Biochar Market Size, Share, and Trends and Forecast by Feedstock Type, Technology Type, Product Form, Application, and Region, 2026-2034

Global Biochar Market Size, Share, Trends & Forecast (2026-2034)

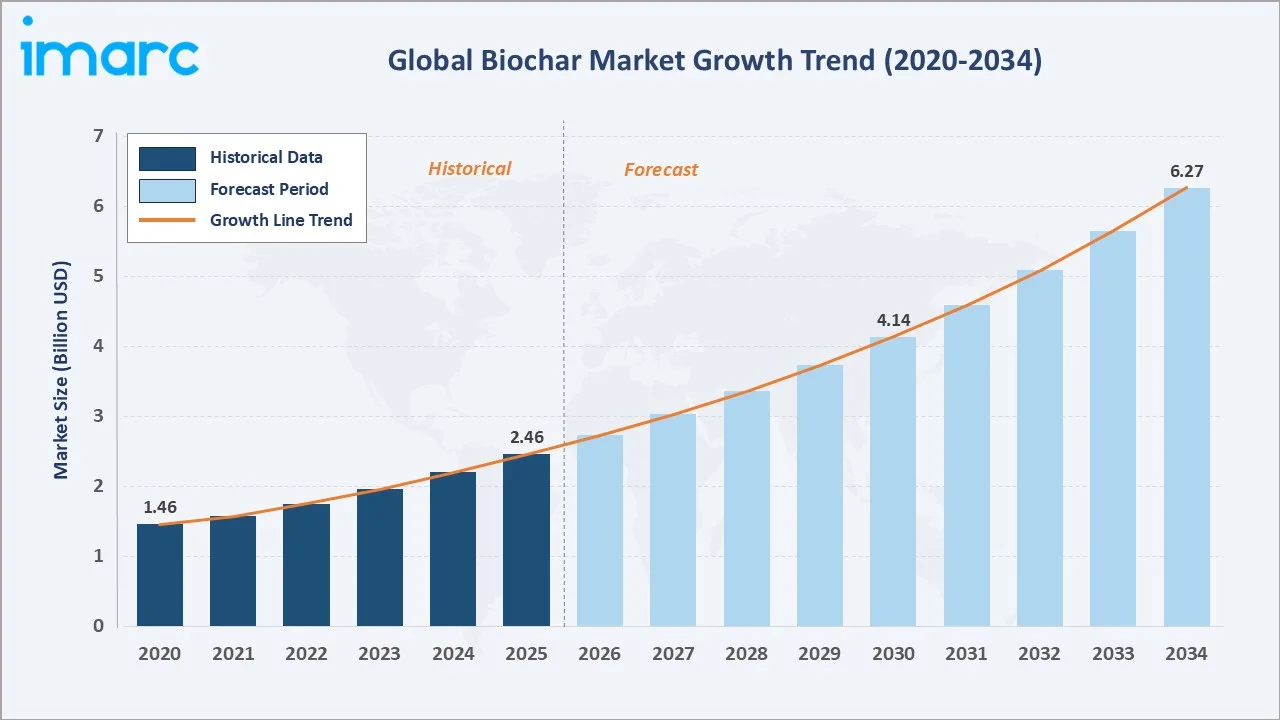

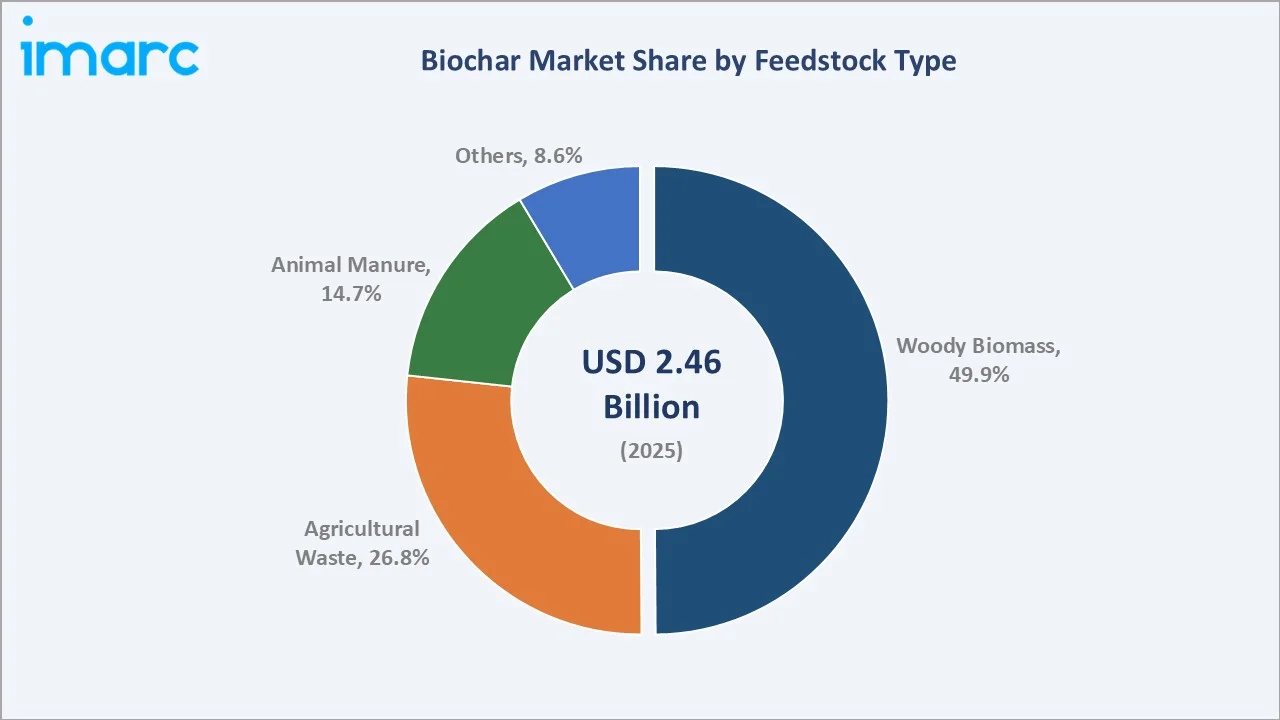

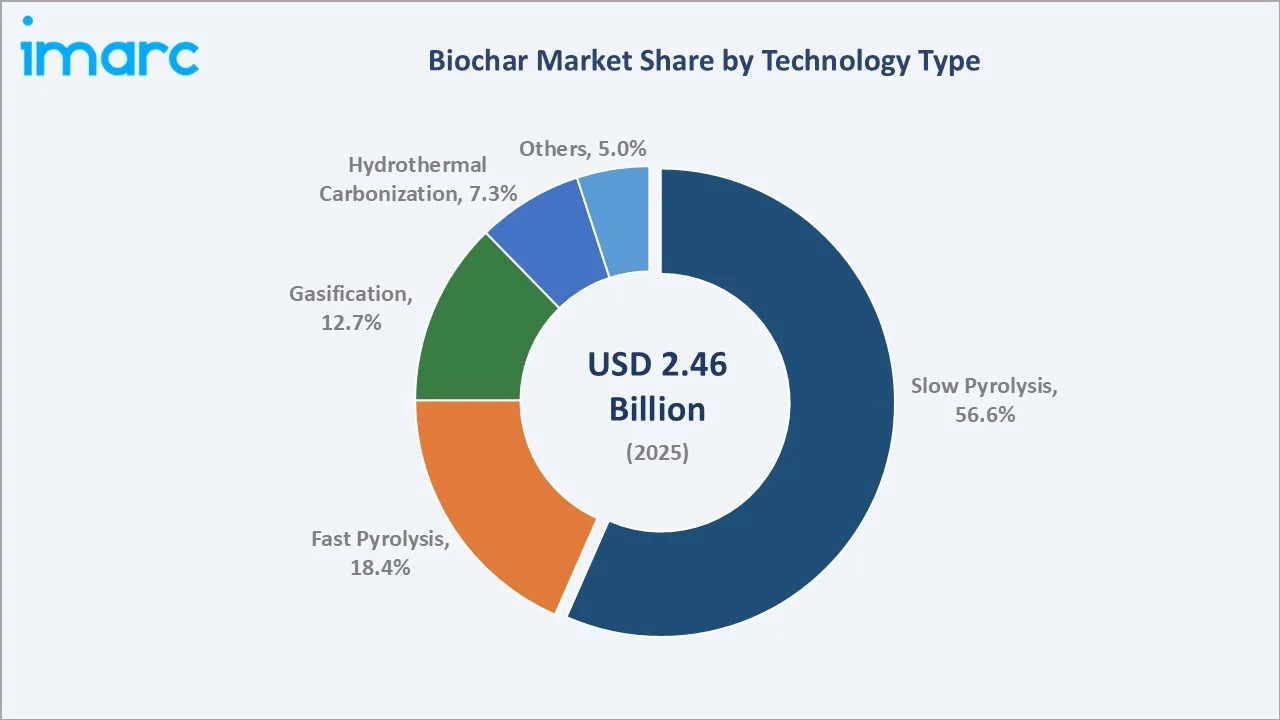

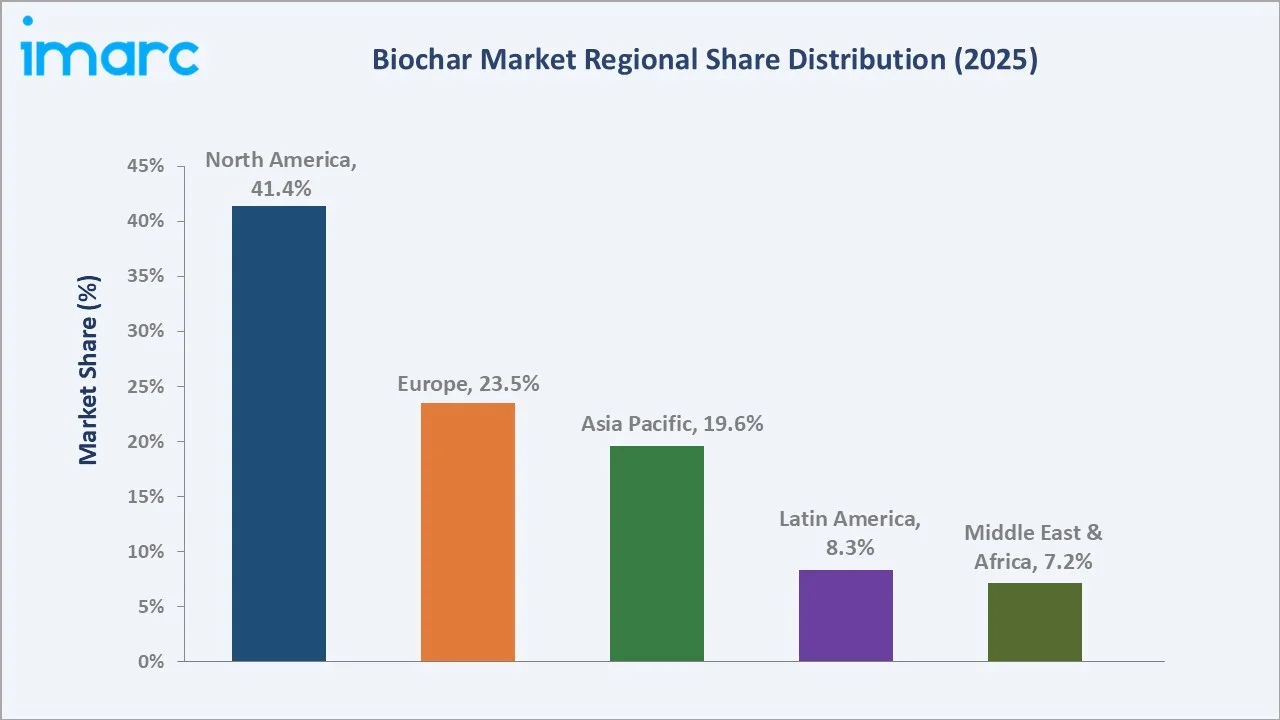

The global biochar market size was valued at USD 2.46 Billion in 2025 and is projected to reach USD 6.27 Billion by 2034, at a CAGR of 10.95% during 2026-2034. Rising demand for sustainable agriculture, expanding carbon credit programs, growing soil amendment applications, and mounting regulatory support for carbon sequestration are collectively driving biochar market growth. Woody Biomass dominates with a 49.9% share in 2025, while Slow Pyrolysis accounts for 56.6% of global production. North America leads regional demand with a 41.4% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.46 Billion |

|

Forecast Market Size (2034) |

USD 6.27 Billion |

|

CAGR (2026-2034) |

10.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (41.4% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Feedstock Type |

Woody Biomass (49.9%, 2025) |

|

Leading Technology Type |

Slow Pyrolysis (56.6%, 2025) |

The chart below illustrates biochar market growth from 2020-2034, with policy-driven adoption accelerating recent history and carbon-removal credits supporting forecasts.

To get more information on this market, Request Sample

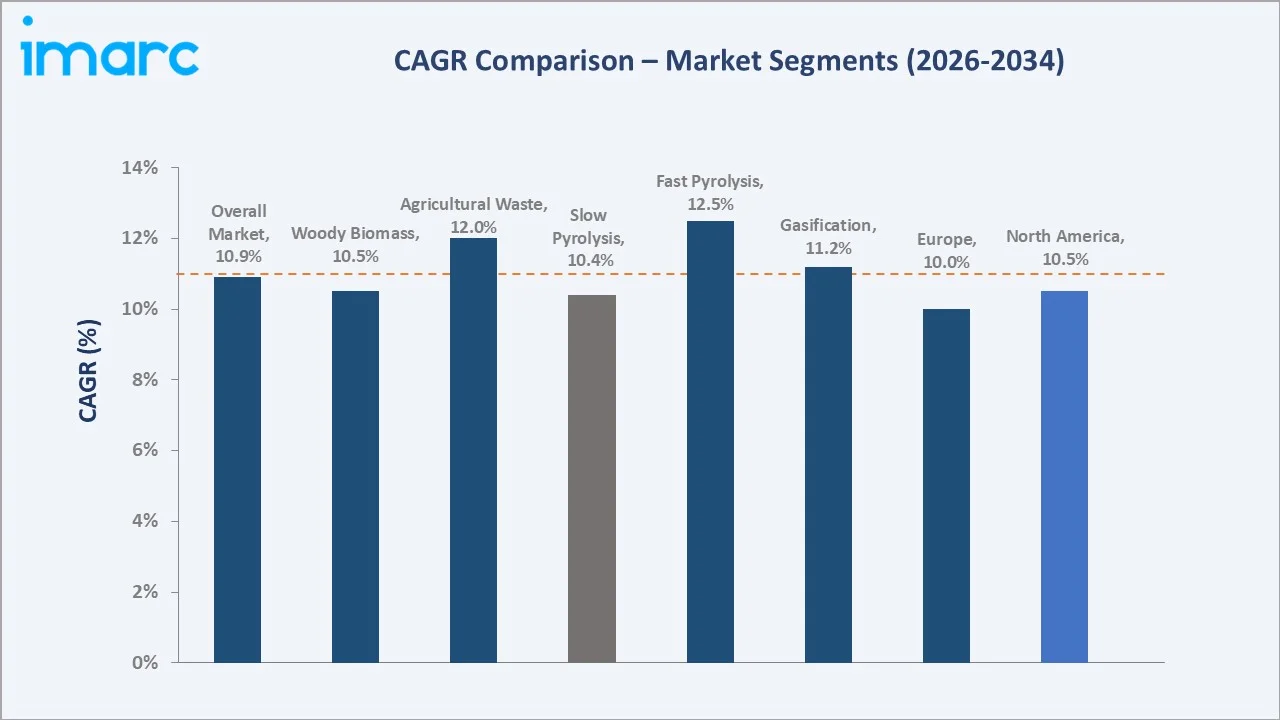

CAGR analysis identifies Slow Pyrolysis and Woody Biomass as the fastest-scaling segments in the global biochar market through 2034.

Executive Summary

The global biochar market is transforming due to climate-driven carbon sequestration demand, regenerative agriculture momentum, and circular economy mandates. Valued at USD 2.46 Billion in 2025, it is projected to reach USD 6.27 Billion by 2034, at a 10.95% CAGR. Rising awareness around soil health, water retention, and crop yield improvement is accelerating broad farmer and corporate adoption.

Woody Biomass leads with a 49.9% share in 2025, supported by abundant forestry residues and high carbon-content output. Slow pyrolysis holds 56.6% of global production, reflecting cost efficiency and process maturity. Key trends include carbon-credit monetization, livestock-feed integration, smart-soil applications, and use of biochar in green construction materials.

North America leads the global biochar market with a 41.4% share in 2025, supported by U.S. carbon-removal incentives, strong soil-amendment demand, and Canadian forestry feedstock availability. Europe holds 23.5%, driven by EU carbon-farming policy and pyrolysis technology leadership. Asia Pacific accounts for 19.6% and is the fastest-growing region, fueled by agricultural intensity, paddy-residue management mandates, and government soil-quality initiatives.

Key Market Insights

|

Insight |

Data |

|

Largest Feedstock Segment |

Woody Biomass - 49.9% share (2025) |

|

Second Feedstock Segment |

Agricultural Waste - 26.8% share (2025) |

|

Leading Technology Type |

Slow Pyrolysis - 56.6% share (2025) |

|

Leading Region |

North America - 41.4% (2025) |

|

Second Region |

Europe - 23.5% (2025) |

|

Top Companies |

Pacific Biochar Benefit Corporation, Carbon Gold Ltd, and Phoenix Energy |

Key Analytical Observations Supporting The Above Data:

- Woody biomass's 49.9% dominance in 2025 reflects high carbon yield per ton of feedstock, supported by a steady supply of forestry residues across North America and Europe.

- Agricultural waste at 26.8% in 2025 is rising rapidly, underpinned by paddy-straw burning bans in India, corn-stover utilization in the U.S., and EU farm-residue valorization programs.

- Slow pyrolysis's 56.6% share in 2025 reflects its dominance, driven by higher biochar yield and strong carbon stability, making it the most widely adopted method for efficient carbon sequestration and scalable production.

- North America's 41.4% global lead in 2025 reflects strong regional momentum, supported by large-scale U.S. funding programs exceeding USD 3.1 billion that promote climate-smart agriculture and carbon sequestration initiatives.

- Asia Pacific's position as the fastest-growing region is driven by India's National Mission on Sustainable Agriculture, China's soil-pollution remediation goals, and Australia's expanding agricultural carbon-credit framework.

- Cool Planet, Pacific Biochar Benefit Corporation, Carbon Gold, and Phoenix Energy are key industry players, actively expanding production capacity and advancing biochar commercialization, though specific cumulative investment.

Global Biochar Market Overview

Biochar is a stable, carbon-rich solid produced through the thermal decomposition of organic biomass under low-oxygen conditions. The ecosystem includes feedstock suppliers, pyrolysis equipment manufacturers, biochar producers, distribution partners, and end-user industries spanning agriculture, livestock, environmental remediation, and construction.

The market spans applications such as soil amendment, livestock feed, water treatment, air purification, construction materials, and carbon removal. Growth is driven by sustainability initiatives, climate-smart agriculture policies, expanding voluntary carbon markets, and increasing recognition of biochar’s multi-functional environmental benefits.

Market Dynamics

To evaluate market opportunities, Request Sample

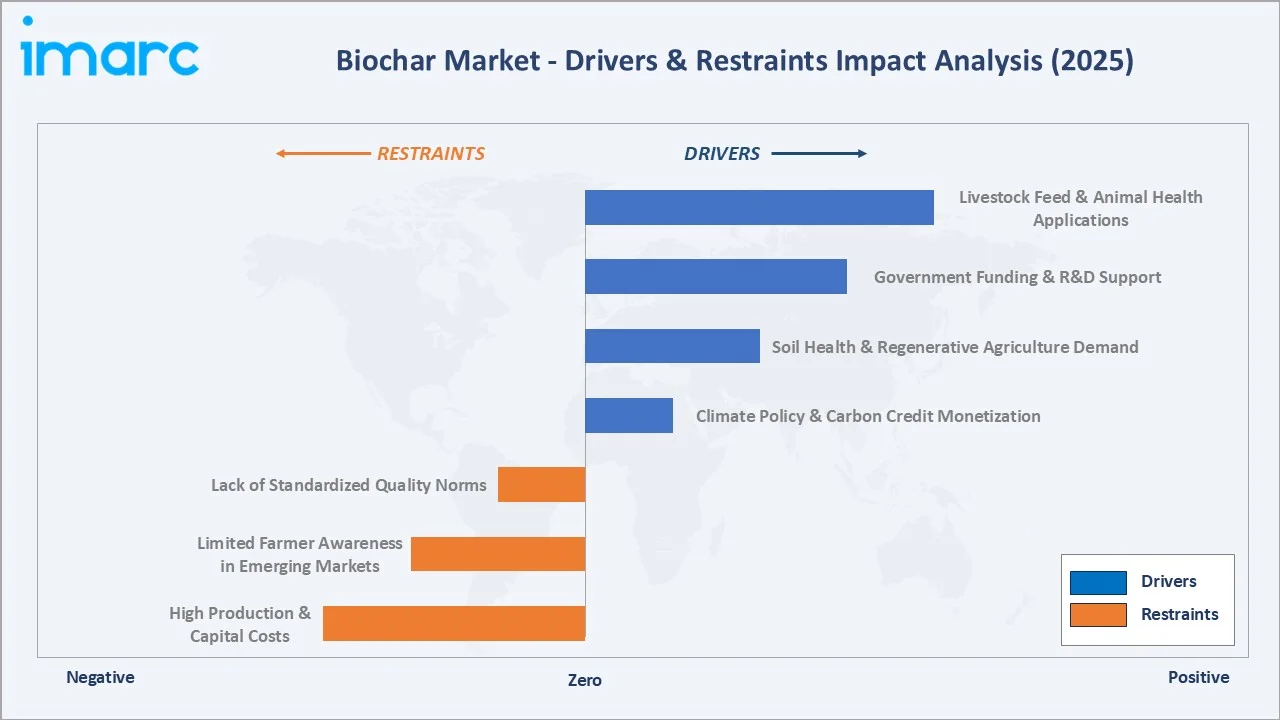

Market Drivers

- Climate Policy and Carbon Credit Monetization: Frameworks such as the Section 45Q tax credit and the EU’s Carbon Removal Certification Framework support carbon removal solutions, including biochar. Carbon removal credits in voluntary markets vary widely, often ranging roughly between USD 100–200 per ton depending on quality and certification.

- Soil Health and Regenerative Agriculture Demand: Regenerative agriculture is expanding rapidly, with biochar improving soil moisture retention, boosting microbial activity, and increasing nutrient efficiency, offering measurable productivity gains for farmers.

- Government Funding and R&D Support: USDA's Climate-Smart Commodities program and EU Horizon Europe allocations have directed significant funding toward biochar research, pyrolysis demonstration plants, and field-scale agronomic trials.

- Livestock Feed and Animal Health Applications: Biochar inclusion at 0.5–1.0% in livestock feed has shown methane reduction potential and improves gut health, enabling expansion across European and U.S. dairy and poultry production systems.

Market Restraints

- High Production and Capital Costs: Biochar production via pyrolysis requires significant capital investment, and costs vary widely depending on scale, feedstock, and technology, limiting adoption in price-sensitive markets.

- Limited Farmer Awareness in Emerging Markets: Awareness gaps around biochar's agronomic and economic benefits remain significant across South Asia and Africa, slowing rural penetration despite favorable feedstock availability.

- Lack of Standardized Quality Norms: Variability in feedstocks, pyrolysis temperature, and ash content creates inconsistent product quality, complicating large-scale procurement and regulatory acceptance across multiple application categories.

Market Opportunities

- Voluntary Carbon Market Expansion: Voluntary carbon markets are expected to grow significantly, with biochar gaining traction due to its long-term carbon storage potential, supporting premium carbon removal credits.

- Biochar in Construction and Cement Composites: Biochar is being explored as a sustainable additive in concrete and building materials to reduce embodied carbon, though reduction levels vary by formulation and project scale.

- Industrial Wastewater Treatment Applications: Biochar's adsorption capacity for heavy metals and organic contaminants is supporting adoption in industrial water treatment, particularly in China, Japan, and Northern Europe.

Market Challenges

- Feedstock Supply Volatility: Seasonality of agricultural residues and competition from biofuel and bioenergy sectors create feedstock price volatility, affecting plant utilization rates and cost predictability for biochar producers.

- Verification and MRV Costs in Carbon Markets: Measurement, reporting, and verification (MRV) for biochar carbon credits can be complex and costly, creating financial and administrative burdens especially for small producers though exact per-ton costs vary by standard and project.

- Limited Logistics and Distribution Infrastructure: Low bulk density of biochar increases transportation costs per ton-mile, restricting profitable distribution radius and limiting market reach beyond regional clusters.

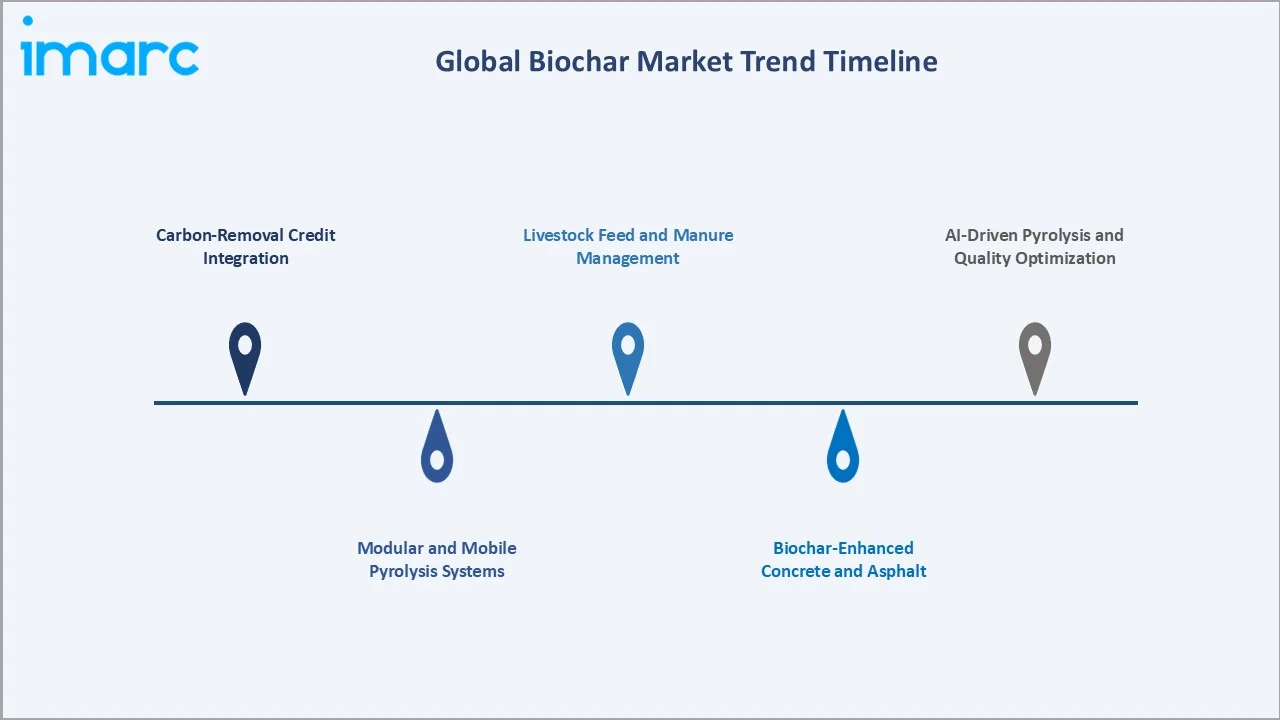

Emerging Market Trends

1. Carbon-Removal Credit Integration

Biochar is emerging as a key durable carbon removal solution, with companies such as Microsoft, JPMorgan Chase, and Frontier actively procuring biochar-based carbon credits to meet net-zero commitments.

2. Modular and Mobile Pyrolysis Systems

Compact, mobile pyrolysis units are gaining adoption, allowing farmers and forestry operators to convert residues on-site, reducing logistics costs and decentralizing production across rural geographies worldwide.

3. Biochar-Enhanced Concrete and Asphalt

Construction-sector adoption is expanding, with biochar serving as a carbon-storing additive in cement, mortar, and asphalt mixes, supporting net-zero building targets and circular construction materials strategies.

4. Livestock Feed and Manure Management

Biochar use in animal feed and bedding is improving methane reduction, ammonia control, and manure-nutrient retention, increasingly adopted across European dairy farms and U.S. poultry operations.

5. AI-Driven Pyrolysis and Quality Optimization

AI and IoT technologies are being deployed to optimize pyrolysis parameters such as temperature, residence time, and feedstock mix, enhancing process efficiency and ensuring more consistent biochar quality at scale.

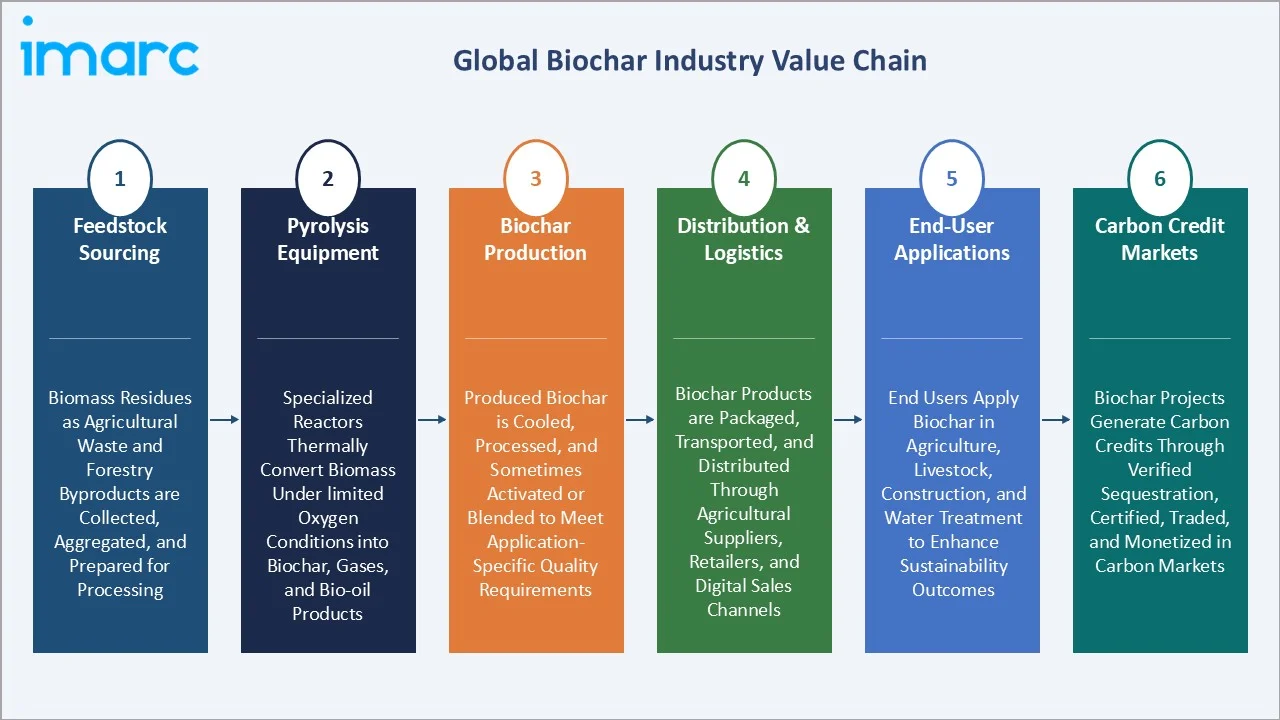

Industry Value Chain Analysis

The biochar value chain spans six stages, from agricultural and forestry inputs to end-consumer applications, each involving distinct competitive dynamics, margin structures, and technology dependencies.

|

Stage |

Key Players / Examples |

|

Feedstock Sourcing |

Biomass residues as agricultural waste and forestry byproducts are collected, aggregated, and prepared for processing |

|

Pyrolysis Equipment |

Specialized reactors thermally convert biomass under limited oxygen conditions into biochar, gases, and bio-oil products |

|

Biochar Production |

Produced biochar is cooled, processed, and sometimes activated or blended to meet application-specific quality requirements |

|

Distribution & Logistics |

Biochar products are packaged, transported, and distributed through agricultural suppliers, retailers, and digital sales channels |

|

End-User Applications |

End users apply biochar in agriculture, livestock, construction, and water treatment to enhance sustainability outcomes |

|

Carbon Credit Markets |

Biochar projects generate carbon credits through verified sequestration, certified, traded, and monetized in carbon markets |

Tier-1 producers integrate feedstock sourcing, pyrolysis operations, and credit certification, capturing the highest value through carbon-removal sales priced at USD 100-200 per ton in 2024 markets.

Technology Landscape in the Biochar Industry

Slow Pyrolysis Technology

Slow pyrolysis is the most widely adopted method for biochar production, offering high carbon retention and stable operation. It typically operates at moderate temperatures and is well-suited for woody biomass and decentralized, small-to-medium scale systems.

Fast Pyrolysis and Gasification

Fast pyrolysis and gasification prioritize production of bio-oil and syngas, with biochar generated as a secondary by-product in smaller quantities. These technologies are often used in energy-focused and waste-to-energy applications.

Hydrothermal Carbonization (HTC)

HTC converts wet biomass such as sludge and manure into hydrochar under moderate temperature and pressure conditions, enabling efficient processing of high-moisture feedstocks unsuitable for conventional pyrolysis technologies in municipal and industrial applications.

Smart Process Control and Digital MRV

IoT sensors, AI process tuning, and blockchain-based MRV platforms are improving plant efficiency and credit traceability. Companies like CarbonFuture and Puro.earth use digital MRV for carbon-credit certification.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Feedstock Type | Woody Biomass | 49.9% | 2025 |

| Technology Type | Slow Pyrolysis | 56.6% | 2025 |

| Product Form | Fine Powder | 41.3% | 2025 |

| Application | Farming | 41.9% | 2025 |

| Region | North America | 41.4% | 2025 |

.webp)

By Feedstock Type

Woody biomass holds a 49.9% share in 2025, driven by abundant forestry residues, sawmill byproducts, and high carbon yield. Producers across Canada, the U.S., and Scandinavia rely heavily on this feedstock for premium-grade biochar suitable for soil and credit applications.

To access detailed market analysis, Request Sample

Agricultural waste accounts for 26.8% in 2025, supported by paddy straw, corn stover, and sugarcane bagasse, with India's residue-burning bans and U.S. corn-belt valorization programs accelerating commercial adoption through 2034. Animal Manure represents 14.7% in 2025, valued for nutrient-rich biochar used in dairy and poultry operations. The Others segment holds 8.6%, including municipal organic waste and food processing residues.

By Technology Type

Slow pyrolysis leads with a 56.6% share in 2025, favored for high carbon retention, lower capital intensity, and operational simplicity. Most certified biochar producers globally rely on slow pyrolysis platforms for premium agricultural and credit-grade output.

Fast pyrolysis accounts for 18.4% in 2025, used in integrated plants targeting bio-oil and biochar co-products. Gasification holds 12.7%, deployed in waste-to-energy systems with smaller biochar yields but stronger thermal cogeneration economics. Hydrothermal carbonization holds 7.3% in 2025, suited to wet feedstocks. Others represent 5.0%, including microwave-assisted pyrolysis and emerging plasma-based carbonization platforms under pilot deployment globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

41.4% |

USDA Climate-Smart Commodities, soil amendment demand, forestry feedstock |

|

Europe |

23.5% |

EU Carbon Removal Certification Framework, regenerative farming, pyrolysis tech leadership |

|

Asia Pacific |

19.6% |

India residue-burn bans, China soil remediation goals, Australian carbon farming initiatives |

|

Latin America |

8.3% |

Brazil sugarcane bagasse, Argentina soybean residue, expanding regenerative coffee farming |

|

Middle East & Africa |

7.2% |

Date palm residue projects, South Africa soil restoration, GCC sustainability mandates |

North America commands a 41.4% in 2025, driven by U.S. Inflation Reduction Act incentives, Canadian forestry feedstock, and large-scale biochar removal-credit purchasing led by Microsoft, Frontier, and Stripe.

Europe holds 23.5% in 2025, anchored by Germany, the UK, Sweden, and Finland, where pyrolysis technology providers and carbon-farming regulations create strong policy pull. Asia Pacific at 19.6% is the fastest-growing region, with India, China, and Australia investing in farm-residue valorization, soil restoration, and emerging carbon-credit frameworks supporting incremental growth through 2034.

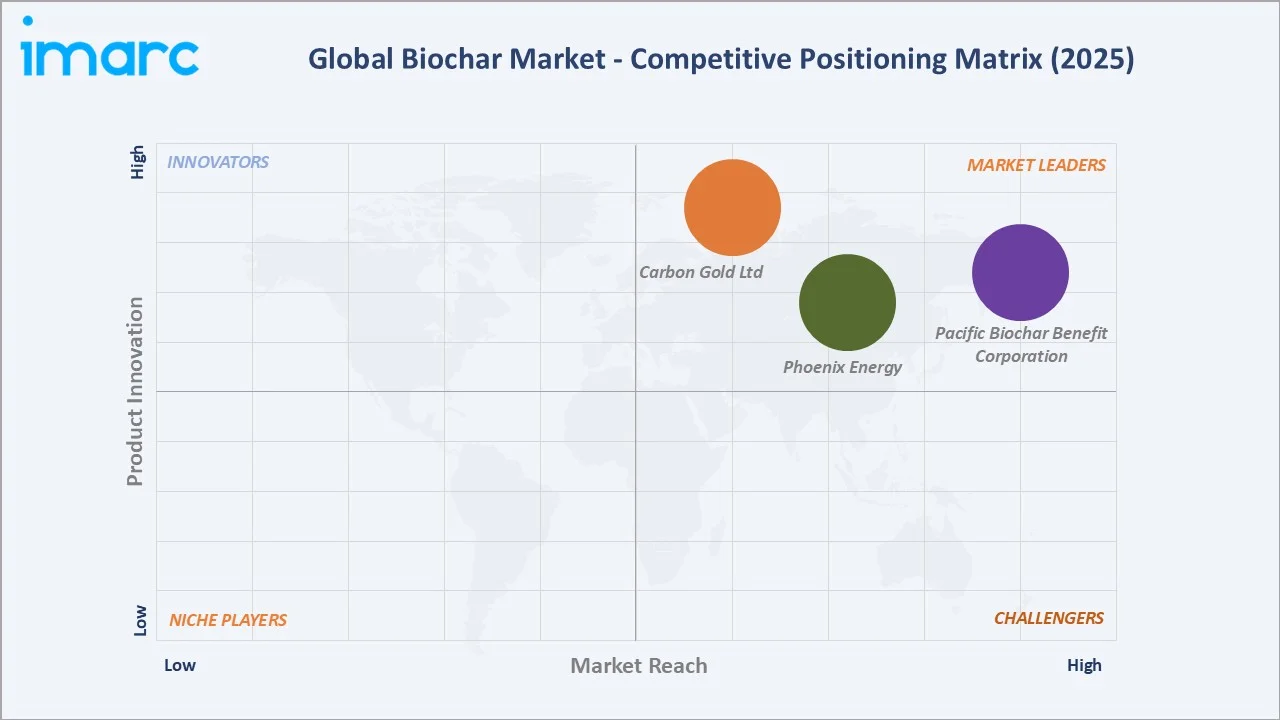

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Pacific Biochar Benefit Corporation |

Pacific Biochar |

Leader |

Forestry residue conversion, California carbon-credit issuance |

|

Carbon Gold Ltd |

GroChar |

Leader |

Premium horticulture and arboriculture biochar, UK and EU presence |

|

Phoenix Energy |

Earthworks Biochar |

Leader |

Biomass-to-energy with biochar co-products |

The biochar market is fragmented, with regional specialists operating alongside global pyrolysis equipment providers. Companies such as Pacific Biochar Benefit Corporation and Carbon Gold Ltd are expanding production capacity to address growing demand, particularly from carbon removal and sustainability-driven applications.

Key Company Profiles

Pacific Biochar Benefit Corporation

Pacific Biochar Benefit Corporation is a U.S.-based producer headquartered in California, specializing in forestry-residue biochar and carbon removal solutions. The company collaborates with biomass power facilities to convert waste into biochar for agriculture and verified carbon credit markets.

- Product & Service Portfolio: Pacific Biochar supplies bulk and specialty biochar for agriculture, including vineyard applications, and generates carbon removal credits through platforms such as Puro.earth.

- Recent Developments: Pacific Biochar partnered with Hat Creek Bioenergy in Burney, California, to develop a bioenergy facility converting forest thinnings into renewable electricity and biochar. The project is producing 5,000+ tonnes of biochar annually and delivering 15,000+ tonnes of CO₂ removal.

- Strategic Focus: Pacific Biochar focuses on forestry-residue valorization, commercial biochar distribution across California agriculture, and scaling certified carbon-removal credit issuance to corporate sustainability buyers.

Carbon Gold Ltd

Carbon Gold Ltd is a UK-based biochar producer headquartered in Bristol, focused on soil enhancement solutions for horticulture, landscaping, and agriculture. Through its GroChar range, the company serves professional growers, retailers, and sustainability-driven markets across the UK and Europe.

- Product & Service Portfolio: Biochar-based products including GroChar soil improvers, peat-free compost blends, tree and turf conditioners, and customized biochar formulations for horticulture, landscaping, and agricultural applications.

- Recent Developments: In 2024, Carbon Gold Ltd partnered with Westland Horticulture to expand distribution of enriched biochar products into mainstream garden retail channels, while also launching peat-free biochar blends aligned with sustainable gardening demand.

- Strategic Focus: Carbon Gold focuses on premium horticulture biochar, professional grower relationships, regenerative gardening retail growth, and European carbon-farming compliance positioning under the EU CRCF framework.

Phoenix Energy

Phoenix Energy is a U.S.-based renewable energy company headquartered in California, specializing in biomass gasification and biochar production. It develops community-scale BECCS facilities that convert forestry and agricultural waste into renewable energy, biochar, and carbon removal solutions.

- Product & Service Portfolio: Phoenix Energy produces and markets biochar (via Earthworks Biochar), renewable electricity, syngas-based energy, and carbon credits by converting biomass waste through gasification and pyrolysis technologies.

- Recent Developments: In 2024, Phoenix Energy partnered with Carbonfuture to scale its biochar-based carbon removal business, supporting financing and development of multiple facilities, with a second plant targeted for completion by 2026 and plans for 50 plants over the next decade.

- Strategic Focus: Phoenix Energy focuses on premium agronomic biochar, expanded distribution networks, university-partnered field trials, and entry into voluntary carbon-removal markets through certified product traceability.

Market Concentration Analysis

The global biochar market is moderately fragmented, with the top 5 players collectively accounting for approximately 20-25% of global revenue in 2025. Regional specialists, equipment providers, and pyrolysis technology firms create a diverse competitive base.

Fragmentation is highest in Asia Pacific and Latin America, where small-scale on-farm pyrolysis units and cooperative producers proliferate. North America and Europe show stronger consolidation, supported by certified producers servicing carbon-credit and large-scale agricultural buyers.

Consolidation trends are accelerating through capacity expansions, acquisitions of pyrolysis technology firms, and corporate offtake agreements. Microsoft's multi-year biochar offtake commitments and rising private-equity interest in scaling producers signal a shift toward industrial-scale market structure through 2030.

Investment & Growth Opportunities

Fastest-Growing Segments

Carbon-removal credits are a key growth area, with biochar credits commonly priced around USD 100–200 per tonne in voluntary markets. Buyers such as Microsoft and Frontier are driving demand. Biochar use in construction is also emerging, with pilot projects showing reduced embodied carbon.

Emerging Market Expansion

Asia Pacific represents the most strategic emerging opportunity, with India's paddy-residue management, China's soil-remediation programs, and Australia's carbon-farming framework creating multi-year demand expansion through 2034 across diverse feedstock and application categories.

Venture & Strategic Investment Trends

Investment in biochar is expanding through climate-tech funding and advance market commitments. Companies like Stripe, Shopify, and Microsoft support carbon removal purchases, accelerating commercialization and scaling of biochar technologies globally.

Future Market Outlook (2026-2034)

The global biochar market forecast projects sustained value expansion from USD 2.46 Billion in 2025 to USD 6.27 Billion by 2034 at a CAGR of 10.95%, representing a value increase of nearly USD 3.81 Billion through the forecast period. Growth will be driven by carbon-credit market scaling, regenerative agriculture adoption, construction-sector integration, and policy-led farmer incentives.

Three transformational trends will reshape biochar through 2034. Carbon-removal credits will become a primary revenue stream alongside physical biochar sales, while modular pyrolysis units will decentralize production. Additionally, biochar-enhanced construction materials will emerge as a major application category, supporting industry-wide value chain expansion.

By 2034, biochar is expected to evolve from a niche soil amendment into a mainstream climate-tech, agriculture, and construction input. Producers investing in MRV technology, certified credits, and scalable pyrolysis platforms are positioned to capture premium opportunities across global sustainability markets.

Research Methodology

Primary Research

Primary research encompassed structured interviews and surveys conducted in 2024-2025 with biochar industry stakeholders including senior executives at Tier-1 producers, pyrolysis equipment manufacturers, agricultural distributors, carbon-credit registry administrators, regenerative-farming consultants, and procurement leaders at corporate carbon-credit buyers.

Secondary Research

Secondary sources include company annual reports (Pacific Biochar Benefit Corporation, Carbon Gold Ltd, Phoenix Energy, and others), trade publications (International Biochar Initiative, European Biochar Industry Consortium), government program data (USDA Climate-Smart Commodities, EU CRCF), carbon-credit registry data (Verra, Puro.earth), and academic literature on pyrolysis and soil science.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth, agricultural production trends, carbon-credit pricing, policy adoption timelines, and scenario analysis under base, optimistic, and conservative assumptions.

Biochar Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Feedstock Types Covered | Woody Biomass, Agricultural Waste, Animal Manure, Others |

| Technology Types Covered | Slow Pyrolysis, Fast Pyrolysis, Gasification, Hydrothermal Carbonization, Others |

| Product Forms Covered | Coarse and Fine Chips, Fine Powder, Pellets, Granules and Prills, Liquid Suspension |

| Applications Covered | Farming, Gardening, Livestock Feed, Soil, Water and Air Treatment, Others |

| Regions Covered | Asia Pacific, Europe, North America, Middle East and Africa, Latin America |

| Companies Covered | Pacific Biochar Benefit Corporation, Carbon Gold Ltd, Phoenix Energy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative biochar market analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global biochar market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the biochar industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Biochar Market Report

The global biochar market was valued at USD 2.46 Billion in 2025, driven by rising soil-amendment demand, carbon-credit growth, and expanding adoption across regenerative agriculture worldwide.

The market is projected to reach USD 6.27 Billion by 2034, growing at a CAGR of 10.95% during 2026-2034, supported by carbon credits, climate policy, and pyrolysis technology scaling.

Woody Biomass leads with a 49.9% share in 2025, driven by abundant forestry residues, high carbon yield, and superior performance in soil amendment and carbon-credit applications worldwide.

Slow Pyrolysis commands a 56.6% share in 2025, favored for high carbon retention, operational simplicity, lower capital intensity, and consistent biochar quality across small and large-scale plants.

North America leads with a 41.4% share in 2025, anchored by USDA programs, Section 45Q credits, robust forestry feedstock, and strong corporate carbon-removal procurement activity globally.

Key drivers include carbon-credit monetization, soil health initiatives, government funding, regenerative agriculture, livestock feed adoption, and biochar's emerging role in construction-material decarbonization.

Asia Pacific is the fastest-growing region, fueled by India's residue-burning bans, China's soil-remediation goals, and Australia's expanding carbon-farming policies through the 2026-2034 forecast period.

Leading companies include Pacific Biochar Benefit Corporation, Carbon Gold Ltd, and Phoenix Energy, among major global players.

Agricultural Waste held a 26.8% share in 2025, supported by paddy straw, corn stover, and bagasse valorization, particularly across India, the United States, Brazil, and Southeast Asia.

Carbon-removal credits priced at USD 100-200 per ton in 2024 are creating a major revenue stream, with corporate buyers like Microsoft purchasing hundreds of thousands of tons of biochar credits.

Modular pyrolysis units, AI-driven process control, IoT monitoring, and blockchain-based MRV platforms are enhancing yield, traceability, and certification efficiency across global biochar production operations.

Soil amendment in farming and gardening represents the largest application globally, supported by improvements in soil moisture retention, microbial activity, nutrient efficiency, and crop yields across diverse agricultural geographies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)