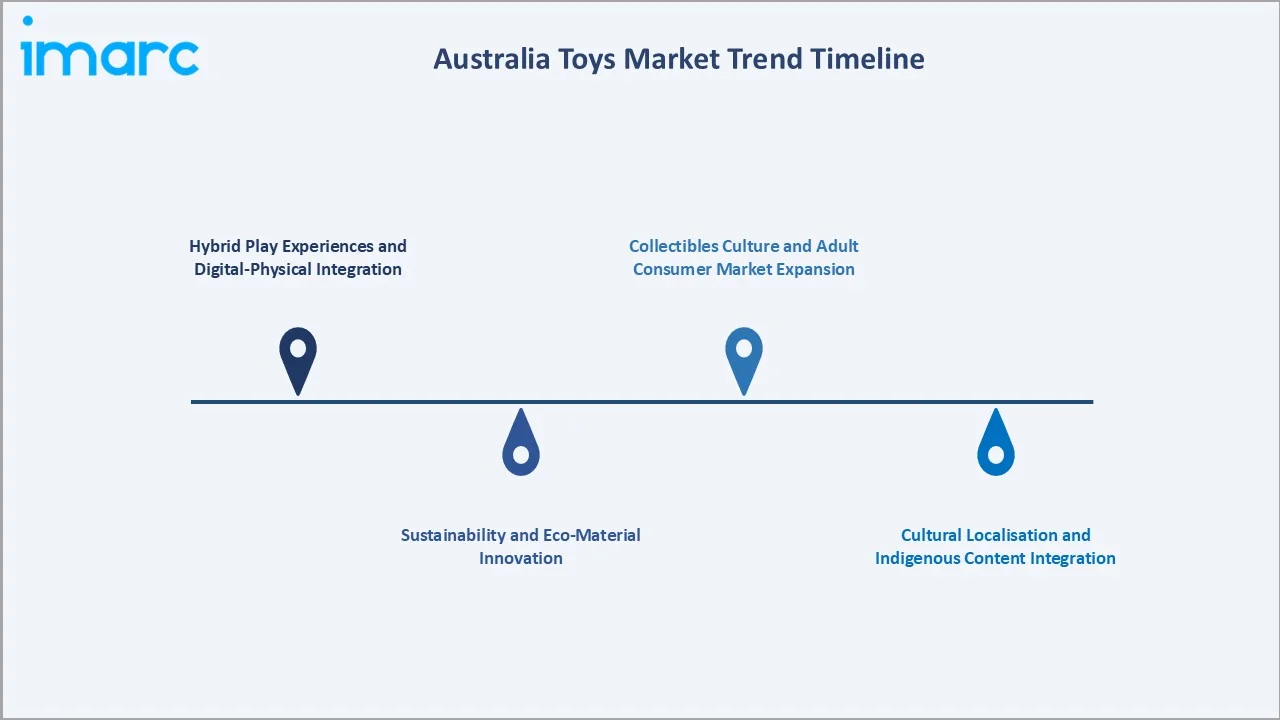

Emerging Market Trends

1. Hybrid Play Experiences and Digital-Physical Integration

The convergence of physical toys with digital experiences is reshaping Australia's toy landscape. Augmented reality components, app-based learning modules, and QR-code-enabled interactive content are being integrated into traditional toy formats. STEM toys incorporating coding interfaces and app-connected robotics are gaining mainstream adoption, driven by parental demand for screen time that delivers genuine developmental value alongside entertainment.

2. Sustainability and Eco-Material Innovation

Environmental consciousness among Australian consumers, particularly millennial and Gen Z parents, is driving rapid adoption of sustainable toy materials including FSC-certified wood, biodegradable polymers, and organic textiles. The Australian Packaging Covenant Organisation's introduction of eco-modulation fees from FY27 is accelerating manufacturer transition to recyclable packaging across all toy categories sold in Australia.

3. Cultural Localisation and Indigenous Content Integration

Australian consumers demonstrate strong preference for toys with local cultural resonance, spanning licensed products based on domestic franchises to board games featuring Australian wildlife, landmarks, and Aboriginal art themes. Government support for Indigenous-owned businesses is increasing representation of Aboriginal stories in children's games and activity sets, creating a distinct and growing product sub-category.

