Bioethanol Market Size, Share, Trends and Forecast by Type, Fuel Blend, Generation, End Use Industry, and Region, 2026-2034

Global Bioethanol Market Size, Share, Trends & Forecast (2026-2034)

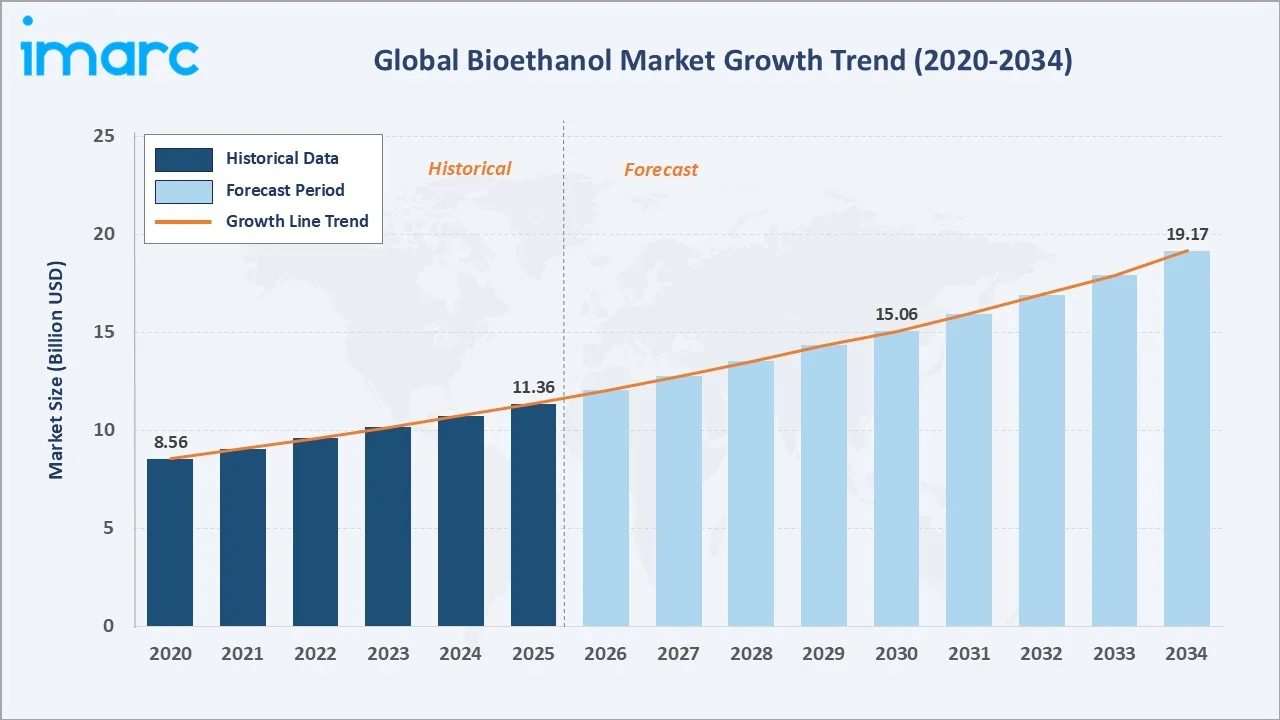

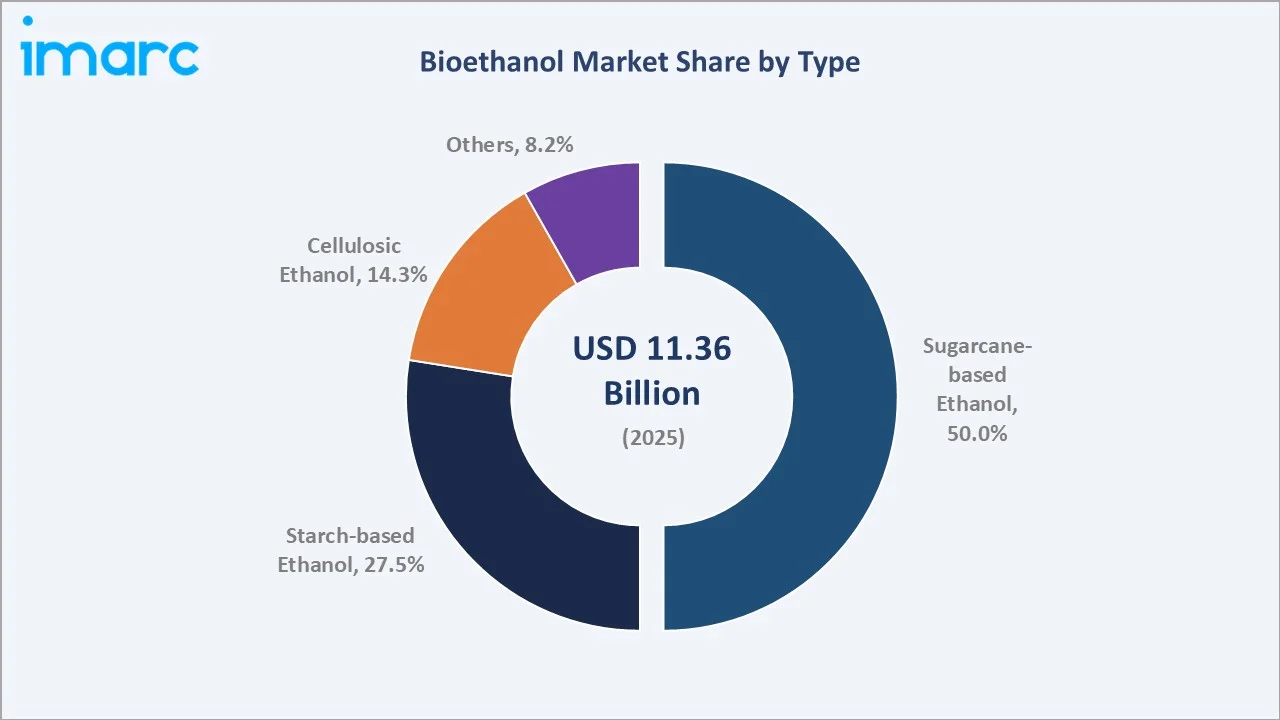

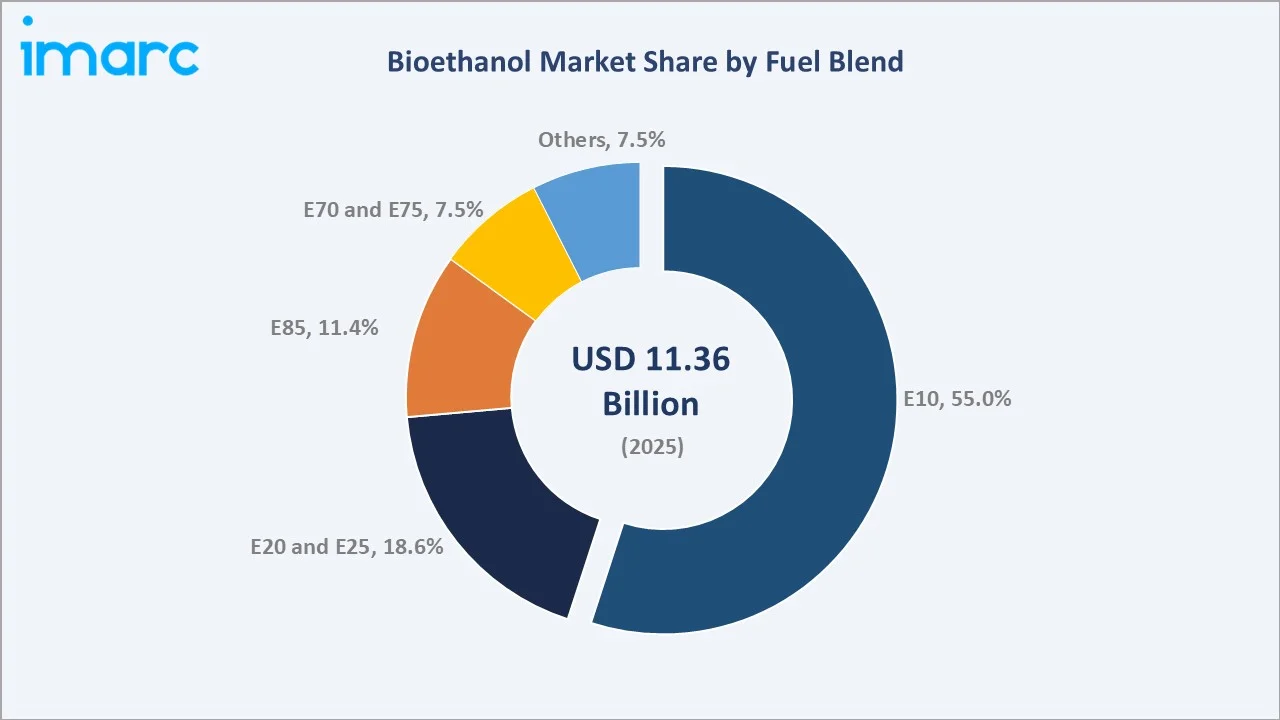

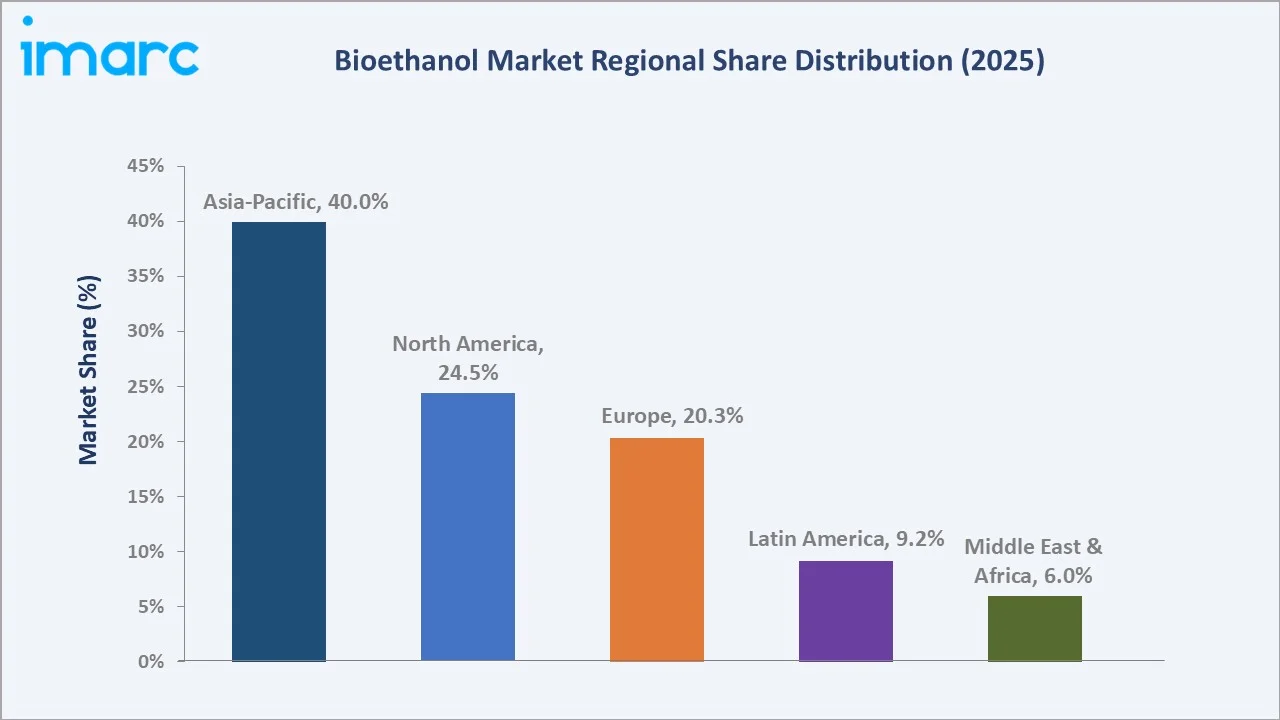

The global bioethanol market size was valued at USD 11.36 Billion in 2025 and is projected to reach USD 19.17 Billion by 2034, exhibiting a CAGR of 5.81% during the forecast period 2026-2034. Rising crude oil price volatility, strengthening national biofuel blending mandates across India, the United States, and Brazil, and accelerating decarbonisation of transport fuels are the principal forces reshaping the bioethanol industry. Sugarcane-based ethanol leads the type segment at 50.0% in 2025, while the E10 blend dominates the fuel blend segment with a 55.0% share. Asia-Pacific accounts for 40.0% of global revenue in 2025, emerging as the world's largest and fastest-growing regional bioethanol hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 11.36 Billion |

|

Forecast Market Size (2034) |

USD 19.17 Billion |

|

CAGR (2026-2034) |

5.81% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (40.0% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~6.8%) |

|

Leading Type |

Sugarcane-based Ethanol (50.0%, 2025) |

|

Leading Fuel Blend |

E10 (55.0%, 2025) |

The global bioethanol market growth trajectory from 2020 through 2034 reflects steady historical expansion backed by an accelerating forecast curve, powered by blending mandates, flex-fuel vehicle adoption, and scaling investments in second-generation biorefineries.

