Automotive Glass Market Size, Share, Trends and Forecast by Glass Type, Material Type, Vehicle Type, Application, End-User, Technology, and Region, 2026-2034

Automotive Glass Market Size, Share, Trends & Forecast (2026-2034)

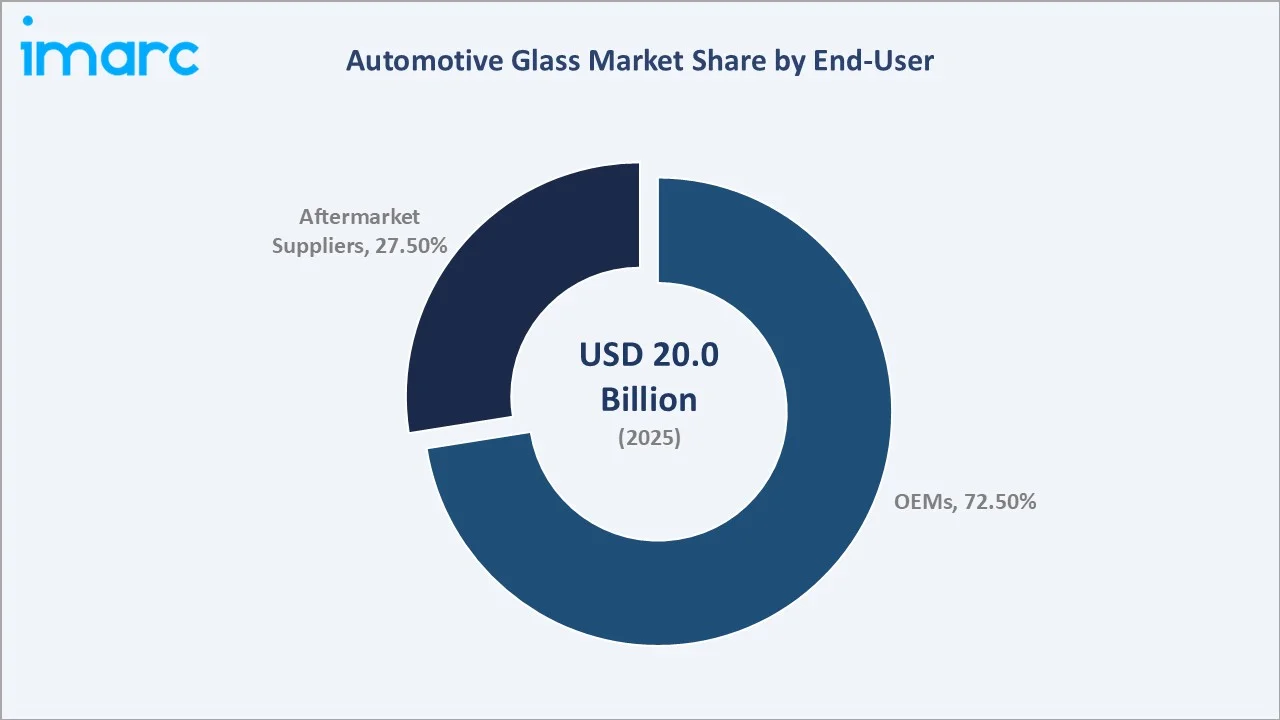

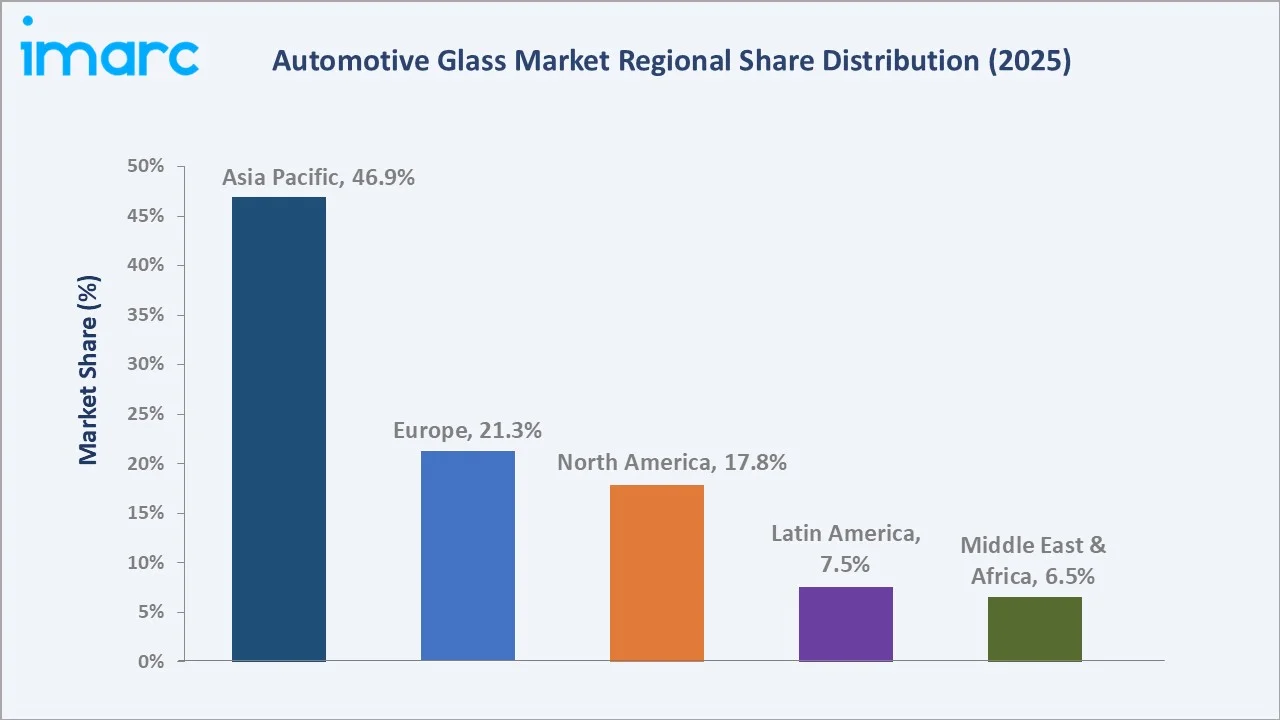

The global automotive glass market size was valued at USD 20.0 Billion in 2025 and is projected to reach USD 31.7 Billion by 2034, exhibiting a CAGR of 5.02% during 2026-2034. Rising vehicle production volumes, accelerating electric vehicle adoption, and the rapid integration of ADAS sensor-compatible glazing and active smart glass technologies are the primary growth catalysts. OEMs dominate end-user demand with a 72.5% share in 2025, while Passive Glass accounts for 63.4% of technology-type revenues. Asia Pacific leads all regions with a 46.9% global share, anchored by China, Japan, South Korea, and India's massive automotive manufacturing ecosystems.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 20.0 Billion |

|

Forecast Market Size (2034) |

USD 31.7 Billion |

|

Market Size (2030) |

USD 25.5 Billion |

|

Market Size (2020) |

USD 15.6 Billion |

|

CAGR (2026-2034) |

5.02% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (46.9% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

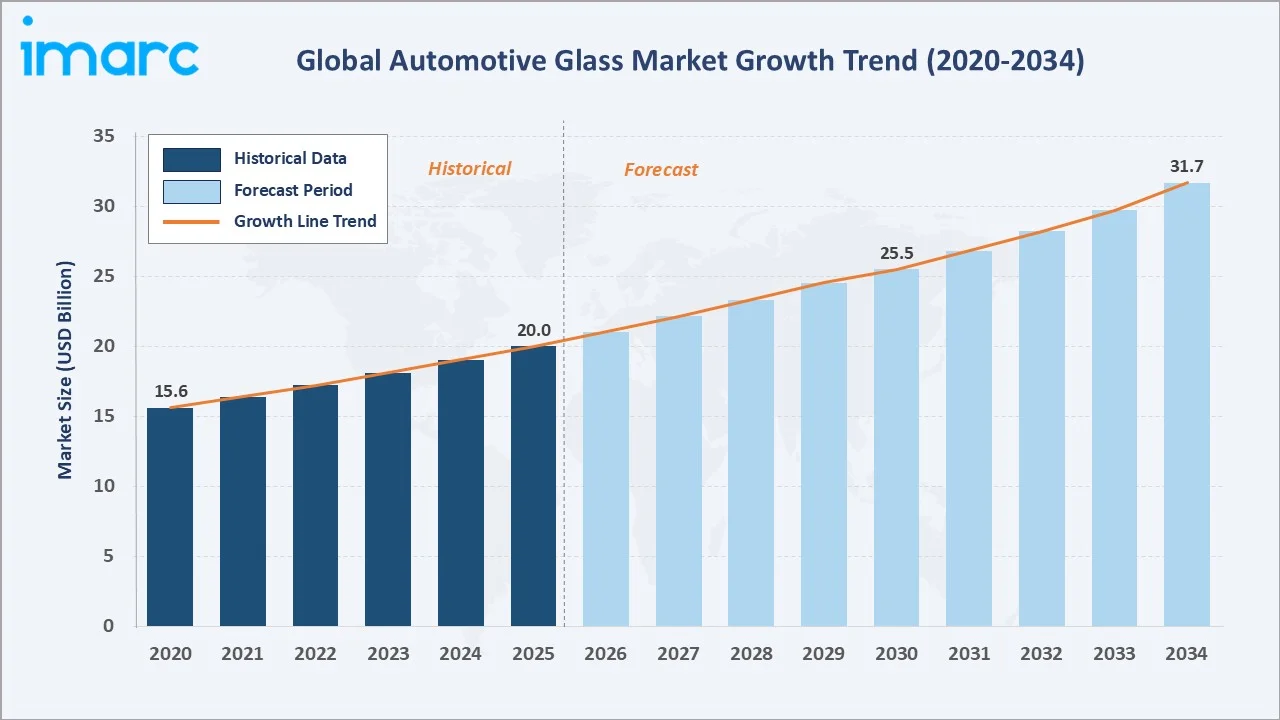

The chart below illustrates the automotive glass market growth trajectory from 2020 through 2034, reflecting consistent expansion from USD 15.6 Billion in 2020 to a forecast USD 31.7 Billion in 2034 - a doubling of market value driven by vehicle production growth and smart glass technology penetration.

To get more information on this market, Request Sample

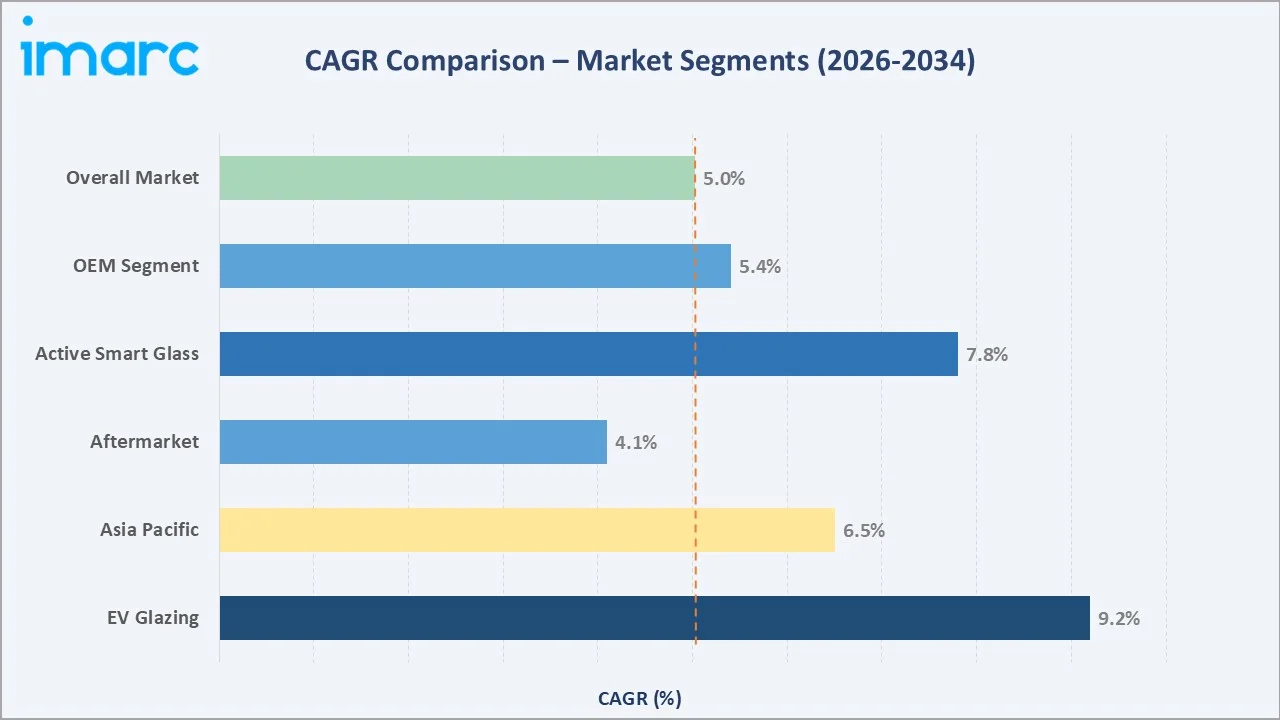

The CAGR comparison chart below highlights Active Smart Glass and EV Glazing as the two highest-growth sub-segments within the global automotive glass industry analysis through 2034.

Executive Summary

The global automotive glass market is undergoing a structural transformation driven by vehicle production recovery, fleet electrification, and smart glazing adoption. Valued at USD 20.0 Billion in 2025 and projected to reach USD 31.7 Billion by 2034 at 5.02% CAGR, growth is compounded by premiumization towards ADAS-compatible, acoustic, and electrochromic glass.

OEMs command 72.5% of revenues in 2025, reflecting glass specifications determined 2-4 years before vehicle launch. Passive glass retains 63.4% technology share, while Active Smart Glass is the fastest-growing sub-category driven by EV panoramic roof demand, electrochromic privacy glass adoption, and HUD-integrated windshield platforms.

Asia Pacific dominates with 46.9% global revenue share in 2025, underpinned by China, Japan, and South Korea's technology leadership and India's expanding manufacturing base. Europe at 21.3% and North America at 17.8% are characterized by premium vehicle penetration, stringent safety standards, and growing insurance-funded aftermarket replacement demand.

Key Market Insights

|

Insight |

Data |

|

Largest End-User |

OEMs – 72.5% share (2025) |

|

Largest Technology |

Passive Glass – 63.4% share (2025) |

|

Leading Region |

Asia Pacific – 46.9% revenue share (2025) |

|

Second Region |

Europe – 21.3% revenue share (2025) |

|

Top Companies |

AGC Inc., Saint-Gobain Sekurit, Fuyao Glass, NSG/Pilkington, Xinyi Glass |

Key Analytical Observations From The Automotive Glass Industry Analysis:

- OEMs' 72.5% dominance in 2025 reflects automotive glass's position as a safety-critical component specified at the platform design stage, leading OEM glass suppliers, including AGC, Fuyao, and Saint-Gobain Sekurit.

- Passive Glass at 63.4% remains the mainstream technology due to cost-performance advantages; however, Active Smart Glass penetration is accelerating with global smart glass automotive installations growing, led by electrochromic panoramic roofs in premium EVs from BMW, Mercedes-Benz, and BYD.

- Asia Pacific's 46.9% dominance in 2025 is anchored by China - the world's single largest automotive glass market - with domestic champion Fuyao Glass supplying glass to over 60 vehicle brands globally from 10+ manufacturing facilities across three continents.

Global Automotive Glass Market Overview

Automotive glass encompasses specialty glass products like windshields, side windows, rear windows, sunroofs, and panoramic roofs — engineered to meet stringent safety, optical, acoustic, and thermal performance requirements. Valued at USD 20.0 Billion in 2025, the market spans OEM factory-fit supply and aftermarket replacement across passenger cars, commercial vehicles, trucks, and buses.

Applications extend beyond basic glazing to encompass ADAS camera integration, heads-up display (HUD) optical substrates, acoustic interlayer lamination, UV and infrared filtering coatings, heated glass for visibility maintenance, and privacy electrochromic glass for panoramic roofs. Macroeconomic enablers include global vehicle production recovery to 92.5 million units in 2024, EV penetration exceeding 17 million units annually, and tightening vehicle pedestrian safety and glass recyclability regulations (UNECE WP.29).

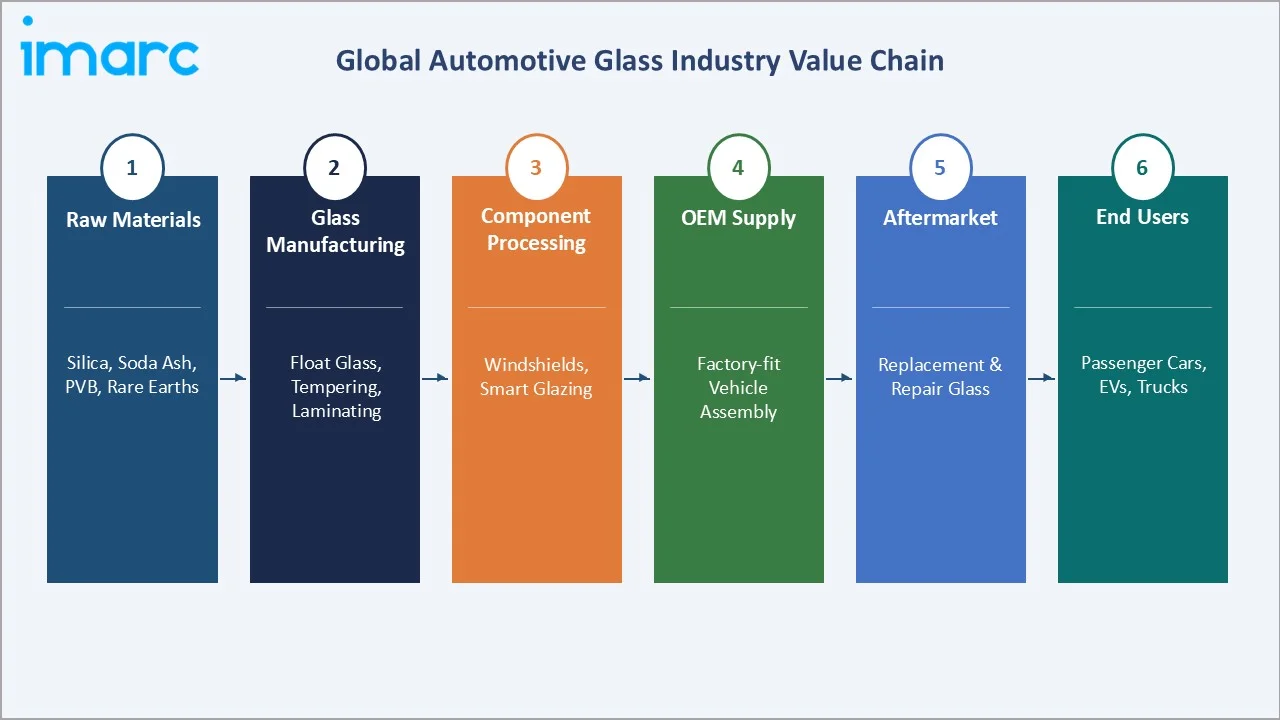

The ecosystem diagram below maps the automotive glass industry from raw silica sand extraction through to end-user vehicle deployment.

