Blood Bags Market Size, Share, Trends and Forecast by Product Type, Application, End User, Material, Capacity, and Region, 2026-2034

Global Blood Bags Market Size, Share, Trends & Forecast (2026-2034)

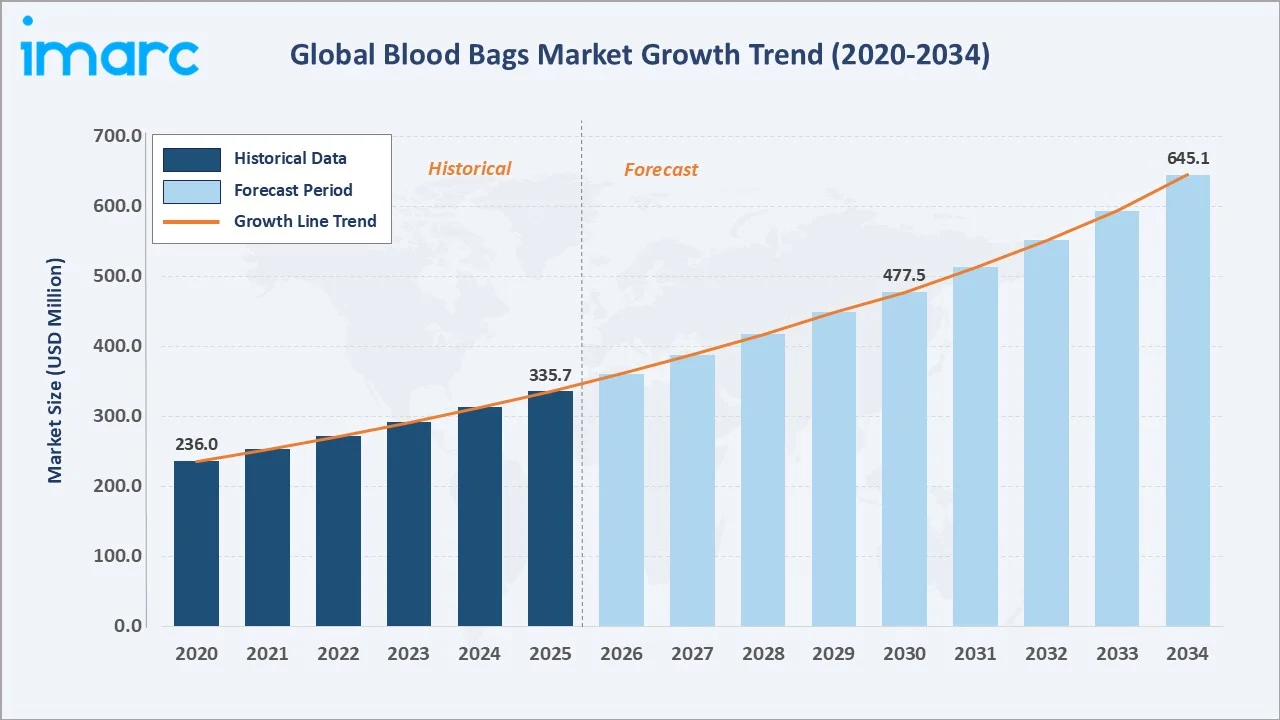

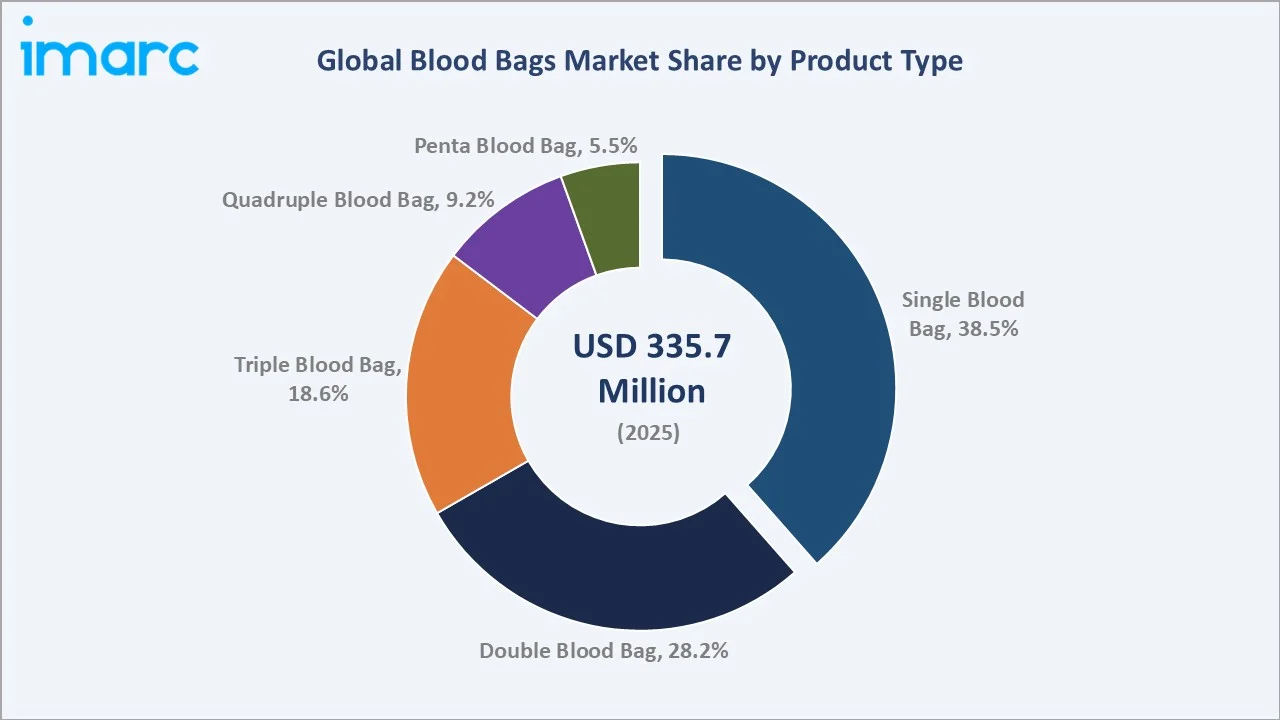

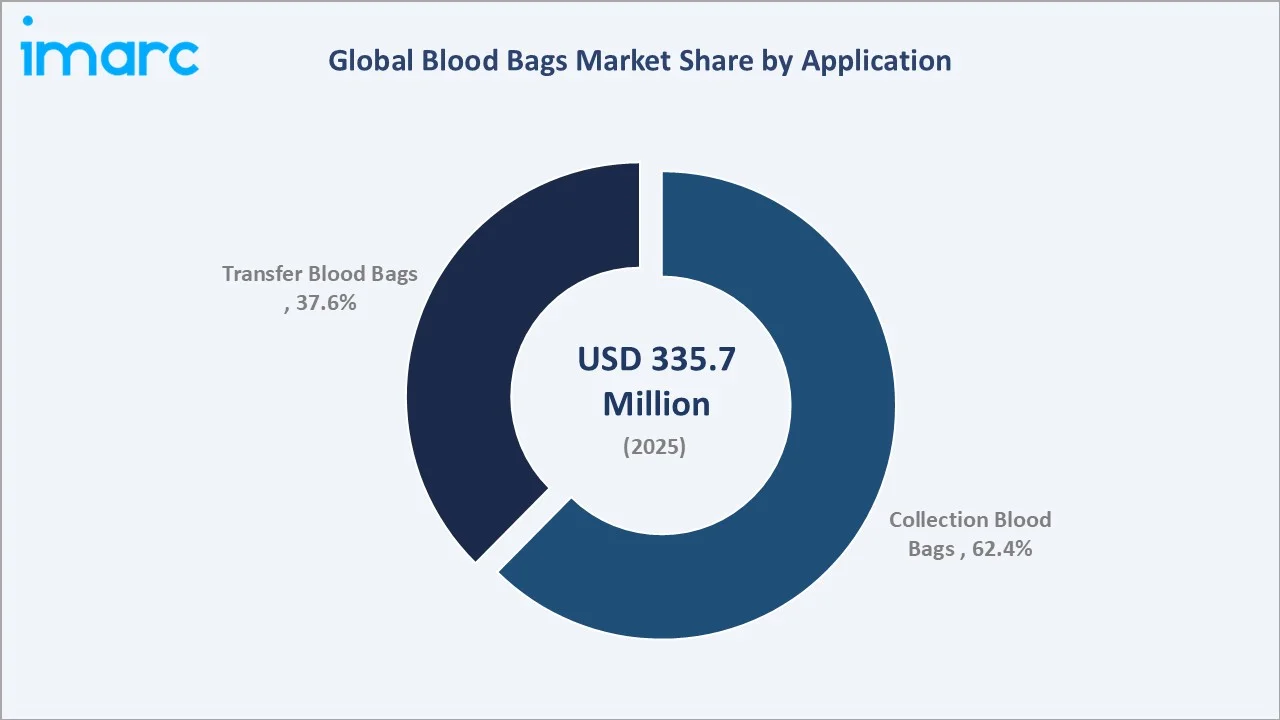

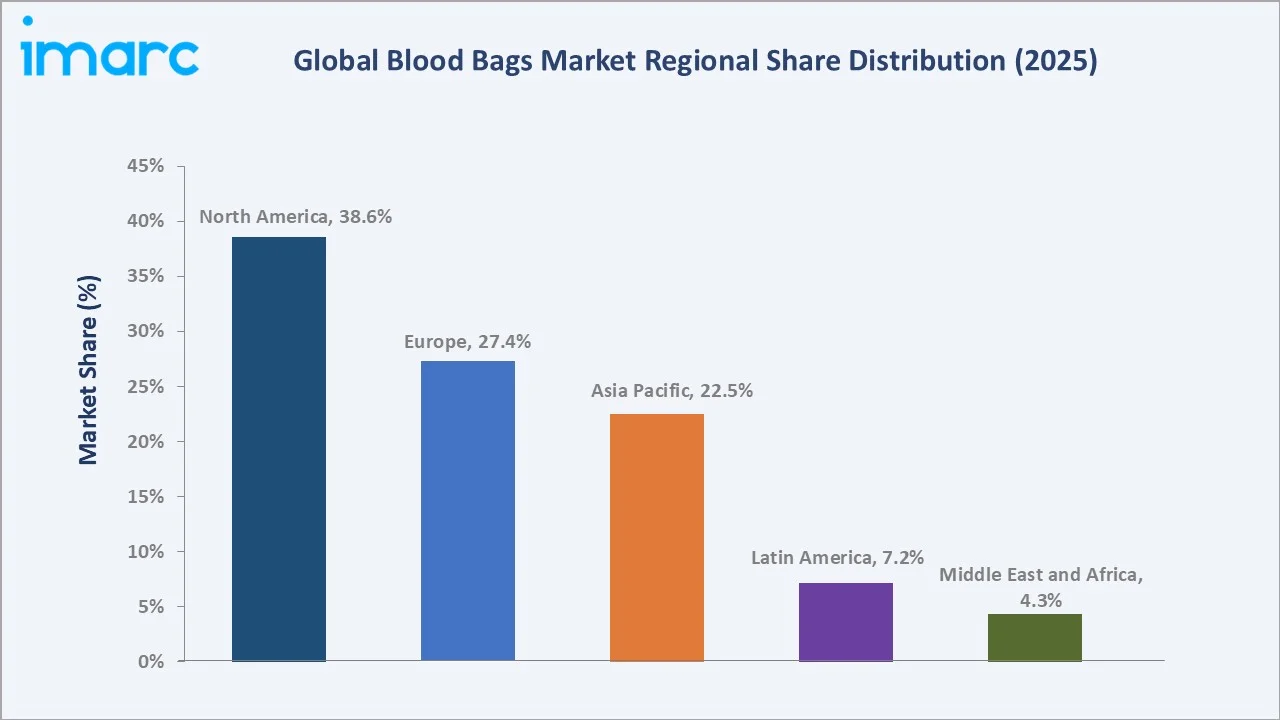

The global blood bags market size was valued at USD 335.7 Million in 2025 and is projected to reach USD 645.1 Million by 2034, exhibiting a CAGR of 7.30% during the forecast period 2026-2034. Rising global blood transfusion volumes, expanding healthcare infrastructure in emerging economies, and strict regulatory mandates on blood collection safety are the primary blood bags market growth drivers. Single Blood Bag leads product type at 38.5% in 2025, while Collection Blood Bags dominate application at 62.4%. North America commands 38.6% of global revenue in 2025, supported by an advanced hospital network and robust blood banking systems.