4. Collectibles Culture and Adult Consumer Market Expansion

Social-media-amplified collectibles culture, particularly blind box formats and limited-release licensed collaborations, is expanding the toys market's consumer base beyond children. Domestic and international toy companies are leading this segment in Australia with innovative collectible ranges that generate social media engagement, unboxing content creation, and sustained repeat purchase demand from teenage and adult consumers.

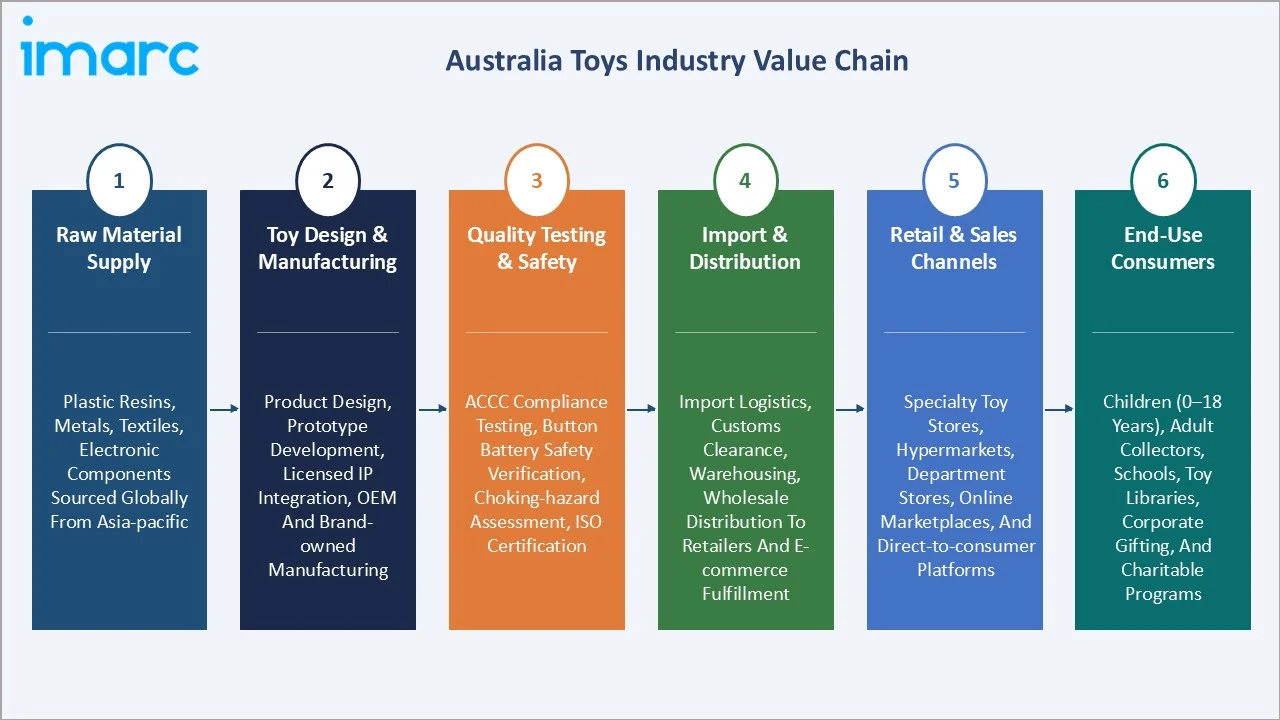

Industry Value Chain Analysis

The Australia toys value chain spans six stages from raw material inputs through end-user consumption. Design and IP development capture the highest value-add margins, while distribution logistics and safety compliance certification generate significant working capital requirements favouring well-capitalised manufacturers and distributors operating within the Australian regulatory framework.

|

Stage |

Key Activities & Examples |

|

Raw Material Supply |

Plastic resins, metals, textiles, electronic components sourced globally from Asia-Pacific suppliers |

|

Toy Design & Manufacturing |

Product design, prototype development, licensed IP integration, OEM and brand-owned manufacturing |

|

Quality Testing & Safety |

ACCC standard compliance testing, button battery safety verification, choking-hazard assessment, ISO certification |

|

Import & Distribution |

Import logistics, customs clearance, warehousing, wholesale distribution to retailers and e-commerce fulfillment |

|

Retail & Sales Channels |

Specialty toy stores, hypermarkets, department stores, online marketplaces, and direct-to-consumer platforms |

|

End-Use Consumers |

Children (0–18 years), adult collectors, schools, toy libraries, corporate gifting, and charitable programs |

Integrated toy companies with proprietary IP ownership, in-house design studios, and direct-to-consumer e-commerce capabilities achieve superior margin structures compared to pure-play distributors dependent on third-party brand licences and wholesale pricing. IP ownership and omnichannel distribution capability represent the primary competitive advantages in the Australian toys market.