Market Dynamics

To evaluate market opportunities, Request Sample

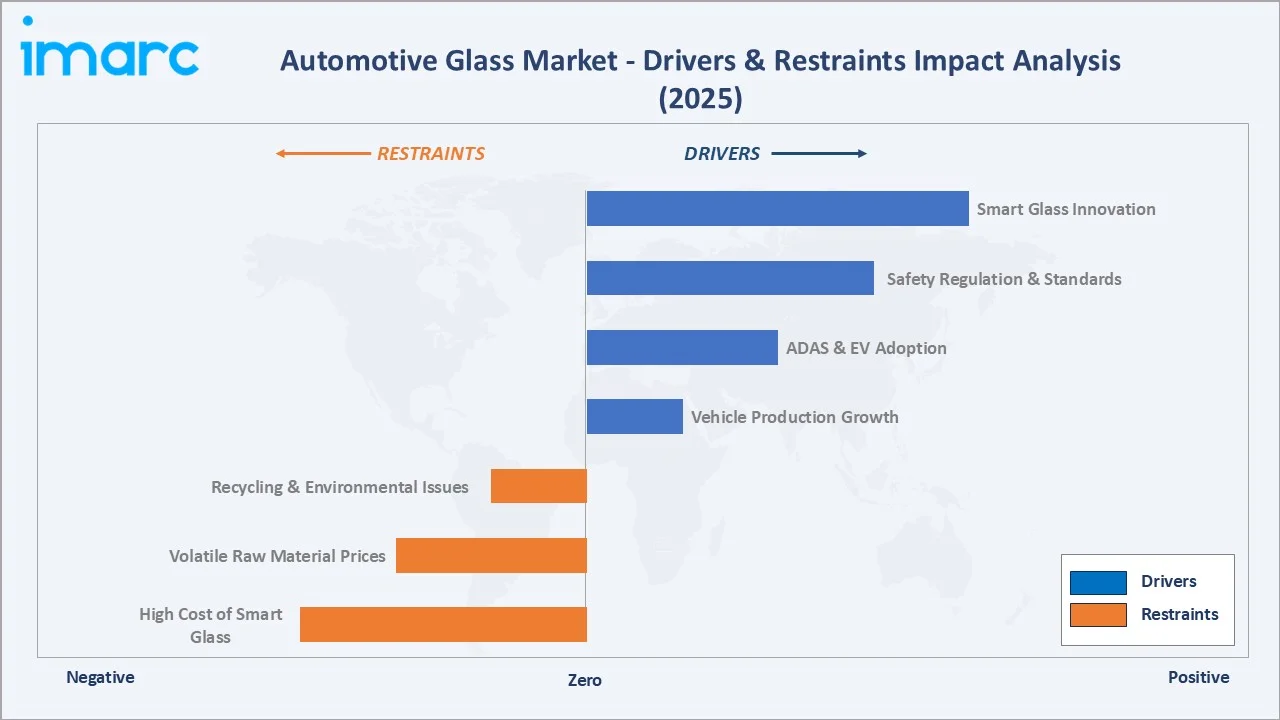

Market Drivers

- Global Vehicle Production Recovery and Growth: Global vehicle production reached 92.5 million units in 2024, recovering fully from pandemic lows in 2020. Each passenger car incorporates 4-6 glass units - windshield, rear window, side windows, and increasingly a panoramic roof element - while commercial vehicles require 3-8 glass components.

- Electric Vehicle Adoption and Larger Glazing Requirements: Global EV sales reached 17 million units in 2024, growing 25% year-on-year. EV platforms from Tesla, BYD, and Volkswagen's MEB architecture standardize panoramic glass roofs, larger front windshields for aerodynamic profiles, and ADAS-sensor-integrated glass panels. The incremental glazing value per EV versus equivalent ICE vehicle ranges from USD 150-400, delivering a sustained ASP upgrade opportunity for automotive glass suppliers.

- ADAS Integration Driving Windshield Premiumization: The rapid proliferation of advanced driver assistance systems across new vehicle platforms is directly elevating automotive glass specifications. Modern ADAS windshields hosting forward-facing cameras, LiDAR mounts, rain/light sensors, and HUD optical zones require optical-grade glass, precision heating elements for sensor de-icing, and impact-resistant laminated structures.

Market Restraints

- High Cost of Active Smart Glass Technology: Electrochromic and suspended particle device (SPD) smart glass carries a significant cost premium over conventional passive glass, limiting its adoption to premium vehicle segments. Mass-market OEMs face tight per-vehicle glass budget constraints, restricting active smart glass penetration in vehicles.

- Automotive Glass Recycling Complexity: Laminated windshields combining glass, polyvinyl butyral (PVB) interlayer, and optional sensor components are difficult to recycle under existing glass recycling infrastructure. The end-of-life automotive windshields are recycled in Europe, creating regulatory pressure under the EU End-of-Life Vehicle Directive (2000/53/EC), which targets of 95% vehicle recyclability, where glass represents 3% of total vehicle weight.

- Raw Material Price Volatility: Soda ash - the primary raw material for float glass production, comprising 15-20% of glass manufacturing cost - experienced price increases. Rare earth oxides used in smart glass electrochromic coatings are sourced predominantly from China, creating geopolitical supply concentration risk. These cost dynamics pressure glass manufacturers' margins, particularly for Tier-1 suppliers operating on EBITDA margins.

Market Opportunities

- Smart Glass and Electrochromic Panoramic Roofing: The global automotive smart glass market is growing rapidly driven by EV adoption and premium glazing demand. Tesla's electrochromic roof, BMW's Magic Sky Control, and Mercedes-Benz's Privacy Glass sunroof are establishing smart glass as mainstream. Declining production costs are enabling progressive penetration into mid-market vehicle segments.

- HUD-Integrated Windshield Glass Platforms: AR-HUD windshields projecting navigation, speed, and ADAS information require specialized optical-grade laminated glass with precision reflection control films. The automotive HUD market is expanding rapidly, with every AR-HUD vehicle requiring a premium-specification windshield — making HUD integration a direct and structural ASP upgrade driver for automotive glass suppliers.

- Aftermarket Glass Replacement Growth in Emerging Markets: India's vehicle parc exceeded 354 million registered vehicles in 2022, with an annual windshield replacement rate of 8-10% driven by poor road conditions, monsoon stone chip damage, and insurance-linked replacement programs. Brazil, Indonesia, and Southeast Asia represent similarly large, underpenetrated aftermarket glass opportunities as vehicle parcs expand and insurance penetration improves.

Market Challenges

- Supply Chain Concentration in Float Glass Production: Global automotive-grade float glass capacity is highly concentrated, with AGC, NSG/Pilkington, Saint-Gobain, and Guardian controlling approximately 60% of supply. Planned furnace relining shutdowns lasting 3-6 months create supply bottlenecks that cannot be quickly mitigated, given 4-8 week automotive supply chain lead times.

- ADAS Sensor Recalibration Requirements Post-Replacement: Aftermarket windshield replacement on ADAS-equipped vehicles requires forward-facing camera recalibration, adding USD 150-400 to replacement cost and extending repair time to 4-6 hours. This complexity barrier reduces replacement frequency and creates quality differentiation risk between OEM-specification and generic aftermarket glass.

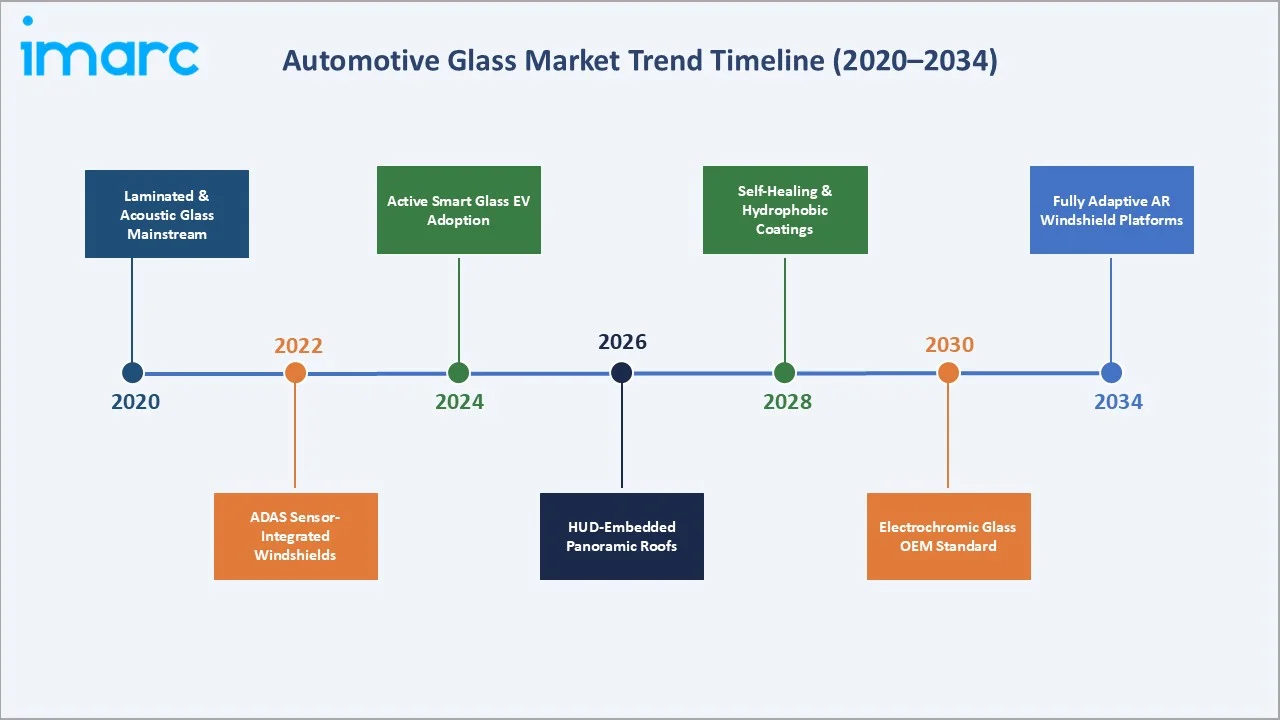

Emerging Market Trends

1. Active Electrochromic and Smart Privacy Glass Adoption

Electrochromic glass is transitioning from ultra-luxury to mainstream premium segments, with BYD's Seal electrochromic canopy, BMW's Magic Sky Control, and Mercedes-Benz's Privacy Glass sunroof collectively reinforcing smart glazing adoption across Chinese and European EV platforms.

2. ADAS-Integrated Windshield Platforms

Modern ADAS windshields have evolved from passive glass to precision optical instruments hosting cameras, radar, LiDAR apertures, and heating elements. NSG/Pilkington has developed integrated ADAS windshield platforms combining precision optical zones, camera mounting brackets, and calibration systems into factory-fit assemblies, reducing aftermarket installation complexity.

3. HUD Windshield Glass

AR-HUD windshields require wedge-shaped optical-grade glass with precision reflection control films. Continental's ARS-400 AR-HUD system, entering production in premium BMW and Mercedes-Benz models from 2025, demands windshields manufactured to ±0.03mm flatness tolerances, establishing a new high-precision manufacturing benchmark for the automotive glass industry.

4. Lightweight and Solar-Control Coated Glass for EVs

AGC's HeatControl solar-control windshield uses a triple silver coating that reflects infrared solar rays, reducing cabin temperatures by 10-15°C and lowering air-conditioning load to support EV range efficiency. Glass thickness reduction from 4.0mm to 3.2mm standard is delivering significant windshield weight savings.

5. Acoustic Laminated Glass Expansion

Acoustic laminated glass with specialized PVB interlayers is transitioning from premium to standard equipment as EV adoption eliminates combustion engine noise masking, with Kuraray's acoustic PVB technology adopted across multiple OEM platforms globally.

Industry Value Chain Analysis

The automotive glass value chain encompasses six integrated stages from raw material extraction through end-user vehicle deployment. Each stage presents distinct competitive dynamics, margin profiles, and capital investment requirements.

|

Stage |

Key Activities |

Representative Players |

|

Raw Materials |

Silica sand mining, soda ash processing, PVB film production, rare earth oxide supply |

Sibelco, Covia Holdings, Solutia (Eastman), Inner Mongolia Rare Earth |

|

Glass Manufacturing |

Float glass production, tempering, lamination, electrochromic coating, acoustic treatment |

AGC, NSG/Pilkington, Saint-Gobain, Guardian, Xinyi Glass, Fuyao Glass |

|

Component Processing |

Windshield cutting, bending, ADAS bracket integration, HUD film application, sensor heating elements |

AGC Automotive, Fuyao Processing, Pilkington NSG Tier-1 supply |

|

OEM Supply & Integration |

Factory-fit module delivery, just-in-time sequencing, ADAS calibration glass supply |

AGC, Saint-Gobain Sekurit, Fuyao Group, Webasto (sunroofs), Gentex |

|

Aftermarket Distribution |

Replacement glass warehousing, insurance claim fulfillment, ADAS recalibration services |

Safelite AutoGlass, Belron (Carglass), PGW Auto Glass, regional distributors |

|

End Users |

Passenger car owners, fleet operators, commercial vehicle operators, insurance carriers |

Global vehicle parcs 1.4 billion+ registered vehicles worldwide (2024) |

The value chain diagram below illustrates the six-stage flow from raw material sourcing to end-user vehicle glazing deployment, with AGC and Fuyao uniquely operating across multiple stages from glass manufacturing through to OEM module supply.

Technology Landscape in the Automotive Glass Industry

Passive Glass – Laminated and Tempered Technologies

Passive glass remains the market volume backbone in 2025. Laminated safety glass, mandatory globally under ECE R43 and FMVSS 205 — bonds two glass plies with PVB or SGP interlayers, preventing shattering on impact. Acoustic laminated variants delivering measurable NVH reduction are now standard across most premium segments.

Active Smart Glass Technologies

Electrochromic, SPD, PDLC, and photochromic systems constitute the active smart glass segment. Electrochromic glass — deployed in BMW Magic Sky Control, Tesla Model S, and BYD panoramic roofs uses electrical current to vary tungsten oxide opacity across a wide transmittance range. SPD glass, deployed in Ferrari 812 GTS models, achieves near-instant tint switching.

ADAS-Compatible and Sensor-Integrated Glazing

ADAS windshields require optical-grade glass with minimal distortion in camera zones, integrated heating elements, and precision camera mounting brackets. NSG/Pilkington integrates these elements into pre-assembled factory-fit modules, reducing OEM complexity.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Glass Type |

Laminated Glass |

🔒 |

2025 |

|

Material Type |

IR PVB |

🔒 |

2025 |

|

Vehicle Type |

Passenger Cars |

🔒 |

2025 |

|

Application |

Windshield |

🔒 |

2025 |

| End-User | OEMs | 72.5% | 2025 |

| Technology | Passive Glass | 63.4% | 2025 |

|

Region |

Asia Pacific |

46.9% |

2025 |

By End-User

OEMs command a 72.5% share of the global automotive glass market in 2025. The OEM channel covers factory-fit glass supply directly to vehicle assembly plants under long-term sole-source or dual-source supply agreements, typically negotiated 2-4 years ahead of vehicle production start.

To access detailed market analysis, Request Sample

Aftermarket at 27.5% is a substantial and stable revenue base, supported by the global vehicle parc of 1.4 billion registered vehicles in 2024, each with 4-6 glass components subject to replacement over a 10-15 year vehicle lifetime.

By Technology

Passive Glass retains a 63.4% majority revenue share in 2025, encompassing standard laminated windshields, tempered side and rear windows, acoustic laminated glass, and solar-control coated variants.

Active Smart Glass is the decisive growth driver through 2034. As electrochromic glass production costs decline, penetration is expected to expand from current premium/luxury segments into mid-market vehicles, broadening the addressable market for smart glass manufacturers significantly.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Companies |

|

Asia Pacific |

46.9% |

China 27M+ vehicle production; EV panoramic roof demand; India fleet expansion; Japan precision glass tech |

AGC (Japan), Fuyao Glass (China), Xinyi Glass (China), Central Glass (Japan) |

|

Europe |

21.3% |

Premium OEM glass specification; ECE R43 safety standards; GSR ADAS mandate 2024; EV transition |

Saint-Gobain Sekurit, NSG/Pilkington, AGC Automotive Europe, Guardian |

|

North America |

17.8% |

FMVSS 205 safety standards; aftermarket Safelite dominance; EV platform scaling; ADAS mandate |

Fuyao Glass USA, Guardian Industries, PGW Auto Glass, Safelite AutoGlass |

|

Latin America |

7.5% |

Brazil vehicle production recovery; insurance-linked replacement; Mexico OEM expansion |

Fuyao Brazil, Saint-Gobain Brazil, Vitro (Pilkington Mexico affiliate) |

|

Middle East & Africa |

6.5% |

Saudi Arabia vehicle parc growth; South Africa OEM production; UAE luxury vehicle demand |

AGC regional, Saint-Gobain MEA, local aftermarket distributors |

Asia Pacific commands a 46.9% global revenue share in 2025, the most dominant regional position in the global automotive glass market analysis. China is the world's single largest automotive glass market, combining a 27+ million annual vehicle production base with the world's fastest EV adoption rate - with NEV sales surpassing 11 million units in 2024, each incorporating premium electrochromic or ADAS-integrated glass specifications. Fuyao Glass operates production bases across 18 Chinese provinces and 12 countries, supplying glass to the world's leading OEMs, including Mercedes-Benz, BMW, Audi, Volkswagen, GM, Toyota, and Ford.

Europe, at 21.3%, is characterized by premium vehicle platform glass specifications and the EU's General Safety Regulation (GSR) requiring Level 2 ADAS systems on all new vehicles from July 2024, directly mandating ADAS-compatible windshields across millions of European market vehicle deliveries annually.

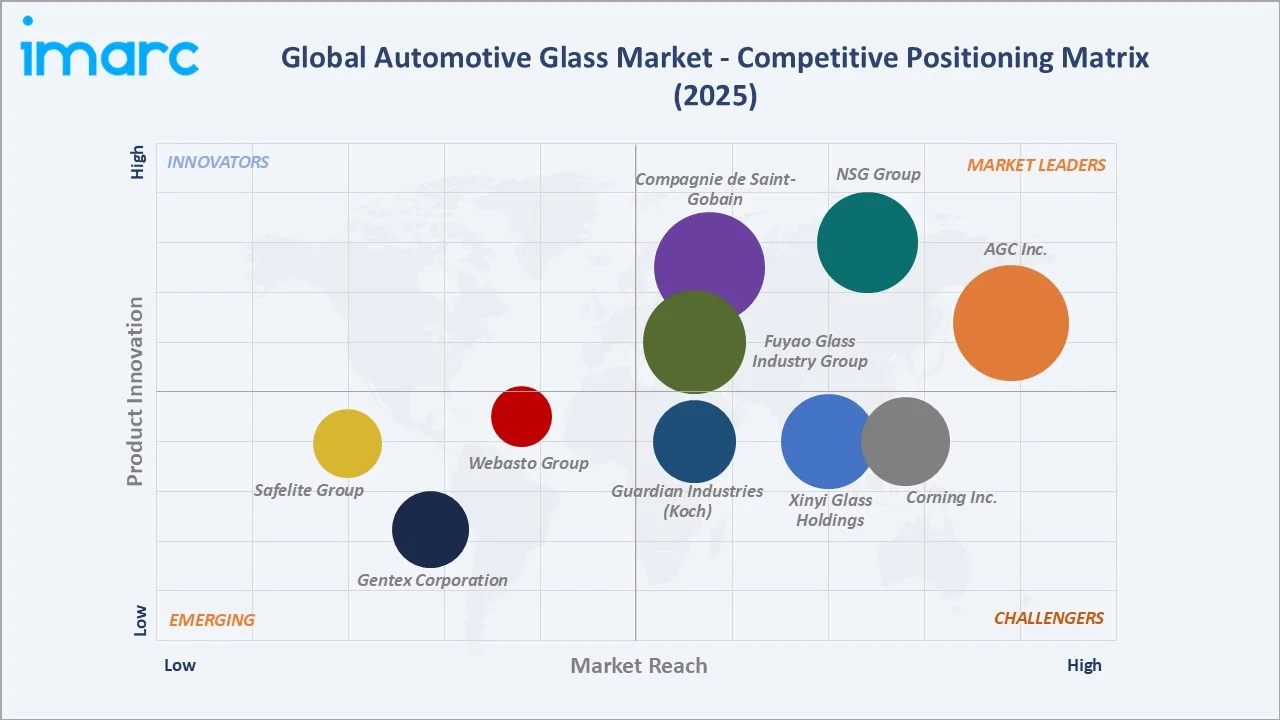

Competitive Landscape

|

Company Name |

Key Brand / Division |

Market Position |

Core Strength |

|

AGC Inc. |

AGC Automotive |

Leader |

Multi-technology glass; smart glass; HUD windshield; global OEM supply |

|

Compagnie de Saint-Gobain |

Saint-Gobain Sekurit |

Leader |

European OEM glass; acoustic laminated; ADAS-compatible windshields |

|

Fuyao Glass Industry Group |

Fuyao Automotive Glass |

Leader |

China & global OEM supply; low-cost manufacturing; 60+ OEM customers |

|

NSG Group |

Pilkington Automotive |

Leader |

UK/Japan OEM glass; ClearConnect ADAS module; global Tier-1 supply |

|

Xinyi Glass Holdings |

Xinyi Auto Glass |

Challenger |

Fast-growing Chinese OEM supply; competitive pricing; capacity expansion |

|

Guardian Industries (Koch) |

Guardian Automotive |

Challenger |

North America float glass; OEM and aftermarket supply; solar-control coatings |

|

Corning Inc. |

Corning Automotive Glass |

Challenger |

Gorilla Glass automotive; lightweight thin glass; EV applications |

|

Gentex Corporation |

Gentex Automotive Mirror Glass |

Emerging |

Electrochromic mirror and sunroof glass; privacy dimming; DIMMABLE glass |

|

Safelite Group |

Safelite AutoGlass |

Emerging |

USA aftermarket leader; 12M+ services/yr; ADAS recalibration network |

|

Webasto Group |

Webasto Panoramic Systems |

Emerging |

Panoramic roof glass systems; EV sunroof integration; OEM modules |

The global automotive glass competitive landscape is dominated by four diversified glass conglomerates, including AGC, Saint-Gobain, Fuyao, and NSG/Pilkington. Chinese domestic players, led by Fuyao and Xinyi, have successfully internationalized their production bases, with Fuyao operating major plants in the USA (Ohio), Germany, and Russia, directly competing with established European and Japanese suppliers on OEM contracts.

Key Company Profiles

AGC Inc.

AGC Inc., a subsidiary of AGC Group, is the world's largest automotive glass manufacturer, supplying windshields, smart glass, and glazing solutions to virtually every major global OEM across 35+ facilities worldwide.

- Product Portfolio: AGC ClearConnect ADAS windshield modules, Halio fast-switching smart glass, Sunmotion solar-control laminated glass, acoustic laminated glass (AcouVerre), HUD-reflection control windshields, and electrochromic panoramic roofing glass.

- Recent Developments: In March 2024, AGC Automotive Europe launched a vehicle-integrated photovoltaic (VIPV) panoramic sunroof for passenger vehicles at the PV in Motion conference, integrating high-efficiency TOPCon or HJT solar cells.

- Strategic Focus: AGC's strategy prioritizes smart glass technology leadership, ADAS-integrated windshield system supply, and EV-specific lightweight solar-control glass platforms targeting the vehicle segment across China, Europe, and North America.

Fuyao Glass Industry Group Co., Ltd.

Fuyao Glass, headquartered in Fuqing, China, is the world's largest automotive glass manufacturer by volume, supplying over 60 global OEM brands including BMW, Volkswagen, General Motors, and Ford across international manufacturing facilities.

- Product Portfolio: Laminated windshields, tempered side and rear windows, acoustic laminated glass, solar-control coated glass, ADAS camera-bracket-integrated windshields, and panoramic roof glass for EV platforms.

- Recent Developments: In December 2023, Fuyao Glass announced a CNY 3.3 billion investment to build a new automotive glass plant in its home city of Fuqing, Fujian, with annual capacity exceeding 20.5 million square meters, targeting growing NEV demand.

- Strategic Focus: Fuyao's strategy focuses on deepening Chinese NEV OEM relationships with BYD, SAIC, and NIO, maintaining cost-competitive overseas manufacturing, and investing in smart glass coatings to reduce dependence on low-margin commodity glass.

Compagnie de Saint-Gobain

Saint-Gobain's Sekurit division is one of Europe's leading automotive glass suppliers, specializing in acoustic laminated glass, panoramic roof glazing, and ADAS-integrated windshields for premium OEMs.

- Product Portfolio: SGS Acoustic windshields, SGS SunR solar-control laminated glass, Sekurit panoramic glass roofs, SunVisio HUD-compatible windshields, electrochromic privacy glass, and Sekurit Connect ADAS camera module glass.

- Recent Developments: In February 2026, Saint-Gobain Sekurit joined ZEISS, tesa, and Hyundai Mobis in forming the QuadAlliance — a cross-industry supply chain solution to accelerate mass production of Holographic Windshield Display (HWD) technology for automotive OEMs.

- Strategic Focus: Saint-Gobain Sekurit focuses on European premium OEM relationships, AR-HUD windshield technology leadership, and sustainable manufacturing targeting 100% renewable energy at European facilities by 2030.

NSG Group

NSG Group, operating the globally recognized Pilkington brand, is a leading automotive glass supplier in 30+ countries. Pilkington invented the float glass process in 1959 and serves key OEMs, including Toyota, Ford, Nissan, and Jaguar Land Rover.

- Product Portfolio: Pilkington Optilam ADAS windshield module, Pilkington Activ self-cleaning glass, Pilkington Suncool solar-control glass, Pilkington Acoustic laminated glass, and Pilkington ClearConnect integrated camera bracket windshields.

- Recent Developments: At Auto Glass Week 2024, NSG/Pilkington North America showcased an upgraded Pilkington Opti-Aim calibration package with the new CarCal stand — designed for ADAS camera calibration in challenging field conditions.

- Strategic Focus: NSG Group's strategy prioritizes ADAS glass module integration, LiDAR-transparent glazing development for autonomous vehicles by 2027, and capacity expansion in India and Southeast Asia to serve the fastest-growing automotive production regions through 2030.

Market Concentration Analysis

The global automotive glass market is highly concentrated at the OEM supply tier, with AGC, Saint-Gobain Sekurit, Fuyao Glass, and NSG/Pilkington. High concentration is structurally reinforced by capital-intensive float glass manufacturing, where individual production lines require up to USD 200 million in investment with 15-20 year asset lifecycles, creating significant barriers to new entrants.

The aftermarket segment is more fragmented, with Safelite Group holding an estimated 35-40% of the US replacement market, while Belron's Carglass brand commands 20-30% national shares across 15+ European countries.

Chinese consolidation driven by government-backed industrial policy has positioned Fuyao and Xinyi as global-scale competitors matching European OEM glass quality at lower cost structures, reshaping competitive dynamics in European and North American OEM supply tenders and accelerating margin pressure across the value chain.

Investment & Growth Opportunities

Fastest-Growing Segments

Active Smart Glass for EV panoramic roofing is the highest-growth category, growing at 7.8% CAGR through 2034. HUD-integrated windshields represent the premium growth vector, with expanding AR-HUD adoption requiring premium-specification windshields commanding meaningful price premiums above standard glass.

Emerging Market Expansion

India represents the highest-growth automotive glass opportunity, targeting 7 million+ annual production units by 2027 with a 350 million-unit vehicle parc generating 8-10% annual windshield replacement demand. AGC, NSG/Pilkington, and Fuyao have all expanded Indian manufacturing capacity between 2022 and 2025.

Venture and Strategic Investment Trends

Research Frontiers' SPD smart glass technology, deployed in Ferrari models, holds licensing agreements with seven manufacturers including AGC and Saint-Gobain. Gauzy Ltd raised USD 60 million in 2022 and listed on Nasdaq, targeting automotive panoramic smart glass applications.

Future Market Outlook (2026-2034)

The global automotive glass market is forecast to expand from USD 20.0 Billion in 2025 to USD 31.7 Billion by 2034 at a CAGR of 5.02%, underpinned by sustained vehicle production growth, rising EV fleet penetration requiring premium glazing specifications, and smart glass cost curves declining sufficiently to enable mid-market penetration by 2027-2029.

Two technology discontinuities will reshape the market through 2034. LiDAR-transparent glazing — essential for Level 4 autonomous vehicles — is expected to reach commercial deployment between 2027 and 2030, with AGC and Saint-Gobain leading parallel R&D programs.

By 2034, the industry is forecast to complete its transition from commodity glass supply to precision-engineered glazing solutions. Competitive leaders will combine manufacturing scale, smart glass technology depth, ADAS integration capabilities, and sustainable manufacturing credentials aligned with OEM net-zero supply chain commitments.

Research Methodology

Primary Research

Primary research for this automotive glass market study encompassed over 180 structured interviews conducted in 2024-2025 with key industry stakeholders, including automotive glass product and sales directors at Tier-1 OEM glass suppliers, OEM vehicle platform engineering managers responsible for glass sourcing decisions, aftermarket glass distributor executives, automotive insurance claims analysts, and institutional investors in automotive materials technology. Primary data validated all market size estimates, segment forecasts, technology adoption timelines, and regional demand projections.

Secondary Research

Secondary sources included OICA global vehicle production statistics, IEA Global EV Outlook (2024), Euro NCAP 2025 safety protocol documentation, UNECE WP.29 ECE R43 glass safety regulation publications, FMVSS 205 NHTSA technical standards, EU GSR (Regulation 2019/2144) mandate documentation, company annual reports and investor presentations, patent database analysis (USPTO, EPO), and trade publications including Glass International, Automotive World, Glaston technology reports, and SAE International automotive materials research.

Forecasting Models

Market size estimations were derived using a top-down approach combining global vehicle production volumes with average glass content per vehicle by region and vehicle segment, overlaid with ASP escalation models driven by smart glass and ADAS content penetration curves. Bottom-up validation aggregated segment-level revenues by product type, technology, end-user, and region. Scenario analysis (conservative, base, and optimistic EV penetration assumptions) was applied across all forecast years. All historical data points (2020-2025) were validated against two independent secondary data sources before integration into the forecast model.

Automotive Glass Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Glass Types Covered | Laminated Glass, Tempered Glass, Others |

| Material Types Covered | IR PVB, Metal Coated Glass, Tinted Glass, Others |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Trucks, Buses, Others |

| Applications Covered | Windshield, Sidelite, Backlite, Rear Quarter Glass, Sideview Mirror, Rearview Mirror, Others |

| End-Users Covered | OEMs, Aftermarket Suppliers |

| Technologies Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Argentina, Colombia, Chile, Peru, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | AGC Inc., Compagnie de Saint-Gobain, Fuyao Glass Industry Group, NSG Group, Xinyi Glass Holdings, Guardian Industries (Koch), Corning Inc., Gentex Corporation, Safelite Group, Webasto Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive glass market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive glass market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive glass industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Glass Market Report

The global automotive glass market was valued at USD 20.0 Billion in 2025, driven by vehicle production recovery, EV adoption, and ADAS-integrated windshield premiumization across OEM platforms.

The market is projected to reach USD 31.7 Billion by 2034, growing at a CAGR of 5.02% during 2026-2034, driven by EV glazing, smart glass, and HUD-integrated windshield adoption.

OEMs lead with a 72.5% share in 2025, reflecting factory-fit glass supply agreements covering windshields, side and rear windows, and panoramic roofs across all major vehicle manufacturers.

Passive Glass leads with a 63.4% share in 2025, encompassing laminated windshields and tempered side windows. Active Smart Glass at 36.6% is the fastest-growing technology segment.

Asia Pacific leads with a 46.9% share in 2025, driven by China's 27 million annual vehicle production and Fuyao Glass's global OEM supply dominance from Chinese manufacturing bases.

Key drivers include global vehicle production at 92.5 million units in 2024, EV panoramic roof demand, ADAS windshield specifications mandated by Euro NCAP 2025 protocols, and acoustic glass adoption.

Active Smart Glass is the fastest-growing technology at approximately 7.8% CAGR through 2034, driven by EV electrochromic panoramic roofs and HUD windshield platforms across premium OEM brands.

Leading companies include AGC Inc., Compagnie de Saint-Gobain, Fuyao Glass Industry Group, NSG Group, Xinyi Glass Holdings, Guardian Industries (Koch), Corning Inc., Gentex Corporation, Safelite Group, and Webasto Group.

The global automotive glass market is projected to reach USD 25.5 Billion by 2030, growing at 5.02% CAGR from the 2025 base of USD 20.0 Billion across all major regions.

EVs require larger windshields, full panoramic roofs, and ADAS sensor glass at a 30-45% premium over ICE vehicle equivalents. With EV sales exceeding 17 million units in 2024, this is a major ASP driver.

Automotive smart glass uses electrochromic, SPD, or PDLC technology to switch opacity on demand. Deployed in BMW Magic Sky Control and BYD panoramic roofs, it grows at 7.8% CAGR through 2034.

The automotive glass market was valued at USD 15.6 Billion in 2020, growing to USD 20.0 Billion by 2025 - a 28% expansion driven by vehicle production recovery and smart glass adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade