Automotive Remote Diagnostics Market Size, Share, Trends and Forecast by Product Type, Connectivity, Vehicle Type, Application, and Region, 2026-2034

Automotive Remote Diagnostics Market Report and Forecast (2026-2034)

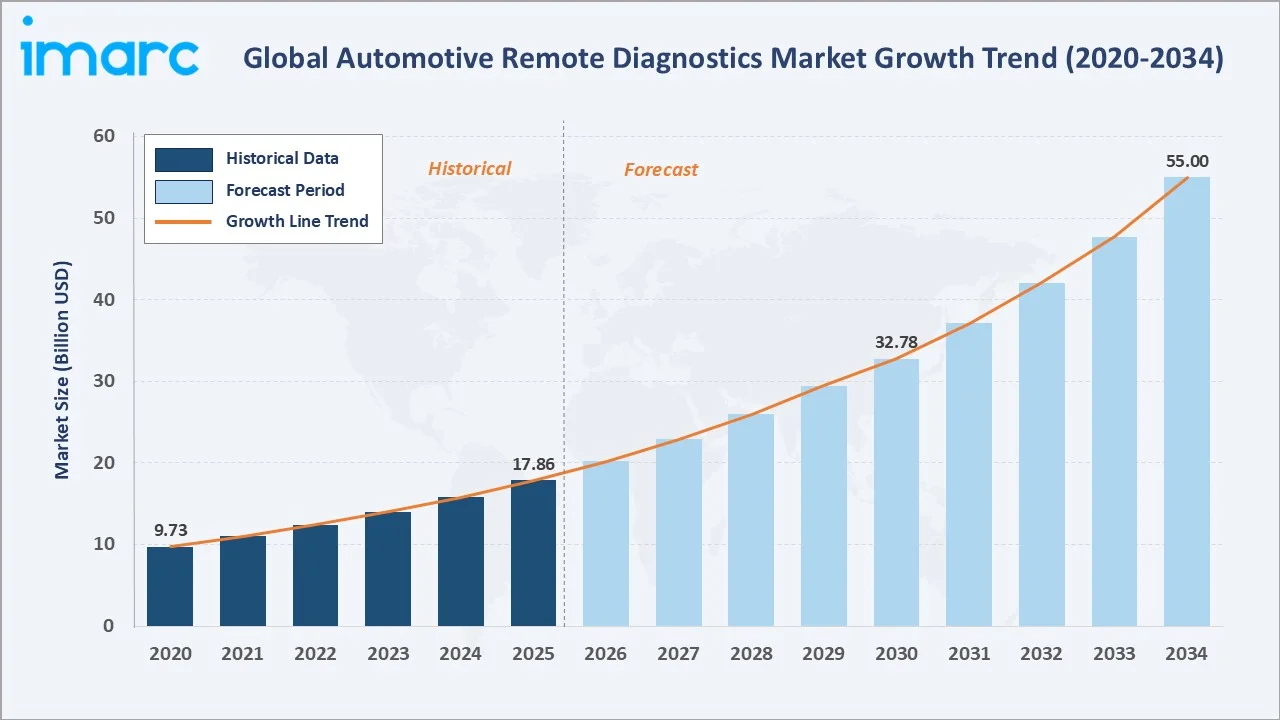

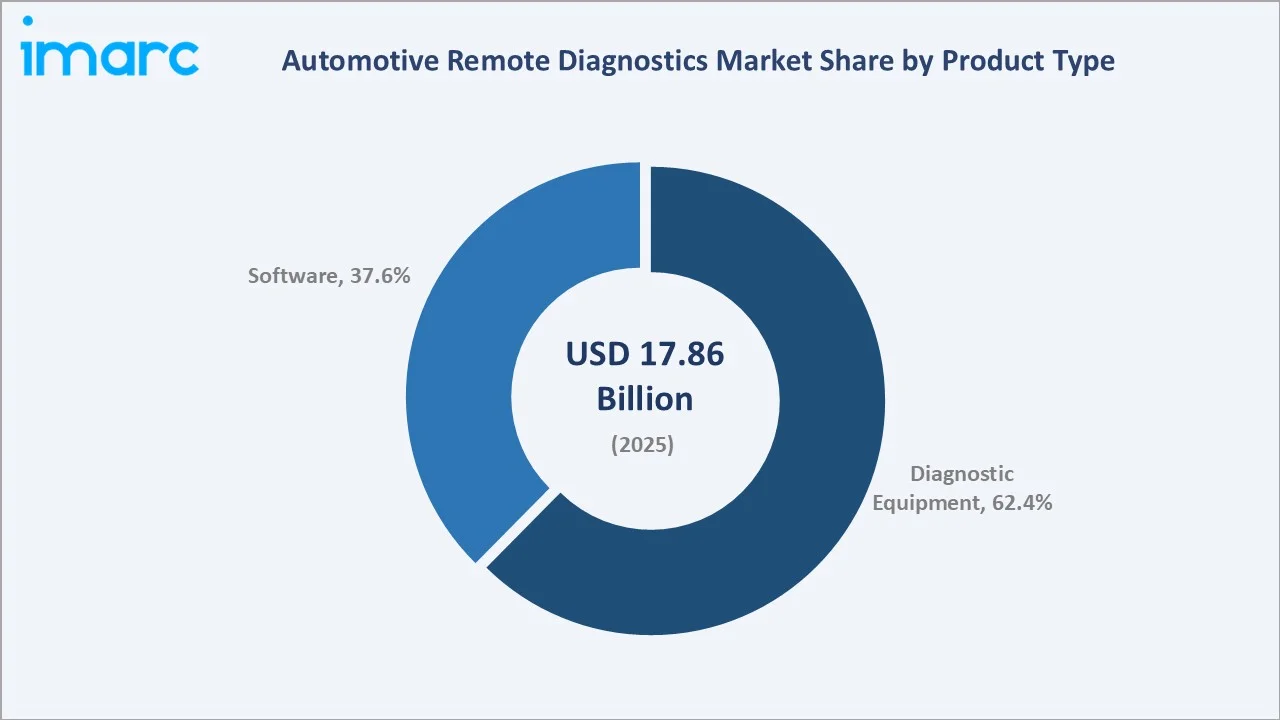

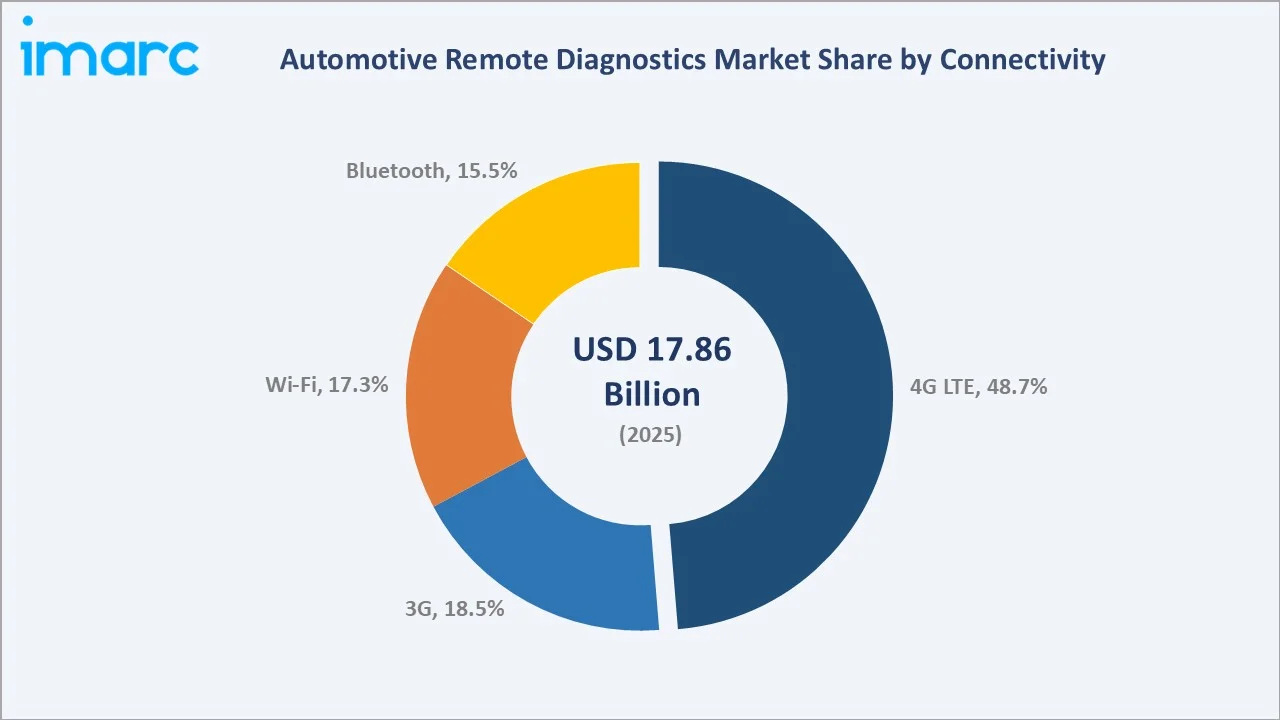

The global automotive remote diagnostics market size was valued at USD 17.86 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 55.00 Billion by 2034, exhibiting a CAGR of 12.92% during 2026-2034.

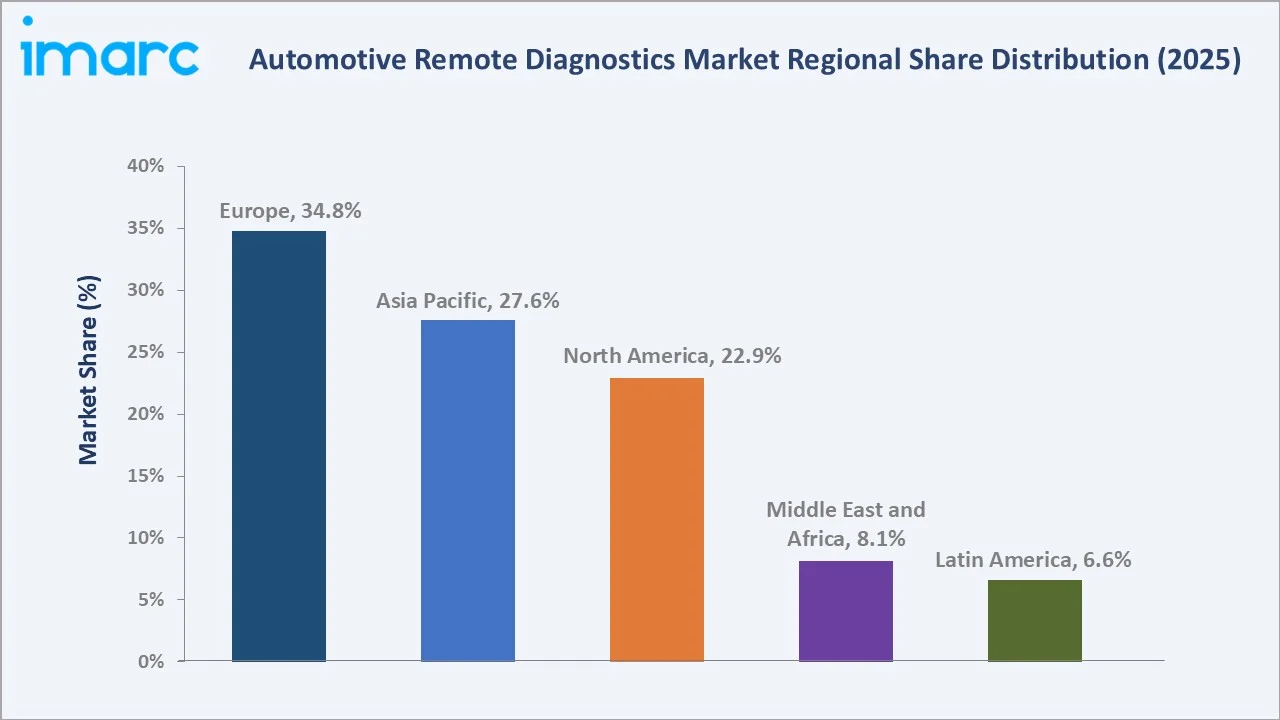

Europe currently dominates, commanding 34.8% share in 2025, supported by strict emission norms, advanced OEM telematics, and rising connected-vehicle penetration across passenger and commercial fleets. Asia Pacific remains the fastest-growing region amid China and India's EV acceleration.

Automotive remote diagnostics integrates onboard telematics, connectivity modules, and cloud analytics to continuously monitor vehicle health, detect faults, trigger alerts, and enable over-the-air corrective actions. Rising connected-car volumes, electrification, stringent safety mandates, and fleet-efficiency imperatives are driving rapid adoption.

Market Snapshot

|

Report Attribute |

Key Statistics |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2020-2025 |

|

Market Size in 2025 |

USD 17.86 Billion |

|

Market Forecast in 2034 |

USD 55.00 Billion |

|

CAGR (2026-2034) |

12.92% |

|

Leading Region (2025) |

Europe (34.8%) |

|

Leading Product Type |

Diagnostic Equipment (62.4%) |

|

Leading Connectivity |

4G LTE (48.7%) |

The trajectory demonstrates strong forecast momentum, with market value projected to more than triple between 2025 and 2034. Forecast-year expansion is driven by accelerating connected-vehicle shipments, embedded telematics integration, and aftermarket retrofits targeting commercial fleets across mature and emerging markets.

To get more information on this market, Request Sample

The 12.92% CAGR reflects structural shifts in how diagnostics are delivered, from workshop-bound scan tools toward always-on, cloud-connected platforms generating recurring revenue. Growth accelerates between 2028 and 2032 as 5G coverage, edge-AI accelerators, and regulatory cybersecurity frameworks converge to unlock new use cases.

Executive Summary

The automotive remote diagnostics market is entering a high-growth phase as connected-vehicle ecosystems mature, and electrification expands the diagnostic scope from mechanical faults to battery health, thermal management, and software integrity. Rising OEM adoption of embedded telematics and fleet-efficiency priorities are key accelerators.

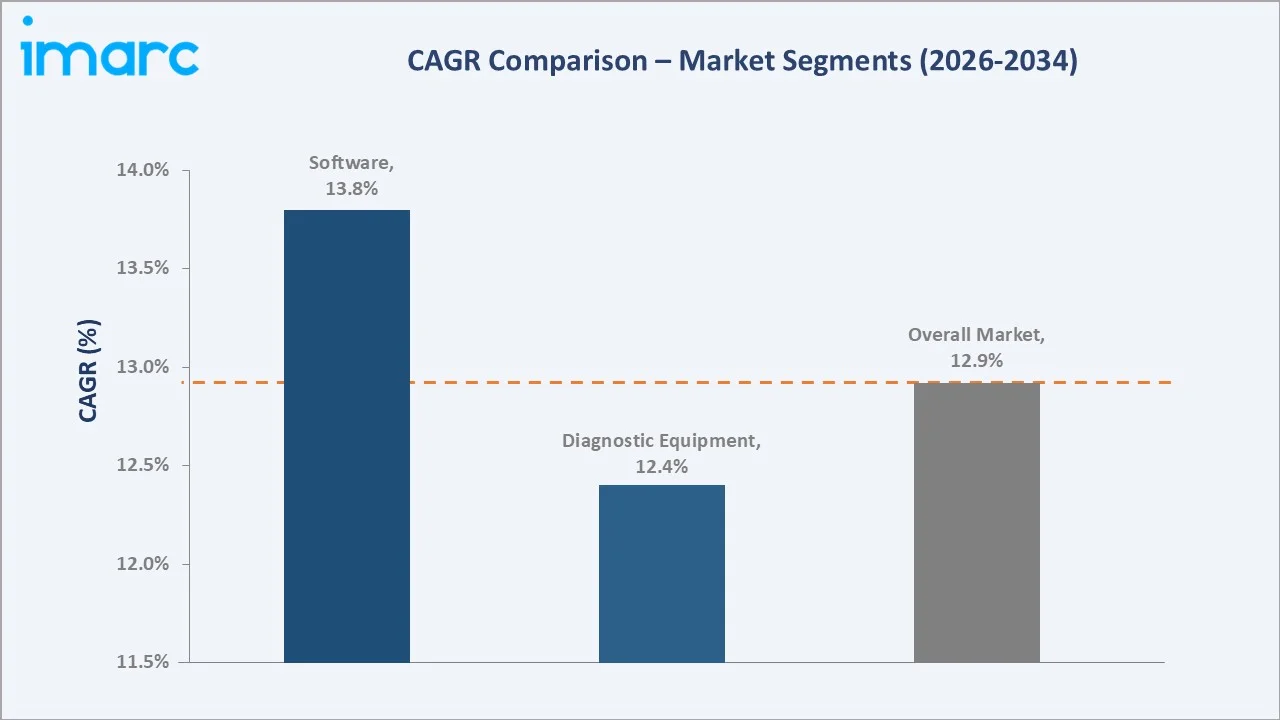

By product type, diagnostic equipment dominates at 62.4% share in 2025, reflecting the installed base of onboard interfaces and scan tools across passenger and commercial vehicles. By connectivity, 4G LTE leads with 48.7%, driven by its balance of coverage, latency, and bandwidth for telemetry streams.

5G migration is set to redefine diagnostic architecture post-2028, enabling ultra-low latency use cases such as live remote intervention, ADAS recalibration, and V2X integration. Competitive dynamics are consolidating around a handful of Tier-1 OEM-grade suppliers complemented by software specialists.

Regionally, Europe anchors the market at 34.8% share, supported by stringent regulations, while the Asia Pacific is the fastest-growing region. North America benefits from deep fleet telematics adoption and mature usage-based insurance ecosystems. Emerging markets in Latin America and Africa remain nascent but present long-term growth upside.

Key Market Insights

|

Parameter |

Insight |

|

Demand Driver |

Rapid rise in connected vehicles and embedded telematics adoption |

|

Leading Segment |

Diagnostic Equipment holds 62.4% of 2025 revenue |

|

Growth Engine |

4G LTE at 48.7%; 5G migration accelerating post-2028 |

|

Regional Leader |

Europe (34.8%), followed by Asia Pacific (27.6%) |

|

Key Trend |

AI-based predictive diagnostics replacing scheduled maintenance |

Key Analytical Observations Expanding On The Above Data:

- Electrification expands scope: Electrification broadens diagnostic scope to include battery state-of-health, thermal management, and powertrain software integrity, creating entirely new revenue pools for software and subscription models.

- OTA closes the loop: OTA software updates transform diagnostics into a continuous, closed-loop service rather than event-driven workshop visits, deepening OEM engagement over the vehicle lifecycle.

- Fleet economics: Fleet operators extract measurable ROI through lower unplanned downtime, optimised maintenance schedules, and insurance premium efficiencies tied to usage-based data.

- Regulatory pressure: Cybersecurity frameworks (UNECE R155/R156, ISO/SAE 21434) are becoming non-negotiable, elevating compliance spend and reshaping vendor shortlists across OEM programs globally.

- AI transformation: AI and machine-learning models trained on fleet-wide telematics data are shifting diagnostics from rule-based fault detection toward truly predictive failure forecasting.

Global Automotive Remote Diagnostics Market Overview

Automotive remote diagnostics is the real-time, wireless transmission of vehicle telemetry, fault codes, sensor values, battery and powertrain data, and driving parameters, from an onboard unit to a cloud platform where analytics flag anomalies, guide service decisions, and trigger OTA interventions.

The market operates at the intersection of automotive engineering, cloud computing, and telecommunications. Growth is anchored in the shift from reactive to predictive maintenance, deeper OEM-customer engagement through digital channels, and regulatory pressure for cybersecurity, safety, and emissions monitoring.

Value creation is shifting from one-off hardware sales toward recurring software and data-service revenues. OEMs are bundling diagnostics into connected-car subscriptions, dealer networks are using it to protect service share, and insurers are integrating remote data into usage-based pricing models.

Aftermarket penetration is widening on older fleets via plug-in OBD-II devices, while OEM programs focus on factory-fitted telematics control units. This dual-path expansion is broadening the addressable market across passenger vehicles, light commercial vehicles, heavy trucks, and specialty mobility platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

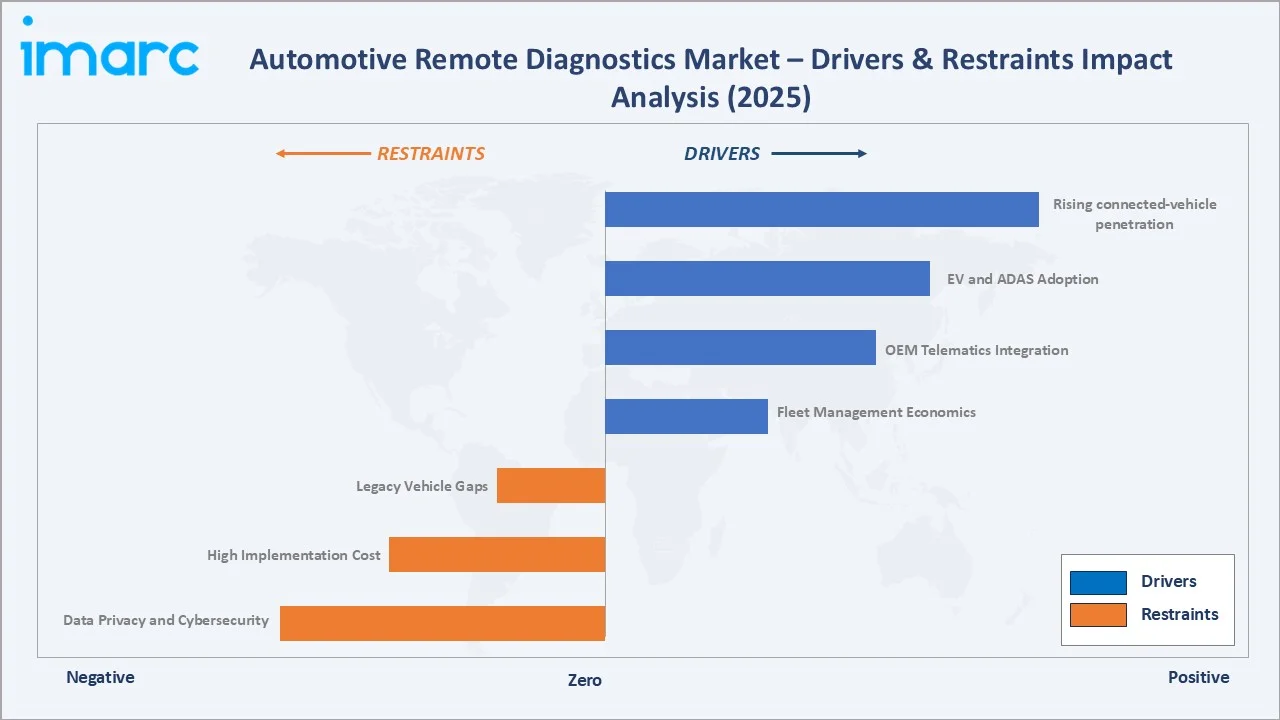

Market Drivers

- Rising connected-vehicle penetration: The global installed base of connected vehicles is projected to surpass 400 million units in 2025, with embedded SIMs increasingly standardized across both mature and emerging markets. This pervasive connectivity enables continuous, real-time data transmission from vehicle ECUs, forming the foundational infrastructure for remote diagnostics at scale. As telecom networks evolve with broader 5G deployment, improved bandwidth and lower latency are further enhancing the reliability of remote fault detection, OTA updates, and cloud-based diagnostic interventions.

- EV and ADAS adoption: The rapid adoption of electric vehicles (EVs) and Advanced Driver Assistance Systems (ADAS) is fundamentally reshaping diagnostic requirements, as critical components such as battery systems, thermal management, and high-voltage architectures cannot be effectively assessed using legacy OBD-II tools. Additionally, ADAS introduces complex sensor ecosystems involving radar, LiDAR, and cameras, necessitating advanced analytics to interpret multi-source data. This transition is driving demand for sophisticated, software-defined remote diagnostics platforms capable of handling next-generation vehicle architectures and safety-critical systems.

- OEM telematics integration: Automotive OEMs are increasingly integrating diagnostics into their native telematics platforms, positioning it as a strategic lever to prevent aftermarket disintermediation while unlocking recurring digital revenue streams. By maintaining direct access to vehicle data, OEMs can deliver proactive maintenance alerts, remote troubleshooting, and over-the-air fixes without requiring physical service visits. This approach not only enhances customer experience but also strengthens brand loyalty and enables new monetization models through subscription-based connected services and predictive maintenance offerings.

- Fleet management economics: Fleet operators are realizing significant economic benefits from adopting remote diagnostics, including 10–18% improvements in vehicle uptime and 6–9% reductions in maintenance costs through the shift from reactive or scheduled servicing to predictive maintenance models. Real-time monitoring allows early fault detection and intervention, minimizing costly breakdowns and operational disruptions. Furthermore, data-driven maintenance strategies optimize asset utilization, extend vehicle component lifespans, and reduce total cost of ownership, making remote diagnostics a critical capability for modern fleet management.

Market Restraints

- Data privacy and cybersecurity: The collection and transmission of granular vehicle and driver data introduce significant regulatory and security challenges, particularly under frameworks such as the General Data Protection Regulation (GDPR) and California Consumer Privacy Act (CCPA), along with emerging data-localisation mandates across key markets. Compliance requires robust encryption, consent management, and cross-border data governance mechanisms, increasing operational complexity and cost.

- High implementation cost: Deploying remote diagnostics infrastructure involves substantial upfront investment in telematics control units (TCUs), secure in-vehicle gateways, backend cloud platforms, and integration with existing OEM systems. These deployments typically require multi-year engineering validation, homologation, and certification cycles, particularly in safety-critical automotive environments.

- Legacy vehicle gaps: A significant portion of the global vehicle parc, particularly pre-2015 models, lacks embedded connectivity and standardized electronic architectures required for seamless remote diagnostics. Retrofitting such vehicles with aftermarket telematics solutions often proves economically unviable due to hardware costs, limited data access, and integration constraints. This creates a structural barrier to penetration in emerging markets, where older vehicles dominate and capital availability is constrained, thereby slowing the overall pace of remote diagnostics adoption despite clear long-term benefits.

Market Opportunities

- 5G and edge computing: The rollout of 5G networks is set to transform automotive remote diagnostics by enabling ultra-low latency and high-bandwidth data transmission, supporting real-time telemetry and advanced analytics at scale. Coupled with edge computing, this allows diagnostic algorithms to run closer to the vehicle, reducing response times and enabling use cases such as edge-AI fault detection, vehicle-to-everything (V2X) communication, and remote-assisted driving support.

- Usage-based insurance: The rise of usage-based insurance (UBI) models is creating a new demand vector for remote diagnostics, as insurers leverage real-time driving behavior, vehicle health, and risk data to personalize premiums and underwriting. By integrating telematics-derived insights, insurers can offer pay-how-you-drive and pay-as-you-drive products that align pricing with actual risk exposure.

- Software monetisation: Remote diagnostics platforms are increasingly serving as a foundation for software-driven revenue models, enabling OEMs and ecosystem players to offer subscription-based digital services such as remote vehicle access, predictive health scoring, and guided maintenance. These services deliver high-margin, recurring revenue streams while enhancing customer engagement and retention over the vehicle lifecycle.

Market Challenges

- Protocol fragmentation: The lack of standardized communication protocols across OEMs, combined with fragmented aftermarket interfaces, creates significant interoperability challenges for remote diagnostics platforms operating in multi-brand fleet environments. Proprietary vehicle architectures and data schemas require custom integrations, increasing deployment time, engineering effort, and total integration cost. This fragmentation limits scalability for platform providers and constrains the ability to deliver unified diagnostics solutions across diverse vehicle portfolios, ultimately slowing ecosystem-wide adoption.

- Cybersecurity burden: Ensuring robust cybersecurity across connected vehicle ecosystems introduces ongoing operational and financial strain, as stakeholders must continuously manage threat detection, incident response, and over-the-air (OTA) patching cycles. Long-term vulnerability management is particularly complex given extended vehicle lifecycles, requiring sustained updates to safeguard against evolving attack vectors.

- Consumer trust: Consumer trust remains a critical barrier to adoption, as awareness and understanding of in-vehicle data collection and sharing practices vary widely across regions and demographics. Concerns around data privacy, misuse, and lack of transparency can deter users from opting into connected diagnostic services, particularly in price-sensitive markets where perceived value must clearly outweigh perceived risks.

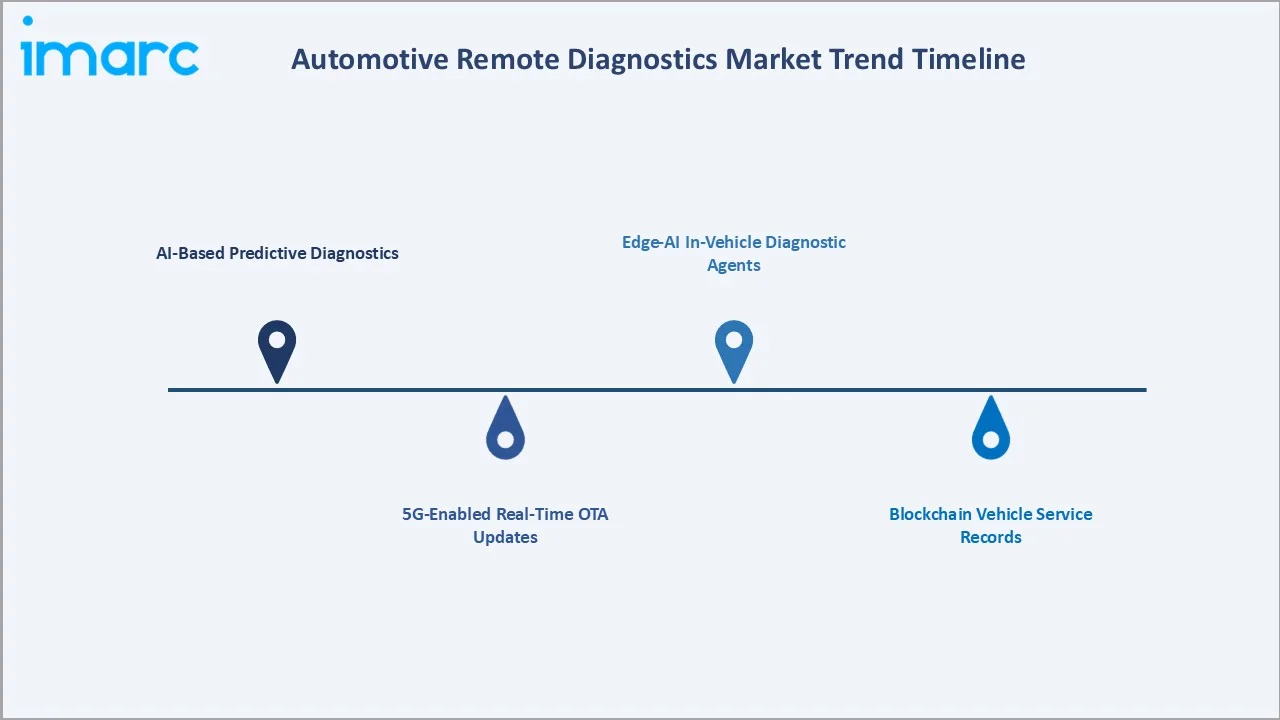

Emerging Market Trends

1. AI-Based Predictive Diagnostics

Machine-learning models trained on fleet-wide telematics data predict component failures days or weeks in advance. Suppliers and OEMs are embedding anomaly-detection engines directly into the cloud stack, shifting servicing from scheduled maintenance to truly predictive workflows with measurable uptime gains.

2. 5G-Enabled Real-Time OTA Updates

5G rollouts shrink update windows from hours to minutes while enabling bandwidth-intensive use cases such as full-stack ADAS calibration and high-definition sensor-data streaming, making continuous software refresh a baseline OEM capability across new model programs.

3. Blockchain Vehicle Service Records

Tamper-proof service and ownership histories support insurance, warranty, and resale workflows. Consortium blockchains linking OEMs, dealers, and insurers are being piloted to unify records across a vehicle's lifecycle and across multiple custodians in a trust-minimised environment.

4. Edge-AI In-Vehicle Diagnostic Agents

On-vehicle AI accelerators perform first-pass anomaly detection locally, filtering data before transmission. This reduces cloud bandwidth cost and latency while strengthening privacy posture in data-sensitive geographies such as the European Union and data-localised Asian markets.

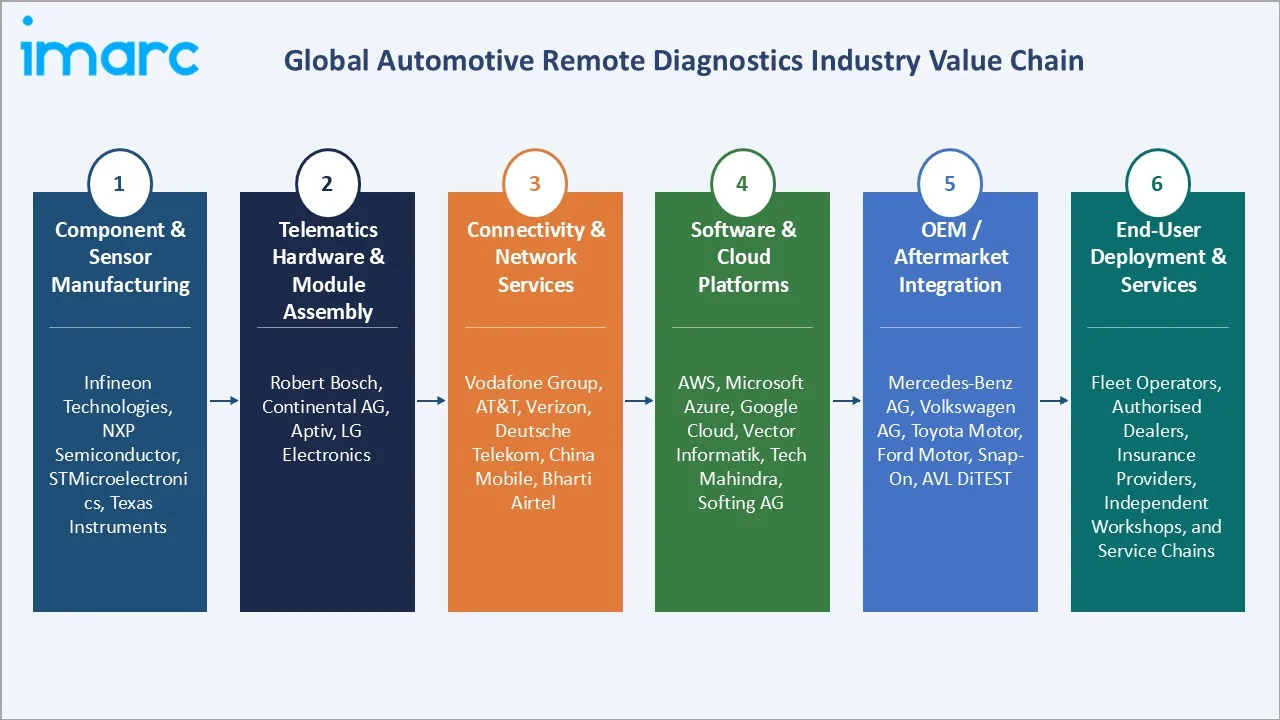

Industry Value Chain Analysis

The value chain spans sensor and ECU manufacturers upstream, through telematics module assemblers, software and cloud-platform developers, OEM and aftermarket integrators, and finally the end-user deployment layer covering fleets, dealers, insurers, and individual drivers.

|

Stage |

Key Players / Examples |

|

Component & Sensor Manufacturing |

Infineon Technologies, NXP Semiconductor, STMicroelectronics, Texas Instruments |

|

Telematics Hardware & Module Assembly |

Robert Bosch, Continental AG, Aptiv, LG Electronics |

|

Connectivity & Network Services |

Vodafone Group, AT&T, Verizon, Deutsche Telekom, China Mobile, Bharti Airtel |

|

Software & Cloud Platforms |

AWS, Microsoft Azure, Google Cloud, Vector Informatik, Tech Mahindra (India), Softing AG |

|

OEM / Aftermarket Integration |

Mercedes-Benz AG, Volkswagen AG, Toyota Motor, Ford Motor, Snap-On Incorporated, AVL DiTEST |

|

End-User Deployment & Services |

Fleet operators, authorised dealers, insurance providers, independent workshops, and service chains |

Value capture is shifting decisively toward the software and services layers. Hardware margins are compressing as scale economics take hold, while platform operators generate premium margins through recurring subscription, analytics, and cybersecurity services that compound over the vehicle lifecycle.

Technology Landscape

Cloud Platforms & Data Analytics

Hyperscaler-hosted platforms (AWS, Azure, Google Cloud) underpin most commercial deployments, offering elastic telemetry ingest, time-series databases, and integrated ML services. Multi-tenant architectures are standard, though large OEMs increasingly pursue dedicated-region deployments for data-sovereignty reasons.

Connectivity Standards

4G LTE remains the volume backbone through the forecast period, with 5G NR Release 16/17 capabilities unlocking low-latency diagnostics for mission-critical use cases. Dual-SIM and multi-IMSI strategies are widely deployed to ensure cross-border continuity for commercial vehicles operating internationally.

Cybersecurity & Compliance

UNECE R155/R156 compliance, ISO/SAE 21434 adherence, and hardware security modules (HSMs) in TCUs have become table stakes for OEM programs. Zero-trust architectures, certificate-based authentication, and continuous vulnerability management define the modern security baseline.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Diagnostic Equipment | 62.4% | 2025 |

| Connectivity | 4G LTE | 48.7% | 2025 |

| Vehicle Type | Passenger Cars | 🔒 | 2025 |

| Application | Vehicle Tracking | 🔒 | 2025 |

| Region | Europe | 34.8% | 2025 |

By Product Type

Diagnostic equipment accounts for 62.4% of 2025 revenue, encompassing onboard hardware, interface modules, scan tools, and plug-in OBD devices that form the sensing layer of every remote diagnostic deployment. Software follows at 37.6%, covering cloud platforms, analytics engines, and driver- and fleet-facing applications.

To access detailed market analysis, Request Sample

While hardware delivers current revenue scale, the software layer offers the highest growth leverage through subscription models, data monetisation, and AI-driven service upsell. Expect the hardware-software revenue mix to converge meaningfully over the forecast period as platform economics mature.

Within equipment, factory-fitted TCUs are displacing aftermarket OBD dongles in new vehicles, while plug-in devices retain strong aftermarket demand for older fleets. Software competition is intensifying as hyperscaler-native platforms challenge incumbent Tier-1 offerings on analytics depth and deployment agility.

By Connectivity

4G LTE dominates with 48.7% share in 2025, striking the optimal balance of coverage, latency, and cost for continuous telemetry. Legacy 3G (18.5%) persists in older vehicle parcs but is sunsetting rapidly as carriers refarm spectrum. Wi-Fi (17.3%) handles bulk data transfers during dwell time.

Bluetooth (15.5%) serves short-range diagnostic pairings with smartphones and handheld tools, particularly in aftermarket workshop settings. 5G migration accelerates from 2028 onward, supporting ultra-reliable low latency use cases, including live remote intervention and ADAS calibration.

Hybrid architectures combining cellular, Wi-Fi, and Bluetooth will persist to optimise cost, coverage, and battery efficiency across vehicle types. Satellite connectivity (via partnerships with LEO constellations) is emerging as a niche opportunity for heavy-duty fleets operating in remote geographies.

Regional Market Insights

|

Region |

Share 2025 |

Key Growth Drivers |

|

Europe |

34.8% |

Strict emission/safety norms, premium OEMs, UNECE R155 |

|

Asia Pacific |

27.6% |

China/India vehicle production, EV surge, 5G rollout |

|

North America |

22.9% |

Fleet telematics, insurance UBI, mature aftermarket |

|

Middle East and Africa |

8.1% |

GCC smart-city programs, logistics digitalisation |

|

Latin America |

6.6% |

Brazil/Mexico fleets, anti-theft mandates |

Europe leads with 34.8% share, underpinned by rigorous type-approval rules, UNECE R155/R156 mandates, and heavy adoption among German premium OEMs. The region's focus on sustainable mobility, combined with EU data protection regulations, creates both a demand tailwind and a compliance hurdle for suppliers.

The Asia Pacific, at 27.6%, grows fastest, thanks to Chinese connected-car volumes, India's EV acceleration, and Japan-Korea's sensor-hardware leadership. Local champions such as NIO, BYD, and Hyundai are pushing proprietary diagnostic platforms while attracting Tier-1 partnerships for scale.

North America (22.9%) benefits from deep fleet-telematics penetration, advanced usage-based insurance products, and OnStar's multi-decade head-start in consumer-grade remote services. Middle East & Africa and Latin America together contribute 14.7% today but are poised for above-average growth off a lower base.

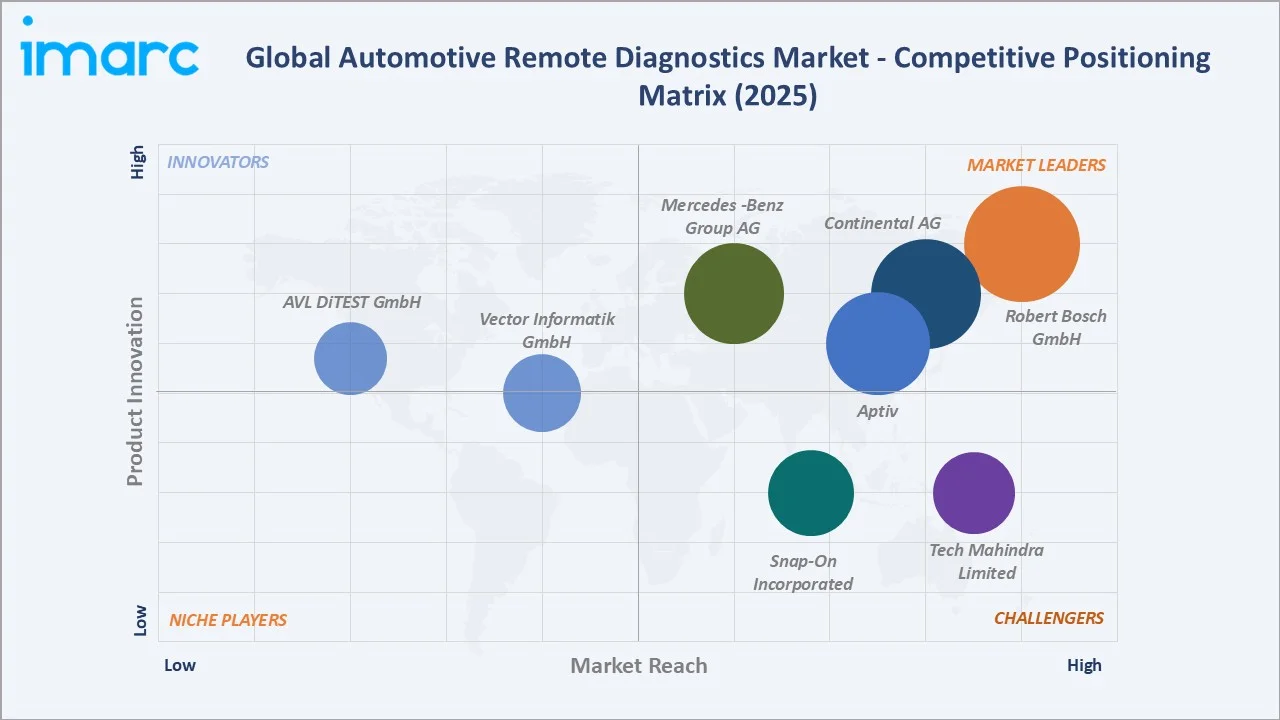

Competitive Landscape

The market is semi-consolidated with Tier-1 automotive suppliers, aftermarket specialists, and software platform providers competing on technology depth, OEM relationships, and cybersecurity certifications.

|

Company |

Key Platform / Brand |

Market Position |

Core Strength |

|

Robert Bosch GmbH |

ESI [tronic], Connected Repair, KTS series |

Leader |

OEM-grade breadth, R&D intensity, cybersecurity depth |

|

Continental AG |

ContiConnect |

Leader |

Vehicle networking heritage, zonal E/E architecture |

|

Aptiv |

Smart Vehicle Architecture (SVA) |

Leader |

Full-stack SVA, connected services platforms |

|

Mercedes-Benz Group AG |

Mercedes me connect |

Leader |

Premium OEM integration, end-to-end data ownership |

|

Snap-On Incorporated |

ZEUS+, TRITON-D10, Mitchell1 |

Challenger |

Aftermarket workshop dominance, franchise network |

|

Tech Mahindra Limited |

Connected vehicle platforms, DX services |

Challenger |

Software engineering scale, OEM IT services depth |

|

Vector Informatik GmbH |

CANoe, CANalyzer, Indigo |

Emerging |

Diagnostic tooling specialist, in-vehicle networks |

|

AVL DiTEST GmbH |

Diagnostic testers, ADAS calibration |

Emerging |

OEM-grade test equipment, ADAS calibration focus |

Key players include Robert Bosch GmbH, Continental AG, Aptiv, Mercedes -Benz Group AG, Snap-On Incorporated, Tech Mahindra Limited, Vector Informatik GmbH, AVL DiTEST GmbH, and others.

Key Company Profiles

Robert Bosch GmbH

Germany-headquartered Tier-1 supplier with deep telematics, ECU, and diagnostic-tool heritage. Its Mobility business generates roughly 61% of Group revenue and serves virtually every major OEM globally with integrated hardware, software, and cloud solutions for vehicle diagnostics.

- Product Portfolio: ESI[tronic] workshop platform, Connected Repair, Secure Truck Parking, OTA update management, and vehicle cloud services spanning passenger cars, commercial fleets, and two-wheelers. KTS series diagnostic testers are the industry standard across authorised workshops worldwide.

- Recent Developments: In October 2025, Bosch expanded its remote diagnostics service by introducing enhanced functionalities and extending compatibility across a broader range of vehicle brands. The upgraded offering enables workshop technicians to access expert support remotely, allowing complex diagnostic procedures, programming, and software updates to be carried out more efficiently without requiring in-house expertise. By increasing multi-brand coverage and adding new capabilities, Bosch aims to improve workshop productivity, reduce vehicle downtime, and provide more comprehensive support for increasingly complex vehicle systems.

- Strategic Focus: Scaling software-defined-vehicle services, deepening OTA and cybersecurity capabilities, and extending platform reach across EV and ADAS diagnostics.

Continental AG

Hannover-based automotive technology major organised around autonomous mobility, software, and vehicle networking solutions for leading OEMs. One of Europe's largest Tier-1 suppliers with a century-plus heritage in rubber, tires, and now connected-vehicle electronics.

- Product Portfolio: Telematics control units, vehicle-to-cloud gateways, fleet solutions, high-performance computer platforms, and integrated connectivity modules. ContiConnect Live telematics platforms, Continental Automotive Edge (CAEdge), and high-performance computer platforms.

- Recent Developments: In August 2023, Continental introduced a real-time digital tire monitoring solution through its ContiConnect Live platform, enabling continuous tracking of tire conditions for truck trailers, including those operating independently. The system uses sensor data transmitted via telematics units to provide live insights into tire pressure, temperature, and overall status, even when trailers are not actively connected, supported by a rechargeable battery for periodic updates.

- Strategic Focus: Accelerating the transition to zonal E/E architectures, software-defined vehicles, and platform-based monetisation of diagnostic data streams. Deepening software capabilities through targeted M&A and organic engineering investment focused on cloud-native platforms.

Aptiv

Switzerland-headquartered mobility technology company focused on Smart Vehicle Architecture, signal-and-power solutions, and advanced connected-services platforms. Spun off from Delphi Automotive in 2017 and now counted among the top global automotive electronics suppliers.

- Product Portfolio: Connected services platforms, smart vehicle compute, advanced telematics gateways, wireless charging, and data-management frameworks. Full-stack SVA solutions simplify OEM integration costs and enable lifecycle diagnostic and software-update services.

- Recent Developments: In April 2025, ServiceNow and Aptiv formed a strategic partnership to advance intelligent automation and operational resilience across telecommunications, automotive, enterprise, and industrial sectors. By combining ServiceNow’s AI-driven workflow platform with Aptiv’s edge-to-cloud and virtualization technologies, the collaboration aims to connect real-time data from complex systems with digital enterprise processes, enabling faster decision-making, improved efficiency, and greater operational agility.

- Strategic Focus: Building full-stack SVA solutions that simplify OEM integration costs and unlock scalable, lifecycle diagnostic and software-update services. Investing in AI-driven vehicle analytics and cybersecurity-by-design architectures to differentiate on future vehicle programs.

Market Concentration Analysis

The market is semi-consolidated. The top five suppliers hold roughly 46% of 2025 revenue, a concentration reinforced by OEM sourcing preferences for certified, financially resilient partners capable of meeting UNECE R155 cybersecurity and ISO/SAE 21434 engineering standards.

The remaining share is fragmented across regional specialists, emerging aftermarket entrants, and software-pure-play startups competing on speed, cloud-native depth, and vertical focus. Consolidation is likely to accelerate through 2028 as smaller players seek scale, OEM qualification depth, or complementary software capabilities.

Investment and Growth Opportunities

EV Diagnostics

Battery state-of-health monitoring, charging-system analytics, and powertrain software management define the next frontier of diagnostic innovation. Dedicated EV platforms command margin premiums versus legacy ICE tooling and are strategic differentiators for OEMs scaling their electric portfolios globally.

Fleet Telematics Platforms

Subscription-based platforms for commercial fleets combine diagnostics, routing, driver scoring, and fuel/energy optimisation. Consolidation of sub-scale fleet-management providers is accelerating as larger platforms bundle diagnostics with comprehensive operational value propositions.

Cybersecurity Services

UNECE-mandated cybersecurity management systems require continuous monitoring, patching, and certification support — a persistent, recurring service opportunity benefiting specialist security providers and Tier-1 partners alike. Managed security services are emerging as a distinct revenue line.

AI-Powered Analytics

Machine-learning models trained on fleet-wide data deliver predictive failure forecasts, driver coaching, and component-warranty analytics. Providers who can monetise this capability via API-based services or outcome-linked pricing models will capture outsized value in the forecast window.

Future Market Outlook (2026-2034)

Between 2026 and 2034, the market transitions from hardware-led revenue to software- and services-dominated growth. 5G rollouts, edge-AI adoption, and regulatory tightening will jointly reshape supplier economics, favouring platforms that can certify, scale, and monetise connected-vehicle data lifecycle-wide.

By 2034, remote diagnostics will be a default capability on every new vehicle, with differentiation migrating to analytics quality, user-experience depth, and ecosystem partnerships spanning insurance, mobility services, and energy providers. Market leaders will be those who turn raw telemetry into recurring, margin-rich digital services.

Autonomous and software-defined vehicles will further expand the diagnostic surface area, requiring continuous verification of perception stacks, decision algorithms, and over-the-air software integrity. This creates a long-duration innovation runway stretching well beyond the immediate forecast horizon.

Research Methodology

Primary Research

Structured interviews with OEM telematics lead, Tier-1 product managers, fleet operators, insurance analysts, and aftermarket distributors across mature and emerging markets, providing qualitative validation and forward-looking insight into technology adoption and buyer economics.

Secondary Research

Analysis of annual reports, regulatory filings, trade association data, patents, industry conferences, and curated proprietary databases covering connected-vehicle shipments, telematics revenues, and aftermarket trends across all major regions and vehicle segments.

Market Estimation

Bottom-up and top-down triangulation with cross-validation against connected-vehicle penetration, ARPU benchmarks, and regional GDP-automotive elasticity. Forecasts incorporate scenario analysis and sensitivity testing across regulatory and macroeconomic inflection points.

Automotive Remote Diagnostics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Diagnostic Equipment, Software |

| Connectivities Covered | 3G, 4G LTE, Wi-Fi, Bluetooth |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles |

| Applications Covered | Automatic Crash Notification, Vehicle Tracking, Vehicle Health Alert, Roadside Assistance |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, Continental AG, Aptiv, Mercedes-Benz Group AG, Snap-On Incorporated, Tech Mahindra Limited, Vector Informatik GmbH, AVL DiTEST GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Automotive Remote Diagnostics Market Report

The market was valued at USD 17.86 Billion in 2025 and is projected to reach USD 55.00 Billion by 2034, exhibiting a CAGR of 12.92%.

The market is expected to grow at a CAGR of 12.92% from 2026 to 2034.

Diagnostic Equipment leads with 62.4% share in 2025, driven by onboard interfaces, scan-tool deployments, and embedded telematics control units.

4G LTE commands 48.7% share in 2025, balancing coverage, latency, and cost for continuous telemetry across global vehicle parcs.

Europe leads with 34.8% share in 2025, supported by strict regulations, UNECE R155/R156 mandates, and premium OEM adoption.

Asia Pacific (27.6% share) is the fastest-growing region, led by China, India, and Japan-Korea sensor-hardware leadership.

Leading players include Robert Bosch GmbH, Continental AG, Aptiv, Mercedes -Benz Group AG, Snap-On Incorporated, Tech Mahindra Limited, Vector Informatik GmbH, AVL DiTEST GmbH, and others.

Connected-vehicle growth, EV and ADAS adoption, OEM telematics integration, and fleet-management economics together underpin demand expansion.

Data privacy and cybersecurity concerns, high implementation cost, and legacy-vehicle compatibility gaps are the most material restraints.

AI-based predictive diagnostics, 5G-enabled OTA updates, blockchain service records, and edge-AI in-vehicle diagnostic agents are reshaping the landscape.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)