Automotive Charge Air Cooler Market Report by Product Type (Air-cooled, Liquid-cooled), Position Type (Integrated, Standalone), Design Type (Fin and Tube, Bar and Plate), Fuel Type (Diesel, Gasoline), Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, and Others), Sales Channel (OEM, Aftermarket), and Region 2026-2034

Automotive Charge Air Cooler Market Size:

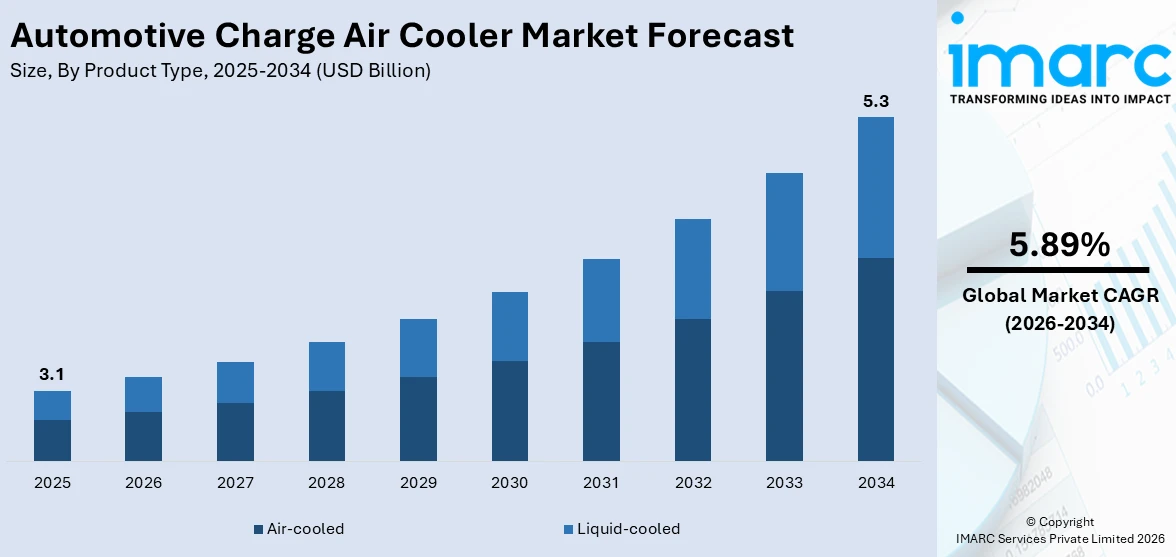

The global automotive charge air cooler market size reached USD 3.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 5.3 Billion by 2034, exhibiting a growth rate (CAGR) of 5.89% during 2026-2034. Increasing demand for fuel-efficient vehicles, the widespread adoption of turbocharged engines, heightened consumer awareness of performance and longevity, advancements in automotive technology, growth in electric and hybrid vehicles, expansion of the aftermarket sector, and innovation in cooling designs are factors fueling the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.1 Billion |

| Market Forecast in 2034 | USD 5.3 Billion |

| Market Growth Rate (2026-2034) | 5.89% |

Automotive Charge Air Cooler Market Analysis:

- Major Market Drivers: The escalating need for fuel-efficient vehicles has considerably surged the product demand as these components make engine more efficient and help optimize its performance, which is one of the primary factors supporting the market growth. Additionally the increasing number of stringent regulations across the globe, which are compelling the automakers to downsize and reduce emissions, is further creating a positive automotive charge air cooler market outlook. This is further supported by the growing automotive industry, especially in developing regions, and the development of new materials and manufacturing technologies. Apart from this, the burgeoning adoption of electric and hybrid vehicles, which also use charge air coolers, is further driving the automotive charge air cooler market growth.

- Key Market Trends: The rising application of advanced materials, such as aluminum and composite material, in charge air coolers to improve their efficiency and durability is one of the primary market trends. This is further bolstered by the escalating demand for products with compact size and lighter weight to comply with the requirements of modern car designs. As per the automotive charge air cooler market forecast, the key automotive manufacturers and charge air cooler producers are engaging in collaborations to introduce advanced product variants, which is further accelerating the market growth. Furthermore, the integration of smart technologies such as sensors and the Internet of Things (IoT) to enable real-time monitoring and maintenance in charge air coolers is driving the automotive charge air cooler market value.

- Geographical Trends: North America leads the market due to the escalating use of turbocharged engines and strict emission policies introduced in the US and Canada. Moreover, the region al market is bolstered by the presence of several major automotive companies and advanced technologies, which is facilitating the product demand.. Additionally, Europe holds a considerable share in the market, which can be attributed to the growing demand for electric and hybrid vehicles and stringent government regulations. Apart from this, in Asia-Pacific, China emerges as one of the fastest-growing countries owing to expanding automotive industry and burgeoning disposable income, complemented by the surging inclination towards fuel-efficient vehicles, which is further boosting the automotive charge air cooler demand.

- Competitive Landscape: Some of the major market players in the automotive charge air cooler industry include AKG Group, Banco Products (India) Ltd., C, G, & J Inc., Dana Limited, Dura-Lite Heat Transfer Products Ltd., Hanon Systems, MAHLE GmbH, Modine Manufacturing Company, T. RAD Co. Ltd., Valeo, and Vestas Aircoil A/S., among many others.

- Challenges and Opportunities: One of the primary challenges for the market is the escalating competition among key market players, which, in turn, creates downward pressure on pricing. Additionally, stringent emission regulations have risen the demand for cleaner and more efficient products, which is further hindering the market growth. According to the automotive charge air cooler market overview, the increasing demand for fuel-efficient and high-performance cars presents significant opportunities. Additionally, the expanding aftermarket segment provides opportunities for companies to offer replacement and upgraded charge air coolers, catering to the rising consumer awareness regarding vehicle maintenance and performance optimization.

To get more information on this market Request Sample

Automotive Charge Air Cooler Market Trends:

Growing Demand for Fuel-Efficient and High-Performance Vehicles

The increasing consumer inclination towards fuel-efficient and high-performance vehicles boosts the demand for automotive charge air coolers. The growing environmental standards and the push towards efficient product variants have compelled the key manufacturers to introduce fuel-efficient vehicles that produce fewer emissions, which is further driving the automotive charge air cooler market revenue. These air coolers help in boosting the engine’s energy efficiency by compressing air temperature before it enters the combustion chamber. Apart from this, the rising environmental consciousness among the consumers have escalated the demand for fuel-efficient vehicles, which is creating a positive outlook for the market.

Adoption of Turbocharged Engines

The burgeoning product demand across the automotive industry is one of the primary factors boosting the market growth. Turbochargers deliver more air to the combustion chamber, which further offers a higher fuel-air mixture for improved power output. However, this generates a significant amount of heat, which further reduces engine performance, which has further surged the demand for charge air coolers as they help in cooling down compressed air from the turbochargers to the engine. Apart from this, the increasing use of turbocharging technology across various vehicles, such as passenger cars, trucks, and sports utility vehicles (SUVs) are supporting the market growth.

Rising Consumer Awareness of Vehicle Performance and Longevity

Growing awareness regarding the performance and life span of a vehicle is a major factor facilitating the market growth. This is further supported by the escalating awareness among consumers regarding the advantages of sophisticated automotive technologies have burgeoned their expenditure on top-quality parts that will improve vehicle performance and life. This has boosted the product demand as it helps in lowering the intake of air temperatures, further preventing engine overheating, reducing wear and tear on engine components, and improving overall reliability.

Automotive Charge Air Cooler Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product type, position type, design type, fuel type, vehicle type, and sales channel.

Breakup by Product Type:

- Air-cooled

- Liquid-cooled

Air-cooled accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product type. This includes air-cooled and liquid-cooled. According to the report, air-cooled represented the largest segment.

The air-cooled segment is driven by the need for simplified cooling solutions in automotive applications. Air-cooled charge air coolers are favored for their straightforward design, which eliminates the need for complex liquid cooling systems and associated components such as pumps, hoses, and radiators. This simplicity translates into reduced maintenance requirements and lower overall system costs. Additionally, air-cooled systems are often preferred for their lighter weight and more compact design compared to liquid-cooled alternatives, making them suitable for applications where space and weight are critical considerations. The ease of installation and integration of air-cooled charge air coolers into existing vehicle designs further enhances their appeal. Furthermore, advancements in air-cooled technology, including the development of more efficient and durable heat exchangers, have improved the performance of these systems, making them more competitive with liquid-cooled options.

Breakup by Position Type:

- Integrated

- Standalone

A detailed breakup and analysis of the market based on the position type have also been provided in the report. This includes integrated and standalone.

The integrated segment is driven by the increasing demand for compact and efficient cooling solutions in modern automotive designs. Integrated charge air coolers, which combine the charge air cooler with other engine components such as intercoolers or radiators, offer significant space-saving advantages and streamlined installation. This is particularly important as vehicle manufacturers strive to optimize engine bays for better performance and reduced weight. The integration of charge air coolers with other components helps to minimize the number of parts and associated complexity, leading to lower production costs and reduced potential for system failures.

The standalone segment is driven by the growing preference for customizable and flexible cooling solutions in the automotive sector. Standalone charge air coolers, which operate independently of other engine components, offer distinct advantages in terms of installation flexibility and performance optimization. These systems are often used in high-performance vehicles and aftermarket applications where specific cooling requirements and performance enhancements are crucial. Standalone coolers allow for precise tuning and adjustment to meet the unique needs of various engine configurations, making them ideal for applications where maximum cooling efficiency and reliability are essential.

Breakup by Design Type:

- Fin and Tube

- Bar and Plate

Fin and tube represent the leading market segment

The report has provided a detailed breakup and analysis of the market based on the design type. This includes fin and tube and bar and plate. According to the report, fin and tube represented the largest segment.

The fin and tube segment in the automotive charge air cooler market is driven by the increasing emphasis on enhancing engine performance and fuel efficiency. This segment benefits from its ability to provide efficient heat dissipation through its design, which features multiple fins and tubes that maximize surface area for improved thermal management. As automotive manufacturers seek to meet stringent emission regulations and consumer demands for higher performance, fin and tube charge air coolers offer a cost-effective solution by efficiently cooling the compressed air from turbochargers, thereby enhancing engine efficiency and power output. Furthermore, advancements in materials and manufacturing processes have led to the development of more durable and lightweight fin and tube coolers, which contribute to overall vehicle performance and longevity. The growing trend towards the adoption of turbocharged engines across various vehicle segments, including passenger cars, trucks, and SUVs, has increased the demand for efficient cooling solutions, further boosting the fin and tube segment.

Breakup by Fuel Type:

- Diesel

- Gasoline

Diesel exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the fuel type have also been provided in the report. This includes diesel and gasoline. According to the report, diesel accounted for the largest market share.

The diesel segment is driven by the increasing demand for diesel engines in commercial vehicles and heavy-duty applications, where charge air coolers play a crucial role in enhancing engine performance and efficiency. Diesel engines are favored for their superior torque and fuel efficiency, which are essential for trucks, buses, and agricultural machinery that require high power output and durability. To optimize the performance of these engines, charge air coolers are essential as they reduce the temperature of the compressed air before it enters the combustion chamber, improving air density and combustion efficiency. Additionally, the stringent emission regulations imposed globally necessitate advanced cooling solutions to ensure that diesel engines operate within permissible emission limits while maintaining performance. The ongoing advancements in turbocharging technology, commonly used in diesel engines, further drive the demand for effective charge air coolers to manage the increased heat generated by these systems.

Breakup by Vehicle Type:

- Passenger Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Others

Passenger vehicles dominates the market

The report has provided a detailed breakup and analysis of the market based on the vehicle type. This includes passenger vehicles, light commercial vehicles, heavy commercial vehicles, and others. According to the report, passenger vehicles represented the largest segment.

The passenger vehicles segment is driven by the growing emphasis on fuel efficiency and reduced emissions, as stringent environmental regulations compel manufacturers to adopt advanced cooling technologies. Charge air coolers play a crucial role in enhancing engine performance by lowering the intake air temperature, which improves combustion efficiency and power output while reducing fuel consumption. The increasing consumer preference for high-performance vehicles with better fuel economy further drives the demand for efficient charge air coolers. Additionally, the widespread adoption of turbocharged engines in passenger vehicles necessitates the use of charge air coolers to manage the elevated temperatures generated by turbocharging, ensuring optimal engine performance and longevity.

Breakup by Sales Channel:

Access the comprehensive market breakdown Request Sample

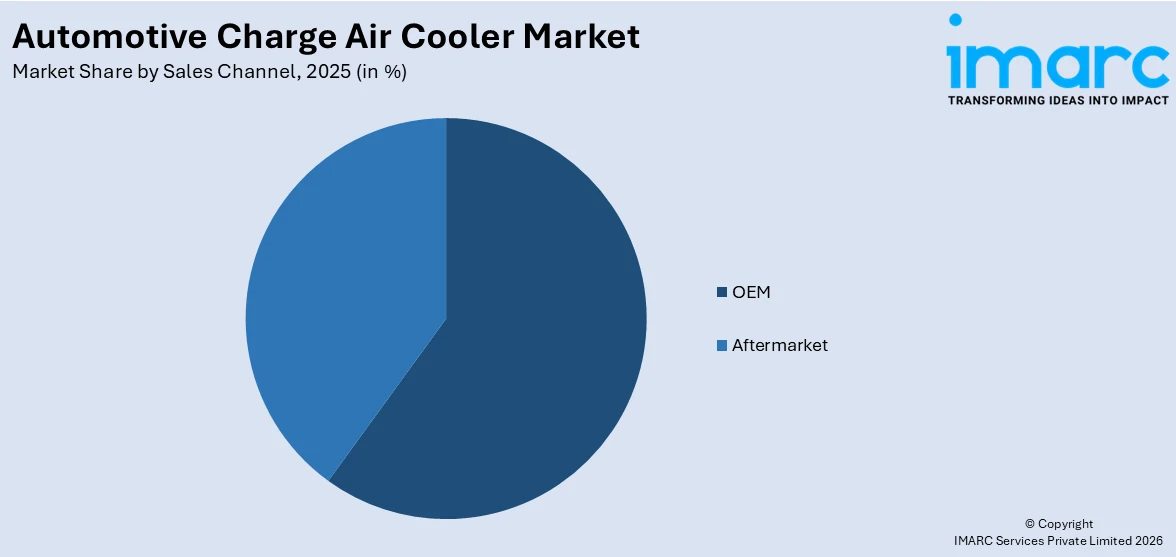

- OEM

- Aftermarket

OEM is the predominant market segment

A detailed breakup and analysis of the market based on the sales channel have also been provided in the report. This includes OEM and aftermarket. According to the report, OEM accounted for the largest market share.

As per the automotive charge air cooler market research report, the OEM segment is driven by the increasing emphasis on enhancing vehicle performance and fuel efficiency. Automakers are prioritizing the integration of advanced charge air coolers in their new vehicle models to meet stringent emission regulations and consumer demands for high-performance engines. The adoption of turbocharged and high-compression engines across various vehicle segments necessitates efficient charge air coolers to manage the increased heat generated by these systems, ensuring optimal air intake temperatures and improved combustion efficiency. Additionally, the growth of electric and hybrid vehicles, which require sophisticated thermal management solutions to handle the additional heat generated by electric motors and batteries, is also boosting demand for OEM charge air coolers.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest automotive charge air cooler market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for automotive charge air cooler.

The Asia Pacific regional market is driven by the burgeoning automotive industry, with rapid growth in vehicle production and sales across key countries such as China, India, and Japan. This expansion is largely fueled by rising disposable incomes, urbanization, and a growing middle-class population, which increases demand for both personal and commercial vehicles. The adoption of advanced engine technologies, including turbocharging, is another significant driver. As manufacturers aim to enhance engine performance and comply with stringent emission standards, the need for effective charge air coolers becomes critical. Additionally, the region's increasing focus on fuel efficiency and performance upgrades further propels the market, as consumers and manufacturers alike seek solutions to improve vehicle efficiency and reduce environmental impact. Government regulations and policies aimed at reducing vehicle emissions and improving fuel economy also play a crucial role, pushing automotive companies to integrate advanced cooling systems.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the automotive charge air cooler industry include AKG Group, Banco Products (India) Ltd., C, G, & J Inc., Dana Limited, Dura-Lite Heat Transfer Products Ltd., Hanon Systems, MAHLE GmbH, Modine Manufacturing Company, T. RAD Co. Ltd., Valeo, Vestas Aircoil A/S., etc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- The key automotive charge air cooler companies are actively engaging in various strategic initiatives to maintain their competitive edge and address evolving industry demands. They are investing heavily in research and development (R&D) to innovate and improve charge air cooler designs, focusing on enhancing thermal efficiency, reducing weight, and optimizing performance for turbocharged engines. This involves the development of advanced materials and technologies, such as lightweight alloys and innovative cooling technologies, which contribute to better heat dissipation and overall engine efficiency. Additionally, players are expanding their manufacturing capabilities and establishing new production facilities in key regions to meet the growing demand and cater to diverse market needs. Strategic partnerships and collaborations with automotive manufacturers are also a common approach, enabling these companies to integrate their cooling solutions into a broader range of vehicle models and applications.

Automotive Charge Air Cooler Market News:

- In 2022, Conflux Technology introduced its first three-dimensional (3D) printed automotive charge air cooler, which is water based. This innovative product, launched at an international automotive exhibition, represents a significant advancement in automotive thermal management. The 3D-printed design allows for intricate geometries that enhance cooling efficiency and reduce weight, thereby improving overall vehicle performance and fuel efficiency. This launch marks Conflux Technology's entry into the automotive market, leveraging their expertise in 3D printing to offer cutting-edge thermal management solutions.

- In 2023, Modine Manufacturing Company announced the sale of three of its German-based automotive businesses to affiliates of Regent LP. These businesses, located in Neuenkirchen, Pliezhausen, and Wackersdorf, primarily manufacture parts for internal combustion engine applications, including charge air cooler modules. This divestiture aligns with Modine's strategic focus on high-margin, innovative technologies with strong growth potential.

Automotive Charge Air Cooler Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Air-cooled, Liquid-cooled |

| Position Types Covered | Integrated, Standalone |

| Design Types Covered | Fin and Tube, Bar and Plate |

| Fuel Types Covered | Diesel, Gasoline |

| Vehicle Types Covered | Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Others |

| Sales Channels Covered | OEM, Aftermarket |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AKG Group, Banco Products (India) Ltd., C, G, & J Inc., Dana Limited, Dura-Lite Heat Transfer Products Ltd., Hanon Systems, MAHLE GmbH, Modine Manufacturing Company, T. RAD Co. Ltd., Valeo, Vestas Aircoil A/S, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global automotive charge air cooler market performed so far, and how will it perform in the coming years ?

- What are the drivers, restraints, and opportunities in the global automotive charge air cooler market ?

- What is the impact of each driver, restraint, and opportunity on the global automotive charge air cooler market ?

- What are the key regional markets ?

- Which countries represent the most attractive automotive charge air cooler market ?

- What is the breakup of the market based on the product type ?

- Which is the most attractive product type in the automotive charge air cooler market ?

- What is the breakup of the market based on the position type ?

- Which is the most attractive position type in the automotive charge air cooler market ?

- What is the breakup of the market based on the design type ?

- Which is the most attractive design type in the automotive charge air cooler market ?

- What is the breakup of the market based on the fuel type ?

- Which is the most attractive fuel type in the automotive charge air cooler market ?

- What is the breakup of the market based on the vehicle type ?

- Which is the most attractive vehicle type in the automotive charge air cooler market ?

- What is the breakup of the market based on the sales channel ?

- Which is the most attractive sales channel in the automotive charge air cooler market ?

- What is the competitive structure of the market ?

- Who are the key players/companies in the global automotive charge air cooler market ?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive charge air cooler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive charge air cooler market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive charge air cooler industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)