Biopsy Devices Market Size, Share, Trends and Forecast by Procedure Type, Product, Application, Guidance Technique, End User, and Region, 2026-2034

Global Biopsy Devices Market Size, Share, Trends & Forecast (2026-2034)

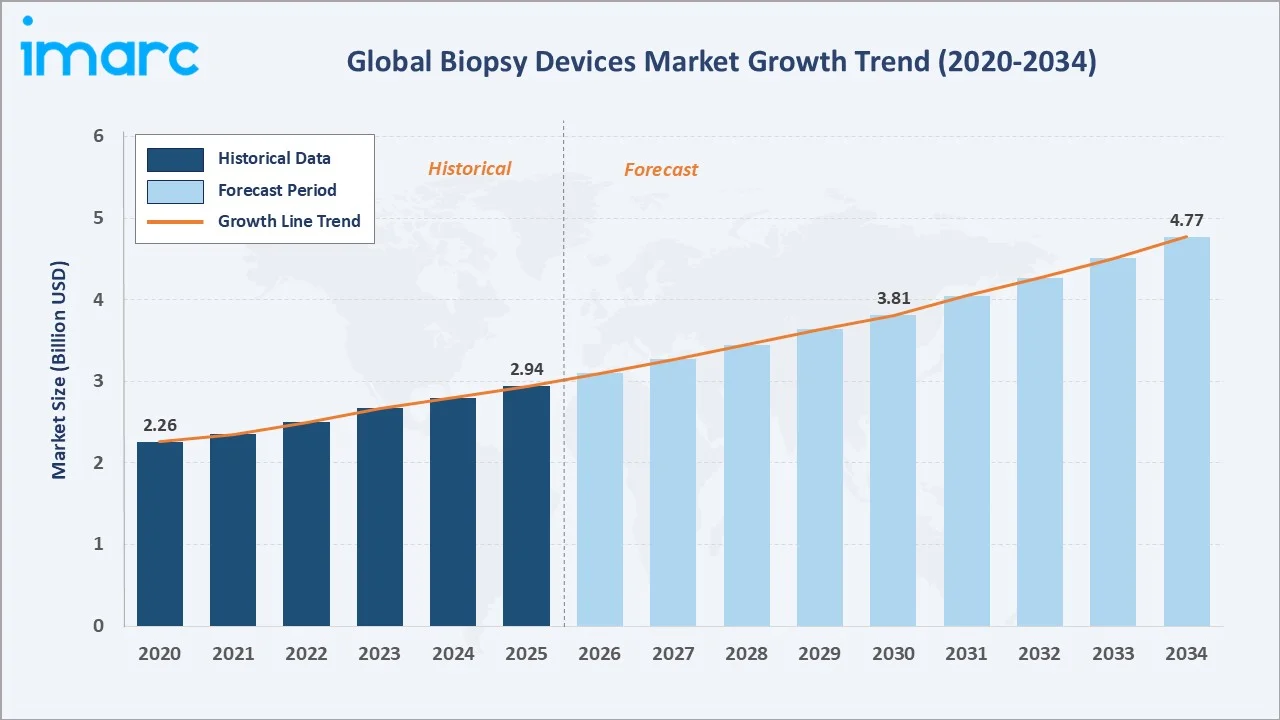

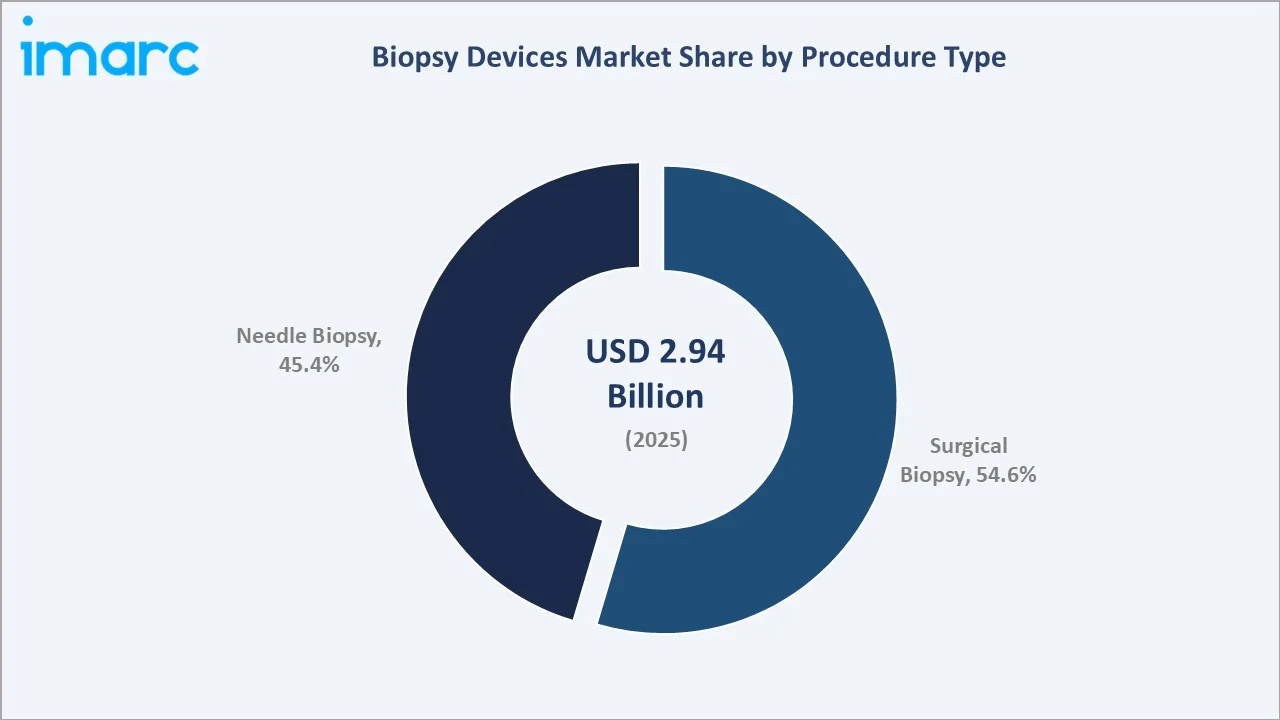

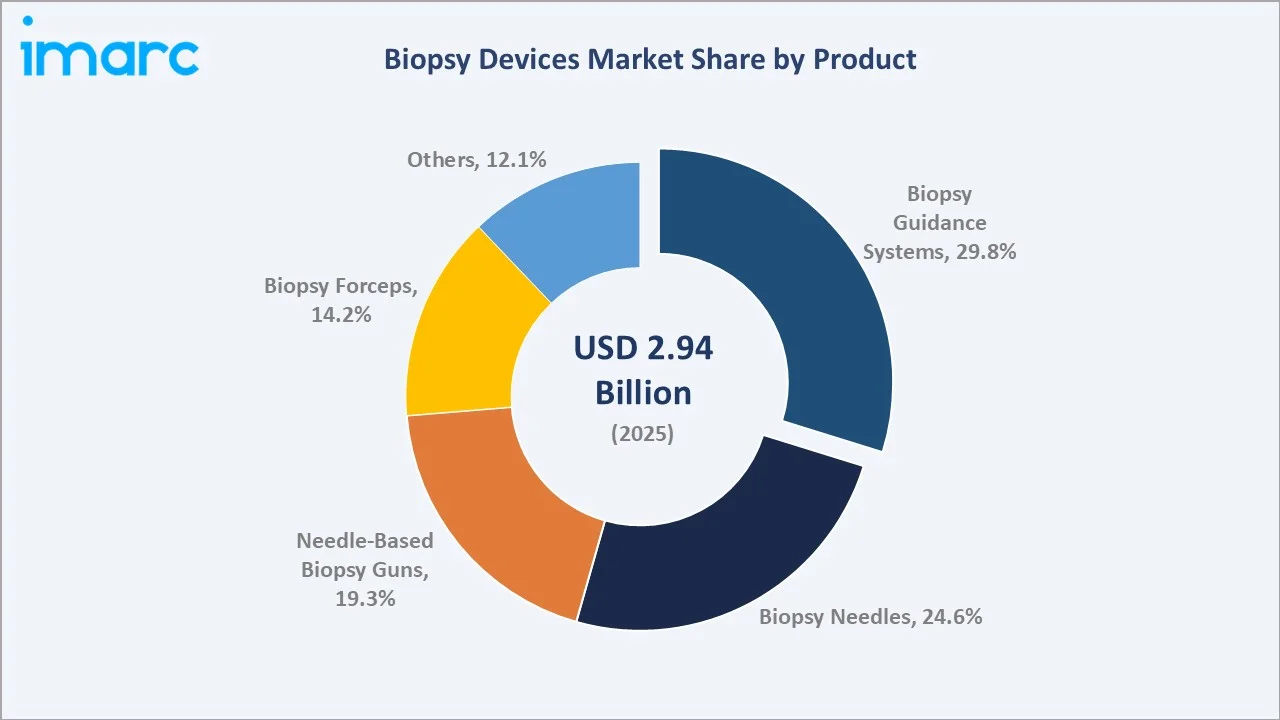

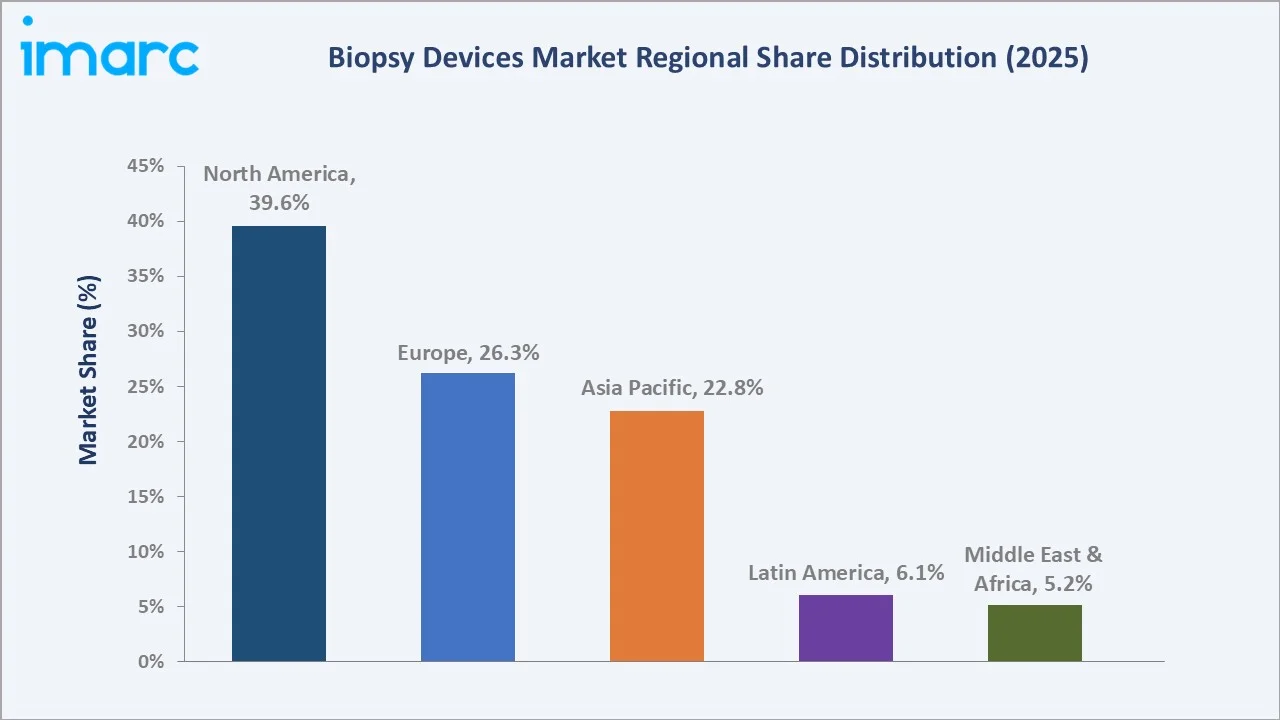

The global biopsy devices market size was valued at USD 2.94 Billion in 2025 and is projected to reach USD 4.77 Billion by 2034, exhibiting a CAGR of 5.36% during 2026-2034. Rising global cancer incidence, with the WHO recording over 20 million new cancer cases in 2022, growing adoption of minimally invasive procedures, and rapid integration of image-guided and AI-assisted biopsy techniques drive market growth. Surgical Biopsy leads the procedure type at 54.6% in 2025, while Biopsy Guidance Systems dominate products at 29.8%. North America accounts for 39.6% of global revenue, the largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.94 Billion |

|

Forecast Market Size (2034) |

USD 4.77 Billion |

|

CAGR (2026-2034) |

5.36% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (39.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

|

Leading Procedure Type |

Surgical Biopsy (54.6%, 2025) |

|

Leading Product |

Biopsy Guidance Systems (29.8%, 2025) |

The market trajectory from 2020 to 2034 reflects a healthcare-modernisation-driven path. Historical revenue held flat at USD 2.94 Billion through 2020-2025, reflecting pandemic-era procedure deferrals, with the forecast curve extending to USD 4.77 Billion by 2034 as elective biopsy backlogs normalise and screening expands.

To get more information on this market, Request Sample

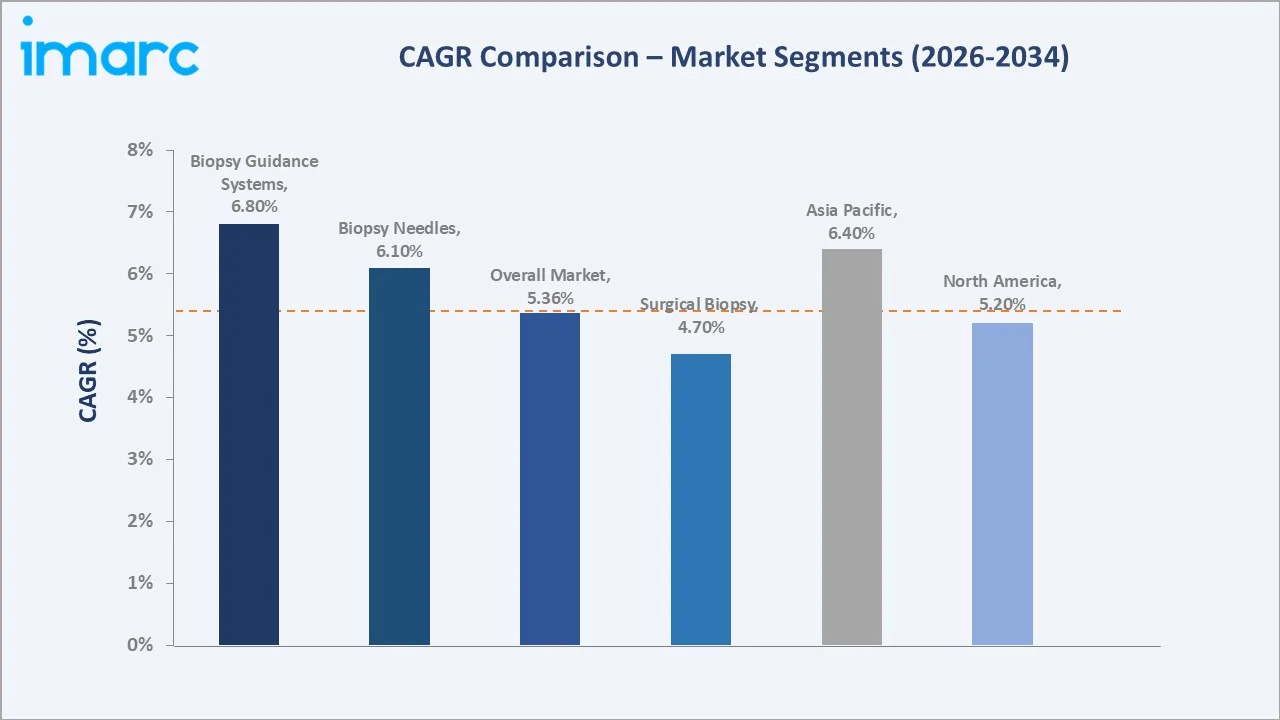

Segment-level CAGR comparisons highlight Biopsy Guidance Systems and Asia Pacific as the two fastest-growing sub-categories, fueled by image-guided procedure adoption and rising cancer screening volumes through 2034.

Executive Summary

The global biopsy devices market is undergoing structural transformation, shaped by the rising global cancer burden, accelerating shift to minimally invasive diagnostics, and convergence of imaging, AI, and robotics in biopsy workflows. Valued at USD 2.94 Billion in 2025, the market is forecast to reach USD 4.77 Billion by 2034 at a CAGR of 5.36%. WHO recorded over 20 million new cancer cases globally in 2022.

Surgical Biopsy leads the procedure type with 54.6% share in 2025, sustained by its diagnostic gold-standard status for many tumour types. Needle Biopsy at 45.4% is the faster-growing category. Biopsy Guidance Systems lead products at 29.8%, followed by Biopsy Needles at 24.6% and Needle-Based Biopsy Guns at 19.3%.

North America dominates with 39.6% revenue share in 2025, anchored by high cancer screening rates and reimbursement coverage. Asia Pacific at 22.8% is the fastest-growing region, led by China's expanding diagnostic infrastructure and India's growing private hospital network. Europe holds 26.3%, with Latin America and MEA at 6.1% and 5.2%.

Key Market Insights

|

Insight |

Data |

|

Largest Procedure Type |

Surgical Biopsy - 54.6% share (2025) |

|

Leading Product |

Biopsy Guidance Systems - 29.8% share (2025) |

|

Leading Region |

North America - 39.6% revenue share (2025) |

|

Fastest-Growing Region |

Asia Pacific - 22.8% share (2025) |

|

Top Companies |

BD (Becton Dickinson), Hologic, Inc., Boston Scientific Corporation, Cook, Medtronic, Olympus America, Argon Medical Devices, Devicor Medical Products, Inc., INRAD, Inc., and Mauna Kea Technologies |

Key Analytical Observations Supporting The Above Data:

- Surgical Biopsy's 54.6% share in 2025 reflects its diagnostic gold-standard role for breast, prostate, and lymph-node tumours, where excisional sampling remains preferred.

- Biopsy Guidance Systems at 29.8% in 2025 lead products on the back of stereotactic, ultrasound, and MRI-guided platform demand from Hologic and BD.

- North America's 39.6% leadership reflects high cancer screening adherence, with the US recording over 310,720 new breast cancer cases in 2024 per ACS estimates.

- Asia Pacific at 22.8% combines China's hospital-tier expansion, India's diagnostics boom, and Japan's high cancer-screening adherence under universal coverage.

Global Biopsy Devices Market Overview

Biopsy devices are medical instruments used to extract tissue or cell samples from the body for laboratory examination, primarily to diagnose cancer and other diseases. The category includes surgical instruments, core and fine-needle biopsy devices, vacuum-assisted systems, and image-guidance platforms.

Applications span oncology, gastroenterology, urology, gynaecology, dermatology, and interventional radiology. Macroeconomic enablers include the global cancer burden of over 20 million new cases in 2022 (WHO), rising healthcare expenditure exceeding USD 9.8 trillion in 2021, and the expansion of cancer screening programmes across emerging economies.

Market Dynamics

To evaluate market opportunities, Request Sample

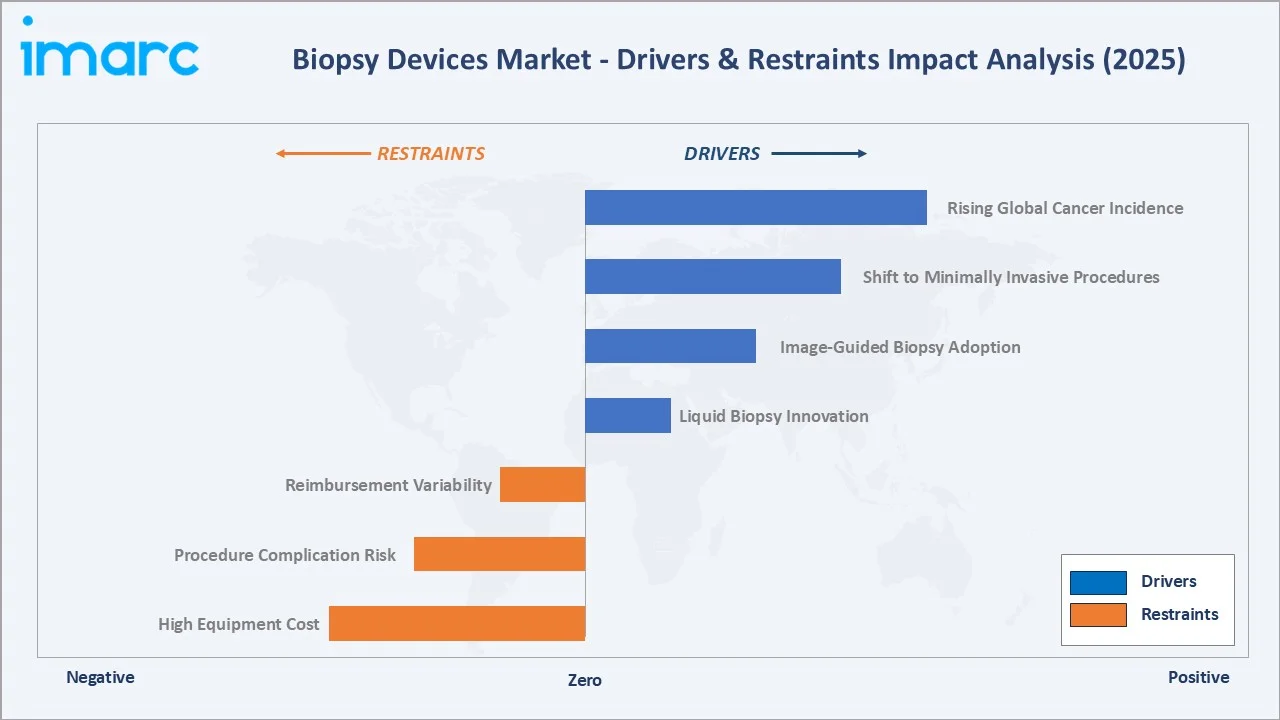

Market Drivers

- Rising Global Cancer Incidence: The WHO recorded over 20 million new cancer cases globally in 2022, with breast, lung, and prostate cancers leading. Cases are projected to rise to 35 million by 2050.

- Shift to Minimally Invasive Procedures: Core-needle, vacuum-assisted, and percutaneous techniques have largely displaced open biopsy in many indications, reducing patient recovery time and enabling outpatient workflows.

- Image-Guided Biopsy Adoption: Stereotactic, ultrasound, and MRI-guided platforms achieve sampling accuracy exceeding 95% in lesions under 10 mm, expanding biopsy use in early-stage detection.

- Liquid Biopsy Innovation: Liquid biopsy (ctDNA analysis from blood) is a complementary modality with expanding indications across oncology. A defining milestone was the July 2024 FDA approval of Guardant Health's Shield blood test, the first blood-based primary screening option approved for colorectal cancer in adults aged 45 and over.

Market Restraints

- Reimbursement Variability: Reimbursement coverage and rates vary significantly across regions. US Medicare CPT code structure favours certain modalities, while many emerging markets lack standardised coverage.

- Procedure Complication Risk: Procedure-related complications, including bleeding, infection, and pneumothorax in lung biopsies, create clinical caution, with reported rates of 1-5% by site and technique.

- High Equipment Cost: Advanced biopsy guidance platforms, such as stereotactic tables, MRI suites, and vacuum-assisted consoles, carry substantial capital, infrastructure, and training costs, limiting penetration in lower-resource settings and concentrating capacity in tertiary centres.

Market Opportunities

- Liquid Biopsy Expansion: Liquid biopsy is the highest-growth adjacency, with FDA approvals expanding for ctDNA tests. Guardant Health and Natera are scaling commercial deployments. For instance, Natera's Signatera MRD test secured broad Medicare coverage in June 2025 across colorectal, breast, bladder, ovarian, and lung cancers, plus pan-cancer immunotherapy monitoring (LCD L38779), validated across 100+ clinical studies.

- AI-Enhanced Guidance Systems: AI-powered image analysis is augmenting biopsy guidance, with Hologic, GE, and Siemens deploying AI features in breast, lung, and prostate workflows. For example, Siemens Healthineers' FDA-cleared AI-Rad Companion Prostate MR for Biopsy Support auto-segments the prostate and marks suspicious lesions for MRI-ultrasound fusion during targeted biopsy.

- Emerging Market Penetration: India, China, Brazil, and Indonesia represent structural growth markets as cancer screening expands and private networks deploy advanced biopsy capabilities.

Market Challenges

- Regulatory Compliance Burden: EU MDR transition has tightened device certification requirements, extending timelines and raising compliance costs, particularly for smaller manufacturers.

- Skilled Operator Shortage: Interventional radiologists and trained operators remain in short supply globally, with the ACR documenting persistent workforce shortages across small, rural, and community hospital settings, creating bottlenecks in advanced biopsy service delivery.

- Modality Substitution Risk: Competition from emerging diagnostic modalities, including liquid biopsy and advanced imaging, may displace tissue biopsy in low-yield indications long term.

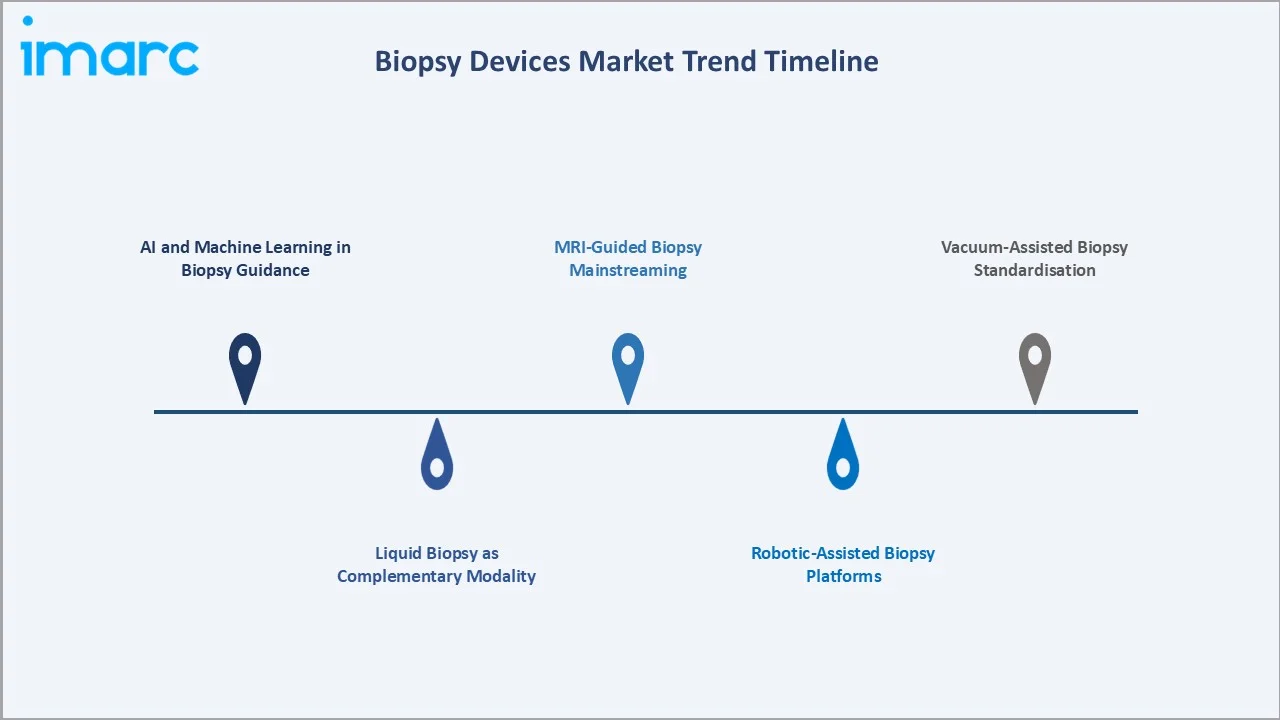

Emerging Market Trends

1. AI and Machine Learning in Biopsy Guidance

AI is transforming biopsy guidance through automated lesion detection, real-time targeting, and post-procedure pathology correlation. For instance, iCAD's ProFound AI, the first AI software approved for digital breast tomosynthesis, is now deployed across over 50 countries and has helped analyze an estimated 40 million mammograms in the last five years alone, with clinical studies showing an improvement in radiologist sensitivity and a reduction in reading time for 3D mammography.

2. Liquid Biopsy as Complementary Modality

Liquid biopsy is shifting from research to clinical practice. The FDA has approved multiple ctDNA companion diagnostics since 2020, including Guardant360 CDx and FoundationOne Liquid CDx. Guardant Health reported 53,100 clinical tests in Q3 2024 alone, underscoring the transition from pilot to mainstream commercial scale.

3. Robotic-Assisted Biopsy Platforms

Robotic-assisted prostate, breast, and lung biopsy platforms are emerging. KOELIS Trinity for prostate and Veran SPiN for lung biopsy enable sub-millimetre targeting accuracy.

4. MRI-Guided Biopsy Mainstreaming

MRI-guided breast and prostate biopsy adoption is accelerating, particularly for lesions occult on ultrasound or mammography. Siemens, Philips, and GE have all expanded MRI-compatible biopsy product lines through 2026.

5. Vacuum-Assisted Biopsy Standardisation

Vacuum-assisted biopsy (VAB) has become a standard of care for many breast lesions, driven by its higher diagnostic accuracy and minimally invasive nature, with leading systems from companies such as Hologic and BD supporting widespread global adoption.

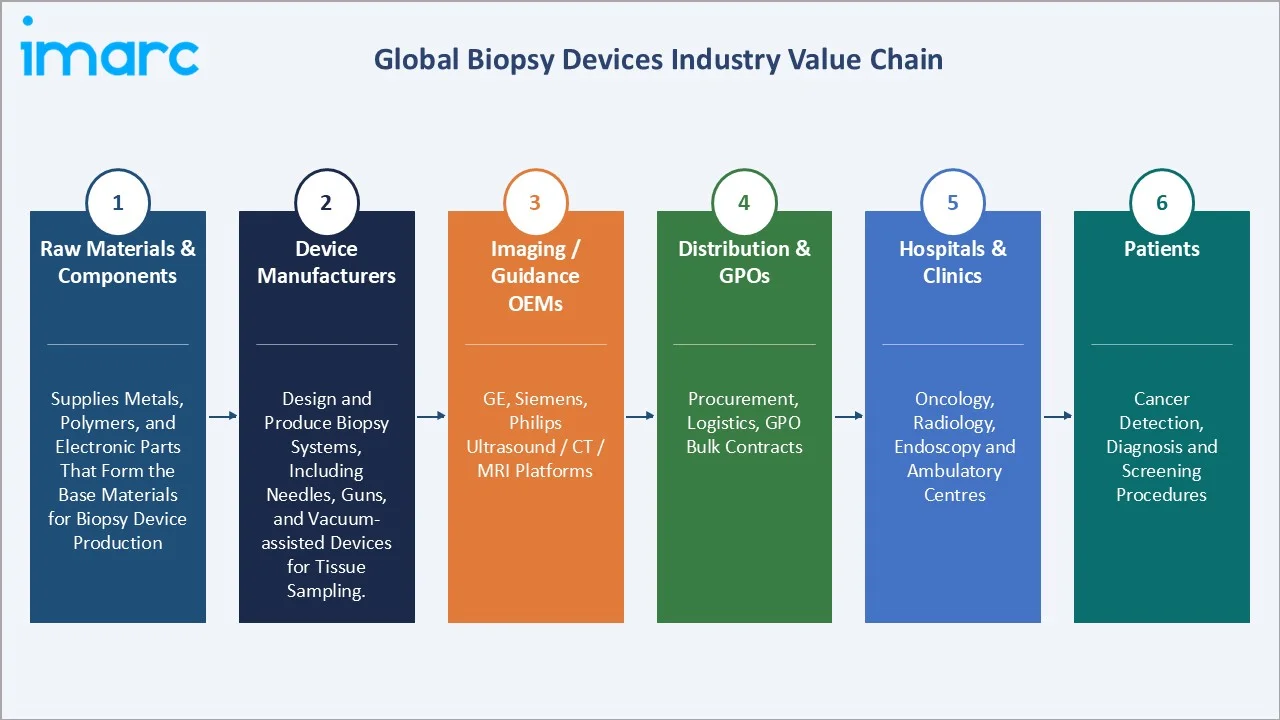

Industry Value Chain Analysis

The biopsy devices value chain spans six integrated stages from raw materials and components through patient delivery, each with distinct competitive dynamics and margin profiles.

|

Stage |

Key Players / Examples |

|

Raw Materials & Components |

Supplies metals, polymers, and electronic parts that form the base materials for biopsy device production. |

|

Device Manufacturers |

Design and produce biopsy systems, including needles, guns, and vacuum-assisted devices for tissue sampling. |

|

Imaging / Guidance OEMs |

Provide imaging technologies (ultrasound, CT, MRI) that guide accurate biopsy procedures. |

|

Distribution & GPOs |

Manage procurement, logistics, and supply of devices to healthcare providers through contracts and bulk purchasing. |

|

Hospitals & Clinics |

Perform biopsy procedures using integrated devices and imaging systems for diagnosis. |

|

Patients |

Receive biopsy procedures for cancer detection, diagnosis, and screening programs. |

Device manufacturers occupy the highest strategic value position, integrating proprietary needle, gun, and vacuum technologies. Imaging OEMs are increasingly bundling biopsy guidance into broader diagnostic platforms.

Technology Landscape in the Biopsy Devices Industry

Image Guidance: Stereotactic, Ultrasound, MRI

Image-guided biopsy is the dominant technology category. Stereotactic for breast, ultrasound for thyroid and abdominal, and MRI for prostate and breast lesions collectively represent over 70% of advanced biopsy procedures in 2025.

Vacuum-Assisted Biopsy (VAB)

Vacuum-assisted biopsy (VAB) systems use suction to acquire larger, contiguous tissue samples through a single insertion, with platforms such as Hologic’s Brevera system integrating vacuum acquisition with real-time imaging and specimen verification to improve procedural efficiency and accuracy.

Liquid Biopsy and ctDNA Analysis

Liquid biopsy detects circulating tumour DNA in blood. Guardant Health, Natera, and Foundation Medicine lead clinical deployment, with FDA-approved companion diagnostics expanding across NSCLC, colorectal, and breast indications.

Robotic and AI-Augmented Biopsy

Robotic-assisted and AI-augmented biopsy systems are rapidly emerging, enabling highly precise and targeted tissue sampling. Platforms such as the KOELIS Trinity® integrate MRI–ultrasound fusion, real-time tracking, and AI-based lesion detection to improve targeting accuracy.

Market Segmentation Analysis

The report includes following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Procedure Type |

Surgical Biopsy |

54.6% |

2025 |

|

Product |

Biopsy Guidance Systems |

29.8% |

2025 |

|

Application |

Breast Biopsy |

🔒 |

2025 |

|

Guidance Technique |

Ultrasound-guided Biopsy |

🔒 |

2025 |

| End-User | 🔒 | 🔒 | 2025 |

|

Region |

North America |

39.6% |

2025 |

By Procedure Type

Surgical Biopsy commands a 54.6% majority share in 2025, anchored by its diagnostic gold-standard status for many tumour types where excisional or incisional sampling provides definitive histopathology. The segment benefits from preference in complex breast, lymph-node, and lesion staging cases.

To access detailed market analysis, Request Sample

Needle Biopsy at 45.4% in 2025 is the faster-growing procedure type, supported by core-needle and vacuum-assisted techniques. The segment's appeal stems from outpatient compatibility, lower complication rates, and lower cost-per-procedure versus open surgical biopsy.

By Product

Biopsy Guidance Systems dominate at 29.8% in 2025, reflecting the capital-intensive nature of stereotactic, ultrasound, and MRI-guided platforms. Hologic, BD (Bard), and Mammotome lead the breast guidance market, while GE and Siemens lead broader imaging-integrated platforms.

Biopsy Needles at 24.6% and Needle-Based Biopsy Guns at 19.3% together represent a significant share of the product market in 2025, scaling with overall procedure volumes. Biopsy Forceps at 14.2% serve endoscopic gastroenterology and pulmonology, while Others at 12.1% include vacuum-assisted consumables and accessories.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

39.6% |

High cancer screening rates, broad reimbursement, Hologic and BD home market |

|

Europe |

26.3% |

EU MDR-driven device upgrades, national screening programmes, and ageing population |

|

Asia Pacific |

22.8% |

China hospital-tier expansion, India private diagnostics, Japan screening adherence |

|

Latin America |

6.1% |

Brazil and Mexico private hospital growth, expanding cancer screening initiatives |

|

Middle East & Africa |

5.2% |

GCC oncology infrastructure, Saudi Vision 2030 healthcare investment, South Africa growth |

North America commands a 39.6% revenue share in 2025, the most dominant regional position globally. The US records over 2 million new cancer cases annually per ACS 2024 estimates, with broad Medicare and private insurance coverage of biopsy procedures. Hologic and BD's domestic presence further anchors regional share.

Europe holds 26.3% in 2025, driven by national cancer screening across the UK, Germany, France, and Nordics, alongside EU MDR-driven upgrades. Asia Pacific at 22.8% is the fastest-growing region, led by China's hospital-tier expansion, India's private diagnostic chains, and Japan's screening adherence under universal coverage.

Latin America at 6.1%, is anchored by Brazilh's SUS expansion and Mexico's private oncology growth. MEA at 5.2% is led by GCC oncology infrastructure, Saudi Vision 2030 healthcare allocation, and South Africa's private hospital networks.

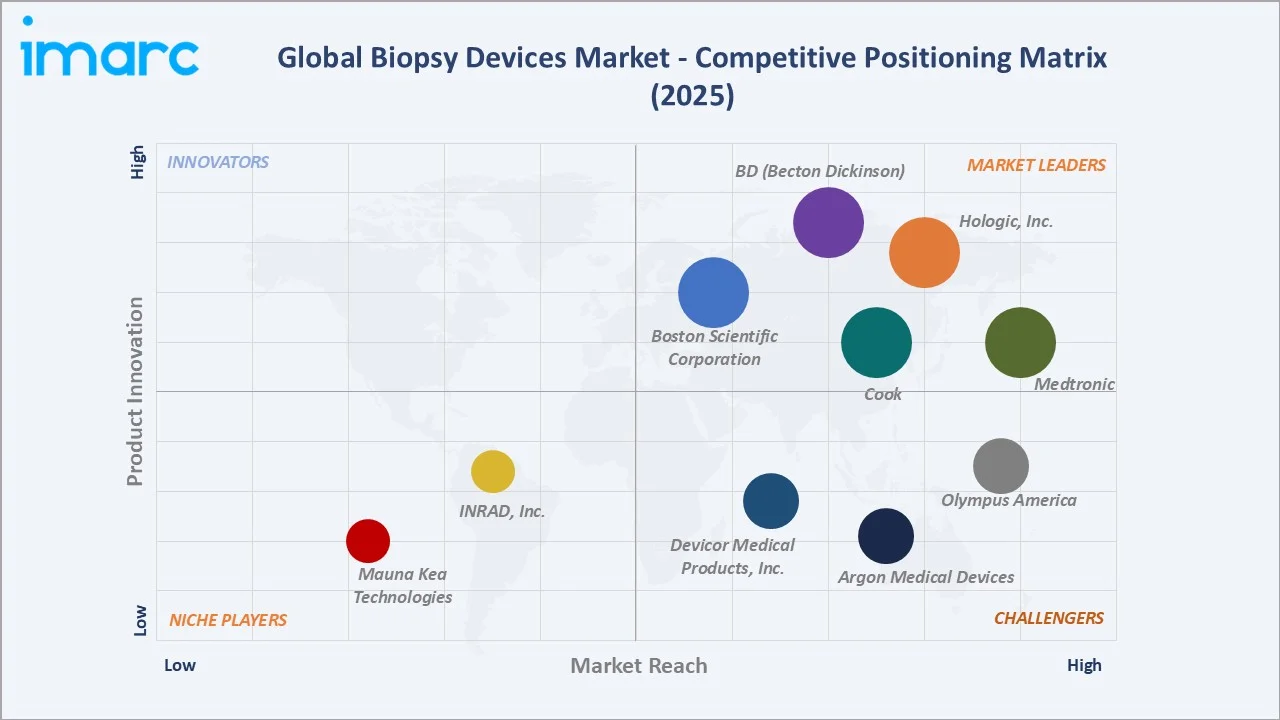

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Position |

Core Strength |

|

BD (Becton Dickinson) |

EnCor Enspire, Magnum |

Leader |

Vacuum-assisted biopsy, core-needle, broad portfolio |

|

Hologic, Inc. |

Brevera, Eviva, ATEC |

Leader |

Breast biopsy guidance, vacuum-assisted, AI-enabled |

|

Boston Scientific Corporation |

Expect, Acquire |

Leader |

Endoscopic biopsy, EUS-FNA, GI applications |

|

Cook |

EchoTip ProCore HD |

Leader |

Needle biopsy, EUS-FNA, interventional radiology |

|

Medtronic |

superDimension |

Leader |

Surgical and core-needle biopsy, broad GI portfolio |

|

Olympus America |

EZ Shot 3 Plus |

Challenger |

Endoscopic biopsy, gastroenterology focus |

|

Argon Medical Devices |

BioPince Full Core, SuperCore |

Challenger |

Core-needle biopsy systems, interventional radiology |

|

Devicor Medical Products, Inc. |

Mammotome Elite |

Challenger |

Breast vacuum-assisted biopsy, image-guided |

|

INRAD, Inc. |

INRAD Core biopsy needles |

Emerging |

Specialty biopsy needles, niche oncology focus |

|

Mauna Kea Technologies |

Cellvizio |

Emerging |

Optical biopsy, real-time in-vivo cellular imaging |

The competitive landscape features a small core of global biopsy device leaders dominating breast, prostate, and core-needle segments, complemented by emerging entrants in optical biopsy, AI-augmented platforms, and robotic-assisted biopsy.

Key Company Profiles

BD (Becton Dickinson)

BD is a global leader in biopsy devices, strengthened by its Bard Biopsy portfolio following the acquisition of C. R. Bard, Inc., offering a broad range of diagnostic and interventional solutions.

- Product & Platform Portfolio: EnCor Enspire vacuum-assisted breast biopsy, Magnum core-needle, Mission disposable, Achieve programmable, Finesse Ultra biopsy systems.

- Recent Developments: In January 2026, Becton Dickinson received FDA clearance for its EnCor EnCompass breast biopsy system, marking the official launch phase of its next-generation multi-modality platform.

- Strategic Focus: Vacuum-assisted breast biopsy leadership, core-needle expansion, and integration with imaging-guidance platforms across hospital and ambulatory settings.

Hologic, Inc.

Hologic is a leading provider of breast health solutions, specializing in advanced breast biopsy systems, imaging technologies, and AI-driven diagnostics for early cancer detection and women’s health.

- Product & Platform Portfolio: Brevera real-time breast biopsy, Eviva stereotactic, ATEC sapphire vacuum-assisted, Trident specimen radiography, ProFound AI.

- Recent Developments: In 2025, Hologic advanced its breast imaging portfolio through AI-driven solutions that improve workflow efficiency and support enhanced cancer detection and risk assessment.

- Strategic Focus: Breast biopsy leadership, AI-augmented breast imaging integration, vacuum-assisted innovation, and global commercial expansion.

Boston Scientific Corporation

Boston Scientific Corporation is a leading medical technology company specializing in minimally invasive devices, with strong capabilities in endoscopy and urology, particularly supporting biopsy procedures in gastrointestinal and prostate applications.

- Product & Platform Portfolio: Expect Slimline EUS-FNA, Acquire EUS-FNB, Captura biopsy forceps, Resolution clip with biopsy access.

- Recent Developments: In 2024, Boston Scientific announced plans to acquire Axonics, Inc. for $3.7 billion to expand its medical device portfolio and strengthen its position in minimally invasive therapies.

- Strategic Focus: Endoscopic biopsy leadership, EUS-FNA and EUS-FNB innovation, GI and pancreatic indication expansion.

Market Concentration Analysis

The global biopsy devices market is moderately-to-highly concentrated. The top five players, BD, Hologic, Boston Scientific, Cook Medical, and Medtronic, collectively account for approximately 55-65% of global revenue, with Olympus, and Argon Medical adding another 10-15%.

The landscape is segmented by clinical application. In breast biopsy, Hologic and BD dominate. In endoscopic biopsy, Boston Scientific, Cook Medical, and Olympus lead. In core-needle and IR biopsy, BD, Cook, and Argon share leadership. Emerging entrants are gaining ground in optical and robotic-assisted biopsy.

Investment & Growth Opportunities

Fastest-Growing Sub-Segments

Biopsy Guidance Systems is the highest-growth sub-segment, anchored by AI integration and MRI-guided adoption. Liquid biopsy as an adjacent category is growing at over 14% CAGR through 2030.

Emerging Market Expansion

China, India, Brazil, and Indonesia represent the highest-potential emerging markets, driven by hospital expansion in China, the rapid growth of private diagnostic chains in India, and strengthening oncology infrastructure in Brazil, collectively creating significant incremental demand through 2030.

Venture & Private Investment Trends

Medical device private capital remained strong in 2024, reflecting sustained investor interest in high-growth medtech segments. Liquid biopsy companies, including Guardant Health, Natera, and Grail, have collectively raised substantial multi-billion-dollar funding across venture rounds and public listings since 2018, reflecting strong investor interest in the liquid biopsy ecosystem.

Future Market Outlook (2026-2034)

The global biopsy devices market forecast projects expansion from USD 2.94 Billion in 2025 to USD 4.77 Billion by 2034 at a CAGR of 5.36%, driven by image-guided systems, AI integration, and emerging-market screening expansion.

Three structural discontinuities will reshape the industry through 2034. AI-augmented guidance systems will compress procedure time and improve targeting accuracy. Liquid biopsy will continue to complement, not replace, tissue biopsy. Robotic-assisted platforms will move from early adoption to mainstream in tertiary centres.

By 2034, the biopsy industry will have completed a partial transformation toward integrated, AI-enabled, image-guided platforms, with ~30-40% of incremental value captured by software, AI, and digital workflow solutions rather than disposables alone.

Research Methodology

Primary Research

Primary research included 40+ structured interviews in 2024-2025 with product directors at biopsy device manufacturers, interventional radiologists, oncology programme leads, GPO procurement leads, and institutional medical-device investors. Interviews validated market sizing, segmentation, and competitive positioning.

Secondary Research

Secondary sources included WHO GLOBOCAN cancer statistics, American Cancer Society reports, FDA, EU MDR registrations, OECD Health at a Glance, annual reports of listed players, industry journals, and McKinsey/Deloitte healthcare analyses through 2025.

Forecasting Models

Projections were derived using top-down and bottom-up models, cross-validated against cancer-incidence trajectories, hospital capex trends, reimbursement coverage data, and historical biopsy procedure volumes. Base, optimistic, and conservative scenarios were modelled.

Biopsy Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Procedure Types Covered | Surgical Biopsy, Needle Biopsy |

| Products Covered | Biopsy Guidance Systems, Needle Based Biopsy Guns, Biopsy Needles, Biopsy Forceps, Others |

| Applications Covered | Breast Biopsy, Lung Biopsy, Colorectal Biopsy, Prostate Biopsy, Others |

| Guidance Techniques Covered | Ultrasound Guided Biopsy, Stereotactic Guided Biopsy, MRI Guided Biopsy, Others |

| End Users Covered | Hospitals and Clinics, Academic and Research Institutes, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BD (Becton Dickinson), Hologic, Inc., Boston Scientific Corporation, Cook, Medtronic, Olympus America, Argon Medical Devices, Devicor Medical Products, Inc., INRAD, Inc., Mauna Kea Technologies, etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the biopsy devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global biopsy devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the biopsy devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Biopsy Devices Market Report

The global biopsy devices market was valued at USD 2.94 Billion in 2025, driven by rising cancer incidence, minimally invasive procedure adoption, and image-guided biopsy expansion.

The biopsy devices market is projected to reach USD 4.77 Billion by 2034, growing at a CAGR of 5.36% during 2026-2034, led by AI-guided systems.

Surgical Biopsy leads with a 54.6% share in 2025, anchored by its diagnostic gold-standard role for breast, prostate, and lymph-node tumour sampling globally.

North America dominates with a 39.6% revenue share in 2025, supported by high cancer screening rates, broad reimbursement, and Hologic and BD domestic presence.

Asia Pacific is the fastest-growing region, led by China's hospital-tier expansion, India's private diagnostics boom, and Japan's high cancer-screening adherence.

Top companies include BD (Becton Dickinson), Hologic, Inc., Boston Scientific Corporation, Cook, Medtronic, Olympus America, Argon Medical Devices, Devicor Medical Products, Inc., INRAD, Inc., and Mauna Kea Technologies.

Rising cancer incidence, minimally invasive procedure adoption, image-guided biopsy expansion, and liquid-biopsy innovation drive market growth across global oncology programmes.

Trends include AI-augmented guidance, liquid biopsy as a complementary modality, robotic-assisted platforms, MRI-guided mainstreaming, and vacuum-assisted biopsy standardisation in clinical practice.

Biopsy Guidance Systems lead with 29.8% share in 2025, driven by stereotactic, ultrasound, and MRI-guided platform demand and AI integration in breast workflows.

AI enables automated lesion detection, real-time targeting, and pathology correlation. Hologic's and GE's products are reference deployments.

Needle Biopsy holds 45.4% share in 2025 and is the faster-growing procedure type, supported by core-needle and vacuum-assisted techniques enabling outpatient compatibility.

Challenges include reimbursement variability, procedure complication risk, high equipment cost, EU MDR compliance burden, skilled operator shortages, and modality substitution risk.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)