To get more information on this market, Request Sample

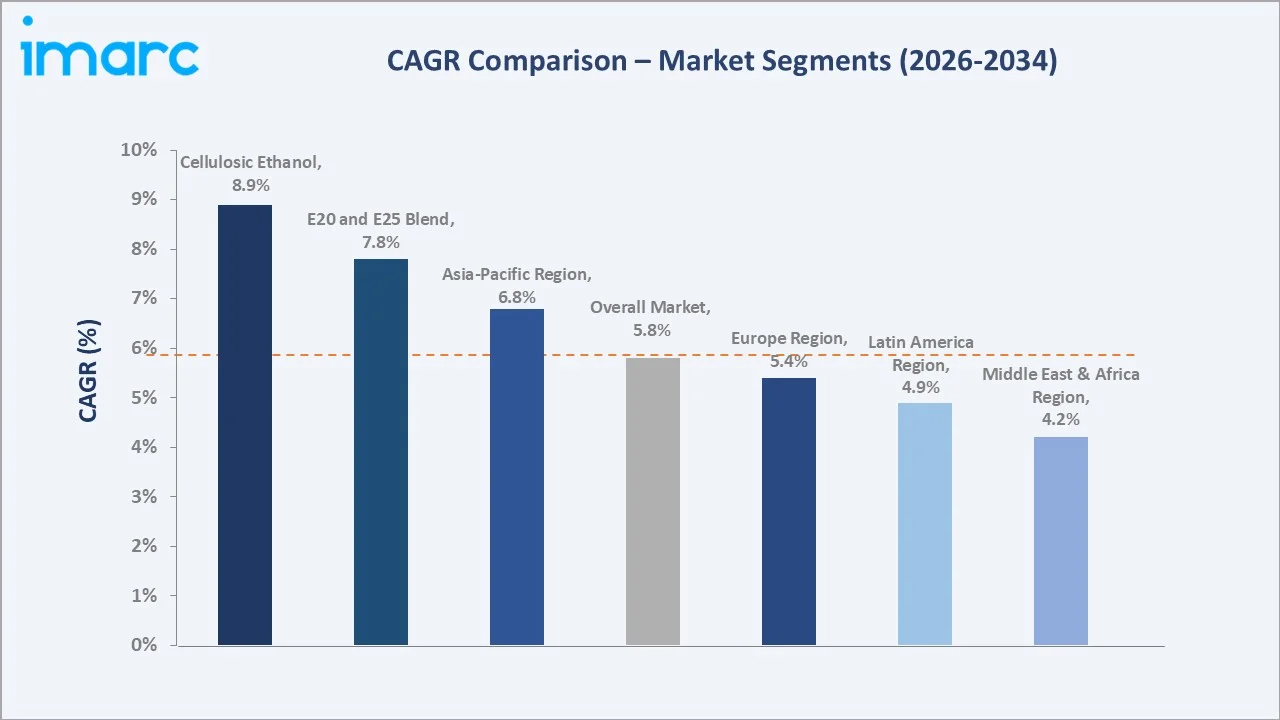

Segment-level CAGR comparison highlighting cellulosic ethanol and E20/E25 blends as the two fastest-growing technology sub-categories within the global bioethanol industry through 2034.

Executive Summary

The global bioethanol market is transitioning into a strategic pillar of the global energy-transition agenda. It was valued at USD 11.36 Billion in 2025 and is expected to reach USD 19.17 Billion by 2034, at a CAGR of 5.81% across 2026-2034. Momentum is powered by national blending mandates such as India's E20 target, the U.S. Renewable Fuel Standard, and Brazil's RenovaBio programme.

Sugarcane-based ethanol commands 50.0% of the type segment in 2025, reflecting Brazil's legacy feedstock advantage and India's rapid acreage expansion. Starch-based ethanol follows at 27.5%, supported by the U.S. corn-ethanol infrastructure. On the fuel-blend side, E10 dominates with a 55.0% share in 2025, anchored by universal adoption in North America and Europe, while higher-blend E20 and E25 variants contribute 18.6%, driven by India's E20 roadmap.

Asia-Pacific leads regional contribution with a 40.0% revenue share in 2025, powered by India's accelerated bioethanol programme, China's fuel ethanol pilot zones, and Thailand's sugarcane surplus. North America holds 24.5% on corn-belt ethanol output, while Europe contributes 20.3% through RED III compliance. Latin America and the Middle East & Africa round out at 9.2% and 6.0%, respectively.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Sugarcane-based Ethanol – 50.0% share (2025) |

|

Leading Fuel Blend |

E10 – 55.0% share (2025) |

|

Leading Region |

Asia-Pacific – 40.0% revenue share (2025) |

|

Second Region |

North America – 24.5% revenue share (2025) |

|

Fastest Growing Type |

Cellulosic Ethanol (~8.9% CAGR) |

|

Top Companies |

ADM, POET LLC, Royal Dutch Shell plc, BP p.l.c., Südzucker AG |

|

Market Opportunity |

Second-generation cellulosic capacity scale-up |

Key Analytical Observations Supporting the Above Data:

- Sugarcane-based ethanol's 50.0% share in 2025 reflects Brazil's cost advantage, with mills producing ethanol at roughly USD 1.7 per gallon, among the lowest globally.

- E10 leads fuel blend adoption at 55.0% in 2025, supported by universal compatibility with the global vehicle fleet exceeding 1.47 billion ICE vehicles.

- Asia-Pacific's 40.0% share in 2025 is driven by India's E20 roadmap, which raised the national blend rate from 1.5% in 2014 to over 15% by mid-2024.

- Cellulosic ethanol is the fastest-growing sub-segment with an estimated 8.9% CAGR, propelled by advanced biorefineries in the U.S., Europe, and India.

- The U.S. produced a record 16.1 billion gallons of fuel ethanol in 2024, reinforcing North America's position as a top exporter of starch-based bioethanol.

- Second-generation feedstocks represent a ~USD 3.5 Billion opportunity pool over 2026-2034.

Global Bioethanol Market Overview

Bioethanol is a renewable alcohol fuel produced through fermentation of sugar and starch-rich biomass such as sugarcane, corn, wheat, and cassava, as well as cellulosic feedstocks including agricultural residues and forestry waste. It functions as a low-carbon gasoline substitute, an oxygenate, and a feedstock for the chemicals, pharmaceuticals, and personal-care industries.

Applications span automotive fuel blending, aviation biofuel synthesis, industrial solvents, hand sanitisers, beverage-grade ethanol, and bio-based ethylene pathways. Macroeconomic enablers include the IEA's forecast that global biofuel demand will rise by 38 billion litres between 2023 and 2028, tightening carbon-pricing regimes, and mandatory greenhouse-gas reduction targets across the EU, U.S., and Asia-Pacific.

Market Dynamics

To evaluate market opportunities, Request Sample

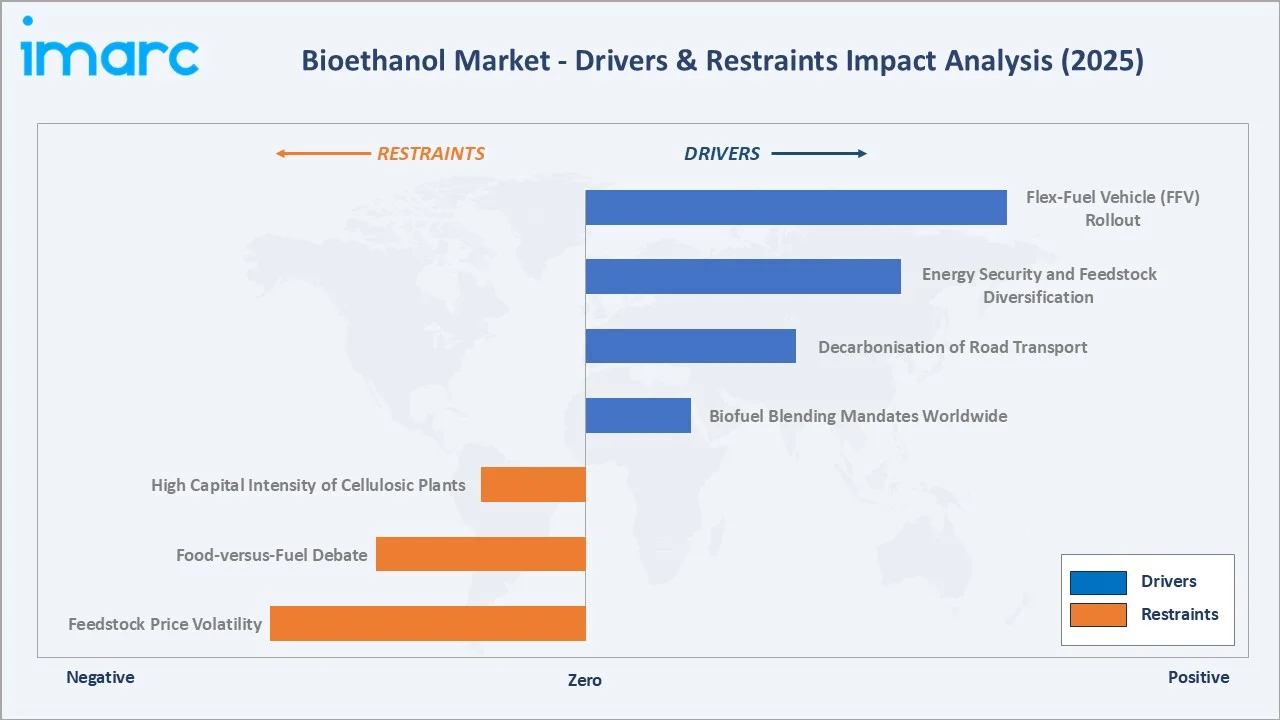

Market Drivers

- Biofuel Blending Mandates Worldwide: Over 65 countries had biofuel mandates by 2024, creating structural demand. India advanced its E20 target to 2025-26, while Brazil's Anhydrous Ethanol mandate continues at 27% in gasoline.

- Decarbonisation of Road Transport: Road transport accounts for nearly 12% of global GHG emissions. Bioethanol delivers lifecycle CO2 reductions of 40-90% versus gasoline, making it central to low-carbon fuel standards in California, the EU, and Japan.

- Energy Security and Feedstock Diversification: Nations with high oil-import dependence are investing in domestic bioethanol. India's crude-oil import bill exceeded USD 132 Billion in FY 2024, pushing policy toward 20% blending.

- Flex-Fuel Vehicle (FFV) Rollout: Brazil's FFV fleet exceeds 30 million vehicles, consuming roughly 90% of the country's gasoline pool. India mandated flex-fuel engines across major OEMs from 2023, expanding addressable demand.

Market Restraints

- Feedstock Price Volatility: Corn and sugarcane prices fluctuate with weather and global demand, compressing producer margins. U.S. corn prices swung by over 35% between 2022 and 2024.

- Food-versus-Fuel Debate: Use of arable land and food crops for ethanol continues to attract criticism, particularly in low-income economies sensitive to diverted grain volumes.

- High Capital Intensity of Cellulosic Plants: Second-generation biorefineries demand capital outlays of USD 300-500 Million per facility, slowing capacity additions outside subsidy-rich geographies.

Market Opportunities

- Sustainable Aviation Fuel (SAF) via Alcohol-to-Jet: Ethanol-derived SAF is commercially viable for aviation decarbonisation. LanzaJet's Freedom Pines facility produces 10 million gallons of SAF annually from bioethanol.

- Second-Generation Cellulosic Expansion: Agricultural residues, bagasse, and municipal waste enable ethanol output without food-crop competition. India targets 12 second-generation refineries by 2030.

Market Challenges

- Logistics and Blending Infrastructure Gaps: Ethanol-compatible pipelines, rail fleets, and fuel retail dispensers remain underdeveloped in many emerging markets, limiting effective blend-rate ceilings.

- Evolving Sustainability Certification: RED III, CORSIA, and LCFS schemes impose evolving thresholds, raising compliance costs for first-generation feedstock producers.

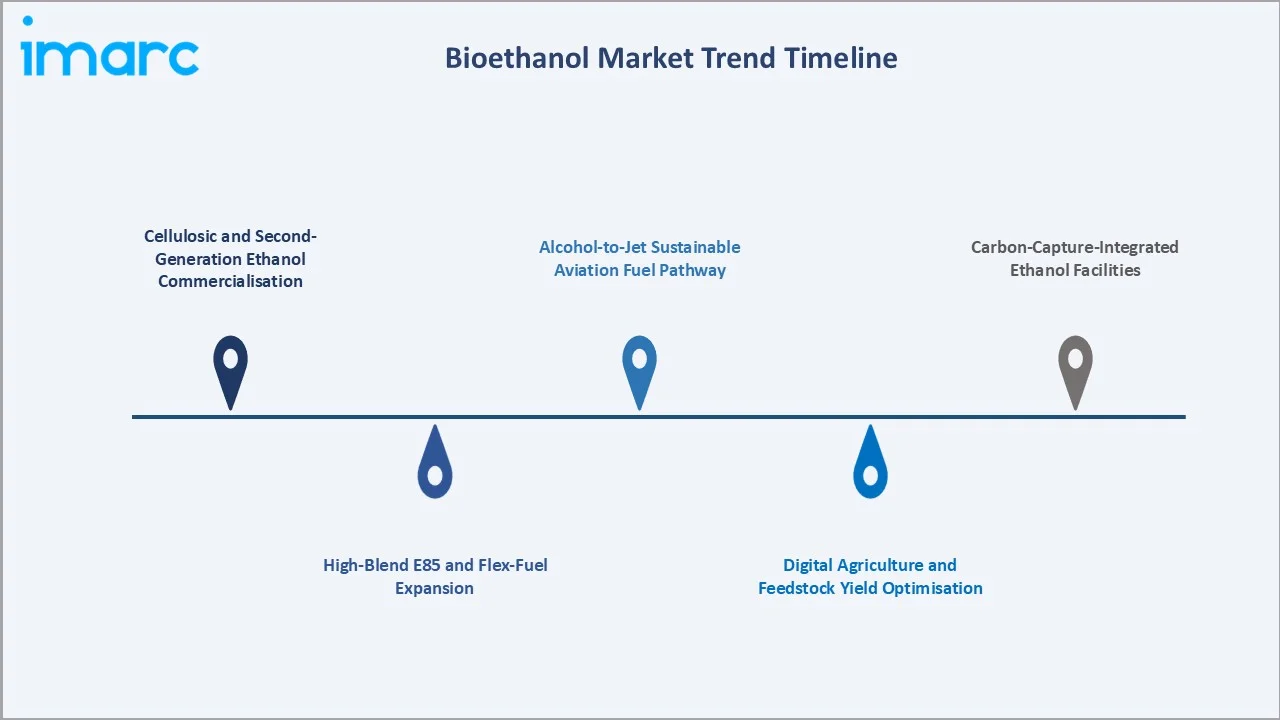

Emerging Market Trends

1. Cellulosic and Second-Generation Ethanol Commercialisation

Cellulosic ethanol, produced from agricultural residues, straw, and forestry waste, is scaling from pilot to commercial output. In 2024, India commissioned multiple 2G plants, and the U.S. DOE approved USD 1.97 Billion in loan guarantees for cellulosic biorefineries.

2. Alcohol-to-Jet Sustainable Aviation Fuel Pathway

Airlines, including United, JetBlue, and All Nippon Airways, have signed multi-year offtake agreements for ethanol-based SAF, with ICAO forecasting SAF demand to reach 17 Billion litres by 2030.

3. Carbon-Capture-Integrated Ethanol Facilities

Ethanol fermentation yields nearly pure CO2, offering the lowest-cost carbon capture pathway. Summit Carbon Solutions' 2,500-km pipeline in the U.S. Midwest, valued at USD 9 billion, aims to sequester 18 million tonnes of CO2 annually.

4. High-Blend E85 and Flex-Fuel Expansion

E85 deployment is accelerating in markets with large FFV fleets. Brazil and the U.S. together operate over 32 million FFVs as of 2025, with India preparing FFV scale-up from 2025 onwards.

5. Digital Agriculture and Feedstock Yield Optimisation

Precision farming, satellite yield monitoring, and AI-driven feedstock logistics are compressing ethanol costs. Bunge and Cargill digital-agri platforms have lifted average corn yields by 8-12% across contracted suppliers.

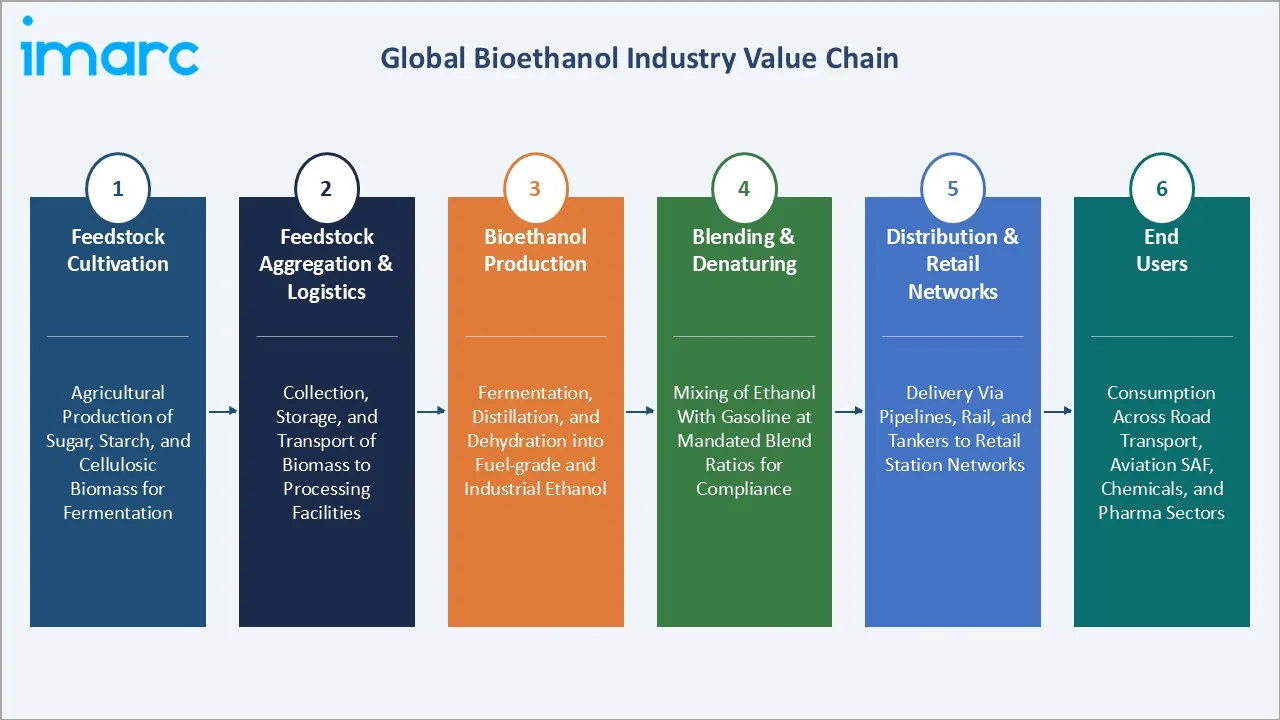

Industry Value Chain Analysis

The global bioethanol value chain extends across six stages, from feedstock cultivation to end-user fuel blending and chemical applications. Each stage features distinct competitive dynamics, margin profiles, and policy exposure.

|

Stage |

Description |

|

Feedstock Cultivation |

Agricultural production of sugar, starch, and cellulosic biomass is used as a primary input for ethanol fermentation. |

|

Feedstock Aggregation & Logistics |

Collection, storage, and transportation of raw biomass from farms to bioethanol processing facilities. |

|

Bioethanol Production |

Fermentation, distillation, and dehydration of biomass into fuel-grade and industrial-grade anhydrous ethanol. |

|

Blending & Denaturing |

Mixing of ethanol with gasoline at mandated blend ratios and denaturing for tax and regulatory compliance. |

|

Distribution & Retail Networks |

Delivery of blended fuel through pipelines, rail, tanker trucks, and retail station networks to end markets. |

|

End Users |

Final consumption across road transport, aviation SAF, chemicals, pharmaceutical, food & beverage, and cosmetics sectors. |

Bioethanol producers sit in the highest-value node of the chain, capturing margins from both fuel and chemical end-uses. Producer profitability remains tightly linked to feedstock cost, denaturing requirements, and logistics access to blending terminals.

Technology Landscape in the Bioethanol Industry

Advanced Fermentation and Enzyme Technology

Novozymes and DSM have commercialised next-generation enzyme cocktails that raise cellulosic ethanol yields by up to 15% while cutting enzyme loading costs by 20-30%, materially improving 2G plant economics.

Feedstock Innovation: Algae and Synthetic Biology

Research on third-generation algal ethanol and CRISPR-edited microbial strains is progressing, with start-ups demonstrating yields exceeding 20 g/L from engineered cyanobacteria under laboratory conditions.

Carbon Capture and Sequestration (CCS) Integration

Ethanol plants generate CO2 streams exceeding 99% purity, enabling the lowest-cost industrial CCS. Section 45Q credits in the U.S. provide USD 85 per tonne for sequestered CO2, transforming plant economics when paired with pipelines.

Automation and Digital Process Optimisation

Plant-wide digital-twin deployments, predictive maintenance, and AI-driven distillation control are cutting ethanol energy intensity by 8-12%. Honeywell's UOP ethanol-to-jet process technology exemplifies this digital-first approach.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Sugarcane-based Ethanol | 50.0% | 2025 |

| Fuel Blend | E10 | 55.0% | 2025 |

| Generation | First Generation | 70.0% | 2025 |

| End Use Industry | Automotive and Transportation | 65.0% | 2025 |

| Region | Asia Pacific | 40.0% | 2025 |

By Type

Sugarcane-based ethanol holds a commanding 50.0% share in 2025, driven by Brazil's production dominance and India's expansion under the E20 roadmap. Brazilian mills produce ethanol at approximately USD 1.7 per gallon, versus USD 2.1-2.3 for U.S. corn ethanol.

To access detailed market analysis, Request Sample

Starch-based ethanol accounts for 27.5% in 2025, anchored by the U.S. corn ecosystem, which produced 16.1 billion gallons in 2024. Cellulosic ethanol contributes 14.3%, the fastest-growing sub-category. The Others category (8.2%) captures molasses-derived and dedicated energy-crop pathways.

By Fuel Blend

E10 dominates the fuel blend segment with a 55.0% share in 2025, benefiting from universal compatibility with the global ICE vehicle parc and default-blend status across the U.S., Canada, Europe, and most Asia-Pacific economies.

E20 and E25 blends hold 18.6% in 2025, driven by India's E20 target and Brazil's 27% anhydrous mandate. E85, at 11.4%, is concentrated in Brazil and the U.S. Midwest corridors. E70 and E75 hold 7.5%, primarily in cold-weather markets such as Sweden and Finland, while Others round out at 7.5%.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

40.0% |

India E20 mandate, China fuel ethanol pilots, Thailand sugarcane surplus, Indonesia B35 parallel |

|

North America |

24.5% |

U.S. RFS mandates, corn-belt output, California, and Oregon low-carbon fuel standards |

|

Europe |

20.3% |

RED III compliance, Germany/France flex-fuel expansion, UK E10 rollout |

|

Latin America |

9.2% |

Brazil RenovaBio, 27% anhydrous mandate, Argentina & Colombia blending targets |

|

Middle East & Africa |

6.0% |

South Africa E10 discussions, UAE green fuel roadmap, Kenya/Uganda sugarcane investments |

Asia-Pacific commands a 40.0% global revenue share in 2025 making it the most dominant regional bioethanol market. India is the principal growth engine, lifting its ethanol blend rate from 1.5% in 2014 to more than 15% by mid-2024 under the Ethanol Blended Petrol programme. China maintains fuel ethanol pilot zones in Anhui, Heilongjiang, and Jilin provinces, while Thailand leverages sugarcane surplus to serve both domestic and export demand.

North America, with 24.5% share in 2025, is anchored by the U.S. corn-belt complex and the Renewable Fuel Standard framework. The U.S. produced a record 16.1 billion gallons in 2024, while Canada's Clean Fuel Regulations have accelerated ethanol demand across Ontario and Quebec.

Europe holds 20.3% of global revenue in 2025, governed by RED III, which mandates a 29% renewable share in transport by 2030. Germany and France account for nearly half of EU bioethanol consumption, while the UK's 2021 E10 rollout lifted national ethanol demand by ~19%.

Latin America, at 9.2%, is led by Brazil, the world's second-largest ethanol producer with annual output exceeding 33 billion litres. The Middle East & Africa, at 6.0%, presents long-term upside via South Africa's proposed E10 mandate and the UAE's sustainable fuel roadmap aligned with COP28 commitments.

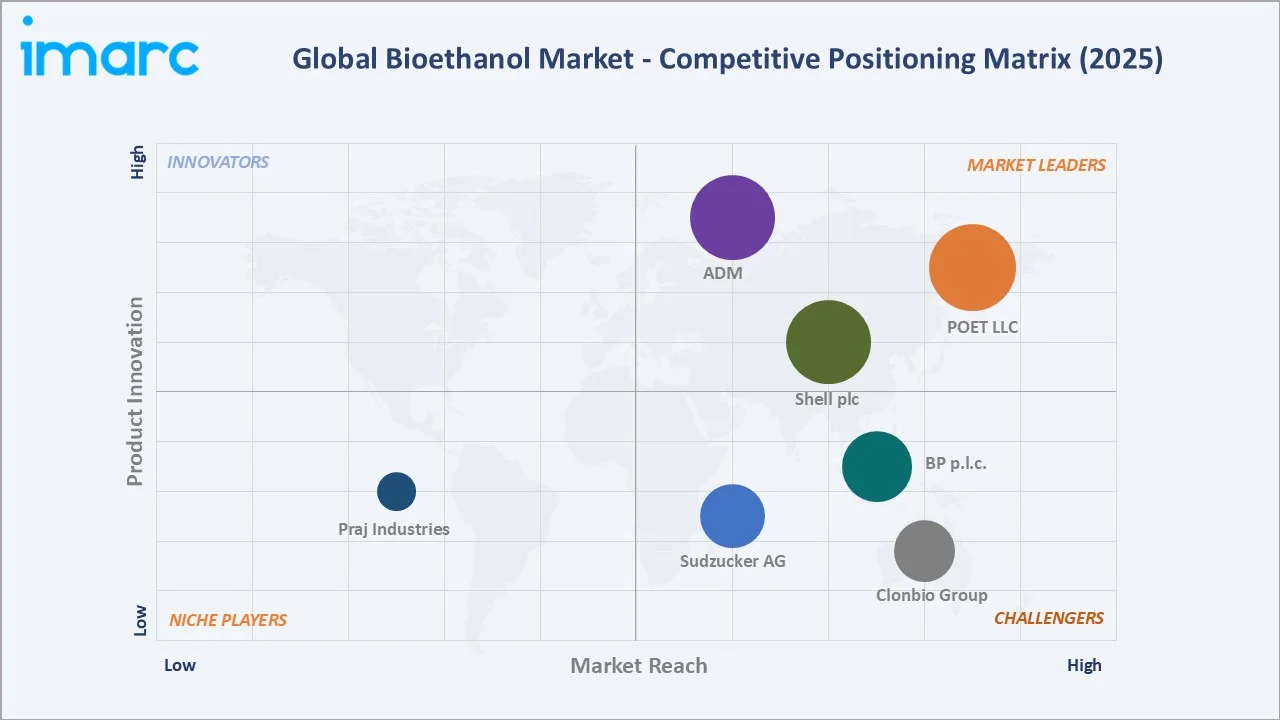

Competitive Landscape

|

Company Name |

Key Platform / Offerings |

Market Position |

Core Strength |

|

ADM |

Ethanol |

Leader |

Corn ethanol scale, integrated agri-chain |

|

POET LLC |

Bioproducts |

Leader |

Largest U.S. corn ethanol producer, 34 plants |

|

Shell plc |

Raízen |

Leader |

World's largest sugarcane ethanol producer via 44% Raízen JV |

|

BP p.l.c. |

BP Bunge Bioenergia |

Challenger |

Brazil sugarcane, ~50,000 bpd ethanol equivalent, 11 mills, SAF pathway |

|

Südzucker AG |

CropEnergies |

Challenger |

EU's largest ethanol producer, E10 supplier |

|

Clonbio Group |

Bioethanol & bioproducts |

Challenger |

One of Europe's largest single-site ethanol biorefineries (Hungary) |

|

Praj Industries |

2G Ethanol |

Emerging |

Licensed cellulosic ethanol technology platforms |

The global bioethanol market features a moderately consolidated structure at the top, with five global producers controlling roughly 35-40% of traded ethanol volumes in 2025. Leadership reflects feedstock integration, refinery scale, and fuel-distribution depth.

Key Company Profiles

ADM

ADM (Archer-Daniels-Midland Company) is a global agribusiness leader headquartered in Chicago, Illinois, with integrated operations across grain trading, oilseed processing, and biofuel production, generating over USD 85 billion in revenue in 2024.

- Product & Platform Portfolio: Corn-based ethanol, dry-milled fuel ethanol, industrial ethanol, DDGS, corn oil.

- Recent Developments: In October 2021, ADM and Gevo, Inc., announced that they had signed a memorandum of understanding (MoU) to support the production of sustainable aviation fuel (SAF) and other low-carbon-footprint hydrocarbon fuels.

- Strategic Focus: ADM's strategy emphasises carbon capture integration, SAF co-products, and premium industrial-grade ethanol for chemicals and pharmaceuticals.

POET LLC

POET LLC is the largest pure-play bioethanol producer globally, headquartered in Sioux Falls, South Dakota, operating 34 bioprocessing facilities with a combined output of approximately 3 billion gallons annually.

- Product & Platform Portfolio: Fuel ethanol, Dakota Gold DDGS animal feed, corn oil, purified alcohol for industrial use.

- Recent Developments: In February 2026, NASCAR announced a landmark partnership with POET, naming the company the Official Bioethanol Partner of NASCAR. As part of the agreement, NASCAR will become the first major motorsports series to utilize zero-carbon bioethanol in combination with its existing fuel partner Sunoco, reinforcing the sport’s commitment to innovation, performance, and healthy environments in accordance with its NASCAR IMPACT goals.

- Strategic Focus: POET's focus is scale leadership, producer-owned logistics, carbon-intensity reduction, and SAF partnerships.

Royal Dutch Shell plc

Royal Dutch Shell plc’s Raízen is the world's largest sugarcane ethanol producer, a 50-50 JV between Shell and Cosan, operating 35 Brazilian mills with annual bioethanol output exceeding 4 billion litres.

- Product & Platform Portfolio: First-generation sugarcane ethanol, second-generation (E2G) cellulosic ethanol, bioelectricity, sugar co-products.

- Recent Developments: In January 2025, the Brazilian Development Bank (BNDES) approved a R$1 billion loan for Raízen Energia to construct its third second-generation ethanol (E2G) production unit. The new facility, to be located in Andradina, São Paulo, will have an annual production capacity of up to 82 million liters.

- Strategic Focus: Royal Dutch Shell plc targets global leadership in second-generation ethanol, SAF feedstock supply, and export-oriented low-carbon ethanol.

Market Concentration Analysis

The global bioethanol market exhibits moderate concentration, with the top five producers (ADM, POET LLC, Royal Dutch Shell plc, BP p.l.c., Südzucker AG) collectively accounting for approximately 38-42% of global volumes in 2025. The balance remains fragmented across mid-sized producers, regional cooperatives, and state-owned enterprises.

Consolidation is accelerating at the premium tier, where carbon-capture-integrated plants and SAF-ready biorefineries demand capital intensity that only the largest operators can sustain. Emerging markets like India are fostering domestic champions through state-backed offtake contracts.

Investment & Growth Opportunities

Fastest-Growing Segments

Cellulosic ethanol is the highest-growth sub-segment with an estimated CAGR of ~8.9% through 2034, driven by commercial deployments such as Raízen's E2G pipeline and LanzaJet's Freedom Pines SAF facility. Ethanol-to-SAF is the second fastest vector, with offtake commitments exceeding 10 billion litres globally by 2030.

Emerging Market Expansion

India, Indonesia, and the Philippines collectively represent a ~USD 4.5 billion incremental opportunity between 2026 and 2034, anchored by rising blending mandates. African markets, including Kenya, Uganda, and Nigeria, are piloting E10 frameworks.

Venture & Private Investment Trends

Notable transactions include LanzaJet's USD 200 Million Series B, Summit Carbon Solutions' USD 9 Billion pipeline project, and Gevo's USD 1.46 Billion USDA loan guarantee for Net-Zero 1. Private equity interest is consolidating around 2G ethanol and CCS biorefineries.

Future Market Outlook (2026-2034)

The global bioethanol market forecast projects expansion from USD 11.36 Billion in 2025 to USD 19.17 Billion by 2034 at a CAGR of 5.81%, reflecting structural demand boost from transport decarbonisation, aviation SAF pull, and policy-driven blending mandates.

Three forces will reshape the industry through 2034. First, SAF will convert bioethanol from a road-fuel commodity into a strategic aviation feedstock, with ICAO projecting SAF demand at 17 Billion litres by 2030. Second, carbon-capture-equipped plants will dominate low-carbon fuel credit markets. Third, cellulosic feedstocks will resolve the food-versus-fuel tension.

By 2034, bioethanol is forecast to evolve into a multi-use strategic platform fuel, spanning road, aviation, industrial solvents, and bio-based chemicals. Competitive leadership will be defined by feedstock flexibility, carbon-intensity optimisation, and integration into SAF value chains.

Research Methodology

Primary Research

Primary research included over 45 structured interviews during 2024-2025 with bioethanol producers, feedstock suppliers, oil marketing companies, blending terminal operators, technology licensors, and regulatory officials. Primary insights validated market sizing, regional blend-rate estimates, and forward feedstock economics.

Secondary Research

Secondary sources include IEA Renewables 2024, EIA Monthly Energy Review, USDA grain statistics, UNICA Brazil data, ePURE ethanol data, India's Ministry of Petroleum notifications, company annual reports, SEC filings, and industry publications such as Ethanol Producer Magazine and S&P Platts biofuel indices.

Forecasting Models

Market size estimates were derived through bottom-up (plant-level capacity × utilisation × blend rates) and top-down (transport fuel demand × mandate compliance) approaches. Scenario analysis was performed under base, optimistic, and conservative cases, accounting for feedstock price volatility and mandate timing risk.

Bioethanol Market Report Coverage

|

Attribute |

Details |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2025) |

USD 11.36 Billion |

|

Market Forecast (2034) |

USD 19.17 Billion |

|

CAGR (2026-2034) |

5.81% |

|

Units |

USD Billion |

|

Segmentation |

By Type, By Fuel Blend, By Generation, By End Use Industry, By Region |

|

Regional Analysis |

North America, Asia-Pacific, Europe, Latin America, Middle East & Africa |

|

Countries Covered |

U.S., Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, UK, Italy, Spain, Russia, Brazil, Mexico |

|

Key Companies |

ADM, POET LLC, Shell plc, BP p.l.c., Südzucker AG, Clonbio Group, Praj Industries, etc. |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the bioethanol market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global bioethanol market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the bioethanol industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Bioethanol Market Report

The global bioethanol market was valued at USD 11.36 Billion in 2025, driven by blending mandates, flex-fuel vehicle adoption, and low-carbon fuel compliance.

The market is projected to reach USD 19.17 Billion by 2034, growing at a CAGR of 5.81% during 2026-2034, supported by SAF demand, cellulosic scale-up, and E20 mandates.

Sugarcane-based ethanol leads with 50.0% share in 2025, anchored by Brazil's cost-leader production base and India's accelerated E20 programme.

E10 dominates with 55.0% share in 2025, benefiting from universal compatibility with the global ICE vehicle fleet and default-blend status in the U.S., Europe, and Canada.

Asia-Pacific leads with 40.0% share in 2025, fuelled by India's E20 mandate, China's fuel ethanol pilots, Thailand's sugarcane surplus, and Indonesia's biofuel programme.

Key drivers include national biofuel mandates, transport decarbonisation targets, flex-fuel vehicle adoption, low-carbon fuel standards, and the emerging ethanol-to-SAF pathway.

Cellulosic ethanol is the fastest-growing type segment with an estimated CAGR of ~8.9% through 2034, driven by commercial-scale second-generation biorefineries.

Leading companies include ADM, POET LLC, Royal Dutch Shell plc, BP p.l.c., Südzucker AG, Clonbio Group, and Praj Industries.

Ethanol fermentation yields near-pure CO2 streams, enabling the lowest-cost industrial carbon capture, boosted by the U.S. Section 45Q USD 85/tonne sequestration credit.

First-generation ethanol uses food crops such as corn and sugarcane, while second-generation (cellulosic) ethanol uses non-food biomass, including agricultural residues and forestry waste.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)