Brazil Cosmetics Products Market Size, Share, Trends and Forecast by Product Type, Category, Distribution Channel, and Region, 2026-2034

Brazil Cosmetics Products Market Size & Forecast 2026-2034

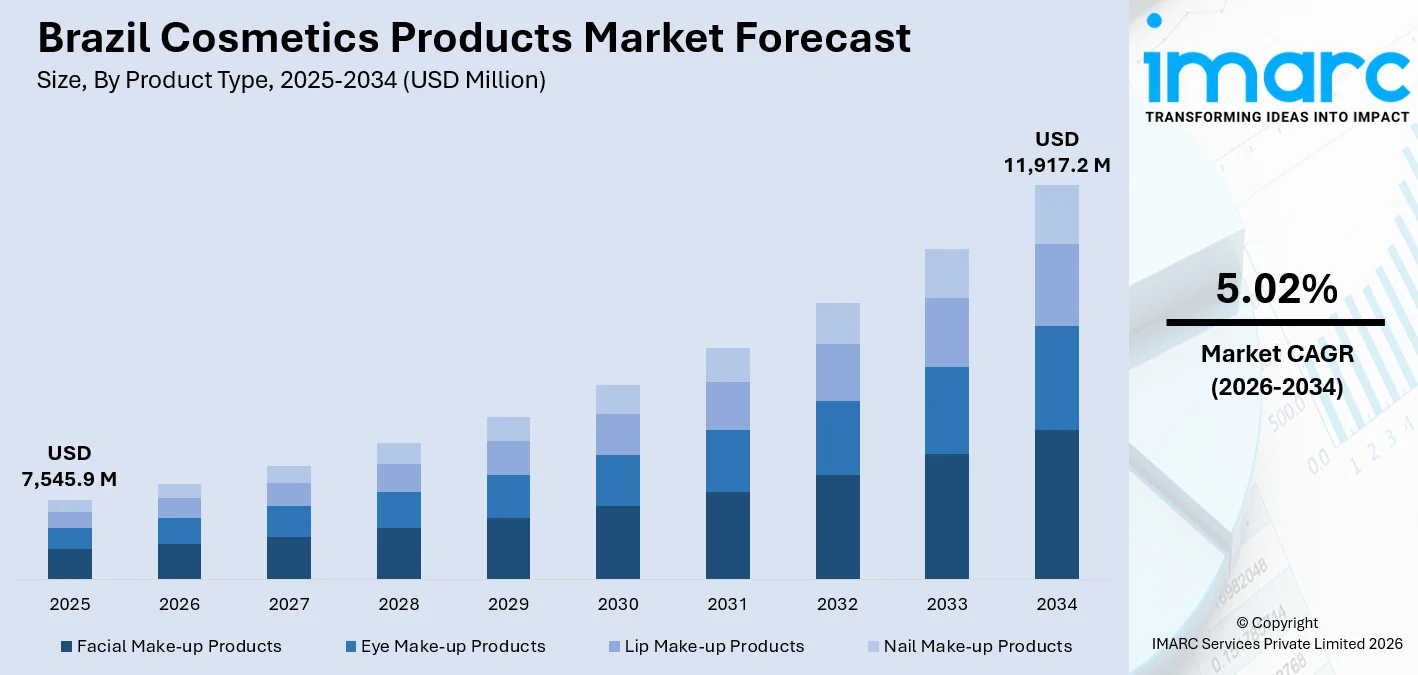

Brazil cosmetics products market size, valued at USD 7,545.9 Million in 2025, is projected to reach USD 11,917.2 Million by 2034, growing at a CAGR of 5.02% during 2026-2034, driven by rising middle-class spending, growing social media influence, and strong demand for inclusive beauty. Brazil's beauty sector recorded 12.7% value sales growth in 2024, underpinned by robust consumer commitment.

To get more information on this market Request Sample

Brazil Cosmetics Products Industry Analysis - Key Insights

- Facial make-up products lead at 34.6% by product type in 2025- foundation, blush, and bronzer anchor Brazil's makeup spend. Culturally ingrained face-focused beauty rituals, fueled by social media trends, keep this segment structurally ahead of eye and lip alternatives.

