Australia Used Car Market Size, Share, Trends and Forecast by Vehicle Type, Vendor Type, Fuel Type, Sales Channel, and Region, 2026-2034

Australia Used Car Market Size, Share, Trends & Forecast (2026-2034)

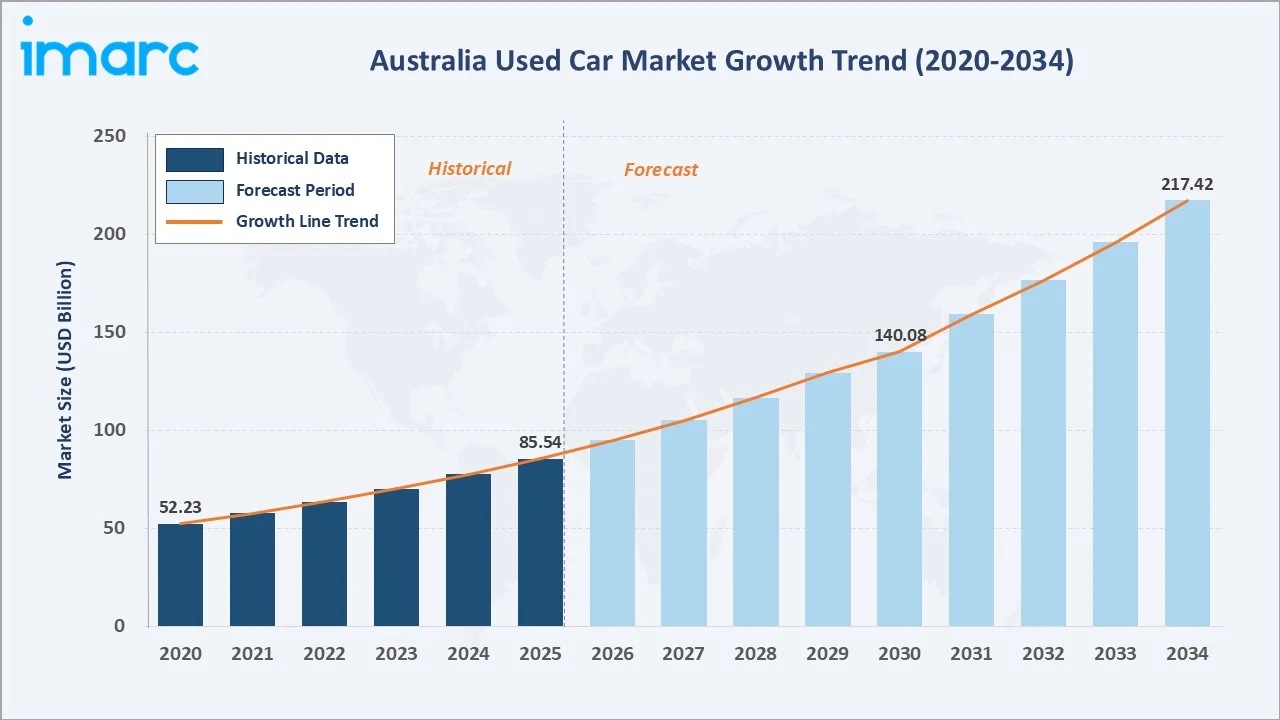

The Australia used car market size was valued at USD 85.54 Billion in 2025 and is projected to reach USD 217.42 Billion by 2034, exhibiting a CAGR of 10.37% during the forecast period 2026-2034. Rising cost-of-living pressures, rapid expansion of digital automotive platforms, and sustained consumer demand for affordable pre-owned vehicles are the primary growth levers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 85.54 Billion |

|

Forecast Market Size (2034) |

USD 217.42 Billion |

|

CAGR 2026-2034) |

10.37% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

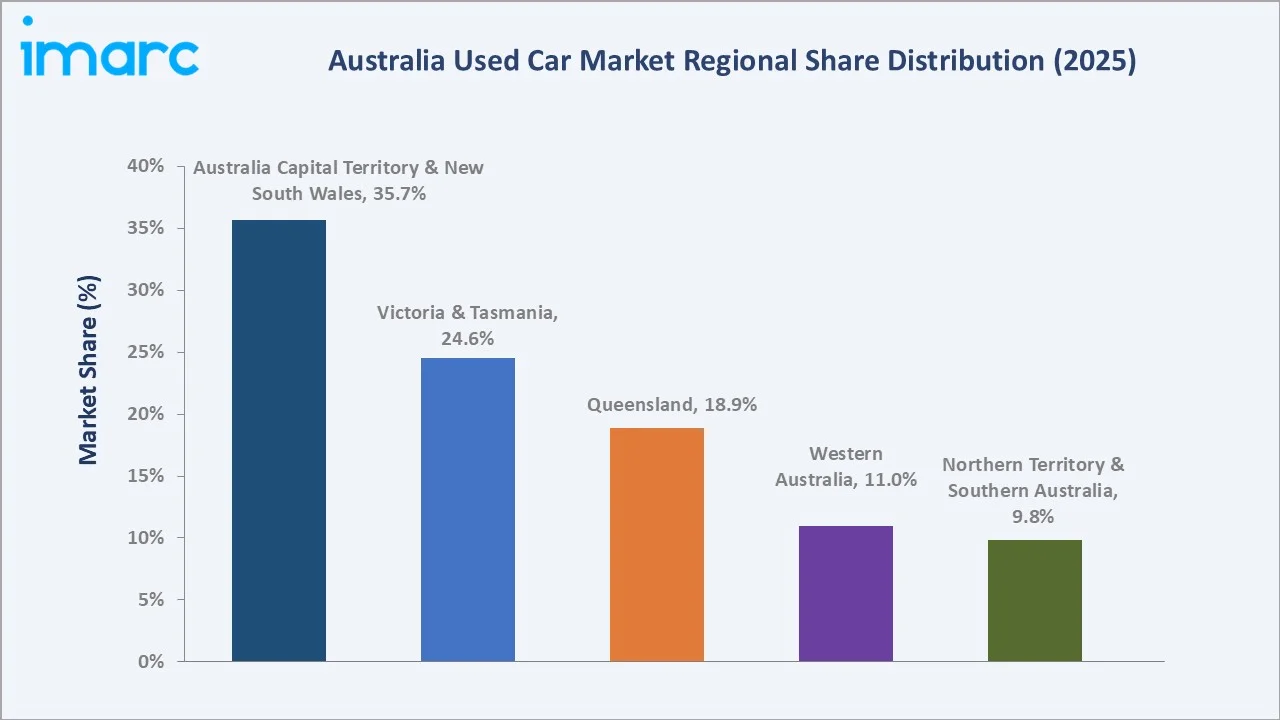

Australia Capital Territory & New South Wales (35.7%, 2025) |

|

Fastest Growing Region |

Western Australia |

|

Leading Fuel Type |

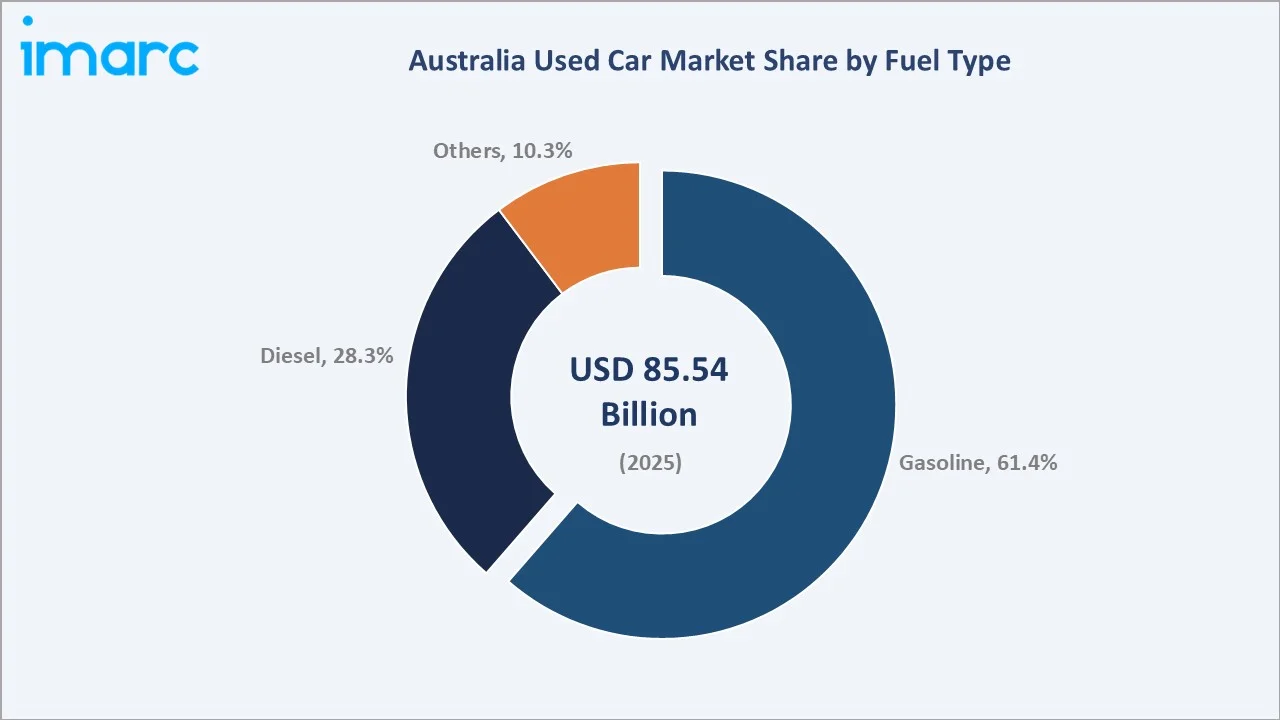

Gasoline (61.4%, 2025) |

|

Leading Vendor Type |

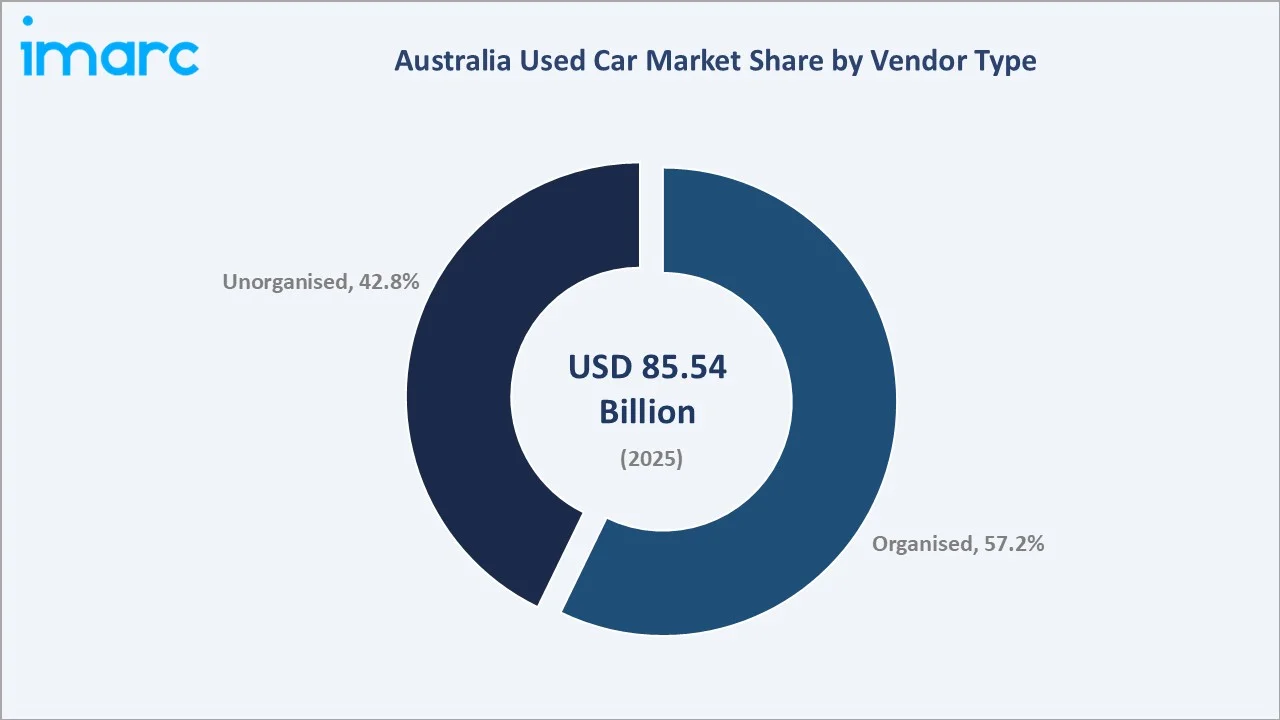

Organised (57.2%, 2025) |

The chart below illustrates the Australia used car market growth trajectory from 2020 through 2034, contrasting historical performance against the sustained forecast expansion.

To get more information on this market, Request Sample

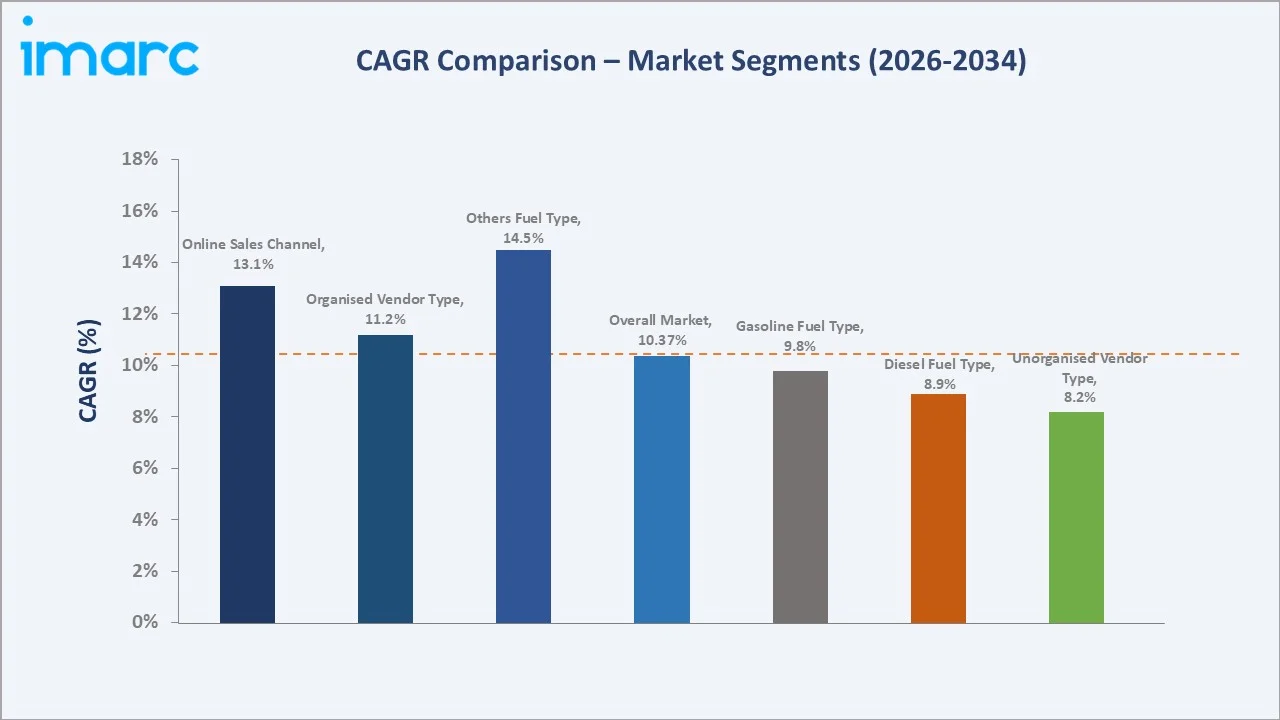

The CAGR comparison chart below highlights segment-level compound annual growth rates against the overall market CAGR of 10.37% for the forecast period 2026-2034.

Executive Summary

The Australia used car market recorded a value of USD 85.54 Billion in 2025 and is projected to expand at a CAGR of 10.37% between 2026 and 2034, reaching USD 217.42 Billion. This growth reflects fundamental shifts in consumer purchasing behaviour, driven by cost-of-living pressures, robust supply of quality pre-owned vehicles, and the rapid rise of digital automotive marketplaces. The market recorded USD 52.23 Billion in 2020, affirming more than 63% cumulative growth in the historical period.

Gasoline-powered vehicles dominate the fuel-type segmentation at 61.4% share in 2025, supported by broad model availability and established refuelling infrastructure. Diesel vehicles follow at 28.3%, primarily driven by commercial and regional-use preferences. On the vendor front, organised dealers account for 57.2% of transactions, aided by certification programmes, transparent pricing platforms, and structured financing options that build consumer trust. The unorganised segment at 42.8% is gradually ceding share as digital tools formalise private transactions.

Geographically, the Australian Capital Territory and New South Wales lead with a combined 35.7% share, underpinned by high population density and strong digital platform adoption. Victoria and Tasmania follow at 24.6%, Queensland at 18.9%, Western Australia at 11.0%, and the Northern Territory and Southern Australia at 9.8%. Digital transformation, growing acceptance of electric and hybrid pre-owned vehicles, and expanding organised dealer networks will serve as the key structural drivers through 2034.

Key Market Insights

|

Insight |

Data |

|

Market Size (2025) |

USD 85.54 Billion |

|

Forecast Market Size (2034) |

USD 217.42 Billion |

|

CAGR (2026-2034) |

10.37% |

|

Largest Fuel Segment |

Gasoline – 61.4% share (2025) |

|

Largest Vendor Segment |

Organised – 57.2% share (2025) |

|

Dominant Region |

Australia Capital Territory & New South Wales– 35.7% (2025) |

|

Top Companies |

BMW Group, Carma, CARS24, CAR Group Limited, Only Sales Limited, Nine Entertainment Company |

|

Market Opportunity |

Growing EV pre-owned segment & digital-first dealerships |

The Following Analytical Observations Expand on the Key Data Points Above:

- Gasoline's 61.4% dominance (2025): reflects broad model diversity and an extensive refuelling network across Australia. The segment benefits from consumer familiarity, competitive insurance costs, and wide availability across all price tiers from compact city cars to full-size SUVs.

- Diesel's 28.3% share: is underpinned by strong demand from rural buyers, tradespersons, and fleet operators who value diesel's fuel economy over long distances and towing capacity. The Toyota HiLux, Ford Ranger, and Mitsubishi Triton consistently rank among Australia's most-traded used diesel vehicles.

- Organised vendors' 57.2% (2025): reflect growing consumer preference for certified pre-owned programmes with warranty coverage, vehicle history reports, and structured financing. Platforms such as CARS24 and Carsales.com are catalysts for this formalisation.

- Australia Capital Territory & New South Wales lead at 35.7%: is driven by Sydney's large population base, high per-capita incomes, and the concentration of organised dealerships and digital platform headquarters in the metropolitan area.

- Historical growth USD 52.23B (2020) to USD 85.54B (2025): Establishes a strong growth baseline, remaining closely aligned with the projected expansion trajectory through 2034.

- EV pre-owned opportunity: is accelerating as rising plug-in hybrid adoption and strong growth in EV registrations are significantly expanding the future supply of second-hand electrified vehicles for organized dealers.

Australia Used Car Market Overview

Australia's used car market encompasses all pre-registered passenger vehicles, light commercial units, SUVs, and specialty automobiles transacted through organised dealers, certified platforms, and private seller channels. The industry spans the full ecosystem from vehicle acquisition and reconditioning through to financing, warranty provision, and digital transaction services. Key segments include fuel type (gasoline, diesel, others) and vendor type (organised, unorganised).

Macroeconomic drivers rising new vehicle costs, inflationary pressures, and supply chain disruptions – have structurally redirected consumer demand toward pre-owned alternatives. Digital platforms have fundamentally reshaped the buying experience, improving transparency and accessibility. By 2034, the market will benefit from a maturing supply of pre-owned hybrid and electric vehicles as Australia's EV penetration accelerates.

Market Dynamics

To evaluate market opportunities, Request Sample

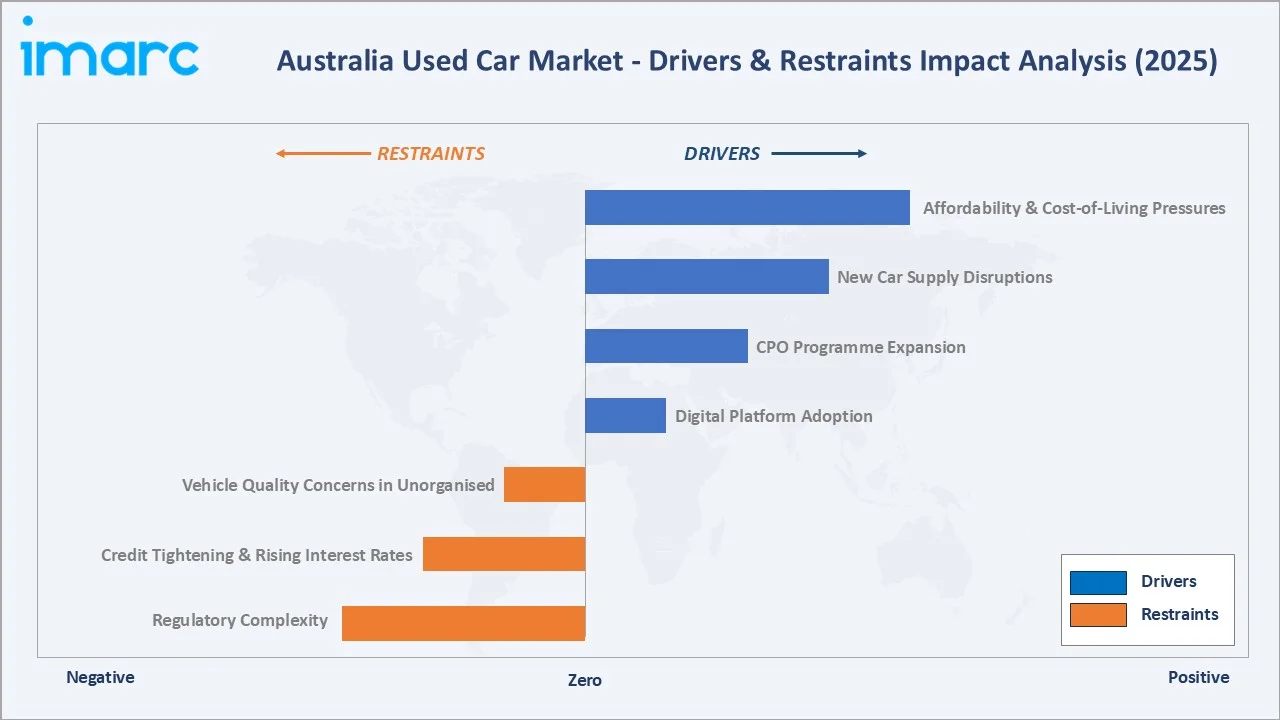

Market Drivers

- Affordability and Cost-of-Living Pressures: New vehicle prices in Australia have increased significantly due to supply chain disruptions and currency pressures, making pre-owned vehicles a more attractive alternative. With substantial cost advantages compared to new models, used vehicles are increasingly preferred by first-time buyers, young families, and budget-conscious consumers facing higher living expenses.

- New Car Supply Disruptions: Global semiconductor shortages and logistics disruptions significantly constrained new vehicle supply between 2021 and 2023, tightening availability across key markets. As a result, models like the Land Rover Defender in the two- to four-year age bracket have retained or even exceeded their original value, highlighting a persistent supply-demand imbalance that continues to support strong demand and pricing in the used car market.

- Certified Pre-Owned Programme Expansion: Authorised CPO programmes from BMW, Toyota, and Hyundai provide multi-point inspections, warranty extensions, and structured financing. These programmes reduce the traditional risk perception of used car purchases, broadening the addressable buyer base to include risk-averse segments such as suburban families and retirees.

- Digital Platform Adoption: Online automotive marketplaces led by Carsales.com, CARS24, and Drive.com.au have democratised access to pricing benchmarks, vehicle history, and condition data. FinTech startup AutoSettle launched in March 2024, improving settlement security and instant payment processing – further reinforcing digital confidence.

Market Restraints

- Vehicle Quality Concerns in Unorganised Channels: Limited inspections, lack of certified documentation, and risk of hidden defects reduce buyer confidence. This drives preference toward authorised dealers, restricting growth and transaction volumes within informal or peer-to-peer vehicle sales segments.

- Credit Tightening and Rising Interest Rates: The Reserve Bank of Australia's rate hiking cycle between 2022 and 2024 raised financing costs for buyers and dealers alike. Higher monthly repayments reduce the effective affordability advantage of used vehicles, particularly for buyers relying on personal loans or dealer financing.

- Regulatory Complexity Across States: Roadworthy certificate requirements, emissions testing standards, and consumer protection regulations vary by state and territory. This increases compliance costs for dealers operating multi-state networks and creates inconsistencies in the buyer experience.

Market Opportunities

- Growth of Pre-Owned EV and Hybrid Segment: With EV registrations rising sharply year-on-year, the supply of pre-owned electric and hybrid vehicles is expected to expand significantly from the near term. Organised dealers establishing specialist EV reconditioning and battery health-check capabilities are likely to capture premium margins in this emerging, high-growth sub-segment.

- Expansion into Regional and Rural Markets: Regional Australia remains underserved by organised dealers. Digital platforms and hub-and-spoke dealer models offer significant opportunities to formalise rural market transactions, increase average selling prices, and grow market share in Queensland, Western Australia, and the Northern Territory.

- Subscription and Flexible Ownership Models: Emerging vehicle subscription services offering flexible monthly-fee access to pre-owned vehicles are gaining interest among urban consumers, particularly younger buyers and short-term residents, representing an incremental revenue stream for dealer groups.

Market Challenges

- Inventory Volatility and Vehicle Sourcing Costs: As new car supply normalises post-pandemic, the pipeline of quality three-to-five-year-old trade-in vehicles is tightening. Dealers face increased competition at auctions and from manufacturer buy-back programmes, elevating procurement costs and compressing gross margins on resales.

- Cybersecurity and Data Privacy Risks: The proliferation of online platforms handling payment data, identity verification, and vehicle history records creates exposure to data breaches. As FinTech integration deepens exemplified by AutoSettle's March 2024 launch robust cybersecurity frameworks will be essential to maintain buyer trust and regulatory compliance.

Emerging Market Trends

1. Digital-First Buying Experience and Online Platform Proliferation

Online platforms – including Carsales.com, CARS24, and Drive.com.au – accounted for a growing share of used car transactions in Australia by 2024, offering end-to-end digital experiences from vehicle discovery through to financing and home delivery. The launch of AutoSettle in March 2024 further digitised settlement and payment workflows. This trend is reshaping buyer expectations toward transparency, speed, and convenience across all transaction stages.

2. Accelerating SUV and Crossover Demand in the Pre-Owned Segment

Pre-owned SUV demand has reached record levels, reflecting a shift in Australian consumer preferences toward versatile, family-oriented vehicles. Organised dealers are increasingly aligning inventory strategies to prioritize SUVs and crossovers, with models such as the Toyota HiLux, Ford Ranger, and Mazda CX-5 consistently ranking among the most traded in the used vehicle market, particularly across Queensland and Western Australia.

3. Rise of Eco-Friendly and Fuel-Efficient Pre-Owned Vehicles

Plug-in hybrid vehicle adoption in Australia is rising as consumers seek to reduce fuel costs, with this shift increasingly reflected in the used car market. Hybrid models from Toyota, Hyundai, and Mitsubishi Motors are gaining greater visibility in pre-owned inventory.

4. Organised Dealer Formalisation and Certification Programmes

Organised vendors held 57.2% of the market in 2025, reflecting ongoing formalisation supported by certified pre-owned programmes, digital inventory management, and structured buyer financing. OEM-backed CPO offerings from BMW, Toyota, and Hyundai are gaining share over unorganised channels by providing warranty coverage, multi-point inspections, and transparent pricing – building consumer confidence particularly among first-time pre-owned buyers.

5. FinTech Integration and Flexible Financing Innovation

Flexible financing products – including novated leases, personal loans, and subscription-based models – are broadening market accessibility. FinTech platforms are enabling faster credit approvals, reducing friction in the purchase journey, and extending the buyer base to individuals previously excluded from traditional dealer financing.

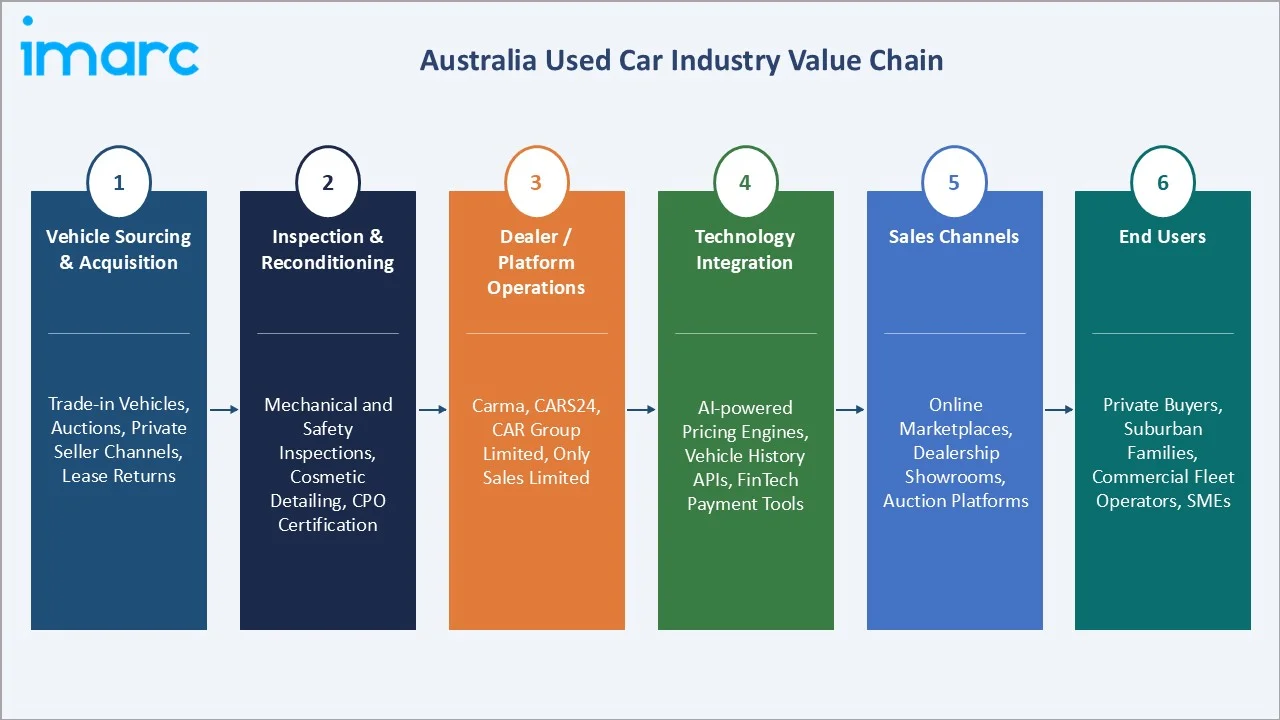

Industry Value Chain Analysis

The Australia used car industry value chain spans six integrated stages, from initial vehicle sourcing through to end-user delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Value Chain Stage |

Description |

|

Vehicle Sourcing & Acquisition |

Trade-in vehicles, auctions, private seller channels, lease returns, and fleet disposal programmes |

|

Inspection & Reconditioning |

Mechanical and safety inspections, cosmetic detailing, paintwork, tyre replacement, and CPO certification processes |

|

Dealer / Platform Operations |

Carma, CARS24, CAR Group Limited, Only Sales Limited |

|

Technology Integration |

AI-powered pricing engines, vehicle history APIs, digital identity verification, and FinTech payment tools |

|

Sales Channels |

Online marketplaces (~13.1% CAGR), dealership showrooms, auction platforms (offline), and subscription services |

|

End Users |

Private buyers, suburban families, commercial fleet operators, SMEs, and regional consumers |

The value chain diagram below illustrates the sequential flow from vehicle sourcing through to end-user delivery, highlighting the alternating roles of reconditioning, technology, and distribution.

Technology Landscape in the Industry

Digital Marketplace and AI Pricing Technology

AI-driven pricing algorithms have become the backbone of organised used car platforms in Australia. Carsales.com and CARS24 deploy proprietary data analytics to optimise vehicle pricing, inventory turnover velocity, and lead quality. These systems ingest real-time supply and demand data, historical transaction records, and macroeconomic indicators to generate dynamic pricing recommendations, improving margin management for dealers and pricing transparency for buyers.

Vehicle History and PPSR Integration

The Personal Property Securities Register (PPSR) is the Australian government's primary vehicle encumbrance database. Digital platforms have deeply integrated PPSR checks, enabling instant verification of finance owing, stolen vehicle status, and write-off history. Automated PPSR integration has materially reduced buyer risk in online transactions, accelerating the shift of consumer trust toward organised digital channels relative to unorganised private sales.

FinTech and Digital Settlement Platforms

The March 2024 launch of AutoSettle introduced a purpose-built transaction platform for the Australian used car market, enabling instant digital settlement, enhanced security protocols, and identity verification integrated with dealerships, financiers, and state motor registries. This FinTech layer reduces settlement timeframes from days to hours, minimising fraud exposure and improving cash flow for dealer groups operating at scale.

EV Battery Health Assessment Technology

As pre-owned electric and hybrid vehicles enter the Australian market in greater numbers from 2026, battery health certification is emerging as a critical technology differentiator for organised dealers. State-of-health (SoH) battery diagnostic tools, battery passport platforms, and third-party certification standards are being adopted by forward-looking dealer groups to underpin credible EV CPO programmes, addressing buyer concerns about degradation and remaining range life.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Sports Utility Vehicle |

38.6% |

2025 |

|

Vendor Type |

Organized |

57.2% |

2025 |

|

Fuel Type |

Gasoline |

61.4% |

2025 |

|

Sales Channel |

Offline |

68.9% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

35.7% |

2025 |

By Fuel Type

To access detailed market analysis, Request Sample

Gasoline leads the Australia used car market fuel-type segmentation with a 61.4% share in 2025. Petrol-powered vehicles remain the dominant choice due to their broad model diversity, established maintenance ecosystem, and lower upfront purchase prices relative to diesel or hybrid alternatives. Demand is particularly strong in urban markets where short commutes limit the fuel-efficiency advantage of diesel.

By Vendor Type

Organised vendors dominate with a 57.2% share in 2025. This segment includes licensed dealerships, certified pre-owned programmes, and technology-enabled platforms such as CARS24, Carsales.com, and HelloCars. The organised segment's growth reflects increasing consumer preference for certified inventory, structured financing, and transparent pricing.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Cities |

|

Australia Capital Territory & New South Wales |

35.7% |

High population density, digital platform adoption, CPO concentration, financial services hub |

Sydney, Canberra |

|

Victoria & Tasmania |

24.6% |

Melbourne dealership networks, state EV incentives, diverse consumer demographics, urban density |

Melbourne, Hobart |

|

Queensland |

18.9% |

SUV demand, lifestyle vehicles, mining-related commercial fleets, interstate migration growth |

Brisbane, Gold Coast |

|

Western Australia |

11.0% |

Resource sector workforce vehicles, remote market expansion, strong diesel demand, digital expansion |

Perth, Broome |

|

Northern Territory & Southern Australia |

9.8% |

Rural and regional demand, LPG and diesel preference, lower new-car penetration, Adelaide hub |

Darwin, Adelaide |

Australia Capital Territory & New South Wales (35.7%)

The ACT and New South Wales corridor commands the largest regional share at 35.7% in 2025. Sydney – Australia's largest city with a population exceeding 5 million – is the primary driver, supported by a high concentration of organised dealerships, digital platform headquarters, and a financially sophisticated consumer base. The presence of major auction houses and OEM-certified pre-owned centres further consolidates the region's leadership position in both volume and value per transaction.

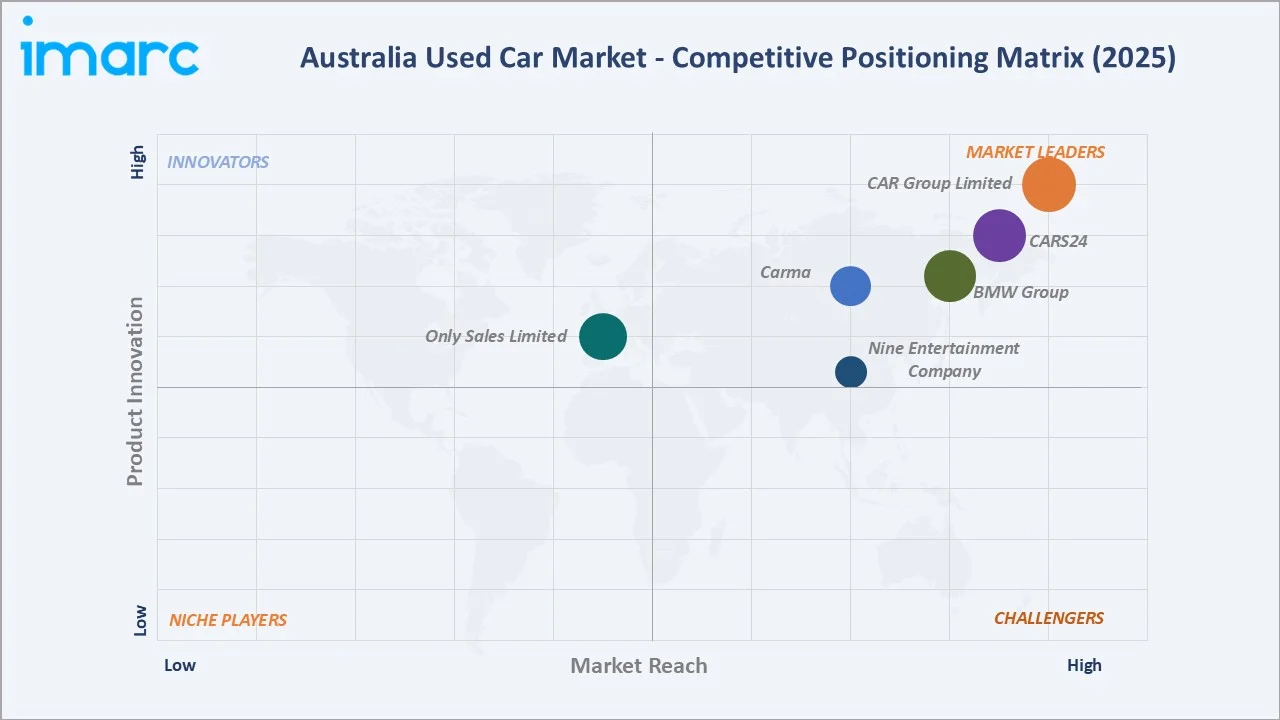

Competitive Landscape

|

Company Name |

Platform / Brand |

Market Position |

Core Strength |

|

BMW Group |

BMW Premium Certified |

Leader |

OEM-certified CPO, premium segment, warranty coverage |

|

Carma |

Carma |

Leader |

Online-first, no-haggle pricing, home delivery model |

|

CARS24 |

CARS24 |

Leader |

Tech-driven, instant cash offers, rapid inventory turnover |

|

CAR Group Limited |

Carsales |

Leader |

Largest marketplace, data analytics, multi-channel reach |

|

Only Sales Limited |

Only Cars |

Challenger |

Community marketplace, broad listing categories |

|

Nine Entertainment Company |

Drive |

Challenger |

Media integration, editorial content, national reach |

The competitive landscape is moderately fragmented, with established digital marketplaces, OEM-certified platforms, and independent online dealers competing for market share. Leaders compete on inventory transparency, digital experience, and financing integration. Technology differentiation – particularly in pricing algorithms, vehicle history data, and instant valuation tools is becoming the primary basis for competitive advantage among organised vendors.

Key Company Profiles

BMW Group

BMW Group is a leading global manufacturer of premium automobiles and motorcycles, headquartered in Munich. It operates the BMW Premium Certified pre-owned programme, offering factory-backed warranty coverage, comprehensive multi-point inspections, and roadside assistance for eligible BMW, MINI, and BMW M vehicles across Australia.

- Product & Platform Portfolio: BMW Premium Certified inventory includes vehicles up to five years old with under 100,000 km, covering the BMW 1-8 Series, X-Series SUVs, i-Series electric and hybrid models, and MINI range, each with extended warranty and service coverage.

- Recent Developments: In 2026, BMW Group is strengthening its presence in the pre-owned vehicle market through its BMW Premium Certified Used Cars program, aimed at enhancing buyer confidence and resale value. The initiative ensures that every certified vehicle undergoes a rigorous 360-degree technical and safety inspection, along with a verified service history before being approved for sale.

- Strategic Focus: BMW's strategy centres on defending premium segment positioning through certified quality assurance, while expanding its i-Series and xDrive pre-owned inventory as the Australian EV fleet matures into secondary market supply.

CARS24

CARS24 is a global used car technology platform operating in Australia with a full-stack model – sourcing, reconditioning, and reselling vehicles directly to consumers. The company is headquartered in Gurugram, India, with Australian operations and presence across the UAE and Southeast Asia.

- Product & Platform Portfolio: CARS24 offers a curated inventory of inspected and reconditioned passenger vehicles across all major brands, available through its online platform with home delivery, seven-day returns, and integrated financing solutions.

- Recent Developments: In 2026, CARS24 is accelerating its expansion in Australia as it prepares for a potential IPO in India within the next 6–12 months. The company is increasing investments in logistics infrastructure, including a new operations hub in Sydney, to scale its end-to-end used car platform.

- Strategic Focus: The company's strategy focuses on gaining share in organised vendor channels through superior digital UX, competitive instant-buy offers to private sellers, and data-driven pricing transparency that builds buyer and seller confidence.

CAR Group Limited

CAR Group Limited is a global leader in online automotive classifieds and digital marketplaces, headquartered in Melbourne. The company operates some of the most prominent vehicle buying and selling platforms worldwide, connecting consumers, dealers, and OEMs.

- Product & Platform Portfolio: The carsales platform (CAR Group Limited ) hosts over 200,000 vehicle listings at any given time, complemented by data services, dealer management tools, insurance products, and consumer financing integrations through partnerships with major Australian lenders.

- Recent Developments: In 2023, CAR Group Limited has announced a strategic acquisition alongside an equity raising to strengthen its global position in digital automotive marketplaces. The move includes expanding its stake in key international platforms.

- Strategic Focus: Carsales is focused on deepening its data and services ecosystem for dealer partners, growing its finance and insurance revenue streams, and leveraging international scale to import marketplace technology innovations from its Korean and Brazilian operations.

Market Concentration Analysis

The Australia used car market exhibits moderate fragmentation with a clear bifurcation between organised and unorganised channels. Organised vendors collectively hold 57.2% of the market in 2025, but within that segment, the top five platforms BMW Group, Carma, CARS24, CAR Group Limited, Only Sales Limited are estimated to account for 30-40% of organised market revenue.

The remaining organised market share is distributed across hundreds of licensed dealerships, franchise dealers, and regional operators. The unorganised 42.8% is highly fragmented, comprising millions of private transactions annually across Gumtree, Facebook Marketplace, and direct seller-to-buyer arrangements. Consolidation trends are strongly evident in organised channels, with well-funded digital platforms leveraging data and scale advantages to aggregate inventory and buyer demand at the expense of standalone regional dealers.

Through 2034, continued platform consolidation, OEM investment in certified pre-owned programmes, and the increasing capital requirements for EV reconditioning capabilities are expected to raise the minimum scale threshold for competitive viability among organised dealers, accelerating formalisation of market share among the top ten platforms.

Investment & Growth Opportunities

Fastest-Growing Segments

The Others fuel-type segment – comprising hybrid, PHEV, and battery electric vehicles – is the highest-growth sub-segment in Australia's used car market, expanding at an estimated CAGR of approximately 14.5% through 2034. This is driven by the expanding supply of first-generation electrified vehicles returning from lease as the EV fleet matures. Organised dealers with specialist EV battery-health certification and charging-integration capabilities will command pricing premiums and attract a growing pool of eco-conscious buyers.

Online transaction channels are outpacing offline sales, with digital-first platforms growing their share of organised vendor transactions at a CAGR of approximately 13.1% through 2034. This channel shift favours asset-light, technology-enabled platforms over traditional showroom-centric models, offering superior unit economics at scale.

Emerging Market Expansion

Regional Australia – particularly the Northern Territory, rural Queensland, and inland Western Australia – remains significantly underserved by organised used car dealers. As digital platform reach extends and logistics networks improve, these markets present high-growth opportunities for platforms willing to invest in local delivery, inspection, and financing infrastructure. Western Australia is identified as the fastest-growing regional market through 2034.

Venture and Strategic Investment Trends

FinTech integration is a primary investment focus, as evidenced by AutoSettle's March 2024 platform launch targeting digital settlement infrastructure. Investors are funding AI-powered pricing tools, vehicle health telemetry platforms, and subscription-based mobility services as the next generation of value-added services in the used car ecosystem. Strategic capital is also flowing into battery health inspection technology as a prerequisite for credible EV pre-owned certification programmes.

Future Market Outlook (2026-2034)

The Australia used car market forecast projects expansion from USD 85.54 Billion in 2025 to USD 217.42 Billion by 2034 at a CAGR of 10.37%. The intermediate milestone of USD 140.08 Billion in 2030 confirms a consistently high-growth trajectory with no projected deceleration inflection point within the forecast period.

Three structural dynamics will define the market through 2034. First, the EV supply transition as the first cohort of Australian electric vehicles completes initial ownership cycles, a significant supply of pre-owned EVs will enter the market from approximately 2027, creating a new premium sub-segment that challenges traditional fuel-type hierarchies. Second, digital platform maturation will drive further consolidation among organised vendors and permanently reduce the information asymmetry that previously supported unorganised channel pricing power. Third, demographic shifts the growing share of younger buyers comfortable with fully digital automotive transactions – will accelerate the share of online sales channels relative to traditional showroom models.

Organised vendors are projected to strengthen their market share beyond 57.2% in 2025, supported by sustained investment in certification standards, EV readiness, and FinTech-enabled financing. The ACT and New South Wales region is expected to retain regional leadership, while Western Australia emerges as the fastest-growing regional market on the back of resource sector growth and digital platform expansion.

Research Methodology

Primary Research

IMARC's primary research for the Australia used car market comprised structured interviews and surveys with industry executives, dealer network operators, platform technology teams, and regulatory stakeholders. Primary data collection included inputs from organised dealership groups across New South Wales, Victoria, Queensland, and Western Australia, supplemented by consumer surveys capturing buyer preferences across fuel type, channel, and price range segments.

Secondary Research

Secondary research drew on publicly available sources including Australian Bureau of Statistics (ABS) vehicle registration data, Federal Chamber of Automotive Industries (FCAI) VFACTS monthly reporting, ASX-listed company filings from CAR Group and related entities, state government EV incentive policy documents, and industry publications from automotive research organisations.

Forecasting Models

IMARC Group deployed both bottom-up and top-down forecasting approaches. The bottom-up model aggregates segment-level demand forecasts across fuel type, vendor type, vehicle category, and region, while the top-down model cross-validates projections against macroeconomic GDP forecasts, household income trends, and automotive penetration benchmarks. Historical CAGR analysis from 2020 to 2025 served as the baseline calibration reference for the 2026-2034 projection model.

Australia Used Car Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Hatchbacks, Sedan, Sports Utility Vehicle, Others |

| Vendor Types Covered | Organized, Unorganized |

| Fuel Types Covered | Gasoline, Diesel, Others |

| Sales Channels Covered | Online, Offline |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | BMW Group, Carma, CARS24, CAR Group Limited, Only Sales Limited, Nine Entertainment Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Used Car Market Report

The Australia used car market was valued at USD 85.54 Billion in 2025 and is projected to reach USD 217.42 Billion by 2034, exhibiting a CAGR of 10.37%.

The market is projected to grow at a CAGR of 10.37% during the forecast period 2026-2034, up from USD 85.54 Billion in 2025 to USD 217.42 Billion by 2034.

Gasoline dominates with a 61.4% market share in 2025, followed by diesel at 28.3% and other fuel types (hybrid, EV, LPG) at a combined 10.3%.

Organised vendors account for 57.2% of the Australia used car market in 2025, driven by CPO programmes, digital platforms, and structured consumer financing.

The Australian Capital Territory and New South Wales lead with a combined 35.7% market share in 2025, followed by Victoria & Tasmania at 24.6%.

Key drivers include rising new car prices, digital platform proliferation, certified pre-owned programme expansion, cost-of-living pressures, and new car supply chain disruptions.

Key players include BMW Group, Carma, CARS24, CAR Group Limited, Only Sales Limited, and Nine Entertainment Company.

The market was valued at USD 52.23 Billion in 2020, growing to USD 85.54 Billion by 2025, reflecting strong historical expansion consistent with the 10.37% forecast CAGR.

The Australia used car market is projected to reach USD 140.08 Billion by 2030, reflecting consistent double-digit compound growth through the mid-point of the forecast period.

Rising EV registrations are expanding the supply of pre-owned electric and hybrid vehicles, creating a fast-growing others segment projected at ~14.5% CAGR.

The report covers segmentation by fuel type (gasoline, diesel, others), vendor type (organised, unorganised), vehicle type, sales channel, and five regional markets across Australia.

The report covers the historical period 2020-2025 and provides detailed forecasts for the period 2026-2034, with key data points at 2025, 2030, and 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)