Bancassurance Market Size, Share, Trends and Forecast by Product Type, Model Type, and Region, 2026-2034

Global Bancassurance Market Size, Share, Trends & Forecast (2026-2034)

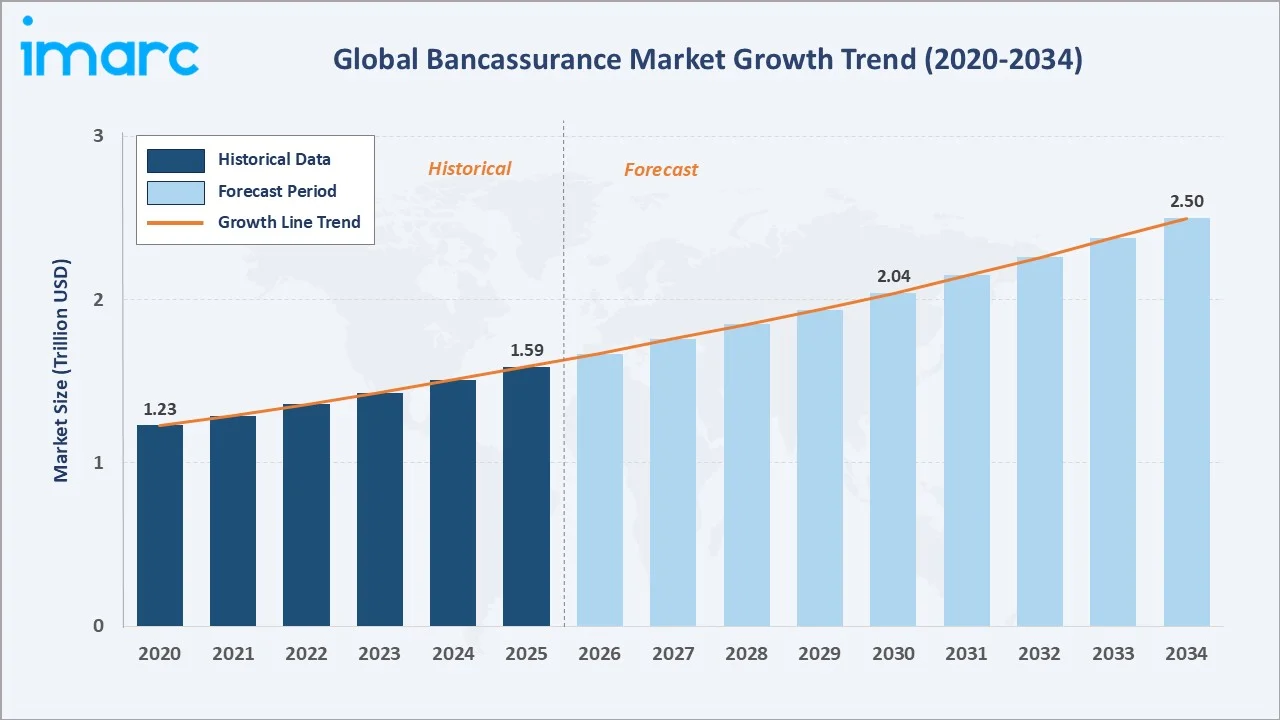

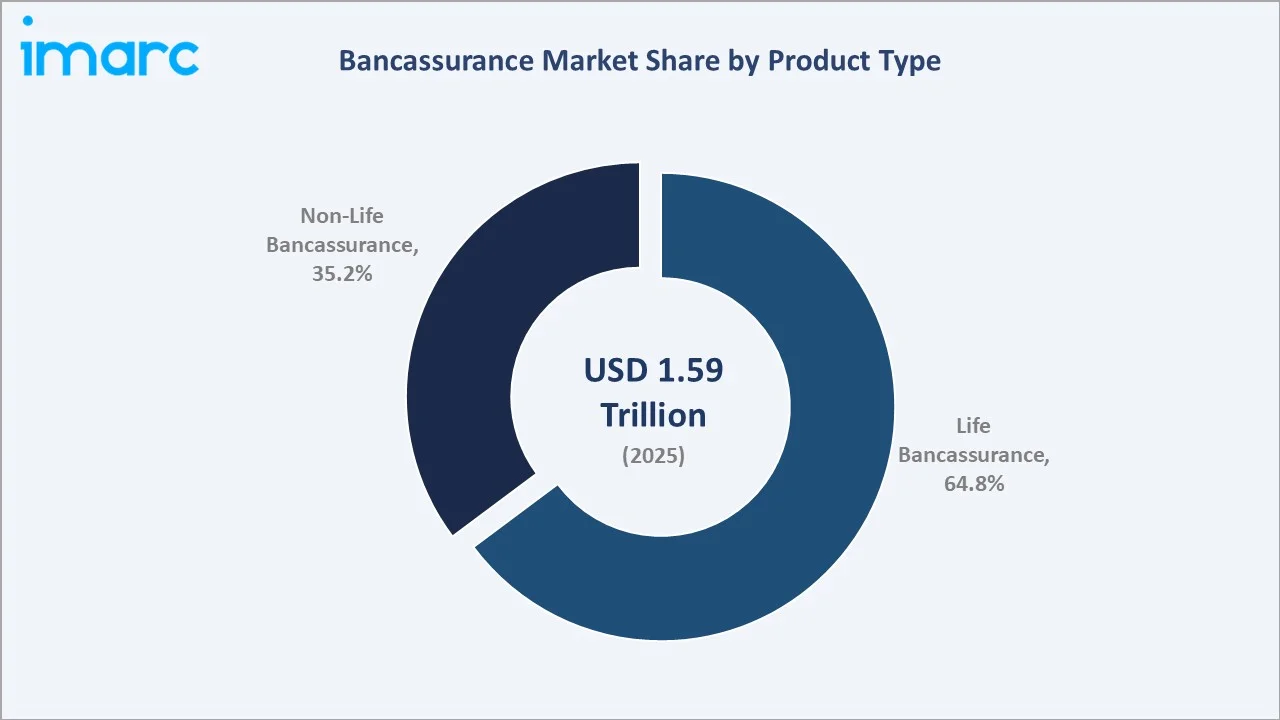

The global bancassurance market size was valued at USD 1.59 Trillion in 2025 and is projected to reach USD 2.50 Trillion by 2034, exhibiting a CAGR of 5.17% during the forecast period 2026-2034. Rising consumer demand for one-stop financial services, expanding bank branches and digital distribution networks, accelerating adoption of embedded life and non-life insurance products, and rising middle-class wealth accumulation across emerging markets, supported by sustained insurer-bank partnership formation, are driving the bancassurance market growth. Life Bancassurance dominates the product type segment at 64.8%, while Pure Distributor leads the model type segment at 38.9% in 2025. Europe accounts for 38.6% of global revenue in 2025, the world’s largest regional market, supported by deep insurer-bank consolidation.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.59 Trillion |

|

Forecast Market Size (2034) |

USD 2.50 Trillion |

|

CAGR (2026-2034) |

5.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (38.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~6.1%) |

|

Leading Product Type |

Life Bancassurance (64.8%, 2025) |

|

Leading Model Type |

Pure Distributor (38.9%, 2025) |

The global bancassurance market growth trajectory from 2020 through 2034 reflects a steady historical expansion from USD 1.23 Trillion to USD 1.59 Trillion, followed by a sustained forecast curve powered by digital distribution scale-up, embedded insurance growth, and rising middle-class wealth in Asia Pacific.

To get more information on this market, Request Sample

Segment-level CAGR comparisons highlight Asia Pacific and Joint Venture model bancassurance as two of the fastest-growing sub-segments within the global bancassurance industry analysis through 2034.

Executive Summary

The global bancassurance market is undergoing a digital reset, fuelled by the convergence of embedded insurance, mobile-first underwriting, and middle-class wealth accumulation in emerging Asia. Valued at USD 1.59 Trillion in 2025, the market is forecast to reach USD 2.50 Trillion by 2034 at a CAGR of 5.17%. Global insurance premiums crossed USD 7.1 Trillion in 2024, with bancassurance representing a significant share of global life-insurance distribution and signalling that bank-channel insurance is now a structural pillar of household financial services. Banks generate higher-margin fee income from bancassurance versus traditional lending, supporting deeper insurer-bank integration globally.

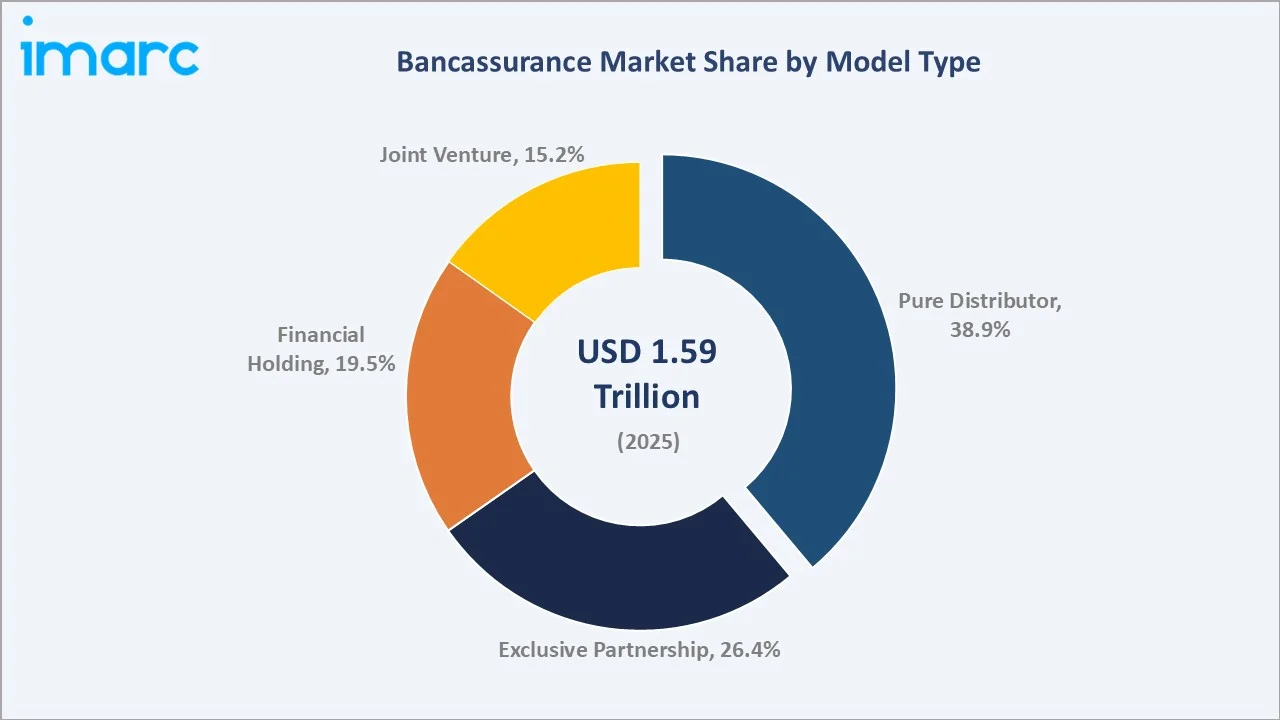

Life Bancassurance leads product type at 64.8% in 2025, anchored by long-tenor savings, retirement, and protection products embedded into bank wealth advisory channels. Pure Distributor commands the dominant model type share at 38.9% in 2025, supported by simple commission-based distribution agreements. Exclusive Partnership follows at 26.4%, with Financial Holding at 19.5% and Joint Venture at 15.2%.

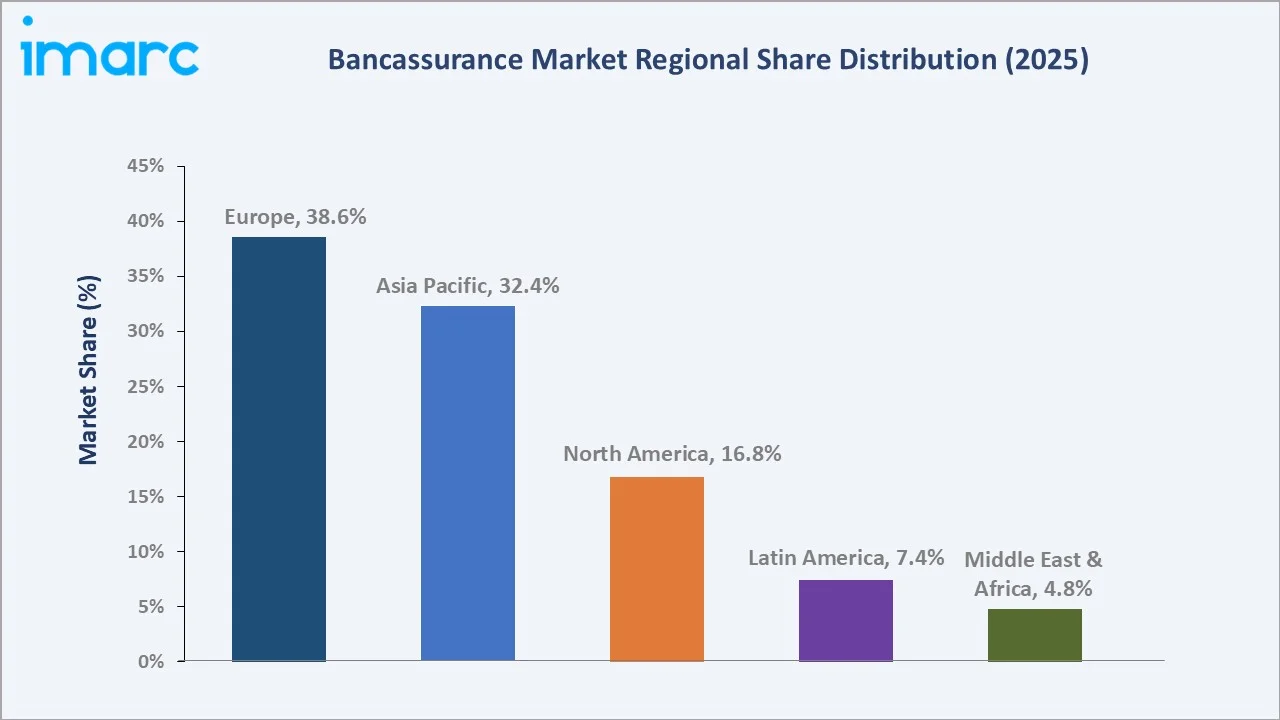

Europe dominates with a 38.6% global revenue share in 2025, led by France, Italy, and Spain, where bancassurance accounts for over 60% of life-insurance distribution, alongside vertically integrated leaders such as BNP Paribas Cardif, CNP Assurances, and Allianz. Asia Pacific holds 32.4%, with rapid growth in China, India, and Indonesia. North America at 16.8% remains underpenetrated relative to Europe, leaving structural growth headroom under the forecast period.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Life Bancassurance – 64.8% share (2025) |

|

Largest Model Type |

Pure Distributor – 38.9% share (2025) |

|

Leading Region |

Europe – 38.6% revenue share (2025) |

|

Second Region |

Asia Pacific – 32.4% revenue share (2025) |

|

Top Companies |

AXA, Allianz, BNP Paribas Cardif, AIA Group Limited, Prudential plc, MetLife Services and Solutions, LLC, Manulife, and Aviva |

Key Analytical Observations Supporting the Above Data:

- Life Bancassurance at 64.8% in 2025 dominates the product type segment, anchored by long-tenor savings, retirement, and protection products that align naturally with bank wealth advisory and customer relationships.

- Pure Distributor’s 38.9% dominance in 2025 reflects the simplicity of commission-based distribution agreements between banks and insurers, where the bank acts purely as a sales channel without underwriting risk.

- Europe’s 38.6% global dominance in 2025 reflects mature insurer-bank consolidation in France, Italy, and Spain, where bancassurance accounts for over 60% of life-insurance distribution across the largest national markets.

Global Bancassurance Market Overview

Bancassurance refers to the partnership-based distribution of insurance products through bank channels, where banks leverage their customer relationships, branch networks, and digital platforms to sell life and non-life insurance underwritten by partner or affiliated insurers. The model spans pure distribution agreements, exclusive partnerships, financial holding structures, and joint ventures.

Applications span the full retail and corporate financial services sector: life insurance, savings and retirement products, mortgage protection, motor and home insurance, health insurance, credit life policies, and increasingly embedded micro-insurance for SME banking customers across emerging markets.

Macroeconomic enablers include global insurance premiums crossing USD 7.1 Trillion in 2024, expanding emerging-market middle-class wealth, accelerating digital banking penetration, and rising consumer demand for one-stop financial services across the forecast period.

Market Dynamics

To evaluate market opportunities, Request Sample

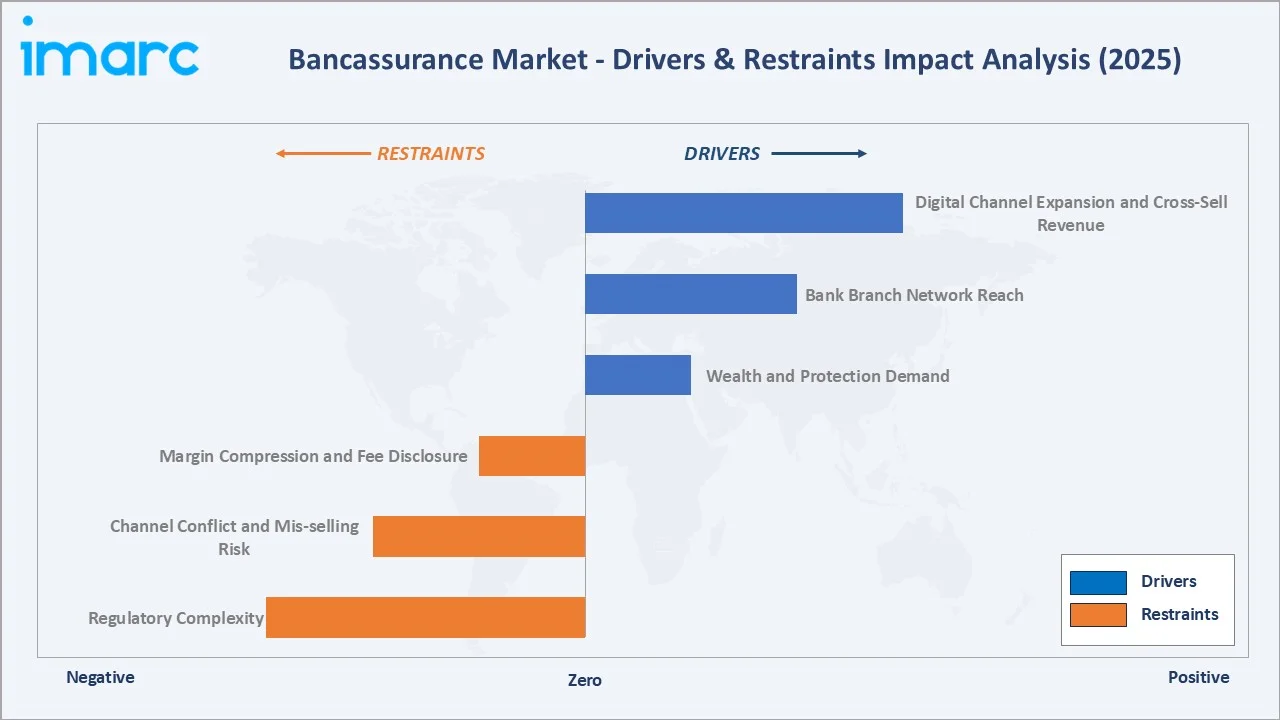

Market Drivers

- Wealth and Protection Demand: Global insurance premiums crossed USD 7.1 Trillion in 2024, which is the most powerful structural driver for sustained bancassurance demand. Rising middle-class wealth in Asia Pacific and Latin America is expanding demand for life, savings, and protection products that banks are uniquely positioned to distribute through long-standing customer relationships.

- Bank Branch Network Reach: Banks operate extensive physical and digital customer networks, serving billions globally and creating a highly efficient distribution platform for insurance. For example, in 2025, RHB Bank entered a 20-year exclusive bancassurance partnership with Tokio Marine and Takaful Malaysia to leverage its network for insurance distribution.

- Digital Channel Expansion and Cross-Sell Revenue: Mobile-first underwriting, embedded insurance APIs, and AI-driven cross-sell engines are enabling banks to monetise customer data through targeted insurance offers, with bancassurance fee income growing materially faster than traditional lending revenue across major banks.

Market Restraints

- Regulatory Complexity: Bancassurance operates under dual banking and insurance regulation. Capital adequacy rules, sales conduct codes, and anti-mis-selling regulations add structural compliance overhead, with rules varying significantly across the EU, US, India, and ASEAN jurisdictions.

- Channel Conflict and Mis-selling Risk: Bank-employee insurance sales create incentive misalignment risks, with multiple jurisdictions imposing fines on banks for misleading sales practices, complicating commission models and slowing aggressive cross-sell strategies in mature markets.

Market Opportunities

- Embedded Insurance and API-Native Distribution: Open banking and embedded insurance APIs are enabling instant policy issuance at the point of bank-product purchase. For instance, HSBC highlights that API platforms and embedded insurance are opening new distribution channels, enabling seamless, point-of-sale policy issuance and personalised customer experiences across digital ecosystems.

- Asia Pacific Middle-Class Wealth Expansion: India, Indonesia, Vietnam, and the Philippines are seeing rapid bancassurance penetration. Asia Pacific is expected to be the fastest-growing regional bancassurance market globally through 2034.

- AI-Driven Cross-Sell and Personalised Underwriting: Generative AI applied to bank customer data unlocks personalised insurance product recommendations, dynamic underwriting, and lifetime-value-optimised cross-sell across deposits, loans, and protection products through the forecast period.

Market Challenges

- Margin Compression and Fee Disclosure: Tightening transparency rules in the EU (IDD), UK (FCA), and India (IRDAI) require explicit commission disclosure, structurally compressing bank distribution margins and forcing rebalancing toward higher-value advisory products versus pure commission sales.

- Customer Trust and Sales Conduct: Multiple jurisdictions have penalised banks for bancassurance mis-selling, eroding customer trust and forcing investment in compliance, training, and product simplification, with conduct risk now a board-level priority across global banks.

Emerging Market Trends

1. Embedded Insurance and API-Native Distribution

The industry is transitioning from branch-led sales to API-native embedded insurance, where policies are issued instantly at the point of mortgage origination, credit card issuance, or SME loan disbursement, supporting straight-through underwriting at scale.

2. AI and Generative Underwriting in Bank Channels

Generative AI and large language models are entering bancassurance distribution at a pace. AXA’s 2024 generative AI underwriting pilot is the landmark reference deployment, enabling banker-assistant tools that recommend personalised insurance products in real time from customer data.

3. Mobile-First Insurance Onboarding

Mobile banking apps are becoming primary insurance distribution channels in Asia Pacific. In India, Indonesia, and the Philippines, mobile banking platforms drove a 26% increase in bancassurance penetration between 2022 and 2025.

4. ESG and Sustainable Insurance Products

Banks and insurers are co-developing climate-linked life, health, and home insurance products. ESG-linked bancassurance volume is forecast to scale meaningfully, supported by EU SFDR disclosure rules and growing customer demand for sustainable financial products.

5. Wealth Bancassurance and Private Banking Cross-Sell

Private banks and wealth advisors are increasingly bundling life insurance, annuities, and structured savings products into integrated wealth propositions, with mass affluent and high-net-worth segments driving disproportionate bancassurance fee revenue growth.

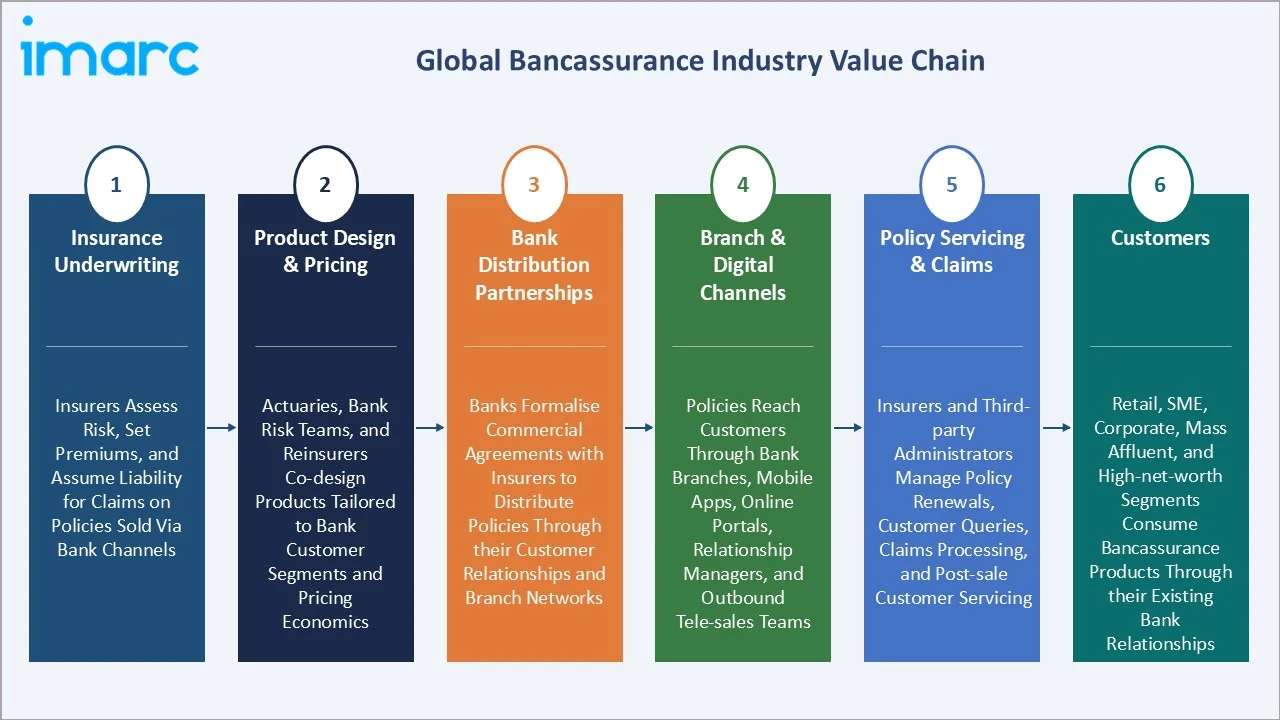

Industry Value Chain Analysis

The bancassurance value chain spans six integrated stages from insurance underwriting through end-customer servicing. Each stage exhibits distinct margin profiles, with bank distribution partnerships and product design capturing the largest share of unit economics.

|

Stage |

Key Players / Examples |

|

Insurance Underwriting |

Insurers assess risk, set premiums, and assume liability for claims on policies sold via bank channels. |

|

Product Design & Pricing |

Actuaries, bank risk teams, and reinsurers co-design products tailored to bank customer segments and pricing economics. |

|

Bank Distribution Partnerships |

Banks formalise commercial agreements with insurers to distribute policies through their customer relationships and branch networks. |

|

Branch & Digital Channels |

Policies reach customers through bank branches, mobile apps, online portals, relationship managers, and outbound tele-sales teams. |

|

Policy Servicing & Claims |

Insurers and third-party administrators manage policy renewals, customer queries, claims processing, and post-sale customer servicing. |

|

Customers |

Retail, SME, corporate, mass affluent, and high-net-worth segments consume bancassurance products through their existing bank relationships. |

Bank distribution partnerships and product design occupy the highest strategic value position in the bancassurance value chain, integrating actuarial pricing, customer data, and physical-plus-digital distribution into compelling consumer propositions. Banks retain a high share of distribution economics through commission and fee-sharing arrangements.

Technology Landscape in the Bancassurance Industry

API-Native Embedded Insurance Platforms

Modern bancassurance increasingly relies on API-native distribution layers connecting bank front-ends to insurer underwriting engines. Embedded insurance is experiencing strong growth, with platforms such as Bolttech, Wefox, and Cover Genius enabling real-time policy issuance within bank customer journeys across mortgage, credit card, and loan origination flows.

AI and Predictive Underwriting

AI-driven underwriting is transforming risk assessment and product personalisation. AXA, Allianz, and AIA have deployed generative AI underwriting tools that meaningfully reduce policy issuance time versus traditional manual underwriting workflows.

Mobile and Open Banking Integration

Mobile-first bancassurance is now the dominant onboarding channel in Asia Pacific. Open banking APIs combined with electronic Know-Your-Customer (eKYC) standards enable end-to-end mobile policy issuance in under 5 minutes, supporting embedded insurance scale across emerging markets through 2030.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Life Bancassurance |

64.8% |

2025 |

|

Model Type |

Pure Distributor |

38.9% |

2025 |

|

Region |

Europe |

38.6% |

2025 |

By Product Type

Life Bancassurance dominates at 64.8% in 2025, anchored by long-tenor savings, retirement, and protection products embedded into bank wealth advisory and mortgage origination journeys. Life bancassurance accounts for over 60% of life-insurance distribution in France, Italy, Spain, and Portugal, the deepest mature-market penetration globally, reflecting decades of insurer-bank integration across Continental Europe.

To access detailed market analysis, Request Sample

Non-Life Bancassurance at 35.2% in 2025 is anchored by motor, home, health, and credit-life insurance distributed alongside loan origination, credit cards, and current-account servicing, with the segment forecast to grow at a faster CAGR than life bancassurance through 2034 as embedded insurance scales globally.

By Model Type

Pure Distributor commands a 38.9% majority share in 2025, the largest of any model type, supported by simple commission-based distribution agreements where banks act purely as sales channels without underwriting risk. Exclusive Partnership follows at 26.4%, anchored by single-insurer banca-deals such as BNP Paribas Cardif’s long-standing tie-ups across European retail banks.

Financial Holding at 19.5% in 2025 reflects integrated bank-insurer corporate structures common in Continental Europe (Crédit Agricole-Predica, Generali Banca Generali) and parts of Asia. Joint Venture at 15.2% is the fastest-growing model, with insurer-bank JVs concentrated in India, China, and ASEAN where regulation supports multi-shareholder bancassurance ventures.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Europe |

38.6% |

France/Italy/Spain insurer-bank consolidation, Solvency II framework, mature retail bancassurance penetration |

|

Asia Pacific |

32.4% |

China life insurance growth, India IRDAI bancassurance expansion, Indonesia/Vietnam mobile bancassurance scale-up |

|

North America |

16.8% |

US bank-insurer wealth integration, Canada credit-protection bancassurance, structural growth headroom |

|

Latin America |

7.4% |

Brazil banca-deals expansion, Mexico mortgage-protection growth, rising middle-class formal financial inclusion |

|

Middle East & Africa |

4.8% |

GCC banca-deals expansion, takaful integration, South Africa retail bancassurance scale-up |

Europe commands a 38.6% global revenue share in 2025, the most dominant regional position of any global bancassurance market. France, Italy, Spain, and Portugal lead with bancassurance accounting for over 60% of life-insurance distribution across the four Mediterranean banking markets, supported by long-standing insurer-bank consolidation and Solvency II regulatory framework backing capital efficiency for bancassurance underwriting.

Asia Pacific at 32.4% in 2025 is anchored by China’s life-insurance market, India’s IRDAI bancassurance regulatory expansion, and rapid mobile-first onboarding across Indonesia, Vietnam, and the Philippines. India bancassurance enrolments grew over 65% via mobile channels in 2024, each representing a meaningful step-change in formal financial inclusion. North America at 16.8% remains underpenetrated relative to Europe, leaving structural growth headroom for US wealth-bancassurance expansion through 2034.

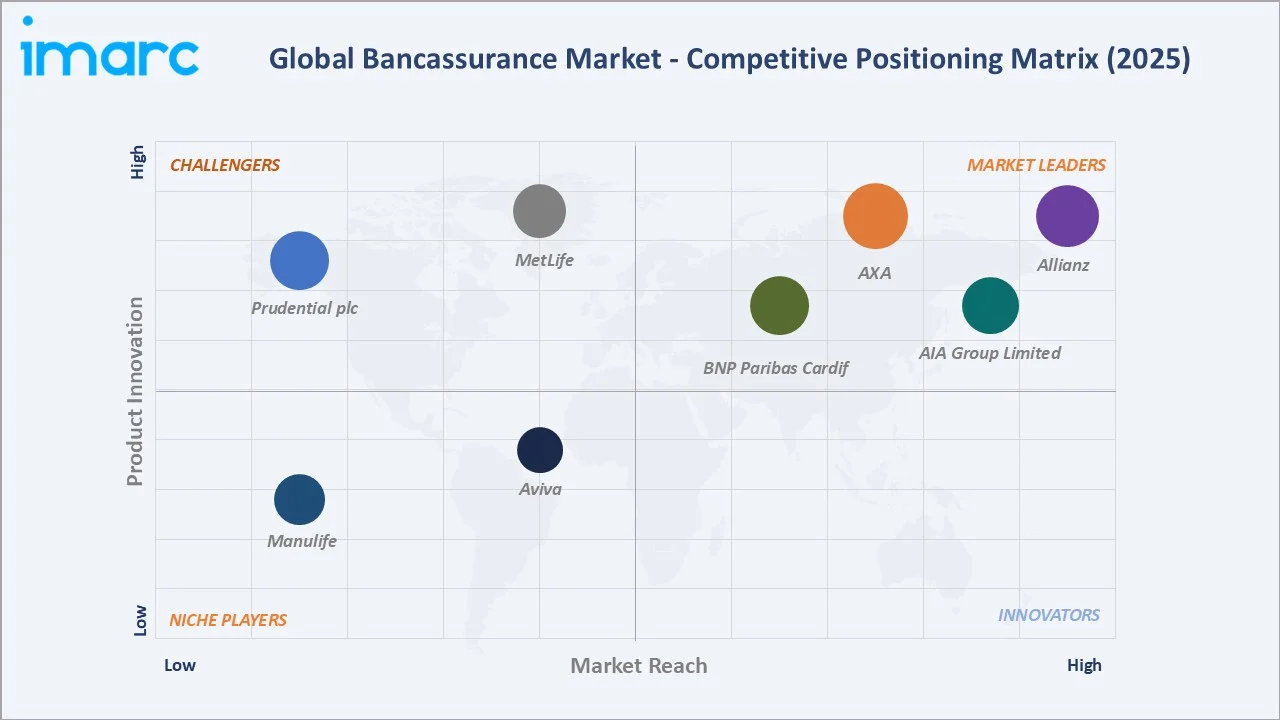

Competitive Landscape

|

Company Name |

Key Brand / Product Line |

Market Position |

Core Strength |

|

AXA |

AXA Life |

Leader |

European bancassurance scale, AXA-Banque tie-ups, generative AI underwriting |

|

Allianz |

Allianz Life |

Leader |

Pan-European banca-deals, Asia growth, integrated risk and asset management |

|

BNP Paribas Cardif |

Cardif |

Leader |

Largest exclusive bancassurance partner globally, 35+ country presence |

|

AIA Group Limited |

AIA Insurance (Hong Kong & Singapore) |

Leader |

Asia Pacific bancassurance leader, China and ASEAN bank tie-ups, digital underwriting |

|

Prudential plc |

Prudential |

Challenger |

Asia and Africa banca-deals, ICICI Pru tie-up, digital expansion |

|

MetLife Services and Solutions, LLC |

MetLife Insurance |

Challenger |

US group benefits, Asia bancassurance growth, integrated wealth proposition |

|

Manulife |

Manulife Asia Banca-Deals |

Emerging |

Asia Pacific banca-deals, DBS partnership, mobile-first underwriting investment |

|

Aviva |

Aviva UK & India |

Emerging |

UK bancassurance restructuring, India and Asia growth focus |

The bancassurance competitive landscape features integrated insurer-bank leaders commanding deep mature-market scale, alongside Asia Pacific specialist insurers with rapidly expanding bank distribution partnerships, and challenger players pivoting toward digital-native embedded insurance.

Key Company Profiles

AXA

AXA Group is one of the largest global insurance companies and a major bancassurance partner across Europe, with deep distribution tie-ups spanning multiple Continental European banks and a growing Asia Pacific footprint.

- Product & Platform Portfolio: AXA Life, AXA Health, AXA Wealth, AXA Banque, AXA Mobility, generative AI underwriting tools.

- Recent Developments: In August 2025, AXA announced the acquisition of Prima, the leading direct insurance player in Italy, with Euro 1.2 billion of premiums in 2024. In July 2025, AXA completed the sale of AXA Investment Managers (AXA IM) to BNP Paribas for cash proceeds of Euro 5.1 billion.

- Strategic Focus: AXA is pursuing a fully integrated bancassurance strategy spanning life, non-life, health, and wealth product distribution through bank channels. The group prioritises long-term exclusive bancassurance partnerships with deep cross-sell economics across European and Asian retail banking markets.

BNP Paribas Cardif

BNP Paribas Cardif is the dedicated bancassurance and creditor-protection arm of BNP Paribas, operating across 35+ countries with a uniquely large exclusive bancassurance partner network globally.

- Product & Platform Portfolio: Life insurance, creditor protection, savings products, motor and property insurance, partnership-distributed across multiple bank brands.

- Recent Developments: In April 2026, following the signature of a framework agreement between the BNP Paribas and Ageas Groups, BNP Paribas Fortis sold its 25% stake in AG Insurance for a total amount of EUR 1.9 billion and renewed its historical partnership in bancassurance with AG Insurance in Belgium.

- Strategic Focus: BNP Paribas Cardif’s strategy centers on building deep, exclusive bancassurance partnerships, embedded creditor protection, and digital distribution across mortgage, consumer finance, and SME banking flows. The group prioritises high-volume, long-term commercial relationships globally.

AIA Group Limited

AIA Group is the largest pan-Asian life insurer and a dominant bancassurance partner across China, ASEAN, India, and the broader Asia Pacific region, with deep multi-decade bank distribution tie-ups.

- Product & Platform Portfolio: Life and protection insurance, savings and retirement products, health insurance, distributed via bank partners and tied agency networks.

- Recent Developments: In April 2026, AIA Group Limited announced 13 per cent growth in value of new business (VONB) on constant exchange rates (CER), with Mainland China and Hong Kong, its two largest markets, both growing over 20%.

- Strategic Focus: AIA’s strategy combines deep pan-Asia bancassurance partnership scale with mobile-first digital underwriting and integrated agency-plus-bank distribution. The company prioritises long-tenor savings and protection products distributed through both bank partners and direct agency channels across Asia Pacific markets.

Market Concentration Analysis

The global bancassurance market exhibits moderate concentration. The top five insurer-bank groups, AXA, Allianz, BNP Paribas Cardif, AIA Group, and Prudential, collectively account for approximately 30-35% of global bancassurance gross written premiums and distribution agreements in 2025.

The market remains structurally fragmented at the regional level, with hundreds of bank-insurer distribution agreements active globally. Fragmentation is most pronounced in Asia Pacific and Latin America, where new banca-deals continue to form rapidly across emerging-market retail banking.

Consolidation is accelerating around three vectors: insurer-bank financial holding integration, exclusive partnership renegotiation, and Asia Pacific joint venture formation. The top 10 insurers are projected to capture over 55% of global bancassurance value by 2030.

Investment & Growth Opportunities

Fastest-Growing Segments

Joint Venture model bancassurance and Non-Life Bancassurance are among the highest-growth sub-segments through 2034. JV models benefit from regulatory support in India, China, and ASEAN, while non-life embedded insurance is scaling rapidly via API distribution into bank credit and mortgage flows.

Emerging Market Expansion

India, Indonesia, Vietnam, and the Philippines represent the highest-velocity expansion markets, supported by mobile bancassurance, IRDAI regulatory expansion in India, and rapid middle-class wealth accumulation. Combined, these markets are forecast to add substantial cumulative bancassurance value through 2034.

Venture & Private Investment Trends

Notable transactions include AXA’s expanded Asia bancassurance investments, BNP Paribas Cardif’s embedded insurance API rollout, and the emergence of dedicated insurtech-bancassurance funds. Bancassurance technology platforms continued attracting venture investment through 2024-2025, supporting bank distribution of life, non-life, and credit-protection insurance products.

Future Market Outlook (2026-2034)

The global bancassurance market forecast projects steady value expansion from USD 1.59 Trillion in 2025 to USD 2.50 Trillion by 2034 at a CAGR of 5.17%, a steady increase over nine years, underpinned by digital distribution scale-up, embedded insurance growth, AI-driven cross-sell, and rising emerging-market middle-class wealth.

Three structural discontinuities will reshape the bancassurance market through 2034. Embedded insurance will dissolve historical channel boundaries by 2027, unlocking real-time policy issuance at scale. AI-driven cross-sell will redefine personalised underwriting by 2028. Open banking standards will enable cross-bank insurance product portability by 2030.

By 2034, the bancassurance industry is forecast to have transformed from a primarily branch-led commission model into a multi-channel, API-native distribution platform spanning physical, mobile, and embedded insurance flows. The competitive landscape will be shaped by integrated European bancassurance leaders, Asia Pacific specialist insurers, and digital-native embedded insurance platforms.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with bancassurance industry stakeholders, including insurer distribution executives, bank insurance heads, regulatory policy specialists, embedded insurance platform leaders, and institutional investors in insurer-bank partnerships. Primary insights validated market sizing, segmentation, and competitive positioning.

Secondary Research

Secondary sources include Swiss Re sigma reports, Allianz Global Insurance Map, OECD Insurance Statistics, IRDAI Annual Reports, EIOPA publications, IFRS 17 implementation reports, and trade coverage from Reuters, Insurance Insider, and Asia Insurance Review.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating gross written premium trends, bancassurance penetration rates, bank branch counts, ARPU benchmarks, and digital channel adoption curves. Scenario analysis (base, optimistic, conservative) accounted for regulatory and macro risk.

Bancassurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Life Bancassurance, Non-Life Bancassurance |

| Model Types Covered | Pure Distributor, Exclusive Partnership, Financial Holding, Joint Venture |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | AXA, Allianz, BNP Paribas Cardif, AIA Group Limited, Prudential plc, MetLife Services and Solutions, LLC, Manulife, Aviva, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the bancassurance market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global bancassurance market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the bancassurance industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Bancassurance Market Report

The global bancassurance market was valued at USD 1.59 Trillion in 2025, driven by digital distribution scale-up, embedded insurance growth, and rising middle-class wealth across major emerging markets.

The market is projected to reach USD 2.50 Trillion by 2034, growing at a CAGR of 5.17% during 2026-2034, driven by AI cross-sell, embedded insurance, and Asia Pacific middle-class wealth expansion.

Pure Distributor leads with a 38.9% share in 2025, supported by simple commission-based distribution agreements where banks act as sales channels without underwriting risk for the partner insurer.

Life Bancassurance leads with a 64.8% share in 2025, anchored by long-tenor savings, retirement, and protection products that align naturally with bank wealth advisory and customer lifecycle.

Europe leads with a 38.6% share in 2025, driven by France, Italy, and Spain where bancassurance accounts for over 60% of life-insurance distribution across mature retail banking markets.

Key drivers include rising wealth and protection demand, expansive bank branch and digital networks, embedded insurance API distribution, and AI-driven personalised underwriting across global retail banking.

Asia Pacific and Joint Venture model bancassurance are the fastest-growing combinations through 2034, both projecting over 5.5% CAGR, fuelled by regulatory expansion and middle-class wealth growth.

Leading companies include AXA, Allianz, BNP Paribas Cardif, AIA Group Limited, Prudential plc, MetLife Services and Solutions, LLC, Manulife, and Aviva.

Bancassurance is the partnership-based distribution of insurance products through bank channels, where banks leverage customer relationships and branch networks to sell life and non-life policies underwritten by insurers.

Embedded insurance integrates policy issuance directly into bank product flows, such as mortgage origination or credit card issuance, enabling real-time underwriting and policy delivery without separate sales journeys.

AI is being integrated into underwriting, cross-sell engines, customer segmentation, and policy servicing, unlocking personalised insurance product recommendations and faster policy issuance through bank channels.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)