- Mass commands 72.1% by category in 2025- accessibility and scale define Brazil's cosmetics landscape. With over 55% of the population identifying as Black or mixed-race, demand for inclusive shade structurally privileges mass-market brands over premium alternatives.

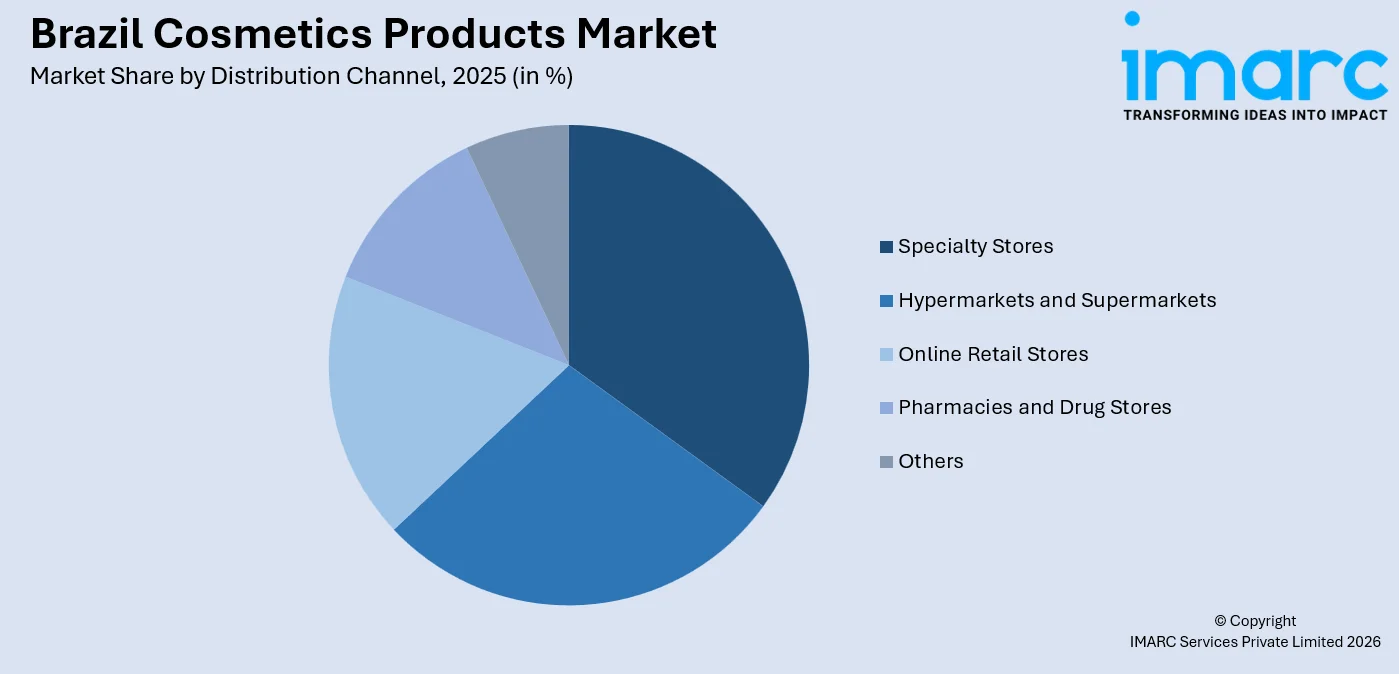

- Specialty stores dominate the distribution channel at 34.0% in 2025- the highest of any single channel, reflecting Brazil's high-touch beauty culture. In-store advisors, product sampling, and curated brand environments drive purchase conversions that hypermarkets and online platforms cannot easily replicate.

- Southeast drives 53.2% of regional demand in 2025- over half of Brazil's cosmetics revenue originates here, driven by São Paulo and Rio de Janeiro's dense urban populations, elevated per-capita income, and the country's deepest specialty retail network.