Technology Landscape in the Australia Toys Industry

Digital Integration: Augmented Reality and App-Connected Play

The integration of augmented reality and mobile application connectivity into physical toy products is redefining play experiences in Australia. AR toys that overlay digital content onto physical play spaces, and app-connected robotic kits that teach coding through interactive challenges, are becoming mainstream product categories supported by Australia's high smartphone penetration rate exceeding 90% across family demographics.

STEM Robotics and Coding Toy Technology

Educational robotics platforms incorporating programmable microcontrollers, sensor arrays, and block-based or Python coding interfaces are experiencing accelerated adoption across Australian primary and secondary school markets. These products align directly with the Australian Curriculum's Digital Technologies learning area, providing institutional procurement momentum that supplements home consumer demand.

Smart Toy AI Personalisation

AI-powered toys capable of personalising content, difficulty levels, and narrative pathways to individual children's developmental stages are emerging as a premium segment. The global smart AI toys market is projected to reach USD 7,502 Million by 2033, and Australian consumers' demonstrated appetite for premium educational products positions this segment for above-market growth in the local context.

Sustainable Material Technology

Bioplastics derived from renewable feedstocks and FSC-certified wooden toy production using precision CNC machining are being adopted by progressive toy manufacturers to address sustainability demands. These material innovations deliver safety standards equivalent to conventional plastic products while meeting certification requirements increasingly demanded by eco-conscious Australian consumers and forthcoming regulatory changes.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Age Group |

5 to 10 Years |

38.5% |

2025 |

|

Sales Channel |

Online Stores |

34.8% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

31.7% |

2025 |

By Age Group

The 5 to 10 Years age group commands a 38.5% majority share in 2025 owing to its developmental breadth and purchasing power concentration. This segment's broad product compatibility across action figures, construction sets, educational toys, board games, and outdoor play categories drives multi-category demand and the highest average transaction values across the age spectrum.

To access detailed market analysis, Request Sample

The Up to 5 Years segment at 34.2% in 2025 is driven by strong parental investment in developmental toys for infants and preschoolers, including STEM-aligned early learning products, sensory toys, and safety-certified plush ranges.

By Sales Channel

Online stores dominate the sales channel mix at 34.8% in 2025, reflecting Australia's highly developed e-commerce infrastructure, competitive online pricing, and broad SKU availability on major platforms.

Supermarkets and hypermarkets at 26.7% in 2025 maintain strong positioning through convenience-driven purchasing and gifting impulse buys. Specialty stores at 18.9% command premium brand depth, particularly for construction, educational, and boutique toy ranges.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

ACT & New South Wales |

31.7% |

Highest household incomes; greatest retail density; largest child population base |

|

Victoria & Tasmania |

24.6% |

Strong specialty retail culture; multicultural consumer diversity; educational toy demand |

|

Queensland |

19.8% |

Rapid population growth; interstate migration; growing suburban family household base |

|

Western Australia |

13.4% |

Resource-sector household income supporting premium toy spending; retail market maturation |

|

NT & Southern Australia |

10.5% |

Emerging retail infrastructure; Indigenous content toy growth; growing urban family segment |

The Australia Capital Territory & New South Wales region commands a 31.7% share of the Australian toys market in 2025, driven by Sydney's retail density, Australia's highest average household income levels, and the largest concentration of specialty toy retailers and department store toy sections nationally. The federal government workforce in ACT contributes to above-average household purchasing power that supports premium toy category expenditure.

Victoria & Tasmania, with 24.6% in 2025, benefits from Melbourne's established retail culture, diverse multicultural consumer base driving broad product category demand, and strong specialty retailer presence.

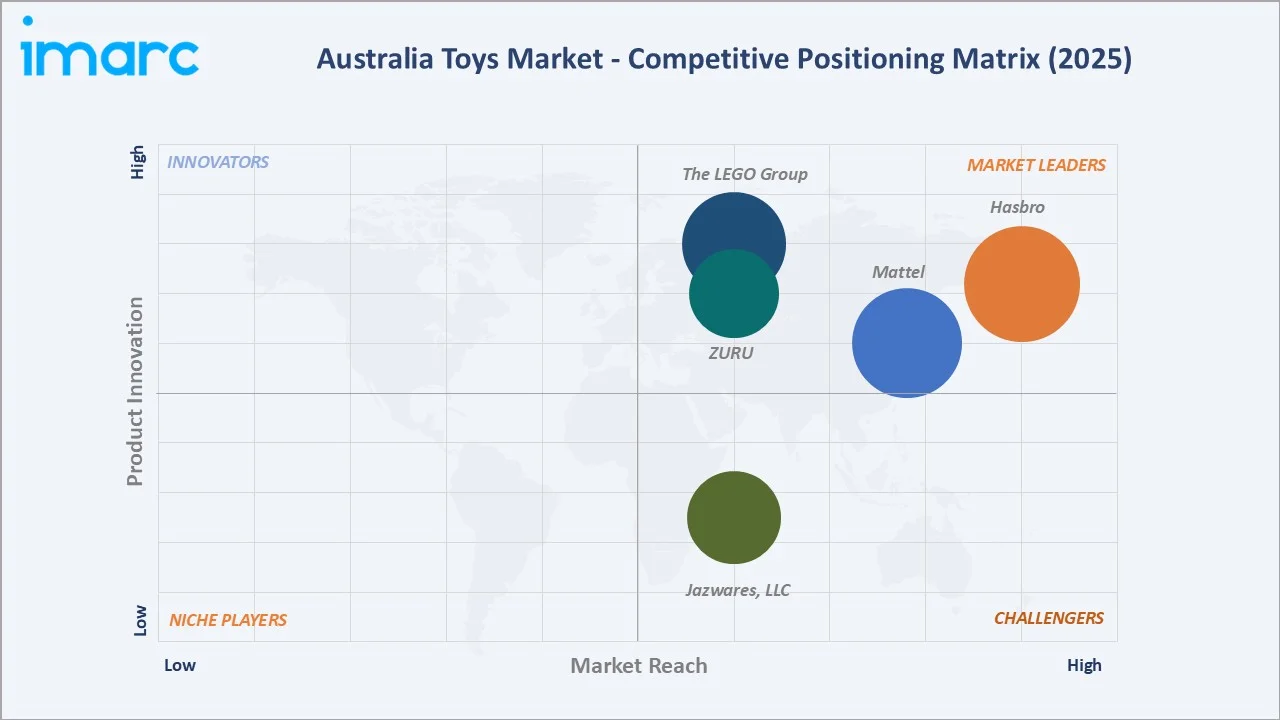

Competitive Landscape

The Australia toys market is moderately concentrated, with a mix of global multinational toy manufacturers operating through Australian subsidiaries or distributors, an influential domestic manufacturer, and specialist local brands competing in niche categories.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Hasbro |

Monopoly, Play-Doh, Transformers, My Little Pony |

Leader |

Multi-category franchise management; digital-physical play integration |

|

Jazwares, LLC |

Pokémon, Fortnite, BumBumz, Squishmallows |

Challenger |

Digital gaming-linked merchandise; youth collectibles category |

|

Mattel |

Barbie, Hot Wheels, Fisher-Price |

Leader |

Brand rejuvenation via media tie-ins; sustainable product development |

|

The LEGO Group |

LEGO Classic, LEGO Technic, LEGO licensed sets |

Leader |

Premium construction; educational positioning; sustainability leadership |

|

ZURU |

Bunch O Balloons, Mini Brands, X-Shot, SMASHERS |

Leader |

Innovation-driven collectibles; value segment penetration globally |

Key players include Hasbro, Jazwares, LLC, Mattel, The LEGO Group, ZURU, and others.

Key Company Profiles

The LEGO Group

The LEGO Group is the world's largest toy manufacturer by revenue, headquartered in Billund, Denmark. In Australia, LEGO commands the premium construction toy segment with an unmatched brand trust profile among parents and children. Its extensive retail presence spans specialty LEGO stores, major department stores, hypermarkets, and e-commerce channels across all major Australian metropolitan markets.

- Product Portfolio: LEGO Classic, LEGO Technic, LEGO licensed sets, and others.

- Recent Developments: In October 2024, The LEGO Group strengthened its logistics capabilities in Australia with the launch of a new distribution centre in Truganina, Victoria, operated in partnership with Kuehne+Nagel.

- Strategic Focus: LEGO's Australia strategy leverages its sustainability credentials, premium licensed partnerships, and LEGO Education institutional channel expansion to align with school curriculum requirements for digital technologies and coding, securing both household and institutional revenue streams.

Mattel

Mattel is one of the world's largest toy companies, with a diversified portfolio spanning infant and preschool, dolls, vehicles, games, and licensed products distributed across Australian retail channels. The company's media-to-merchandise pipeline, demonstrated through the Barbie franchise's global film success, is a key strategic asset for market share growth.

- Product Portfolio: Barbie, Hot Wheels, Fisher-Price, and others

- Recent Developments: In July 2023, Mattel Australia announced a strategic partnership with Retail Prodigy Group (RPG) to strengthen its direct-to-consumer presence in Australia through a new online retail platform. The collaboration is aimed at delivering a broader and more immersive shopping experience for fans of Mattel’s iconic brands, including Barbie, Hot Wheels, Fisher-Price, and Thomas & Friends.

- Strategic Focus: Mattel's strategy focuses on media-to-merchandise pipeline leverage, sustainable product material transition, and digital play integration across its core brand portfolio to address Australian consumers' demand for innovative, responsibly manufactured toys with strong entertainment IP anchoring.

Hasbro

Hasbro is one of the world's largest toy and entertainment companies, with an extensive brand portfolio distributed in Australia through its local operations. The company's multi-category presence spans action figures, games, arts and crafts, and outdoor toys across all major Australian retail channels, supported by strong franchise management capabilities built over decades of brand stewardship.

- Product Portfolio: Monopoly, Play-Doh, Transformers, My Little Pony, and others

- Recent Developments: In July 2025, Hasbro appointed Jasnor Australia as the master toy distributor for its preschool franchise Peppa Pig across Australia and New Zealand, strengthening the brand’s retail presence in the ANZ market. The partnership, facilitated by Merchantwise, will see Jasnor manage distribution across categories including plush toys, figurines, playsets, roleplay items, nursery products, electronic learning aids, and feeding accessories.

- Strategic Focus: Hasbro's Australia strategy leverages franchise longevity and cross-generational appeal, with nostalgia-driven product revivals targeting parent purchasers alongside fresh digital-integration features designed to engage digitally-native children, maintaining dual-generational relevance across its core portfolio.

Market Concentration Analysis

The Australia toys market is moderately concentrated at the national level, with no single company holding more than 10-15% of total market revenue. The market reflects the global toys industry structure of major multinational brand owners competing alongside strong regional challengers and growing direct-to-consumer digital-native brands that are reshaping traditional distribution economics.

Domestic consolidation is more advanced in specific segments. The leading domestic manufacturer holds a disproportionate value share in the collectibles and local IP segment through franchise licensing scale, while the leading international construction toy company dominates the premium construction category. Global consolidation through M&A is ongoing as digital entertainment companies seek physical merchandise revenue streams through toy company acquisitions and licensing partnerships aligned with streaming content strategies.

Investment & Growth Opportunities

Fastest-Growing Segments

Online stores at ~4.2% CAGR through 2034 represent the highest-growth channel, driven by e-commerce infrastructure maturation, same-day delivery capability, and the ongoing transition of toy purchasing behaviour toward digital platforms. The Above 10 Years age segment at ~3.8% CAGR is the fastest-growing consumer group, fuelled by collectibles, STEM robotics, and digital-integrated toy categories commanding above-average price points.

Emerging Market Opportunities

The eco-friendly toys segment presents a significant whitespace opportunity aligned with Australian consumer sustainability values and forthcoming packaging regulation changes. Brands successfully communicating and certifying sustainable credentials are positioned to command premium pricing and elevated brand loyalty in the Australian market, where environmental consciousness among millennial parents is a documented purchasing decision driver across retail categories.

Venture & Investment Trends

Private equity interest in the Australian toy distribution and retail sector is growing, with the fragmented specialty retail landscape presenting consolidation opportunities. Digital-physical hybrid toy platforms combining app ecosystems with physical product lines represent high-valuation investment targets given their potential for recurring digital revenue alongside traditional product sales. Indigenous-owned toy brands and culturally significant content developers represent emerging investment opportunities supported by government cultural development funding.

Future Market Outlook (2026-2034)

The Australia toys market is forecast to expand from USD 2.35 Billion in 2025 to USD 3.12 Billion by 2034 at a CAGR of 3.10%, adding approximately USD 770 Million in incremental annual market value over the forecast period. This consistent growth reflects stable demographic fundamentals, ongoing STEM education investment, and expanding adult consumer participation through collectibles and gaming-linked toy categories.

Three structural forces will shape the Australia toys market through 2034. First, digital-physical integration will deepen with AI personalisation, AR enrichment, and IoT-connected play becoming standard features across premium toy categories. Second, sustainability mandates under the Australian Packaging Covenant Organisation's eco-modulation framework will reshape material and packaging strategies across all market participants. Third, Australia's multicultural demographic evolution and growing Indigenous cultural representation will create sustained demand for culturally localised and inclusive toy product lines across all age categories.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Australia toys market stakeholders, including senior brand managers at major toy companies, retail category buyers, early childhood development educators, ACCC product safety specialists, and consumer insights professionals. Primary data validated market sizing, age group and sales channel segment shares, regional demand estimates, and technology adoption timelines across the Australian market.

Secondary Research

Key secondary sources include Australian Bureau of Statistics household expenditure surveys, ACCC product safety enforcement reports, Toy Association of Australia industry data, Australian Curriculum documentation for Digital Technologies, Retail Doctor Group Australian toy retail analysis, and trade publications including Toy & Hobby Retailer Magazine. International toy industry data from leading market research organisations were cross-referenced for global context and benchmarking.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating Australian GDP growth projections, birth rate and age demographic trends, household disposable income forecasts, e-commerce penetration trajectories, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty and regulatory change.

Australia Toys Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Action Figures, Building Sets, Dolls, Games and Puzzles, Sports and Outdoor Toys, Plush, Others |

| Age Groups Covered | Up to 5 Years, 5 to 10 Years, Above 10 Years |

| Sales Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Department Stores, Online Stores, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Hasbro, Jazwares, LLC, Mattel, The LEGO Group, ZURU, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia toys market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia toys market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia toys industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Toys Market Report

The Australia toys market reached USD 2.35 Billion in 2025, reflecting consistent demand from STEM education spending, licensed franchise products, and a growing omnichannel retail environment across all major Australian states and territories.

The market is projected to reach USD 3.12 Billion by 2034, growing at a CAGR of 3.10% during 2026-2034, driven by digital-physical toy integration, rising household incomes, collectibles culture expansion, and sustained demand for educationally-validated products.

The 5 to 10 Years age group leads with a 38.5% share in 2025, valued for its broad product compatibility across educational, creative, and physical play categories. The Up to 5 Years segment follows at 34.2%, while Above 10 Years accounts for 27.3%.

Online stores lead at 34.8% in 2025, reflecting Australia's mature e-commerce infrastructure and the structural shift in toy purchasing behaviour toward digital platforms. Supermarkets and hypermarkets follow at 26.7%, with specialty stores at 18.9%.

The Australia Capital Territory & New South Wales commands a dominant 31.7% share in 2025, driven by Sydney's retail density and Australia's highest household income levels. Victoria & Tasmania follow at 24.6%, with Queensland at 19.8%.

Online stores are the fastest-growing channel at approximately 4.2% CAGR through 2034, driven by same-day delivery capability, broad SKU range, competitive pricing, and the continued shift of family purchasing behaviour toward digital retail platforms.

Leading companies include Hasbro, Jazwares, LLC, Mattel, The LEGO Group, ZURU, and others.

Key growth drivers include rising STEM education adoption and government funding, strong licensed franchise demand led by Australian IP such as Bluey, increasing household disposable income, expanding e-commerce infrastructure, and the growing adult collectibles and gaming-linked toy segment.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)