Australia Travel Insurance Market Size, Share, Trends and Forecast by Insurance Type, Coverage, Distribution Channel, End User, and Region, 2026-2034

Australia Travel Insurance Market Size & Forecast 2026-2034

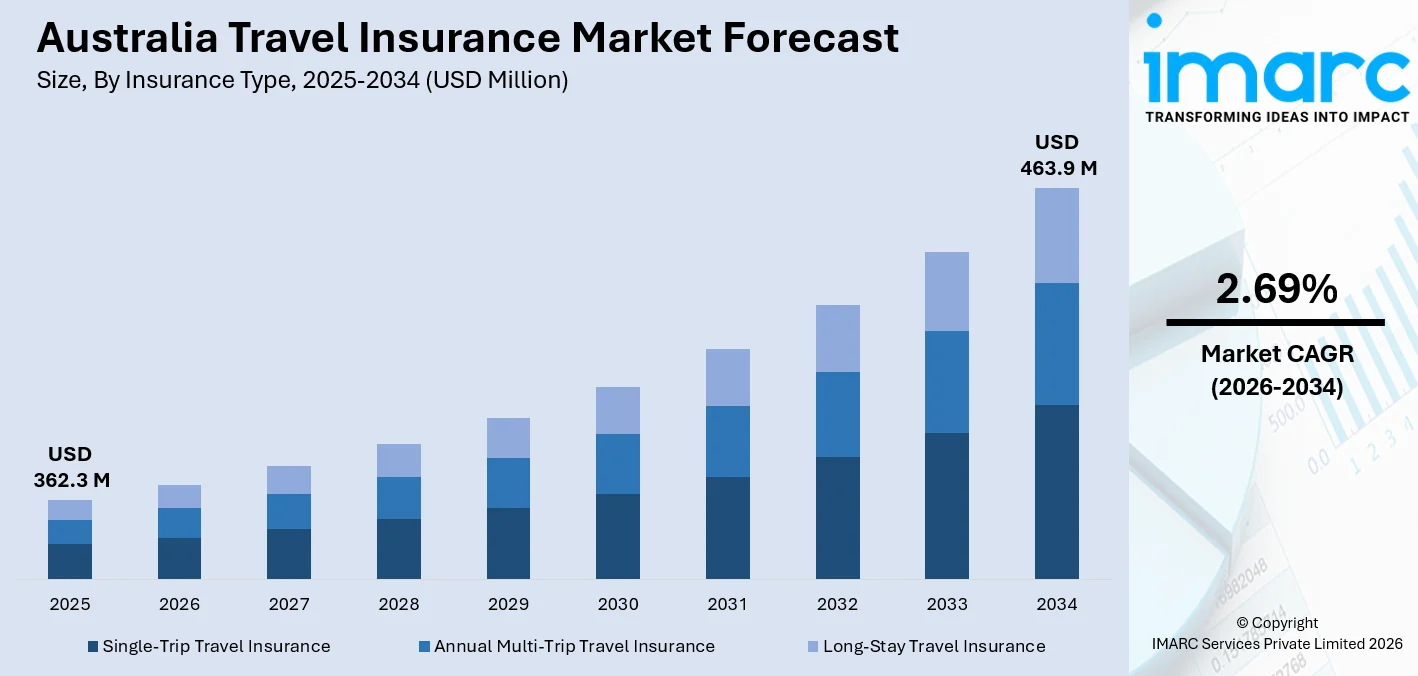

The Australia travel insurance market size, valued at USD 362.3 Million in 2025, is projected to reach USD 463.9 Million by 2034, growing at a CAGR of 2.69% from 2026-2034, driven by surging outbound travel, rising consumer awareness of travel-related financial risks, and rapid adoption of digital insurance platforms. According to the Australian Bureau of Statistics, Australians completed 11.5 million overseas trips in 2024, surpassing pre-pandemic levels for the first time, generating expanding demand for travel protection across the Australia travel insurance market share.

To get more information on this market Request Sample

Australia Travel Insurance Industry Analysis — Key Insights

- Single-Trip Travel Insurance commands 48% of the insurance type segment in 2025- ideal for one-off leisure and business trips, its affordability and per-trip customization make it the structural preference for the majority of Australian travelers.

- Medical Expenses leads coverage at 42% in 2025- overseas healthcare represents the most severe and unpredictable cost risk for travelers, making medical expense coverage the undisputed anchor product in every policy tier.

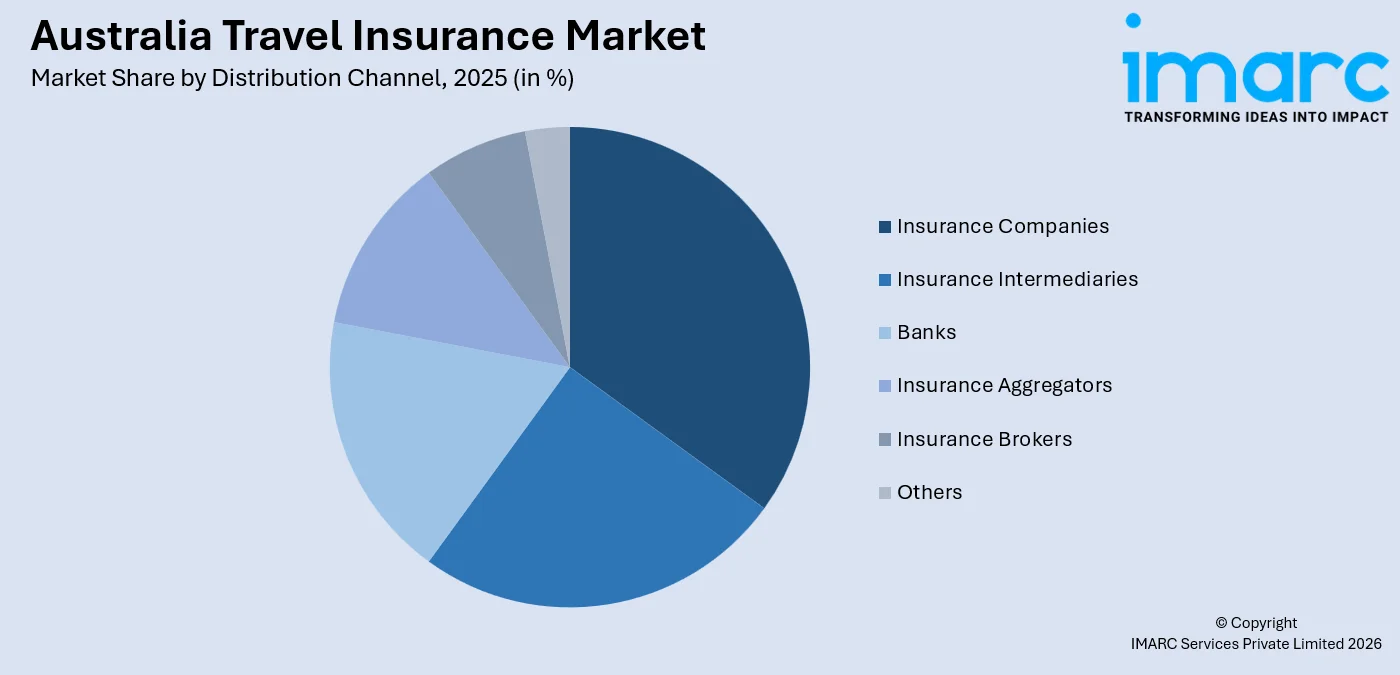

- Insurance Companies hold 32% of the distribution channel segment in 2025- direct insurer channels dominate because consumers trust branded providers for policy clarity, claims support, and compliance-backed product disclosures.

- Family Travelers lead end user at 35% in 2025- multi-person trips multiply financial exposure to cancellations and medical emergencies, making comprehensive family plans the highest-value and most widely purchased policies.

- Australia Capital Territory & New South Wales leads regionally at 33% in 2025- Sydney's status as Australia's primary international gateway drives the highest volume of outbound departures and insurance policy uptake in the country.

Australia Travel Insurance Trends and Dynamic 2026

Market Trends

Rising Risk Awareness and Post-Pandemic Behavioral Shifts

Australia's post-pandemic travel habits have significantly altered consumers' perceptions about insurance. Nowadays, it is common for travelers to include coverage in their planning budgets, viewing insurance as an essential safety measure rather than an optional expense. According to industry reports, comprehensive, all-inclusive policies accounted for 86% of all travel insurance sales in Australia in 2025, demonstrating the market's evident preference for breadth over basic coverage. This cultural shift is most evident in product purchase patterns.

Digital Transformation and AI-Driven Insurance Platforms

From distribution to claims processing, the whole travel insurance value chain is being transformed by technology. Leading Australian travel insurance Fast Cover and claims technology company Five Sigma collaborated in 2025 to implement an AI-driven claims management platform, which greatly reduced claim turnaround times and sped up the entire process from the first notice of loss to payment. Travel insurance market developments in Australia are being defined by this shift toward AI-powered underwriting, real-time policy management, and embedded digital distribution.

Cruise and Niche Travel Segment Expansion

As Australians expand their travel habits, specialty insurance markets are expanding quickly. In partnership with Norwegian Cruise Line, Allianz Partners Australia introduced a cruise-specific travel insurance package in May 2025 that provides integrated coverage for emergency evacuation, shipboard medical care, and cabin confinement at the time of booking. The wider trend toward embedded distribution as a growth engine is reflected in the incorporation of specialized insurance products into travel partner platforms.

- Premium Customization and Add-On Culture: Travelers can now customize base policies to fit particular activity profiles thanks to insurers' growing selection of modular add-ons, such as adventure packs, cruise packs, and snow packs.

- Embedded Insurance at Point of Sale: In order to increase policy take-up rates through smooth, contextual purchase moments, airlines, travel agencies, and online booking platforms are integrating insurance at the point of sale.

- Annual Multi-Trip Policy Uptake: Due to the cost-effectiveness of annual multi-trip plans, frequent business and leisure travelers are pushing insurers to expand their product offerings and become more competitive in this market.

- Telemedicine Integration in Claims: By offering passengers real-time medical consultations overseas, telehealth services integrated into travel insurance plans are preventing small health issues from escalating into complete repatriation occurrences.

Growth Drivers

Surging Outbound and Inbound Travel Activity

Travel volumes in Australia have firmly returned to a rising trend. In the 2024–2025 fiscal year, the Australian Bureau of Statistics recorded 8,402,400 tourist arrivals, a 5.5% increase over the previous year. In January 2025, resident returns increased 10.9% year over year to 1,544,890 journeys as Australians' own international departures reached record speed. Higher travel volumes directly translate into increased uptake across the expansion of the Australian travel insurance market since each new departure represents a potential insurance purchase.

Rising Overseas Medical Costs Heightening Protection Needs

Medical coverage is becoming the main factor driving Australian travelers to purchase travel insurance due to rising healthcare costs overseas. Travelers are being encouraged to prioritize comprehensive protection when planning international excursions due to growing awareness of the potential financial risks involved with abroad medical treatment and emergency help. As travelers seek financial stability and access to medical support services while overseas, destinations with higher healthcare costs, especially long-haul travel markets that Australians commonly visit, are highlighting the need of having sufficient insurance coverage.

Favorable Demographics and Growing Senior Traveler Base

The need for more expensive, all-inclusive travel insurance policies is structurally supported by Australia's aging population. According to industry data from 2025, the top buyer demographic in the Australian travel insurance market is mature travelers and early retirees, who regularly select comprehensive coverage for increased peace of mind. Specialty senior traveler products are positioned as a significant opportunity within the Australia travel insurance market projection due to this demographic's demand for all-inclusive plans with greater coverage limits, which maintains premium revenue growth.

- Digital Distribution Expansion: By making policy comparison, purchasing, and claims easier, online aggregators, mobile apps, and direct insurer websites are greatly reducing obstacles and growing the addressable consumer base.

- Regulatory Oversight and Consumer Trust: APRA and ASIC oversight guarantees product transparency and claims dependability, bolstering consumer trust and promoting increased insurance acceptance among previously uninsured travelers.

- International Education and Student Travel Growth: Demand for long-stay insurance, a specialist market with significant growth potential and higher average premiums, is being driven by an increase in foreign student arrivals and Australians studying overseas.

- Consolidation and Product Innovation: Major insurers' strategic M&A activity is growing their product portfolios, distribution networks, and brand reach, giving Australian consumers more competitive and unique coverage options.

Market Restraints

Complex Policy Terms and Consumer Confusion: Average consumers may find it challenging to understand the complex exclusions, sub-limits, and qualifying requirements found in travel insurance products. In the end, this complexity can limit market penetration among less financially competent traveler segments by undermining customer confidence, causing policy under-purchasing, and creating friction at the time of sale.

High Premium Sensitivity Among Budget Travelers: Travelers who are cost-conscious, especially younger travelers and backpackers, often choose to directly absorb risk rather than get travel insurance. In particular traveler profiles, price sensitivity puts a structural ceiling on market penetration, putting pressureokay on insurers to strike a compromise between affordability and sufficient coverage depth without sacrificing profitability.

Pre-Existing Medical Condition Exclusions and Coverage Gaps: Policies that prohibit or place burdensome restrictions on pre-existing medical illnesses are a major barrier for travelers who are elderly or chronically ill, a demographic group that is expanding. For a segment of the market with the greatest demands for travel protection, these exclusions diminish the applicability and perceived value of ordinary policies.

Australia Travel Insurance Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Insurance Type |

Single-Trip Travel Insurance |

48% |

2025 |

|

Coverage |

Medical Expenses |

42% |

2025 |

|

Distribution Channel |

Insurance Companies |

32% |

2025 |

|

End User |

Family Travelers |

35% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

33% |

2025 |

Insurance Type Insights

Single-Trip Travel Insurance - 48% Market Share (2025) | Leading Insurance Type

Single-trip travel insurance remains the most widely adopted product in the Australia travel insurance market, capturing nearly half of all policy sales.

Single-trip policies predominate because they perfectly cater to the needs of Australia's largest traveler cohorts, which include business professionals on specified assignments and leisure travelers enjoying yearly vacations. Customers can pay only for the coverage they require without having to make the larger commitment of an annual plan because these policies are activated for a predetermined journey duration. For most Australian outbound travelers, especially families and first-time foreign visitors, single-trip goods are the preferred option due to their price and ease of use.

|

Segment Breakdown Single-Trip Travel Insurance (48%) · Annual Multi-Trip Travel Insurance · Long-Stay Travel Insurance |

Coverage Insights

Medical Expenses - 42% Market Share (2025) | Leading Coverage

Medical expenses coverage is the single most sought-after component of any Australian travel insurance policy, holding the highest share across all coverage categories.

Due to the financial risks involved in receiving medical care overseas, medical expense protection is still the main feature of travel insurance coverage in Australia. In order to accommodate overseas travelers' probable treatment and repatriation needs, insurers are designing plans with extensive medical and emergency assistance coverage. Because of this, large medical coverage limits that are intended to offer comprehensive protection against unforeseen health-related accidents abroad are frequently included in Australian travel insurance packages. This reinforces medical coverage as the primary component of policy design in the market.

|

Segment Breakdown Medical Expenses (42%) · Trip Cancellation · Trip Delay · Property Damage · Others |

Distribution Channel Insights

Access the comprehensive market breakdown Request Sample

Insurance Companies - 32% Market Share (2025) | Leading Distribution Channel

Direct sales through insurance companies represent the leading distribution channel, reflecting Australian consumers' preference for engaging directly with branded, compliance-regulated providers.

Strong brand trust and the complexity of travel insurance products, which customers frequently prefer to buy from a reputable supplier they can interact with directly for claims or policy inquiries, are the main reasons why insurance companies dominate direct distribution. According to IBISWorld statistics from 2025, Allianz Australia has a domestic market share of about 25%, while Zurich/Cover-More has a share of about 24%. Together, these companies control almost half of the industry, demonstrating the power that insurer-direct brands have in acquiring customers throughout Australia.

|

Segment Breakdown Insurance Companies (32%) · Insurance Intermediaries · Banks · Insurance Aggregators · Insurance Brokers · Others |

End User Insights

Family Travelers - 35% Market Share (2025) | Leading End User

Family travelers account for the largest share of end users, driven by the compounding financial risk of multi-person trips that makes comprehensive insurance coverage effectively indispensable.

Families that travel together are more vulnerable to lost luggage, medical problems, and cancellation fees overall. In response, insurers provide family-specific plan structures that provide coverage for traveling companions and dependents under a single policy, frequently at advantageous all-inclusive premium prices. Both the volume of family vacation travel in Australia and the segment's proven willingness to invest on complete protection for high-stakes trips are reflected in the concentration of family travelers in the 35% leading share position.

|

Segment Breakdown Family Travelers (35%) · Senior Citizens · Education Travelers · Business Travelers · Others |

Regional Insights

Australia Capital Territory & New South Wales - 33% Market Share (2025) | Leading Region

New South Wales and the Australian Capital Territory together command the largest regional share of the Australia travel insurance market, anchored by Sydney's position as the country's primary international aviation gateway. The Australian Bureau of Statistics recorded 308,940 short-term resident returns through New South Wales in November 2025, the highest of any Australian state or territory, confirming the region's structural importance as the national center of outbound travel activity and, by extension, insurance demand.

Sydney's concentration of corporate headquarters, financial services firms, and high-income professional households reinforces demand for both individual and business travel insurance across premium policy tiers. The ACT contributes a government and public service traveler base with strong compliance-driven insurance uptake. Together, the NSW & ACT region's concentration of travel departures, commercial activity, and high-value itineraries makes it the dominant insurance market across all product categories.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 33% |

| Key Growth Drivers | International gateway status, corporate travel volumes, premium policy demand, high household income levels |

| Outlook | Continues to lead national insurance market |

|

Regional Breakdown Australia Capital Territory & New South Wales (33%) · Victoria & Tasmania · Queensland · Northern Territory & SA · Western Australia |

Market Outlook (2026-2034)

What is the future outlook of the Australia travel insurance market?

Rising travel activity, growing consumer risk awareness, and continuous digital revolution in insurance distribution and service delivery all contribute to the travel insurance market's promising future outlook in Australia. Long-term market demand is being strengthened by Australian travelers' growing perception of travel insurance as a necessary part of trip planning rather than an optional add-on as both domestic and international travel continue to normalize and grow. Policy adoption among leisure and business travelers is anticipated to be sustained by rising outward travel volumes and increased exposure to disruptions such medical emergencies, cancellations, and climate-related disasters.

Australia Travel Insurance Market - Leading Key Players

The Australia travel insurance market is served by a blend of global insurance conglomerates and specialized domestic providers, with the competitive landscape currently shaped by significant consolidation activity. Allianz Australia and Zurich's Cover-More collectively command nearly half of the domestic market, while digital-native insurers and travel-affiliate brands are competing on product innovation and platform integration to capture younger, price-sensitive consumers.

| Company | Leading Brands | Highlights |

|---|---|---|

|

Allianz Australia Limited |

Allianz Travel, Allianz Comprehensive, Domestic, Multi-Trip |

Australia's largest travel insurer with ~25% market share; led October 2025 acquisition bid for NIB Holdings' travel unit (World Nomads, Travel Insurance Direct); cruise add-on and adventure pack product range |

|

Fast Cover Pty Ltd |

Fast Cover Travel Insurance |

Leading digital-first travel insurer; partnered with Five Sigma in June 2025 to deploy AI-driven claims platform accelerating FNOL-to-settlement process; strong online aggregator presence |

|

American Express Company |

Amex Travel Insurance, Platinum Travel Credit |

Bundles premium travel insurance within high-value card membership tiers; strong uptake among frequent flyers and business travelers; complements broader travel rewards and lounge access benefits |

Some of the major players in the Australia travel insurance market include Zurich Financial Services Australia Ltd., nib Travel Services (Australia) Pty Ltd., AIG Australia Limited, 1Cover Pty Ltd., Australia Post Group, etc.

Latest Development & News

- In May 2025, a new AI-powered claims management platform created in collaboration with Five Sigma was implemented by Fast Cover, a well-known Australian travel insurance company. The solution shortens processing times and enhances customer results by streamlining the whole claims lifecycle from the initial notice of loss to settlement. The implementation is a component of a larger industry shift in Australian travel insurance toward technology-led service transformation.

- In May 2025, in collaboration with Norwegian Cruise Line, Allianz Partners Australia introduced a cruise-specific travel insurance package that is offered at the time of booking. The product is a calculated addition to Allianz's specialty embedded insurance portfolio for Australian tourists in the expanding cruise travel market. It offers embedded coverage for shipboard medical treatment, emergency evacuation, and cabin confinement.

Australia Travel Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Insurance Types Covered | Single-Trip Travel Insurance, Annual Multi-Trip Insurance, Long-Stay Travel Insurance |

| Coverages Covered | Medical Expenses, Trip Cancellation, Trip Delay, Property Damage, Others |

| Distribution Channels Covered | Insurance Intermediaries, Banks, Insurance Companies, Insurance Aggregators, Insurance Brokers, Others |

| End Users Covered | Senior Citizens, Education Travelers, Business Travelers, Family Travelers, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia travel insurance market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Australia travel insurance market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia travel insurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Travel Insurance Market Report

The Australia travel insurance market was valued at USD 362.3 Million in 2025.

The Australia travel insurance market is anticipated to reach a value of USD 463.9 Million by 2034.

Single-trip travel insurance dominates the market with a share of 48%, driven by its affordability and suitability for one-off leisure and business journeys, making it the default choice for the majority of Australian travelers seeking straightforward, cost-effective protection.

Medical expenses coverage commands the market with a share of 42%, reflecting the high financial risk of overseas healthcare costs and the deeply embedded consumer understanding that medical coverage is the most critical component of any travel insurance plan.

Some of the major players in the Australia travel insurance market include Allianz Australia Limited, Zurich Financial Services Australia Ltd., nib Travel Services (Australia) Pty Ltd., Fast Cover Pty Ltd, AIG Australia Limited, 1Cover Pty Ltd., Australia Post Group, American Express Company, etc.

Key trends include the rapid integration of AI and digital technology across the policy and claims lifecycle, the growth of embedded insurance distribution through airlines and booking platforms, rising demand for cruise-specific and adventure specialty products, and increasing adoption of annual multi-trip policies by frequent travelers. Telemedicine integration and parametric insurance models are also emerging as forward-looking product innovations.

Australia Capital Territory & New South Wales currently leads the Australia travel insurance market, accounting for a share of 33%. The region benefits from Sydney's status as Australia's primary international aviation gateway, high household income levels, concentrated corporate travel activity, and the greatest volume of outbound international departures nationally.

Growth is driven by the sustained recovery and expansion of Australian outbound travel volumes, rising overseas medical costs that elevate consumer demand for financial protection, favorable ageing demographics with high insurance uptake rates among senior travelers, expanding digital distribution channels, and increasing product innovation including family-focused plans, niche coverage for cruise and adventure travelers, and embedded insurance at point of booking.

Key challenges include the complexity of policy terms and exclusion clauses that generate consumer confusion and reduce uptake among less informed buyer segments, persistent premium sensitivity among younger and budget-focused traveler cohorts, and the restrictive treatment of pre-existing medical conditions which limits the relevance of standard policies for a growing base of senior and chronically ill travelers who represent some of the market's highest-potential buyers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)