Brazil Cosmetics Products Market Trends and Dynamic 2026

Market Trends

Accelerating Shift Toward Natural and Clean Formulations

Consumer demand for transparent, ingredient-conscious formulations is reshaping Brazil cosmetics products market. In December 2024, Granado, a storied Brazilian beauty house backed by Puig, acquired 100% of Care Natural Beauty, a clean cosmetics brand targeting to operate 27 stores and 35 kiosks, generating BRL 270 million in revenue by 2028. This acquisition indicates that retailers are actively adapting to consumer-driven pressure for eco-conscious makeup alternatives.

Rising Category Momentum in Color Cosmetics and Lip Products

Color cosmetics in Brazil are experiencing broad-based acceleration, with Brazil's cosmetics products market trends pointing toward complexion and expression products. In 2024, Brazil’s lip cosmetics registered 47% growth, driven by a consumer shift toward expressive makeup aligned with diverse skin-tone representation. Multifunctional formats, tinted SPF balms, and dual blush-bronzer sticks are consolidating cross-category demand.

- Clean Beauty Adoption: Brazilian consumers are pivoting toward formulations free from parabens, sulfates, and synthetic additives, with clean beauty brands rapidly expanding their specialty retail footprint.

- E-Commerce Channel Growth: Online beauty retail is expanding 3x faster than in-store sales, powered by social influencers and digital-native consumers discovering makeup through curated content.

- Skin-First Hybrid Makeup: Foundations with SPF, tinted serums with hyaluronic acid, and balms with active ingredients are gaining rapid adoption across urban demographics.

- Inclusive Shade Innovation: Brands are broadening shade ranges to cater to Brazil's richly diverse skin tones, with Black and mixed-race consumers driving demand for better color-matched cosmetics.

Growth Drivers

Rising Middle-Class Spending and Demographic Dividend

Brazil's expanding middle class is a structural demand driver for the cosmetics products market. Tendências Consultoria estimated that the Brazilian middle-class households earning more than USD 550 monthly surpassed 50% of the total population for the first time in 2024. The IMF projected Brazil’s GDP per capita reached USD 10,578 in 2025, up from USD 10,252 in 2024, representing a 3.2% growth. This sustains consumer spending on cosmetics, which is expected to be well-supported over the coming years.

Export Competitiveness and International Brand Expansion

Brazil's cosmetics industry is developing a strong international commercial presence, reinforcing domestic production confidence. According to ABIHPEC, Brazilian cosmetics, toiletries & fragrances (CT&F) exports reached USD 927.3 million in 2024. This export momentum is attracting manufacturing investment domestically and reinforcing Brazil cosmetics products market growth.

- Social Media and Influencer Commerce: Brazil leads globally in beauty brand social engagement, with Sephora Brazil, Maybelline Brazil, and Mary Kay Brazil among the most-followed beauty brand accounts worldwide.

- Strong Consumer Beauty Commitment: 72% of Brazilian consumers say they would never stop buying cosmetics, 12 points higher than in the U.S., reflecting a structurally deep and resilient beauty demand base.

- Cultural Emphasis on Personal Appearance: Brazil's unique beauty identity, rooted in diversity and expressiveness, creates consistent category demand across demographics, income levels, and regional markets.

- Regulatory Modernization for Clean Products: Evolving ANVISA frameworks and the growing cruelty-free movement are creating structural incentives for product innovation and cleaner, safer cosmetics formulations.

Market Restraints

High Tax and Regulatory Burden: Brazil's complex, multi-layered tax system, including ICMS variations across states, imposes significant cost pressures on cosmetics manufacturers and importers. Compliance with ANVISA's extensive registration requirements diverts operational resources from product development, particularly for mid-sized domestic brands.

Currency Volatility and Import Dependence: A significant share of premium raw materials is imported, making the market vulnerable to BRL depreciation. Currency fluctuations directly inflate consumer prices and dampen demand in the mid-to-premium segment, creating persistent margin pressure for brands dependent on imported cosmetics inputs.

Counterfeiting and Informal Distribution: The prevalence of counterfeit cosmetics, particularly through informal retail channels in lower-income urban areas, undermines brand equity and poses consumer health risks. Brazil's large informal economy complicates quality enforcement and limits the effectiveness of standard distribution controls for legitimate manufacturers.

Brazil Cosmetics Products Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Product Type |

Facial Make-up Products |

34.6% |

2025 |

|

Category |

Mass |

72.1% |

2025 |

|

Distribution Channel |

Specialty Stores |

34.0% |

2025 |

|

Region |

Southeast |

53.2% |

2025 |

Product Type Insights

Facial Make-up Products - 34.6% Market Share (2025) | Leading Product Type

Facial make-up products anchor Brazil's cosmetics products market, comprising foundation, blush, bronzer, highlighter, and primer. The deeply ingrained Brazilian cultural tradition of face-focused self-presentation, amplified by social media beauty trends and rising dermocosmetics adoption, sustains this segment's structural leadership. In September 2024, Givaudan Active Beauty launched the [N.A.S.] Vibrant Collection in Brazil, featuring vegan botanical extracts for hybrid make-up, exemplifying the category's evolution toward multifunctional skin-care-infused formulations.

|

Segment Breakdown Facial Make-up Products (34.6%) · Eye Make-up Products · Lip Make-up Products · Nail Make-up Products |

Category Insights

Mass - 72.1% Market Share (2025) | Leading Category

The mass category's dominance reflects Brazil's economic structure, where a large and growing middle-class population is seeking accessible beauty at everyday price points. In July 2025, Brazil's federal government enacted a landmark ban on cosmetic animal testing, prompting mass brands to accelerate the development of vegan and cruelty-free product lines, reinforcing the mass segment's ability to remain competitive on both price and ethical credentials.

|

Segment Breakdown Mass (72.1%) · Premium |

Distribution Channel Insights

Access the comprehensive market breakdown Request Sample

Specialty Stores - 34.0% Market Share (2025) | Leading Distribution Channel

Specialty beauty stores maintain their position as the primary sales channel for cosmetics in Brazil, underpinned by the country's high-touch beauty culture. In October 2024, Care Natural Beauty expanded to all Sephora stores across Brazil, simultaneously announcing plans to open two Care-branded stores in 2025. This move underscores how emerging clean beauty brands view specialty retail as the pivotal launch channel for premium consumer engagement in the Brazilian market.

|

Segment Breakdown Specialty Stores (34.0%) · Hypermarkets and Supermarkets · Online Retail Stores · Pharmacies and Drug Stores · Others |

Regional Insights

Southeast - 53.2% Market Share (2025) | Leading Region

The Southeast region accounts for over half of the total cosmetics business in Brazil, with São Paulo and Rio de Janeiro being the business hubs of the national market. São Paulo is where most brand headquarters, specialty retail flagships, and logistics are centered to meet national supply chain demand. This business concentration, combined with higher-than-average household income and the densest e-commerce infrastructure, creates a disproportionate volume engine compared to population percentage.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 53.2% |

| Major States | São Paulo, Rio de Janeiro, Minas Gerais, Espírito Santo |

| Key Growth Drivers | Highest per-capita cosmetics spending, e-commerce leadership, specialty retail concentration, beauty brand headquarters |

| Outlook | Sustained market leadership with premiumization upside |

|

Regional Breakdown Southeast (53.2%) · South · Northeast · North · Central-West |

South:

South Brazil hosts a well-developed specialty beauty retail infrastructure, with Curitiba (Paraná) and Porto Alegre (Rio Grande do Sul) being key hubs. Grupo Boticário, a company based in Curitiba, derives significant sales from its O Boticário and Quem Disse Berenice brand franchise operations, which boast strong penetration in higher-income urban centers in this region.

|

Metric

|

Details

|

|---|---|

| Major States | Paraná, Santa Catarina, Rio Grande do Sul |

| Key Growth Drivers | Strong Grupo Boticário franchise network, above-average incomes, active specialty retail |

| Outlook | Stable growth anchored by domestic brand loyalty |

Northeast:

The Northeast is the second most populous region in Brazil and the second largest market in the country in terms of cosmetics products consumed, with Bahia, Pernambuco, and Ceará being the main markets. The door-to-door distribution of beauty and personal care products in Brazil, dominated by players like Natura and Avon, results in a disproportionate volume in the Northeast since there is a low density of physical specialty retail outlets in this region, but direct sales representatives are active to a significant extent.

|

Metric

|

Details

|

|---|---|

| Major States | Bahia, Pernambuco, Ceará, Maranhão, Rio Grande do Norte, Paraíba, Alagoas, Sergipe, Piauí |

| Key Growth Drivers | Door-to-door distribution strength, growing e-commerce adoption, rising aspirational beauty spend |

| Outlook | Fastest-growing region for e-commerce channel transition |

North:

North Brazil is a smaller yet growing cosmetics and personal care products market, with Pará and Amazonas being the main markets in this area. Manaus is the main distribution hub in this area due to its status as the largest city in this region of Brazil, and it is also a key distribution hub for various cosmetics and personal care products. With an untapped resource in Amazonian biodiversity, ingredients like açaí berries, cupuaçu butter, and andiroba oil, align with the growing trend of "clean" products globally.

|

Metric

|

Details

|

|---|---|

| Major States | Amazonas, Pará, Rondônia, Tocantins, Amapá, Roraima, Acre |

| Key Growth Drivers | Amazonian natural ingredients, growing urban middle class, e-commerce reach expansion |

| Outlook | Emerging market with niche biodiversity advantage |

Central-West:

Central-West Brazil, anchored by Brasília (Federal District), Goiânia (Goiás), and Campo Grande (Mato Grosso do Sul), is an increasingly important cosmetics market buoyed by strong government employment, growing middle-class incomes, and expanding retail infrastructure. In June 2024, Natura & Co launched Natura Ventures, a corporate venture capital fund of BRL 50 million, aiming to invest in up to 15 Brazilian beauty startups, with Central-West urban consumers among the target beneficiaries of these digital beauty innovations.

|

Metric

|

Details

|

|---|---|

| Major States | Mato Grosso, Mato Grosso do Sul, Goiás, Distrito Federal |

| Key Growth Drivers | Government employment base, growing specialty retail, and digital beauty adoption |

| Outlook | Steady growth supported by expanding urban middle class |

Market Outlook (2026-2034)

What is the future outlook of Brazil Cosmetics Products market?

Brazil Cosmetics Products market is expected to sustain steady revenue growth through 2034.

Brazil's cosmetics products market has strong foundations in demographic trends, growing digital commerce, and product development. Brazil's unparalleled dedication to beauty, growing middle-class population, and growing ingredient understanding will ensure sustained volume growth in makeup products. Clean Beauty Regulations, rising E-commerce Penetration, and multinational manufacturing investments will collectively drive the Brazil cosmetics products market forecast.

Brazil Cosmetics Products Market - Leading Key Players

Brazil cosmetics products market has strong competitive positioning with both local giants and established multinational companies. Local companies like Natura & Co and Grupo Boticario use their strong distribution and cultural connections, while multinationals like L'Oréal Brasil and Coty use their global product development and brand recognition to compete in Brazil cosmetics products market.

| Company | Leading Brands | Highlights |

|---|---|---|

|

Natura & Co Holding S.A. |

Natura, Avon |

Q2 2025 Latin America net income of BRL 445M; launched Natura Ventures fund (BRL 50 million) in June 2024, targeting 15 Brazilian beauty startups |

|

Grupo Boticário |

O Boticário, Quem Disse Berenice, Eudora, Vult, OUi Paris, Truss, The Beauty Box, Beleza na Web |

40% annual international growth in 2024; Gabriel Medina appointed brand ambassador for Clash men's fragrance in February 2025 |

|

L'Oréal Brasil Ltda. |

Maybelline, L'Oréal Paris, NYX Professional Makeup, Garnier, Lancôme, Kérastase, La Roche-Posay, Vichy |

New distribution center in São Paulo with double capacity; Maybelline Brazil among top beauty brand social accounts globally |

Some of the existing key players in the market are Avon Products Inc., Coty Inc., Unilever Brasil, Beiersdorf AG (NIVEA), The Estée Lauder Companies, Procter & Gamble Brasil, etc.

Latest Development & News

- In July 2025, Brazil's federal government enacted a historic nationwide ban on cosmetic animal testing, requiring ANVISA to update its product evaluation framework accordingly. The legislation positions Brazil among the leading global markets for cruelty-free cosmetics regulation, with all manufacturers and importers now required to adopt alternative testing methods for personal hygiene and cosmetics products commercialized in the country.

- In April 2025, Dove launched its first dedicated facial care line, Dove Regenerative, in Brazil. Developed after testing on more than 100 different Brazilian skin tones, the range features niacinamide and retinyl propionate as key active ingredients, targeting Brazil's rapidly expanding dermocosmetics segment and making premium-grade skincare actives accessible at mass-market price points.

- In March 2025, Lubrizol, in partnership with Suzano, pre-launched Carbopol BioSense in Brazil, the first fully biodegradable ingredient in the Carbopol line. The innovation marks a sustainable formulation milestone for Brazil's cosmetics industry, offering eco-friendly performance alternatives for make-up and personal care brands responding to growing consumer demand for green ingredients and circular beauty practices.

Brazil Cosmetics Products Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Facial Make-up Products, Eye Make-up Products, Lip Make-up Products, Nail Make-up Products |

| Categories Covered | Mass, Premium |

| Distribution Channels Covered | Hypermarkets and Supermarkets, Specialty Stores, Online Retail Stores, Pharmacies and Drug Stores, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil cosmetics products market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Brazil cosmetics products market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil cosmetics products industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Cosmetics Products Market Report

Brazil cosmetics products market was valued at USD 7,545.9 Million in 2025.

Brazil cosmetics products market is anticipated to reach a value of USD 11,917.2 Million by 2034.

Facial make-up products dominate the market with a share of 34.6% in 2025, driven by deep consumer investment in complexion, blush, and bronzer categories.

Mass dominates the market with a share of 72.1% in 2025, driven by affordability requirements across Brazil's diverse income spectrum, strong consumer commitment to regular beauty purchases, and the dominance of local and mass-oriented international brands.

Specialty stores dominate the market with a share of 34.0% in 2025, driven by Brazil's high-touch beauty culture, where in-store advisory services, product sampling, and curated brand discovery experiences.

Southeast leads the market with a share of 53.2% in 2025. São Paulo and Rio de Janeiro anchor this dominance through high consumer spending, extensive specialty retail infrastructure, and a dense concentration of major beauty brand headquarters serving the national supply chain.

Key trends include the rise of skin-first hybrid makeup, foundations, and K-beauty influence on Brazilian formulations. Growing male grooming cosmetics, refillable packaging initiatives, and AI-driven personalized beauty consultation tools are also reshaping consumer engagement and product development in Brazil.

Some of the major players in the market include Natura & Co Holding S.A., Grupo Boticário, L'Oréal Brasil Ltda., Avon Products Inc., Coty Inc., Unilever Brasil, Beiersdorf AG (NIVEA), The Estée Lauder Companies, Procter & Gamble Brasil, etc.

Growth is driven by the increasing influence of K-beauty trends, rising male grooming awareness, government investment in beauty manufacturing clusters, growing LGBTQIA+ community spending on cosmetics, and innovation in long-wear waterproof formulations suited to Brazil's hot and humid climate conditions, driving sustained product development.

Key challenges include persistent counterfeiting in informal markets, logistical complexity in serving Brazil's vast and geographically dispersed territory, currency volatility impacting import-dependent ingredient costs, and difficulty achieving consistent product quality across supply chains spanning from São Paulo to remote North and Northeast states.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade