Automatic Identification and Data Capture (AIDC) Market Size, Share, Trends and Forecast by Offering, Product Type, Vertical, and Region 2026-2034

Global Automatic Identification and Data Capture (AIDC) Market Size, Share, Trends & Forecast (2026-2034)

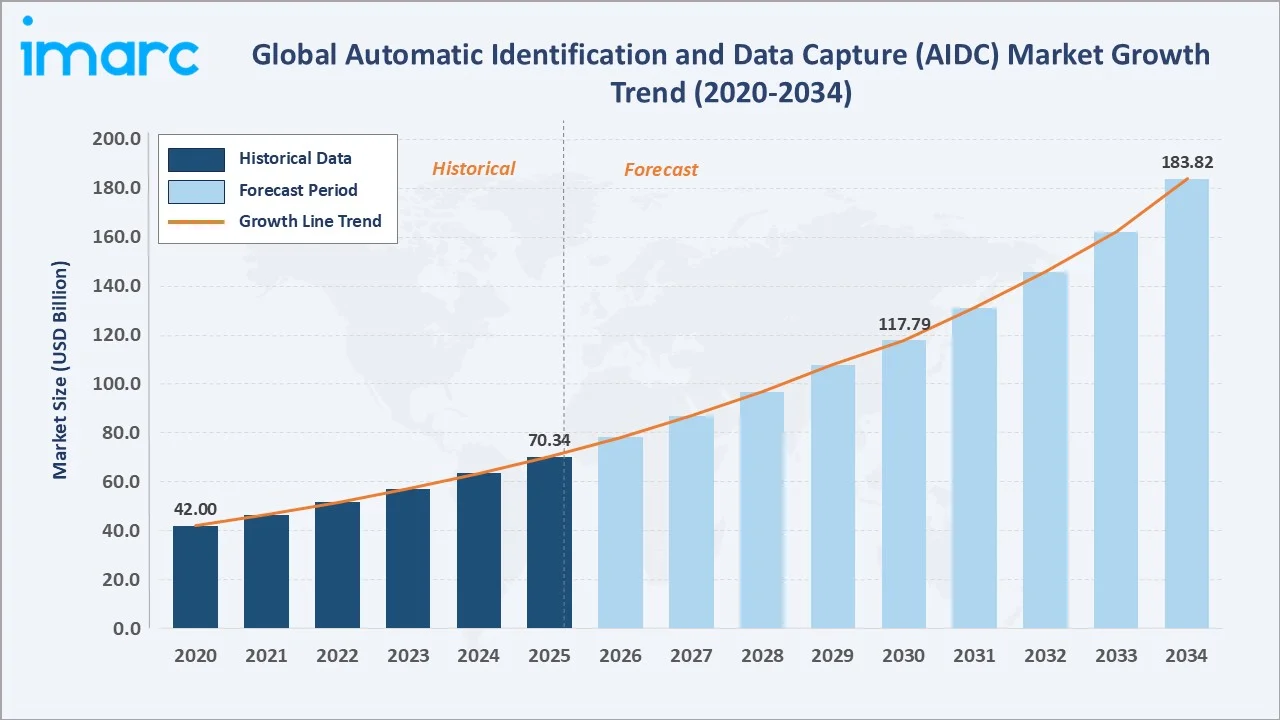

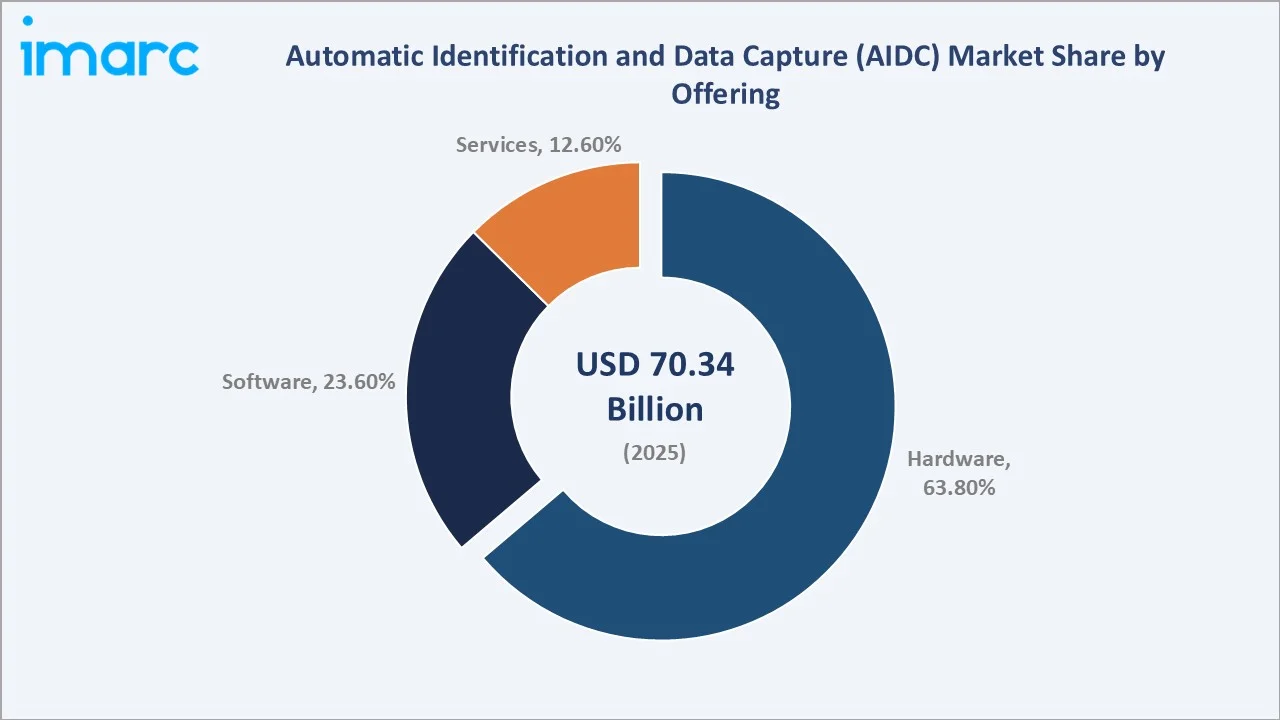

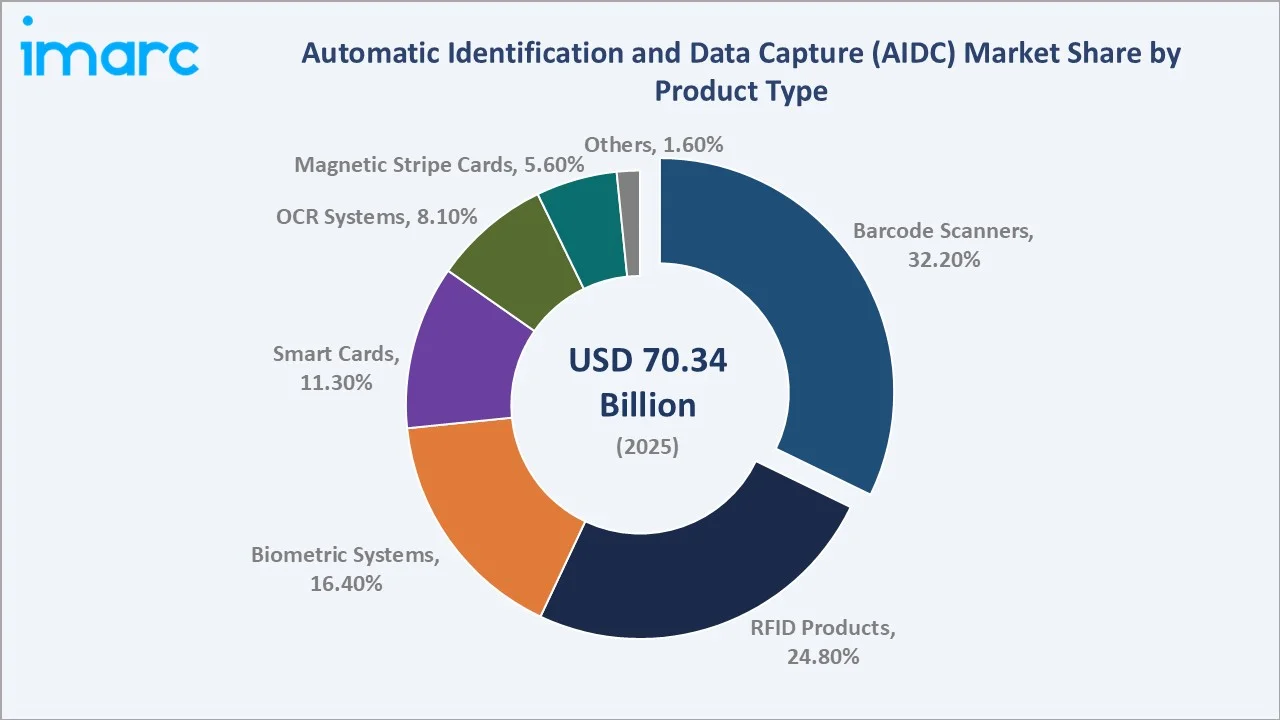

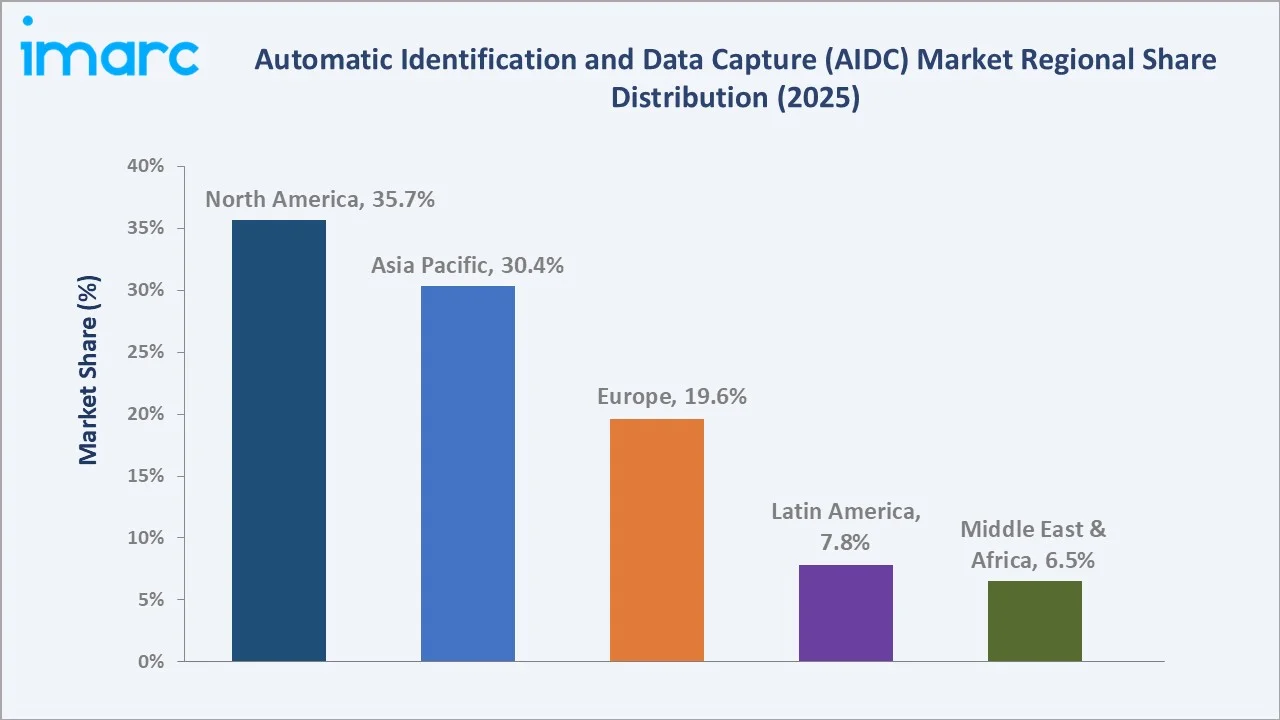

The global Automatic Identification and Data Capture (AIDC) market was valued at USD 70.34 Billion in 2025 and is projected to reach USD 183.82 Billion by 2034, expanding at a CAGR of 10.86% during the forecast period (2026-2034). Growth is propelled by accelerating Industry 4.0 adoption, with manufacturing companies invested $102 Billion in Industry 4.0 in 2021, accounting for 20% of the total manufacturing technology expenditure, e-commerce supply chain automation, healthcare patient safety mandates, and the rapid scaling of biometric identity programs worldwide. Hardware dominates with 63.8% market share (2025), while barcode scanners lead product types at 32.2%. North America holds the largest regional share at 35.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 70.34 Billion |

|

Forecast Market Size (2034) |

USD 183.82 Billion |

|

CAGR (2026-2034) |

10.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (35.7%, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~12.4%, 2026-2034) |

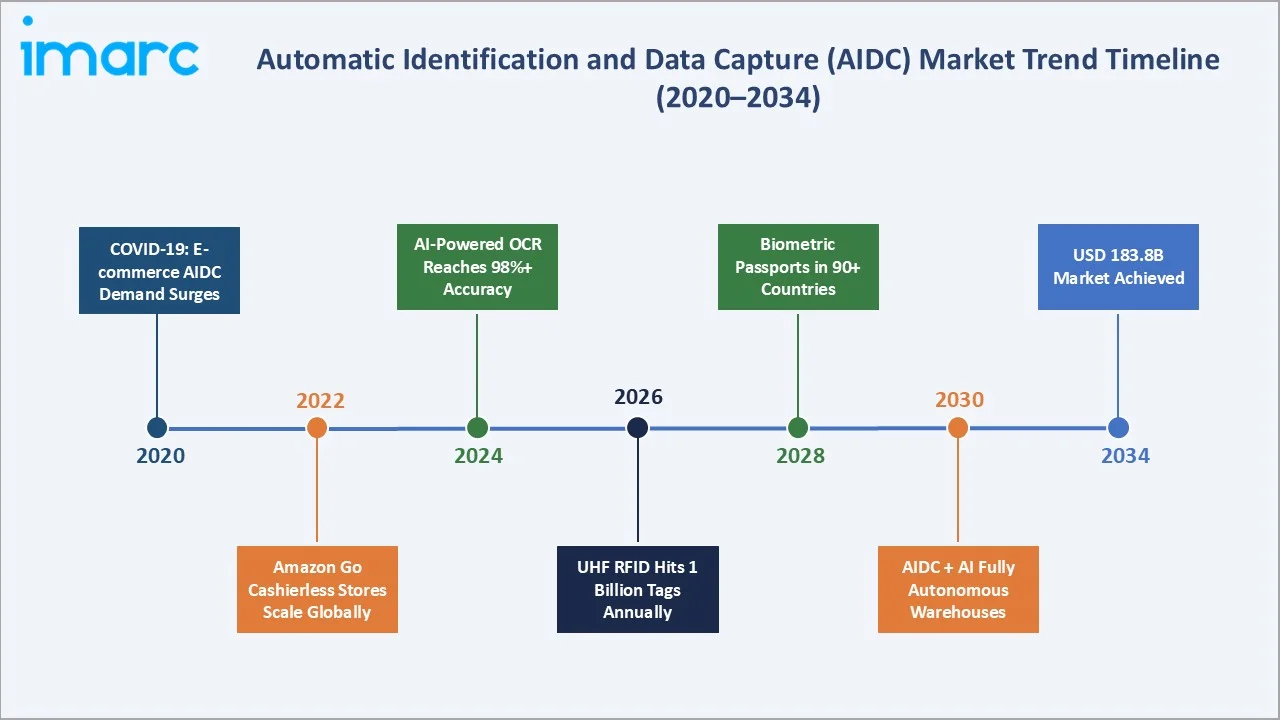

The global Automatic Identification and Data Capture (AIDC) market volume from 2020 through 2034, expanded from USD 42.0 Billion in 2020 to USD 70.34 Billion in 2025, anchored at USD 117.79 Billion in 2030 before reaching USD 183.82 Billion by 2034.

To get more information on this market, Request Sample

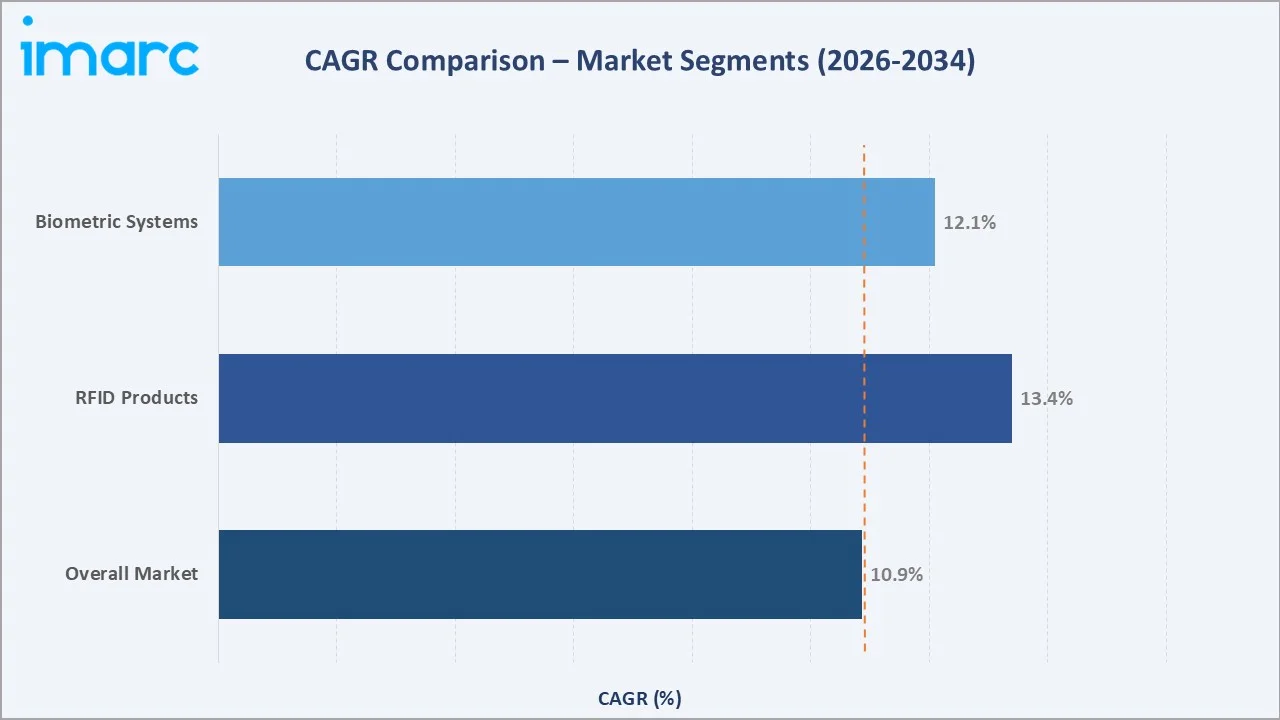

The overall market CAGR is 10.86%, the RFID products segment is growing at a CAGR of 13.4%, and the biometric systems segment is growing at 12.1% CAGR.

Executive Summary

The global AIDC market represents one of the most structurally robust technology segments of the decade. From USD 42.0 Billion in 2020, the market grew to USD 70.34 Billion by 2025, recording consistent double-digit CAGR driven by digital transformation across all major end-use industries. The market’s growth trajectory to USD 183.82 Billion by 2034 reflects the convergence of four powerful demand vectors, supply chain intelligence, contactless identity verification, healthcare safety compliance, and the mass deployment of IoT-connected AIDC devices across smart manufacturing environments.

Hardware retains dominance at 63.8% market share (2025), encompassing barcode scanners, RFID readers and tags, biometric terminals, and smart card readers that form the physical interface of every AIDC deployment. Software at 23.6% is the fastest-growing offering segment at approximately 14.2% CAGR through 2034, as AI-powered analytics, cloud-based data management, and API-driven integration platforms command premium pricing and create high-retention recurring revenue streams for vendors. Services at 12.6% represents the systems integration and managed services layer enabling enterprise-scale AIDC deployments across complex multi-site operations.

North America leads with a 35.7% market share (2025), anchored by the U.S. retail and logistics sector’s RFID mandates, FDA Unique Device Identification (UDI) healthcare requirements, and the TSA’s biometric airport screening expansion. Asia Pacific at 30.4% is the fastest-growing region at approximately 12.4% CAGR, driven by China’s Industry 4.0 manufacturing digitization, India’s 1.4 Billion-registration Aadhaar biometric program with over 80 million transactions per day, and Southeast Asia’s exploding e-commerce logistics infrastructure investment through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Offering Segment |

Hardware – 63.8% revenue share (2025) |

|

Largest Product Type |

Barcode Scanners – 32.2% revenue share (2025) |

|

Leading Region |

North America – 35.7% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~12.4%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Hardware dominates at 63.8% (2025): The physical device layer remains the primary AIDC spend category. Enterprise mobile computers, industrial barcode scanners, and RFID infrastructure for distribution centers driving the hardware segment growth.

- Barcode Scanners lead at 32.2% (2025): GS1 barcodes are trusted by over 2 million companies globally and are scanned more than 10 Billion times daily, making barcoding the world’s most widely deployed AIDC technology.

- North America leads at 35.7% (2025): Major demand catalysts include the FDA’s mandatory UDI compliance covering medical devices, DHS’s biometric entry/exit program processing international travelers, and the U.S. Department of Defense’s UID marking mandate for all defence assets.

Global AIDC Market Overview

Automatic Identification and Data Capture (AIDC) encompasses the technologies and systems used to automatically identify objects, collect data about them, and enter that data directly into computer systems with minimal human intervention. The AIDC ecosystem spans barcode scanning, Radio Frequency Identification (RFID), biometric recognition, smart cards, Optical Character Recognition (OCR), and magnetic stripe card reading, each addressing distinct identification and data capture requirements across industrial, commercial, and government applications.

Applications extend across every major industry vertical: retail inventory management, healthcare patient safety, supply chain and logistics asset tracking, border control and passport verification, banking payment card processing, manufacturing quality control, and government national identity programs. Macroeconomic drivers include global e-commerce penetration, post-pandemic supply chain resilience investment, and government digital identity infrastructure commitments.

Market Dynamics

To evaluate market opportunities, Request Sample

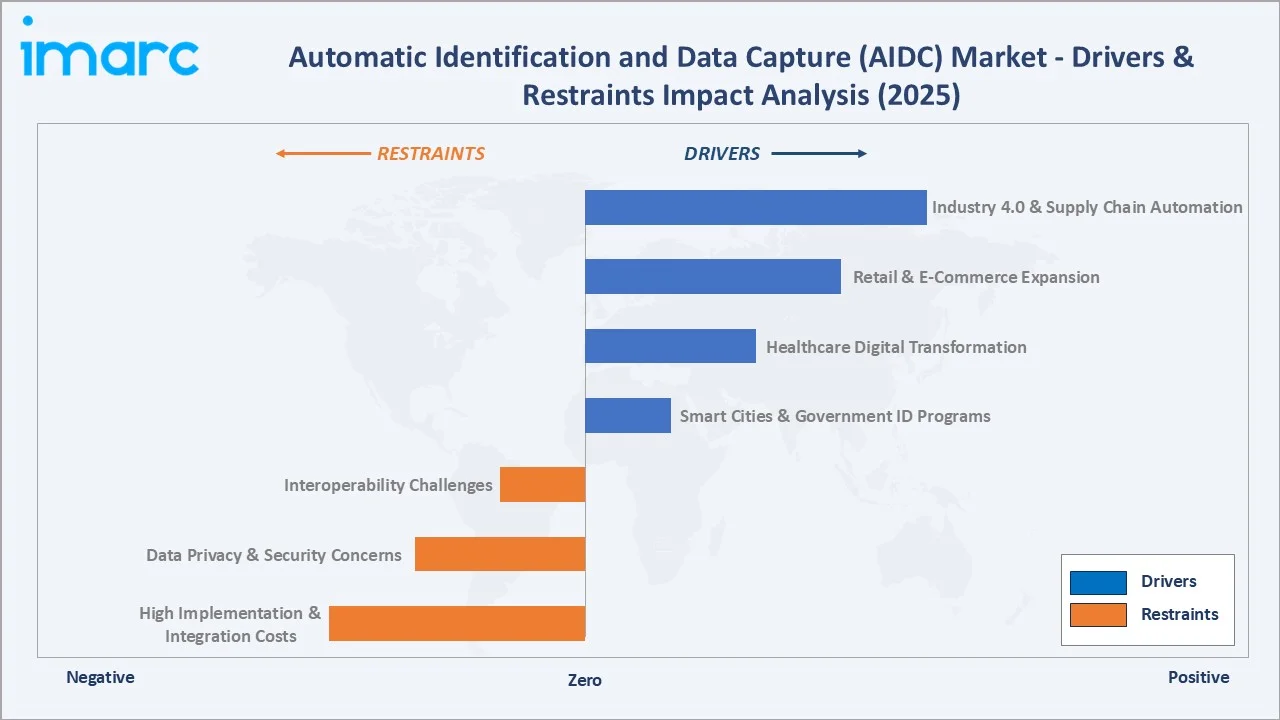

Market Drivers

- Industry 4.0 and Supply Chain Automation: Global supply chain digitization investments, with AIDC technologies representing the physical sensing layer of smart warehouse and factory floor automation. Amazon operates more than 750,000+ mobile robots.

- Retail and E-Commerce Expansion: Each e-commerce shipment requires 3–6 AIDC scan events from manufacturer to consumer doorstep.

- Healthcare Digital Transformation and Compliance: The FDA’s UDI regulation mandates machine-readable identification on medical devices sold in the U.S. The global healthcare AIDC market growth is driven by mandatory patient safety regulations in the U.S., EU MDR, Japan PMDA, and emerging market health ministry digitization programs.

- Smart City and Government Identity Programs: India’s 1.4 Billion-registration Aadhaar biometric program with over 80 million transactions per day. These government programs collectively represent the world’s largest single AIDC procurement category by government contract value.

Market Restraints

- High Implementation and Total Cost of Ownership: The high capital intensity limits adoption among mid-market retailers and manufacturers operating with limited IT budgets, despite the substantial ROI available from inventory accuracy improvements and reduced shrinkage.

- Data Privacy and Biometric Security Concerns: GDPR’s classification of biometric data as a special category requiring explicit consent has slowed enterprise biometric deployment in Europe, creating legal risk aversion among U.S. enterprise deployers.

- Interoperability and Standards Fragmentation: The AIDC market contains multiple competing standards, EPC Gen2 versus ISO 18000-63 for RFID, EMV versus NFC versus proprietary smart card protocols, and competing biometric file format standards, creating system integration complexity.

Market Opportunities

- AI-Powered OCR and Machine Vision Replacing Manual Processes: From factory floor to front door, Cognex barcode readers achieve over 99% read rates on 1D and 2D codes.

- Biometric Payment and Financial Services Expansion: Visa and Mastercard are piloting biometric payment cards, embedding fingerprint sensors directly in payment cards, with NXP Semiconductors and Synaptics providing the fingerprint sensor ICs.

Market Challenges

- Cybersecurity Vulnerabilities in RFID and Contactless Systems: RFID eavesdropping, relay attacks on contactless payment cards, and RFID cloning of access control credentials are documented attack vectors.

- Technology Obsolescence Risk in Long-Cycle Deployments: AIDC hardware deployed in manufacturing and logistics environments has replacement cycles. Technology transitions, such as the ongoing shift from 1D to 2D barcode reading, or from high-frequency (HF) to ultra-high-frequency (UHF) RFID, create stranded asset risk for operators mid-cycle.

- Counterfeit and Non-Standard AIDC Devices: The AIDC hardware market faces significant counterfeit product pressure, particularly in barcode scanners and RFID readers sold through grey market channels in Asia and Latin America.

Emerging Market Trends

1. RAIN RFID and Item-Level Visibility at Scale

RAIN Alliance, supporting the development and adoption of standards-based Ultra High Frequency (UHF) Radio Frequency Identification (RFID), announced that 52.8 Billion RAIN tag chips / ICs were shipped globally in 2024.

2. Multimodal Biometrics and Frictionless Authentication

Next-generation biometric systems are combining facial recognition, fingerprint, and iris scanning into single unified platforms for border control and high-security access. The Transportation Security Administration (TSA) screens around 2 million passengers per day.

3. AI-Enhanced Machine Vision and Code Reading

AI-powered OCR is enabling postal automation, pharmaceutical track-and-trace, and document digitization at unprecedented accuracy and speed.

4. Converged AIDC Platforms Replacing Point Solutions

Enterprise customers are consolidating from multiple single-purpose AIDC point solutions to converged unified platforms. Converged vendors achieve higher customer retention rates than point-solution vendors, creating strong competitive moats through platform lock-in.

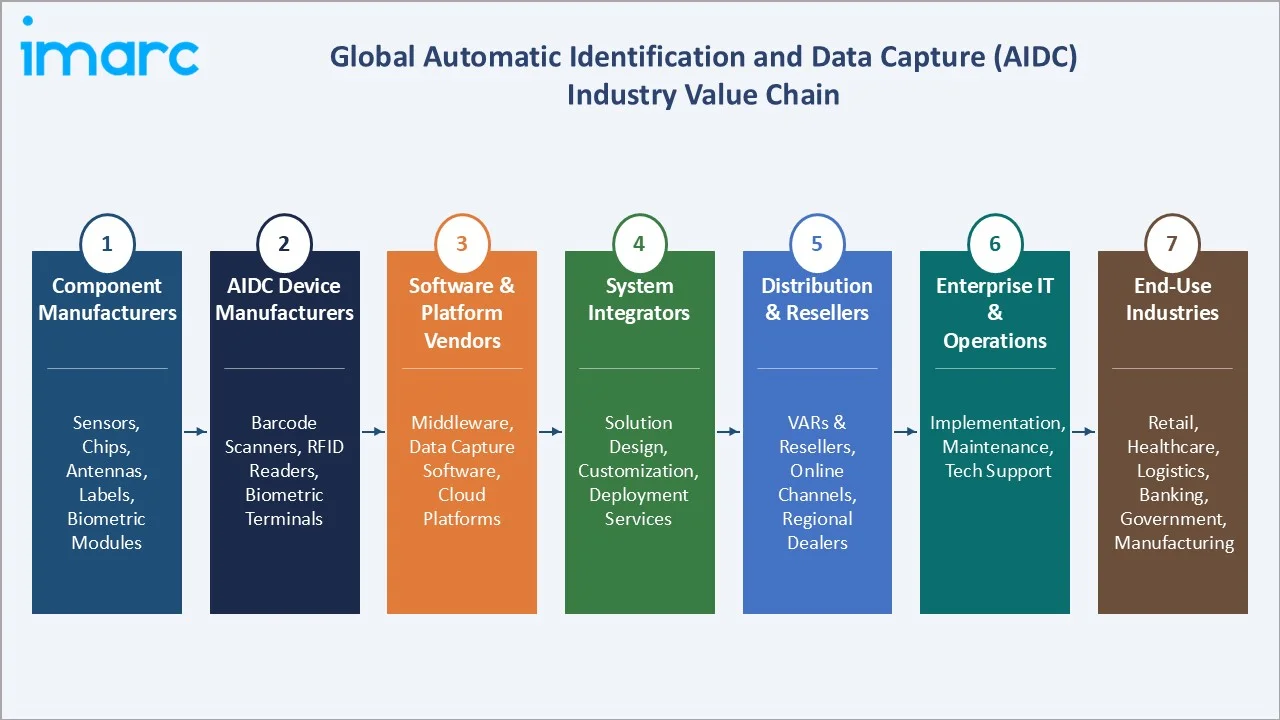

Industry Value Chain Analysis

The AIDC industry value chain extends from semiconductor raw materials through physical device manufacturing, software development, and system integration to final enterprise end-user deployment. The chain is highly specialized at each stage, with distinct competitive dynamics and margin profiles.

|

Stage |

Key Participants |

|

Raw Materials & Semiconductors |

Chips, sensors, antennas, optical components |

|

Component Manufacturing |

RFID ICs, microcontrollers, biometric sensors |

|

Device & System Manufacturing |

Scanners, printers, readers |

|

Software & Platform Development |

Middleware, analytics |

|

System Integration & Deployment |

End-to-end AIDC solution deployment |

|

Distribution & Channel Partners |

Specialist AIDC distributors and value-added resellers (VARs) |

|

End-Use Verticals |

Retail, healthcare, manufacturing, T&L, banking & finance, government, defence |

The hardware manufacturing layer captures the highest absolute revenue in the AIDC chain, but software and platform layers are growing fastest and generating the highest gross margins. Systems integrators and VARs collectively add value in total services to AIDC deployments globally.

Technology Landscape in the AIDC Industry

Advanced Barcode and 2D Imaging Technology

Modern area-imaging barcode scanners, using CMOS image sensors rather than traditional laser diodes, now achieve higher read rates per second for industrial applications. The industry set the deadline of Sunrise 2027 for transitioning to 2D barcodes at point-of-sale (POS) and point-of-care (POC). By the end of 2027, retailers must ensure their POS systems can read both traditional and 2D barcodes. The shift is already underway, with the new technology being tested in 48 countries, covering 88% of the global GDP.

Ultra-High-Frequency RFID and Passive IoT

RAIN RFID reader infrastructure, embedded in store ceilings, dock doors, and conveyor systems, is creating permanent AIDC infrastructure analogous to Wi-Fi networks in physical retail and logistics environments.

Biometric Sensor Miniaturization and Edge AI

Next-generation biometric systems are integrating multi-modal sensing (fingerprint + face + iris) into compact edge AI modules capable of authentication without cloud connectivity. NEC’s AI-powered facial recognition achieves over 99.9% accuracy against the world’s most challenging datasets, including masked-face recognition.

Smart Card Convergence and Multi-Application Security

Modern smart cards based on NXP’s SmartMX3 platform integrate PKI cryptographic processing, contactless communication, and application memory in a single card chip capable of simultaneously hosting transit, access control, payment, and government ID applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Offering |

Hardware |

63.8% |

2025 |

|

Product Type |

Barcode Scanners |

32.2% |

2025 |

|

Vertical |

Manufacturing |

🔒 |

2025 |

|

Region |

North America |

35.7% |

2025 |

By Offering

Hardware dominates with 63.8% market share (2025). This segment encompasses barcode scanners, mobile computers, RFID readers and antennas, biometric terminals, smart card readers, and label printers. The hardware segment is growing at approximately 8.5% CAGR through 2034, driven by device refresh cycles in logistics, continued retail RFID infrastructure build-out, and biometric terminal deployments in government and banking.

To access detailed market analysis, Request Sample

Software at 23.6% (2025) is the fastest-growing offering at ~14.2% CAGR through 2034. Cloud-based AIDC management platforms, AI-powered analytics, and API-first middleware are commanding premium SaaS pricing. Services at 12.6% represent systems integration, deployment, training, and managed services.

By Product Type

Barcode scanners lead with 32.2% share (2025). GS1 barcodes are trusted by over 2 million companies globally and are scanned more than 10 Billion times daily. The segment is being transformed by the shift from 1D laser to 2D area-imaging scanners, which offer omni-directional reading, image capture for proof-of-delivery, and QR/2D code compatibility in a single device platform.

RFID products at 24.8% and biometric systems at 16.4% represent the two fastest-growing product categories at ~14.2% and ~15.8% CAGR, respectively through 2034. Smart cards at 11.3% are driven by government national ID programs and EMV payment migration. OCR systems at 8.1% are being transformed by AI deep learning, achieving 99.9%+ text recognition accuracy in complex document processing environments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

35.7% |

Amazon/Walmart supply chain automation, U.S. healthcare barcode mandates |

|

Asia Pacific |

30.4% |

China manufacturing automation (Industry 4.0), India Aadhaar biometric ID (1.4B registrations) |

|

Europe |

19.6% |

EU Digital Product Passport mandate 2026; Germany Industrie 4.0 traceability |

|

Latin America |

7.8% |

Brazil NF-e fiscal barcode mandate; Mexico IMMEX supply chain tracking; growing supermarket chain scan-verify adoption |

|

Middle East & Africa |

6.5% |

Saudi Arabia Vision 2030 smart logistics; UAE Emirates ID biometric system; South Africa retail RFID adoption; GCC government e-ID projects |

North America’s 35.7% market dominance (2025) is structurally reinforced by the U.S.’s position as the world’s largest retail, logistics, and healthcare AIDC market. The Amazon company’s USD 100+ Billion spending on AWS infrastructure is the single largest driver of global AIDC demand.

Asia Pacific’s 30.4% share (2025) is forecast to grow to approximately 35–36% by 2034 at ~12.4% CAGR, driven by China built over 30,000 smart factories as part of a nationwide push to accelerate industrial digitalization and intelligent upgrading, according to the Ministry of Industry and Information Technology (MIIT) and India’s digital infrastructure build-out. Europe’s 19.6% share (2025) is being transformed by regulatory mandates.

Competitive Landscape

The global AIDC market is moderately concentrated at the hardware platform tier, with Zebra Technologies and Honeywell International collectively accounting for approximately 28–32% of global AIDC hardware revenue.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Zebra Technologies Corp. |

Zebra DataCapture DNA, Zebra General Purpose Scanners, Zebra Healthcare Scanners, Specialty Scanners |

Market Leader |

RFID, and analytics, AI-powered tracking platform |

|

Honeywell International Inc. |

General purpose scanners, Industrial-grade scanners, Healthcare Scanners, Presentation Scanners, Wearable scanners, Fixed mount scanners |

Market Leader |

Broadest portfolio of industrial barcode scanners and mobile computers, leading position in U.S. healthcare and warehouse automation |

|

NXP Semiconductors |

UCODE RAIN RFID, HITAG Readers and Transponders, MIFARE |

Specialist Leader |

World’s #1 RFID chip manufacturer, leading contactless smart card IC MIFARE technology, dominant in transit and payments |

|

Cognex Corporation |

All-purpose barcode reader powered by AI, High-resolution, AI-powered barcode reader, Rugged handheld scanner for industrial environments, Compact fixed-mount barcode reader, Compact barcode readers for high-speed manufacturing, High-resolution barcode reader, Fixed-mount barcode reader |

Market Leader |

AI-powered vision systems for factory automation |

|

Datalogic S.p.A. |

RFID Readers, OEM Barcode Readers, Fixed Retail Scanners, Handheld Scanners, Sensors, Mobile Computers |

Strong Challenger |

European leader in barcode readers for retail and T&L, strong Italian and EU market presence |

|

NEC Corporation |

Bio-IDiom, NeoFace |

Established |

World’s #1 facial recognition biometric accuracy, government ID and border control systems |

|

Sick AG |

Image-based Code Reading (1D, 2D) (Lector 620, Lector 650), Linear / 1D Code Reading (CLV600 series bar code scanners), RFID (ultra-high frequency RFU620/630, and the high frequency RFH620/630), Hand-held Scanners |

Established |

CLV barcode readers for intralogistics; 3D vision-based identification |

|

TSC Auto ID Technology Co. Ltd. |

Mobile Printers, Desktop Printers, Industrial Printers, Enterprise Printers, RFID Printers, Barcode Inspection Printers |

Growth Challenger |

Cost-competitive industrial and desktop label printers, OEM manufacturing for global brands |

The broader AIDC ecosystem, including RFID semiconductor, biometric, and smart card subsegments, is served by a diverse set of specialist vendors. NXP Semiconductors dominates RFID and smart card ICs, and NEC leads government biometric identity systems, each controlling distinct technology segments with different competitive dynamics.

Key Company Profiles

Zebra Technologies Corp.

Zebra Technologies is the undisputed global leader in enterprise-grade AIDC hardware and software.

- Product Portfolio: Intelligent Document Capture, Zebra DataCapture DNA, Zebra General Purpose Scanners, Zebra Healthcare Scanners, Specialty Scanners.

- Recent Developments: In March 2026, Zebra Technologies Corporation launched Orchestrated Care, a forward-thinking framework aimed at helping healthcare organizations enhance visibility, empower teams, and streamline operations. This approach leverages Zebra's comprehensive healthcare technology portfolio, which includes mobile computers, scanners, printers, touchscreen displays, RFID, real-time location solutions, and software, all backed by a strong network of implementation and technology partners.

- Strategic Focus: AI-powered enterprise visibility platform convergence; 5G and private wireless AIDC infrastructure; machine vision integration through Matrox; healthcare AIDC expansion; software and services revenue as percentage of total revenue growth target.

Honeywell International Inc.

Honeywell is one of the largest global AIDC vendors by revenue, with its Productivity Solutions and Services (PSS) division. The division serves retail, T&L, healthcare, and manufacturing with a comprehensive portfolio spanning barcode scanners, mobile computers.

- Product Portfolio: General purpose scanners, Industrial-grade scanners, Healthcare Scanners, Presentation Scanners, Wearable scanners, Fixed mount scanners.

- Recent Developments: In January 2026, Honeywell launched its new connected workforce solution, Honeywell Performance+ for Guided Work.

- Strategic Focus: Connected worker and industrial IoT platform as primary growth vector; healthcare AIDC compliance solutions for FDA UDI and medication safety; Forge software subscription revenue expansion; supply chain sustainability tracking through AIDC data layer.

NXP Semiconductors

NXP Semiconductors is the world’s number one RFID and contactless smart card IC manufacturer, with AIDC-related products.

- Product Portfolio: UCODE RAIN RFID, HITAG Readers and Transponders, MIFARE.

- Recent Developments: In November 2024, NXP Semiconductors unveiled the MIFARE DUOX, the first NFC contactless IC in its category to integrate both asymmetric and symmetric cryptography in a single solution. This innovation streamlines security for NFC applications, including electric vehicle (EV) charging authentication, secure car access, and other access management systems, by simplifying key management and distribution.

- Strategic Focus: UHF RFID cost reduction to enable mass consumer goods serialization below USD 0.03/tag; secure element expansion for automotive V2X and IoT authentication; biometric smart card platform for national ID and payment convergence; post-quantum cryptography integration.

Cognex Corporation

Cognex is the global market leader in machine vision and industrial barcode reading. The company’s AI-powered vision systems and fixed-mount barcode readers are deployed in manufacturing facilities across automotive, electronics, pharmaceutical, and food & beverage industries.

- Product Portfolio: All-purpose barcode reader powered by AI, High-resolution, AI-powered barcode reader, Rugged handheld scanner for industrial environments, Compact fixed-mount barcode reader, Compact barcode readers for high-speed manufacturing, High-resolution barcode reader, Fixed-mount barcode reader.

- Recent Developments: In March 2024, Cognex Corporation introduced the 380 Modular Vision Tunnel, a new addition to the Modular Vision Tunnel portfolio, featuring the powerful DataMan 380 barcode reader.

- Strategic Focus: AI-powered vision as the primary differentiation against traditional machine vision competitors; EV battery manufacturing quality control as a priority vertical; logistics sortation barcode reading for FedEx/UPS warehouse automation; software and services revenue growth as percentage of mix.

Market Concentration Analysis

The global AIDC market exhibits a bifurcated concentration structure. At the broadest enterprise hardware tier, Zebra Technologies and Honeywell International collectively represent approximately 28–32% of global AIDC hardware revenue, a moderate concentration that reflects their unmatched portfolio breadth and channel scale.

Individual product sub-segments exhibit significantly higher concentration. NXP Semiconductors controls approximately 35–40% of UHF RFID chip supply and 45–50% of contactless transit smart card ICs globally. Cognex holds approximately 55–60% of the industrial machine vision market by revenue. These subsegment monopoly positions create both pricing power and technology dependency risk for enterprise customers.

Consolidation is accelerating across the AIDC landscape. Zebra’s USD 875 million Matrox Imaging acquisition, Honeywell’s multiple bolt-on IoT software acquisitions, and NXP’s semiconductor portfolio expansion signal the industry’s structural shift from point-solution hardware vendors to converged platform companies competing on data intelligence rather than device specifications.

Investment & Growth Opportunities

Fastest Growing Segments

Biometric Systems (CAGR ~15.8%), RFID Products (CAGR ~14.2%), and AIDC Software platforms (CAGR ~14.2%) represent the three highest-growth investment vectors through 2034. The AI-enhanced AIDC subsegment crossing hardware, software, and services is projected at USD 22 Billion by 2030 at 24% CAGR, creating the most attractive value creation opportunity within the broader market for both strategic investors and venture-backed startups.

Emerging Markets

India’s AIDC market is the single largest emerging market opportunity, with the government’s Digital India and Production Linked Incentive (PLI) schemes driving manufacturing AIDC investment. Africa’s mobile money and financial inclusion biometrics market is expected to add high-value biometric-authenticated accounts through 2030.

Venture Investment Trends

Venture and growth equity investment in AIDC-adjacent technology, with computer vision AI startups, RFID IoT platforms, and biometric identity verification attracting the largest share.

- Key investment themes: AI-native AIDC platforms, passive IoT RFID sensing, biometric payment convergence, computer vision for unstructured environments, and digital product passport compliance technology.

- Strategic PE interest: AIDC distribution and VAR consolidation, particularly in APAC and LATAM where fragmented distribution networks can be aggregated into regional managed services platforms with recurring revenue models.

Future Market Outlook (2026-2034)

The global AIDC market is positioned for sustained high-growth expansion through 2034. From USD 70.34 Billion in 2025, the market is forecast to reach USD 183.82 Billion by 2034, an absolute value addition of USD 113.48 Billion at a 10.86% CAGR. This growth trajectory is structurally secured by four non-discretionary demand catalysts: regulatory mandates, e-commerce fulfilment infrastructure investment, Industry 4.0 factory automation, and government digital identity program completion.

Between 2026 and 2030, the dominant transformation will be the convergence of AIDC hardware, software, and AI into unified “Visibility-as-a-Platform” offerings. Zebra and Honeywell are each executing strategies to generate 30–40% of total revenue from recurring software and services by 2028, fundamentally changing the financial profile of the AIDC industry from a hardware-dominated lumpy revenue model to a high-margin, recurring subscription business. Vendors achieving this transition will command 3–5× higher EV/revenue multiples than pure hardware peers, creating significant shareholder value divergence within the competitive set.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 160+ industry stakeholders in 2025, comprising AIDC vendor executives, supply chain and IT directors, government procurement officers, healthcare technology managers, retail operations executives, and financial analysts covering the technology sector. Geographic coverage spanned North America, Europe, Asia Pacific, Latin America, and the Middle East. Primary insights validated market sizing, segment shares, and identified convergence trends not visible in secondary data.

Secondary Research

Secondary research encompassed company annual reports and earnings call transcripts, IDC and Gartner market data, GS1 global barcode statistics, NIST biometric evaluation reports, ISO/IEC AIDC standards documentation, IBISWorld industry analyses, government procurement databases, trade publication databases, and patent filing records across 35 countries. Over 320 secondary sources were reviewed and triangulated.

Forecasting Models

Market size forecasts were developed using a bottom-up and top-down hybrid methodology. Key input variables include global e-commerce GMV growth, Industry 4.0 investment trajectories, biometric program deployment schedules across 90+ government programs, and RFID tag ASP decline curves.

Automatic Identification and Data Capture (AIDC) Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offerings Covered | Hardware, Software, Services |

| Product Types Covered | Barcode Scanners, Magnetic Stripe Cards, Smart Cards, Optical Character Recognition (OCR) Systems, RFID Products, Biometric Systems |

| Verticals Covered | Manufacturing, Retail, Transportation and Logistics, Banking and Finance, Healthcare, Government, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Zebra Technologies Corp., Honeywell International Inc., NXP Semiconductors, Cognex Corporation, Datalogic S.p.A., NEC Corporation, Sick AG, TSC Auto ID Technology Co. Ltd., etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automatic identification and data capture (AIDC) market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automatic identification and data capture (AIDC) market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automatic identification and data capture (AIDC) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automatic Identification and Data Capture (AIDC) Market Report

The global AIDC market was valued at USD 70.34 Billion in 2025 and is projected to reach USD 183.82 Billion by 2034, growing at a CAGR of 10.86%.

AIDC stands for Automatic Identification and Data Capture, encompassing barcode scanners, RFID, biometric systems, smart cards, OCR, and magnetic stripe readers.

North America leads with 35.7% revenue share (2025), anchored by U.S. retail RFID mandates, FDA UDI healthcare compliance, DHS biometric border programs, and Amazon supply chain investment.

Hardware dominates with 63.8% market share (2025). Zebra Technologies and Honeywell collectively represent approximately 35–40% of global AIDC hardware revenue in 2025.

Biometric Systems are fastest growing at ~15.8% CAGR, followed by RFID Products at ~14.2% CAGR, driven by government ID programs, border control, and retail inventory automation mandates.

Key companies include Zebra Technologies Corp., Honeywell International Inc., NXP Semiconductors, Cognex Corporation, Datalogic S.p.A., NEC Corporation, Sick AG, and TSC Auto ID Technology Co. Ltd.

Key trends include RAIN RFID item-level visibility, multimodal biometrics for frictionless authentication, AI-powered OCR and machine vision, GS1 digital watermarking, and converged AIDC platform consolidation.

RFID growth is driven by Walmart's 2025 all-merchandise mandate requiring 25+ Billion tags annually, Amazon warehouse automation, EU Digital Product Passport regulation, and UHF RFID tag costs falling below USD 0.05.

Asia Pacific holds 30.4% market share (2025) and is the fastest growing region at ~12.4% CAGR, led by China Industry 4.0, India Aadhaar biometrics, and Southeast Asia e-commerce logistics growth.

Key challenges include high implementation costs, GDPR biometric data restrictions in Europe, RFID-smart card interoperability complexity, cybersecurity vulnerabilities, and counterfeit device proliferation in Asia markets.

Top opportunities include AI-native vision platforms, passive IoT RFID infrastructure, biometric payment convergence, India and Southeast Asia emerging markets, and EU Digital Product Passport compliance technology.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade