Auto Parts Manufacturing Market Size, Share, Trends and Forecast by Component Type, Sales Channel, Vehicle Type, and Region, 2026-2034

Global Auto Parts Manufacturing Market Size, Share, Trends & Forecast (2026-2034)

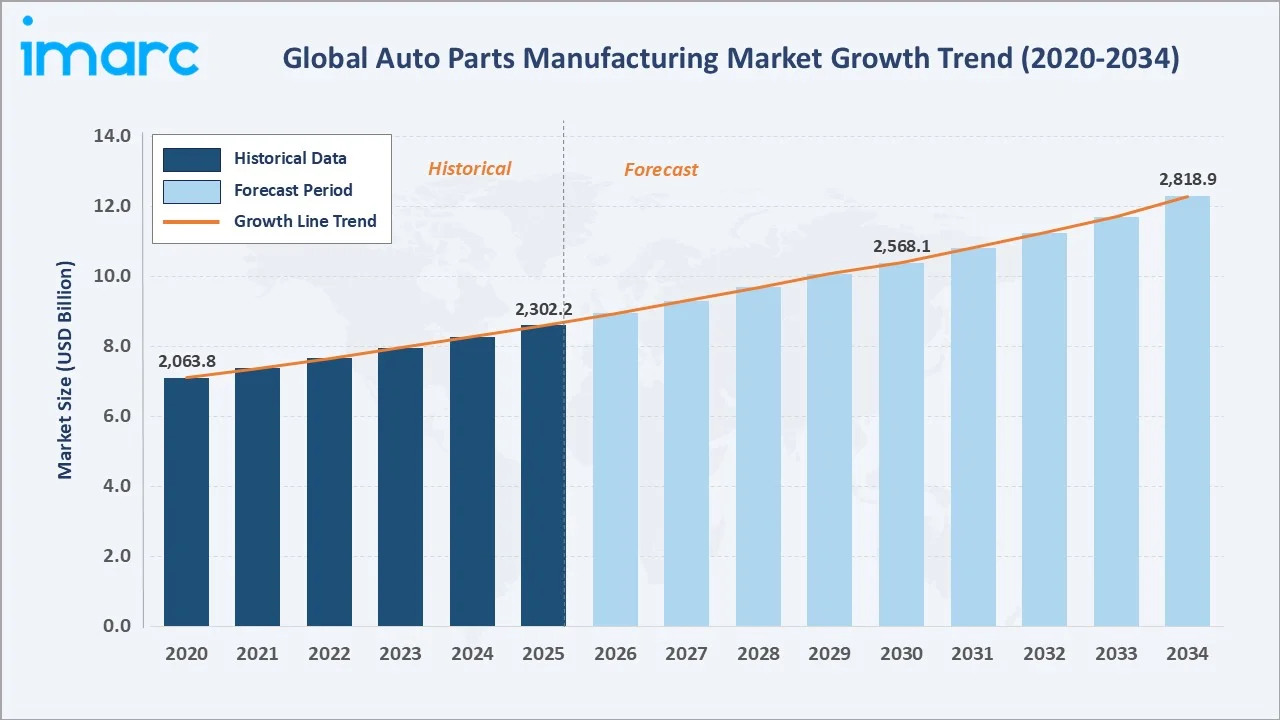

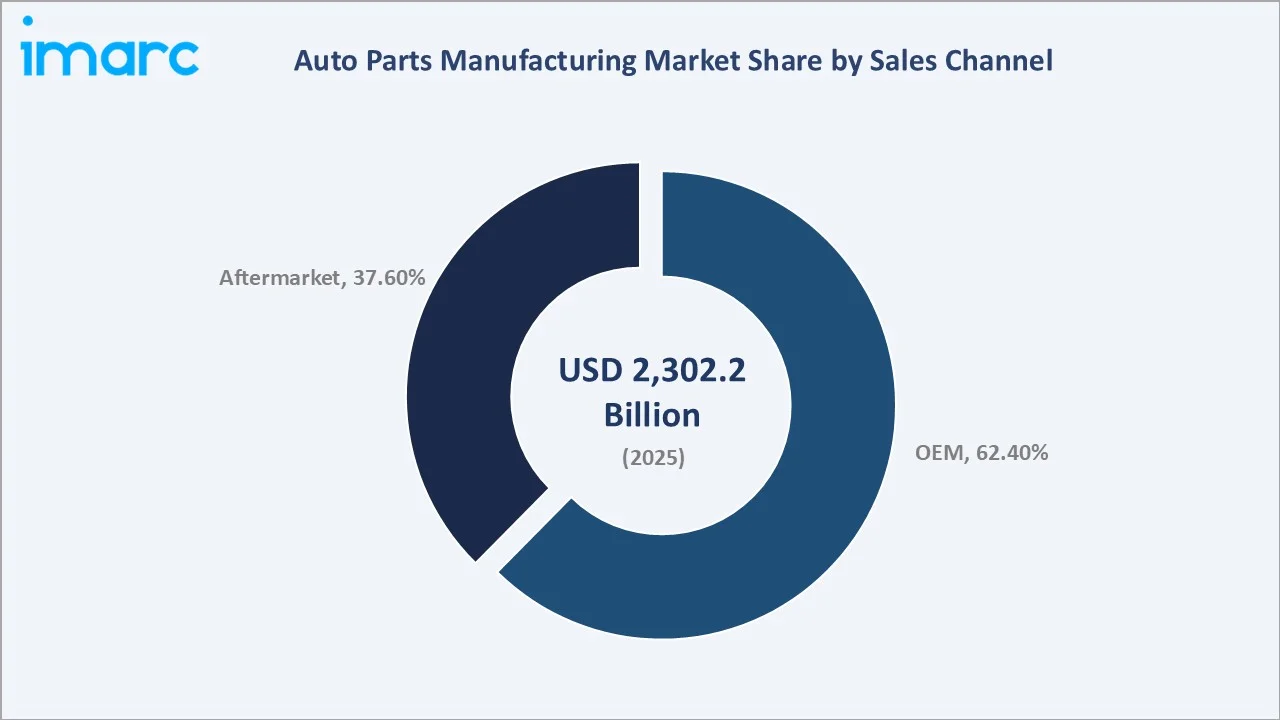

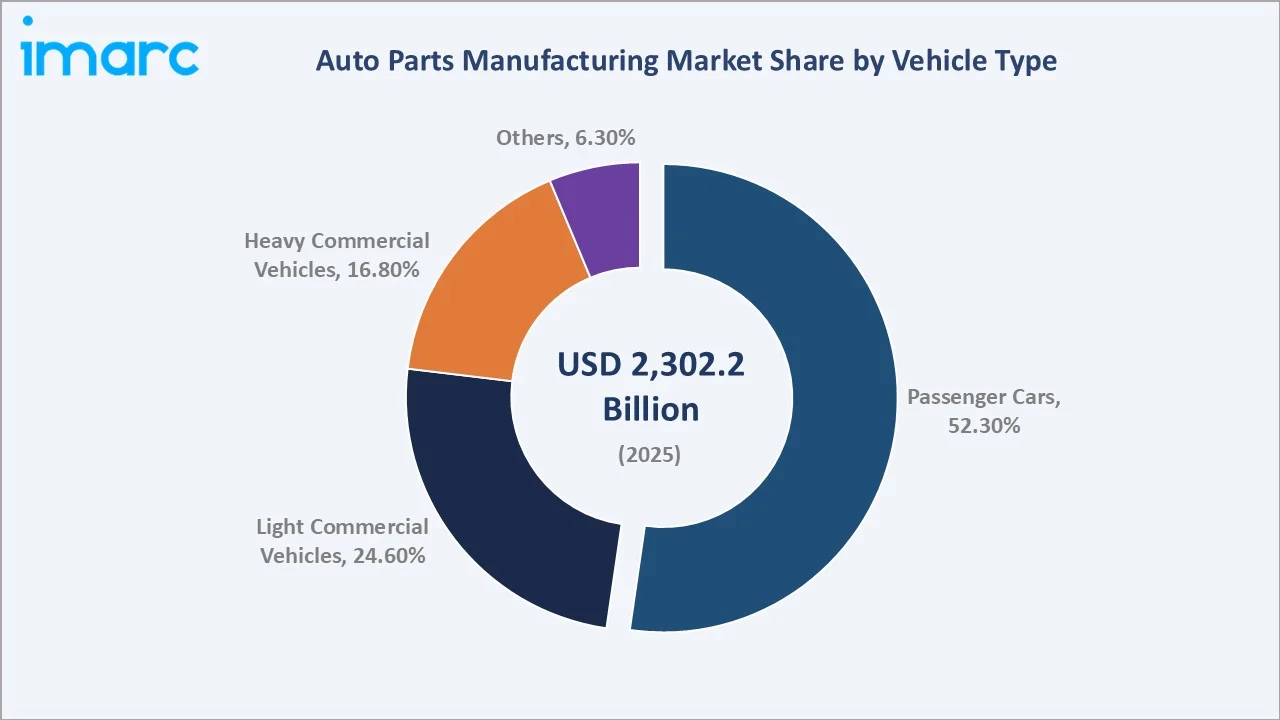

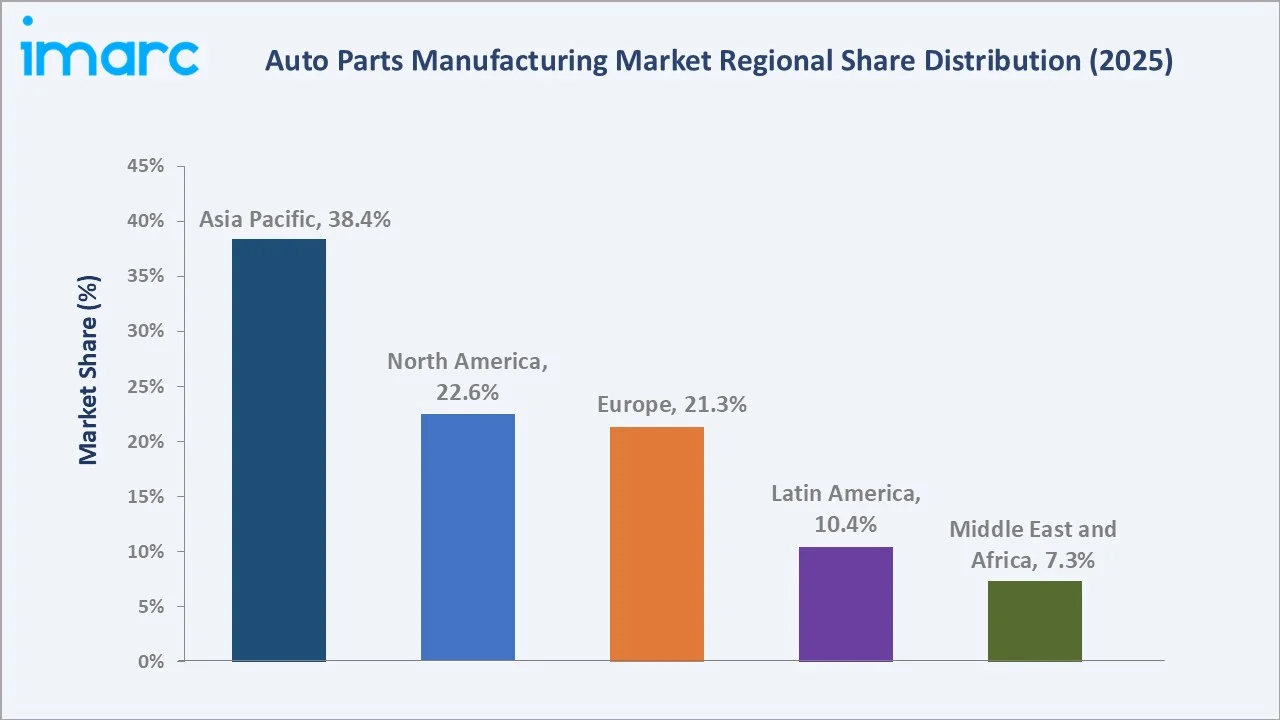

The global auto parts manufacturing market size reached USD 2,302.2 Billion in 2025 and is projected to reach USD 2,818.9 Billion by 2034, exhibiting a CAGR of 2.21% during 2026-2034. Rising global vehicle production, stringent safety and emission standards, increasing penetration of electric vehicles (EVs), and surging demand for lightweight and advanced components are the principal growth drivers. The OEM dominates sales channel at 62.4% in 2025, while Passenger Cars lead the vehicle type segment at 52.3%. Asia Pacific commands the largest regional share at 38.4%, anchored by China, Japan, South Korea, and India. North America (22.6%) and Europe (21.3%) follow closely, underpinned by premium automotive demand and robust Tier-1 supplier networks.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2,302.2 Billion |

|

Forecast Market Size (2034) |

USD 2,818.9 Billion |

|

CAGR (2026-2034) |

2.21% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (38.4% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~3.1%) |

|

Leading Sales Channel |

OEM (62.4%, 2025) |

|

Leading Vehicle Type |

Passenger Cars (52.3%, 2025) |

The chart below illustrates the global auto parts manufacturing market growth trend from 2020 through 2034, contrasting the historical expansion base against a sustained forecast curve powered by EV proliferation, regulatory mandates, and advanced manufacturing technologies.

To get more information on this market, Request Sample

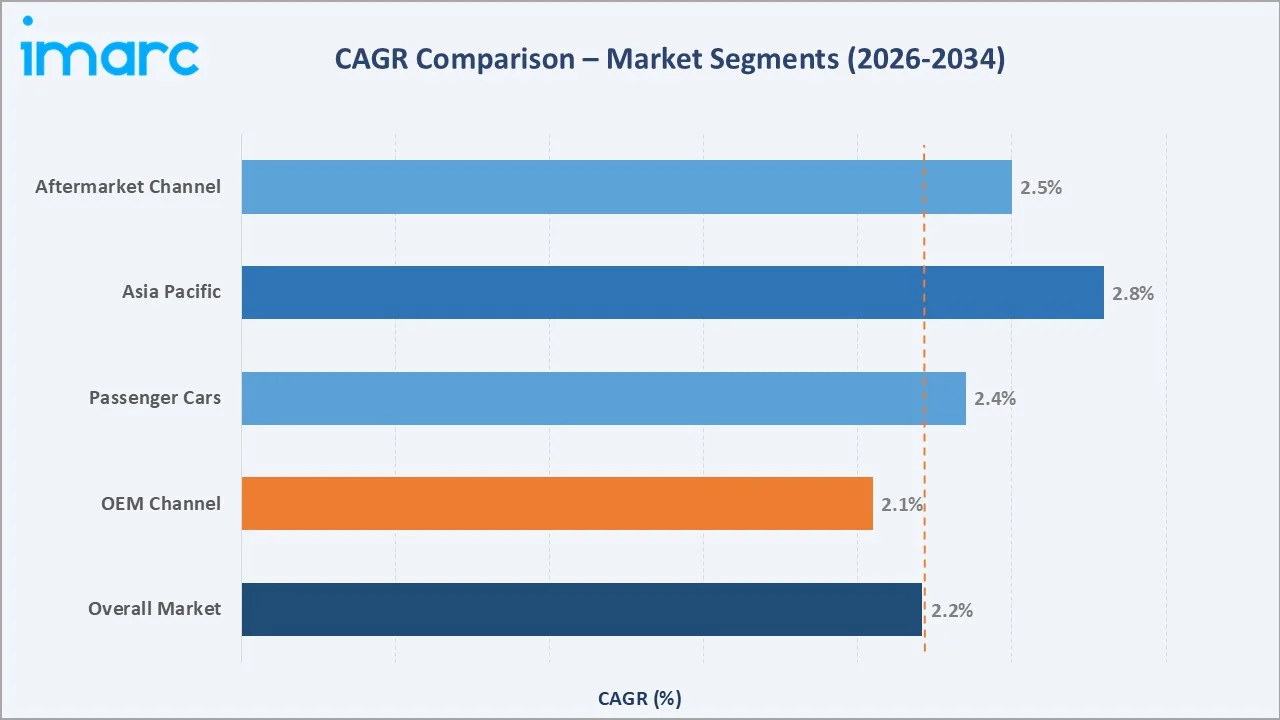

The segment-level CAGR comparison below highlights Passenger Cars and the Asia Pacific region as the two fastest-growing categories within the global auto parts manufacturing industry analysis through 2034.

Executive Summary

The global auto parts manufacturing market is undergoing a structural transformation driven by the convergence of electrification, advanced materials science, and digital manufacturing. Valued at USD 2,302.2 Billion in 2025, the market is forecast to reach USD 2,818.9 Billion by 2034 at a CAGR of 2.21%. Over 92 million vehicles were produced globally in 2024, sustaining robust OEM component demand. At the same time, a rapidly maturing aftermarket segment – representing 37.6% of 2025 revenue – is being energized by the expansion of aging vehicle parc populations globally.

OEM partnerships continue to define the competitive landscape, commanding a 62.4% channel share in 2025. Passenger Cars remain the dominant vehicle type at 52.3%, yet Light Commercial Vehicles (LCVs) at 24.6% are gaining traction amid last-mile logistics and urbanization trends. The electrification wave is reshaping component demand: EV-specific parts – battery enclosures, thermal management systems, and power electronics – are among the fastest-growing product categories. Global EV sales exceeded 17 million units in 2024 (IEA), creating structural demand shifts within the auto parts ecosystem.

Asia Pacific commands 38.4% of global revenue in 2025, led by China's 30+ million annual vehicle production base, Japan's precision Tier-1 supplier ecosystem, and India's rapidly scaling domestic automotive sector. North America at 22.6% and Europe at 21.3% are characterized by premium vehicle penetration, advanced regulatory compliance requirements, and heightened EV infrastructure investments. Latin America (10.4%) and Middle East and Africa (7.3%) represent emerging growth corridors, supported by improving manufacturing infrastructure and rising vehicle ownership rates.

Key Market Insights

|

Insight |

Data Point |

|

Largest Sales Channel Segment |

OEM – 62.4% share (2025) |

|

Largest Vehicle Type Segment |

Passenger Cars – 52.3% share (2025) |

|

Leading Region |

Asia Pacific – 38.4% revenue share (2025) |

|

Second Region |

North America – 22.6% revenue share (2025) |

|

Fastest-Growing Segment |

EV-specific components & Asia Pacific |

|

Top Companies |

Bosch, Denso, Magna International, Continental, ZF Friedrichshafen |

|

Market Opportunity |

EV transition, lightweighting materials, and ADAS integration |

Key Analytical Observations Supporting the Data Above:

- OEM's 62.4% sales channel dominance in 2025reflects the tightly integrated OEM-supplier relationship model, where Tier-1 suppliers deliver just-in-time components directly to vehicle assembly lines, enabling cost efficiencies and quality standardization across high-volume models.

- Passenger Cars at 52.3% remain the largest vehicle type due to persistent global consumer demand for personal mobility. Emerging markets in Asia Pacific and Latin America are recording first-time car-buyer growth rates of 6–8% annually (2023–2025), reinforcing component volumes.

- Asia Pacific's 38.4% share is anchored by China – the world's largest vehicle market with over 30 million units produced annually – alongside Japan's precision engineering expertise and India's rapidly growing domestic OEM base exceeding 4 million vehicles in 2024.

- North America's 22.6% share reflects strong aftermarket revenues driven by the 290+ million registered vehicles (2024) and a high average vehicle age of 12.6 years, creating consistent demand for replacement parts.

- EV-specific auto parts represent the fastest-growing sub-category, with battery management system components, thermal management parts, and power electronics modules projected to grow at 3–4× the overall market CAGR through 2034.

- The aftermarket channel at 37.6% is growing faster than OEM, driven by digitally-enabled parts marketplaces, subscription-based maintenance services, and the expanding global fleet of post-warranty vehicles.

Global Auto Parts Manufacturing Market Overview

Auto parts manufacturing is the industrial process of designing, engineering, and producing components, systems, and sub-assemblies that are integrated into motor vehicles during original assembly (OEM) or sold as replacement and enhancement parts through aftermarket channels. The ecosystem spans a broad range of component categories including engine and powertrain parts, chassis and suspension systems, braking assemblies, electrical and electronic systems, body and exterior components, interior trim, and increasingly, EV-specific modules such as battery packs, power inverters, and e-axle assemblies.

Applications encompass all vehicle categories: passenger cars, LCVs, heavy commercial vehicles (HCVs), buses, two-wheelers, and autonomous mobility platforms. Key macroeconomic enablers include global vehicle production volumes (92+ million units in 2024), rising consumer spending on automotive comfort and connectivity features, tightening emission regulations accelerating electrification, and trade liberalization enabling global supply chain optimization across low-cost manufacturing hubs.

Market Dynamics

Market Drivers

- Rising Global Vehicle Production and Ownership Rates: Global vehicle production reached over 92 million units in 2024, creating direct and proportional demand for auto components. Emerging market vehicle ownership rates – India at 34 vehicles per 1000 people (2024) – signal significant long-term volume upside for parts manufacturers.

- Electric Vehicle Proliferation Reshaping Component Mix: EV sales surpassed 17 million worldwide in 2024, rising by more than 25%. The number of key components will decrease from around 30 in an ICE powertrain to around 9 in a BEV powertrain, fewer traditional mechanical parts but introduces new demand for EV-specific components – battery systems, thermal management modules, and high-voltage wiring harnesses – driving net-positive volume for advanced parts manufacturers.

- ADAS and Vehicle Intelligence Integration: Regulatory mandates requiring advanced driver-assistance systems (ADAS) – including automatic emergency braking (AEB), lane-departure warning, and blind-spot monitoring – across new vehicle models in North America, Europe, and China from 2024 onwards are driving rapid adoption of sensors, cameras, radar units, and control modules.

- Stringent Safety and Emission Standards: Euro 7 emission regulations, US CAFE standards, and China's Phase VI emission norms are compelling OEMs and Tier-1 suppliers to invest heavily in cleaner, lighter, and more efficient powertrain components, directly supporting market revenues.

Market Restraints

- Semiconductor and Raw Material Supply Chain Vulnerabilities: Auto parts manufacturing relies on microprocessors, specialty metals (lithium, cobalt, rare earths), and engineered plastics – all subject to geopolitical supply disruptions. Semiconductor shortages during 2021–2023 significantly disrupted global automotive supply chains, reducing vehicle production by an estimated 7–8 million units and highlighting supply chain vulnerabilities.

- Rapid Technology Obsolescence Cycles: The transition from internal combustion engine (ICE) to EV platforms is rendering existing ICE-specific manufacturing assets – engine blocks, exhaust systems, transmission components – potentially stranded, requiring capital-intensive retooling investments across the Tier-1 supplier base.

- Pricing Pressure from OEM Consolidation: Increasing OEM consolidation and platform-sharing strategies are intensifying cost-reduction pressures on Tier-1 and Tier-2 suppliers, compressing operating margins, which averaged approximately 5–7% for major automotive suppliers in 2024.

Market Opportunities

- EV Component Ecosystem Expansion: The USD 500+ Billion EV battery manufacturing investment pipeline through 2030 creates parallel opportunities for EV-adjacent component suppliers, including battery enclosure manufacturers, thermal interface material producers, and high-voltage connector specialists.

- Lightweighting and Advanced Materials Adoption: Regulatory pressure to reduce vehicle weight for fuel efficiency and EV range optimization is accelerating the adoption of aluminum, carbon fiber composites, and advanced high-strength steels (AHSS)

- Aftermarket Digitalization and E-Commerce Growth: Automotive aftermarket online sales are projected to reach $42.4 billion in 2024, with a 6.7% annual growth rate through 2027, driven by growing e-commerce adoption and aging vehicle fleets. Digital platforms are enabling smaller suppliers to access global aftermarket demand, improving market reach and margin realization.

Market Challenges

- Geopolitical Trade Disruptions and Tariff Risks: US-China trade tensions, European carbon border adjustment mechanisms, and supply chain re-shoring mandates are forcing automotive suppliers to reconfigure established low-cost manufacturing networks, adding cost and complexity.

- Workforce Reskilling Requirements: The shift to EV and software-defined vehicle (SDV) platforms demands new competencies in power electronics, battery systems engineering, and embedded software – skillsets that are scarce in traditional auto parts manufacturing workforce pools globally.

Emerging Market Trends

The auto parts manufacturing industry is experiencing five defining structural trends that will shape the competitive and technological landscape through 2034.

1. EV-Driven Component Portfolio Transformation

The rapid expansion of EV production is fundamentally restructuring the component demand mix. Battery-related components, electric drivetrains, and thermal management systems are emerging as the highest-growth sub-categories. EV sales will increase six-fold by 2030, significantly expanding demand for electrification-specific components.

2. Lightweighting and Advanced Materials Revolution

Automakers are targeting 10–15% weight reductions per vehicle generation to meet fuel efficiency and EV range standards. Multi-material vehicle architectures combining AHSS, aluminum alloys, and carbon fiber-reinforced polymers (CFRPs) are becoming standard in premium and mid-range segments, creating new fabrication and joining technology demands for parts manufacturers.

3. Industry 4.0 and Smart Manufacturing Adoption

Auto parts manufacturers are deploying industrial IoT (IIoT) sensors, digital twins, AI-powered quality inspection, and collaborative robots (cobots) to achieve zero-defect manufacturing targets. Industry 4.0 adoption is enabling up to 50% defect reduction and 10–20% cost savings, while improving productivity and operational efficiency in smart factories creating significant competitive differentiation.

4. Circular Economy and Remanufacturing Growth

Automotive remanufacturing – restoring used parts to OEM-equivalent specification – generated an estimated USD 65 Billion in global revenues in 2024 .European circular economy legislation and OEM sustainability commitments are accelerating remanufacturing adoption for alternators, starters, turbochargers, and increasingly, EV battery packs.

5. Software-Defined Component Integration and OTA Capability

Auto parts are increasingly incorporating embedded software and OTA (over-the-air) update capability. ADAS sensors, infotainment modules, and powertrain control units now require software lifecycle management extending 10–15 years, blurring the traditional boundary between hardware component manufacturing and software services.

Industry Value Chain Analysis

The auto parts manufacturing value chain spans six integrated stages – from raw material procurement to end-consumer delivery. Each stage involves distinct competitive dynamics, capital investment requirements, and margin profiles that shape supplier strategy and OEM partnership models.

|

Stage |

Key Players / Examples |

|

Raw Materials |

ArcelorMittal (steel), Alcoa (aluminum), BASF (specialty polymers), Umicore (battery materials) |

|

Component Manufacturing |

Bosch, Denso, Continental, ZF Friedrichshafen, Aisin, Valeo, Delphi Technologies |

|

Tier-1 / Tier-2 Suppliers |

Magna International, Aptiv, Lear Corporation, Faurecia, Hyundai Mobis, BorgWarner |

|

OEM Assembly |

Toyota, Volkswagen Group, General Motors, Stellantis, Ford, Hyundai-Kia, SAIC, Tata Motors |

|

Distribution & Aftermarket |

LKQ Corporation, Genuine Parts Company, AutoZone, Amazon Automotive, O'Reilly Auto Parts |

|

End Users |

Individual vehicle owners, Fleet operators, Repair shops, Insurance companies |

[Diagram: Auto Parts Manufacturing Industry Value Chain – illustrating material flow, value addition, and key stakeholder interactions across six stages]

Technology Landscape in Auto Parts Manufacturing

Advanced Manufacturing Technologies

Additive manufacturing (3D printing) is transforming prototype development and low-volume specialty part production. Metal 3D printing – using selective laser sintering (SLS) and direct metal laser sintering (DMLS) – enables complex geometries impossible with traditional casting, reducing tooling lead times by 60–80%.

Electric Powertrain Component Technologies

EV-specific parts require precision lithium-ion battery cell manufacturing, power electronics (SiC and GaN-based inverters), and high-efficiency e-motor production technologies. Silicon carbide (SiC) power modules – enabling 10–15% greater EV range versus silicon-based equivalents – are being adopted by Tesla, BYD, Hyundai, and major European OEMs in 2024–2025 model transitions.

Smart Connected Components and ADAS Hardware

Modern automotive components increasingly integrate embedded electronics such as millimeter-wave radar (76–81 GHz), LiDAR sensors, high-resolution cameras, and vehicle-to-everything (V2X) communication modules. These technologies enable advanced driver-assistance systems (ADAS), real-time environment detection, and connected vehicle functionality. Radar operating in the 76–81 GHz band is widely used for collision detection, adaptive cruise control, and autonomous driving features, while LiDAR, cameras, and V2X communication enhance situational awareness and vehicle safety capabilities.

Lightweighting Material Sciences

Advanced high-strength steels (AHSS – Grades 780–1500 MPa), third-generation AHSS, aluminum alloys (5xxx and 7xxx series), and long-fiber thermoplastics are progressively replacing conventional steel in structural and closure components. Carbon fiber-reinforced polymers (CFRPs) are gradually transitioning from motorsport and luxury vehicles toward broader EV applications as manufacturing scale improves and recycled carbon fiber reduces costs. Automotive-grade carbon fiber prices typically range around USD 28–30 per kg, while recycled carbon fiber materials are emerging as lower-cost alternatives, improving feasibility for higher-volume vehicle production.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component Type |

Engine Components |

🔒 |

2025 |

|

Sales Channel |

OEM |

62.4% |

2025 |

|

Vehicle Type |

Passenger Cars |

52.3% |

2025 |

|

Region |

Asia Pacific |

38.4% |

2025 |

By Sales Channel

The OEM holds a dominant 62.4% revenue share in 2025. OEM suppliers operate under long-term supply agreements with vehicle manufacturers, providing just-in-time delivery of engineered components directly to assembly plants. Price transparency, volume certainty, and collaborative product development characterize OEM partnerships. The channel's dominance reflects the continued primacy of new vehicle production – globally exceeding 92 million units in 2024 – as the primary driver of auto parts demand.

To access detailed market analysis, Request Sample

The Aftermarket channel at 37.6% in 2025 is expanding at a faster pace than OEM, driven by the growing global vehicle parc exceeding 1.5 billion registered vehicles (OICA 2024), rising average vehicle age (12.6 years in the US, 11.8 years in Europe), and e-commerce-enabled parts accessibility. Independent aftermarket (IAM) players are gaining share versus OEM dealers as digital platforms commoditize part discovery and procurement.

By Vehicle Type

Passenger Cars command a 52.3% share in 2025, reflecting their position as the dominant global vehicle category. Rising first-time car ownership in India, Southeast Asia, and Latin America – markets recording 5–8% annual vehicle sales growth (2023–2025) – is sustaining passenger car parts demand. Premium and electric passenger car segments are driving higher average component value per vehicle, with the number of key components will decrease from around 30 in an ICE powertrain to around 9 in a BEV powertrain.

Light Commercial Vehicles (LCVs) represent 24.6% of 2025 market revenues. The surge in last-mile delivery logistics – accelerated by Global e-commerce penetration increased from 19.4% of total retail sales in 2023 to 20.1% in 2024 – is driving LCV fleet expansion, particularly in urban delivery vans and pickup trucks. LCV electrification is also gaining momentum in Europe. Electrically-chargeable vans increased their market share from 5.8% to 9.5% year-on-year, indicating rapid adoption of electric LCVs rather than the previously stated 45% growth. This shift is creating demand for EV-specific LCV components including battery systems, power electronics, and thermal management technologies.

Regional Market Insights

To get more information on this market, Request Sample

|

Region |

2025 Share |

Key Growth Drivers |

Major Companies |

|

Asia Pacific |

38.4% |

China/India vehicle production, EV expansion, low-cost manufacturing |

Denso, Aisin, Hyundai Mobis, Bosch Asia |

|

North America |

22.6% |

Aging vehicle parc, aftermarket strength, EV retooling |

Delphi, BorgWarner, Magna, LKQ Corp. |

|

Europe |

21.3% |

Euro 7 compliance, EV mandates, premium vehicle demand |

Bosch, Continental, ZF, Valeo, Faurecia |

|

Latin America |

10.4% |

Rising vehicle ownership, Brazil & Mexico OEM expansion |

Volkswagen (components), GM Brasil, Bosch |

|

Middle East and Africa |

7.3% |

UAE & Saudi infrastructure, rising fleet, import demand |

Abdul Latif Jameel, Inchcape, Petromin |

Asia Pacific dominates with a 38.4% share in 2025. China alone produces over 30 million vehicles annually – more than Europe and North America combined – positioning its Tier-1 supplier network at the epicenter of global OEM component demand. India’s passenger vehicle market exceeded 4 million annual units in 2024, reflecting strong domestic demand and rising localization. Additionally, the government’s Production-Linked Incentive (PLI) scheme has attracted over USD 4.3 billion in automotive and component manufacturing investments, supporting advanced automotive technology and domestic supply chain development.

North America's 22.6% share is underpinned by robust aftermarket revenues. The US vehicle parc exceeding 290 million registered vehicles (2024) and an average age of 12.6 years sustains consistent replacement part demand. The U.S. Inflation Reduction Act’s domestic content requirements for EV batteries are incentivizing onshore battery material and component manufacturing. Since 2022, over USD 120 billion in EV and battery-related investments have been announced, accelerating domestic supply chain development and creating demand for localized component production.

Europe at 21.3% is characterized by rigorous Euro 7 emission compliance requirements driving component R&D investment, a premium vehicle segment demanding higher-specification parts, and ambitious EV fleet electrification targets – 100% zero-emission new car sales mandated by 2035. Latin America (10.4%) is benefiting from Mexico's emergence as a US auto parts manufacturing hub, with parts exports reaching USD 100+ Billion. Middle East and Africa (7.3%) is growing steadily, with Gulf Cooperation Council (GCC) nations driving premium vehicle sales and fleet expansion.

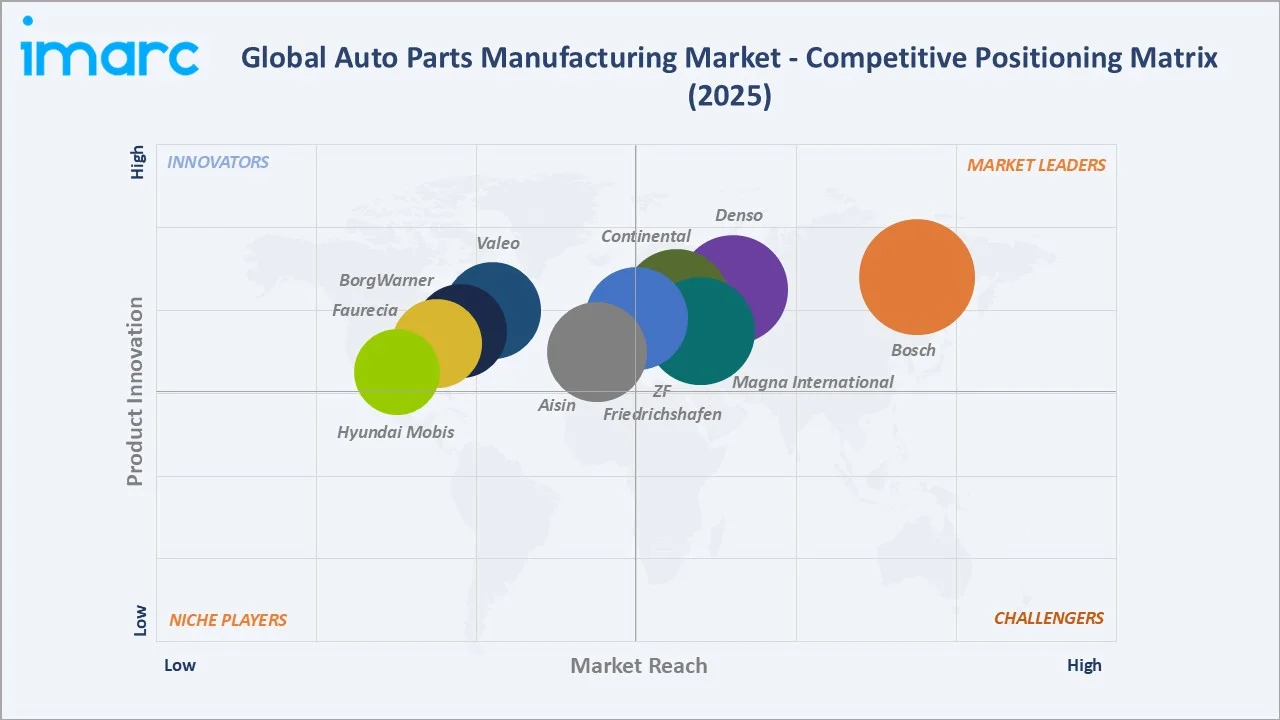

Competitive Landscape

The global auto parts manufacturing market exhibits a moderately consolidated competitive structure with the top 10 players collectively accounting for approximately 35–40% of total revenues in 2025. The remaining share is fragmented across thousands of regional Tier-2 and Tier-3 suppliers. Strategic differentiation is increasingly defined by EV electrification portfolio breadth, software-defined vehicle integration capabilities, and geographic manufacturing footprint.

|

Company Name |

Brand/Division |

Market Position |

Core Strength |

|

Robert Bosch GmbH |

Bosch Automotive |

Leader |

Powertrain, ADAS, electrical systems |

|

Denso Corporation |

Denso |

Leader |

Thermal, electrification, sensing systems |

|

Magna International |

Magna |

Leader |

Body systems, powertrain, seating |

|

Continental AG |

Continental Automotive |

Leader |

Chassis, safety, tires, electronics |

|

ZF Friedrichshafen |

ZF TRW |

Challenger |

Transmission, chassis, safety systems |

|

Aisin Corporation |

Aisin |

Challenger |

Drivetrain, body, brake systems |

|

Valeo SE |

Valeo |

Challenger |

Electrification, thermal, lighting |

|

BorgWarner Inc. |

BorgWarner |

Challenger |

EV propulsion, thermal management |

|

Faurecia (FORVIA) |

FORVIA |

Emerging Leader |

Interiors, clean mobility, seating |

|

Hyundai Mobis |

Mobis |

Emerging Leader |

EV modules, ADAS, chassis |

Key Company Profiles

Robert Bosch GmbH (Bosch Automotive Technology)

- Company Overview: Headquartered in Stuttgart, Germany, Bosch Automotive Technology is the world's largest auto parts supplier with revenues exceeding EUR 56 Billion in 2024 from its Mobility Solutions division. The company serves 150+ OEM customers globally across 120 countries.

- Product Portfolio: Powertrain solutions (electrified and ICE), ADAS and automated driving systems, vehicle electrical systems, body electronics, and workshop services including diagnostics and repair tools.

- Recent Developments: Bosch announced USD 6 Billion in electrification and software investments through 2026. In 2024, the company launched new SiC-based power electronics for EV drivetrains, targeting a 10% range increase.

- Strategic Focus: Electrification leadership, software-defined vehicle platforms, and ADAS silicon content growth.

Denso Corporation

- Company Overview: Japan-based Denso is the second-largest auto supplier globally, generating JPY 7.2 Trillion (approx. USD 48 Billion) in FY2024 revenues. The company operates 200+ manufacturing subsidiaries across 38 countries.

- Product Portfolio: Electrification products, thermal systems, mobility electronics (including sensing and connectivity), and powertrain systems. Denso is Toyota Group's primary Tier-1 component partner.

- Recent Developments: Denso invested USD 3.5 Billion in R&D in FY2024. The company acquired significant stakes in SiC wafer production assets to secure supply chain for EV power modules.

- Strategic Focus: EV ecosystem component integration, energy management systems, and next-generation automated driving sensor platforms.

Magna International Inc.

- Company Overview: Canada-headquartered Magna International operates 342 manufacturing facilities and 103 product development and engineering centers globally, generating USD 42.8 Billion in 2024 revenues.

- Product Portfolio: Body exteriors and structures, power and vision systems, seating systems, complete vehicle assembly, and EV drivetrain systems through its Magna Powertrain business unit.

- Recent Developments: Automotive suppliers such as Magna are expanding electrification-related product portfolios including battery enclosures, e-drive systems, and power electronics. However, 2024 growth remained moderate as automakers adjusted EV production plans and prioritized hybrid and ICE platforms in the near term. The company's eDrive (electric drivetrain) business secured supply agreements with major European and Asian OEMs for 2026–2030 model programs.

- Strategic Focus: Full-vehicle electrification capability, lightweight structural systems, and assembly outsourcing for EV startups.

Continental AG

- Company Overview: German multinational Continental AG generated EUR 39.7 Billion in 2024 revenues, operating through its Automotive (technology & systems) and Tires divisions across 200+ manufacturing plants in 57 countries.

- Product Portfolio: Automotive chassis and safety systems, vehicle networking, user experience (HMI), tires, and ContiTech industrial polymer components.

- Recent Developments: Continental completed a significant restructuring in 2024–2025, separating its Automotive and Tires divisions. The company launched next-generation ADAS domain controllers targeting 2026 model-year vehicle programs.

- Strategic Focus: Software-defined vehicle architecture enablement, tire technology leadership, and ADAS/autonomous driving systems.

ZF Friedrichshafen AG

- Company Overview: ZF Friedrichshafen, headquartered in Friedrichshafen, Germany, generated EUR 43.8 Billion in 2024 revenues. Following the acquisition of WABCO and TRW, ZF operates as a full-spectrum mobility systems supplier.

- Product Portfolio: Transmissions (8HP automated), chassis systems, advanced driver assistance systems (including radar and camera sensors), braking systems, and e-mobility components.

- Recent Developments: ZF’s electrified powertrain technologies represented nearly one-quarter of company revenues in 2024, highlighting the growing contribution of EV-specific components such as e-axles, inverters, and electric driveline systems. with strong demand for its e-axle products.

- Strategic Focus: Electric mobility systems, autonomous driving enablement, and commercial vehicle safety technology.

Market Concentration Analysis

|

Parameter |

Details |

|

Top 5 Market Share (2025) |

~25–28% combined (Bosch ~9.5%, Denso ~7.2%, Magna ~6.8%, Continental ~6.5%, ZF ~6.0%) |

|

Top 10 Market Share (2025) |

~35–40% combined |

|

Fragmentation Level |

Moderate – thousands of Tier-2/Tier-3 regional suppliers hold 60–65% share |

|

Consolidation Trend |

Active M&A activity – 45+ strategic acquisitions in 2023–2024 |

|

Regional Concentration |

Asia Pacific leads with the most fragmented supplier base, Europe most concentrated |

The global auto parts manufacturing market maintains a moderate concentration level. The top 5 players collectively account for approximately 25–28% of 2025 revenues, while the top 10 represent 35–40%. The remaining 60–65% is distributed across an estimated 3,000–5,000 active Tier-2, Tier-3, and regional specialty suppliers globally.

Consolidation is accelerating, driven by three forces: (1) OEM supply base rationalization programs targeting 20–30% reduction in supplier counts; (2) electrification requiring scale investments beyond the financial capacity of smaller suppliers; and (3) private equity rollup strategies targeting fragmented component sub-categories. Major acquisitions in 2023–2024 included ZF's sensor division divestiture, BorgWarner's Delphi Technologies integration maturation, and several strategic stake-takings in Asian EV component startups by European Tier-1 giants.

Investment & Growth Opportunities

Fastest-Growing Segments

- EV Battery and Power Electronics Components: Electrification is driving rapid growth in EV battery and power electronics components, with the lithium-ion battery value chain projected to grow over 30% annually through 2030. Global EV and battery manufacturing investment announcements have approached USD 500 billion, accelerating gigafactory expansion and creating downstream demand for battery enclosures, thermal management, and BMS hardware.

- Advanced Driver-Assistance Systems (ADAS) Hardware: Regulatory mandates expanding ADAS fitment requirements across all new vehicle segments from 2024–2027 in major markets are driving sensor, radar, and camera module.

- Aftermarket E-Commerce and Digital Parts Platforms: Online auto parts retail is growing, significantly outpacing traditional brick-and-mortar aftermarket channels, creating high-return investment opportunities in digital-native parts distribution.

Emerging Geographic Markets

- India: Automotive market projected to reach ~7–8 million units by 2030, with USD 4+ billion PLI-backed investments and rapid EV two- and three-wheeler adoption creating strong supplier entry opportunities..

- Mexico: USMCA-aligned manufacturing hub producing ~4 million vehicles annually and generating USD 100+ billion automotive exports, attracting nearshoring investments from global suppliers..

- Southeast Asia (ASEAN): Thailand, Indonesia, and Vietnam form a multi-million-unit production base, with major EV investments from Toyota, Honda, BYD, and VinFast accelerating regional electrification and supply chain expansion.

Venture and Strategic Investment Trends

- Corporate venture capital from Bosch, Continental, and Denso is actively funding early-stage startups in solid-state battery components, LiDAR manufacturing, and AI-powered quality inspection systems.

- PE-backed consolidation platforms are active in the aftermarket segment, targeting regional parts distributors with USD 50–500 Million revenue profiles for roll-up and digital transformation value creation.

Future Market Outlook (2026-2034)

The global auto parts manufacturing market is projected to expand from USD 2,302.2 Billion in 2025 to USD 2,818.9 Billion by 2034, representing a CAGR of 2.21%. While the headline growth rate appears moderate, the composition of demand will undergo a fundamental transformation driven by three overarching megatrends.

Electrification Transformation (2026–2030): Electrification is becoming the dominant structural shift in the automotive industry. EV adoption is accelerating across major markets, with China already approaching ~50% EV share of new vehicle sales and Europe steadily increasing adoption under tightening emissions regulations. This transition is expected to drive rapid growth in EV-specific components such as batteries, power electronics, and thermal management systems, while demand for traditional ICE-related components gradually declines. Suppliers with strong electrification portfolios are positioned for growth, while ICE-dependent manufacturers face structural transition risks.

Software-Defined Vehicle Revolution (2028–2034): Software-defined vehicle (SDV) architectures are reshaping automotive value creation by enabling over-the-air updates, centralized computing, and feature monetization. The SDV market is projected to grow strongly through 2034, driven by increasing integration of ADAS, connectivity, and digital vehicle platforms. As vehicles become more software-centric, suppliers with embedded electronics and software capabilities are expected to gain premium positioning compared to traditional hardware-focused component manufacturers.

Supply Chain Regionalization (2026–2032): Geopolitical tensions, localization policies, and supply chain resilience priorities are accelerating regionalized automotive manufacturing. OEMs and suppliers are increasingly investing in localized battery production, semiconductor supply chains, and EV component manufacturing across North America, Europe, and Asia. This structural shift is favoring manufacturers with multi-region production capabilities and creating new investment opportunities in battery materials, power electronics, and EV component manufacturing.

Research Methodology

IMARC Group's auto parts manufacturing market analysis employs a comprehensive, multi-layered research framework integrating primary and secondary data collection, quantitative bottom-up market sizing, and scenario-based econometric forecasting. The methodology ensures that all quantitative estimates are grounded in verifiable, current data sources and validated through multi-source triangulation.

|

Research Component |

Methodology Details |

|

Primary Research |

Structured interviews with 200+ industry executives, procurement professionals, and OEM engineers across 12 countries; validated via cross-referencing with secondary data |

|

Secondary Research |

Analysis of regulatory filings, annual reports, trade association data (OICA, ACEA, SEMA, ACMA), patent databases, and peer-reviewed automotive engineering journals |

|

Bottom-Up Market Sizing |

Component-level production volumes × average selling prices across 8 product categories and 5 regions; reconciled against OEM procurement data |

|

Forecasting Model |

Econometric modeling incorporating GDP growth, vehicle production indices, EV penetration curves, raw material price trajectories, and regulatory impact adjustments |

|

Validation |

Data triangulation across 3+ independent sources per data point; statistical confidence intervals applied to CAGR projections |

|

Support |

10–12 weeks post-sale analyst support |

Auto Parts Manufacturing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Component Types Covered |

|

| Sales Channels Covered | OEM, Aftermarket |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, Denso Corporation, Magna International, Continental AG, ZF Friedrichshafen, Aisin Corporation, Valeo SE, BorgWarner Inc., Faurecia (FORVIA), Hyundai Mobis, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the auto parts manufacturing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global auto parts manufacturing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the auto parts manufacturing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Auto Parts Manufacturing Market Report

The market reached USD 2,302.2 Billion in 2025. It is projected to grow at a CAGR of 2.21% to reach USD 2,818.9 Billion by 2034.

The market is expected to grow at a CAGR of 2.21% during the 2026-2034 forecast period, driven by EV adoption and global vehicle production growth.

Asia Pacific leads with a 38.4% revenue share in 2025, primarily driven by China, Japan, South Korea, and India's large-scale vehicle manufacturing ecosystems.

Leading companies include Robert Bosch GmbH, Denso Corporation, Magna International, Continental AG, ZF Friedrichshafen, Aisin, Valeo, BorgWarner, Faurecia, and Hyundai Mobis.

The OEM channel dominates with a 62.4% market share in 2025, underpinned by long-term supply agreements and high-volume new vehicle production.

Passenger Cars account for 52.3% of market revenue in 2025, reflecting global consumer demand for personal mobility and growing first-time vehicle ownership in emerging markets.

Key drivers include rising global vehicle production (92+ million units in 2024), EV proliferation, stringent safety and emission regulations, ADAS adoption, and increasing aftermarket demand.

The aftermarket held 37.6% market share in 2025. It is growing faster than OEM, supported by aging global vehicle fleets, e-commerce platforms, and expanding independent repair networks.

Key challenges include semiconductor supply chain disruptions, raw material price volatility, ICE asset stranding amid EV transition, OEM pricing pressure, and workforce reskilling requirements.

High-return opportunities include EV battery component supply chains, ADAS sensor manufacturing, aftermarket digital platforms, and greenfield production in high-growth markets like India and Mexico.

IMARC employs primary interviews with 200+ industry stakeholders, bottom-up market sizing, secondary research from regulatory and trade sources, and econometric forecasting models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)