Market Snapshot

|

Metric |

Value |

| Market Size (2025) | USD 335.7 Million |

| Forecast Market Size (2034) | USD 645.1 Million |

| CAGR (2026-2034) | 7.30% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Largest Region | North America (38.6% share, 2025) |

| Fastest Growing Region | Asia Pacific (~9.2% CAGR, 2026-2034) |

| Leading Product Type | Single Blood Bag (38.5%, 2025) |

| Leading Application | Collection Blood Bag (62.4%, 2025) |

The global blood bags market growth trajectory from 2020 through 2034, reflecting steady historical expansion and a strong forecast curve powered by rising surgical volumes, trauma care expansion, and increased chronic disease management globally.

To get more information on this market, Request Sample

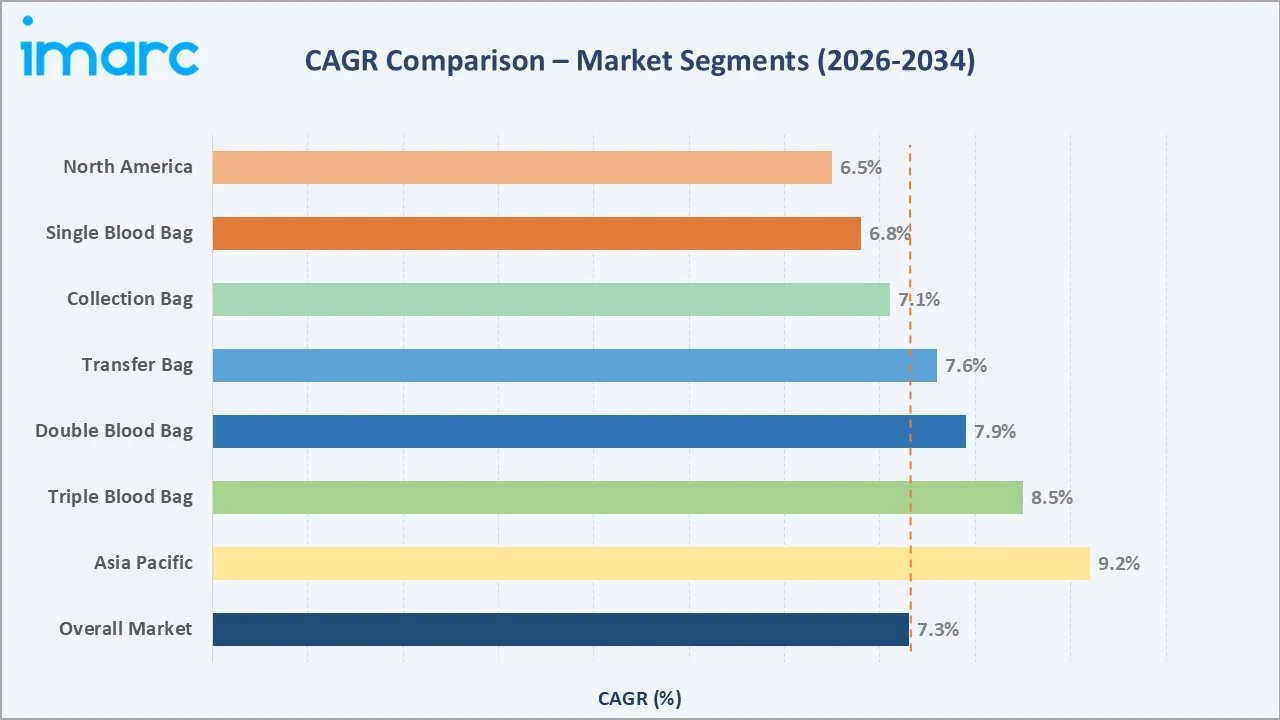

Segment-level CAGR comparisons highlighting Triple Blood Bags and Asia Pacific as the fastest-growing sub-categories within the global blood bags industry analysis through 2034.

Executive Summary

The global blood bags market is undergoing significant structural growth, driven by increasing demand for safe blood collection, storage, and transfusion systems worldwide. Valued at USD 335.7 Million in 2025, the market is forecast to reach USD 645.1 Million by 2034 at a CAGR of 7.30%. According to the World Health Organization (WHO), approximately 118.54 million blood donations are collected globally each year, creating sustained baseline demand for certified blood bag systems. Each unit of whole blood collected requires a minimum one blood bag assembly, with complex multi-component processing requiring triple or quadruple bag systems.

Single Blood Bags command the dominant product share at 38.5% in 2025, driven by widespread use in primary whole blood collection across general hospitals, blood banks, and mobile collection drives globally. Double Blood Bags, growing at approximately 7.9% CAGR through 2034, are gaining traction in plasma separation applications. Collection Blood Bags represent 62.4% of application revenue in 2025, reflecting their indispensable role across all transfusion medicine settings from high-income hospital blood banks to community-level donation centers.

North America holds the largest regional revenue share at 38.6% in 2025, underpinned by a highly organized blood banking infrastructure, with the American Red Cross alone supplying approximately 40% of the U.S. blood supply and collecting 6.8 million units annually in 2024. Asia Pacific at 22.5% share is the fastest-growing region, powered by expanding healthcare infrastructure in China and India. Europe contributes 27.4% share in 2025, supported by well-funded national health systems and stringent EU Blood Directive compliance requirements.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Single Blood Bag - 38.5% share (2025) |

|

Leading Application |

Collection Blood Bag - 62.4% share (2025) |

|

Leading Region |

North America - 38.6% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific - ~9.2% CAGR (2026-2034) |

|

Top Companies |

Fresenius Kabi, Terumo, Haemonetics, Maco Pharma, GRIFOLS |

|

Market Opportunity |

Multi-component bag systems in emerging markets; DEHP-free regulatory transition |

Key Analytical Observations Supporting The Above Data:

- Single Blood Bag's 38.5% product dominance in 2025 reflects its foundational role in primary whole blood collection at all donation settings globally - every blood donation drive, mobile collection, or hospital draw requires a minimum one certified single bag.

- Collection Blood Bags' 62.4% application leadership is anchored by WHO's data of 118.54 million annual global blood donations in 2024, each requiring a certified collection system, creating structurally inelastic baseline demand regardless of broader healthcare budget cycles.

- North America's 38.6% global revenue share in 2025 reflects the U.S. collecting approximately 13.6 million whole blood units annually, with FDA 21 CFR Part 606 quality system regulations ensuring only highest-standard certified blood bag systems are procured by licensed blood establishments.

- Asia Pacific's ~9.2% CAGR through 2034 reflects China's hospital network expansion under its 14th Five-Year Plan, India's 1.5 million new hospital beds target by 2030 under PM-Abhim, and rapidly growing voluntary donation programs across Indonesia, Vietnam, and the Philippines.

Global Blood Bags Market Overview

Blood bags are sterile, flexible plastic containers - typically produced from medical-grade PVC or polyolefin - designed for the collection, storage, processing, and transfusion of human whole blood and its components. The blood bags ecosystem spans upstream raw material suppliers (PVC plasticizer compounds, anticoagulant solutions, sterile tubing), bag manufacturers, sterilization specialists, distributors, and end-users including hospitals, blood banks, ambulatory surgical centers, and military medical units globally.

Applications span whole blood collection, plasma separation, platelet concentrate preparation, red cell processing, and component pooling for therapeutic and surgical use. Macroeconomic enablers include global surgical procedure volumes estimated at 313 million major surgeries annually per WHO 2023 data, increasing road traffic accident rates driving trauma care demand, growing prevalence of blood disorders including thalassemia and hemophilia across Asia, and expanding national blood transfusion service programs in Africa, South Asia, and Southeast Asia supported by WHO technical assistance.

Market Dynamics

To evaluate market opportunities, Request Sample

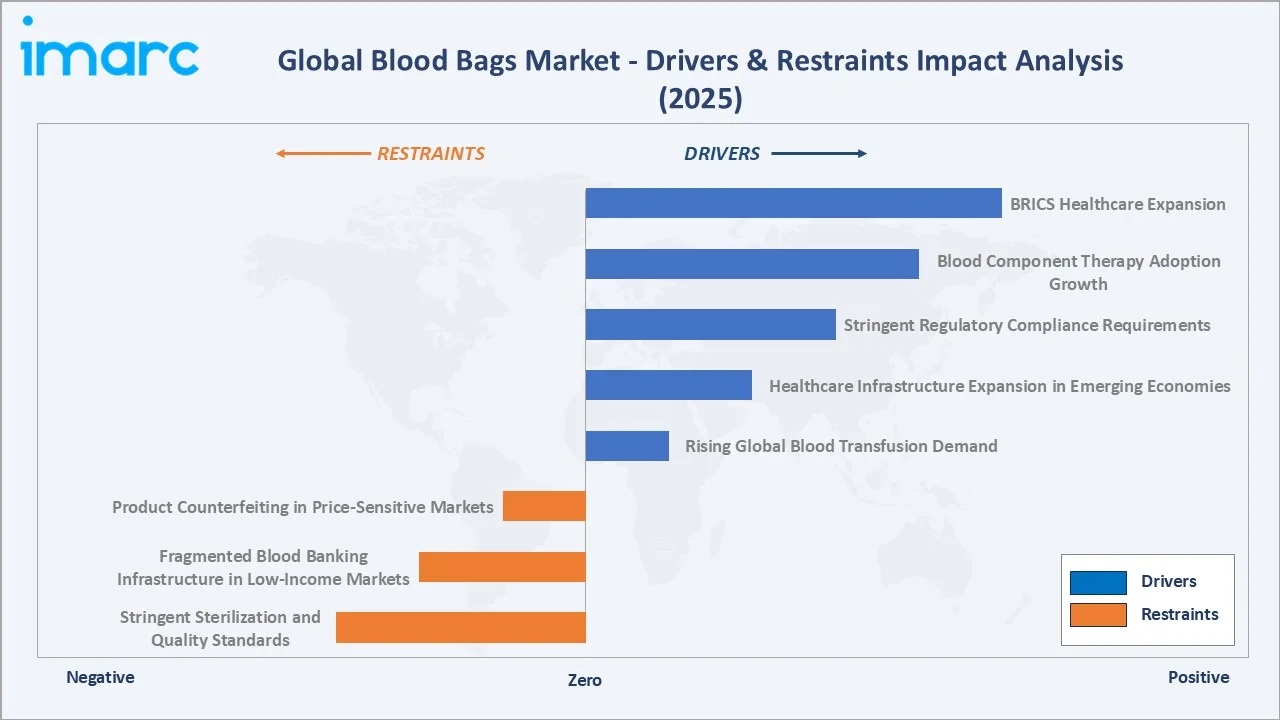

Market Drivers

- Rising Global Blood Transfusion Demand: WHO estimates 118.54 million blood donations collected annually worldwide, with transfusion medicine expanding across both high-income and emerging market healthcare systems. Surgical procedure growth, trauma care, oncology treatment, and obstetric care are the four largest transfusion demand categories.

- Healthcare Infrastructure Expansion in Emerging Economies: India's Ayushman Bharat program, China's Healthy China 2030 initiative, and ASEAN health system strengthening investments are collectively driving new hospital construction, blood bank establishment, and blood safety standard implementation - all generating certified blood bag procurement requirements at scale.

- Stringent Regulatory Compliance Requirements: FDA 21 CFR Part 606, EU Blood Directive 2002/98/EC, and WHO guidelines mandate use of certified, sterile, pyrogen-free blood bag systems in all licensed blood establishments. Compliance creates high-barrier recurring procurement that sustains revenue stability for leading manufacturers with established regulatory approvals.

- Blood Component Therapy Adoption Growth: Modern transfusion medicine increasingly favors component therapy - separating red cells, plasma, and platelets from donated whole blood. This drives demand for Double, Triple, and Quadruple blood bag systems, which are higher-value products growing at 7.9% to 8.8% CAGR through 2034 versus the market average.

Market Restraints

- Stringent Sterilization and Quality Standards: Compliance with ETO (ethylene oxide) sterilization regulations, biocompatibility testing per ISO 10993, and leachables and extractables validation adds significant cost and development time, restricting new entrant competitiveness and raising the cost base for existing manufacturers.

- Fragmented Blood Banking Infrastructure in Low-Income Markets: Inadequate cold chain logistics, unreliable power supply, and limited trained blood bank personnel constrain effective blood bag utilization in Sub-Saharan Africa and parts of South Asia, limiting market development despite high medical need.

Market Opportunities

- BRICS Healthcare Expansion: Brazil, India, and China are collectively investing in national voluntary blood donation programs and blood safety certification infrastructure, creating large-volume procurement opportunities for certified blood bag manufacturers with established regional distribution and local regulatory approvals.

- Premium Multi-Component Bag System Adoption in Mid-Tier Markets: Transition from single to triple and quadruple bag systems in mid-tier hospital segments across Asia Pacific and Latin America represents a significant revenue expansion opportunity as component therapy adoption grows in these markets through 2034.

- Military and Emergency Medical Services Demand: Battlefield blood transfusion requirements and mass casualty emergency protocols drive specialized blood bag procurement by defense medical services across NATO member states, the U.S. Department of Defense, and expanding Asia Pacific defense health programs.

Market Challenges

- Product Counterfeiting in Price-Sensitive Markets: Substandard and falsified blood bags pose patient safety risks in markets where procurement decisions favor cost over certified quality, creating competitive challenges for reputable manufacturers and regulatory enforcement challenges for national health authorities.

- Supply Chain Concentration Risk: Key raw material inputs including medical-grade PVC compounds, anticoagulant solutions, and sterile tubing connectors are sourced from a concentrated supplier base, creating supply disruption exposure under geopolitical or logistics stress - a vulnerability demonstrated during 2020-2021 COVID-19 global supply chain disruptions.

Emerging Market Trends

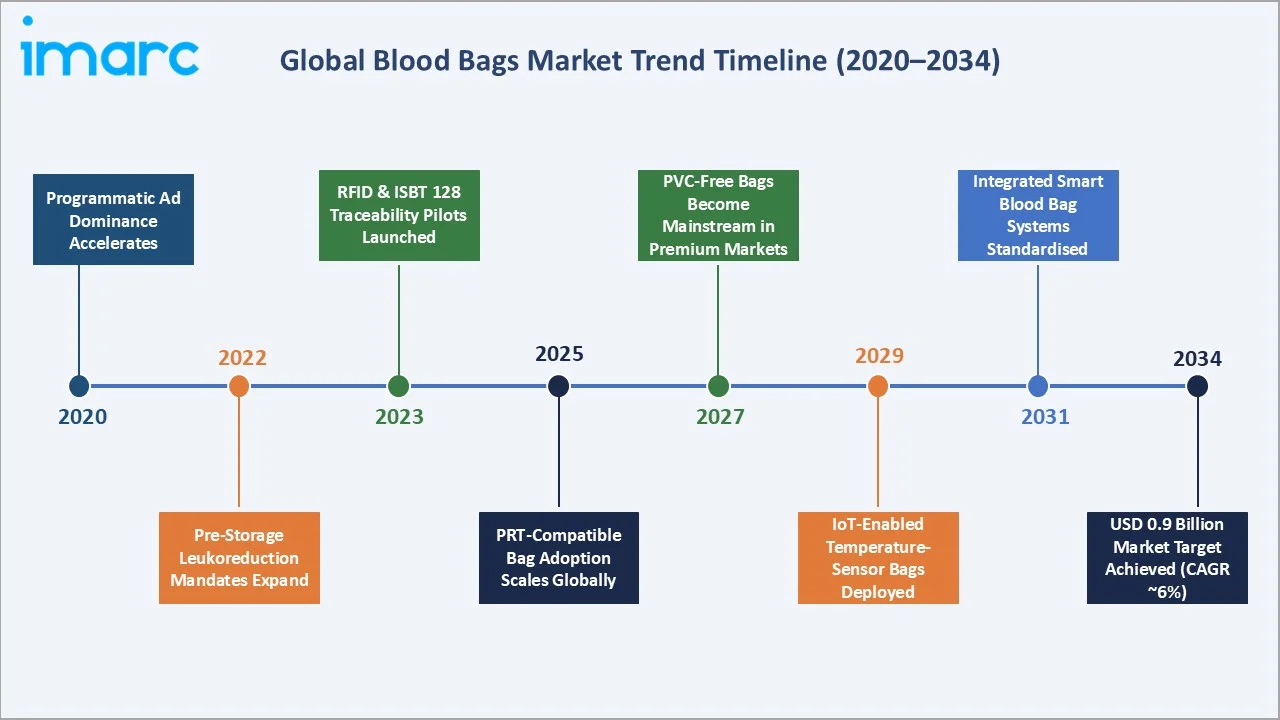

1. PVC-Free and DEHP-Free Blood Bag Development

Regulatory pressure in the EU and North America is accelerating development of DEHP-free blood bags using alternative plasticizers (DINCH, TOTM) and PVC-free materials including polyolefin and ethylene-vinyl acetate. Fresenius Kabi and Terumo have both commercialized DEHP-free bag lines, with EU adoption accelerating from 2023. This material transition expands addressable value per bag unit by 15-25% in premium regulated markets.

2. Integrated Leukoreduction Filtration Systems

Integration of leukoreduction filters directly into blood bag assemblies eliminates a separate filtration step, reducing labor cost and contamination risk. Pre-storage leukoreduction - now mandated in the UK, France, Canada, Germany, and Ireland - improves blood component quality and reduces febrile transfusion reactions. The integrated leukoreduction bag segment is growing at an estimated 10%+ CAGR in high-income markets through 2034.

3. RFID and Digital Traceability Integration

National blood safety authorities are mandating end-to-end blood traceability from donor to recipient. RFID-tagged and ISBT 128 barcode-integrated blood bags enable automated tracking across collection, processing, storage, and transfusion steps. The UK's SHOT framework and FDA blood establishment computer system regulations are accelerating adoption, with pilot IoT temperature-sensor embedded label programs deployed in 2024-2025 by European blood services.

4. Pathogen Reduction Technology (PRT) Compatible Bags

Pathogen reduction technologies - including Cerus Corporation's INTERCEPT and Terumo BCT's Mirasol systems - require especially compatible blood bag assemblies. PRT adoption is growing globally for platelet and plasma components, driven by emerging infectious disease risk awareness post-COVID-19. PRT-compatible bags represent a premium sub-category with significant volume growth potential in European and North American blood services through 2034.

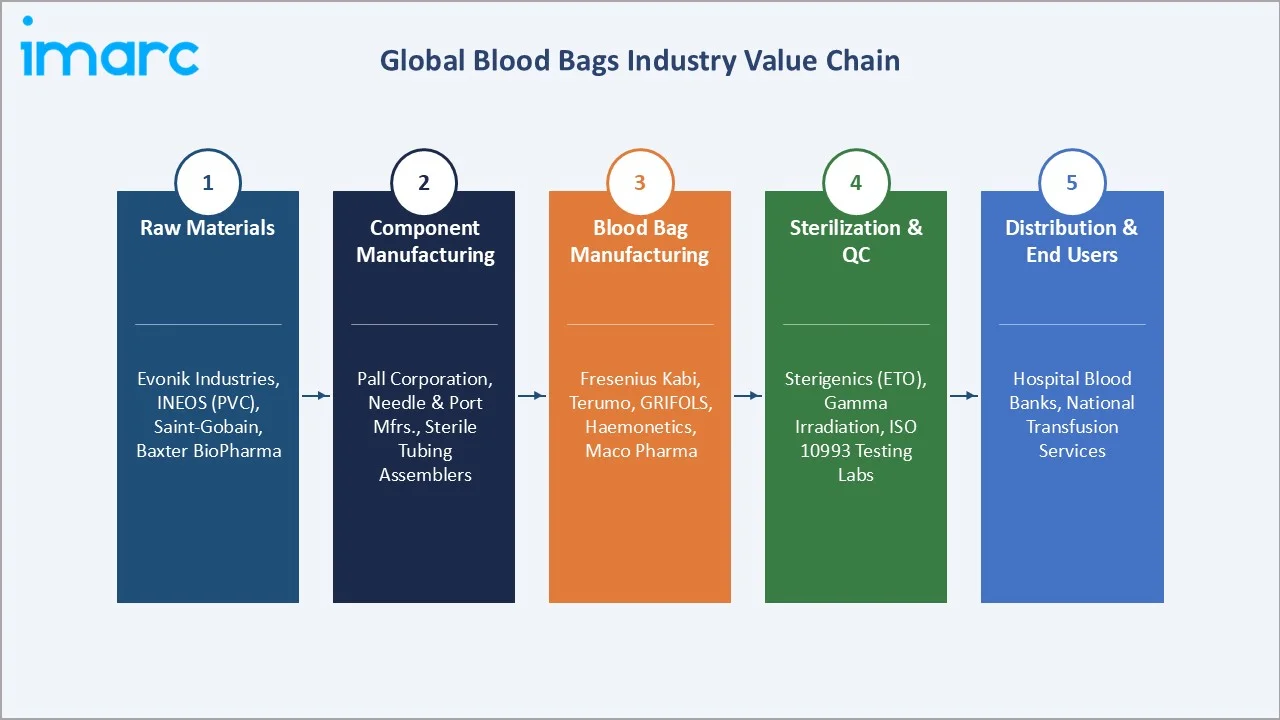

Industry Value Chain Analysis

The blood bags value chain spans five integrated stages from raw material supply through end-user deployment. Each stage involves distinct quality certification requirements, regulatory compliance obligations, and competitive dynamics shaping supplier relationships and pricing power across the global industry.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Evonik Industries (DINCH plasticizers), INEOS (PVC compounds), Baxter BioPharma Solutions (anticoagulants), Saint-Gobain (medical tubing) |

|

Component Manufacturer |

Needle and port manufacturers, filter media producers (Pall Corporation), sterile tubing assemblers, closure system suppliers |

|

Blood Bag Manufacturing |

Fresenius Kabi, Terumo Corporation, GRIFOLS, Haemonetics, Maco Pharma, SURU International, Neomedic |

|

Sterilization & QC |

Sotera Health/Sterigenics (ETO sterilization), in-house gamma irradiation, third-party ISO 10993 biocompatibility testing labs |

|

Distribution & End Users |

Medical device distributors; Hospital blood banks, national blood transfusion services, ambulatory surgical centers, military medical services |

Technology Landscape in the Blood Bags Industry

Material Innovation

Medical-grade PVC dominates at over 75% of production in 2025, valued for flexibility, clarity, and biocompatibility. Polyolefin bags offer superior gas permeability for platelet storage. TOTM and DINCH are the leading DEHP-replacement plasticizers in new product development pipelines at major manufacturers pursuing EU REACH compliance.

Anticoagulant and Additive Solutions

CPDA-1 supports 35-day red cell storage. Extended additive solutions (AS-1, AS-3, AS-5) enable 42-day storage, improving inventory management. Manufacturers are evaluating 56-day and 63-day storage solutions in clinical trials as of 2024-2025, with approvals anticipated by 2027-2030.

Filtration and Leukoreduction Technology

Pre-storage leukoreduction is now standard in North America, UK, France, Germany, and Ireland - reducing febrile reactions, CMV transmission, and HLA alloimmunization. Integrated in-line leukoreduction filter bags are the fastest-growing technology sub-category at 10%+ CAGR through 2034.

Smart Connectivity and Traceability

ISBT 128 barcode standardization is adopted across 88 countries. IoT temperature-sensor embedded labels are being piloted by European blood services in 2024-2025, enabling real-time cold chain monitoring from collection through transfusion - a first for the industry.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Single Blood Bag | 38.5% | 2025 |

| Application | Collection Blood Bag | 62.4% | 2025 |

| End User | Hospitals | 🔒 | 2025 |

| Material | Poly Vinyl Chloride Blood Bag | 🔒 | 2025 |

| Capacity | 300 ml Blood Bag | 🔒 | 2025 |

| Region | North America | 38.6% | 2025 |

By Product Type

Single Blood Bags lead global revenue with a 38.5% market share in 2025, serving as the standard collection vessel for whole blood donation worldwide. Their simplicity, low cost, and universal compatibility with collection protocols sustain dominance across all healthcare settings. Double Blood Bags represent 28.2% in 2025 and are growing at approximately 7.9% CAGR through 2034, driven by plasma separation demand in hospital blood banks upgrading component therapy capabilities.

To access detailed market analysis, Request Sample

Triple Blood Bags hold 18.6% share in 2025 and exhibit approximately 8.5% CAGR - the strongest product category growth rate - reflecting the global trend toward red cell, plasma, and platelet separation from single donations. Quadruple Blood Bags at 9.2% and Penta Blood Bags at 5.5% serve advanced blood processing centers handling high-volume multi-component therapeutic applications.

By Application

Collection Blood Bags dominate application revenue at 62.4% in 2025, reflecting their mandatory use at every blood donation event globally - from fixed blood bank facilities to mobile collection drives. With WHO reporting 118.54 million annual donations worldwide in 2024, collection bags represent a structurally inelastic demand category. Transfer Blood Bags account for 37.6% in 2025 and are growing as blood processing centers increasingly sub-divide collected whole blood into multiple therapeutic components requiring inter-bag transfer steps during processing.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers |

Regulatory Impact |

Major Companies |

|

North America |

38.6% |

13.6M annual blood units; organized blood banking; advanced hospital network |

FDA 21 CFR Part 606 |

Haemonetics, GRIFOLS, Fresenius Kabi |

|

Europe |

27.4% |

Universal healthcare systems; mandatory leukoreduction; DEHP-free transition |

EU Blood Directive 2002/98/EC |

Fresenius Kabi, Maco Pharma |

|

Asia Pacific |

22.5% |

China/India hospital expansion; rising voluntary donation programs |

National blood safety standards evolving |

Terumo, SURU International |

|

Latin America |

7.2% |

Brazil healthcare expansion; growing trauma care |

ANVISA regulations; PAHO guidelines |

International brands via regional distributors |

|

Middle East and Africa |

4.3% |

GCC hospital investment; WHO Africa blood safety programs |

WHO-aligned national standards |

International manufacturers via distributors |

North America's 38.6% global dominance in 2025 reflects the United States' world-class voluntary blood donation infrastructure. The American Red Cross and America's Blood Centers collectively supply approximately 95% of U.S. blood needs. FDA's stringent 21 CFR Part 606 quality system regulations ensure only highest-standard certified blood bag systems are procured by all licensed blood establishments nationally.

Europe at 27.4% is characterized by universal healthcare system procurement, mandatory leukoreduction in major markets (UK, France, Germany, Ireland, Canada), and accelerating DEHP-free blood bag adoption driven by EU REACH regulation restrictions on phthalate plasticizers. France, Germany, and the UK are the three largest European blood bag markets by revenue in 2025.

Asia Pacific's 22.5% share in 2025 and fastest-growing regional CAGR of approximately 9.2% through 2034 reflect China's 14th Five-Year Plan investments in healthcare infrastructure, India's expansion under PM-Abhim and National Blood Transfusion Council standards, and rapidly expanding hospital sectors across Indonesia, Vietnam, and Thailand driving new blood bank establishment.

Competitive Landscape

|

Company Name |

Brand / Platform |

Market Position |

|

Fresenius Kabi AG |

Fresenius Kabi Blood Bags |

Global Leader - broadest portfolio from single to penta system, DEHP-free range |

|

Terumo Corporation |

TERUFLEX / Terumo BCT |

Leader - strong Asia Pacific and global OEM presence; apheresis integration |

|

Haemonetics Corporation |

Haemonetics NexSys |

Leader - plasma collection and apheresis bag specialist; U.S. market dominance |

|

GRIFOLS S.A. |

GRIFOLS Blood Bags |

Challenger - plasma collection bag specialist with global blood center relationships |

|

Maco Pharma International |

Maco Pharma PRT-compatible |

Emerging - pathogen reduction compatible bag systems; European market focus |

|

SURU International |

SURU Blood Bags |

Emerging - cost-competitive supplier for Asia Pacific and MEA emerging markets |

Key Company Profiles

Fresenius Kabi AG

Fresenius Kabi is one of the world's largest blood bag manufacturers, with its Transfusion Technology division producing single-to-penta configurations, DEHP-free variants, and leukoreduction-integrated assemblies for 100+ countries.

- Product Portfolio: Single, double, triple, quadruple, penta systems; DEHP-free TOTM-plasticized bags; integrated leukoreduction sets; CPD, CPDA-1, SAG-M anticoagulant solutions.

- Recent Developments: Since the 1950s, DEHP has been used in blood bag systems to maintain softness, flexibility, and blood quality. However, the European Commission has decided to sunset DEHP in the second half of this decade. In response, Fresenius Kabi developed a blood bag system with a red cell storage bag made of PVC/BTHC (butyryl trihexyl citrate) material in 2023.

- Strategic Focus: Regulatory compliance leadership in the DEHP-free transition, integrated component therapy solutions, and geographic expansion into Asia Pacific and Latin America.

Terumo Corporation

Terumo's Blood and Cell Technologies division (Terumo BCT) produces blood bags, apheresis systems, and processing equipment used by blood banks in 160+ countries globally.

- Product Portfolio: TERUFLEX blood bag systems; Mirasol PRT-compatible bags; Terumo BCT apheresis platforms; cell therapy processing containers.

- Recent Developments: In October 2024, Terumo launched the Reveos™ Automated Blood Processing System in the United States to help blood centers meet blood and platelet supply needs while helping their staff work more efficiently. Carter BloodCare in Texas is getting ready to implement Reveos to manufacture platelets, red blood cells and plasma for transfusion.

- Strategic Focus: Integrated blood processing system platforms, PRT compatible bag development, and Asia Pacific market penetration through established regional infrastructure.

Haemonetics Corporation

Haemonetics is a U.S.-based blood management specialist serving ~2,000 hospital customers and blood centers globally, with leadership in the U.S. source plasma collection market.

- Product Portfolio: Whole blood and apheresis collection sets; plasma collection bags; NexSys PCS plasma platform; red cell storage systems; hospital blood management software.

- Recent Developments: In February 2026, Haemonetics Corporation announced U.S. Food and Drug Administration (FDA) 510(k) clearance for the NexSys PCS® Plasma Collection System with Persona® PLUS technology. Persona PLUS represents the next generation of Haemonetics' proprietary and patented Persona technology that tailors plasma collections to each donor for improved average plasma volume per donation.

- Strategic Focus: U.S. source plasma market leadership, hospital whole blood collection with software integration, and international blood bank automation for recurring revenue beyond hardware.

Maco Pharma International

Maco Pharma International is a French specialist focused on blood bag systems, leukoreduction filtration, and transfusion consumables, with strong EU market positions and expanding global distributor coverage.

- Product Portfolio: Standard and DEHP-free bags; LeukoLab integrated leukoreduction sets; BioSafe PRT-compatible bags; pediatric blood bags; plasma transfer bags.

- Recent Developments: In 2019, Maco Pharma launched their dual needle, FDA NDA approved cord blood collection bag in the United States. Maco Pharma has been a leading supplier of cord blood collection kits in Europe and across the rest of the world for over 15 years.

- Strategic Focus: DEHP-free leadership in EU markets, pathogen reduction compatible bag systems as a premium growth platform, and expanding MEA and Asia Pacific distributor partnerships.

Market Concentration Analysis

The global blood bags market exhibits moderate concentration. The top five players - Fresenius Kabi, Terumo, Haemonetics, and GRIFOLS - collectively account for approximately 55-65% of global revenue in 2025. Concentration is higher in North America and Europe (top 3 hold ~65-70% share) and lower in Asia Pacific and MEA where regional manufacturers compete on price.

Two structural dynamics coexist. In premium segments, DEHP-free, leukoreduction, and PRT technology differentiation concentrates revenue among leading innovators with established regulatory approvals. In price-sensitive emerging markets, fragmentation persists. Consolidation pressure is growing as sterile manufacturing scale, ETO sterilization infrastructure, and compliance costs increasingly favor larger players over mid-tier manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

Triple and Quadruple Blood Bags grow at ~8.5% and ~8.8% CAGR through 2034. Leukoreduction-integrated bags grow at 10%+ CAGR in high-income markets. DEHP-free bags are expanding at 12-15% CAGR in EU and North American regulatory environments as compliance timelines approach.

Emerging Market Expansion

Asia Pacific - particularly India, China, and ASEAN - is the largest emerging opportunity, with new hospital blood bank establishment and voluntary donation scale-up driving demand. India's National Blood Policy mandates improved safety standards. Africa's WHO and Gates Foundation-supported blood safety programs build a long-term procurement pipeline.

Venture & Private Investment Trends

Private equity activity in transfusion consumables has increased since 2022, targeting Asia Pacific blood bag manufacturers. DEHP-free material innovators and RFID traceability integration companies are attracting venture investment as the industry shifts from commoditized PVC bag production toward technology-enhanced blood management platforms.

Future Market Outlook (2026-2034)

The global blood bags market is projected to expand from USD 335.7 Million in 2025 to USD 645.1 Million by 2034 at a CAGR of 7.30% - a near-doubling of value. Growth is underpinned by emerging market volume expansion, product mix premiumization toward multi-component bag systems, and regulatory-driven transition to DEHP-free and leukoreduction-integrated products delivering higher per-unit revenue in developed markets.

The global leukoreduction mandate wave - already covering North America and major European markets - is projected to reach Asia Pacific's leading markets (China, Japan, South Korea, Australia) by 2028-2030, significantly increasing average bag system value per donation event in the world's fastest-growing regional market. By 2034, the industry is expected to have completed its evolution from commoditized PVC bag production to a differentiated technology-integrated blood management system market.

Research Methodology

Primary Research

Primary research encompassed structured interviews with blood banking professionals, hospital procurement directors, national blood transfusion service administrators, medical device regulatory specialists, and institutional investors in healthcare technology. Primary insights validated market sizing estimates, product adoption timelines, regulatory compliance requirements, and competitive positioning assessments across key geographies including North America, Europe, Asia Pacific, and Latin America.

Secondary Research

Secondary sources include WHO Global Status Report on Blood Safety and Availability 2024, FDA blood establishment database, EU Blood Directive compliance publications, ISBT (International Society of Blood Transfusion) standards and reports, AABB Technical Manual (latest edition), company annual reports, NIH transfusion medicine research, and trade publications including Transfusion Medicine Reviews, Vox Sanguinis, and medical device industry databases.

Forecasting Models

Market size estimations and projections were derived using top-down and bottom-up forecasting models incorporating blood donation volume growth data, hospital bed capacity expansion projections, transfusion rate trends by geography, healthcare expenditure indices, and regulatory adoption timelines. Scenario analysis (base, optimistic, and conservative) was applied to account for healthcare funding variability and regulatory transition timing uncertainty across emerging market regions.

Blood Bags Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Single Blood Bag, Double Blood Bag, Triple Blood Bag, Quadruple Blood Bag, Penta Blood Bag |

| Applications Covered | Collection Blood Bag, Transfer Blood Bag |

| End Users Covered | Hospitals, Clinics, Ambulatory Surgical Centers, Blood Banks, Others |

| Materials Covered | Poly Vinyl Chloride Blood Bag, Polyethylene Terephthalate Blood Bag, Others |

| Capacities Covered | 100ml Blood Bag, 150ml Blood Bag, 250ml Blood Bag, 300ml Blood Bag, 350ml Blood Bag, 400ml Blood Bag, 450ml Blood Bag, 500ml Blood Bag |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Singapore, Brazil, Mexico, Argentina, Turkey, South Africa, Saudi Arabia, UAE |

| Companies Covered | Fresenius Kabi AG, Terumo Corporation, Haemonetics Corporation, GRIFOLS S.A., Maco Pharma International, SURU International, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the blood bags market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global blood bags market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the blood bags industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Blood Bags Market Report

The global blood bags market was valued at USD 335.7 Million in 2025, driven by rising global blood donation volumes, healthcare infrastructure expansion, and blood safety regulatory compliance requirements.

The market is projected to reach USD 645.1 Million by 2034, growing at a CAGR of 7.30% during 2026-2034, driven by component therapy adoption, DEHP-free material transitions, and emerging market healthcare growth.

Single Blood Bags lead with 38.5% market share in 2025, driven by universal use in primary whole blood collection across hospitals, donation drives, and community blood banks globally.

Collection Blood Bags dominate at 62.4% application share in 2025, reflecting WHO's data of 118.54 million annual blood donations globally requiring certified collection systems for each unit collected.

North America leads with 38.6% share in 2025, supported by the U.S. collecting approximately 13.6 million whole blood units annually and stringent FDA quality system regulations governing blood bag procurement.

Asia Pacific is the fastest-growing region at approximately 9.2% CAGR through 2034, driven by China and India healthcare infrastructure expansion, new hospital blood bank establishment, and voluntary donation program growth.

Key drivers include rising global blood donation volumes, healthcare infrastructure expansion in emerging economies, blood component therapy adoption, and DEHP-free regulatory compliance requirements in EU and North America.

Leading companies include Fresenius Kabi AG, Terumo Corporation, Haemonetics Corporation, GRIFOLS S.A., Maco Pharma International, and SURU International, among other regional manufacturers.

DEHP-free blood bags replace the plasticizer DEHP with safer alternatives (TOTM, DINCH), addressing EU REACH regulatory restrictions and reducing patient exposure to endocrine-disrupting chemicals during transfusion procedures.

Leukoreduction removes white blood cells from collected blood, reducing transfusion reactions. Integrated leukoreduction filter blood bags combine this step into the bag assembly, growing at 10%+ CAGR in premium markets.

The global blood bags market CAGR is 7.30% during 2026-2034, reflecting sustained demand from healthcare expansion, blood safety standards, regulatory compliance investment, and component therapy adoption globally.

Pathogen reduction systems like INTERCEPT and Mirasol require especially compatible blood bag assemblies, creating a premium sub-segment growing rapidly in European and North American blood services as PRT adoption accelerates post-COVID-19.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)