Automotive Infotainment Market Size, Share, Trends and Forecast by Product Type, Vehicle Type, Operating System, Installation Type, Sales Channel, Technology, Connectivity, and Region, 2026-2034

Global Automotive Infotainment Market Size, Share, Trends & Forecast (2026-2034)

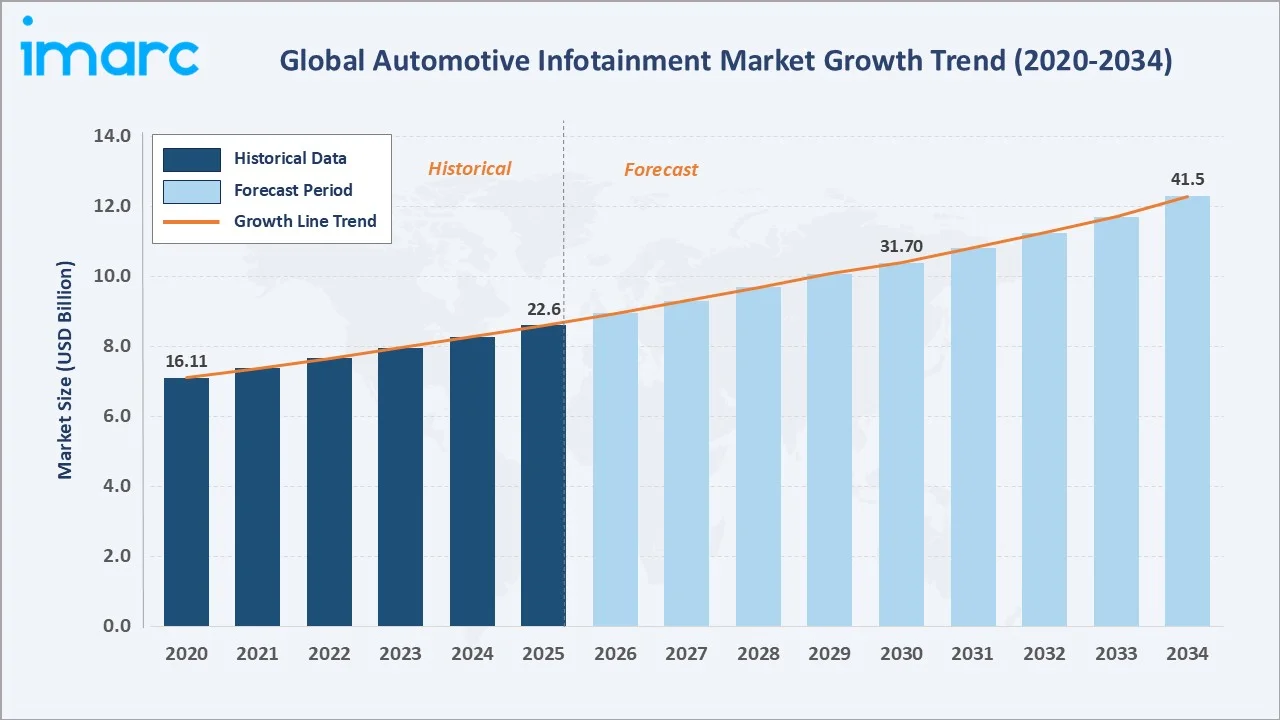

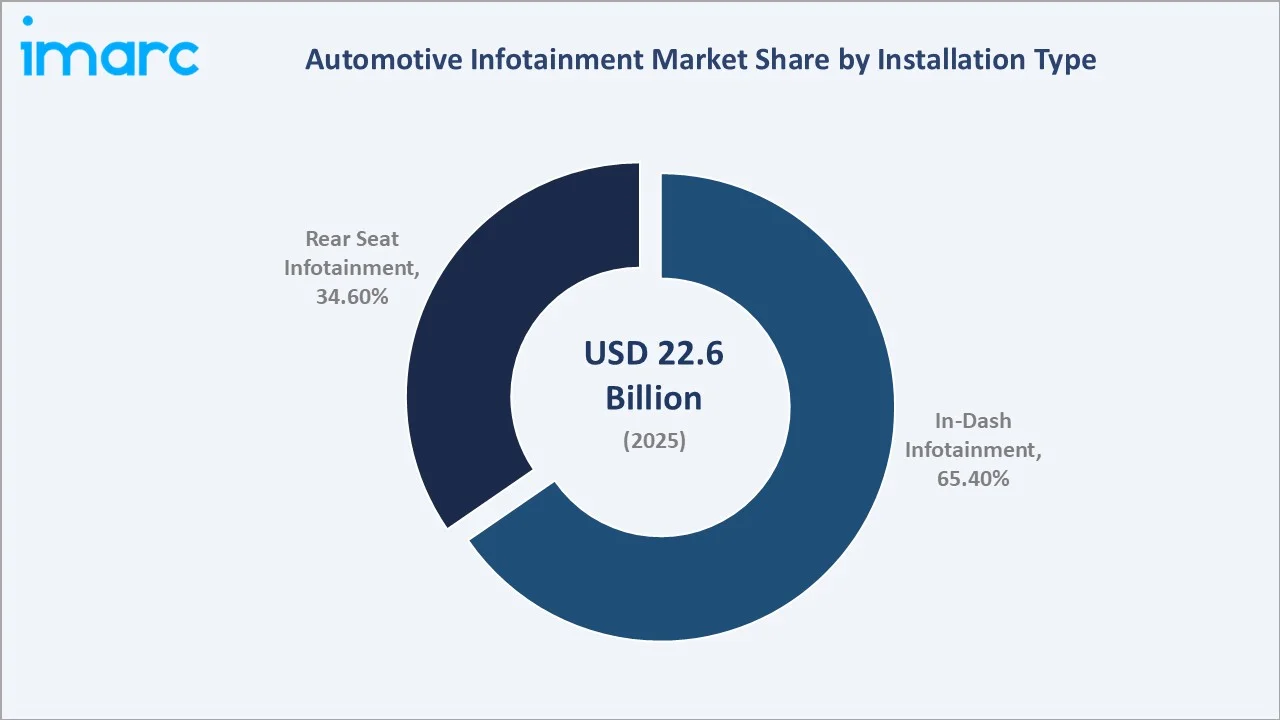

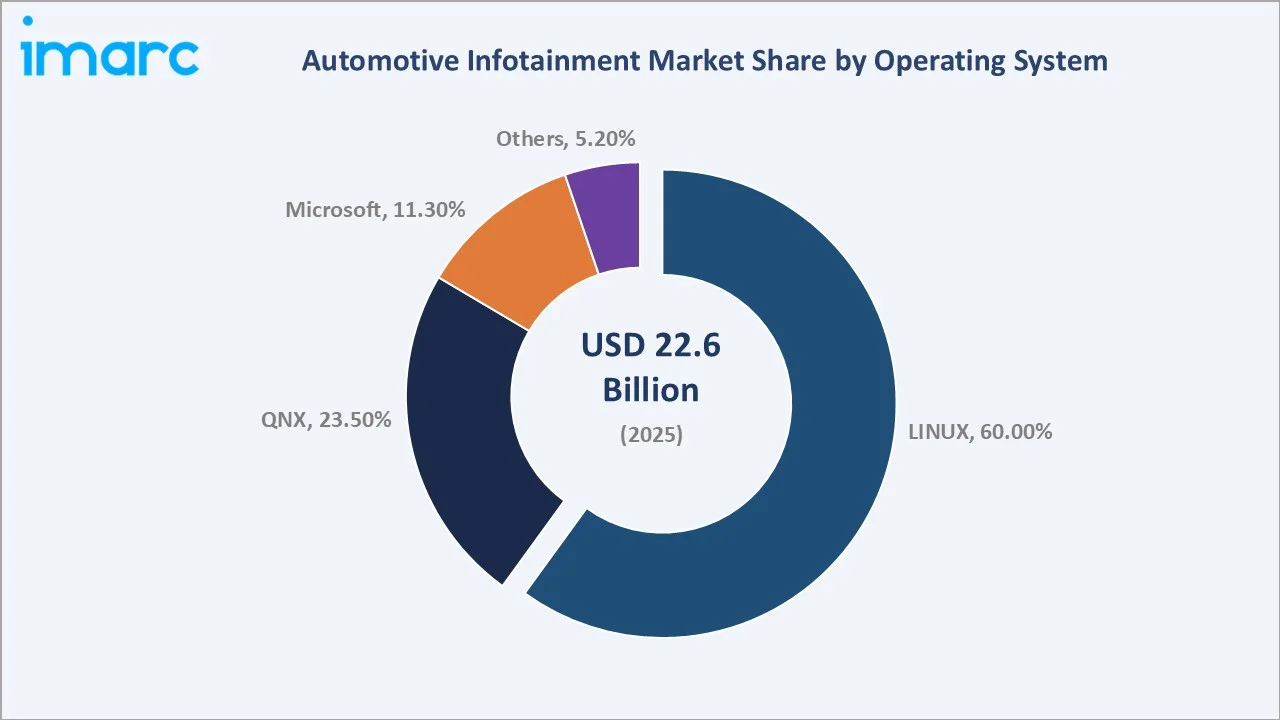

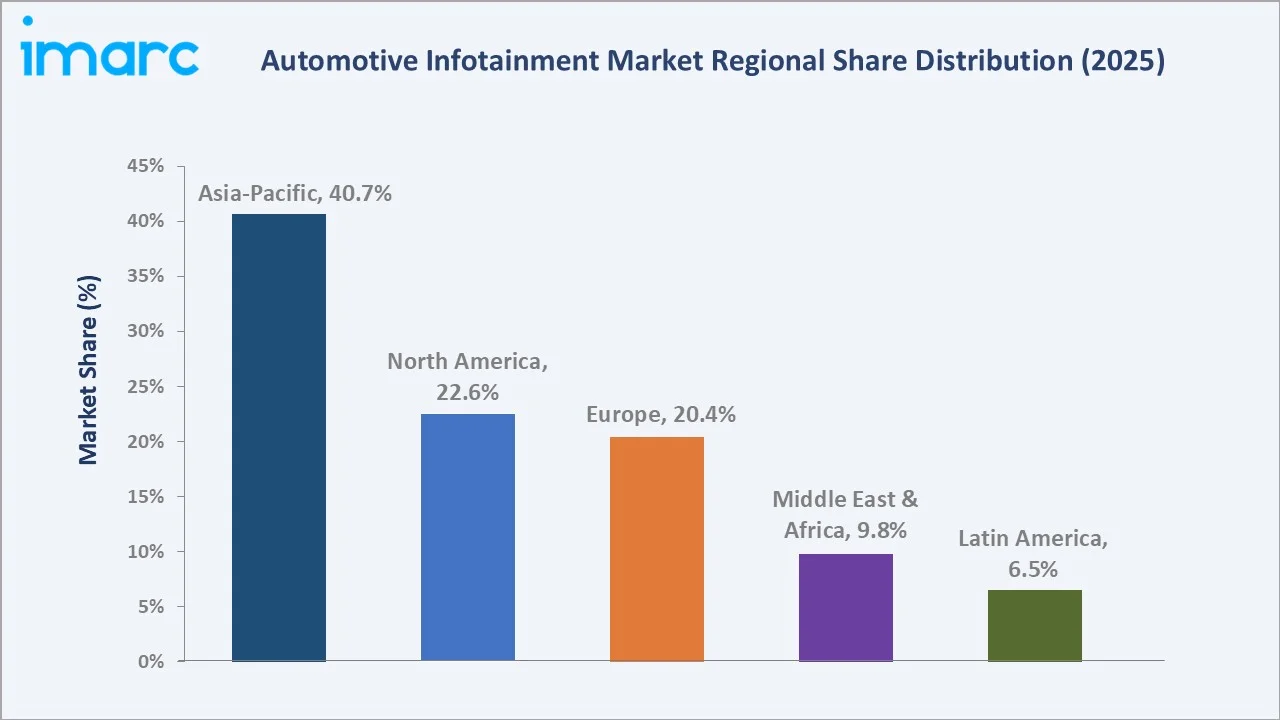

The global automotive infotainment market size was valued at USD 22.6 Billion in 2025 and is projected to reach USD 41.5 Billion by 2034, exhibiting a CAGR of 7.00% during the forecast period 2026-2034. Surging consumer demand for connected, feature-rich in-vehicle experiences, the rapid proliferation of electric vehicles, with electric car sales topped 17 million worldwide in 2024, expanding 5G vehicle connectivity, and deep integration of AI voice assistants and ADAS technologies are driving the automotive infotainment market growth. In-Dash Infotainment leads installation type at 65.4% in 2025, while LINUX dominates the operating system segment at 60.0%. Asia-Pacific accounts for 40.7% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 22.6 Billion |

|

Forecast Market Size (2034) |

USD 41.5 Billion |

|

CAGR (2026-2034) |

7.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (40.7% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~8.7%) |

|

Leading Installation Type |

In-Dash Infotainment (65.4%, 2025) |

|

Leading Operating System |

LINUX (60.0%, 2025) |

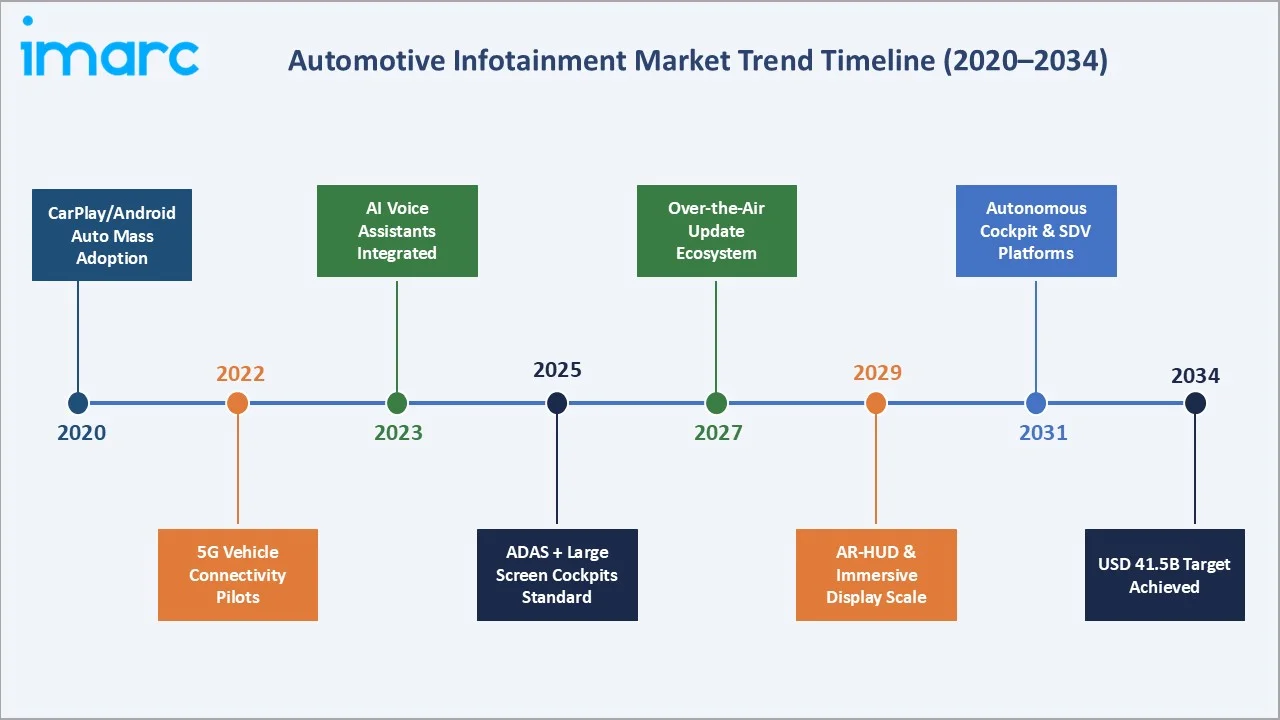

The global automotive infotainment market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by EV proliferation, software-defined vehicle architectures, and 5G-enabled connected services.

To get more information on this market, Request Sample

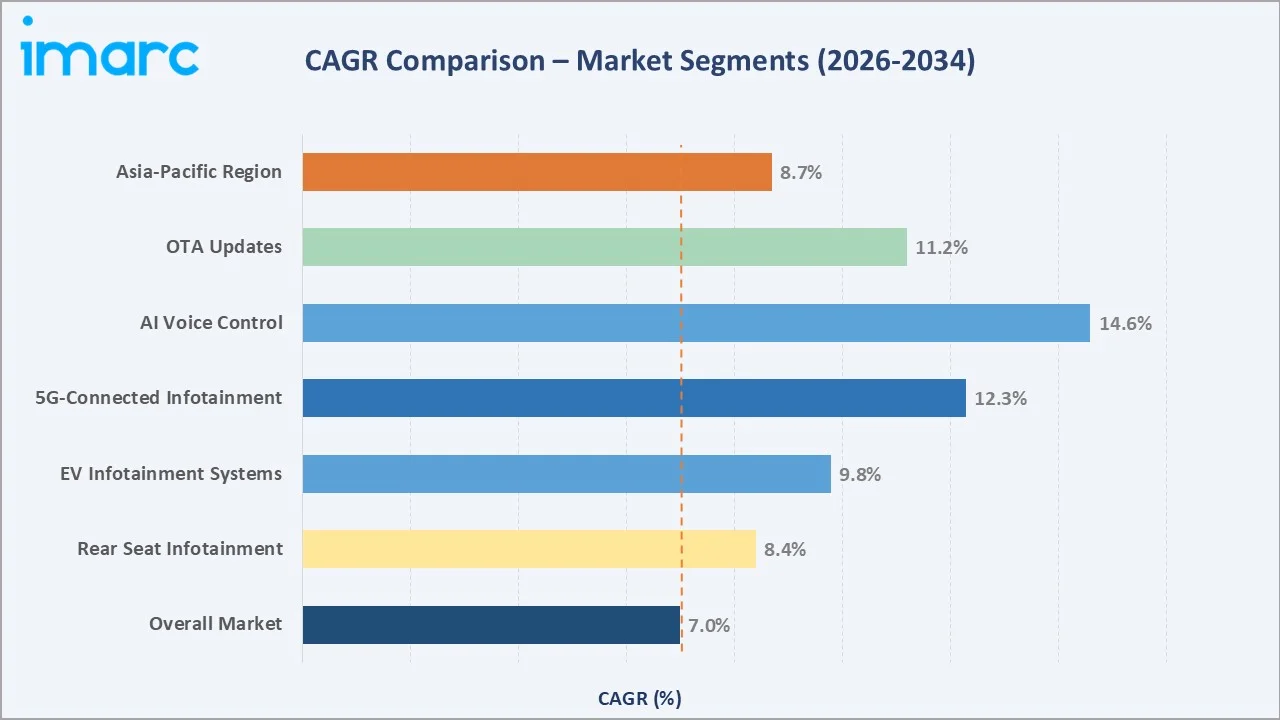

Segment-level CAGR comparisons highlighting AI voice control and 5G-connected infotainment as the two fastest-growing technology sub-categories within the global automotive infotainment industry analysis through 2034.

Executive Summary

The global automotive infotainment market is undergoing a fundamental transformation driven by the convergence of electrification, connectivity, and artificial intelligence in the automotive sector. Valued at USD 22.6 Billion in 2025, the market is forecast to reach USD 41.5 Billion by 2034 at a CAGR of 7.00%. The International Energy Agency estimated global electric car sales exceeded 17 million in 2024, marking an increase of over 25%, with an additional 3.5 million vehicles sold compared to 2023 and each electric vehicle platform demands significantly more sophisticated infotainment integration than its ICE counterpart, given the larger digital cockpit displays, OTA update capabilities, and energy management interfaces that EVs require.

In-Dash Infotainment commands the dominant installation type share at 65.4% in 2025, driven by OEM-standard large-format touch displays, heads-up display (HUD) integration, and centralized digital cockpit architectures that have become standard in vehicles above the entry-level price point. Rear Seat Infotainment at 34.6% is the faster-growing installation type, fuelled by premium passenger car growth in Asia-Pacific and commercial vehicle entertainment demand.

Asia-Pacific dominates with a 40.7% global revenue share in 2025, led by China, the world's largest vehicle production market with 27+ million annual units, alongside Japan's technology-dense Tier-1 supplier ecosystem and South Korea's premium infotainment R&D capabilities. North America holds 22.6% in 2025 and Europe 20.4%, with both regions characterized by premium vehicle penetration and advanced regulatory frameworks governing driver-safety interface design.

Key Market Insights

|

Insight |

Data |

|

Largest Installation Type |

In-Dash Infotainment – 65.4% share (2025) |

|

Leading Operating System |

LINUX – 60.0% share (2025) |

|

Leading Region |

Asia-Pacific – 40.7% revenue share (2025) |

|

Second Region |

North America – 22.6% revenue share (2025) |

|

Top Companies |

HARMAN, Bosch, Continental, Denso, Panasonic, Visteon |

Key Analytical Observations Supporting the Above Data:

- In-Dash Infotainment's 65.4% dominance in 2025reflects the industry-wide shift toward large-format central display architectures.

- LINUX leads the operating system segment at 60.0% in 2025, driven by the rapid adoption of Google Android Automotive OS, open-source flexibility, and OEM preference for customisable software-defined cockpit architectures across EVs and mainstream vehicle segments.

- Asia-Pacific's 40.7% global dominance in 2025reflects China's dual role as the world's largest vehicle market AND the most aggressive adopter of digital cockpit technology.

Global Automotive Infotainment Market Overview

Automotive infotainment systems are integrated electronic platforms installed in vehicles that combine information, entertainment, navigation, communication, and vehicle management functions into a unified user interface. Modern infotainment systems serve as the primary human-machine interface (HMI) for passenger interaction, incorporating touchscreen displays, voice recognition, smartphone mirroring, navigation, audio/video streaming, vehicle diagnostics, and increasingly ADAS status display and control.

Applications span the full automotive sector: passenger cars, light commercial vehicles, heavy trucks, buses, and increasingly autonomous shuttles and robotaxis, where infotainment serves as the primary passenger experience interface in the absence of a driver.

Macroeconomic enablers include global vehicle production with over 92.5 million cars produced globally in 2024 (17 million electric cars in 2024 per IEA), rising middle-class vehicle ownership in Asia-Pacific, and consumer expectation convergence between smartphone digital experience quality and in-vehicle interface quality.

Market Dynamics

To evaluate market opportunities, Request Sample

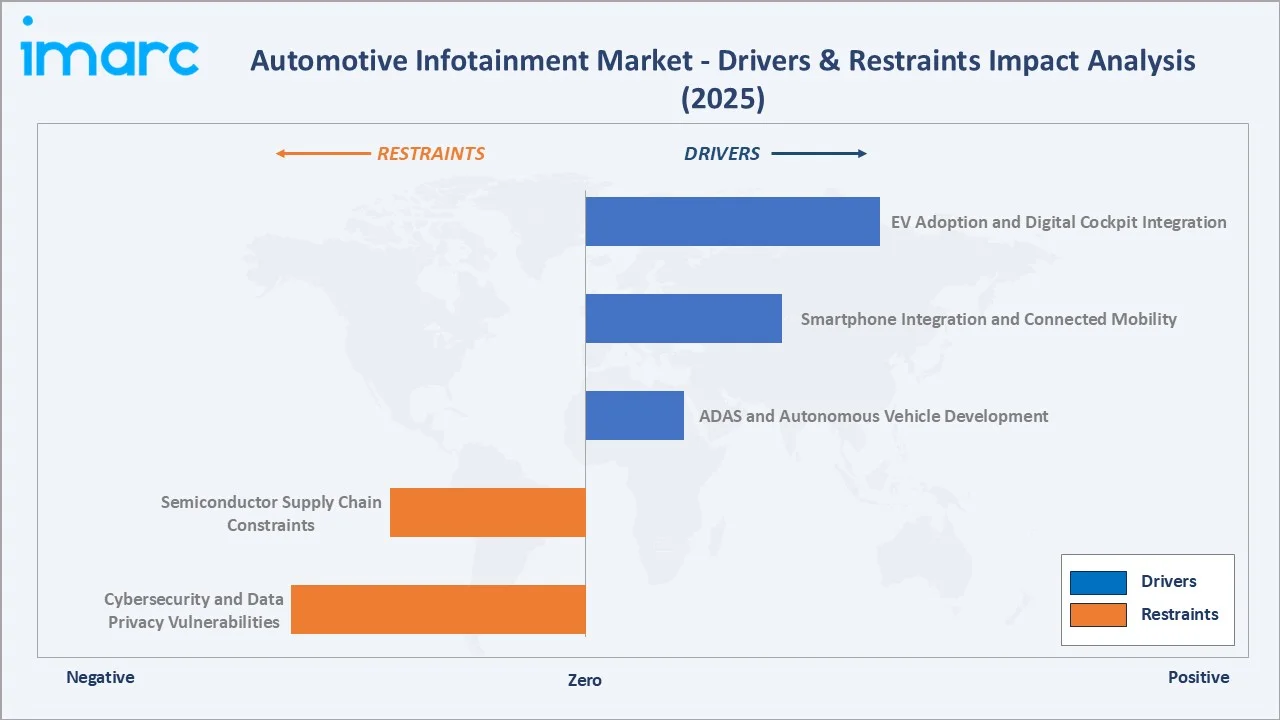

Market Drivers

- EV Adoption and Digital Cockpit Integration: The global electric cars market, reached approximately 17 million annual sales in 2024 (IEA), is the most powerful structural driver for advanced infotainment adoption. EV platforms require larger digital cockpit systems for battery management visualization, charging network navigation, energy consumption analytics, and OTA software update management, content categories that are impossible or impractical in ICE vehicle infotainment.

- Smartphone Integration and Connected Mobility: Apple CarPlay and Android Auto have fundamentally reset consumer expectations for in-vehicle digital experience quality. The Apple CarPlay is now active in over 800 vehicle models globally, creating structural demand for infotainment hardware specification upgrades even in entry-level vehicle segments.

- ADAS and Autonomous Vehicle Development: Advanced Driver-Assistance Systems, lane keeping assistance, adaptive cruise control, automated emergency braking, require infotainment-integrated HMI displays to communicate system status, alerts, and driver takeover requests.

Market Restraints

- Cybersecurity and Data Privacy Vulnerabilities: Modern infotainment systems are connected to vehicle CAN buses, cellular networks, and cloud platforms, creating attack surfaces for remote exploitation.

- Semiconductor Supply Chain Constraints: Supply has largely normalized now, concentration risk in advanced semiconductor supply chains and geopolitical tensions affecting Taiwan Semiconductor Manufacturing Company (TSMC) production capacity for advanced automotive chips remain structural market risks.

Market Opportunities

- Software-Defined Vehicle (SDV) Platform Revenue: The SDV architecture trend, where vehicle software is decoupled from hardware and can be updated, upgraded, and monetized throughout the vehicle lifecycle via OTA updates, is creating new revenue model opportunities for infotainment platform providers.

- Augmented Reality HUD and Immersive Display Technologies: Augmented reality head-up displays (AR-HUDs), projecting navigation and ADAS information into the driver's field of view at windshield scale, are transitioning from luxury flagship to mainstream premium segments.

- Commercial Vehicle Infotainment Expansion: Long-haul trucks, buses, and commercial fleet vehicles represent a structurally underpenetrated infotainment opportunity.

Market Challenges

- OS and Platform Fragmentation: Unlike the mobile industry's iOS/Android duopoly, automotive OS fragmentation means a navigation or streaming app must be certified and maintained across 8+ different platform variants to achieve broad vehicle compatibility.

- Driver Distraction and HMI Complexity: As infotainment screens grow larger and feature sets become more complex, the risk of driver distraction increases.

Emerging Market Trends

1. Software-Defined Vehicle (SDV) Architecture Redefining the Infotainment Model

The industry is transitioning from hardware-centric 'black box' infotainment head units to software-defined platforms where the digital cockpit is a continuously updated, monetisable software layer.

2. AI and Large Language Model Integration in Vehicle Interfaces

Generative AI and large language models are entering automotive infotainment at a pace. Mercedes-Benz's 2023 ChatGPT integration into MBUX voice assistant, enabling genuinely conversational, context-aware interactions beyond keyword commands, is the landmark reference deployment.

3. 5G Connectivity Enabling Cloud-Native Infotainment Services

5G cellular connectivity in vehicles is transitioning infotainment from locally-stored content to cloud-native service delivery. The global number of connected vehicles in use is projected to grow from 192 million in 2023 to 367 million by 2027.

4. Augmented Reality and Immersive Display Technologies

Augmented reality head-up displays (AR-HUDs) are projected to grow from a high-end luxury feature to a mainstream premium segment offering by 2028-2030. AR-HUDs project navigation arrows, ADAS status overlays, and hazard warnings directly into the driver's forward field of view, reducing eyes-off-road time.

5. Personalization and In-Car Commerce Monetization

Modern infotainment platforms are increasingly functioning as personalized digital lifestyle companions, learning driver preferences, adapting UI layouts, curating music and podcast recommendations, and offering transactional services including EV charging reservations, parking payments, and food ordering without leaving the vehicle.

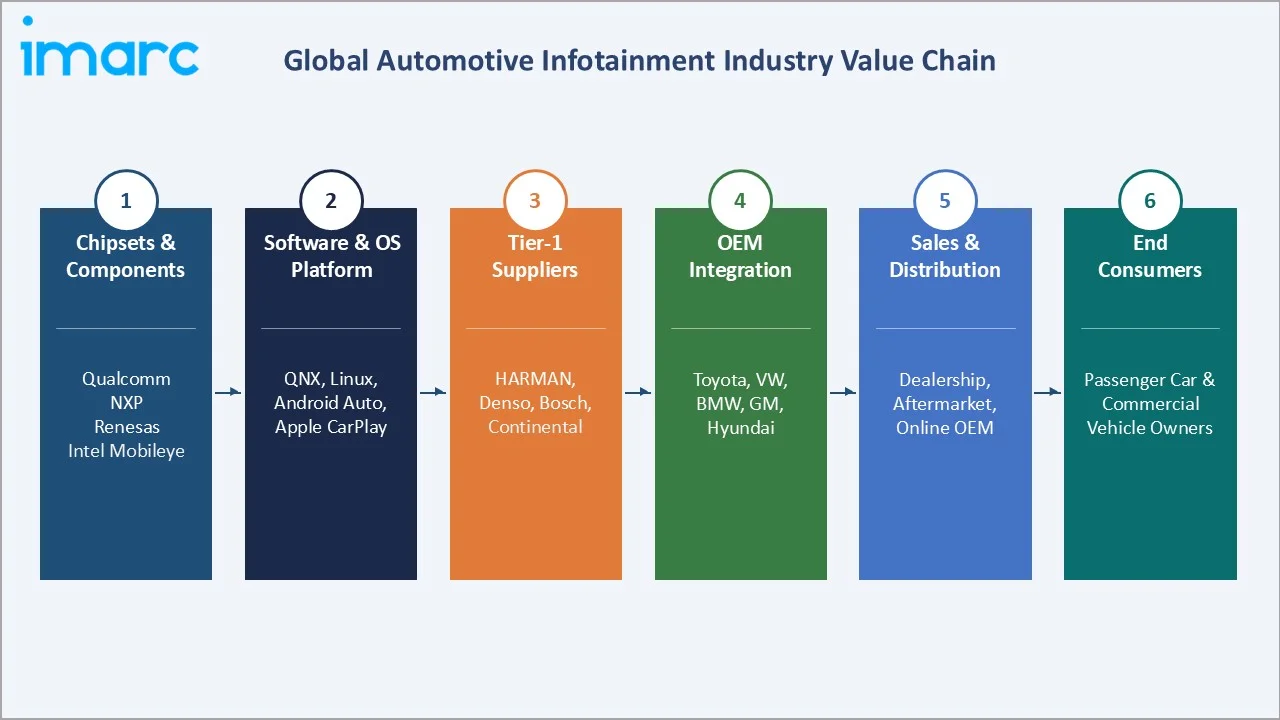

Industry Value Chain Analysis

The automotive infotainment value chain spans six integrated stages from semiconductor component supply through end-consumer vehicle delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Chipsets & Components |

Qualcomm (Snapdragon Auto), NXP Semiconductors, Renesas Electronics, Intel Mobileye, Texas Instruments |

|

Software & OS Platform |

BlackBerry QNX, Linux/AGL, Google Android Automotive OS, Apple CarPlay/Android Auto, Microsoft Azure RTOS |

|

Tier-1 Automotive Suppliers |

HARMAN International, Robert Bosch GmbH, Continental AG, Denso Corporation, Panasonic Automotive |

|

OEM Vehicle Integration |

Toyota, Volkswagen Group, BMW Group, General Motors, Stellantis, Hyundai-Kia, BYD, NIO |

|

Sales & Distribution Channels |

OEM dealership network, authorized installers, aftermarket specialists (Best Buy Auto, Halfords) |

|

End Consumers |

Passenger car owners, commercial fleet operators, ride-hailing operators, autonomous vehicle platforms |

Tier-1 suppliers occupy the highest strategic value position in the automotive infotainment value chain, integrating chipsets, software, displays, and connectivity hardware into turnkey cockpit solutions that OEMs can adopt with minimal in-house engineering. However, this structural position is under threat from OEMs internalising software development to capture greater software value and reduce dependency on supplier-controlled platform evolution.

Technology Landscape in the Automotive Infotainment Industry

Operating System Architecture: QNX, Linux, and the OS Battle

The automotive OS landscape is undergoing a fundamental consolidation battle. In March 2026, BlackBerry unveiled QNX Hypervisor 8.0, a virtualization platform built to meet safety certification requirements while ensuring deterministic performance. Designed to support the rising demand for physical AI applications, the hypervisor enables secure and reliable virtualized environments across sectors such as automotive, robotics, and medical devices.

Artificial Intelligence and Voice Recognition

AI voice assistants have transitioned from keyword-triggered command executors to context-aware, conversational interfaces powered by transformer-based language models. BMW's Alexa-powered voice assistant represents the vanguard.

Connectivity Technologies: 5G, Wi-Fi 6E, and V2X

The connectivity technology stack in modern infotainment is layered: Bluetooth 5.3 for personal device pairing, Wi-Fi 6E for high-bandwidth in-cabin content distribution and hotspot, 5G cellular for cloud services and OTA updates, and C-V2X for safety-critical communications with road infrastructure and other vehicles.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Audio |

🔒 |

2025 |

|

Vehicle Type |

Passenger Cars |

79.5% |

2025 |

|

Operating System |

Linux |

60.0% |

2025 |

|

Installation Type |

In-Dash Infotainment |

65.4% |

2025 |

| Sales Channel | OEM | 72.8% | 2025 |

| Technology | Tethered | 🔒 | 2025 |

| Connectivity | Bluetooth | 35.9% | 2025 |

|

Region |

Asia Pacific |

40.7% |

2025 |

By Installation Type

In-Dash Infotainment commands a 65.4% majority share in 2025, reflecting the industry-wide standardization of large-format central touchscreen architectures as the primary in-vehicle interface. The in-dash segment benefits from the OEM channel's market dominance and the strong trend toward integrated cockpit domain controllers that unify instrument cluster and infotainment in a single hardware platform.

To access detailed market analysis, Request Sample

Rear Seat Infotainment at 34.6% in 2025, driven by premium SUV rear entertainment systems, commercial vehicle long-haul driver and passenger entertainment, and the growing premium minivan segment in Asia-Pacific where rear-seat occupant experience is a primary purchase motivator.

By Operating System

LINUX dominates at 60.0% in 2025, benefitting from open-source flexibility, Google Android Automotive OS momentum, and OEM demand for customisable software stacks. ISO 26262 ASIL-D functional safety certification, essential for cockpit domain controller architectures where infotainment and safety-critical ADAS display functions share computing hardware.

QNX at 23.5% in 2025, maintaining a strong position in safety-critical and premium ADAS-integrated applications due to its ASIL-D ISO 26262 certification and real-time processing capabilities. Microsoft at 11.3% primarily serves European infotainment integrators and commercial vehicle applications where Windows-based fleet management integration is preferred. Others (5.2%) encompass Android Automotive deployments in volume Asian markets and fully proprietary OS implementations by Tesla and Chinese OEMs.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

40.7% |

China NEV boom, Japan/Korea Tier-1 tech, India EV expansion, ASEAN auto growth |

|

North America |

22.6% |

Tesla SDV model, GM/Ford EV platforms, 5G vehicle connectivity, ADAS mandates |

|

Europe |

20.4% |

VW/BMW/Mercedes SDV investment, EU GSR safety mandates, EV mandate 2035 |

|

Middle East & Africa |

9.8% |

GCC premium vehicle adoption, Saudi Vision 2030 smart mobility, South Africa growth |

|

Latin America |

6.5% |

Brazil/Mexico auto production, growing mid-range connected vehicle adoption |

Asia-Pacific commands a 40.7% global revenue share in 2025, the most dominant regional position of any global automotive infotainment market. China is the single most important national market within Asia-Pacific, combining the world's largest vehicle production volume, with China produced 27.477 million passenger vehicles in 2024, marking a 5.2% increase compared to the previous year, with the world's most technologically ambitious infotainment specifications from domestic NEV brands.

North America, with 22.6% in 2025, is anchored by the US market, where Tesla's SDV model has become the competitive reference for the entire industry. The US EV market is projected to see 1-in-5 cars electric by 2030, each vehicle representing a premium infotainment hardware specification versus ICE equivalents. Canada's ADAS regulatory evolution and Mexico's growing vehicle production base add further North American market breadth.

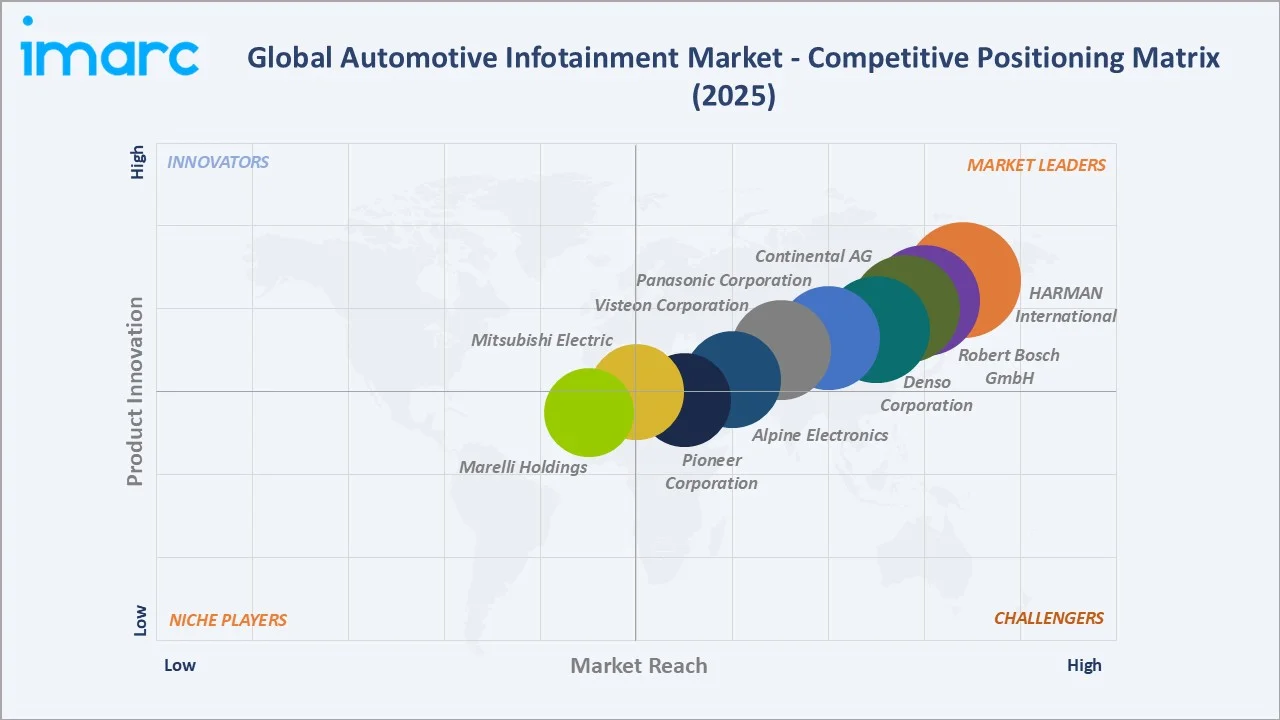

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

HARMAN International (Samsung Electronics) |

HARMAN Ignite / JBL Audio |

Leader |

Digital cockpit, audio, OTA, 5G connected services |

|

Robert Bosch GmbH |

Bosch Cockpit & Display |

Leader |

Full digital cockpit, ADAS display, Tier-1 supplier |

|

Continental AG |

Continental CID / VDO |

Leader |

Cockpit domain controller, AR-HUD, OEM partnerships |

|

Denso Corporation |

Denso Infotainment Unit |

Leader |

Japan/Toyota ecosystem, OEM-grade hardware quality |

|

Panasonic Automotive |

Panasonic Automotive HS |

Challenger |

AR display, premium audio, Tesla/OEM partnerships |

|

Visteon Corporation |

Visteon SmartCore |

Challenger |

Cockpit domain controller, OTA, software-defined |

|

Alps Alpine Co. Ltd |

Alps Alpine Systems |

Challenger |

HMI systems, sensors, automotive electronics integration |

|

Pioneer Corporation |

Pioneer DMH / NEX Series |

Challenger |

In-car entertainment, navigation, aftermarket systems |

|

Mitsubishi Electric Corp. |

Mitsubishi Electric Automotive |

Emerging |

ADAS, power electronics, in-vehicle systems |

|

Marelli Holdings |

Marelli Cockpit |

Emerging |

Lighting, electronics, cockpit integration |

The automotive infotainment competitive landscape is characterized by a small number of global Tier-1 automotive electronics suppliers commanding substantial OEM relationships, alongside semiconductor companies with growing software platform ambitions and disruptive Chinese domestic suppliers challenging the established hierarchy in the world's largest market

Key Company Profiles

HARMAN International (Samsung Electronics)

HARMAN International is the global leader in automotive infotainment, a wholly-owned subsidiary of Samsung Electronics since 2017.

- Product & Platform Portfolio: READYdisplay, READYengage, Readystreamshare, READYcare, Readylink marketplace.

- Recent Developments: In April 2024, HARMAN launched HARMAN Ignite Store, an in-vehicle app store enabling OEMs to offer post-sale software services and revenue-generating applications to vehicle owners.

- Strategic Focus: HARMAN's strategy centers on three platforms: HARMAN Ignite (cloud-connected services and OTA), digital cockpit domain controllers (combining cluster, infotainment, and rear seat in a unified architecture), and premium audio brand leverage. Samsung's semiconductor resources are increasingly enabling HARMAN to offer vertically integrated SoC-to-software cockpit solutions that no other Tier-1 can match.

Robert Bosch GmbH

Robert Bosch is one of the world's largest automotive suppliers with a comprehensive infotainment and digital cockpit portfolio spanning hardware, software, and connected services.

- Product & Platform Portfolio: Cockpit integration platform, connected cluster, adaptive haptics controls.

- Recent Developments: In January 2024, Qualcomm Technologies, Inc. and Robert Bosch GmbH unveiled the automotive industry’s first central vehicle computer capable of running both infotainment and advanced driver assistance system (ADAS) functions on a single system-on-chip. Bosch introduced the platform, called its cockpit and ADAS integration system, which is built on the Snapdragon Ride Flex SoC.

- Strategic Focus: Bosch's automotive infotainment strategy prioritises cross-domain computing architecture leadership (integrating infotainment with safety and body control to reduce OEM system complexity), software-as-a-service expansion through its Connected Mobility division, and maintaining Tier-1 supplier relationships with European premium OEMs while aggressively expanding in China through local partnerships.

Visteon Corporation

Visteon is a pure-play automotive cockpit electronics specialist, one of the few Tier-1 suppliers focused exclusively on digital cockpits, instrument clusters, and infotainment systems.

- Product & Platform Portfolio: Digital cockpit display systems, cockpit domain controller, instrument clusters, android infotainment, connected services.

- Recent Developments: In January 2026, Visteon Corporation announced a strategic partnership with TomTom to introduce the world’s first in-car, locally powered AI conversational navigation assistant. As part of the collaboration, Visteon’s cognitoAI platform integrate TomTom’s Automotive Navigation Application to deliver a privacy-focused navigation experience.

- Strategic Focus: Visteon's focused strategy targets the premium cockpit domain controller market where its pure-play specialization enables faster development cycles and deeper OEM co-engineering relationships than diversified Tier-1 competitors. The company is investing heavily in Android Automotive OS integration, OTA software update infrastructure, and AI-powered personalization capabilities as differentiators for its SmartCore platform.

Market Concentration Analysis

The global automotive infotainment market exhibits moderate-to-high concentration among the top Tier-1 automotive electronics suppliers, with HARMAN, Bosch, and Continental collectively accounting for approximately 35-42% of global market revenue in 2025.

The global automotive infotainment market is experiencing a bifurcated structural dynamic. At the premium OEM tier, consolidation is occurring: complex digital cockpit domain controller architectures require massive R&D investment that only the largest Tier-1s can sustain, effectively excluding mid-size suppliers from flagship OEM programmes.

Simultaneously, the Chinese domestic market is fragmenting and generating new challengers. Chinese OEMs' preference for domestic suppliers, and the technical competitiveness of platforms like Desay's in-dash systems in BYD and SAIC vehicles, is creating competitive pressure on international Tier-1s in the world's largest automotive market.

Investment & Growth Opportunities

Fastest-Growing Segments

AI voice control integration is the highest-growth technology sub-segment at ~14.6% CAGR through 2034. The deployment of GPT-class large language models in vehicle infotainment, pioneered by Mercedes-Benz's ChatGPT integration, is transforming driver interaction from menu-based touchscreen navigation to conversational natural language interfaces. 5G-connected infotainment is growing at ~12.3% CAGR through 2034, enabled by 5G vehicle modem deployments.

Emerging Market Expansion

Augmented Reality Head-Up Display (AR-HUD) is the emerging premium display sub-market, transitioning from flagship luxury to mainstream premium segments. Software-defined vehicle platform services, OTA update infrastructure, post-sale feature subscription management, and in-vehicle commerce platforms, represent the highest-potential revenue model shift in automotive infotainment history.

Venture & Private Investment Trends

The notable transactions include Samsung's deepening HARMAN investment, Qualcomm's Snapdragon Automotive platform investments, and multiple venture rounds in AR display start-ups including WayRay and Envisics. Chinese EV software start-ups, including Banma Technologies and Newrizon are attracting significant domestic venture capital investment, reflecting the rising strategic value of software-defined in-vehicle experience platforms.

Future Market Outlook (2026-2034)

The global automotive infotainment market forecast projects steady value expansion from USD 22.6 Billion in 2025 to USD 41.5 Billion by 2034 at a CAGR of 7.00%, a near-doubling of market value underpinned by premium system specification upgrades, software service revenue layer addition, and structural shifts in both EV penetration and autonomous driving technology integration through the forecast period.

Three technology discontinuities are most likely to reshape the automotive infotainment market through 2034. Software-defined vehicle platform convergence, where infotainment, ADAS, and powertrain software merge onto unified high-performance compute platforms, will restructure the competitive landscape by 2028-2030, potentially displacing traditional Tier-1 hardware suppliers in favour of SoC platform companies that can offer complete vehicle compute architectures.

By 2034, the automotive infotainment industry is forecast to have completed its transformation from a hardware accessories market to a software platform economy. The competitive landscape will be shaped by three dominant platform architectures: HARMAN-Samsung's connected services ecosystem, Google Android Automotive's app economy, and Chinese domestic ecosystems (Baidu Apollo, Alibaba AliOS) dominating within China.

Research Methodology

Primary Research

Primary research encompassed over 60 structured interviews conducted in 2024-2025 with automotive electronics industry stakeholders including product directors at Tier-1 infotainment suppliers, automotive OEM purchasing and digital cockpit programme managers, semiconductor company automotive business unit leads, automotive OS platform managers, and institutional investors in automotive technology. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include IEA Global EV Outlook, GSMA Connected Car report (2024), IHS Markit (S&P Global Mobility) vehicle production and infotainment system fitment data, TechSci Research automotive electronics reports, Gartner Automotive Technology Hype Cycle (2024), UNECE WP.29 regulatory publications, NHTSA driver distraction guidelines, AlixPartners automotive supply chain analyses, company annual reports, and trade publications including Automotive News, SAE International, and Car and Driver connected technology coverage.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, consumer expenditure data, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Automotive Infotainment Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Navigation Unit, Display Audio, Audio, Others |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles |

| Operating Systems Covered | QNX, LINUX, Microsoft, Others |

| Installation Types Covered | In-Dash, Rear Seat Infotainment |

| Sales Channels Covered | OEM, Aftermarket |

| Technologies Covered | Integrated, Embedded, Tethered |

| Connectivities Covered | Bluetooth, Wi-Fi, 3G, 4G, 5G |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico, Turkey, Saudi Arabia, Iran, United Arab Emirates |

| Companies Covered | HARMAN International (Samsung Electronics), Robert Bosch GmbH, Continental AG, Denso Corporation, Panasonic Automotive, Visteon Corporation, Alps Alpine Co. Ltd, Pioneer Corporation, Mitsubishi Electric Corp., Marelli Holdings, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive infotainment market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive infotainment market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive infotainment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Infotainment Market Report

The global automotive infotainment market was valued at USD 22.6 Billion in 2025, driven by EV adoption and digital cockpit demand.

The market is projected to reach USD 41.5 Billion by 2034, growing at a CAGR of 7.00% during 2026-2034, driven by EV platform upgrades, AI voice assistants, and 5G connected services.

In-Dash Infotainment leads with a 65.4% share in 2025, driven by OEM-standard large-format touchscreen adoption and integrated cockpit domain controller architectures across mainstream and premium vehicle segments.

LINUX leads with a 60.0% share in 2025, driven by Android Automotive OS adoption, open-source customisation, and OEM preference for software-defined vehicle platforms across EVs and mainstream segments.

Asia-Pacific leads with a 40.7% share in 2025, driven by China's NEV market, Japan's Tier-1 technology ecosystem, South Korea's R&D capabilities, and rapid ASEAN automotive sector growth.

Key drivers include EV platform digital cockpit demands (17M EV sales globally in 2024), Apple CarPlay/Android Auto smartphone integration, 5G connectivity, ADAS HMI requirements, and consumer premium UX expectations.

AI voice control is the fastest-growing technology at ~14.6% CAGR through 2026-2034, driven by ChatGPT-class language model integration enabling genuine conversational in-vehicle interfaces beyond keyword commands.

Leading companies include HARMAN International (Samsung), Robert Bosch, Continental AG, Denso Corporation, Panasonic Automotive, Visteon Corporation, Pioneer, Alpine Electronics, and Garmin.

SDV architecture enables OTA-updated infotainment software, post-sale feature subscriptions, and in-vehicle app stores, generating USD 500-2,000 per vehicle in software revenue above hardware sales economics.

5G enables cloud-native services, including real-time HD map updates, cloud gaming, V2X safety overlays, and high-speed OTA updates. GSMA forecasts 100 million 5G-connected vehicles globally by 2028.

AR-HUD projects navigation, ADAS, and safety information into the driver's windshield field of view, reducing eyes-off-road time by up to 80%. Continental's ARS-400 is entering mainstream premium vehicles from 2025-2027.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade