Automotive Alternator Market Size, Share, Trends and Forecast by Powertrain Type, Vehicle Type, and Region, 2026-2034

Automotive Alternator Market Size, Share, Trends & Forecast (2026-2034)

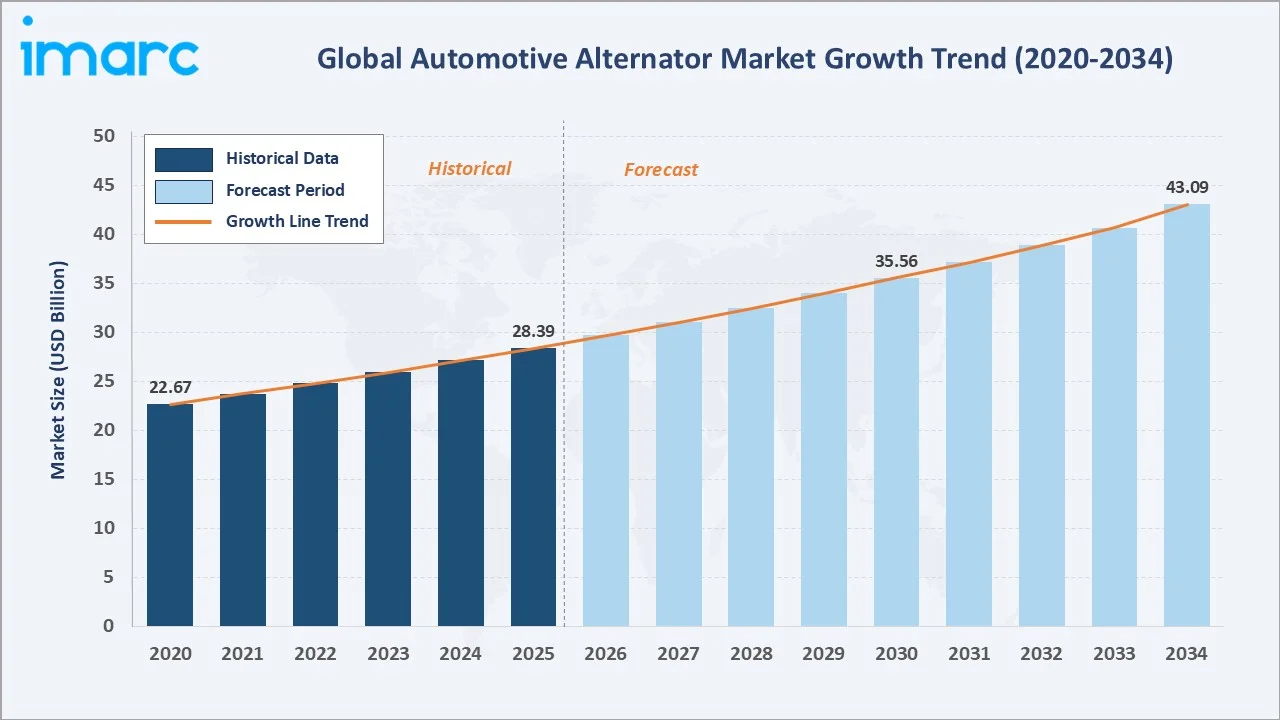

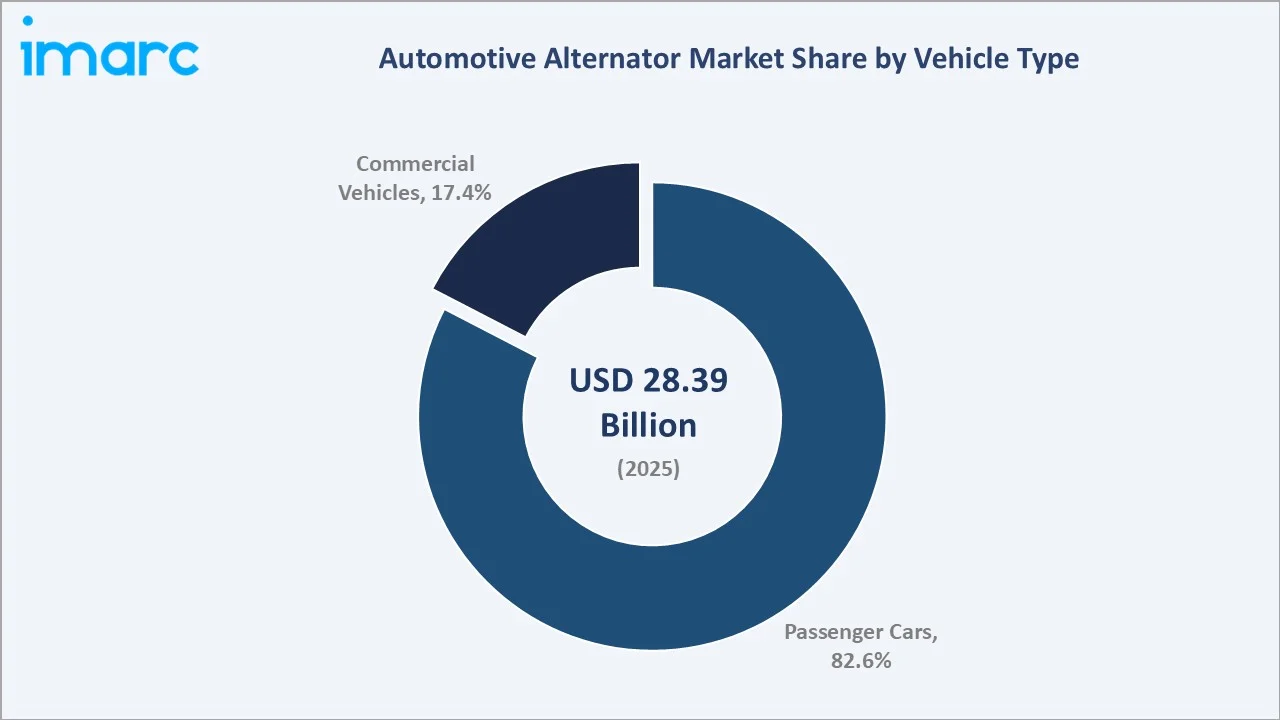

The automotive alternator market was valued at USD 28.39 Billion in 2025 and is projected to reach USD 43.09 Billion by 2034, exhibiting a CAGR of 4.60% during 2026-2034. Sustained vehicle production volumes, increasing adoption of electrically driven accessories, and growing integration of alternators with fuel-saving technologies are the primary drivers shaping market growth.

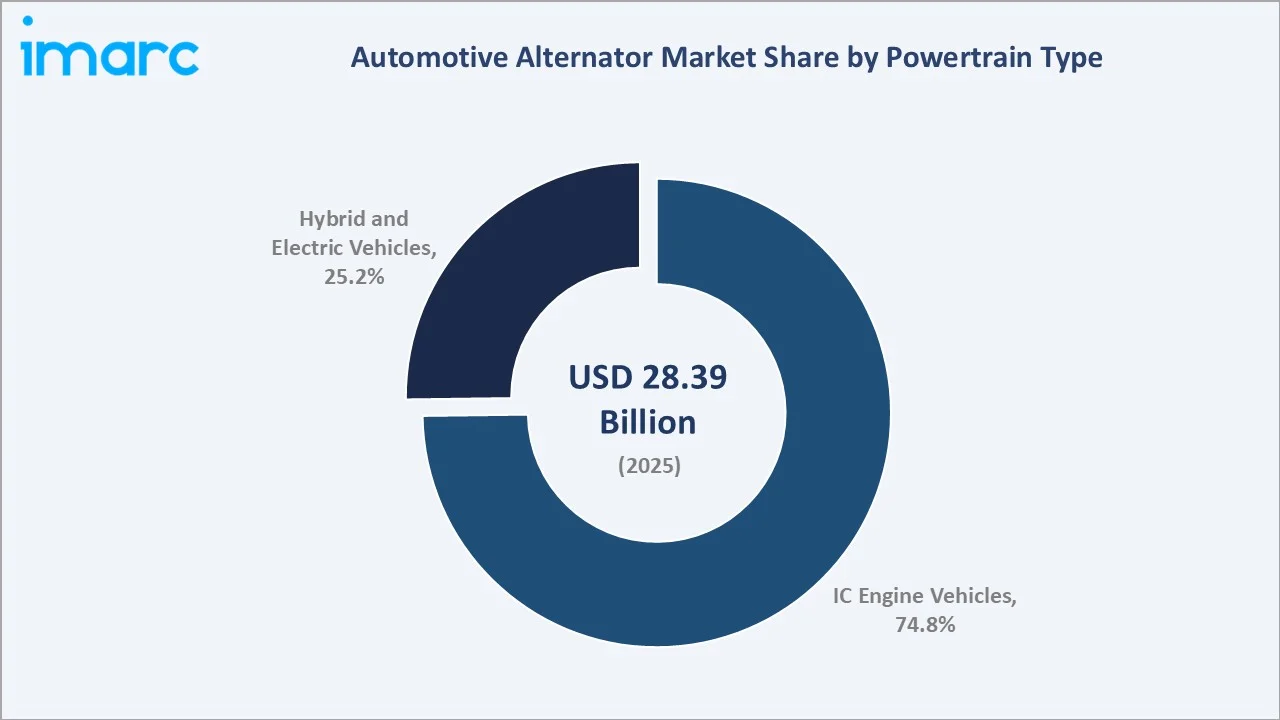

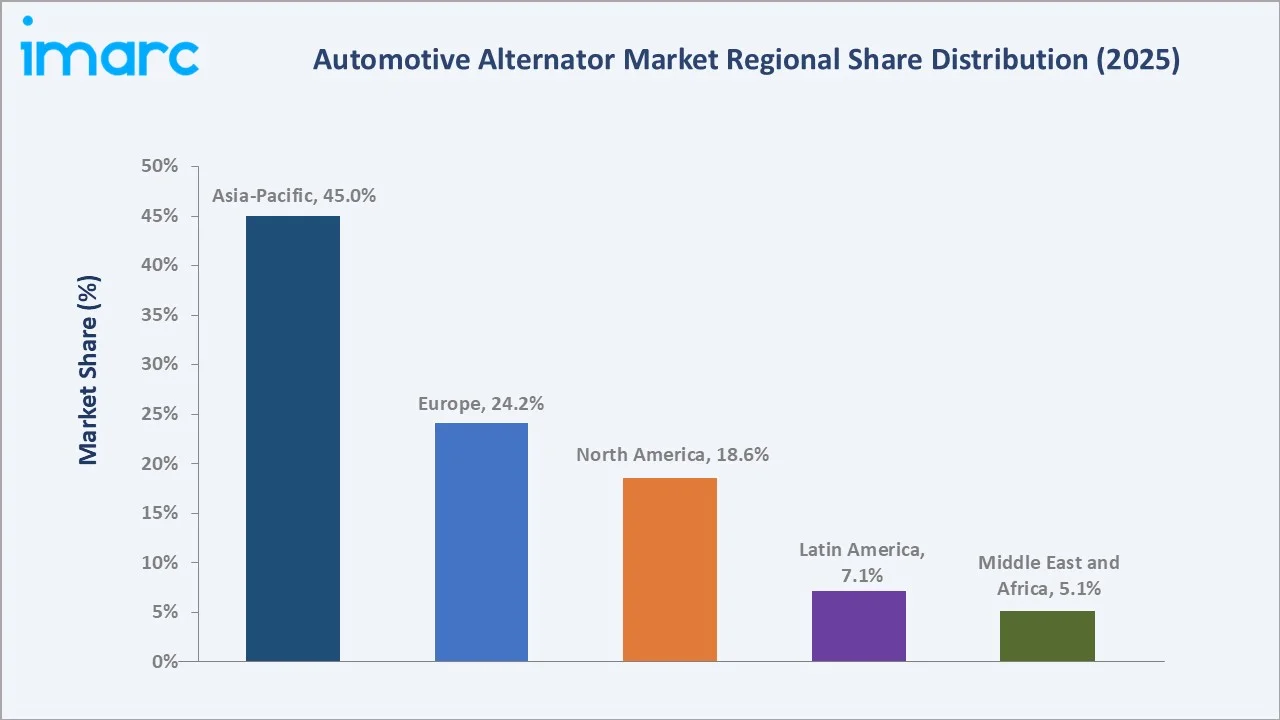

IC engine vehicles lead the powertrain type segment at 74.8%, passenger cars dominate the vehicle type segment at 82.6%, and Asia-Pacific commands 45.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 28.39 Billion |

|

Forecast Market Size (2034) |

USD 43.09 Billion |

|

CAGR (2026-2034) |

4.60% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (45.0%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (45.0%, 2025) |

|

Leading Powertrain Type |

IC Engine Vehicles (74.8%, 2025) |

|

Leading Vehicle Type |

Passenger Cars (82.6%, 2025) |

The automotive alternator market expanded from USD 22.67 Billion in 2020 to USD 28.39 Billion in 2025, driven by steady vehicle production volumes, increasing adoption of electrically driven vehicle accessories, and growing aftermarket replacement demand. Anchored at USD 35.56 Billion in 2030, the forecast to USD 43.09 Billion by 2034 is supported by continued vehicle parc expansion, rising alternator efficiency requirements, and growing integration with mild-hybrid 48V architectures.

To get more information on this market, Request Sample

CAGR trajectories across powertrain type and vehicle type sub-segments show hybrid and electric vehicles and commercial vehicles expanding faster than the overall 4.60% market CAGR, driven by accelerating 48V mild-hybrid adoption and growing electrical power requirements in commercial vehicle platforms.

Executive Summary

The automotive alternator market is on a sustained growth path from USD 22.67 Billion in 2020 to USD 43.09 Billion by 2034. Alternators remain an essential component in conventional and mild-hybrid vehicles, converting mechanical energy into electrical power for battery charging and onboard vehicle electrical systems. Growing electrification of vehicle accessories, rising vehicle production across Asia-Pacific, and expanding aftermarket replacement demand are reinforcing market resilience through the forecast period.

IC engine vehicles lead the powertrain type segment at 74.8% in 2025, reflecting the continued dominance of conventional powertrains in the global vehicle mix. Passenger cars dominate the vehicle type segment at 82.6% in 2025, supported by rising consumer vehicle ownership in emerging economies. In April 2026, passenger vehicle sales in India rose by 2.5% compared to 2025. Asia-Pacific commands 45.0% regional share, led by China, India, Japan, and South Korea.

Key Market Insights

|

Insight |

Data |

|

Leading Powertrain Type |

IC Engine Vehicles – 74.8% share (2025) |

|

Second Largest Powertrain Type |

Hybrid and Electric Vehicles – 25.2% share (2025) |

|

Leading Vehicle Type |

Passenger Cars – 82.6% share (2025) |

|

Second Leading Vehicle Type |

Commercial Vehicles – 17.4% share (2025) |

|

Leading Region |

Asia-Pacific – 45.0% share (2025) |

|

Fastest Growing Region |

Asia-Pacific – 45.0% share (2025) |

|

Top Companies |

MAHLE GmbH, DENSO CORPORATION, PHINIA Inc. |

Key Analytical Observations Expanding On The Data Above:

- IC engine vehicles at 74.8% represent the dominant powertrain type segment in 2025 due to the large installed base of conventional vehicles globally and the multi-decade lifecycle of internal combustion engine powertrains that sustain ongoing OEM and replacement alternator demand.

- Hybrid and electric vehicles at 25.2% represent the fastest-growing powertrain type sub-segment, with demand driven by belt-integrated starter-generators (BiSGs) and 48V alternator-starter systems replacing traditional alternators in mild-hybrid architectures.

- Passenger cars at 82.6% lead the vehicle type segment, reflecting the broader global vehicle mix skewed toward light-duty passenger vehicles and the substantial OEM and aftermarket alternator demand generated by this category.

- Commercial vehicles at 17.4% contribute a smaller but strategically important share, with demand for high-output alternators driven by the power requirements of commercial vehicle electrical systems including telematics, lighting, and refrigeration units.

- Asia-Pacific at 45.0% leads globally on account of China’s position as the world’s leading automotive market, with the China Association of Automobile Manufacturers (CAAM) reporting 30.1 Million vehicles sold in 2023, sustaining high OEM alternator demand across the region.

Automotive Alternator Market Overview

Automotive alternators are electromechanical devices that convert rotational mechanical energy from the engine crankshaft into alternating current, which is then rectified to direct current for battery charging and powering onboard electrical systems. They are a critical component in virtually all conventional and mild-hybrid vehicles, ensuring continuous power supply to lighting, ADAS, infotainment, climate control, and other electrically driven systems.

The global ecosystem integrates raw material suppliers for copper windings and magnetic cores, alternator component manufacturers, Tier 1 alternator assemblers, OEMs incorporating alternators into vehicle powertrains, an extensive independent aftermarket providing remanufactured and new replacement units, and remanufacturers processing returned cores. Together, these stakeholders enable reliable electrical power generation across conventional, mild-hybrid, and commercial vehicle platforms globally.

Market Dynamics

To evaluate market opportunities, Request Sample

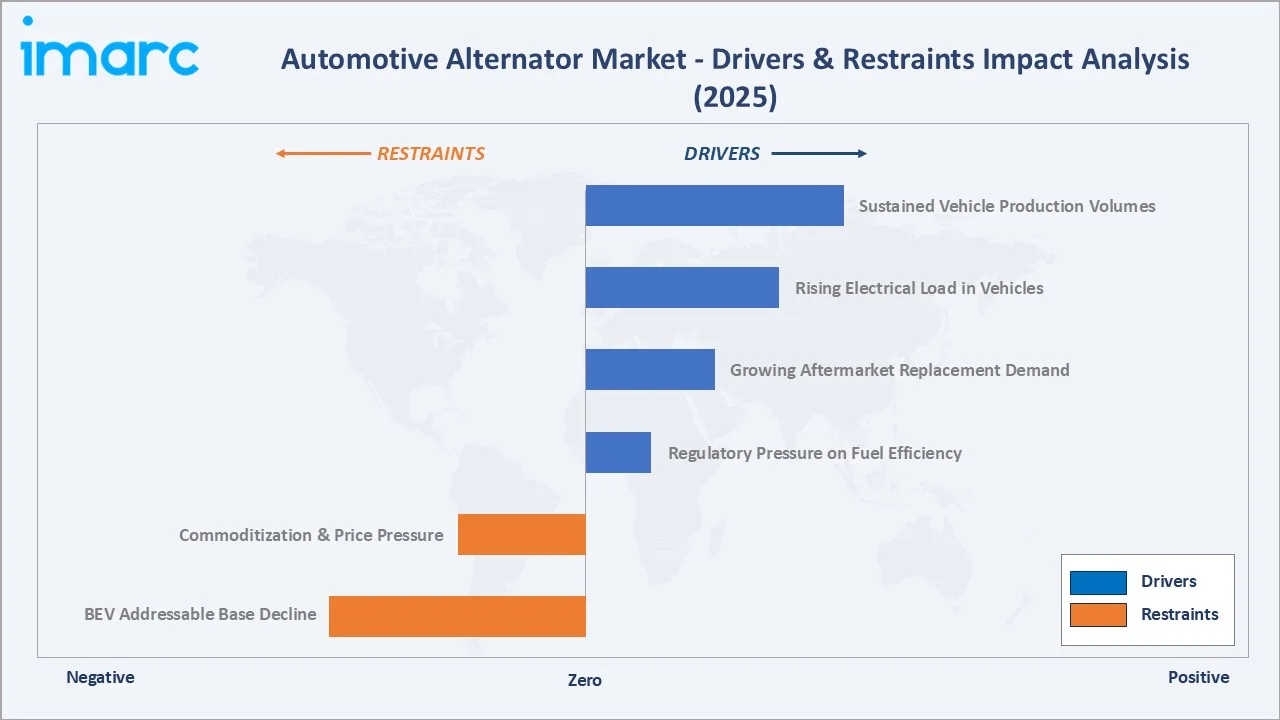

Market Drivers

- Sustained Global Vehicle Production Volumes: Continued high levels of vehicle production globally are generating consistent OEM demand for alternators as a standard component across nearly all non-fully-electric vehicle platforms, supporting market volume stability across all regions.

- Rising Electrical Load in Modern Vehicles: The progressive increase in electrically powered systems, including advanced driver assistance systems (ADAS), in-vehicle infotainment, powered comfort features, and electric power steering, is increasing alternator output requirements and driving demand for higher-capacity units. As per IMARC Group, the global ADAS market size reached USD 33.6 Billion in 2025.

- Growing Aftermarket Replacement Demand: The expanding global vehicle parc and rising average vehicle age are creating sustained aftermarket demand for replacement alternators, supporting revenue growth independent of new vehicle production cycles across both passenger car and commercial vehicle segments.

- Regulatory Pressure on Vehicle Fuel Efficiency: Tightening vehicle emission and fuel-efficiency regulations are encouraging automakers to adopt advanced power management technologies, including high-efficiency alternators with variable voltage regulation and decoupled pulley systems. These regulatory trends are supporting demand for premium alternator variants designed to improve overall vehicle energy efficiency and reduce engine load.

Market Restraints

- Structural Decline in Battery Electric Vehicle (BEV) Addressable Vehicle Base: The accelerating adoption of BEVs is reducing the long-term addressable market for conventional alternators, as fully electric powertrains do not rely on traditional belt-driven charging systems. This transition toward all-electric mobility is expected to create gradual demand pressure on alternator manufacturers focused primarily on internal combustion engine vehicle platforms.

- Commoditization and Aftermarket Price Pressure: Intense competition among remanufacturers and low-cost OEM suppliers in the independent aftermarket is compressing unit margins for standard alternators, limiting revenue growth in segments serving older vehicle platforms and constraining profitability for smaller market participants.

Market Opportunities

- 48V Mild-Hybrid BiSG Adoption: The expanding deployment of 48V mild-hybrid architectures across mainstream passenger vehicles in Europe and China presents a significant opportunity for alternator manufacturers to supply higher-value BiSG units combining starter and alternator functions, commanding premium pricing over conventional units.

- Commercial Vehicle Electrification and High-Output Alternators: Growing demand for auxiliary power in electrified commercial vehicles, including refrigerated transport and construction equipment, is creating opportunities for high-output alternators and auxiliary power units serving specialized applications within the commercial vehicle segment.

Market Challenges

- Shift Toward Fully Electric Powertrains Over the Long Term: The long-term trajectory toward higher BEV penetration represents a structural demand headwind for conventional belt-driven alternators, requiring manufacturers to accelerate product portfolio transition toward electrified powertrain components to maintain long-term revenue relevance.

- Raw Material Cost Volatility: Fluctuations in copper, aluminum, and rare earth element prices introduce cost uncertainty for alternator manufacturers, compressing margins and complicating long-term pricing strategies in a competitive supply environment with limited ability to pass input cost increases to OEM customers.

Emerging Market Trends

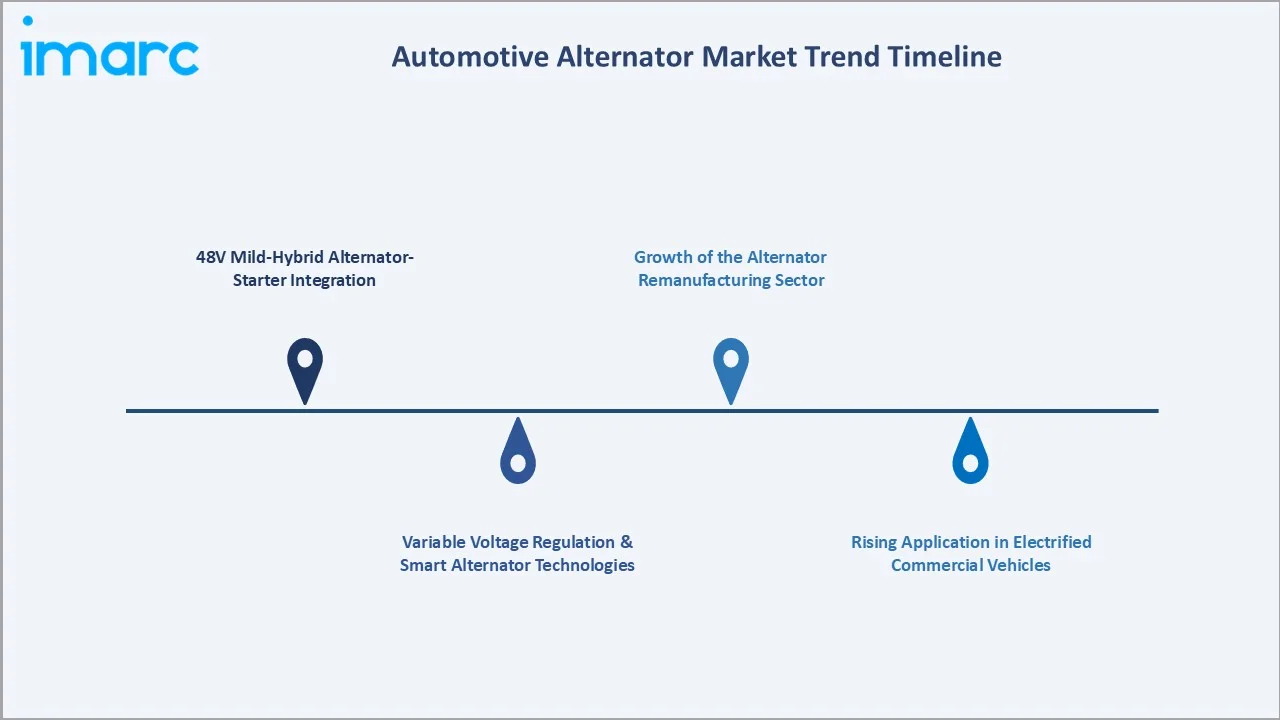

1. Integration of High-Efficiency Alternator-Starters in 48V Mild-Hybrid Architectures

BiSGs operating on 48V electrical architectures are replacing conventional standalone alternators in a growing proportion of new vehicles, particularly in the European and Chinese markets. These systems enable regenerative braking energy recovery, engine start-stop functionality, and torque assist capabilities while continuing to fulfill the charging function of traditional alternators.

2. Adoption of Variable Voltage Regulation and Smart Alternator Technologies

Smart alternators with variable voltage regulation are increasingly adopted by vehicle manufacturers to reduce alternator load on the engine and improve fuel efficiency. These systems modulate output voltage based on driving conditions and battery state of charge, reducing parasitic engine load during acceleration phases. This technology is gaining rapid adoption as a cost-effective fuel economy measure across conventional powertrains, supporting premium alternator market growth ahead of more comprehensive electrification.

3. Growth of the Alternator Remanufacturing Sector

The remanufacturing segment is expanding as rising vehicle ages, increasing core availability, and growing end-user preference for cost-effective replacement solutions drive demand for remanufactured alternators. Remanufacturing reduces material costs and aligns with circular economy principles, attracting investment from independent aftermarket specialists and Tier 1 suppliers establishing in-house remanufacturing capabilities to capture aftermarket margin.

4. Rising Application in Electrified and Hybrid Commercial Vehicles

Commercial vehicle electrification is generating new demand for high-output auxiliary alternators used alongside traction motors in hybrid commercial platforms. Refrigeration, hydraulic, and pneumatic systems in hybrid buses, trucks, and construction equipment require reliable DC power generation, sustaining alternator demand in commercial applications even as electrification progresses across the vehicle industry.

Industry Value Chain Analysis

The automotive alternator value chain spans six stages from raw material supply through end-of-life management. Alternator assembly and OEM integration capture the highest value-add, while aftermarket distribution and remanufacturing generate downstream competitive advantages in this component-driven category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of copper wire, electrical steel laminations, aluminum castings, and rare earth permanent magnets supporting alternator winding and rotor manufacturing |

|

Component Manufacturing |

Producers of rectifier diodes, voltage regulators, slip rings, bearings, and stator windings serving Tier 1 alternator assemblers and remanufacturers |

|

Alternator Assembly |

Tier 1 and Tier 2 suppliers assembling complete alternator units for OEM supply to vehicle manufacturers and for distribution through the independent aftermarket |

|

OEM Integration |

Vehicle manufacturers integrating alternators into engine and electrical system architectures during new vehicle production across all vehicle categories |

|

Distribution & Aftermarket |

Automotive parts distributors, wholesalers, retailers, and e-commerce platforms supplying replacement and remanufactured alternators to repair workshops and end users |

|

End Use & Lifecycle |

Vehicle owners; fleet operators; remanufacturers processing returned cores into serviceable replacement units for secondary market distribution |

Vertically integrated players, which control alternator component manufacturing and assembly, achieve superior cost control and supply security versus integrators relying on third-party component sourcing. This integration advantage reinforces their OEM supply position and supports more competitive aftermarket pricing.

Technology Landscape in the Automotive Alternator Industry

Alternator Design and Efficiency Innovation

Modern alternators are transitioning toward higher efficiency designs incorporating optimized Lundell claw-pole rotor configurations, reduced harmonic distortion in rectification, and improved thermal management to deliver greater output at lower engine RPM. Water-cooled alternators are gaining adoption in high-demand commercial vehicle applications where thermal performance is critical.

48V and Integrated Starter-Generator Technologies

The shift toward 48V mild-hybrid architectures is driving development of BiSGs and crankshaft-integrated motor-generators (CIMGs), which combine alternator, starter, and limited motor-assist functions within a compact electromechanical unit. These systems represent the most significant technology platform transition in the alternator segment, offering higher system value per vehicle for Tier 1 suppliers.

Smart Power Management and Variable Voltage Regulation

Variable voltage regulation systems and smart load management software are enabling demand-responsive power output, reducing alternator parasitic loads, and improving fuel economy in conventional powertrains. Integration with vehicle energy management controllers allows real-time optimization of alternator output based on battery state, driving mode, and electrical load, representing a technically accessible path to fuel savings without full electrification.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Powertrain Type | IC Engine Vehicles | 74.8% | 2025 |

| Vehicle Type | Passenger Cars | 82.6% | 2025 |

| Region | Asia-Pacific | 45.0% | 2025 |

By Powertrain Type

IC engine vehicles command a 74.8% majority share in 2025, driven by the continued dominance of internal combustion engine vehicles in the global vehicle mix across Asia-Pacific, Latin America, Middle East and Africa, and North America. These vehicles rely entirely on belt-driven alternators for all onboard electrical power generation, sustaining consistent OEM and aftermarket demand across a broad range of vehicle platforms.

To access detailed market analysis, Request Sample

Hybrid and electric vehicles at 25.2% in 2025 represent the fastest-growing sub-segment, with demand anchored in mild-hybrid 48V platforms utilizing BiSGs. As OEM adoption of mild-hybrid architectures accelerates across Europe and Asia-Pacific, this segment is expanding its share of total alternator market revenues, supporting premium pricing and higher system value per vehicle than conventional alternator products.

By Vehicle Type

Passenger cars dominate with 82.6% share in 2025, reflecting the scale of the global light vehicle parc and the extensive per-vehicle alternator demand from modern passenger cars equipped with growing electrical loads. Increasing adoption of electrically driven comfort, safety, and infotainment systems continues to drive demand for higher-output alternators in the passenger car segment across all major markets.

Commercial vehicles at 17.4% in 2025 serve a structurally distinct demand profile, with high-output alternators required to power onboard systems such as lighting, refrigeration, hydraulic power units, and fleet telematics. Commercial vehicle alternators command higher average selling prices and are subject to more demanding performance specifications, contributing a disproportionate revenue share relative to unit volume within the overall market.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

45.0% |

Large and expanding automotive manufacturing base, rising vehicle ownership in emerging economies, and strong OEM demand from major automotive production hubs |

|

Europe |

24.2% |

Stringent emissions regulations, widespread adoption of mild-hybrid 48V systems, and mature automotive aftermarket driving demand for efficiency-oriented alternator technologies |

|

North America |

18.6% |

Large vehicle parc with rising average age, strong aftermarket replacement demand, and growing commercial vehicle alternator requirements |

|

Latin America |

7.1% |

Expanding vehicle production in Brazil and Mexico, growing consumer vehicle ownership, and increasing aftermarket demand from an aging regional vehicle fleet |

|

Middle East and Africa |

5.1% |

Increasing vehicle sales in GCC countries, growing automotive assembly activities, and expansion of the independent aftermarket across the region |

Asia-Pacific at 45.0% in 2025 leads the global market, driven by China’s position as the world’s leading automotive production and sales market, combined with significant vehicle manufacturing hubs in Japan, South Korea, India, and Southeast Asia. The region’s large OEM customer base and rapidly growing aftermarket support sustained alternator demand across all vehicle categories.

Europe at 24.2% is driven by stringent vehicle emissions and fuel efficiency regulations, widespread 48V mild-hybrid adoption, and mature OEM relationships with global alternator suppliers. Strong automotive manufacturing capabilities across Germany, France, and other major European vehicle production hubs continue to support steady expansion of the market.

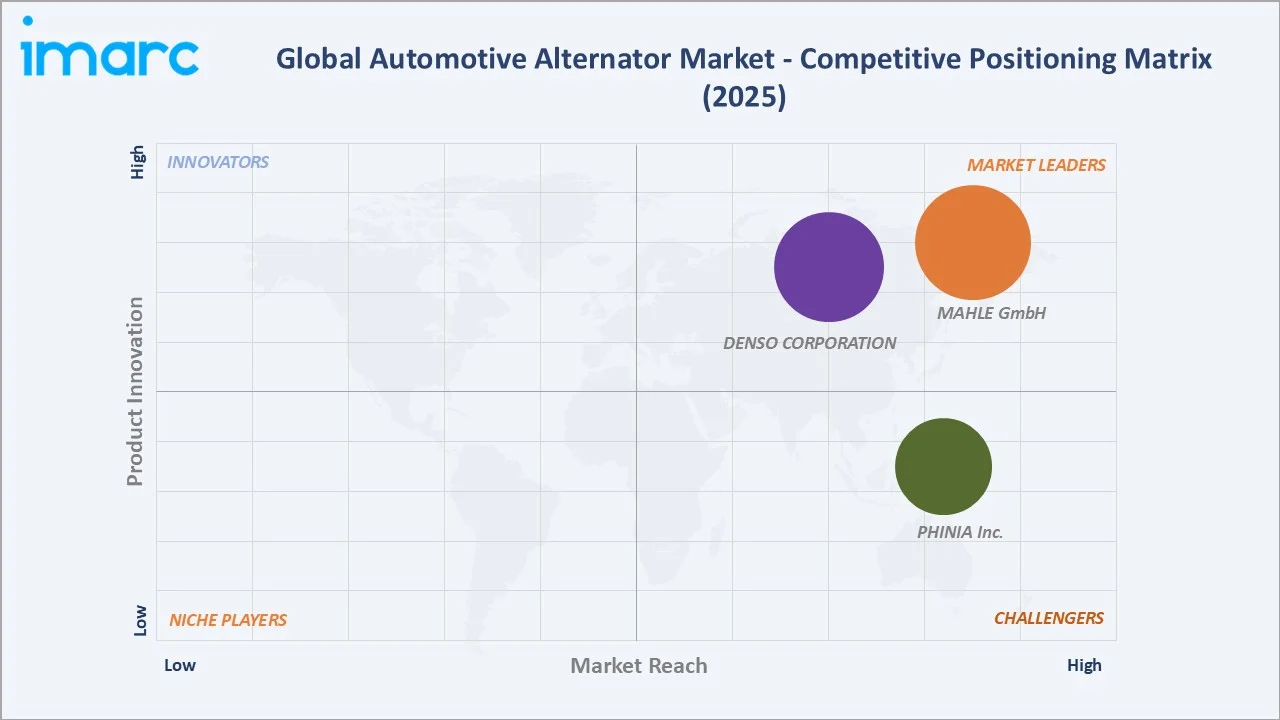

Competitive Landscape

The automotive alternator market is moderately consolidated, with global Tier 1 automotive suppliers dominating OEM supply channels while regional specialists and remanufacturers serve the independent aftermarket. Technological capabilities in alternator efficiency, compact design, and 48V system compatibility form the primary competitive differentiators among leading market participants.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

MAHLE GmbH |

MAHLE Letrika alternators |

Leader |

Broad OEM alternator supply across vehicle and industrial applications |

|

DENSO CORPORATION |

DENSO alternators and starters |

Leader |

Deep OEM integration and advanced electrical systems capabilities |

|

PHINIA Inc. |

Heavy-duty starters and alternators for commercial vehicles |

Challenger |

Commercial vehicle aftermarket leadership and OEM electrical systems supply |

Key players include MAHLE GmbH, DENSO CORPORATION, and PHINIA Inc., among others.

Key Company Profiles

MAHLE GmbH

MAHLE GmbH is a globally recognized automotive supplier headquartered in Stuttgart, Germany, with a comprehensive product portfolio spanning alternators, starters, thermal management systems, filtration, and powertrain components for passenger car, commercial vehicle, and industrial machinery applications worldwide.

- Product Portfolio: MAHLE Letrika alternators and starters for passenger cars, commercial vehicles, trucks, buses, and industrial machinery; thermal management systems; filtration solutions; and powertrain components serving OEM customers across global automotive markets.

- Recent Developments: MAHLE GmbH has continued to expand its automotive alternator and charging system capabilities to support evolving vehicle electrical architecture requirements across passenger and commercial vehicle platforms. The company is also strengthening partnerships with global automotive OEMs while enhancing manufacturing efficiency and product development initiatives focused on advanced energy management solutions.

- Strategic Focus: Strengthening global OEM alternator supply relationships across vehicle and industrial applications, advancing electrification product capabilities, and optimizing manufacturing operations for sustained long-term competitiveness.

DENSO CORPORATION

DENSO CORPORATION is a leading global automotive supplier headquartered in Kariya, Japan, with a broad product portfolio spanning powertrain systems, thermal management, electrification technologies, and electrical components, supplying OEM customers across passenger car, commercial vehicle, and mobility applications globally.

- Product Portfolio: Automotive alternators and starters for passenger cars and commercial vehicles, thermal management systems, powertrain control units, electrification components, and a wide range of automotive electronics serving major OEM customers across all key global markets.

- Recent Developments: DENSO CORPORATION continues to strengthen its alternator and electrical systems product lines, advancing capabilities across OEM supply relationships and investing in next-generation technologies to meet the evolving requirements of global automotive customers.

- Strategic Focus: Deepening OEM integration across global automotive markets, expanding advanced electrical systems capabilities, and accelerating product development for long-term market leadership across passenger car and commercial vehicle platforms.

PHINIA Inc.

PHINIA Inc. is an independent, publicly listed components and solutions provider specializing in commercial vehicle electrical systems, fuel systems, and aftermarket solutions, serving commercial vehicle OEMs, fleet operators, and aftermarket distributors across global markets.

- Product Portfolio: Heavy-duty starters and alternators for commercial trucks, buses, and off-highway equipment; fuel systems for commercial and light vehicles; and aftermarket electrical and fuel system components serving global commercial vehicle and industrial applications.

- Recent Developments: PHINIA Inc. continues to expand its commercial vehicle electrical systems business, growing its product portfolio and strengthening its distribution network across key global markets to reinforce its position as a leading provider of heavy-duty starters and alternators.

- Strategic Focus: Building commercial vehicle aftermarket leadership through expanded distribution networks, strengthening OEM electrical systems supply relationships, and investing in advanced fuel system technologies for alternative fuel applications.

Market Concentration Analysis

The automotive alternator market is moderately concentrated at the OEM level, with MAHLE GmbH, DENSO CORPORATION, and PHINIA Inc. collectively holding a significant share of global OEM alternator supply, supported by their deep integration within major automotive assembly programs across multiple vehicle platforms globally.

Barriers to entry include the substantial engineering investment required for OEM qualification, the need for high-volume manufacturing capabilities with consistent quality, long-term OEM supply agreement structures, and established global aftermarket distribution networks. The remanufacturing segment is more fragmented, with regional specialists and a large number of independent remanufacturers serving local aftermarket demand.

Consolidation is progressing through electrification-focused investments, platform sharing agreements, and vertical integration strategies, as Tier 1 suppliers position their alternator businesses for the transition toward 48V mild-hybrid and fully electric powertrains. Scale advantages in manufacturing, distribution, and engineering are further reinforcing the competitive position of established market leaders.

Investment & Growth Opportunities

Fastest-Growing Segments

Hybrid and electric vehicles at 25.2% of the market in 2025 represents the fastest-growing powertrain type sub-segment, with demand anchored in 48V mild-hybrid BiSGs commanding higher average selling prices than conventional alternators. This segment is expanding faster than the overall 4.60% market CAGR through 2034, driven by OEM electrification programs in Europe and Asia-Pacific.

Emerging Markets

Asia-Pacific at 45.0% leads global market share, with India and Southeast Asia representing the largest untapped growth opportunities. Rising vehicle ownership rates, expanding domestic automotive manufacturing, and growing aftermarket replacement demand are creating favorable conditions for market expansion. Latin America at 7.1% also presents growth potential through rising vehicle production in Brazil and Mexico.

Venture & Investment Trends

Investment is concentrated in 48V BiSG development programs, smart alternator technology with variable voltage regulation capabilities, and high-output commercial vehicle alternators addressing growing electrical demands. Strategic investments targeting remanufacturing assets and aftermarket distribution networks are also attracting capital as leading players seek to secure recurring revenue from the large and growing vehicle replacement market globally.

Future Market Outlook (2026-2034)

The automotive alternator market is forecast to expand from USD 28.39 Billion in 2025 to USD 43.09 Billion by 2034 at a CAGR of 4.60%, adding approximately USD 14.7 Billion in incremental annual market value over the forecast period.

Four dynamics will shape the market through 2034: continued high vehicle production volumes in Asia-Pacific; accelerating adoption of 48V mild-hybrid architectures integrating BiSG systems; rising average vehicle age in developed markets driving aftermarket replacement demand; and ongoing regulatory pressure on vehicle fuel efficiency supporting premium alternator adoption. These forces are expected to sustain positive market growth despite the long-term structural headwind from rising BEV penetration.

By 2034, BiSG-based alternator-starter systems are expected to represent a materially larger proportion of OEM new vehicle installations in leading markets, while the conventional replacement market will continue to provide a stable revenue base supported by the world’s large and aging vehicle parc across emerging economies.

Research Methodology

Primary Research

Primary research included interviews with senior supply chain managers at Tier 1 alternator manufacturers, vehicle assembly plant engineers, automotive aftermarket distributors, and fleet operators, validating market sizing, regional demand, powertrain type splits, and vehicle type distribution assumptions across key geographies.

Secondary Research

Secondary sources included OICA vehicle production statistics, IEA Global EV Outlook, European Automobile Manufacturers’ Association (ACEA) registration data, annual reports and investor presentations from leading alternator manufacturers, trade publications including Automotive News and Just Auto, and regulatory filings from the European Commission and United States Environmental Protection Agency.

Forecasting Models

Market forecasts used top-down and bottom-up models combining global vehicle production data, alternator attachment rates by vehicle segment, OEM and aftermarket revenue splits, and segment-level CAGR estimates. Scenario analysis addressed BEV penetration rate variation and its impact on conventional alternator addressable market sizing through the 2026-2034 forecast period.

Automotive Alternator Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Powertrain Types Covered | IC Engine Vehicles, Hybrid and Electric Vehicles |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicle |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | MAHLE GmbH, DENSO CORPORATION, PHINIA Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive alternator market from 2020-2034.

- The automotive alternator market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive alternator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Alternator Market Report

The automotive alternator market was valued at USD 28.39 Billion in 2025, supported by sustained global vehicle production, rising electrical loads in modern vehicles, and strong aftermarket replacement demand across all major regions.

The market is projected to grow at a CAGR of 4.60% from 2026 to 2034, reaching USD 43.09 Billion, supported by mild-hybrid adoption, growing vehicle parc, and increasing aftermarket replacement activity.

IC engine vehicles lead at 74.8% in 2025, driven by the large installed base of conventional vehicles. Hybrid and electric vehicles at 25.2% represent the fastest-growing sub-segment through 2034.

Passenger cars dominate at 82.6% in 2025, reflecting the scale of the global light vehicle parc and growing per-vehicle electrical load from infotainment, ADAS, and comfort systems.

Asia-Pacific commands 45.0% in 2025, driven by China, Japan, India, and South Korea as major automotive production and sales markets sustaining high OEM and aftermarket alternator demand.

Leading companies include MAHLE GmbH, DENSO CORPORATION, and PHINIA Inc., among others.

Key drivers include sustained vehicle production volumes, rising electrical loads from ADAS and infotainment systems, growing aftermarket replacement demand, and regulatory pressure on vehicle fuel efficiency supporting premium alternator adoption.

Battery electric vehicles do not use traditional alternators, creating a long-term structural headwind. However, mild-hybrid 48V systems are expanding demand for higher-value BiSGs within the broader market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)