Avocado Processing Market Size, Share, Trends and Forecast by Product Type, Application, Distribution Channel, and Region 2026-2034

Global Avocado Processing Market Size, Share, Trends & Forecast (2026-2034)

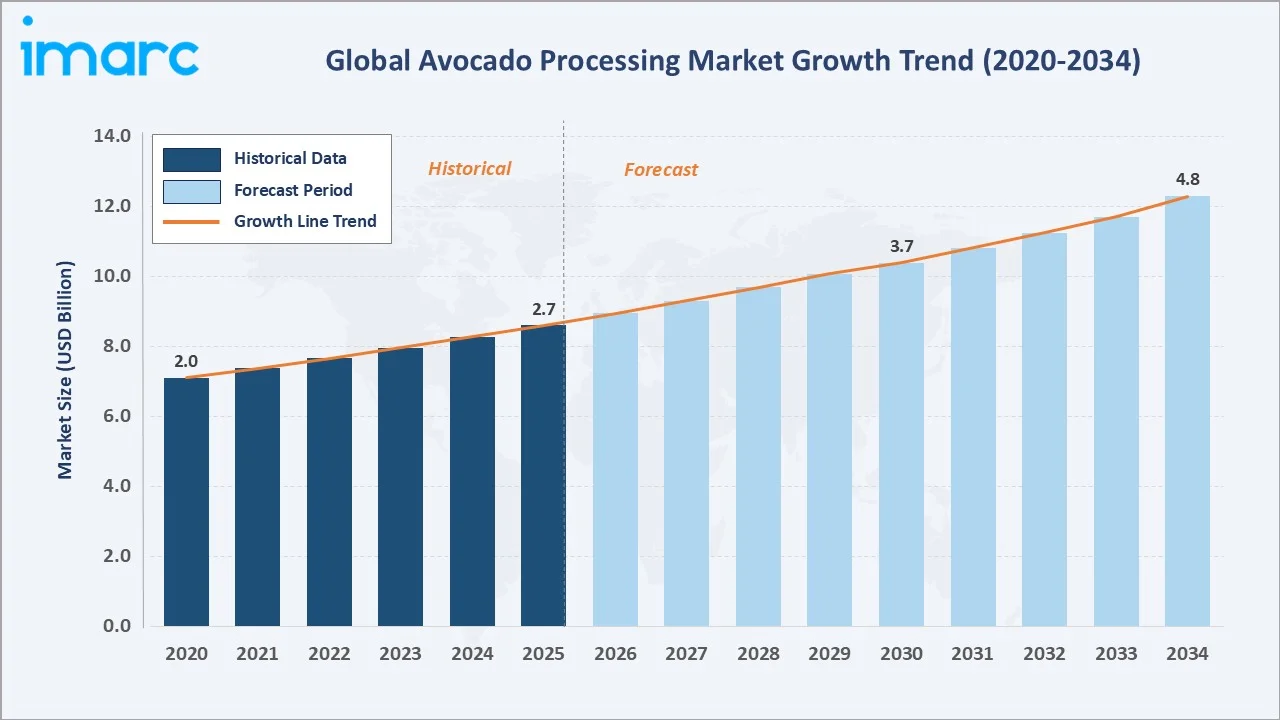

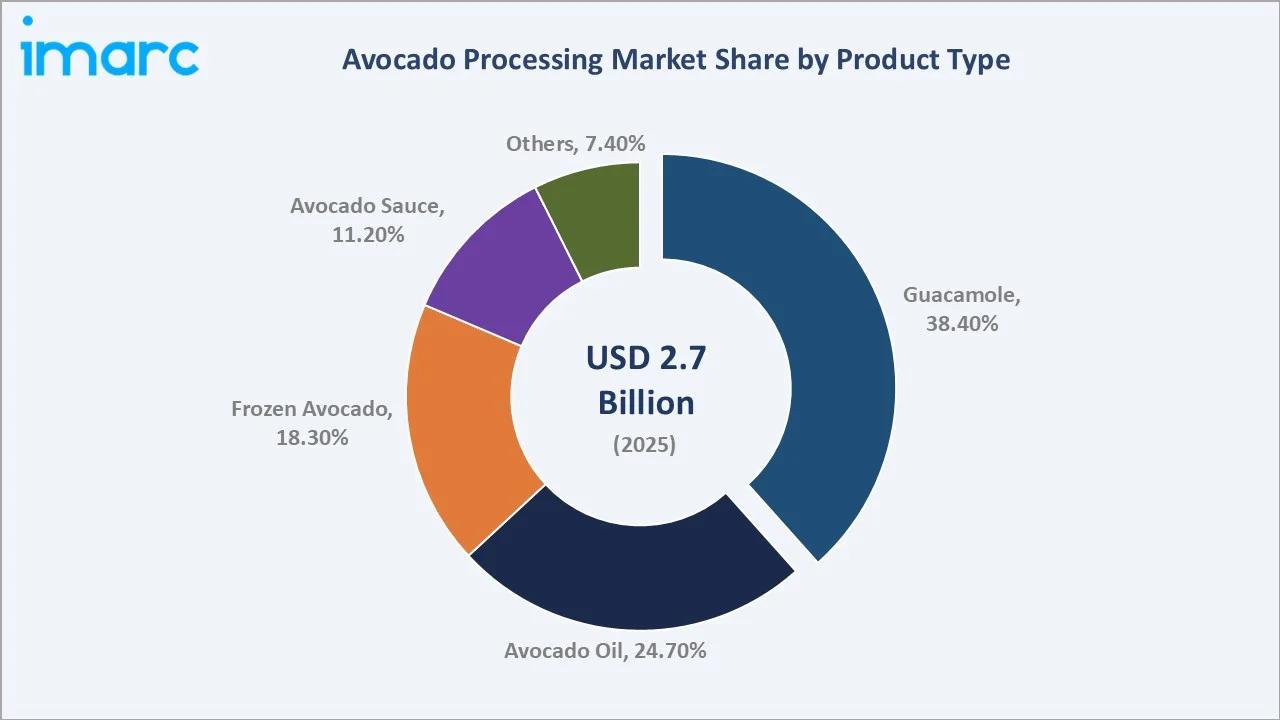

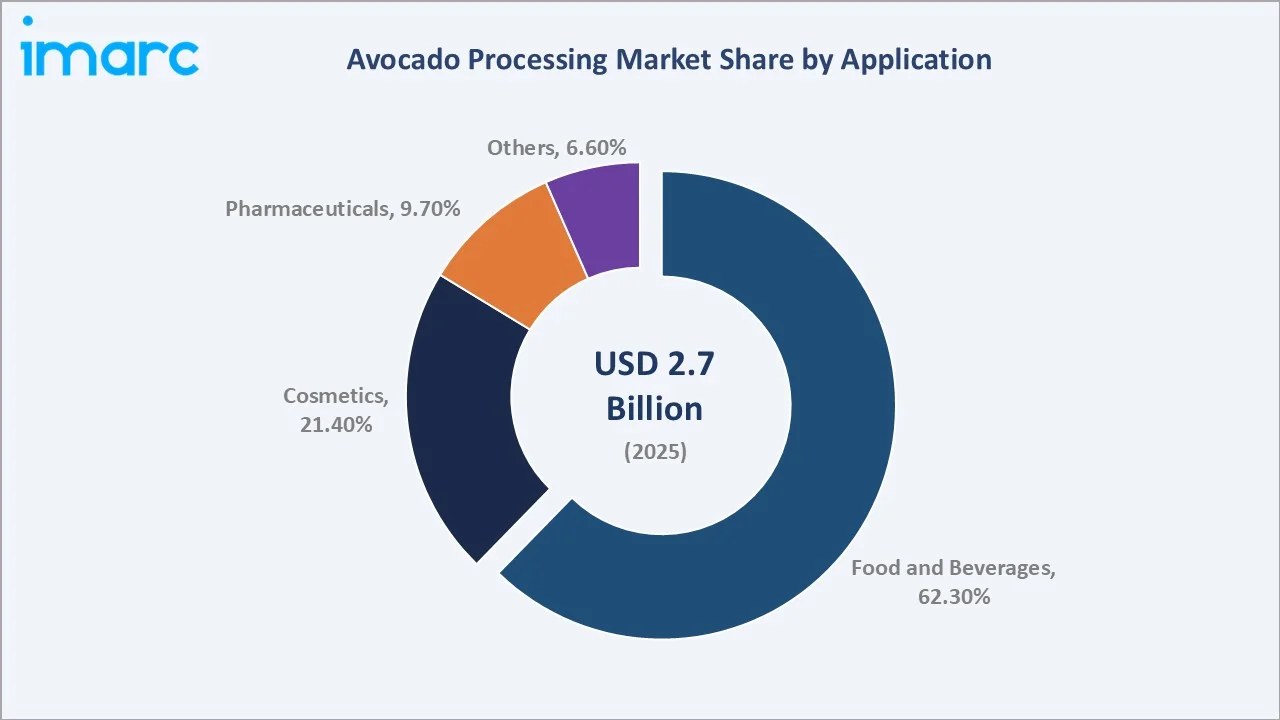

The global avocado processing market size was valued at USD 2.7 Billion in 2025 and is projected to reach USD 4.8 Billion by 2034, exhibiting a CAGR of 6.3% during the forecast period 2026-2034. Surging global demand for clean-label, plant-based food products, accelerating adoption of avocado oil in premium cooking and personal care formulations, and the rapid expansion of food service and retail channels across North America and Europe are driving avocado processing market growth. Guacamole leads the product type segment with a 38.4% share in 2025, while Food and Beverages dominates the application segment at 62.3%. North America accounts for 38.7% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.7 Billion |

|

Forecast Market Size (2034) |

USD 4.8 Billion |

|

CAGR (2026-2034) |

6.3% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~8.9%) |

|

Leading Product Type |

Guacamole (38.4%, 2025) |

|

Leading Application |

Food & Beverages (62.3%, 2025) |

The chart below illustrates the global avocado processing market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by rising consumer preference for avocado-based food products, cosmetics integration, and pharmaceutical applications.

To get more information on this market, Request Sample

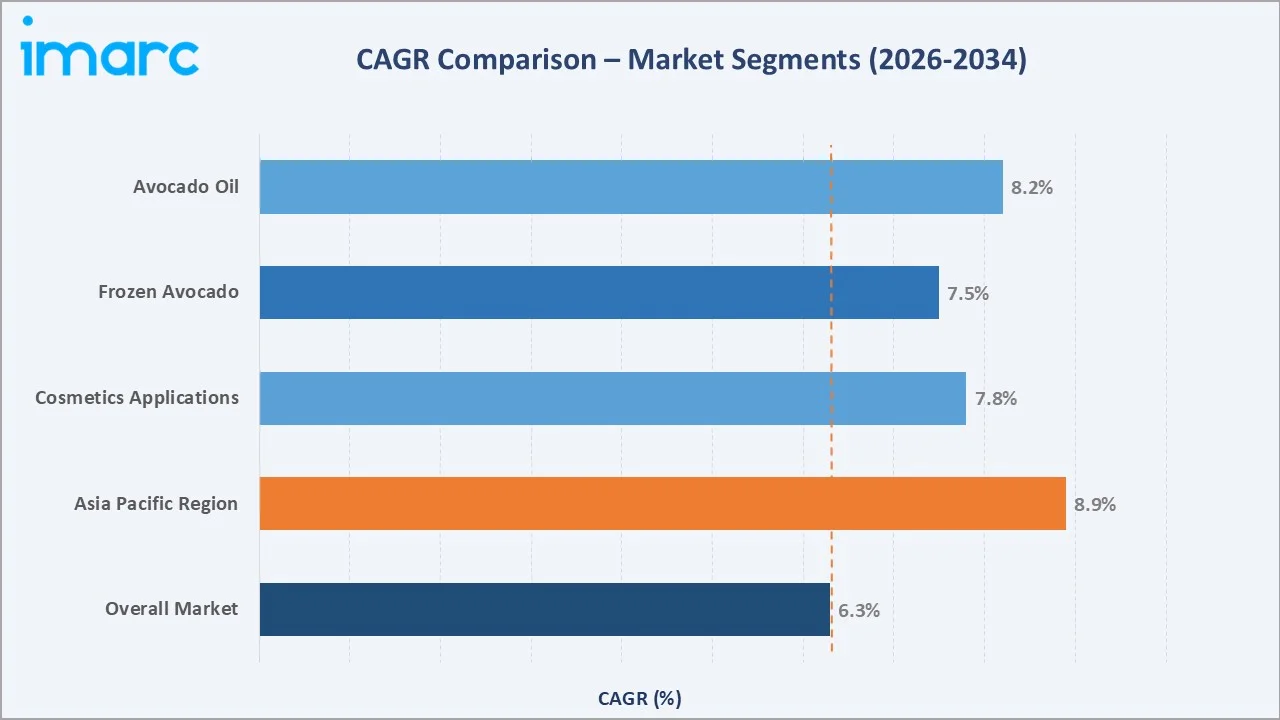

Segment-level CAGR comparisons highlight Asia Pacific and avocado oil sub-categories as the fastest-growing areas within the global avocado processing industry through 2034.

Executive Summary

The global avocado processing market is undergoing a structural transformation driven by the convergence of health and wellness trends, premiumization in food and cosmetics, and expanding supply chain infrastructure across key producing nations. Valued at USD 2.7 Billion in 2025, the market is forecast to reach USD 4.8 Billion by 2034 at a CAGR of 6.3%. According to an FAO report, global avocado exports grew by an estimated 20% in 2023, reaching 3 million metric tons, a figure that continues to rise annually. Each processing segment, guacamole, avocado oil, frozen avocado, and avocado sauce is benefiting from distinct demand catalysts ranging from quick-service restaurant procurement to premium skincare formulation.

Guacamole commands the dominant product type share at 38.4% in 2025, driven by sustained foodservice demand across North American restaurant chains and the rapid growth of retail guacamole in Europe and Asia. Avocado Oil at 24.7% represents the fastest-growing premium cooking oil sub-segment, fuelled by consumer migration from conventional vegetable oils toward high-smoke-point, nutrient-dense alternatives. Frozen Avocado at 18.3% is expanding rapidly, supported by supply chain efficiency gains in flash-freezing technology and the growing export trade from Latin American processors.

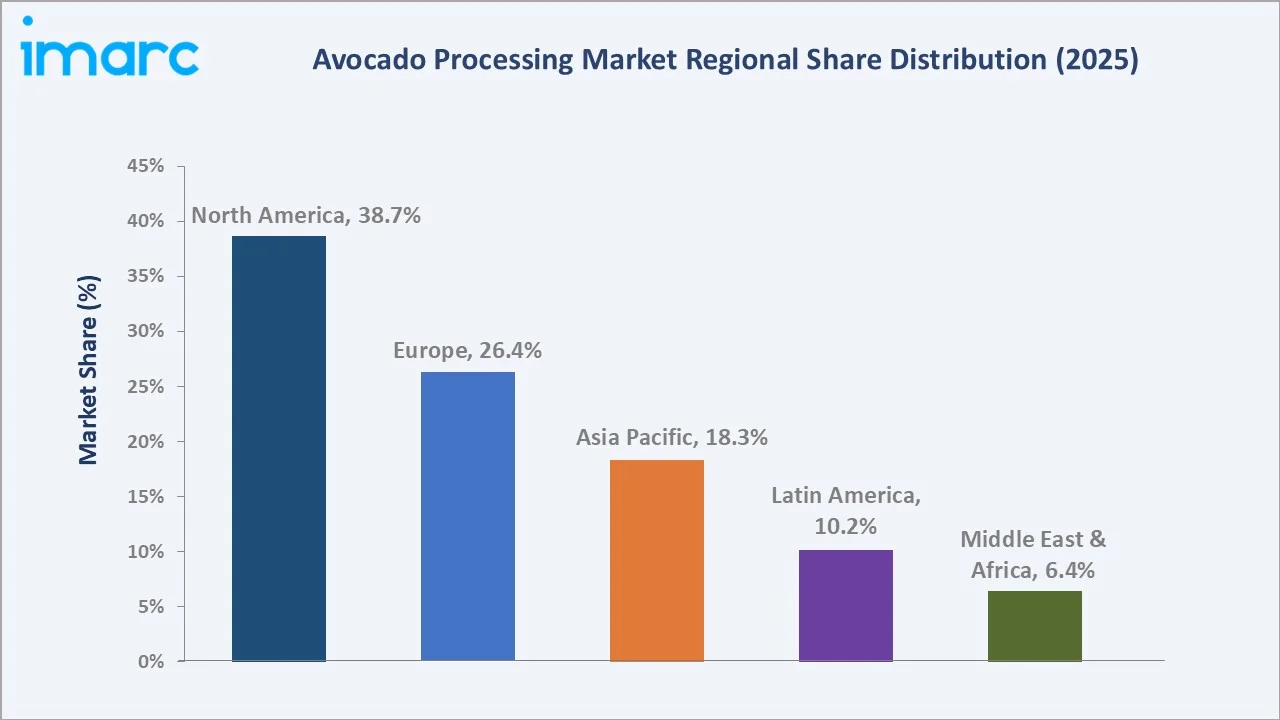

North America dominates with a 38.7% global revenue share in 2025. Europe holds 26.4% in 2025, driven by Germany, France, and the United Kingdom's rapidly growing avocado consumption, while Asia Pacific at 18.3% is the fastest-growing regional market, led by China, Japan, and South Korea's premium food retail expansion.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Guacamole – 38.4% share (2025) |

|

Fastest Growing Product |

Avocado Oil – ~8.2% CAGR (2026-2034) |

|

Leading Application |

Food & Beverages – 62.3% share (2025) |

|

Leading Region |

North America – 38.7% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – ~8.9% CAGR (2026-2034) |

|

Top Companies |

Calavo Growers, Del Monte Foods, Westfalia Fruit, Conagra Brands |

|

Market Opportunity |

Clean-label cosmetics and pharmaceuticals segment expansion |

Key Analytical Observations Supporting The Above Data:

- Guacamole's 38.4% dominance in 2025reflects the deeply entrenched role of avocado-based dips in North American foodservice, with major QSR chains collectively consuming over 1.5 billion pounds of guacamole annually.

- Avocado Oil at 24.7% is accelerating as health-conscious consumers replace refined vegetable oils; the global premium cooking oil market is projected to grow at 7.6% CAGR through 2030, amplifying demand for avocado oil.

- Frozen Avocado at 18.3% benefits from a 40–50% reduction in post-harvest waste achieved through modern cryogenic freezing, improving year-round supply consistency for processors and retailers.

- Food & Beverages application segment at 62.3% is underpinned by both retail and foodservice demand, with the global plant-based food market exceeding USD 30 billion in 2024.

- Cosmetics application at 21.4% is growing driven by the clean beauty movement, with avocado oil's high oleic acid content (55–75%) making it a premium ingredient in moisturizers, serums, and hair care products.

- North America's 38.7% share is anchored by the US avocado market exceeding USD 2.5 billion annually in retail sales alone, creating a robust demand base for processed avocado products across all formats.

Global Avocado Processing Market Overview

Avocado processing refers to the industrial transformation of fresh avocados into value-added products including guacamole, avocado oil, frozen avocado halves and slices, avocado sauce, avocado powder, and avocado-derived cosmetic and pharmaceutical ingredients. The processing ecosystem spans upstream cultivation and harvesting in tropical and subtropical producing regions, mid-stream extraction, homogenization, cold-press oil production, and flash-freezing operations, through to downstream distribution via retail, foodservice, cosmetics, and pharmaceutical channels.

Applications are broad: the food and beverage industry uses processed avocado for dips, spreads, dressings, smoothie ingredients, and baby food formulations; the cosmetics sector incorporates avocado oil and avocado butter as high-value emollients; the pharmaceutical industry leverages avocado-soybean unsaponifiables (ASU) for joint health applications. Macroeconomic enablers include rising disposable incomes in Asia Pacific, global health and wellness expenditure – projected to exceed USD 6 trillion by 2025 – and expanding cold chain infrastructure in emerging markets.

Market Dynamics

Market Drivers

- The global shift toward plant-based diets is a structural driver for avocado processing. With the plant-based food market valued at over USD 13.1 billion in 2025, and avocado positioned as a nutrient-dense, heart-healthy "superfood," consumer demand for processed avocado products in guacamole, spreads, and smoothie ingredients is growing robustly across all major markets. Rising Global Demand for Plant-Based and Functional Foods.

- Avocado oil's high smoke point of approximately 271°C, compared to olive oil's 190°C, and its rich oleic acid (55–75%) and vitamin E content make it a premium choice in both gourmet cooking and clean-label cosmetics. The global specialty oils market, projected to grow at 7.6% CAGR through 2030, is directly amplifying avocado oil processing demand. Expansion of Avocado Oil in Premium Cooking and Cosmetics.

- QSR expansion in North America and Europe is a primary demand driver for commercial guacamole and frozen avocado supply. Chipotle Mexican Grill alone uses approximately 44,000 pounds of avocados in each restaurant annually. From 2023-24, the US imported 2.48 billion pounds of avocados from Mexico, reflecting the depth of consumer adoption. Growth of Quick-Service Restaurant and Retail Foodservice Channels.

- Investment in refrigerated logistics infrastructure across Asia Pacific, Latin America, and the Middle East is enabling the export of frozen avocado products to previously underserved markets, expanding the addressable geographic opportunity for processors significantly. Cold Chain Infrastructure Expansion in Emerging Markets.

Market Restraints

- Avocado production is concentrated in a limited number of countries – Mexico, Indonesia, Colombia, Peru, and Kenya collectively account for over 60% of global supply. Climate-related disruptions, including drought in Mexican growing regions, pose significant supply chain risks to processors dependent on consistent raw material availability. Supply Chain Volatility and Climate Risk.

- Cold-press avocado oil extraction yields are typically 15–20% of raw fruit weight, and high-pressure processing (HPP) technology required for premium guacamole shelf-life extension involves significant capital expenditure, creating barriers for small and mid-tier processors. High Processing and Preservation Costs.

- Avocado cultivation requires approximately 70 liters of water per fruit, and growing regulatory and environmental scrutiny, particularly in Chile and Mexico's water-stressed regions, is generating supply-side risk and reputational challenges for processors. Water Scarcity Concerns and Regulatory Scrutiny.

Market Opportunities

- The global clean beauty market, projected to exceed USD 22 billion by 2030, represents a high-growth opportunity for avocado oil and avocado butter processors. Pharmaceutical-grade avocado-soybean unsaponifiables (ASU) command 3–5x price premiums over food-grade avocado oil, offering processors a high-margin diversification pathway. Clean-Label Cosmetics and Pharmaceutical Applications.

- China, Japan, and South Korea collectively represent the fastest-growing geographic opportunity. Per capita avocado consumption in China grew 300% between 2017 and 2023 from a low base, and the premium retail distribution networks of Alibaba's Hema Fresh and Japanese convenience store chains provide scalable market access for processed avocado importers. Asia Pacific Market Penetration.

- Avocado seeds and skins represent 25–30% of fruit weight and contain bioactive compounds including avocatin B, with demonstrated anti-cancer properties. The emerging nutraceutical valorization of avocado by-products offers processors a circular economy opportunity that could contribute 8–12% incremental revenue on existing raw material inputs. Avocado By-Product Processing.

Market Challenges

- Avocado wholesale prices can fluctuate by 30–50% year-on-year depending on harvest cycles, weather events, and Mexican export policy. This commodity price volatility directly compresses processor margins and complicates long-term supply contracts with retail and foodservice customers. Price Volatility of Raw Avocado.

- In markets where fresh avocado consumption is dominant, processors face the challenge of communicating the nutritional equivalence, convenience, and value proposition of processed avocado products, particularly frozen avocado and HPP guacamole, where consumer perception of "freshness" is a key purchase decision driver. Consumer Education on Processed vs. Fresh Avocado.

Emerging Market Trends

1. High-Pressure Processing (HPP) Revolutionizing Guacamole Shelf Life

HPP technology, which uses ultra-high pressure (400–600 MPa) rather than heat to eliminate pathogens, is enabling guacamole manufacturers to extend shelf life to 45–90 days without preservatives. This clean-label advantage is converting incremental retail category buyers and enabling cross-continental export of premium guacamole. The global HPP food market is projected to grow at 12.4% CAGR through 2030, driving adoption across the avocado processing sector.

2. Cold-Press Avocado Oil Premiumization

Consumer premiumization in edible oils is driving demand for extra-virgin, cold-pressed avocado oil, produced at temperatures below 49°C to preserve maximum phytosterol and vitamin content. Premium avocado oil commands retail prices of USD 15–35 per 500ml versus USD 4–8 for refined variants. This premiumization trend is reshaping oil processor investment decisions toward low-temperature extraction equipment and premium packaging across North America and Europe.

3. Avocado Ingredient Integration in Cosmetics and Skincare

The global cosmetics industry's pivot to plant-derived, clinically validated ingredients is accelerating avocado oil's penetration as a premium emollient in serums, moisturizers, and hair care products. In the United States, 63% of consumers prefer products with natural ingredients– is disproportionately incorporating avocado oil and avocado butter as hero ingredients, creating a new demand channel for cosmetic-grade avocado processors.

4. Sustainable and Regenerative Sourcing Certification

Retailers and food manufacturers are increasingly mandating Rainforest Alliance, Fair Trade, and Sustainability Alliance certifications for avocado supply chains. Certified processors command 12–18% price premiums and preferential shelf placement in European retail. This sustainability trend is reshaping sourcing relationships and creating compliance investment requirements across the global avocado processing value chain.

5. E-Commerce and Direct-to-Consumer Avocado Product Growth

Online retail penetration of processed avocado products – including subscription avocado oil deliveries, DTC guacamole kits, and premium frozen avocado packs – grew at over 25% CAGR from 2020 to 2024. Platforms such as Amazon, Alibaba, and Mercado Libre are enabling small and mid-scale artisan avocado processors to access global consumer markets previously inaccessible without conventional retail distribution agreements.

Industry Value Chain Analysis

The avocado processing value chain spans five integrated stages from raw fruit cultivation through end-consumer delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements specific to the perishable commodity and value-added processing sectors.

|

Value Chain Stage |

Key Players / Examples |

|

Cultivation & Raw Material Supply |

Avocado farmers in Mexico, Peru, Kenya, Indonesia, Colombia; agricultural co-operatives |

|

Primary Processing |

Fruit graders, ripening centers, extraction facilities; Calavo Growers, Westfalia Fruit, Mission Produce |

|

Secondary Processing & Manufacturing |

Guacamole producers, avocado oil extractors, frozen avocado processors; Del Monte Foods, Conagra Brands |

|

Distribution & Logistics |

Cold chain operators, freight forwarders, retail distributors; US Foods, Sysco, regional importers |

|

End Users |

QSR chains, food manufacturers, cosmetics companies, pharmaceutical formulators, retail consumers |

Technology Landscape in the Avocado Processing Industry

High-Pressure Processing (HPP) and Pasteurization

HPP technology has fundamentally transformed premium guacamole production by enabling clean-label, preservative-free products with 45–90 day shelf life. Systems from Hiperbaric and Avure Technologies, priced at USD 1–4 million per unit, are standard capital equipment for any guacamole processor targeting premium retail. Traditional thermal pasteurization, while cheaper, compromises color and flavor, limiting its application to commodity foodservice formats.

Cold-Press and Centrifugal Oil Extraction

Cold-press expeller extraction preserves avocado oil's nutritional profile and qualifies products for "extra-virgin" labeling. Alfa Laval and GEA Group manufacture the primary industrial centrifugal decanters used in large-scale avocado oil production. Extraction yields of 15–20% of fresh fruit weight require efficient raw material procurement to maintain processing economics, with oil yield optimization representing a key R&D focus for leading processors.

Cryogenic and IQF Freezing Technology

Individual Quick Freezing (IQF) technology using liquid nitrogen or mechanical tunnel freezers at temperatures of -40°C enables frozen avocado halves and slices to retain over 90% of fresh fruit nutritional content. This technology, provided by companies including Air Products, JBT FoodTech, and GEA Group, is critical infrastructure for export-oriented frozen avocado processors in Peru, Chile, and South Africa targeting European and Asian markets.

Smart Ripening Management Systems

Controlled atmosphere ripening rooms using ethylene gas management software, supplied by companies including Catalytic Generators and Decco Worldwide, enable processors and distributors to synchronize avocado ripening precisely for retail and foodservice demand calendars. Real-time IoT sensor monitoring of CO₂, O₂, ethylene, and temperature levels in ripening rooms reduces waste by 15–25% compared to unmanaged ripening operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Guacamole |

38.4% |

2025 |

|

Application |

Food and Beverages |

62.3% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

North America |

38.7% |

2025 |

By Product Type

Guacamole commands a 38.4% majority share in 2025, reflecting deeply entrenched North American consumption patterns and the rapid retail expansion of guacamole in European supermarkets. The product benefits from the HPP clean-label premium positioning and the ongoing growth of Mexican and Tex-Mex cuisine globally. Chipotle, Whole Foods Market, and Costco are among the largest volume purchasers driving consistent industrial demand for guacamole processors.

To access detailed market analysis, Request Sample

Avocado Oil at 24.7% in 2025 is driven by consumer premiumization in edible oils, clean-label cosmetics formulation, and the demonstrated health benefits of avocado oil's high monounsaturated fat content – with oleic acid representing 55–75% of fatty acid composition. Frozen Avocado at 18.3% benefits from year-round supply capability and the growing export trade, particularly from Peruvian and Chilean processors to European and Asian markets.

Avocado Sauce at 11.2% is the fastest-growing product format, expanding beyond traditional Mexican cuisine into mainstream condiment applications. Others at 7.4% include avocado powder, avocado butter, and avocado-based baby food formulations, each representing nascent but high-growth sub-categories within the broader product landscape.

By Application

Food and Beverages dominates at 62.3% in 2025, driven by both retail and foodservice channels. The QSR sector's heavy guacamole demand, retail avocado oil grocery penetration, and the rapid integration of frozen avocado into smoothie bowl and açaí bowl foodservice formats collectively underpin the F&B application's dominant position across all major markets.

Cosmetics at 21.4% represents the highest-growth application segment, fuelled by the global clean beauty movement, which now accounts for over 40% of premium skincare launches in the US and Europe. Avocado oil and avocado butter's clinically validated moisturizing, anti-inflammatory, and anti-aging properties position them as premium hero ingredients in serums, face creams, hair masks, and lip care products.

Pharmaceuticals at 9.7% is primarily driven by avocado-soybean unsaponifiables (ASU), which have EU regulatory approval as a symptomatic slow-acting drug for osteoarthritis in France, Belgium, and Portugal. Others at 6.6% encompasses animal nutrition, nutraceutical supplements, and emerging industrial lubricant applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.7% |

US guacamole dominance, premium cooking oil retail, health-food retail expansion, QSR procurement volume |

|

Europe |

26.4% |

Clean-label cosmetics demand, premium food retail, sustainability certification requirements, UK/Germany/France avocado adoption |

|

Asia Pacific |

18.3% |

China premium retail growth, Japan/Korea cosmetics demand, cold chain investment, per capita consumption convergence |

|

Latin America |

10.2% |

Mexico/Peru/Colombia production base, domestic processing investment, export-oriented frozen avocado growth |

|

Middle East & Africa |

6.4% |

Kenya/South Africa emerging processing hubs, GCC premium food retail, growing cosmetics segment |

North America commands a 38.7% global revenue share in 2025, the most dominant regional position in the avocado processing market. The United States is the single most important national market, combining the world's largest guacamole consumption base with rapidly expanding avocado oil retail penetration. US avocado retail sales exceeded USD 2.5 billion in 2024 (Hass Avocado Board), with California and Florida producing approximately 80 million pounds domestically while importing over 2.1 billion pounds annually from Mexico, creating a structural demand advantage for US-based processors.

Europe at 26.4% in 2025 is the second-largest market, led by the United Kingdom, Germany, France, Spain, and the Netherlands. European consumer demand is characterized by strong clean-label requirements, sustainability certification mandates (Rainforest Alliance, Fair Trade), and premium positioning expectations. The UK's avocado market alone reached approximately GBP 400 million in 2024, with significant growth in guacamole retail and avocado oil in both food and cosmetics segments.

Asia Pacific at 18.3% is the fastest-growing regional market at approximately 8.9% CAGR through 2034, driven by China's premium food retail expansion via Alibaba Hema Fresh and JD Fresh, Japan and South Korea's cosmetics-grade avocado ingredient demand, and the growing fitness and wellness culture driving avocado adoption among urban millennials across Southeast Asia.

Latin America at 10.2% represents both the primary production base and an increasingly significant domestic consumption market. Mexico, Peru, Colombia, and Chile collectively produce over 55% of global avocados and are investing in value-added processing to capture margin above raw commodity export economics. Middle East and Africa at 6.4% features Kenya and South Africa as emerging export-oriented processing hubs targeting European markets.

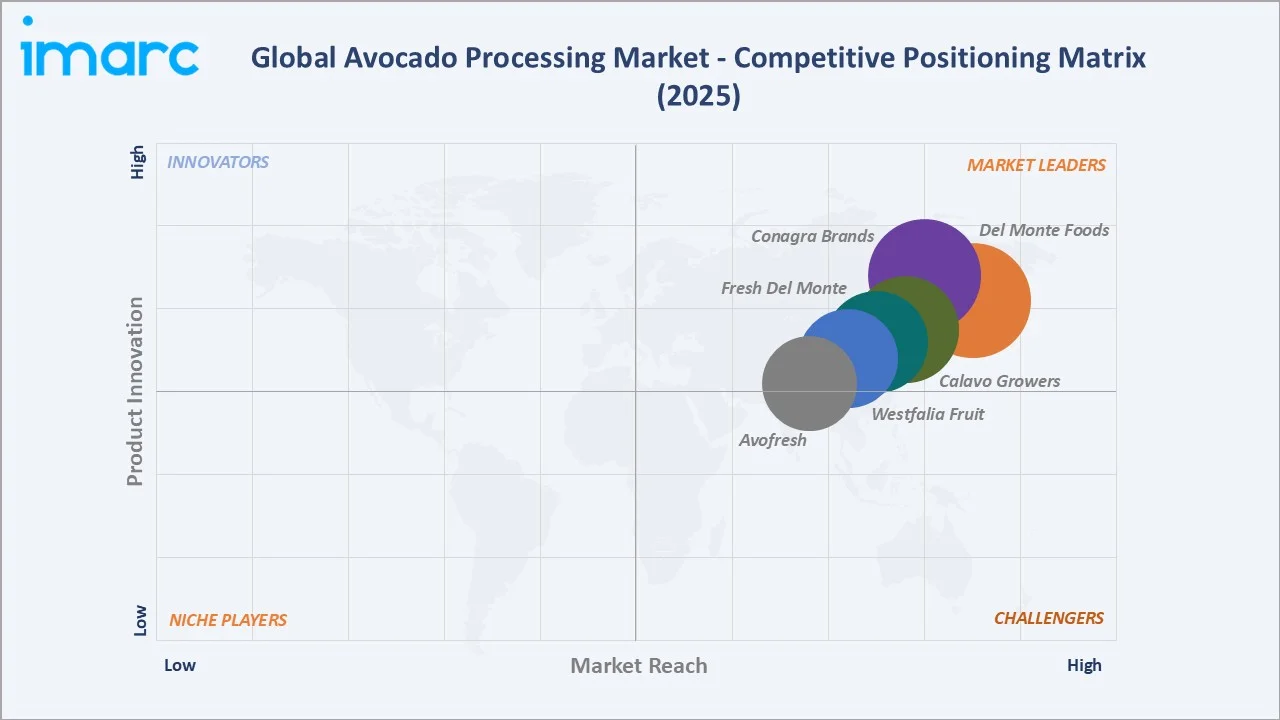

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

Core Strength |

|

Calavo Growers Inc. |

Calavo |

Leader |

Guacamole, fresh-cut avocado, avocado oil; US retail/foodservice |

|

Del Monte Foods Inc. |

Del Monte |

Leader |

Processed fruit and vegetables, avocado-based products, global distribution |

|

Westfalia Fruit Group |

Westfalia |

Leader |

Vertically integrated; avocado processing, oil extraction, global export |

|

Conagra Brands Inc. |

Frontera / Hunt's |

Leader |

Guacamole, salsa, condiments; strong US retail channel |

|

Fresh Del Monte Produce Inc. |

Del Monte Fresh |

Challenger |

Fresh and processed avocado, distribution to retail and foodservice |

|

Avofresh |

Avofresh |

Emerging |

Premium HPP guacamole; European retail market specialist |

The avocado processing competitive landscape is characterized by a mix of vertically integrated global agri-food corporations with deep retail distribution, specialist avocado-focused processors with strong supply chain relationships in Mexico and Peru, and emerging regional players targeting premium guacamole and avocado oil segments in Europe and Asia Pacific.

Key Company Profiles

Calavo Growers Inc.

Calavo Growers is a leading global avocado company headquartered in Santa Paula, California, specializing in the procurement, processing, packaging, and marketing of avocados and avocado products. The company operates three segments: Fresh products, Calavo Foods (processed guacamole and avocado products), and RFG (Renaissance Food Group, fresh-cut and ready-to-eat produce).

- Product & Platform Portfolio: Fresh avocados, guacamole (refrigerated and HPP), avocado slices, avocado-based dips, fresh-cut fruit and vegetable combinations.

- Recent Developments: In fiscal year 2024, Calavo reported consolidated revenue of approximately USD 741 million, with its Calavo Foods segment experiencing growth driven by expanded HPP guacamole distribution across US and Canadian retail chains. The company expanded its processing capacity in Uruapan, Mexico in 2024 to increase guacamole production volume by 15%.

- Strategic Focus: Calavo's strategy focuses on vertical integration from Mexican avocado orchards through US processing and retail distribution, premium HPP guacamole development for clean-label retail positioning, and expansion of the RFG fresh-cut segment to diversify revenue. International market expansion in Europe and Asia Pacific represents the primary growth investment priority.

Westfalia Fruit Group

Westfalia Fruit is a vertically integrated global avocado group headquartered in South Africa, operating across the full value chain from avocado cultivation and primary processing through export logistics and market development across Europe, North America, and Asia. The group owns orchards in South Africa, Mozambique, and Latin America, and operates processing facilities on three continents.

- Product & Platform Portfolio: Fresh avocados, cold-pressed avocado oil, frozen avocado, avocado pulp, avocado-based cosmetic ingredients, and avocado paste for foodservice.

- Recent Developments: In 2024, Westfalia expanded its avocado oil extraction facility in South Africa to increase annual processing capacity to over 500 tonnes of avocado oil, targeting European premium retail and cosmetics ingredient buyers. The group also launched a certified organic avocado oil line in 2024, addressing growing retailer demand for organic certifications in European markets.

- Strategic Focus: Westfalia's strategy leverages its unique Southern Hemisphere cultivation base to supply Northern Hemisphere markets during the Northern Hemisphere off-season, ensuring year-round supply consistency. The company is investing in premium avocado oil processing, cosmetics-grade ingredient certification, and market development in China and Japan as the highest-priority geographic expansion opportunities.

Conagra Brands, Inc.

Conagra Brands is a major US consumer packaged foods company with a broad portfolio spanning frozen, refrigerated, and shelf-stable foods. Its avocado processing presence is primarily through its Frontera brand guacamole and related Mexican cuisine condiment products, distributed through major US retail chains including Walmart, Target, and Kroger.

- Product & Platform Portfolio: Frontera Guacamole (authentic recipe, HPP), Frontera Avocado Salsa, Hunt's tomato products, numerous snack and condiment brands.

- Recent Developments: In fiscal year 2024, Conagra reported revenues of approximately USD 11.5 billion across all segments. The Refrigerated & Frozen segment, which includes guacamole products, grew at approximately 3.2% in the US retail market. Conagra expanded the Frontera guacamole line with new flavor variants in 2024, targeting premium retail and club store channels.

- Strategic Focus: Conagra's avocado processing strategy is oriented around brand leverage and retail distribution scale rather than vertical integration, partnering with Mexican avocado processors for raw material supply. The company is investing in premium HPP guacamole shelf-life innovation, packaging sustainability initiatives, and e-commerce channel development to align with shifting US grocery retail dynamics.

Market Concentration Analysis

The global avocado processing market exhibits moderate fragmentation, with the top five players – Calavo Growers, Westfalia Fruit, Del Monte Foods, Conagra Brands, and Fresh Del Monte Produce – collectively accounting for approximately 30–38% of global market revenue in 2025. This moderate concentration reflects the market's structural diversity: guacamole manufacturing is relatively concentrated among North American food processors, while avocado oil and frozen avocado segments are served by a larger number of mid-tier regional processors, particularly in Mexico, Peru, South Africa, and Chile.

The avocado processing competitive landscape is experiencing bifurcated structural dynamics. At the premium retail tier, consolidation is occurring as HPP technology investment and clean-label certification costs create capital barriers that favor large-scale processors. Simultaneously, the cosmetics and pharmaceutical ingredient segments are generating specialty market entry opportunities for niche processors offering certified organic, food-grade cosmetic, or pharmaceutical-grade avocado oil products.

M&A activity in the sector has been moderate, with notable transactions including Mission Produce's acquisition of Simcha Organic in 2021 and ongoing investment in processing capacity expansion by Westfalia Fruit and Calavo Growers. The Chinese market entry opportunity is attracting both JV and greenfield investment by international processors seeking early positioning in the world's fastest-growing avocado consumption market.

Investment & Growth Opportunities

Fastest-Growing Segments

Avocado Oil processing is the highest-growth product segment at ~8.2% CAGR through 2034, driven by premium cooking oil market expansion and cosmetics ingredient demand. The cosmetics application segment at approximately 7.8% CAGR through 2034 represents the highest-margin growth opportunity, as cosmetics-grade avocado oil commands 3–5x price premiums over food-grade equivalents. Frozen Avocado is growing at ~7.5% CAGR, enabled by IQF technology improvements reducing waste and expanding export trade flows from Latin America to European and Asian markets.

Emerging Market Expansion

Asia Pacific, and specifically China's premium food retail sector, represents the single most significant untapped geographic opportunity. Per capita avocado consumption in China is currently below 0.05 kg annually versus 3.5 kg in the US, suggesting a 70x consumption gap that represents a decade-long structural growth opportunity as Chinese middle-class food premiumization continues. Japanese and South Korean cosmetics-grade avocado ingredient markets are further near-term high-premium opportunities.

Venture & Private Investment Trends

Private equity investment in avocado supply chain infrastructure is accelerating, with Mission Produce's acquisitions, Westfalia Fruit's expansion capital investments, and multiple VC-backed DTC avocado product start-ups collectively reflecting growing institutional confidence in long-term avocado demand fundamentals. Sustainable sourcing certification infrastructure, water-efficient cultivation technology, and avocado by-product nutraceutical start-ups are attracting early-stage investment, reflecting the sector's evolving ESG investment thesis.

Future Market Outlook (2026-2034)

The global avocado processing market forecast projects steady value expansion from USD 2.7 Billion in 2025 to USD 4.8 Billion by 2034 at a CAGR of 6.3%, underpinned by sustained growth in all major product types, geographic market expansion particularly in Asia Pacific, and the progressive premiumization of avocado products in both food and non-food applications.

Three structural trends are most likely to reshape the avocado processing market through 2034. First, sustainability and supply chain transparency will become a market-entry requirement in European retail by 2027–2028, driving compliance investment across the value chain and rewarding processors with established Rainforest Alliance or similar certification. Second, the Asia Pacific market is forecast to increase its revenue share from 18.3% in 2025 to approximately 25% by 2034, driven by China, Japan, South Korea, and Southeast Asian consumption growth.

By 2034, the avocado processing industry is forecast to complete its transformation from a commodity dip ingredient sector to a multi-application premium ingredient platform spanning food, cosmetics, pharmaceuticals, and nutraceuticals. Processors that invest in HPP technology, pharmaceutical-grade oil extraction, and diversified application development will capture disproportionate margin expansion relative to commodity guacamole and bulk frozen avocado producers.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews conducted in 2024–2025 with avocado processing industry stakeholders including supply chain directors at Tier-1 avocado processors, retail category managers at major grocery retailers, cosmetics ingredient procurement managers, and institutional investors in agri-food processing. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include the Hass Avocado Board Market Research, FAO Global Avocado Production Statistics (2024), USDA Agricultural Marketing Service reports, International Trade Centre (ITC) avocado trade data, Euromonitor International food retail reports, the Global Cold Press Oils Association, Mintel Clean Beauty Intelligence reports, and company annual reports and investor presentations from Calavo Growers, Del Monte Foods, Westfalia Fruit, and Conagra Brands.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, per capita food expenditure trends, avocado production volume projections, cold chain investment data, and historical avocado consumption evolution patterns. Scenario analysis (base, optimistic, and conservative) was performed to account for supply chain volatility, climate risk, and macroeconomic uncertainty.

Avocado Processing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Guacamole, Avocado Oil, Frozen Avocado, Avocado Sauce, Others |

| Applications Covered | Food and Beverages, Cosmetics, Pharmaceuticals, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Calavo Growers Inc., Del Monte Foods, Inc., Westfalia Fruit Group, Conagra Brands Inc., Fresh Del Monte Produce Inc., Avofresh, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the avocado processing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global avocado processing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the avocado processing industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Avocado Processing Market Report

The global avocado processing market was valued at USD 2.7 Billion in 2025, driven by strong guacamole demand in North America and growing avocado oil adoption globally.

The market is projected to reach USD 4.8 Billion by 2034, growing at a CAGR of 6.3% during 2026-2034, driven by premiumization, cosmetics expansion, and Asia Pacific growth.

Guacamole leads with a 38.4% share in 2025, driven by North American QSR procurement, US retail channel growth, and HPP clean-label premium positioning.

Food and Beverages dominates at 62.3% in 2025, reflecting broad use in retail dips, cooking oils, smoothie ingredients, and foodservice menu applications globally.

North America leads with 38.7% share in 2025, anchored by the US as the world's largest guacamole consumption market and premium avocado oil retail destination.

Key drivers include plant-based food trends, avocado oil premiumization, QSR guacamole demand, cold chain expansion in Asia Pacific, and clean beauty cosmetics growth.

Asia Pacific is the fastest-growing region at approximately 8.9% CAGR through 2034, led by China's premium food retail expansion and Japan's cosmetics ingredient demand.

Leading companies include Calavo Growers, Del Monte Foods, Westfalia Fruit, Conagra Brands, Fresh Del Monte Produce, and Avofresh.

HPP extends guacamole shelf life to 45–90 days without preservatives, enabling clean-label premium retail positioning and cross-continental export, supporting 12.4% CAGR in HPP food.

Key opportunities include Asia Pacific market penetration, cosmetics-grade avocado oil premiumization, pharmaceutical ASU ingredient growth, and avocado by-product nutraceutical valorization.

Major challenges include avocado price volatility of 30–50% year-on-year, supply chain climate risk, water scarcity in Mexican growing regions, and HPP capital expenditure barriers.

Cosmetics applications hold 21.4% market share in 2025, growing at approximately 7.8% CAGR through 2034, driven by clean beauty trends and avocado oil's proven moisturizing properties.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)