Bio-Lubricants Market Size, Share, Trends and Forecast by Base Oil Type, Application, End Use Industry, and Region 2026-2034

Global Bio-Lubricants Market Size, Share, Trends & Forecast (2026-2034)

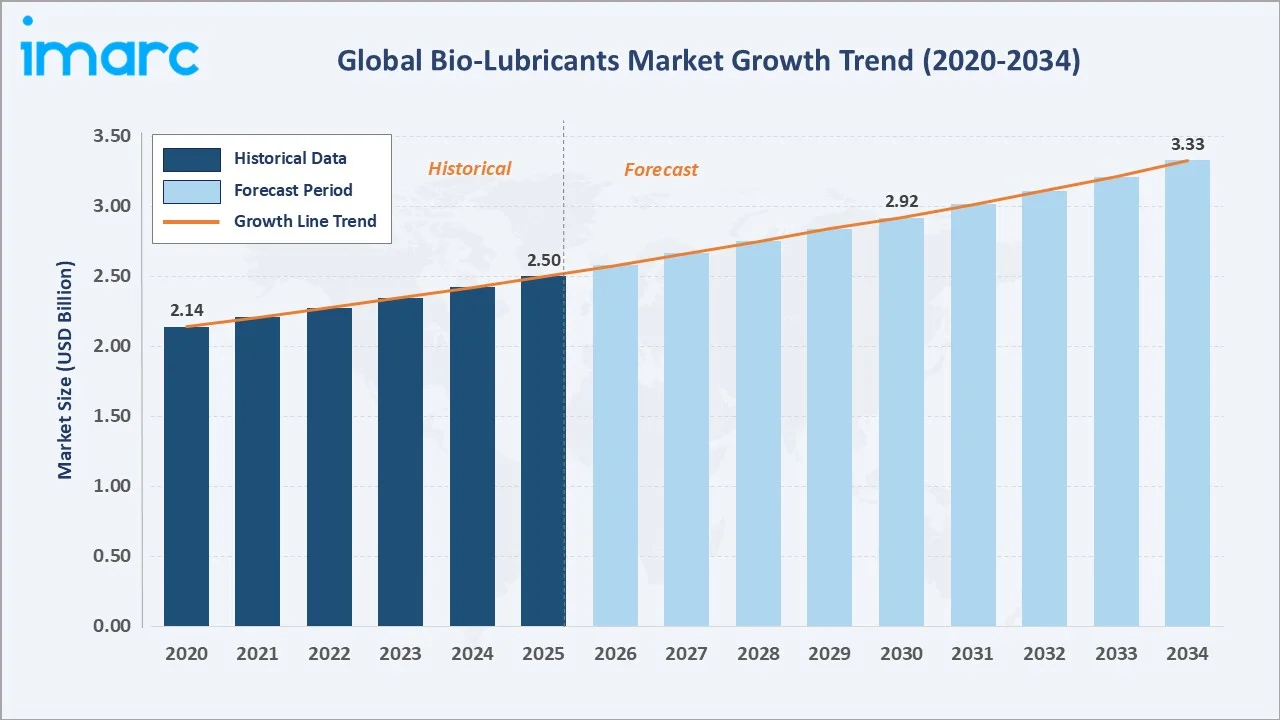

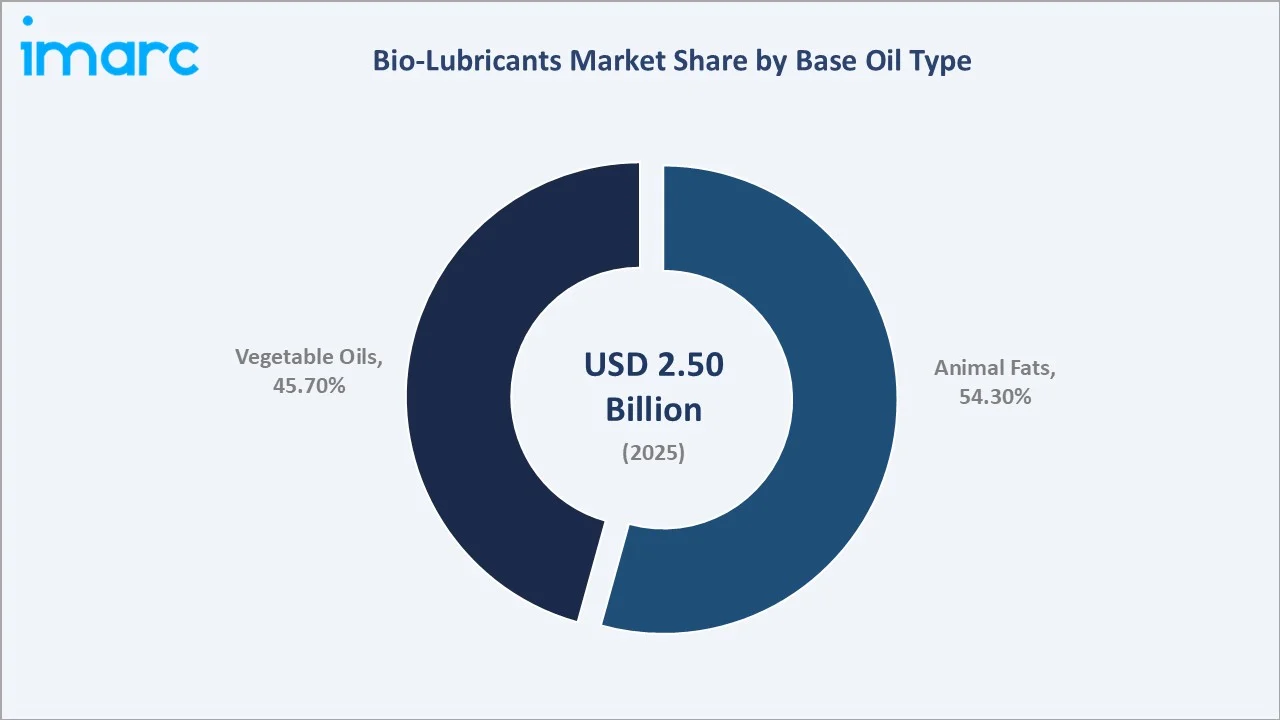

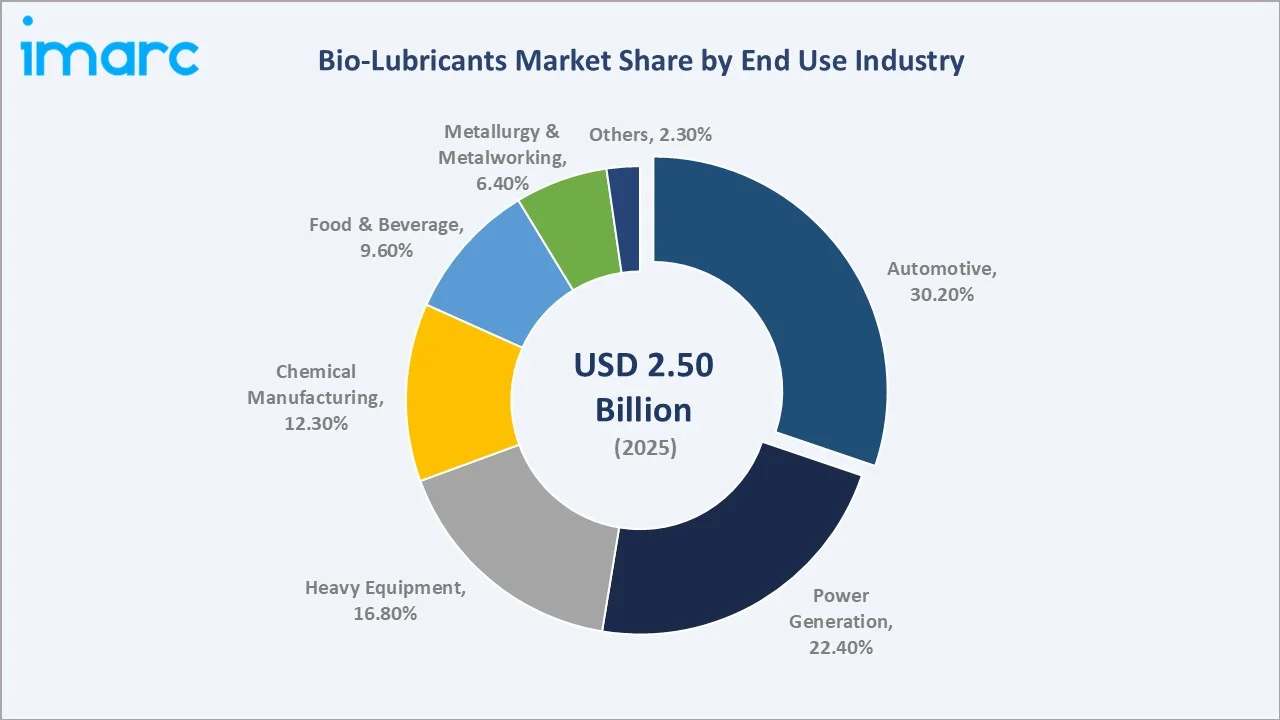

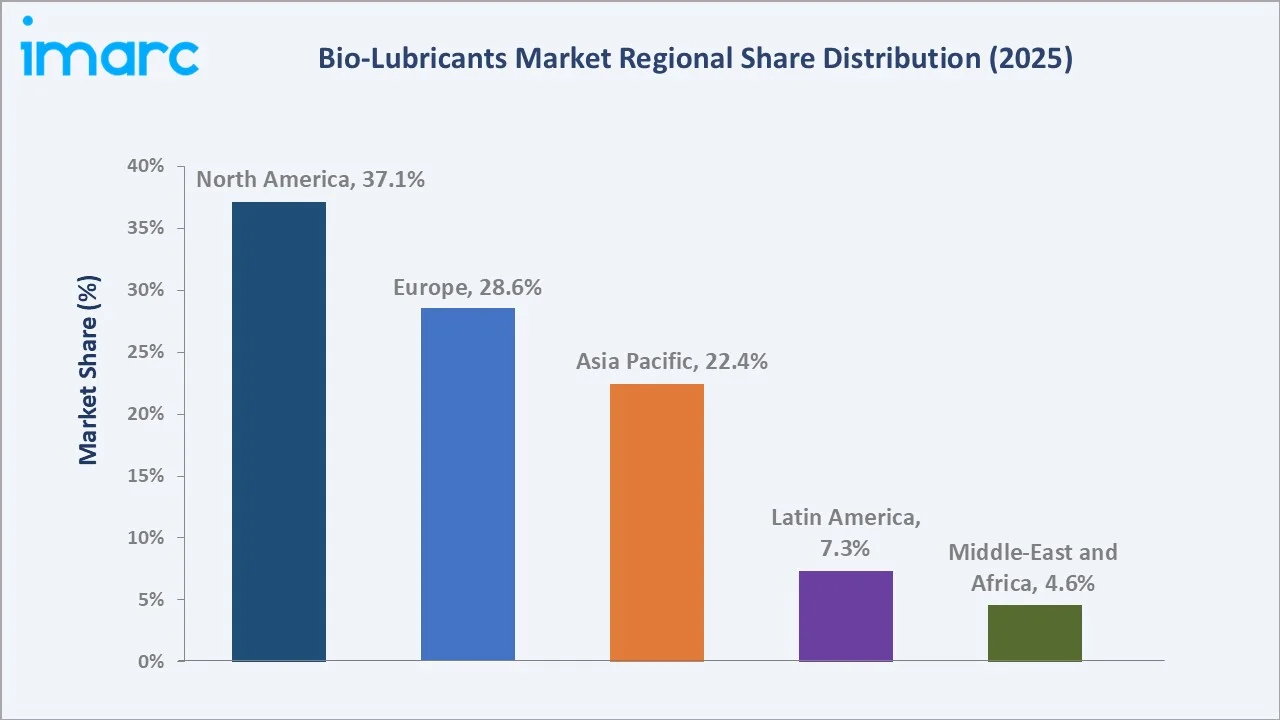

The global bio-lubricants market reached a value of USD 2.50 Billion in 2025 and is projected to reach USD 3.33 Billion by 2034, exhibiting a CAGR of 3.1% during the forecast period (2026-2034). Market expansion is supported by tightening environmental regulations, rising demand for biodegradable industrial inputs, growing adoption across the automotive and power generation sectors, and improving performance parity of bio-based formulations with conventional mineral lubricants. North America dominates with a 37.1% regional share in 2025, followed by Europe (28.6%) and Asia Pacific (22.4%). Animal fats lead by base oil type at 54.3% in 2025. The market is expected to reach USD 2.92 Billion by 2030. Key industry players include Shell plc, TotalEnergies, Fuchs SE, Castrol Limited, and Kluber Lubrication.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.50 Billion |

|

Forecast Market Size (2034) |

USD 3.33 Billion |

|

CAGR (2026-2034) |

3.1% |

|

Base Year |

2025 |

|

Historical Period |

2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.1%, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Dominant Base Oil Type |

Animal Fats (54.3%, 2025) |

|

Largest End Use Industry |

Automotive (30.2%, 2025) |

From USD 2.14 Billion in 2020 to USD 2.50 Billion in 2025, the bio-lubricants market demonstrated consistent resilience through supply chain disruptions and commodity price volatility. The forecast addition of approximately USD 824 Billion through 2034 reflects structural demand momentum anchored by regulatory mandates, sustainability commitments, and ongoing formulation technology improvements.

To get more information on this market, Request Sample

The 3.1% CAGR over 2026–2034 reflects a steady, regulation-backed expansion. Animal fats-based bio-lubricants, commanding a 54.3% share in 2025, serve as the primary volume anchor.

Executive Summary

The global bio-lubricants market stood at USD 2.50 Billion in 2025, driven by the convergence of rising environmental regulation, technological advances in bio-based ester formulations, and expanding middle-class industrial consumption in Asia, North America, and Europe. The market is forecast to reach USD 3.33 Billion by 2034 at a CAGR of 3.1%, passing USD 2.92 Billion by 2030. Animal fats dominate the base oil type landscape at 54.3% (2025), followed by vegetable oils at 45.7%. Automotive leads end use at 30.2%, with power generation (22.4%) and heavy equipment (16.8%) constituting the next two largest segments. These three end-use industries collectively represent over 69% of total market revenues in 2025.

From a regional perspective, North America leads at 37.1% (2025), reflecting EPA Vessel General Permit (VGP) mandates, the USDA BioPreferred Program directing over Billions in federal procurement annually, and robust commercial vehicle fleet adoption. Europe follows at 28.6%, supported by the EU Ecolabel, Blue Angel certification, and Green Deal sustainability targets. Asia Pacific at 22.4% is the fastest-growing region, as China's green manufacturing directives and India's wind energy expansion, targeting 140 GW by 2030, drive structural demand for biodegradable industrial lubricants.

Key Market Insights

|

Insight |

Data |

|

Largest Base Oil Type |

Animal Fats – 54.3% (2025) |

|

Largest End Use Industry |

Automotive – 30.2% (2025) |

|

Leading Region |

North America – 37.1% (2025) |

|

Fastest Growing Region |

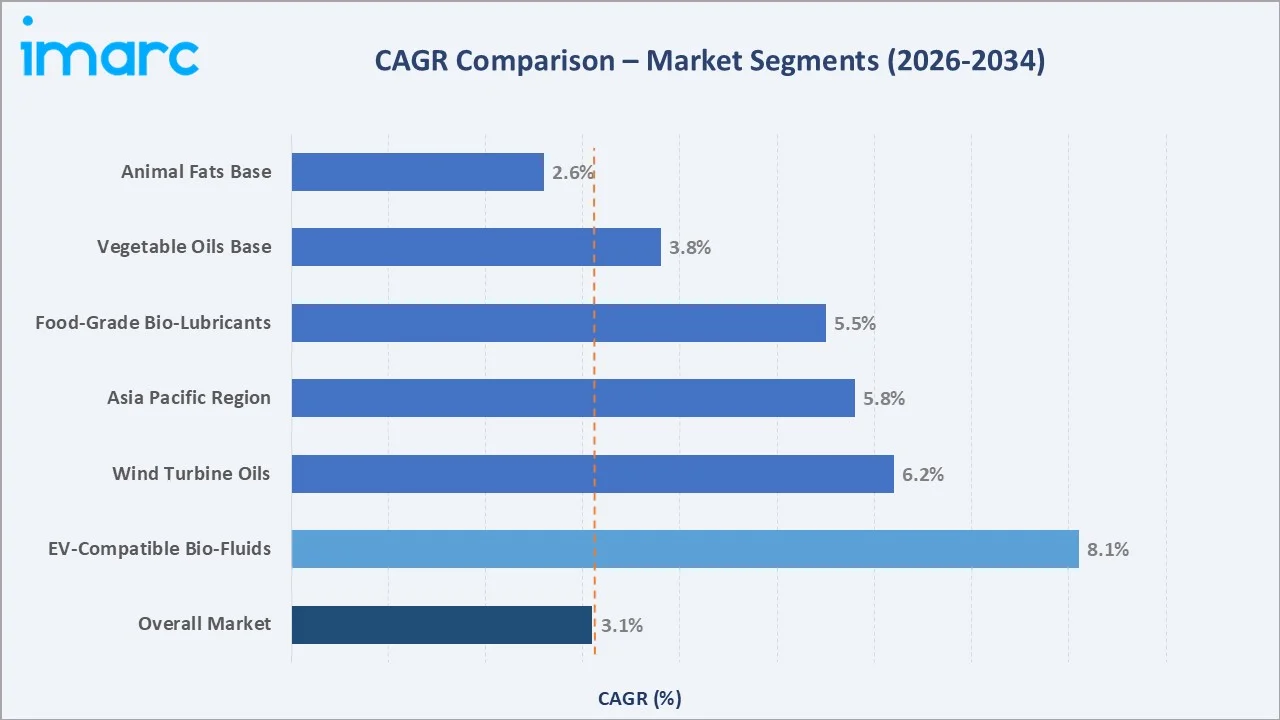

Asia Pacific (~5.8% CAGR, 2026-2034) |

|

Top Companies |

Shell plc, TotalEnergies, Fuchs SE, Castrol Limited, Kluber Lubrication |

|

Market Opportunity |

EV drivetrain bio-fluids and food-grade NSF H1 lubricants in Asia Pacific |

Key Analytical Observations Supporting the Above Data:

- Animal fats' 54.3% dominance (2025) reflects their superior oxidative stability, high viscosity index, and excellent load-bearing capacity, making them the preferred base oil for gear systems, turbines, and heavy-duty compressor applications in industrial environments globally.

- The automotive segment's 30.2% share (2025) is anchored by engine oil, gear oil, and transmission fluid applications. Major OEMs including Volvo and Scania have approved bio-lubricant formulations in their specifications since 2022, accelerating fleet-level adoption.

- North America's 37.1% share is driven by the USDA BioPreferred Program and EPA VGP mandates for environmentally acceptable lubricants (EALs) in water-adjacent marine operations, creating consistent institutional demand that is insulated from commodity price competition.

Global Bio-Lubricants Market Overview

Bio-lubricants are lubricating fluids derived from renewable biological sources, primarily vegetable oils and animal fats, engineered to replace conventional petroleum-based lubricants in automotive, industrial, and specialty applications. The market encompasses the formulation, distribution, and end-use of bio-based hydraulic fluids, gear oils, chainsaw oils, metalworking fluids, mold release agents, two-cycle engine oils, and greases across 100+ countries. As of 2025, the market is valued at USD 2.50 Billion and supports critical operations across energy, manufacturing, transportation, food processing, and construction sectors. Macroeconomic tailwinds including carbon-neutrality pledges by G7 governments, expanding eco-certification programs such as the EU Ecolabel and USDA BioPreferred, and rising agricultural feedstock availability are sustaining structural demand expansion. Despite 20–40% price premiums versus conventional lubricants, total cost of ownership advantages including extended drain intervals, biodegradability compliance cost avoidance, and regulatory penalty risk reduction are driving industrial switching decisions globally.

Market Dynamics

To evaluate market opportunities, Request Sample

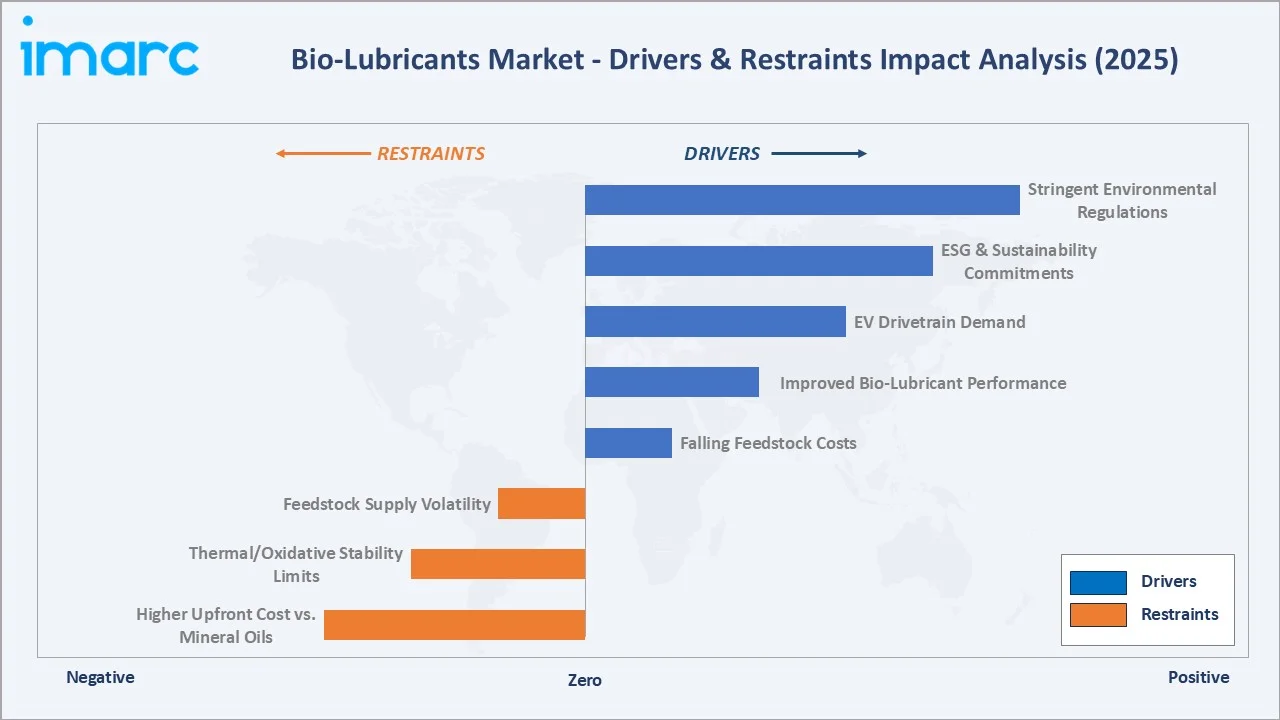

Market Drivers

- Stringent Environmental Regulations: The EU's Water Framework Directive and U.S. EPA Vessel General Permit (VGP) mandate the use of environmentally acceptable lubricants (EALs) in water-adjacent applications, creating sustained baseline demand. Regulatory compliance is increasingly non-negotiable for marine, forestry, and offshore operators across North America and Europe.

- ESG and Sustainability Commitments: Rising corporate ESG obligations are driving fleet operators, power plant managers, and equipment OEMs to adopt bio-lubricants as part of Scope 3 emission reduction commitments. Major automotive OEMs, including Volvo and Scania have approved bio-lubricant formulations in their technical specifications since 2022, accelerating first-fill and aftermarket adoption.

- Improved Bio-Lubricant Performance: Technological advances in esterification and transesterification processing have significantly elevated bio-lubricant performance. Modern formulations achieve viscosity indices exceeding 200, matching or surpassing Group III mineral oil performance, while modern cold-start additives enable pour points down to minus 40 degrees Celsius, expanding application range into cold-climate markets.

- Falling Feedstock Costs: The global scale-up of biodiesel, renewable diesel, and sustainable aviation fuel (SAF) production is increasing the supply and reducing the cost of vegetable oil-based feedstocks, directly lowering bio-lubricant production costs and enabling competitive pricing strategies in price-sensitive industrial segments.

- E-commerce and Expanding Distribution Networks: Online industrial supply platforms and specialized bio-lubricant distributors, including Brenntag and Univar Solutions, are broadening market access for certified bio-lubricant products, reducing the channel access barriers that historically limited bio-lubricant adoption outside of major industrial markets.

Market Restraints

- Higher Upfront Cost Versus Mineral Lubricants: Bio-lubricants carry a 20–40% price premium over conventional mineral lubricants at the point of sale, limiting adoption among price-sensitive SME operators in Latin America, South Asia, and Sub-Saharan Africa, where regulatory mandates remain less stringent and cost competitiveness is the primary procurement criterion.

- Thermal and Oxidative Stability Limitations: Vegetable oil-derived bio-lubricants exhibit limited hydrolytic stability and lower oxidation resistance at elevated temperatures compared to Group III/IV synthetic lubricants, restricting their use in high-temperature turbine and compressor applications without additional additive packages that increase formulation costs.

- Feedstock Supply and Price Volatility: Agricultural-origin feedstock supply is subject to crop yield fluctuations driven by climate events, competition with biofuel mandates, and geopolitical disruptions. Feedstock price volatility directly impacts bio-lubricant manufacturer margins, creating pricing instability that complicates long-term supply contracts with industrial customers.

Market Opportunities

- EV Drivetrain Bio-Lubricant Development: The rapid growth of electric vehicle fleets globally is creating demand for specialized bio-based e-axle gear fluids, thermal management fluids, and dielectric coolants. Bio-based fluids' inherent electrical insulation properties position them advantageously for next-generation EV drivetrain applications, representing the fastest-growing new product category in the bio-lubricants innovation pipeline.

- Food-Grade Certification Market Expansion: Food and beverage manufacturers are transitioning to NSF H1-certified food-grade bio-lubricants to comply with FDA 21 CFR and EU Regulation 1935/2004. The food & beverage segment, at 9.6% of market revenues in 2025, is growing as food safety enforcement intensifies in Asia and Latin America and major processors adopt global procurement standards.

- Offshore Wind Energy Infrastructure: Offshore wind installations, projected to exceed 212 GW cumulatively by 2030, require large volumes of biodegradable hydraulic fluids and gear oils for nacelle and pitch control systems. This creates a structurally growing, specification-driven demand segment with limited substitution risk from conventional lubricants due to EAL regulatory requirements.

Market Challenges

- Complex Multi-Certification Requirements: Obtaining multiple industry-specific certifications including NSF H1, EU Ecolabel, Blue Angel, and ISO 15380, requires significant investment in testing, documentation, and third-party auditing. This certification burden creates barriers for smaller bio-lubricant producers seeking to access premium-priced regulated markets in Europe and North America.

- Technical Knowledge Gaps in Industrial Adoption: Many industrial maintenance engineers and fleet operators lack familiarity with bio-lubricant compatibility requirements, including seal material compatibility, miscibility with mineral oils, and recommended drain intervals. This knowledge gap slows retrofit adoption in established maintenance programs, particularly in developing markets.

- Competition from High-Performance Synthetic Lubricants: Group III and PAO synthetic lubricants combine high performance with moderate sustainability credentials and compete directly with bio-lubricants in premium industrial and automotive segments, offering lower price premiums over mineral oils and broader OEM approvals than most bio-based alternatives currently achieve.

Emerging Market Trends

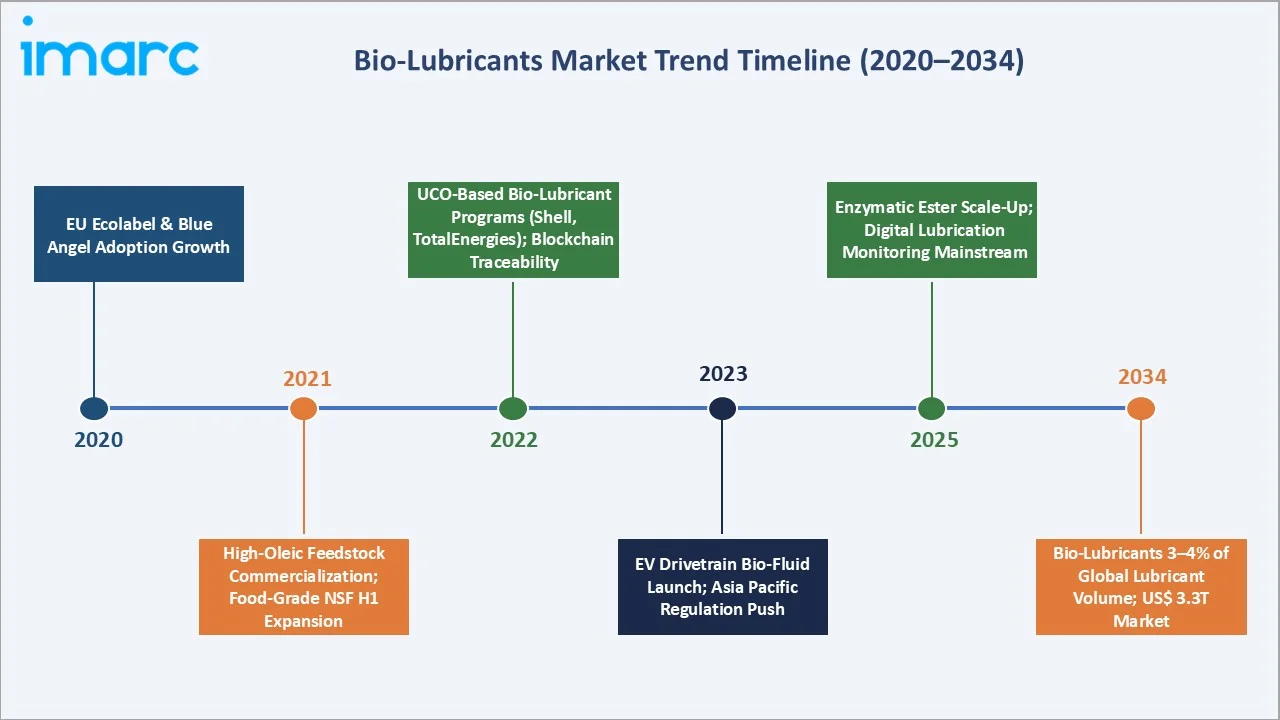

The global bio-lubricants market is being reshaped by five converging trends that are redefining formulation technology, feedstock sourcing, regulatory compliance, and competitive dynamics through 2034.

1. Bio-Based High-Performance Ester Formulations

Synthetic esters derived from bio-based feedstocks are increasingly replacing both mineral and conventional synthetic lubricants in high-performance applications. Polyol esters and complex esters offer superior biodegradability, exceeding 60% in 28 days per OECD 301B while achieving thermal stability up to 250 degrees Celsius, opening turbine oil and aviation fluid applications previously inaccessible to bio-lubricants.

2. Circular Economy Feedstock Integration

Leading bio-lubricant producers are transitioning toward second- and third-generation feedstocks , including used cooking oil (UCO), tallow from meat processing waste, and algae-derived lipids, to reduce competition with food supply chains and qualify for EU Renewable Energy Directive (RED III) waste feedstock incentives.

3. Blockchain-Enabled Supply Chain Traceability

Blockchain-enabled traceability platforms are being deployed across bio-lubricant supply chains to certify feedstock origin, carbon intensity, and sustainability credentials from farm to finished product. This is particularly relevant for food-grade and environmentally acceptable lubricant (EAL) segments, where buyers require auditable chain-of-custody documentation.

4. Asia Pacific Industrial Bio-Lubricant Adoption Acceleration

China, India, and Southeast Asia are progressively adopting bio-lubricant standards in manufacturing, mining, and construction equipment sectors. India's Bureau of Indian Standards (BIS) published updated bio-lubricant performance specifications in 2023.

5. EV-Compatible Bio-Lubricant Product Development

As electric vehicle penetration accelerates globally, targeting 30–40% of new vehicle sales by 2030 in key markets, lubricant manufacturers are investing in bio-based e-axle transmission fluids, thermal interface materials, and dielectric cooling fluids engineered for EV powertrain architectures.

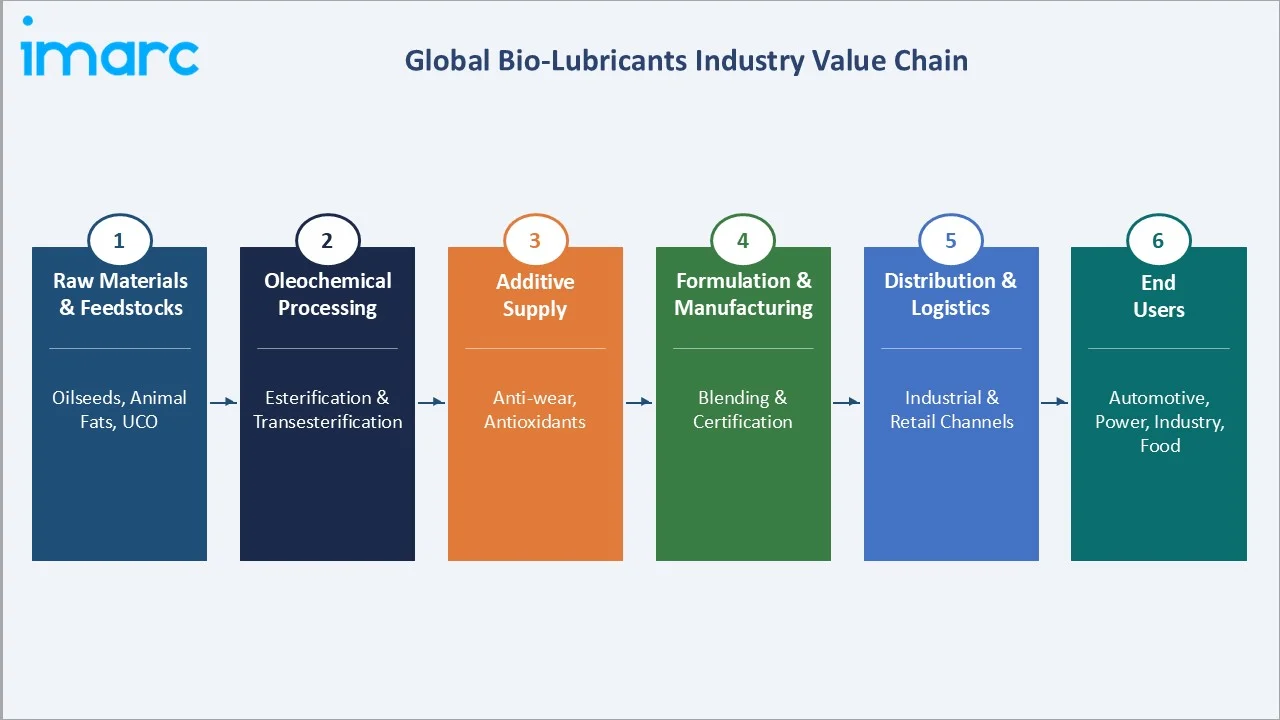

Industry Value Chain Analysis

The bio-lubricants industry value chain spans six interconnected stages from agricultural feedstock sourcing to end-user application. Each stage requires specialized infrastructure, certification expertise, and quality management systems to deliver performance-grade, sustainably certified bio-lubricant products to demanding global markets.

|

Stage |

Key Activities |

Representative Players |

|

Raw Materials & Feedstocks |

Oilseed farming (soy, rapeseed, sunflower), animal rendering, used cooking oil collection |

ADM, Bunge, Cargill, rendering facilities |

|

Oleochemical Processing |

Transesterification, esterification, refining of bio-based base oils and synthetic esters |

Emery Oleochemicals, Croda, BASF |

|

Additive Supply |

Anti-wear, antioxidant, viscosity modifier, and pour point depressant additives for bio-lubricant formulation |

Evonik, Afton Chemical, Lubrizol |

|

Formulation & Manufacturing |

Blending, additive incorporation, packaging, certification testing, quality control |

Shell, TotalEnergies, Fuchs, Kluber, Castrol |

|

Distribution & Logistics |

Industrial distributors, automotive aftermarket channels, e-commerce, cold-chain export |

Brenntag, Univar Solutions, Amazon Business |

|

End Users |

Automotive OEMs, power plants, food manufacturers, heavy equipment operators |

Volvo, Siemens, Nestlé, Caterpillar, John Deere |

The formulation and manufacturing stage is the critical value-creation node in the chain, where commodity bio-based base oils are transformed into specification-grade, certified products commanding retail price premiums of 20–40% over farm-gate feedstock cost. Cold chain integrity and certification compliance across the distribution stage are equally critical determinants of market access for bio-lubricant producers targeting regulated premium markets in Europe and North America.

Technology Landscape in the Bio-Lubricants Industry

Advanced Esterification and Transesterification Technology

Modern continuous-process esterification plants operate at conversion efficiencies exceeding 98%, producing high-purity ester base oils with consistent viscosity and biodegradability profiles. Low-temperature enzymatic transesterification using lipase catalysts is emerging as a next-generation production pathway, reducing energy consumption significantly versus conventional acid/base catalysis and generating fewer chemical waste streams, improving the overall environmental credentials of bio-lubricant production operations.

Genetically Engineered High-Oleic Feedstocks

High-oleic sunflower (HOSO) and high-oleic soybean varieties, with oleic acid content exceeding 80%, deliver superior oxidative stability for bio-lubricant base oil production. Companies including Corteva Agriscience and Nuseed have commercialized tailored oilseed varieties for industrial lubricant applications, reducing the need for synthetic antioxidant additive packages and improving the intrinsic biodegradability profile of finished formulations.

AI-Driven Formulation and Digital Farm Management

Machine learning models are being applied to bio-lubricant formulation optimization, predicting viscosity index, pour point, and biodegradability outcomes for novel ester-additive combinations , dramatically shortening product development cycles from 18 months to under 6 months.

Market Segmentation Analysis

By Base Oil Type

Animal fats dominate the global bio-lubricants market with a 54.3% share in 2025, driven by their high viscosity index, excellent boundary lubrication properties, and widespread availability from meat processing co-streams. Tallow-based lubricants are particularly prevalent in metalworking, gear oil, and heavy-duty industrial segments where thermal load resistance is paramount

To access detailed market analysis, Request Sample

Vegetable oils account for 45.7% of the market in 2025. Rapeseed and soy-based formulations lead within this category, owing to their high oleic acid content, NSF H1 certification eligibility for food-adjacent applications, and favorable CO2 footprint credentials for ESG-driven procurement decisions. The vegetable oils segment is expected to gain market share through the forecast period as performance-enhanced high-oleic varieties progressively reduce the oxidation stability gap with animal fat-based products.

By End Use Industry

Automotive leads with a 30.2% share (2025), followed by power generation (22.4%) and heavy equipment (16.8%). These three segments collectively account for over 69% of global bio-lubricant revenues, underpinned by OEM specification approvals, regulatory compliance mandates, and growing fleet sustainability commitments.

Regional Market Insights

Six major regions, North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, collectively constitute the global bio-lubricants market. North America and Europe together account for 65.7% of market revenues in 2025, reflecting their mature regulatory environments and established bio-lubricant adoption across industrial sectors.

North America leads at 37.1% (2025), driven by the USDA BioPreferred Program, which works on federal procurement toward bio-based products, and EPA VGP mandates for EAL adoption in commercial marine operations. The United States accounts for the largest single-country share, with Canada contributing through bio-lubricant adoption in oil sands operations and regulatory alignment with U.S. EPA standards.

Europe's 28.6% share reflects decades of proactive bio-lubricant policy. Germany, Sweden, and Austria are the largest per-capita consumers, with the German Blue Angel eco-certification recognized as the global benchmark for bio-lubricant performance and biodegradability standards.

Asia Pacific at 22.4% is the fastest-growing region. China's industrial bio-lubricant adoption is accelerating through its green manufacturing programs, while India's expanding wind energy capacity, targeting 140 GW by 2030, drives turbine oil demand.

Competitive Landscape

The global bio-lubricants market is moderately fragmented at the formulation level, with major integrated energy companies competing alongside specialized bio-lubricant producers and oleochemical manufacturers. Shell plc, TotalEnergies, and Fuchs SE collectively represent approximately significant share of global bio-lubricant trade value in 2025 through their branded product portfolios and OEM supply agreements. At the raw material level, the market is more concentrated, with a small number of oleochemical processors supplying bio-based ester base oils to the majority of branded formulators.

|

Company Name |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Shell plc |

Shell Naturelle |

Global Leader |

Circular feedstocks, premium EAL portfolio expansion |

|

TotalEnergies |

Biohydran |

Global Leader |

UCO-based formulations, food-grade Asia Pacific expansion |

|

Fuchs SE |

FUCHS Plantosyn |

Leader – Europe |

High-ester formulations, wind turbine oil specialization |

|

Castrol Limited |

Castrol Bio Range |

Established – Global |

OEM partnerships, EV drivetrain bio-fluid development |

|

Kluber Lubrication |

Klüberbio |

Leader – Industrial |

High-performance bio esters, food-grade and specialty markets |

|

Bechem |

Berusynth, Berugear |

Challenger – Europe |

Metalworking and food-grade bio-lubricant specialization |

|

Emery Oleochemicals |

DEHYLUB |

Leader – Oleochem. |

Ester base oil innovation, renewable supply chain leadership |

|

Kuwait Petroleum |

Q8 Holbein Bio / Q8 Chain Oil Bio |

Established – MEA |

Downstream diversification, bio-product portfolio expansion |

|

Cortec Corporation |

EcoLine |

Challenger – NA |

VCI corrosion protection, bio-based metalworking fluid innovation |

|

Polnox Corporation |

Polnox® 8020 |

Emerging |

Antioxidant additive technology for bio-lubricant performance |

Vertical integration, from feedstock sourcing and oleochemical processing through formulation, certification, and branded distribution is the primary competitive moat for leading companies. Shell and TotalEnergies have invested significantly in second-generation feedstock supply chains and digital traceability systems, reducing supply chain risk and achieving sustainability certification advantages over less-integrated competitors.

Key Company Profiles

Shell plc

Shell plc is one of the world's largest integrated energy companies and a leading producer of bio-lubricants under its Shell Naturelle brand family, serving industrial, marine, and automotive customers across more than 100 countries with a full range of EAL-certified biodegradable lubricant products.

- Recent Developments: In 2025, Shell announced its thermal fluid technology has helped to enable a significant breakthrough in battery electric vehicle (BEV) architecture.

- Strategic Focus: Circular feedstock integration, premium EAL portfolio expansion, digital traceability deployment for bio-based product certification, and strategic OEM first-fill approvals for EV and commercial vehicle applications.

TotalEnergies

TotalEnergies is a global multi-energy company and a leading bio-lubricant manufacturer with an extensive portfolio of biodegradable hydraulic fluids, food-grade lubricants, and industrial bio-lubricants sold under numerous recognized brands across over 50 countries.

- Recent Developments: In 2025, TotalEnergies launched a new portfolio of advanced bio-based lubricants formulated from renewable vegetable oils for supporting low-carbon industrial operations.

- Strategic Focus: Food-grade market penetration in Asia Pacific, UCO feedstock sourcing partnerships, second-generation bio-lubricant R&D, and circular economy product positioning aligned with TotalEnergies' 2050 net-zero commitment.

Fuchs SE

Fuchs SE is Germany's largest independent lubricant manufacturer and a leading European producer of bio-lubricants under the FUCHS Planto brand, with deep expertise in vegetable oil ester formulations for metalworking, industrial, and specialty applications.

- Recent Developments: In 2024, the first German production plant for EV/e-mobility solutions was officially opened at the FUCHS site in Kaiserslautern, European demand driven by wind energy and food processing sector adoption.

- Strategic Focus: Bio-ester formulation leadership in Europe, wind energy turbine oil specialization, ISO 15380 Type HEES compliance portfolio breadth, and industrial sector key account management for major European manufacturers.

Castrol Limited

Castrol Limited, a subsidiary of bp plc, is a global lubricant brand with growing bio-lubricant offerings targeting the automotive OEM and aftermarket segments, leveraging its distribution network across 150+ countries and established OEM technical service relationships.

- Recent Developments: Castrol launched Castrol BioTrans GB, a new lubricant for use in thrusters, some controllable pitch propeller (CPP) systems and deck machinery.

- Strategic Focus: EV-compatible bio-lubricant development and OEM first-fill approvals, bio-lubricant aftermarket channel expansion, and alignment with BP's net-zero transition and Scope 3 emission reduction strategy.

Market Concentration Analysis

The global bio-lubricants market exhibits moderate concentration at the branded product level. The top five players, Shell plc, TotalEnergies, Fuchs SE, Castrol Limited, and Kluber Lubrication, collectively account for approximately 30–35% of global bio-lubricant trade value in 2025. The remaining market is served by regional specialists, private-label producers, and vertically integrated oleochemical companies serving domestic markets in Asia, Latin America, and Eastern Europe.

At the raw material level, the market is more concentrated. A small number of oleochemical processing companies including Emery Oleochemicals, Croda International, and BASF, supply bio-based ester base oils to the majority of branded formulation companies globally. This upstream concentration creates supply chain risk that leading formulators are mitigating through long-term supply agreements, backward integration M&A, and second-source qualification programs.

Consolidation activity is accelerating in the bio-lubricants sector, with an estimated 6–8 M&A or strategic partnership transactions annually from 2024 through 2034. Major lubricant companies are acquiring specialized bio-lubricant and oleochemical producers to secure feedstock access, expand product portfolios, and capture sustainability premiums in regulated markets. Private equity interest in bio-based specialty chemical platforms is increasing, driven by ESG investment mandates, favorable EU and North American regulatory environments, and above-market segment growth rates in food-grade and EV-compatible bio-lubricant categories.

Investment & Growth Opportunities

Fastest Growing Segments

Food-grade bio-lubricants, wind turbine bio-oils, and EV-compatible bio-based drivetrain fluids, represent the highest-growth investment vectors through 2034.

Emerging Market Opportunities

Asia Pacific presents the largest emerging market investment opportunity in bio-lubricants. India's rapidly expanding wind energy sector, targeting 140 GW of wind capacity by 2030, requires significant volumes of biodegradable turbine hydraulic fluid, representing a multi-billion-dollar captive demand pool.

Technology & Innovation Investment Trends

- Enzymatic Transesterification: Enzymatic transesterification technology companies are attracting venture investment as cleaner, lower-energy bio-lubricant production pathways with reduced catalyst waste streams and improved product consistency, with pilot-scale plants operating in the Netherlands and Belgium.

- Algae-Derived Lipid Platforms: Algae-derived lipid production platforms for high-purity ester base oil synthesis are in early commercialization, with pilot facilities in the Netherlands and Singapore attracting agri-food and energy corporate venture capital seeking second-generation feedstock security.

- Digital Lubrication Monitoring: Digital lubrication monitoring platforms, combining IoT sensors with AI-driven predictive maintenance algorithms are generating B2B SaaS investment opportunities across manufacturing, power generation, and transportation sectors, enabling 15–25% consumption reduction benefits.

- Carbon-Intensity Certification: Carbon-intensity-certified bio-lubricants with verified Scope 3 emission reduction credentials are commanding 10–20% price premiums in regulated procurement contexts, creating certification services, software, and advisory investment opportunities aligned with corporate net-zero commitments.

Future Market Outlook (2026-2034)

The global bio-lubricants market is poised for steady, regulation-backed expansion through 2034. Technological disruption will define competitive dynamics over the next decade. Producers achieving high-oleic feedstock security, enzymatic processing cost advantages, and digital supply chain traceability will command durable competitive positions. The transition to electric vehicle drivetrains will restructure conventional automotive lubricant demand while simultaneously creating new bio-lubricant application opportunities in thermal management, dielectric fluids, and e-axle lubrication, segments where bio-based chemistry offers inherent performance advantages.

Companies investing now in regulatory-compliant formulations, second-generation feedstock supply chains, digital performance certification, and EV-specific product development will be best positioned to capture the next decade of market value creation in the bio-lubricants industry.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 140 industry participants in 2024–2025, comprising bio-lubricant manufacturers, oleochemical processors, end-user procurement managers, equipment OEM technical specialists, regulatory officials, and distribution channel executives across North America, Europe, and Asia Pacific. Interviews were conducted across China, India, Germany, the United States, the United Kingdom, France, and Brazil to ensure regional representation in qualitative market intelligence.

Secondary Research

Secondary research encompassed a comprehensive review of USDA BioPreferred Program databases, EPA regulatory filings, EU Ecolabel certification records, company annual reports and sustainability disclosures, trade publications (Lubes'N'Greaves, NLGI Spokesman, Tribology & Lubrication Technology), ASTM and ISO standard databases, and industry associations including ELGI (European Lubricating Grease Institute) and STLE (Society of Tribologists and Lubrication Engineers). Over 250 primary statistical sources were triangulated for market size validation across all segments and regions.

Forecasting Models

Market size estimations were derived using a bottom-up application volume model combined with top-down value chain analysis, incorporating base oil price trajectories, regulatory adoption rate assumptions by region, end-use industry growth projections, and competitive dynamics modeling. Scenario analysis across base, optimistic, and conservative cases was conducted to account for feedstock price volatility, regulatory implementation pace uncertainty, and macroeconomic risk factors. Final market estimates were validated against proprietary trade flow data and company revenue disclosures.

Bio-Lubricants Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Base Oil Types Covered | Vegetable Oils, Animal Fats |

| Applications Covered | Hydraulic Fluids, Metalworking Fluids, Chainsaw Oils, Mold Release Agents, Two-Cycle Engine Oils, Gear Oils and Greases, Others |

| End Use Industries Covered | Power Generation, Automotive, Heavy Equipment, Food & Beverage, Metallurgy & Metalworking, Chemical Manufacturing, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Shell plc, TotalEnergies, Fuchs SE, Castrol Limited, Kluber Lubrication, Bechem, Emery Oleochemicals, Kuwait Petroleum, Cortec Corporation, Polnox Corporation |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the bio-lubricants market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global bio-lubricants market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the bio-lubricants industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Bio-lubricants Market Report

The global bio-lubricants market was valued at USD 2.50 Billion in 2025 and is projected to reach USD 3.33 Billion by 2034.

The market is forecast to grow at a CAGR of 3.1% during 2026-2034, driven by environmental regulations, EV-compatible bio-fluid development, and expanding industrial sustainability mandates globally.

Animal fats dominate at 54.3% in 2025, valued for high viscosity index and thermal stability in heavy-duty industrial gear systems, turbines, and hydraulic applications across global markets.

Automotive leads with 30.2% in 2025, driven by engine oil, transmission fluid, and emerging EV drivetrain bio-lubricant applications. OEM spec approvals from Volvo and Scania accelerate fleet adoption.

North America leads with 37.1% in 2025, driven by USDA BioPreferred mandates, EPA VGP requirements, and strong commercial vehicle fleet adoption of certified environmentally acceptable lubricants.

Key drivers include EPA and EU environmental regulations, OEM bio-lubricant approvals, falling feedstock costs, improved bio-lubricant performance characteristics, and corporate ESG and net-zero commitments.

Asia Pacific is the fastest growing region, driven by China's green manufacturing programs, India's 140 GW wind energy target by 2030, and tightening industrial environmental standards across Southeast Asia.

Leading companies include Bechem, Castrol Limited, Cortec Corporation, Emery Oleochemicals, Fuchs SE, Kluber Lubrication, Kuwait Petroleum, Polnox Corporation, Shell plc, and TotalEnergies.

Key opportunities include food-grade bio-lubricants, EV-compatible bio-fluids, wind turbine oils, enzymatic esterification technology, and digital lubrication monitoring platforms in Asia Pacific and Latin America.

Key challenges include 20–40% price premium versus mineral lubricants, thermal stability limitations, multi-certification complexity, feedstock price volatility, and competition from Group III and PAO synthetic lubricants.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade