Bakery Products Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Global Bakery Products Market Size, Share, Trends & Forecast (2026-2034)

The global bakery products market size was valued at USD 549.1 Billion in 2025 and is projected to reach USD 726.7 Billion by 2034, exhibiting a CAGR of 3.07% during 2026-2034. Shifting consumer preferences toward ready-to-consume (RTC) baked goods, rising urbanization, and accelerating e-commerce penetration are fueling bakery market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 549.1 Billion |

|

Forecast Market Size (2034) |

USD 726.7 Billion |

|

CAGR (2026-2034) |

3.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (36.3% share, 2025) |

|

Fastest Growing Distribution Channel |

Online Stores (~6.2% CAGR) |

|

Leading Product Type |

Bread and Rolls (33.9%, 2025) |

|

Leading Distribution Channel |

Supermarkets and Hypermarkets (38.2%, 2025) |

The chart below illustrates the bakery products market growth trajectory from 2020 through 2034, contrasting historical expansion with the sustained forecast curve powered by convenience trends, premiumization, and digital channel adoption.

To get more information on this market, Request Sample

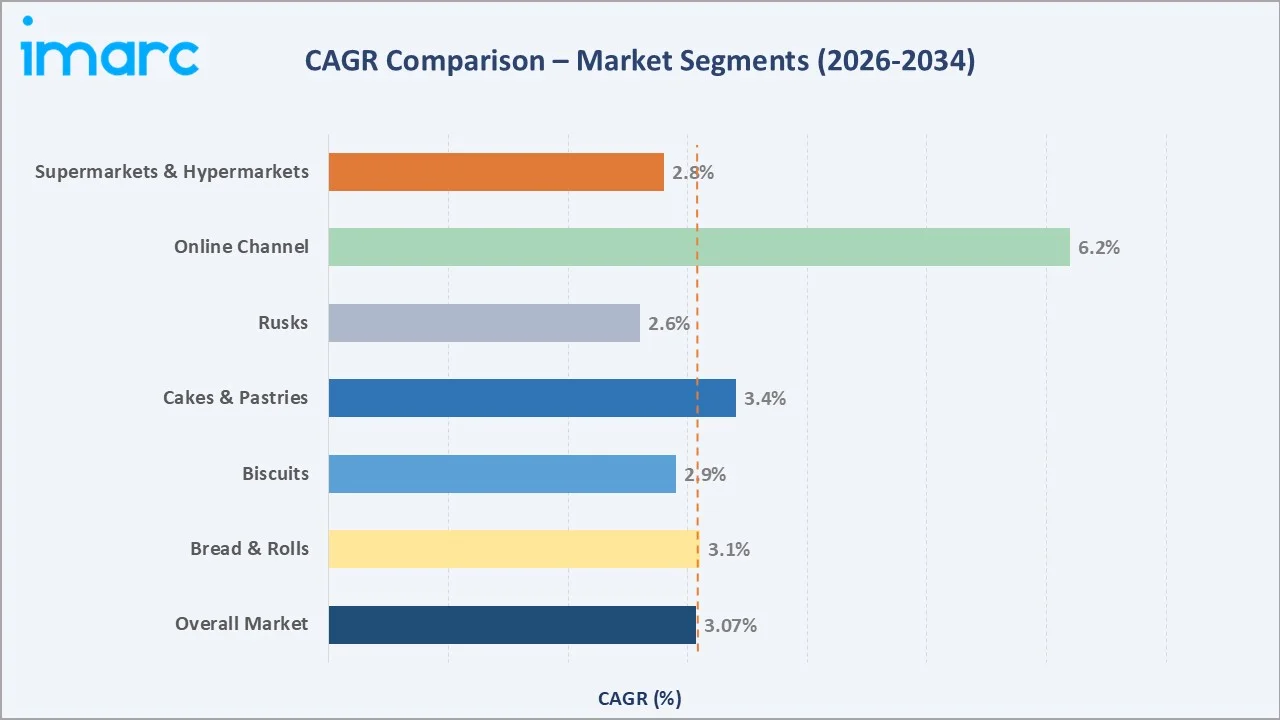

Segment-level CAGR comparisons highlight the online distribution channel and Cakes and Pastries as the fastest-growing sub-categories within the global bakery products market forecast through 2034.

Executive Summary

The global bakery products market is undergoing a structural transformation, driven by shifting consumption habits, rising health-consciousness, and rapid digital commerce adoption. Valued at USD 549.1 Billion in 2025, the market is forecast to reach USD 726.7 Billion by 2034 at a CAGR of 3.07%. Premiumization, clean-label formulation, and direct-to-consumer online platforms are key structural forces reshaping product portfolios and channel strategies across all major regions.

Bread and Rolls command 33.9% share of the product mix in 2025, anchored by staple consumption across Europe and North America. Biscuits contribute 28.4%, driven by the growing snack culture and convenience formats. Supermarkets and Hypermarkets dominate distribution at 38.2%, while Online Stores represent only 8.2% yet are the fastest-growing channel at an estimated CAGR of 6.2% through 2034. Cakes and Pastries are expanding at 3.4% CAGR, supported by the premiumization trend.

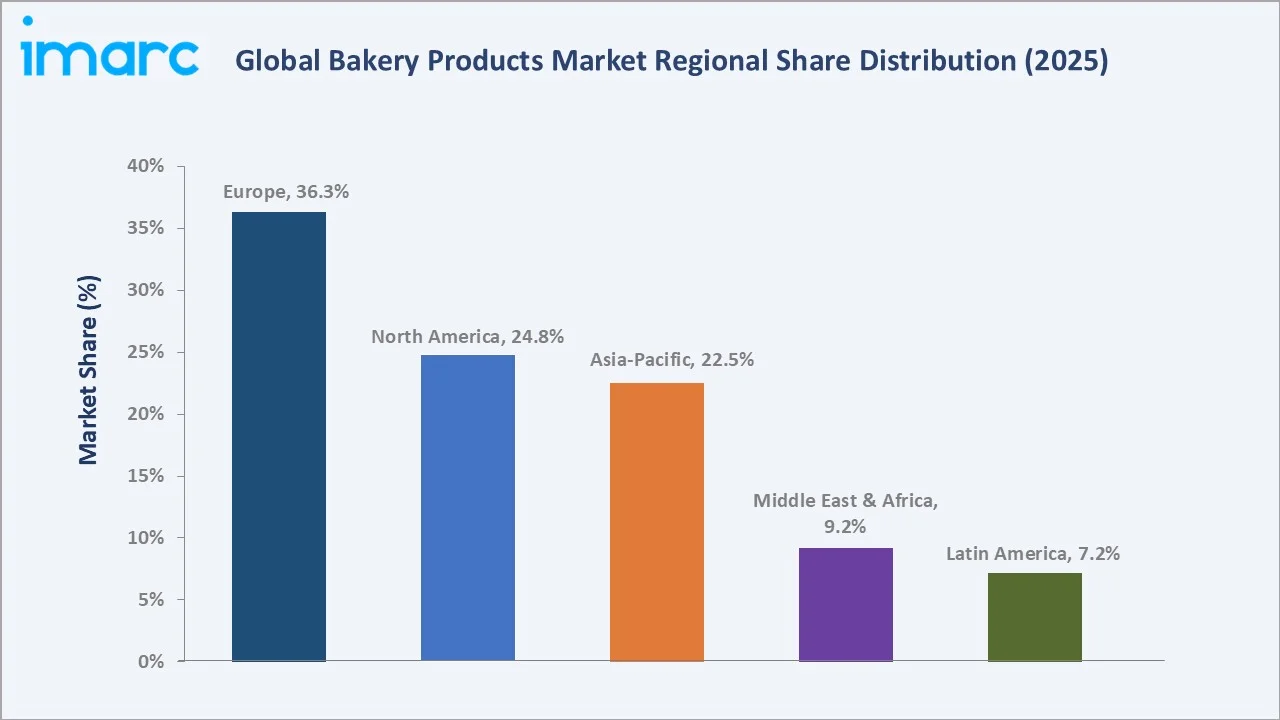

Europe leads the bakery products market share with 36.3% of global revenue in 2025, underpinned by deep-rooted artisanal bakery culture and robust private-label bakery expansion. North America holds 24.8% and Asia-Pacific 22.5%. The bakery products market outlook remains positive as health-and-wellness formulation, sustainability-led packaging, and digital channel penetration converge to redefine purchasing behavior through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Bread and Rolls - 33.9% share (2025) |

|

Second Product Type |

Biscuits - 28.4% share (2025) |

|

Leading Distribution Channel |

Supermarkets and Hypermarkets - 38.2% (2025) |

|

Fastest Growing Channel |

Online Stores - ~6.2% CAGR (2034) |

|

Leading Region |

Europe - 36.3% revenue share (2025) |

|

Top Companies |

Grupo Bimbo, Mondelez International, Nestle, General Mills Inc., Flowers Foods, Britannia Industries, Parle Products, and ITC |

|

Market Opportunity |

Health & wellness, RTC products, clean-label innovation, e-commerce bakery |

Key Analytical Observations Supporting The Above Data:

- Bread and Rolls' 33.9% dominance Bread and Rolls' 33.9% dominance in 2025 reflects strong staple demand across Europe's established bakery retail ecosystem, particularly in France, Germany, and the UK.

- Biscuits' 28.4% share Biscuits' 28.4% share is driven by snacking culture, impulse purchase formats, and premiumization of cream biscuit and cookie sub-segments across emerging markets.

- Supermarkets and Hypermarkets' 38.2% channel leadership Supermarkets and Hypermarkets' 38.2% channel leadership reflects bakery's position as a core center-of-store category, supported by private-label range expansion and in-store bakery sections.

- Online Stores' 6.2% CAGR Online Stores' 6.2% CAGR outpaces all other channels, driven by subscription bakery services, social commerce, and direct-to-consumer artisanal brands capturing urban millennial consumers.

- Europe's 36.3% global revenue share Europe's 36.3% global revenue share is underpinned by deeply embedded bakery culture, EU food quality regulations, and strong consumer willingness to pay premium prices for artisanal and clean-label products.

- The market opportunity the market opportunity in functional and fortified bakery - protein-enriched bread, fiber-rich biscuits, and reduced-sugar cakes - is expanding rapidly, with health-focused variants recording above-average growth rates.

Global Bakery Products Market Overview

Bakery products encompass a broad range of goods manufactured through baking, including bread, rolls, biscuits, cookies, cakes, pastries, and rusks. The industry serves household consumption, foodservice operators, quick-service restaurants (QSRs), institutional catering, and convenience retail channels worldwide.

The ecosystem operates at the intersection of food manufacturing, retail distribution, and evolving consumer lifestyle trends. Macroeconomic influences include urbanization, rising disposable incomes, growing working-population share, and the global shift toward convenience foods. The industry is witnessing structural premiumization alongside volume growth in emerging markets. Clean-label, organic, gluten-free, and plant-based formulations are redefining the product development agenda globally through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

- Shifting Consumer Preferences Toward Healthier Formulations: Research shows 47% of Americans have tried a new brand due to social media engagement. Health-conscious shoppers are driving demand for whole grain, reduced-sugar, and plant-based bakery variants at a compound rate above the overall market.

- Rapid Urbanization and Busy Lifestyles: With 55% of the global population now living in cities and that share expected to reach 68% by 2050, demand for convenient, pre-packaged, grab-and-go bakery formats is expanding structurally.

- E-Commerce Channel Expansion: E-commerce bakery channels are growing at approximately 6.2% CAGR through 2034. Online platforms enable broader geographic reach, subscription delivery models, and direct-to-consumer brand positioning.

- Innovation and Product Diversification: Continuous investment in new flavors, textures, functional ingredients, and dietary variants - gluten-free, keto-friendly, fortified bread - creates recurring category renewal, sustaining volume growth across all price tiers.

Market Restraints

- Raw Material Price Volatility: Wheat, sugar, dairy, and vegetable fat price volatility directly impacts manufacturing margins. Commodity input inflation in 2022-2023 compressed profitability across the industry, affecting mid-size producers most acutely.

- Intense Price Competition from Private Labels: Bakery retail markets in Europe and North America face intense price competition from private-label brands, which represent a significant share of packaged bakery sales in mature markets, intensifying pressure on branded players to differentiate and maintain margins.

- Short Shelf Life and Distribution Challenges: Fresh and artisanal bakery products maintain short shelf lives of 1-3 days, creating distribution complexity and food waste management challenges that elevate operational costs across the supply chain.

Market Opportunities

- Functional and Fortified Bakery Products: Health and wellness bakery including protein-enriched, fiber boosted, and reduced-sodium formulations—represents an underpenetrated premium sub-segment, with functional bread witnessing steady growth.

- E-Commerce and Direct-to-Consumer Models: Online bakery subscription platforms are recording strong customer retention. India's e-commerce food sector is growing at 18% annually, while Southeast Asian digital grocery adoption is accelerating bakery online channel revenues.

- Emerging Market Expansion: Africa and South Asia present high-potential volume markets for affordable packaged bakery. Rising middle-class populations and increasing retail infrastructure investment are creating accessible new consumer segments.

Market Challenges

- Evolving Regulatory Complexity: EU, US FDA, and UK FSA regulations on clean-label, allergen disclosure, trans-fat elimination, and front-of-pack labeling require continuous reformulation investment, adding complexity for multinational bakery manufacturers.

- Sustainability and Packaging Transition Costs: Meeting sustainability targets across bakery packaging - shifting from single-use plastic to recyclable or compostable formats - requires capital investment, and consumer premiums for sustainable packaging remain limited in many segments.

Emerging Market Trends

1. Health and Wellness-Led Reformulation

Consumer demand for reduced-sugar, high-fiber, and whole-grain bakery products is accelerating globally. Functional bread incorporating seeds, ancient grains, and protein fortification commands premium pricing over standard alternatives. This trend is particularly pronounced in North America and Northern Europe, where health-focused labeling plays a critical role in influencing purchase decisions.

2. Premiumization and Artisanal Positioning

Premium and craft bakery is one of the fastest-growing value sub-segments, advancing at an estimated 4.8% CAGR through 2030. Artisanal Bakeries hold 20.5% channel share in 2025. Consumers are trading up to sourdough, specialty patisserie, and origin-specific grain products. This trend is driving average unit price increases across Cakes and Pastries, which hold 22.6% product share in 2025.

3. E-Commerce and Direct-to-Consumer Expansion

Online Stores represent 8.2% distribution share in 2025 and are the fastest-growing channel at approximately 6.2% CAGR through 2034. Bakery subscription services, influencer-driven specialty brands, and dark store delivery models are transforming consumer discovery and purchase behavior. Social media platforms are directly generating demand for premium and novelty bakery formats.

4. Clean-Label and Natural Ingredient Adoption

Clean-label bakery products characterized by short ingredient lists, no artificial additives, and transparent sourcing claims — are experiencing rapid growth. A significant share of new bakery product launches now feature clean-label positioning, reflecting strong consumer preference for simplicity and transparency. Organic certification and non-GMO labeling are increasingly becoming standard in premium bakery segments across North America and Western Europe.

5. Sustainable Packaging and Eco-Formulation

Bakery manufacturers face increasing regulatory and consumer pressure to transition from single-use plastics to paper-based, recyclable, or biodegradable packaging. The EU Single-Use Plastics Directive is accelerating packaging innovation timelines. Simultaneously, eco-friendly formulation practices including reduced water usage and renewable energy integration in baking operations are becoming key supplier qualification criteria for major retailers.

Industry Value Chain Analysis

The global bakery industry value chain spans six integrated stages from raw material supply through end-consumer delivery. Each stage presents distinct competitive dynamics and margin profiles relevant to the overall bakery products market analysis.

|

Stage |

Descriptions |

|

Raw Materials |

Wheat, flour, sugar, eggs, dairy - supplied by agricultural commodity producers |

|

Ingredients & Additives |

Yeast, flavoring agents, preservatives, leavening agents - specialty ingredient suppliers |

|

Manufacturing & Processing |

Industrial bakeries, artisanal producers, co-manufacturers |

|

Packaging & Branding |

Retail-ready packs, eco-friendly packaging, private-label and branded formats |

|

Distribution Channels |

Supermarkets (38.2%), Artisanal Bakeries (20.5%), Independent Retailers (16.8%), Online (8.2%) |

|

End Consumers |

Households, foodservice operators, QSRs, HoReCa, institutional catering |

Major Consumer Packaged Goods (CPG) manufacturers hold the highest strategic value by integrating raw material sourcing, proprietary formulation, and distribution scale into end-to-end solutions. E-commerce and direct-to-consumer channels are reshaping downstream distribution, enabling brands to bypass traditional retail intermediaries and capture higher gross margins.

Technology Landscape in the Bakery Products Industry

Advanced Ingredient Technologies

Enzyme technology is transforming bread softness, shelf-life extension, and crumb structure optimization. Hydrocolloid systems - including hydroxypropyl methylcellulose (HPMC) - are enabling gluten-free dough structures that match conventional counterparts in texture and moisture retention, opening scalable market opportunities in the fast-growing free-from segment.

Automation and Smart Manufacturing

Industrial bakery automation is accelerating, with robotic depositing, automated proofing management, and AI-powered quality control systems reducing waste and improving consistency at scale. Smart oven technologies equipped with IoT sensors optimize bake profiles in real time. Grupo Bimbo, the world's largest bakery company, is investing heavily in Industry 4.0 manufacturing across its global production network.

Clean-Label and Functional Formulation

Natural preservative systems - rosemary extract, cultured wheat, vinegar derivatives - are replacing synthetic equivalents in response to clean-label consumer demand. Sourdough fermentation is being adopted beyond artisanal settings, as industrial producers integrate controlled fermentation to improve flavor, digestibility, and perceived naturalness. Protein fortification using plant-based pea, chickpea, and hemp proteins is a rapidly expanding bakery innovation frontier.

Packaging Innovation

Modified atmosphere packaging (MAP) is extending fresh bakery shelf life in supermarket and convenience formats. Active packaging incorporating oxygen scavengers is becoming standard for premium packaged cakes. Compostable paper-based packaging is accelerating due to regulatory mandates, reshaping supply chain requirements for bakery manufacturers and retailers across Europe.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Bread and Rolls | 33.9% | 2025 |

| Distribution Channel | Supermarkets and Hypermarkets | 38.2% | 2025 |

| Region | Europe | 36.3% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

Bread and Rolls leads the global bakery products market with a 33.9% share in 2025. Staple demand across European and North American households, combined with premiumization into sourdough and specialty grain variants, underpins segment leadership. The segment is growing at approximately 3.1% CAGR through 2034, supported by packaged convenience bread expansion in Asia-Pacific emerging markets.

By Distribution Channel

Supermarkets and Hypermarkets lead distribution with a 38.2% share in 2025. In-store bakery sections, private-label range expansion, and convenient one-stop-shop positioning cement channel leadership. This channel is expected to maintain dominance through 2034, though its relative share will moderate as online adoption accelerates.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

36.3% |

Artisanal bakery culture, clean-label regulation, premium private-label expansion, EU food policy |

|

North America |

24.8% |

Convenience and RTC demand, health reformulation, e-commerce bakery, QSR expansion |

|

Asia-Pacific |

22.5% |

Urbanization, rising middle class, packaged bread adoption, India & China market growth |

|

Middle East & Africa |

9.2% |

Population growth, expanding modern retail infrastructure, affordable packaged bakery |

|

Latin America |

7.2% |

Brazil and Mexico residential growth, QSR expansion, rising disposable incomes |

Europe commands 36.3% global revenue share in 2025. The region's deeply embedded artisanal and industrial bakery ecosystem is anchored by Germany, France, and the UK as the three largest national markets. EU food quality regulations, Geographic Indication (GI) certifications for traditional bakery products, and strong clean-label consumer demand drive consistent premium pricing. European private-label bakery - growing at 4.2% in volume terms - is expanding shelf space in major hypermarket chains.

Competitive Landscape

|

Company Name |

Key Brand(s) |

Market Position |

Core Strength |

|

Grupo Bimbo |

Bimbo, Marinela, Entenmann's |

Leader |

World's largest bakery - global scale, emerging market leadership |

|

Mondelez International |

Oreo, Chips Ahoy!, belVita |

Leader |

Global biscuit leadership, snacking platform, innovation pipeline |

|

Nestle |

Toll House |

Leader |

Ingredient technology, global distribution, R&D capabilities |

|

General Mills Inc. |

Pillsbury, Betty Crocker |

Leader |

North America dominance, convenience baking, retail channel depth |

|

Flowers Foods |

Nature's Own, Wonder, Dave's Killer Bread |

Challenger |

U.S. packaged bread leadership, health-focused reformulation |

|

Britannia Industries |

Britannia, NutriChoice, Good Day |

Challenger |

India market leadership, biscuit innovation, distribution reach |

|

Parle Products |

Parle-G, Hide & Seek, Krackjack |

Challenger |

World's highest-volume biscuit brand, India dominant |

|

ITC |

Sunfeast (Dark Fantasy, Farmlite) |

Challenger |

India premium biscuit growth, diversified distribution |

The global bakery products market competitive landscape is moderately fragmented, with multinational CPG players competing alongside regional specialists and national champions. Leading players compete on formulation innovation, health-positioning, distribution breadth, and private-label supply capabilities. Strategic M&A is reshaping the competitive hierarchy.

Key Company Profiles

Grupo Bimbo

Grupo Bimbo is leader and largest baking Company in the world and a major global player in packaged foods and snacks. Headquartered in Mexico City, the company operates across multiple continents, offering a wide range of bakery and snack products.

- Product Portfolio: Portfolio spans bread, buns, rolls, cakes, cookies, tortillas, and English muffins under brands including Bimbo, Marinela, Entenmann's, Sara Lee, and Thomas' English Muffins across North America, Latin America, Europe, and Asia.

- Recent Developments: In 2024, Grupo Bimbo announced the acquisition of Brazil-based Wickbold and its associated brands, including Seven Boys, as part of its strategy to strengthen its presence in the Brazilian bakery market. The deal includes multiple manufacturing facilities and expands Bimbo’s product portfolio across packaged bread, sweet baked goods, and related categories.

- Strategic Focus: Grupo Bimbo's strategy centers on emerging market volume growth, health and wellness portfolio expansion, and supply chain decarbonization. It is investing in digital route-to-market optimization and direct-to-consumer e-commerce capabilities.

Mondelez International

Mondelez International is a leading global snack food company, known for its strong presence in biscuits, chocolate, gum, candy, and powdered beverages. Headquartered in Chicago, the company operates in over 150 countries and focuses on becoming a global leader in snacking.

- Product Portfolio: Mondelez's bakery portfolio includes Oreo cookies, Chips Ahoy!, belVita breakfast biscuits, Ritz crackers, and Milka biscuit variants. The portfolio spans everyday snacking to premium gifting sub-segments globally.

- Recent Developments: In 2025, Mondelēz International expanded its bakery-snacking portfolio with the launch of belVita Energy Snack Bites, a soft-baked, bite-sized product designed for mid-morning consumption. The new offering features whole grains, fiber, and real fruit ingredients, with clean-label attributes such as no artificial flavors or high-fructose corn syrup.

- Strategic Focus: Mondelez's focus is on premiumizing its core biscuit portfolio, scaling emerging market volume, and leveraging e-commerce as a premium discovery channel for its specialty bakery variants.

Britannia Industries

Britannia Industries Limited is one of India’s leading food and bakery companies, with a dominant position in biscuits and a growing presence in dairy and adjacent food categories. Headquartered in Bengaluru, India.

- Product Portfolio: Britannia's portfolio encompasses biscuits (NutriChoice, Good Day, Marie Gold), bread, cakes, and dairy products, with dominant distribution across India's urban and semi-urban retail channels.

- Recent Developments: In 2025, Britannia Industries expanded its premium biscuit portfolio under the Pure Magic range with the launch of a new indulgent choco cookies lineup, introducing products such as Choco Tarts in hazelnut and milk chocolate variants. The offering focuses on multi-texture experiences combining crispy biscuit layers with rich chocolate crème, targeting the growing premium bakery-snacking segment.

- Strategic Focus: Britannia's strategy focuses on health and wellness portfolio expansion, premiumization of the biscuit category, rural distribution penetration, and building adjacency in adjacent snacking categories across South Asia.

Market Concentration Analysis

The global bakery products market exhibits moderate fragmentation. The top five players - Grupo Bimbo, Mondelez International, Nestle, General Mills Inc., and Flowers Foods - collectively account for approximately 28-35% of global market revenue in 2025.

The market is characterized by a bifurcated dynamic. At the multinational Consumer Packaged Goods (CPG) tier, consolidation is occurring around brand equity, formulation capabilities, and distribution scale. The top 10 companies hold an estimated 40-45% of organized packaged bakery revenue globally in 2025. Simultaneously, artisanal and local bakery operators across Europe and North America are growing their channel share through premiumization and direct consumer relationships.

Consolidation pressure is increasing due to raw material cost inflation, sustainability compliance investment requirements, and the need for technology-led supply chain optimization. Smaller regional producers face structural margin compression, creating acquisition opportunities for well-capitalized multinational players through 2034. The European and Asia-Pacific markets are expected to see the most significant consolidation activity during the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Online channel bakery sales are the highest-growth distribution opportunity at approximately 6.2% CAGR through 2034. Cakes and Pastries are the fastest-growing product sub-segment at 3.4% CAGR. Functional and health-positioned bakery - protein-enriched bread, high-fiber biscuits, reduced-sugar cakes - command premium pricing and above-average growth rates across North America and Europe.

Emerging Market Expansion

India represents the highest-potential emerging market for bakery volume growth. Packaged bread penetration remains low outside major urban centers, representing a structural growth runway as modern retail expands into Tier-2 and Tier-3 cities. India's packaged bakery market is growing at 7-9% annually. Southeast Asia, Sub-Saharan Africa, and the Middle East represent similar long-cycle volume growth opportunities driven by urbanization and retail infrastructure investment.

Venture and Strategic Investment Trends

Strategic acquisitions are reshaping the competitive landscape. Clean-label ingredient companies and functional food startups are attracting significant venture capital, with investors recognizing the reformulation imperative across the bakery category. Investment in e-commerce bakery platforms, AI-driven flavor development, and sustainable packaging materials represents the primary focus for capital deployment in the bakery sector through 2034.

Future Market Outlook (2026-2034)

The global bakery products market forecast projects steady value expansion from USD 549.1 Billion in 2025 to USD 726.7 Billion by 2034 at a CAGR of 3.07%. Europe will retain regional leadership while North America and Asia-Pacific sustain above-average value growth through health-positioned premiumization and digital channel adoption respectively.

Three key shifts will reshape the bakery market through 2034. Health-and-wellness convergence will embed functional claims into mainstream bakery positioning, making clean-label and fortified products standard across most price tiers by 2028-2030. E-commerce is set to capture a growing share of bakery distribution, transforming brand discovery, consumer engagement, and purchasing models. Sustainability-led packaging mandates will require significant capex investment, accelerating consolidation among producers lacking the scale to absorb transition costs.

The competitive advantage in 2034 will belong to producers capable of combining formulation innovation, digital channel mastery, and sustainable manufacturing at global scale. The divergence between premium health-oriented bakery brands and volume commodity producers will intensify, creating distinct margin profiles across the market's two structural tiers.

Research Methodology

Primary Research

Primary research was conducted in 2024-2025 through structured interviews with bakery industry stakeholders including product development directors at multinational Consumer Packaged Goods (CPG) companies, category managers at leading European supermarket chains, supply chain executives at ingredient manufacturers, and institutional investors in global food and beverage sectors. Primary insights validated market sizing, segmentation estimates, and trend adoption timelines.

Secondary Research

Secondary sources include World Bank urbanization data, FAO food production statistics, Nielsen bakery retail panel data, EUROSTAT food and beverage industry reports, company annual reports (Grupo Bimbo, Mondelez International, General Mills Inc., Britannia Industries), trade publications including Bakery and Snacks, Food Navigator, and Modern Bakery Today, and regional food industry association databases across Europe, North America, and Asia-Pacific.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanization indices, per-capita bakery consumption data, retail channel growth trends, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for commodity price volatility and macroeconomic uncertainty across the 2026-2034 forecast horizon.

Bakery Products Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered |

|

| Distribution Channels Covered | Convenience Stores, Supermarkets and Hypermarkets, Independent Retailers, Artisanal Bakeries, Online Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Grupo Bimbo, Mondelez International, Nestle, General Mills Inc., Flowers Foods, Britannia Industries, Parle Products, ITC, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, bakery products market outlook, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global bakery products market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the bakery products industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Bakery Products Market Report

The global bakery products market was valued at USD 549.1 Billion in 2025, driven by rising consumer demand for convenient RTC formats, urbanization, and health-oriented product innovation across all major regions.

The market is projected to reach USD 726.7 Billion by 2034, growing at a CAGR of 3.07% during 2026-2034, supported by e-commerce expansion, premiumization, and emerging market volume growth.

Bread and Rolls lead with a 33.9% product share in 2025, driven by staple household consumption across Europe and North America and growing packaged bread adoption in Asia-Pacific.

Online Stores are the fastest-growing channel at approximately 6.2% CAGR through 2034, driven by e-grocery integration, bakery subscription services, and direct-to-consumer brand expansion.

Europe dominates with a 36.3% share in 2025, underpinned by deeply embedded artisanal bakery culture, strong clean-label consumer demand, and robust EU food quality regulatory frameworks.

Key drivers include shifting consumer preferences toward healthy and convenient formats, rapid urbanization, e-commerce channel expansion, product innovation, and premiumization trends across Europe and North America.

Leading players include Grupo Bimbo, Mondelez International, Nestle, General Mills Inc., Flowers Foods, Britannia Industries, Parle Products, and ITC.

Key opportunities include health and functional bakery expansion, e-commerce platform development, clean-label formulation innovation, and emerging market volume growth across India, Southeast Asia, and Sub-Saharan Africa.

The market is segmented by Product Type (Bread and Rolls, Biscuits, Cakes and Pastries, Rusks), Distribution Channel (supermarkets and hypermarkets, Artisanal Bakeries, Independent Retailers, Convenience Stores, Online Stores), and Region.

Key trends include health and wellness reformulation, e-commerce channel acceleration, artisanal and premium product growth, clean-label adoption, and sustainability-led packaging innovation reshaping the global bakery industry.

Cakes and Pastries are the fastest-growing product sub-segment at 3.4% CAGR through 2034, driven by foodservice and QSR channel expansion, gifting occasions, and premiumization in developed markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)