Baby Feeding Bottles Market Size, Share, Trends and Forecast by Material Type, Capacity, Distribution Channel, and Region 2026-2034

Baby Feeding Bottles Market Size, Share, Trends & Forecast (2026-2034)

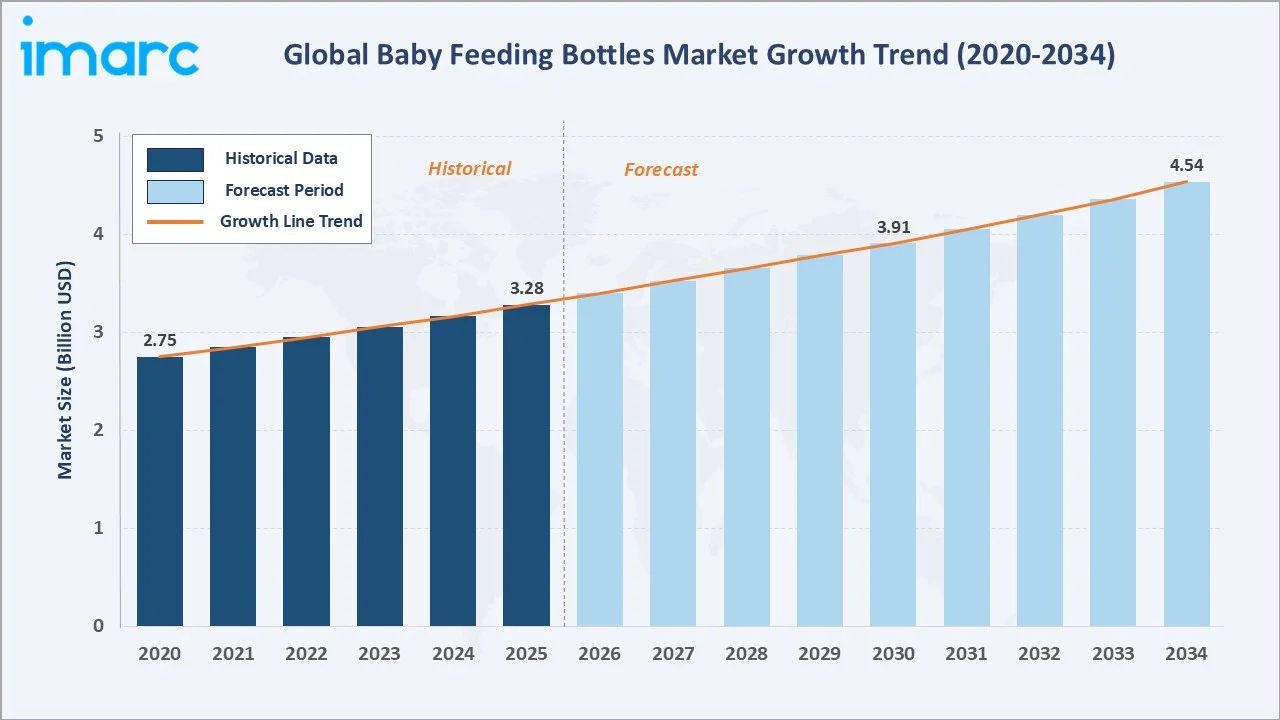

The global baby feeding bottles market size reached USD 3.28 Billion in 2025 and is projected to reach USD 4.54 Billion by 2034, exhibiting a CAGR of 3.58% during 2026-2034. Rising birth rates, growing working mother population, heightened awareness of BPA-free safe materials, and rapid e-commerce expansion are the primary forces driving market growth.

Plastic dominates material type at 46.7%, while 4.1 to 6 Oz capacity leads at 34.6%. North America commands a dominant 33.8% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.28 Billion |

|

Forecast Market Size (2034) |

USD 4.54 Billion |

|

CAGR (2026-2034) |

3.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (33.8% share, 2025) |

|

Second Region |

Asia-Pacific (27.6% share, 2025) |

|

Leading Material Type |

Plastic (46.7%, 2025) |

|

Leading Capacity |

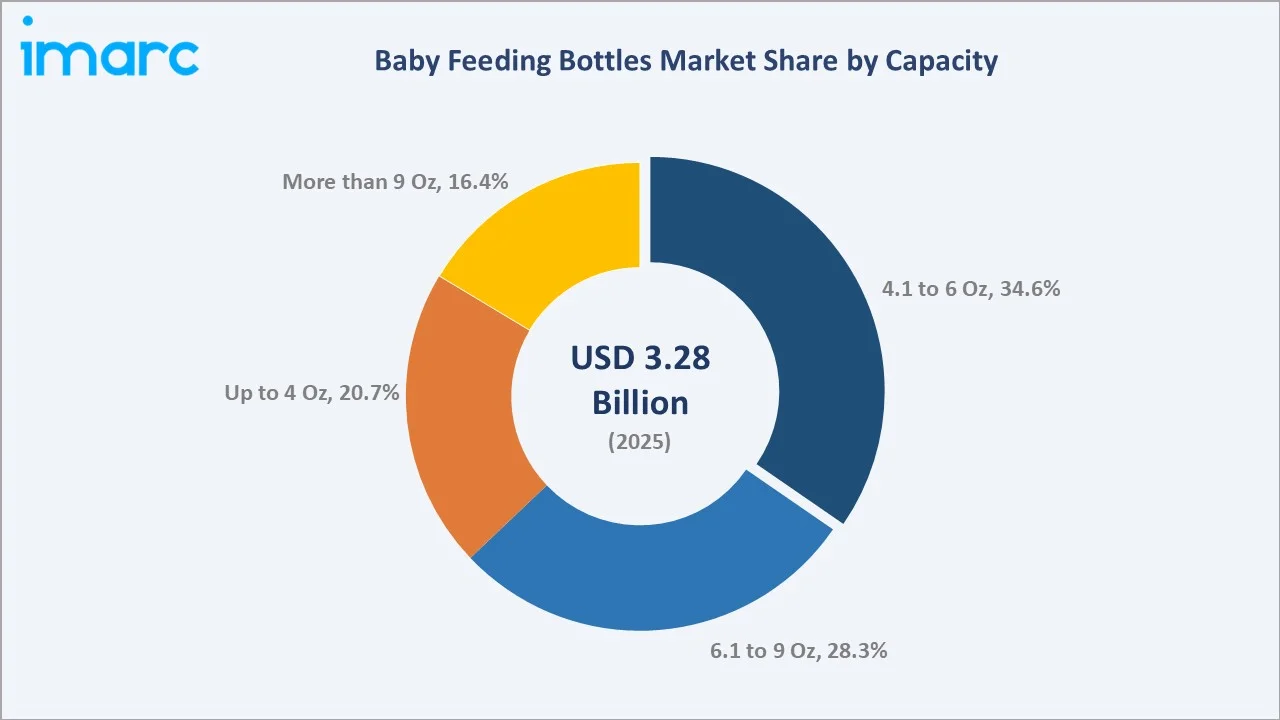

4.1 to 6 Oz (34.6%, 2025) |

The baby feeding bottles market growth trajectory from 2020 through 2034, with the historical expansion to USD 3.28 Billion in 2025, reflects consistent infant care demand, while the forecast to USD 4.54 Billion captures accelerating safe-material innovation, silicone bottle adoption, and e-commerce distribution expansion across all regions.

To get more information on this market, Request Sample

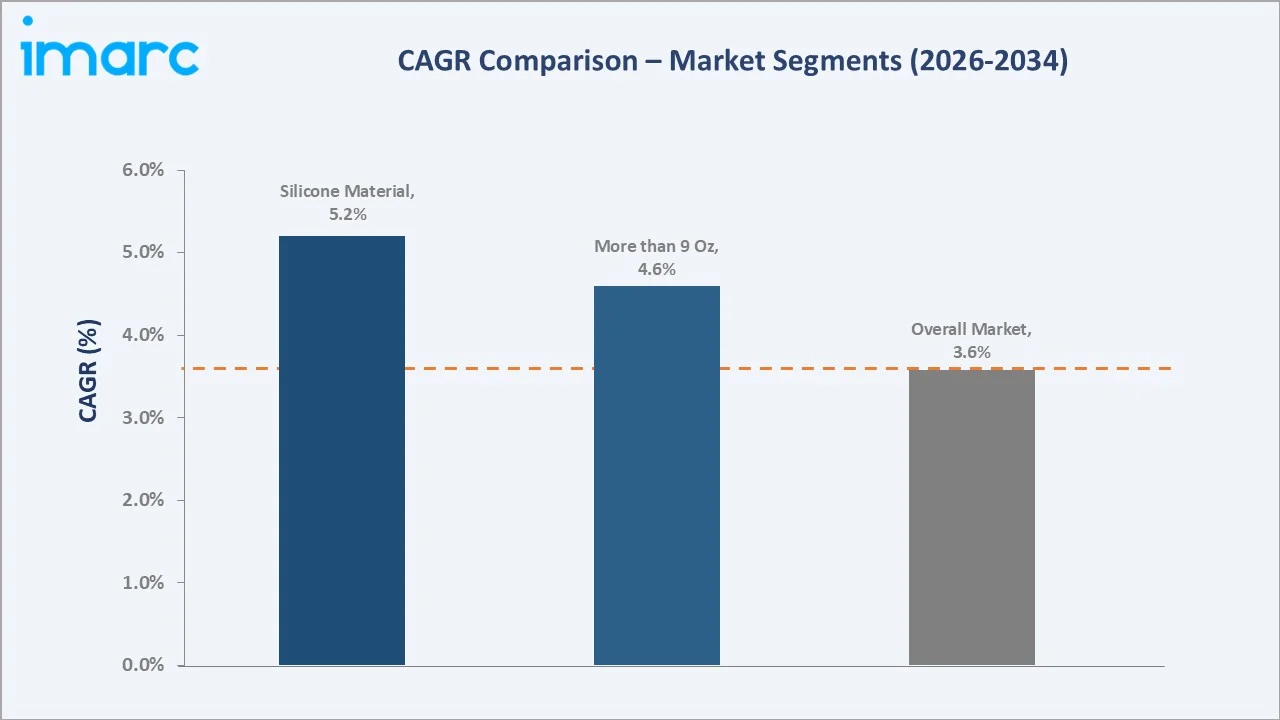

The CAGR trajectories across key material type, capacity, and regional sub-segments, with silicone at ~5.2% CAGR and More than 9 Oz capacity at ~4.6% CAGR, are the fastest-growing categories within the global baby feeding bottles industry analysis through 2034.

Executive Summary

The global baby feeding bottles market is on a sustained growth trajectory from USD 3.28 Billion in 2025 to USD 4.54 Billion by 2034. Baby feeding bottles, an essential infant care product used from birth through the weaning stage, benefit from recurring demand driven by annual birth cohorts and replacement cycles.

Plastic dominates material type at 46.7% in 2025, benefiting from affordability, lightweight design, and BPA-free reformulation that has largely addressed historical safety concerns. Glass (21.5%) and Silicone (18.4%) command growing share among premium-conscious parents. Stainless steel (13.4%) serves the durable, eco-conscious segment.

The 4.1 to 6 Oz capacity range leads at 34.6% in 2025, serving the core infant feeding window of 2-6 months.

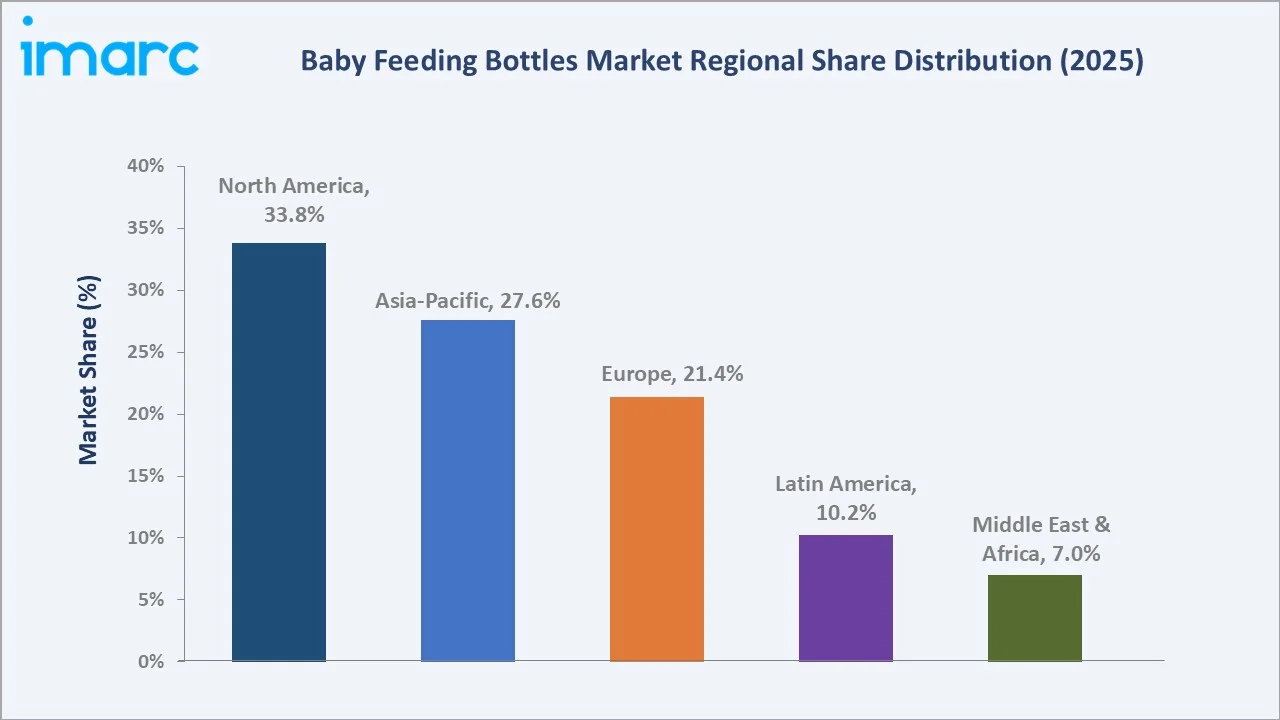

North America commands 33.8% with high safety awareness and spending power. Asia-Pacific (27.6%) represents the fastest-growing region, driven by India and China's large birth cohorts and rising incomes.

Key Market Insights

|

Insight |

Data |

|

Leading Material Type |

Plastic – 46.7% share (2025) |

|

Second Material Type |

Glass – 21.5% share (2025) |

|

Third Material Type |

Silicone – 18.4% share (2025) |

|

Leading Capacity |

4.1 to 6 Oz – 34.6% (2025) |

|

Second Capacity |

6.1 to 9 Oz – 28.3% (2025) |

|

Leading Region |

North America – 33.8% revenue share (2025) |

|

Top Companies |

Koninklijke Philips N.V., Pigeon Corporation, Mayborn Group Limited, Nanobébé, Babisil International Ltd. |

Key Analytical Observations Expanding on the Above Data:

- Plastic at 46.7% dominates due to its unmatched combination of affordability, design flexibility, and BPA-free reformulation. The shift to Tritan copolyester and polypropylene has eliminated health concerns while maintaining the cost advantages that make plastic the default choice across all income brackets globally.

- 4.1 to 6 Oz capacity leads at 34.6% because it precisely matches the recommended feeding volume for infants aged 2-6 months, the highest-consumption age window. This size offers the optimal balance between feed volume and portability, making it the top-selling SKU across all major global brands.

- Silicone bottles at 18.4% are the fastest growing material segment, driven by their soft, squeezable nature that mimics breastfeeding, heat resistance enabling microwave sterilization, and near-zero chemical leaching, aligning with parents' preference for the safest possible feeding vessels.

- North America at 33.8% dominates owing to high per-capita spending on infant care, strong BPA-free and food-safe regulatory frameworks enforced by the FDA, a large working mother population requiring bottle feeding, and a mature e-commerce infrastructure enabling convenient premium product access.

Baby Feeding Bottles Market Overview

Baby feeding bottles are specially designed vessels for feeding infants with breast milk or formula, comprising a bottle body, nipple/teat, collar, and cap. Product variants span standard neck, wide neck, angled neck, and vented configurations across plastic, glass, silicone, and stainless-steel materials.

The global ecosystem integrates raw material suppliers, bottle and nipple manufacturers, BPA-free and food-safety testing laboratories, brand marketing companies, organized retail chains, online marketplaces, and pediatric healthcare channels. Regulatory bodies, including the FDA, EN 14350, and BIS, govern material safety across key markets globally.

Market Dynamics

To evaluate market opportunities, Request Sample

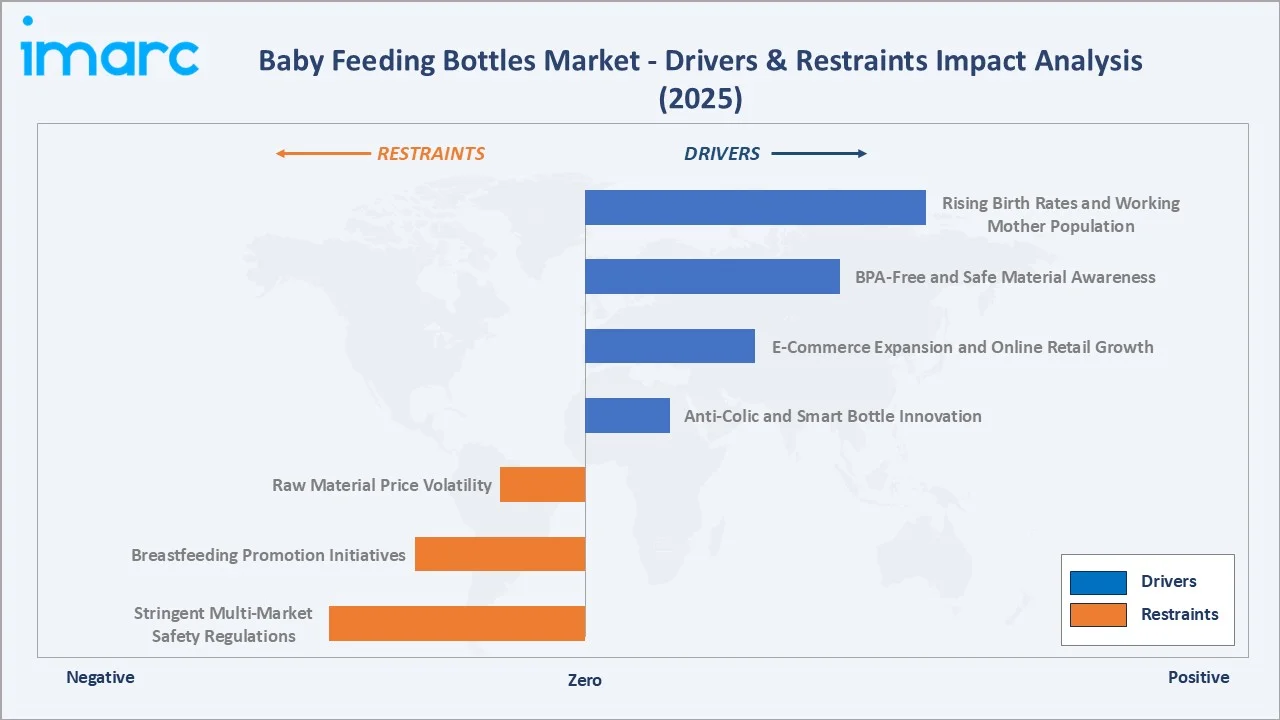

Market Drivers

- Rising Birth Rates and Working Mother Population: Global annual births exceed 140 million, and the increasing participation of women in the workforce across Asia-Pacific, Latin America, and MENA has structurally elevated demand for bottle feeding as a supplement or alternative to exclusive breastfeeding, sustaining recurring high-volume demand.

- BPA-Free and Safe Material Awareness: Growing parental awareness of bisphenol A (BPA) health risks has driven a market-wide shift to BPA-free polypropylene, Tritan copolyester, borosilicate glass, and food-grade silicone, creating an upgrade cycle and premiumization trend that benefits established brands with certified safe portfolios.

- E-Commerce Expansion and Online Retail Growth: The rapid growth of Amazon, Flipkart, JD.com, and regional baby specialty e-commerce platforms has dramatically improved access to global premium brands in tier-2 and tier-3 cities, expanding the addressable market and enabling smaller innovative brands like nanobébé to compete globally.

Market Restraints

- Stringent Multi-Market Safety Regulations: Compliance with divergent safety frameworks, including FDA 21 CFR, European EN 14350, BIS IS 14625, and various national standards, requires significant testing investment from manufacturers, raising barriers for smaller players and creating product launch delays in new markets.

- Breastfeeding Promotion Initiatives: WHO and UNICEF actively promote exclusive breastfeeding for the first six months, with the national health ministry’s implementing awareness programs that moderate bottle-feeding adoption rates, particularly in developing markets where institutional healthcare influence is strongest.

Market Opportunities

- Anti-Colic and Smart Bottle Innovation: Advanced internal venting systems, temperature-indicating color-change bottles, and connected smart bottles that track feeding volumes represent high-margin product tiers over standard bottles, creating significant revenue expansion opportunities for innovation-led manufacturers.

- Emerging Market Penetration in Asia and Africa: Rising income levels in India, Indonesia, Nigeria, and Ethiopia, combined with increasing female labor force participation and improving modern retail infrastructure, represent large untapped volume opportunities for affordable BPA-free bottle portfolios adapted to local feeding practices.

Market Challenges

- Raw Material Price Volatility: Polypropylene, borosilicate glass, and food-grade silicone prices are subject to petrochemical feedstock cycles and energy cost fluctuations that compress manufacturer margins, particularly for mid-market brands operating under price-sensitive retailer contract structures.

- Counterfeit and Low-Quality Product Proliferation: The prevalence of uncertified counterfeit bottles, particularly in online marketplaces across developing markets, undermines consumer trust, creates safety risks, and compresses pricing for legitimate certified manufacturers competing on shared platforms.

Emerging Market Trends

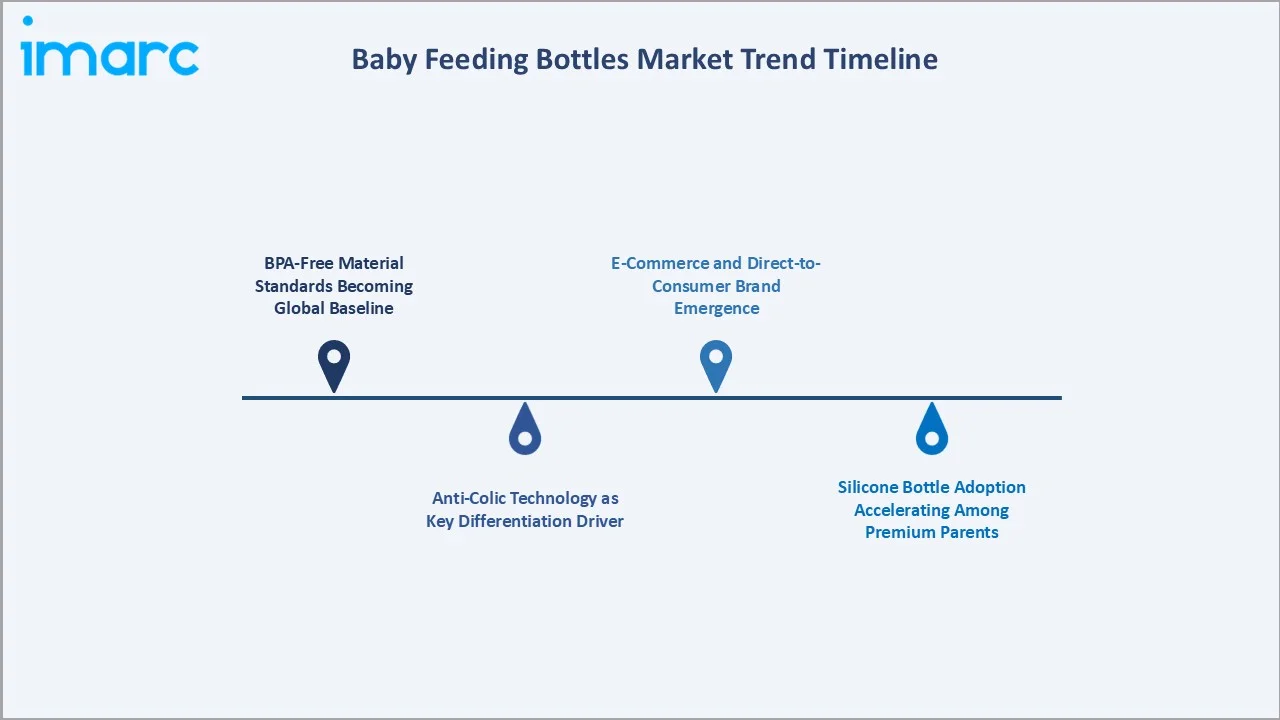

1. BPA-Free Material Standards Becoming Global Baseline

Regulatory bans on BPA in baby bottles enacted in the US (2012), EU (2011), and subsequently across 50+ countries have permanently shifted the material baseline to BPA-free polypropylene, Tritan, and glass. This has elevated consumer safety expectations and creates an ongoing premiumization trend toward glass and silicone alternatives.

2. Anti-Colic Technology as Key Differentiation Driver

Advanced internal venting technologies from Dr. Brown's (multi-piece internal vent), Philips Avent (AirFree vent), and Tommee Tippee (anti-colic valve) have established infant digestive comfort as a central purchase decision factor. Anti-colic bottle segments command price premiums and are growing faster than standard bottle categories globally.

3. Silicone Bottle Adoption Accelerating Among Premium Parents

Food-grade platinum silicone bottles, offering soft squeezable texture mimicking breast tissue, zero chemical leaching, microwave and dishwasher safety, and 10+ year lifespan, are gaining rapid adoption among health-conscious urban parents willing to pay 3-5x standard bottle prices for perceived safety and sustainability benefits.

4. E-Commerce and Direct-to-Consumer Brand Emergence

Digital-native baby bottle brands including nanobébé, Comotomo, and Olababy have built significant market positions exclusively through e-commerce and social media marketing, disrupting traditional retail-dominated brand hierarchies and demonstrating that innovation and safety storytelling can overcome established brand loyalty.

Industry Value Chain Analysis

The baby feeding bottles value chain spans six stages from raw material sourcing through end-use and recycling. Design innovation and safety certification capture the highest value-add, while distribution channel selection and brand positioning generate the competitive advantages that command premium retail pricing in this safety-sensitive category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Plastic resin producers, glass manufacturers, silicone compounders, stainless steel mills |

|

Design & R&D |

Koninklijke Philips N.V., Pigeon Corporation, Handi-Craft Company (Dr. Brown's), Mayborn Group |

|

Manufacturing & QC |

Artsana S.p.A. (Chicco), Munchkin Inc., Babisil International Ltd. |

|

Compliance & Certification |

FDA 21 CFR, EN 14350, BIS IS 14625, BPA-Free & phthalate-free testing labs |

|

Distribution & Retail |

Supermarkets, retail pharmacies, online stores, baby specialty retail, and convenience stores |

|

End Use & Lifecycle |

Infants aged 0-36 months, parents, caregivers; bottle recycling and silicone reuse programs |

Vertically integrated manufacturers with captive nipple and teat production capabilities, such as Pigeon Corporation, which manufactures its own medical-grade silicone nipples, achieve superior quality consistency and margin structures versus brands relying entirely on third-party component sourcing from contract manufacturers in China.

Technology Landscape in the Baby Feeding Bottles Industry

Anti-Colic Venting Technology

Internal venting systems route air away from milk to prevent infant gas ingestion. Dr. Brown's patented multi-piece internal vent system, Philips Avent's AirFree vent, and Comotomo's dual-venting nipple represent the leading commercial implementations, each engineered to specific feeding flow and anti-colic performance parameters.

Material Science and BPA-Free Formulations

Eastman Tritan copolyester has emerged as the leading premium BPA-free plastic, offering glass-like clarity with polycarbonate-like durability at a mid-range price point. Borosilicate glass provides the gold standard in chemical inertness. Medical-grade platinum silicone offers the highest safety profile with unique tactile properties that support breastfeeding transition.

Smart and Connected Bottle Innovation

Temperature-sensing liquid crystal technology, incorporated into bottles by Cherub Baby and others, provides immediate visual temperature feedback, preventing scalding. Connected bottles from Ember Technologies track feeding volumes via paired smartphone apps, providing data-driven feeding analytics for parents and pediatricians managing infant weight gain.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Material Type | Plastic | 46.7% | 2025 |

| Capacity | 4.1 to 6 Oz | 34.6% | 2025 |

| Distribution Channel | Hypermarkets and Supermarkets | 🔒 | 2025 |

| Region | North America | 33.8% | 2025 |

By Material Type

Plastic commands a 46.7% majority share in 2025 due to its fundamental affordability, lightweight handling, drop resistance, and successful reformulation to BPA-free grades that have resolved historical chemical safety concerns. Polypropylene and Tritan plastic bottles serve the broadest global consumer base across all income brackets and distribution channels.

To access detailed market analysis, Request Sample

Glass at 21.5% in 2025 commands a premium positioning, favored by safety-conscious parents seeking zero chemical leaching and maximum hygiene. Silicone at 18.4% is the fastest-growing material at ~5.2% CAGR, with its breastfeeding-mimicking tactile properties driving rapid adoption.

Stainless steel at 13.4% serves the durable, eco-conscious, and travel segment, offering a near-unlimited lifespan and complete absence of any leachable compounds.

By Capacity

The 4.1 to 6 Oz capacity segment leads at 34.6% in 2025, precisely matching the recommended feeding volume for infants aged 2-6 months, the core consumption window. This capacity range is the universal starter bottle size stocked by all major brands and represents the highest-volume SKU in both retail and e-commerce baby category assortments globally.

6.1 to 9 Oz capacity at 28.3% serves older infants aged 6-12 months requiring larger feeds. Up to 4 Oz at 20.7% represents newborn and colostrum-stage feeding for the smallest feed volumes.

More than 9 Oz at 16.4% is the fastest-growing capacity at ~4.6% CAGR, driven by toddler formula consumption and the growing trend of extended bottle use beyond 12 months in emerging markets.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

33.8% |

High spending power; BPA-free regulation leadership; strong e-commerce; working mother population |

|

Asia-Pacific |

27.6% |

High birth rate in India, China, rising disposable income, and expanding modern retail channels |

|

Europe |

21.4% |

Strict EN 14350 safety standards; premium glass/silicone preference; sustainability awareness |

|

Latin America |

10.2% |

Growing urban middle class; rising female workforce participation; Brazil and Mexico leading |

|

Middle East & Africa |

7.0% |

Young population demographics, improving healthcare awareness, and increasing organized retail |

North America at 33.8% in 2025 leads the global market, driven by high per-capita baby product expenditure averaging USD 1,200 per infant annually, FDA-enforced BPA-free mandates that have established a premium safety baseline, and a large working mother population that generates structurally elevated bottle-feeding demand across income segments.

Asia-Pacific at 27.6% in 2025 represents the highest-growth region at ~4.4% CAGR through 2034. India and China contribute the largest absolute birth volumes globally, and rising disposable incomes are enabling the transition from unbranded to branded BPA-free bottles. Japan and South Korea drive premium silicone and glass adoption with among the highest per-unit ASPs in the region.

Europe, at 21.4%, benefits from strict EN 14350 safety enforcement that sustains premium glass and silicone demand. Latin America, at 10.2%, is growing through Brazil and Mexico's expanding urban middle class.

The Middle East and Africa at 7.0% represents the longest-term growth opportunity, with a young demographic profile and improving modern retail infrastructure.

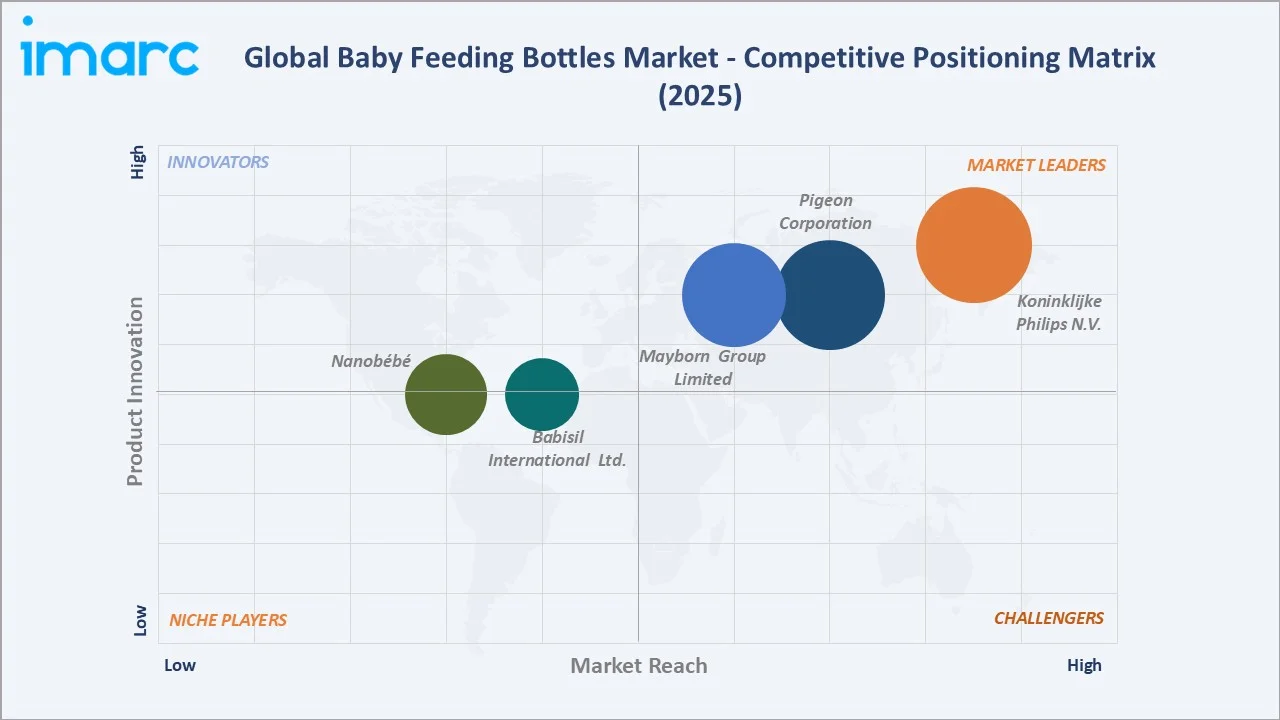

Competitive Landscape

The global baby feeding bottles market is moderately fragmented, with a small number of global leaders commanding brand recognition across major markets, while a larger set of regional and specialty brands serve niche material, innovation, or geographic segments. Safety certification and brand trust are the primary competitive moats.

|

Company Name |

Key Products |

Position |

Strategic Focus |

|

Koninklijke Philips N.V. |

Natural, Anti-Colic, Classic+ Bottles |

Leader |

Broadest global portfolio; natural start nipple innovation; anti-colic vent leadership |

|

Pigeon Corporation |

SofTouch III bottles with Peristaltic PLUS teats |

Leader |

Asia-Pacific dominance; breastfeeding transition; wide hospital channel penetration |

|

Mayborn Group Limited |

Natural Start, Advanced Anti-Colic |

Leader |

Natural breastfeeding mimicry; ergonomic design; strong UK and European base |

|

Nanobébé |

Breastmilk Bottle, Flexy Silicone |

Emerging |

Breast milk preservation innovation; fast-warming design; premium D2C positioning |

|

Babisil International Ltd. |

BabiSil Glass & Silicone Range |

Emerging |

Glass and silicone specialist; eco-conscious positioning; Asia-Pacific distribution |

Key players include Koninklijke Philips N.V., Pigeon Corporation, Mayborn Group Limited, Nanobébé, Babisil International Ltd., and others.

Key Company Profiles

Koninklijke Philips N.V.

Koninklijke Philips N.V. operates its baby feeding portfolio through the Philips Avent brand, one of the world's most recognized baby bottle brands, serving parents across more than 60 countries with a comprehensive range of feeding bottles, breast pumps, and sterilizers.

- Product Portfolio: Natural Response, Anti-Colic, Classic+, and Glass bottle ranges; AirFree vent technology; breast milk storage containers and accessories.

- Strategic Focus: Philips Avent's strategy centers on breastfeeding-to-bottle transition support and anti-colic innovation leadership, leveraging the Philips parent brand's healthcare credibility and global distribution infrastructure to command premium pricing across all major retail channels.

Pigeon Corporation

Pigeon Corporation is Japan's leading baby care brand and a dominant force across Asia-Pacific, known for its SofTouch and Peristaltic Plus bottle ranges engineered specifically to facilitate the transition between breastfeeding and bottle feeding with minimal nipple confusion.

- Product Portfolio: SofTouch bottle range featuring the Peristaltic Plus wide-neck teat technology (available in glass and PPSU variants), along with breast pumps and nipple accessories across newborn to toddler ages.

- Recent Developments: In March 2026, Pigeon announced the nationwide launch of its “Nurture & Nest” baby bottle collection at Target stores and online, expanding its reach to a broader base of parents and caregivers. The range is built on decades of research into infant feeding behaviour and is designed to support babies’ development from newborn through toddler stages with thoughtfully engineered bottles.

- Strategic Focus: Pigeon's strategy leverages its dominant hospital channel relationships across Japan, China, and Southeast Asia to establish product preference from birth, with clinical research partnerships supporting its science-backed breastfeeding transition positioning.

Mayborn Group Limited

Mayborn Group Limited's Tommee Tippee brand has established a strong market position across the UK, Europe, Australia, and North America through its Closer to Nature philosophy of designing bottles that closely mimic the natural breastfeeding experience in shape, flexibility, and nipple texture.

- Product Portfolio: Natural Start, Advanced Anti-Colic, and others

- Recent Developments: In May 2023, Tommee Tippee, a brand of Mayborn Group, announced a partnership with the Maternal Mental Health Alliance (MMHA) to raise awareness of perinatal mental health and provide greater support to new and expectant parents. The collaboration aims to promote understanding of mental health challenges during pregnancy and early parenthood, while offering access to educational resources, guidance, and support networks.

- Strategic Focus: Tommee Tippee's strategy differentiates through ergonomic design and sustainability commitments targeting environmentally conscious millennial and Gen-Z parents, supported by strong social media brand community and influencer partnerships.

Market Concentration Analysis

The global baby feeding bottles market is moderately concentrated, with five companies — Philips Avent, Pigeon, Tommee Tippee, Dr. Brown's, and Munchkin — estimated to collectively hold approximately 40-50% of global market revenue. Safety certification requirements and brand trust act as structural barriers to entry that favor established players.

Consolidation through brand portfolio expansion is the primary growth strategy, with large baby care conglomerates acquiring specialist bottle brands to add anti-colic, silicone, or sustainability differentiation to their portfolios. Digital-native brands are driving market share gains through e-commerce without commensurate traditional retail investment.

Investment & Growth Opportunities

Fastest-Growing Segments

Silicone material at ~5.2% CAGR through 2034 is the highest-growth material segment, driven by safety-first parenting trends and breastfeeding-mimicking product design. More than 9 Oz capacity at ~4.6% CAGR reflects extended bottle use and toddler formula consumption growth, particularly across Asia-Pacific and Latin America.

Emerging Markets

Asia-Pacific at ~4.4% CAGR is the fastest-growing region, with India and Indonesia representing particularly high potential given their large annual birth cohorts, rising incomes, and low current branded bottle penetration. Africa's young demographic profile and improving retail infrastructure represent the longest-term structural growth opportunity.

Venture & Investment Trends

Venture investment in smart connected baby feeding technology, sustainable and reusable bottle systems, and direct-to-consumer baby brand platforms has accelerated. Silicone specialist brands and anti-colic innovators are attracting strategic M&A interest from large baby care conglomerates seeking to add premium safety positioning to existing portfolios.

Future Market Outlook (2026-2034)

The global baby feeding bottles market is forecast to expand from USD 3.28 Billion in 2025 to USD 4.54 Billion by 2034 at a CAGR of 3.58%, adding USD 1.26 Billion in incremental annual market value. This consistent growth reflects the market's demographic-linked, non-discretionary demand characteristics tied to annual birth cohorts.

Three forces will shape the market through 2034: regulatory-driven premiumization toward glass and silicone accelerating material mix upgrade; e-commerce enabling global brand reach into previously underserved emerging markets; and smart bottle innovation creating a high-margin technology segment in a traditionally commodity-oriented product category.

Research Methodology

Primary Research

Primary research encompassed structured interviews with baby feeding bottle industry stakeholders, including senior product managers at major brands, pediatric nutritionists, hospital procurement managers, specialty retail buyers, and online marketplace category managers. Primary data validated market sizing, material type and capacity segment shares, regional demand estimates, and innovation adoption timelines.

Secondary Research

Key secondary sources include WHO infant feeding guidelines, FDA food contact materials regulations, EN 14350 European baby product standards, BIS IS 14625, UNICEF infant and young child feeding data, national birth statistics from UN DESA, trade publications including Baby & Mother and Global Baby Industry Review, and company annual reports.

Forecasting Models

Market size estimations used top-down and bottom-up models incorporating annual birth rate data by region, per-infant bottle spending benchmarks, material mix evolution trajectories, e-commerce penetration rates, and regulatory upgrade cycle timelines. Scenario analysis addressed birth rate uncertainty and premium material adoption pace variation.

Baby Feeding Bottles Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Plastic, Stainless Steel, Silicone, Glass |

| Capacities Covered | Up to 4 Oz, 4.1 to 6 Oz, 6.1 to 9 Oz, More than 9 Oz |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Retail Pharmacies, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Koninklijke Philips N.V., Pigeon Corporation, Mayborn Group Limited, Nanobébé, Babisil International Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the baby feeding bottles market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global baby feeding bottles market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the baby feeding bottles industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Baby Feeding Bottles Market Report

The global baby feeding bottles market reached USD 3.28 Billion in 2025, driven by rising birth rates, growing working mother population, and heightened awareness of BPA-free and safe material feeding products.

The market is projected to grow at a CAGR of 3.58% from 2026 to 2034, reaching USD 4.54 Billion by 2034, supported by silicone and glass adoption growth, e-commerce expansion, and emerging market penetration.

Plastic leads with a 46.7% share in 2025 due to its affordability, lightweight design, and successful BPA-free reformulation. Silicone is the fastest growing material at approximately 5.2% CAGR through 2034.

The 4.1 to 6 Oz capacity segment leads at 34.6% in 2025, precisely matching the recommended feeding volume for infants aged 2-6 months. The More than 9 Oz segment is the fastest growing capacity at approximately 4.6% CAGR.

North America commands a 33.8% share in 2025, driven by high per-capita infant care spending, FDA-enforced BPA-free standards, and a large working mother population. Asia-Pacific at 27.6% is the fastest growing region.

The leading companies include Koninklijke Philips N.V., Pigeon Corporation, Mayborn Group Limited, Nanobébé, Babisil International Ltd., and others.

Silicone bottle growth is driven by its soft breastfeeding-mimicking texture that reduces nipple confusion, zero chemical leaching profile that appeals to safety-focused parents, microwave and dishwasher sterilization compatibility, and a near-unlimited lifespan that supports eco-conscious purchasing decisions across premium market segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)