Brazil EdTech Market Size, Share, Trends and Forecast by Sector, Type, Deployment Mode, End User, and Region, 2026-2034

Brazil EdTech Market Size, Share, Trends & Forecast (2026-2034)

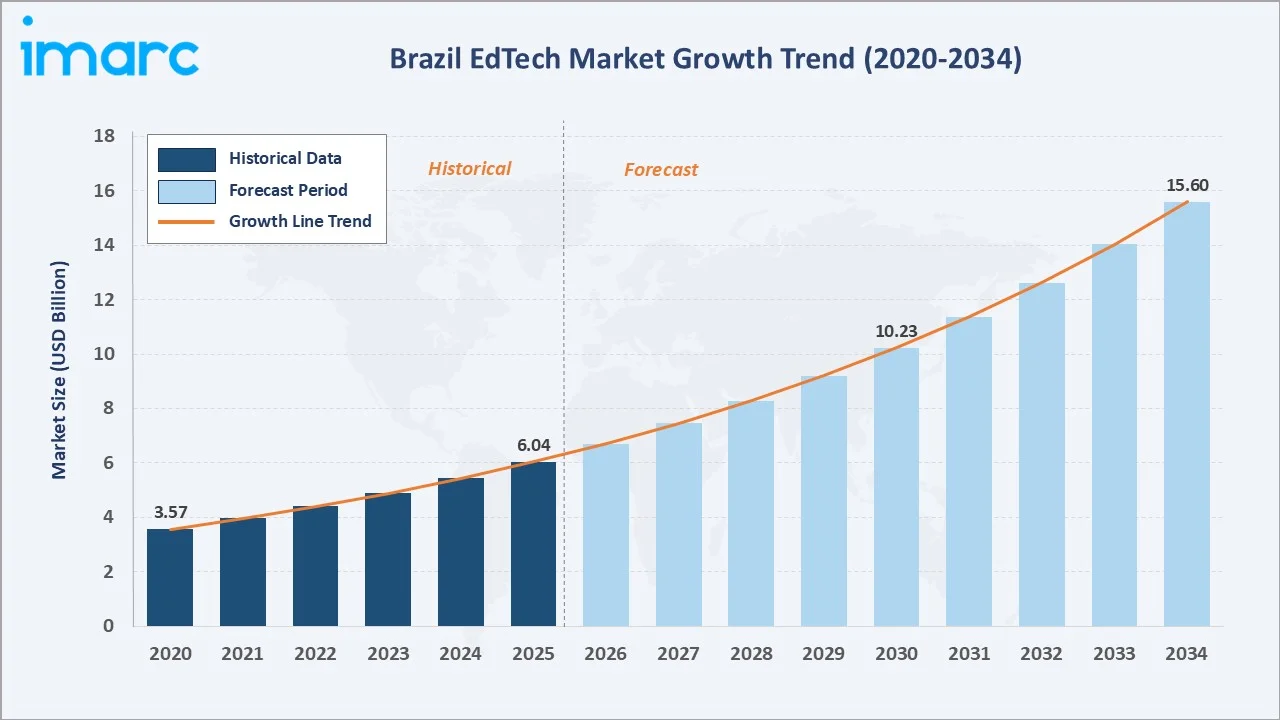

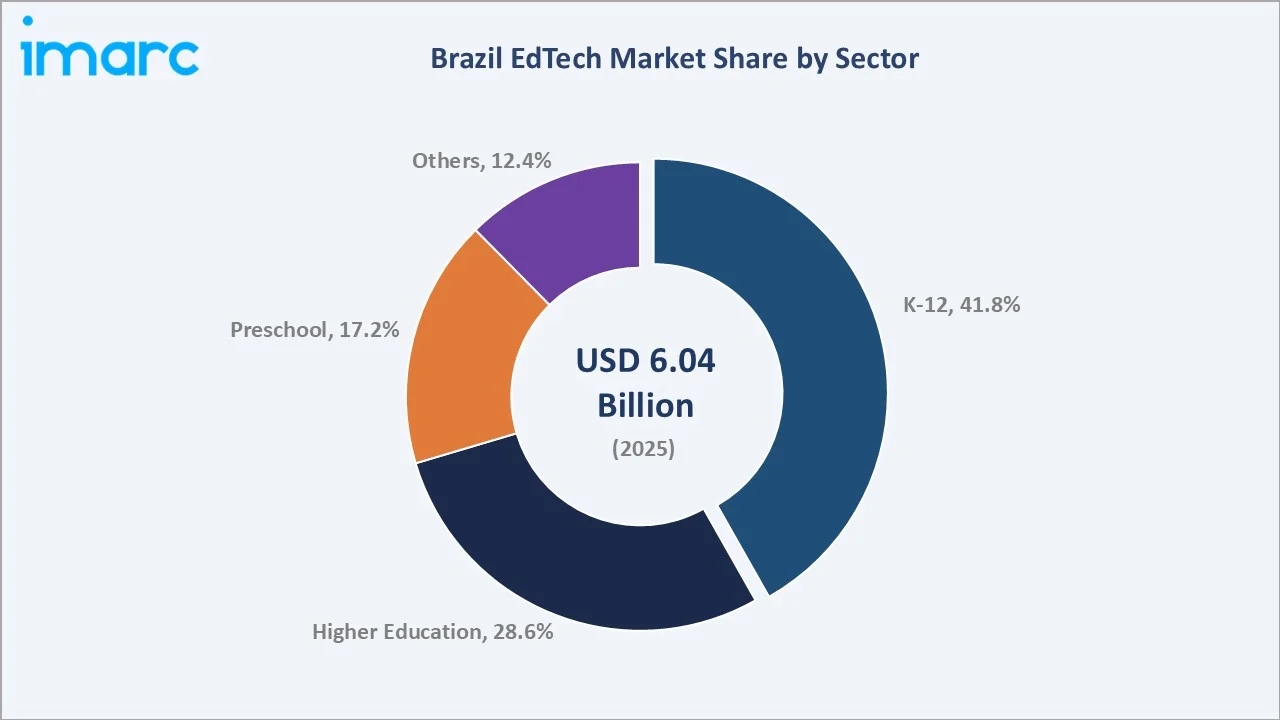

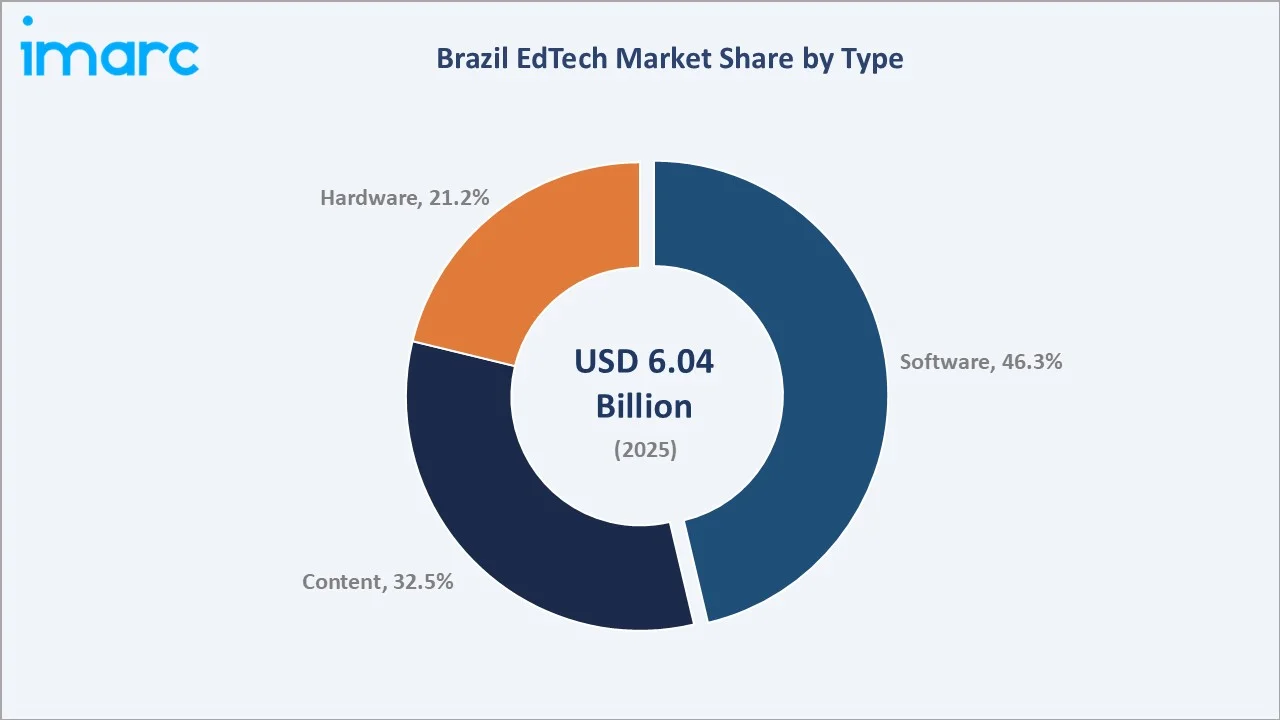

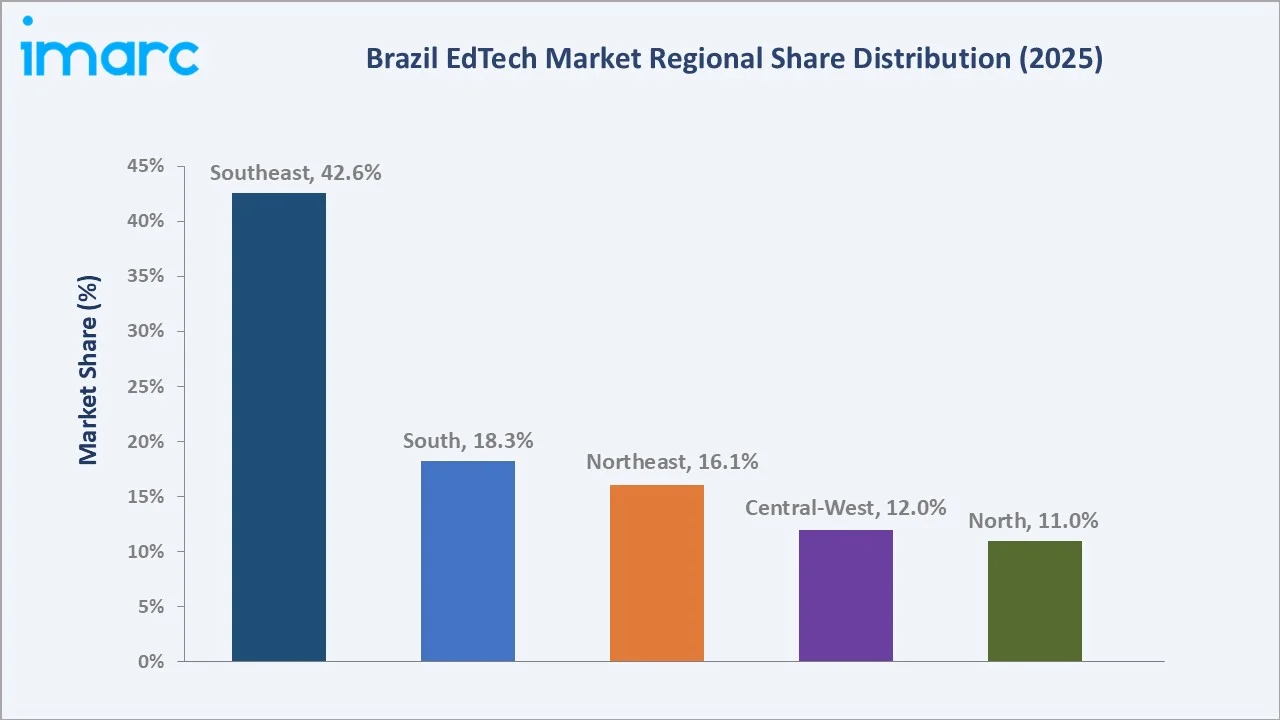

The Brazil EdTech market reached USD 6.04 Billion in 2025 and is projected to reach USD 15.60 Billion by 2034, growing at a CAGR of 11.12% during 2026-2034. The market is driven by rising internet and smartphone penetration, growing adoption of digital learning platforms, and strong demand for flexible, personalized, and remote education solutions. In 2024, around 167.5 million people aged 10 years and above in Brazil owned a mobile phone for personal use, representing 88.9% of this population group. Mobile phone ownership has increased steadily from 77.4% in 2016 to 87.6% in 2023 and further to 88.9% in 2024. Rural areas witnessed stronger growth, with ownership rising from 54.6% in 2016 to 77.2% in 2024. Higher mobile phone ownership, especially in rural areas, is helping bridge education access gaps and enabling students to participate in online classes, skill-development programs, and personalized learning services. K-12 leads the sector at 41.8%. Software dominates type at 46.3%. Southeast Brazil commands 42.6% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.04 Billion |

|

Forecast Market Size (2034) |

USD 15.60 Billion |

|

CAGR (2026-2034) |

11.12% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Sector |

K-12 (41.8%, 2025) |

|

Dominant Type |

Software (46.3%, 2025) |

|

Leading Region |

Southeast Brazil (42.6%, 2025) |

Brazil EdTech market expanded from USD 3.57 Billion in 2020 to USD 6.04 Billion in 2025, anchored at USD 10.23 Billion in 2030, and forecast to reach USD 15.60 Billion by 2034. COVID-19's school closure created Brazil's most commercially transformative single EdTech adoption event, with public and private schools transitioning to remote learning, creating permanent institutional familiarity with digital education tools above the pre-pandemic baseline.

To get more information on this market, Request Sample

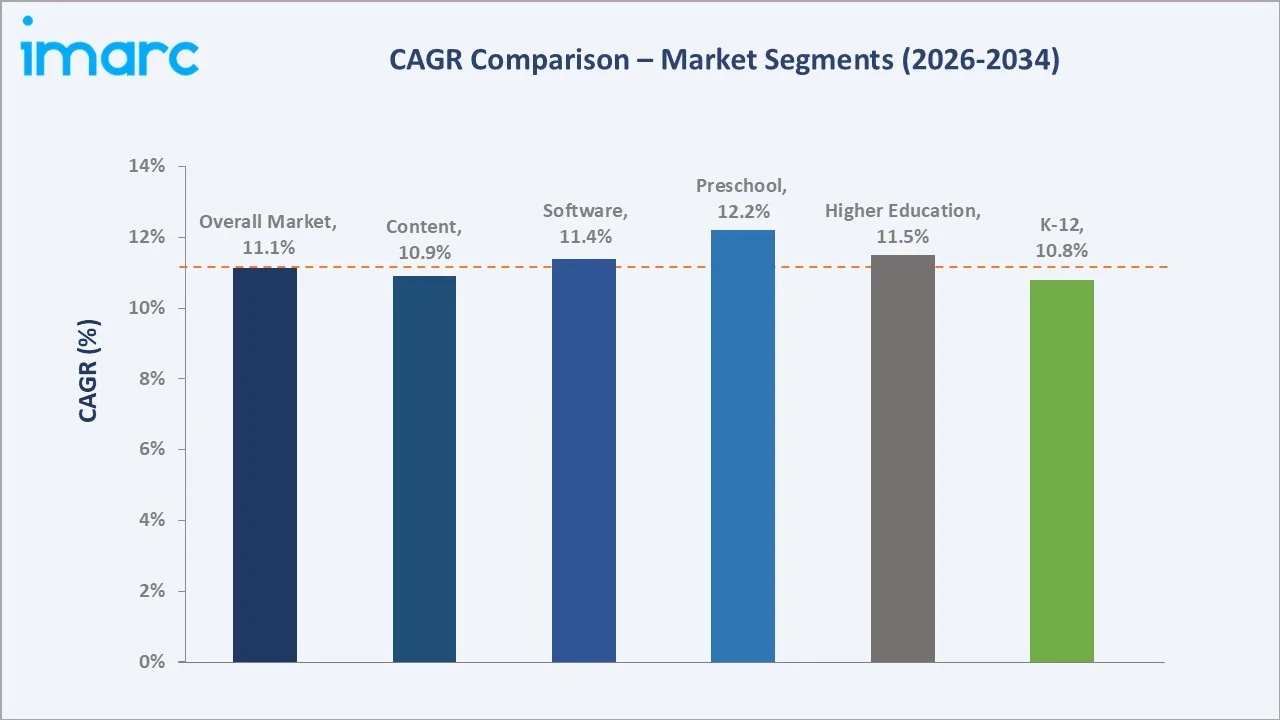

Preschool grows fastest at ~12.2% CAGR through early childhood digital education platform adoption. Software grows at ~11.4% CAGR through LMS, AI-adaptive learning, and SaaS administrative platform proliferation across Brazil's educational institutions.

Executive Summary

Brazil EdTech market at USD 6.04 Billion in 2025 represents Latin America's most commercially dynamic education technology investment destination, a market driven by the convergence of structural educational demand, progressive digital infrastructure investment, and a commercially vibrant startup ecosystem that has produced Brazil's first EdTech unicorn and attracted cumulative EdTech venture investments. The market is projected to reach USD 15.60 Billion by 2034.

K-12 at 41.8% leads through Brazil's K-12 students in schools, creating the most commercially volume-intensive institutional EdTech procurement segment. Software at 46.3% leads the type through SaaS LMS and adaptive learning platform dominance. Southeast Brazil leads regionally at 42.6%.

Key Market Insights

|

Insight |

Data |

|

Dominant Sector |

K-12 - 41.8% share (2025) |

|

Dominant Type |

Software - 46.3% market share (2025) |

|

Leading Region |

Southeast Brazil - 42.6% share (2025) |

|

Market Opportunity |

Distance learning expansion for underserved regions; AI-powered personalized learning; corporate upskilling SaaS; government digital school programs |

Key Analytical Observations Supporting The Above Data:

- K-12 at 41.8%: The K-12 segment dominates due to the country’s large school-age population, rising demand for digital classrooms, and increasing adoption of online tutoring, test preparation, and personalized learning platforms. Growing mobile and internet access is further enabling schools and students to use EdTech solutions for interactive and remote learning.

- Software at 46.3%: The software segment dominates as schools, universities, and training providers increasingly adopt learning management systems, virtual classrooms, assessment tools, and personalized learning platforms. Rising demand for scalable, cost-effective, and mobile-friendly digital education solutions is further strengthening software adoption.

- Southeast Brazil at 42.6%: Southeast Brazil dominates due to its strong concentration of schools, universities, corporate training centers, and technology startups. Higher digital infrastructure, internet penetration, and education spending further support faster adoption of EdTech solutions in the region.

Brazil EdTech Market Overview

Brazil EdTech market operates within the broader Latin American EdTech landscape as Brazil's dominant contributor, representing the highest regional revenue. The market's commercial uniqueness is its structural examination culture, creating EdTech demand above pure curriculum delivery.

The Brazil EdTech ecosystem integrates curriculum developers, technology platform providers, content aggregators, device manufacturers, and the regulatory framework. Macroeconomic factors include rising digitalization, expanding internet and smartphone penetration, and increasing demand for affordable, flexible education amid income and regional learning gaps.

Market Dynamics

To evaluate market opportunities, Request Sample

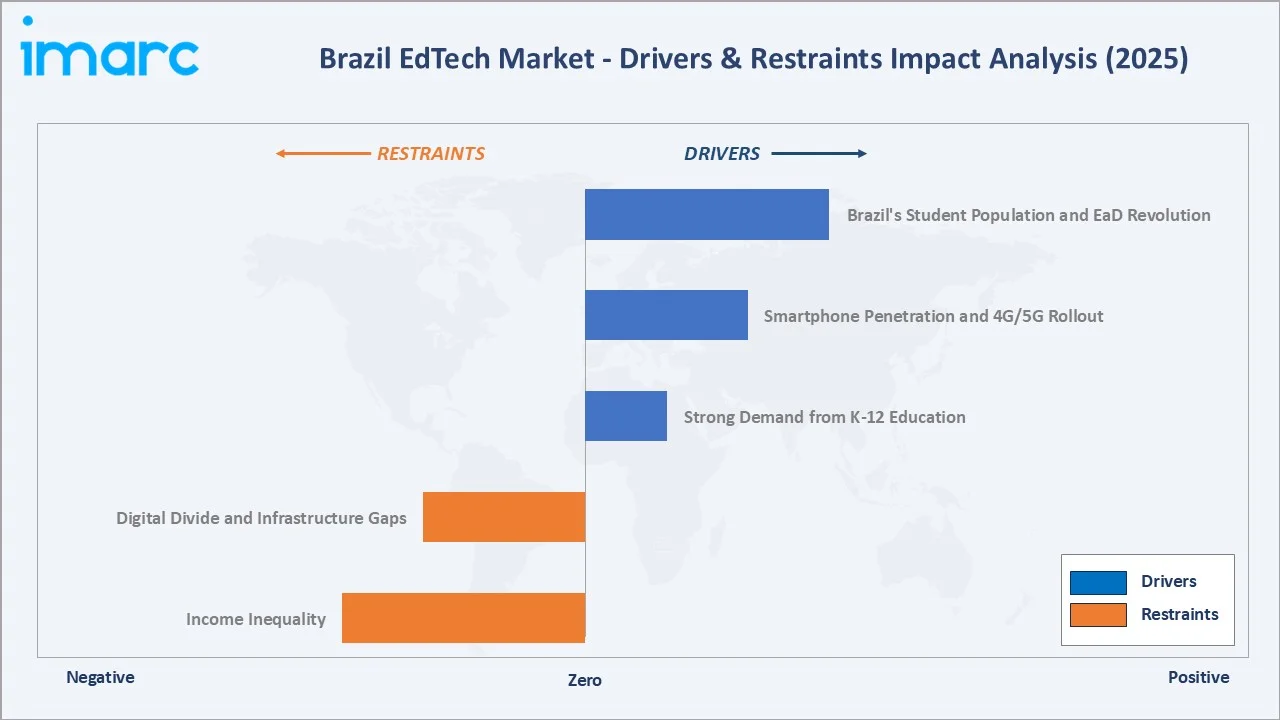

Market Drivers

- Brazil's Student Population and EaD Revolution: Brazil’s large student population is creating strong demand for scalable digital learning solutions across schools, universities, and professional training institutes. The rapid growth of EaD (Educação a Distância) is further expanding access to flexible, low-cost, and remote education. This is encouraging wider adoption of LMS platforms, virtual classrooms, digital content, and assessment tools. It is especially supporting learners in underserved and rural areas, thereby driving Brazil EdTech market growth.

- Smartphone Penetration and 4G/5G Rollout: In 2024, about 167.5 million people aged 10 and above in Brazil owned a mobile phone for personal use, representing 88.9% of this age group. Rural mobile ownership also rose sharply, increasing from 54.6% in 2016 to 77.2% in 2024. High mobile ownership enables students to use EdTech apps, video lessons, online tutoring, and LMS platforms anytime. Faster networks improve live classes, interactive content, and cloud-based learning experiences. This is especially helping rural and underserved regions to participate in remote and affordable education.

- Strong Demand from K-12 Education: Strong demand from K-12 education is driving the market as schools increasingly adopt digital classrooms, online assessments, learning apps, and interactive content. Rising parental focus on quality education and personalized learning is boosting the use of tutoring and test-preparation platforms. EdTech tools also help schools improve student engagement, track performance, and support hybrid learning models.

Market Restraints

- Digital Divide and Infrastructure Gaps: Digital divide and infrastructure gaps are limiting access to online learning in rural and low-income areas. Uneven internet connectivity, lack of devices, and poor broadband quality restrict students’ ability to attend virtual classes or use learning platforms. These gaps reduce EdTech adoption among underserved communities and widen learning inequalities.

- Income Inequality: Income inequality limits the ability of low-income households to pay for premium online courses, tutoring apps, and subscription-based learning platforms. Many students rely on free or low-cost solutions, reducing revenue opportunities for paid EdTech providers. This creates uneven access to quality digital education and slows adoption among underserved communities.

Market Opportunities

- AI Personalized Learning: AI personalized learning enables platforms to deliver customized lessons, assessments, and feedback based on each student’s performance. In March 2026, Brazil’s Ministry of Education introduced a national framework for the responsible use and development of AI in education. The 200-page framework guides institutions, educators, administrators, and policymakers, drawing on inputs from Brazilian authorities, organizations, peer countries, and academic research. It outlines principles and recommended practices to support the ethical, responsible, and socially beneficial integration of AI into education. It can help address learning gaps across diverse student groups and improve engagement in K-12, higher education, and upskilling programs. AI-driven tools also support scalable tutoring and adaptive learning at lower costs.

- Corporate EdTech and Professional Upskilling: Corporate EdTech and professional upskilling offer strong opportunities in Brazil as companies increasingly need digital, technical, and soft-skill training for employees. Online platforms help businesses deliver scalable, flexible, and cost-effective learning programs. Rising demand for reskilling in IT, finance, healthcare, and services further supports EdTech adoption. This creates growth potential for certification courses, microlearning, and enterprise LMS solutions.

Market Challenges

- Low Internet Quality in Rural and Remote Areas: Low internet quality in rural and remote areas limits access to online classes, video-based learning, and cloud-enabled educational platforms. Frequent connectivity issues disrupt learning experiences and reduce student engagement. This restricts the adoption of advanced digital education tools and creates disparities in educational access between urban and rural regions.

- Data Privacy and Cybersecurity Concerns: Data privacy and cybersecurity concerns challenge Brazil EdTech market as platforms collect large volumes of student, teacher, and payment data. Risks related to data breaches, unauthorized access, and misuse of minors’ information can reduce trust among schools and parents. Compliance requirements also increase operating costs for EdTech companies, especially smaller providers.

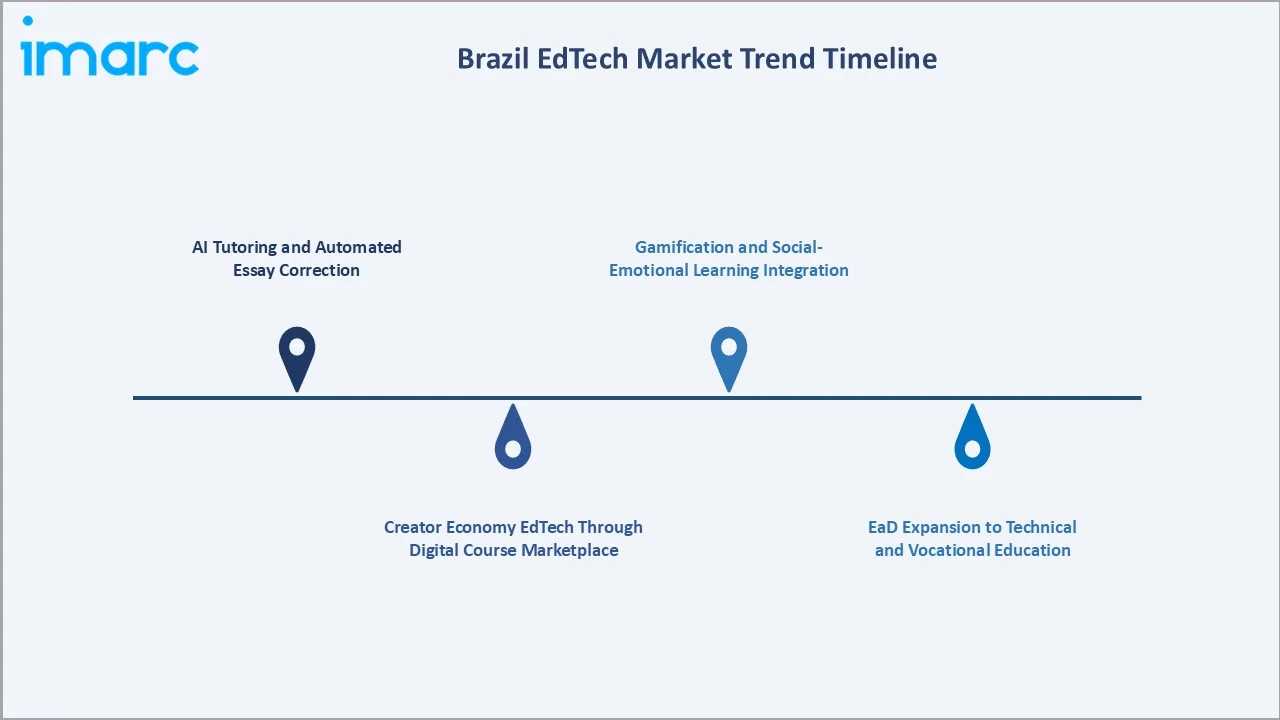

Emerging Market Trends

1. AI Tutoring and Automated Essay Correction

AI tutoring and automated essay correction are emerging as institutions seek scalable tools to improve learning outcomes and reduce teacher workloads. AI tutors provide personalized guidance, instant doubt resolution, and adaptive practice for students across K-12 and higher education. Automated essay correction supports faster feedback, grammar checks, scoring, and writing improvement, especially for exam preparation. These solutions are gaining relevance as Brazil promotes responsible AI use in education.

2. Creator Economy EdTech Through Digital Course Marketplace

Creator economy EdTech through digital course marketplaces is emerging in Brazil as educators, influencers, and subject experts increasingly create and sell online courses. These platforms enable low-cost, flexible learning in areas such as languages, coding, entrepreneurship, finance, and professional skills. They also help learners access practical, career-focused content outside traditional institutions. Rising smartphone use and digital payments are further supporting this trend.

3. EaD Expansion to Technical and Vocational Education

EaD (Distance education) expansion into technical and vocational education is emerging in Brazil as learners seek flexible, job-oriented training without attending full-time physical classes. Distance education accounts for more than 3.7 million undergraduate enrollments across Brazil and caters to a more inclusive and diverse student base compared to traditional face-to-face learning. Online platforms are supporting courses in IT, healthcare, business, industrial skills, and certification programs. This trend helps institutions reach working adults and students in underserved regions. It also supports workforce upskilling and improves access to career-focused education.

4. Gamification and Social-Emotional Learning Integration

Gamification and social-emotional learning integration are emerging as platforms aimed to improve student engagement and motivation. Game-based tools, rewards, quizzes, and interactive challenges make digital learning more enjoyable and easier to retain. At the same time, SEL features support communication, collaboration, confidence, and emotional well-being. This helps schools deliver more holistic and student-centered learning experiences.

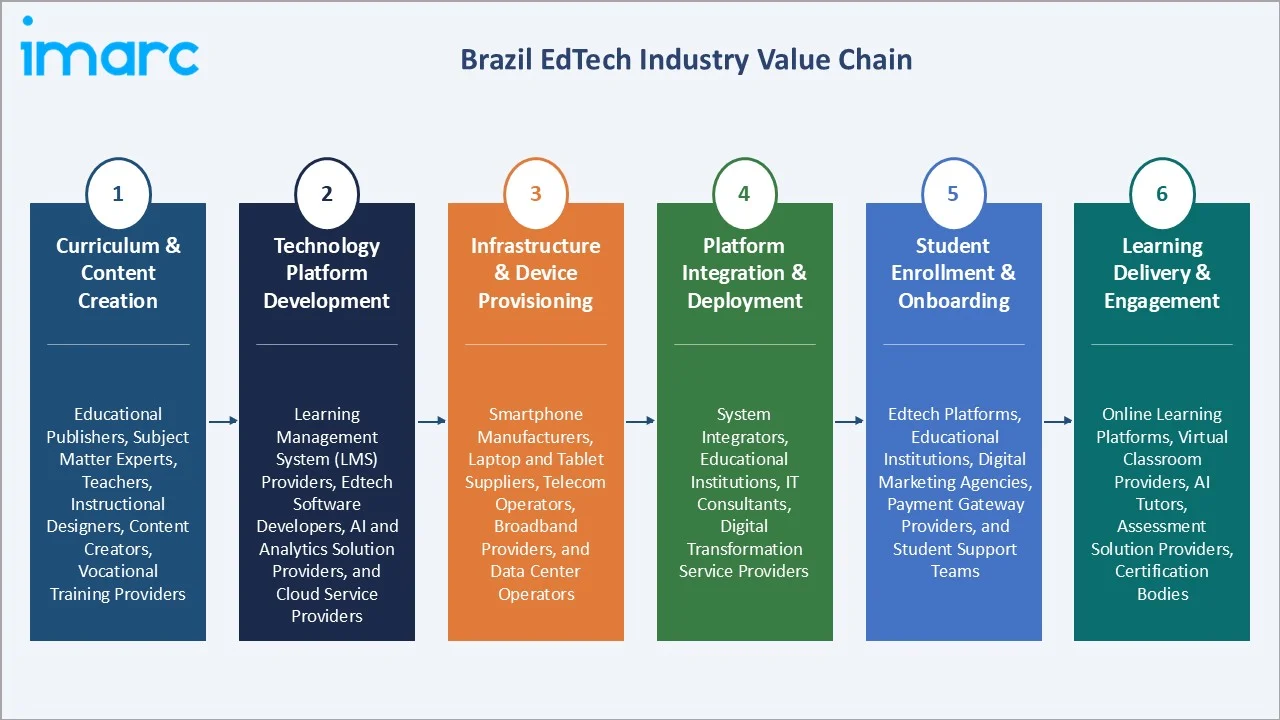

Industry Value Chain Analysis

Brazil EdTech value chain integrates curriculum and content creation, technology platform development, infrastructure & device provisioning, platform integration & deployment, student enrollment & onboarding, and learning delivery & engagement.

|

Stage |

Key Participants |

|

Curriculum & Content Creation |

Educational publishers, subject matter experts, teachers, instructional designers, content creators, vocational training providers |

|

Technology Platform Development |

Learning Management System (LMS) providers, EdTech software developers, AI and analytics solution providers, and cloud service providers |

|

Infrastructure & Device Provisioning |

Smartphone manufacturers, laptop and tablet suppliers, telecom operators, broadband providers, and data center operators |

|

Platform Integration & Deployment |

System integrators, educational institutions, IT consultants, digital transformation service providers |

|

Student Enrollment & Onboarding |

EdTech platforms, educational institutions, digital marketing agencies, payment gateway providers, and student support teams |

|

Learning Delivery & Engagement |

Online learning platforms, virtual classroom providers, AI tutors, assessment solution providers, certification bodies |

Student enrollment & onboarding is the most commercially competitive stage in Brazil EdTech value chain because providers compete intensely to attract and retain students through digital marketing, free trials, flexible pricing, and personalized learning experiences. Success at this stage directly influences user acquisition, subscription revenues, and long-term platform engagement, making it a key differentiator in the market.

Technology Landscape in the Brazil EdTech Industry

Learning Management Systems and Adaptive Platforms

Learning Management Systems (LMS) and adaptive learning platforms enable personalized and data-driven learning experiences. These platforms use analytics and AI to track student performance, identify learning gaps, and recommend customized content. They also support hybrid and remote education through virtual classrooms, assessments, and progress monitoring tools. As institutions seek scalable and flexible digital learning solutions, the adoption of LMS and adaptive platforms continues to accelerate.

Mobile EdTech and Offline Learning Capability

Mobile EdTech and offline learning capabilities are making digital education accessible to students with limited or inconsistent internet connectivity. Platforms are increasingly offering mobile-first applications, downloadable lessons, offline assessments, and synchronized learning features. This approach is particularly valuable in rural and underserved regions where broadband access remains uneven. As smartphone usage continues to rise, mobile-based learning is becoming a key channel for expanding educational reach and engagement.

Digital Course Marketplaces and Creator-Led Platforms

In April 2026, Brazil’s Ministry of Education introduced two free digital platforms, MEC Books and MEC Languages, to broaden access to reading materials and online language learning nationwide. MEC Books supports digital reading access, while MEC Languages provides free language courses for the public. This supports Brazil EdTech technology landscape by strengthening acceptance of digital course platforms and online content delivery. It also encourages creator-led and marketplace-style learning models, where educational content can be distributed widely, accessed flexibly, and scaled across diverse learner groups.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sector |

K-12 |

41.8% |

2025 |

|

Type |

Software |

46.3% |

2025 |

|

Deployment Mode |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

42.6% |

2025 |

By Sector

K-12 leads at 41.8% (2025). Brazil's K-12 EdTech encompasses a public-school government platform, a private school curriculum system, and a supplementary consumer platform, creating the most commercially stratified single-sector EdTech market in Brazil, above higher education's more concentrated EaD platform structure.

To access detailed market analysis, Request Sample

Higher education at 28.6% reflects Brazil's university students with EaD enrollment, creating the most commercially mature EdTech subscription market above K-12's mixed public-private procurement. Preschool at 17.2% grows fastest at ~12.2% CAGR. Others at 12.4% encompasses corporate training, language learning, and professional certification, creating Brazil's most commercially diverse EdTech miscellaneous segment.

By Type

Software leads at 46.3% (2025). Brazil's EdTech software encompasses institutional LMS, adaptive learning AI platform, school ERP, student assessment SaaS, and consumer digital subscription, creating the most commercially recurring revenue EdTech type through annual institutional and consumer subscription above one-time hardware and content purchase.

Content at 32.5% encompasses video lectures, digital textbooks, preparation material, a database, and a creator digital course. Hardware at 21.2% includes educational tablets, interactive whiteboards, and government-procured devices, creating Brazil's most commercially government-dependent single EdTech type.

Regional Market Insights

|

Region |

Share (2025) |

Key Brazil EdTech Market Drivers & Characteristics |

|

Southeast |

42.6% |

Driven by its high concentration of schools, universities, corporate training centers, and technology companies. |

|

South |

18.3% |

Benefits from strong educational indicators, high digital literacy, and widespread broadband connectivity. |

|

Northeast |

16.1% |

Witnessing growing EdTech adoption as governments and institutions leverage digital platforms to improve educational access. |

|

Central-West |

12.0% |

Supported by increasing digital transformation in schools, expanding internet coverage, and growing demand for online professional training. |

|

North |

11.0% |

Experiencing increasing demand for mobile-based and distance learning solutions to overcome geographic barriers. |

Southeast's 42.6% market dominance reflects Brazil's GDP concentration, private school density, and EdTech startup ecosystem. South's 18.3% reflects high student EdTech spending.

Northeast's 16.1% is growing above average CAGR through government digital education investment and EdTech platform demand. Central-West's 12.0% is growing through digital training. North's 11.0% is growing fastest from the smallest base through EdTech investment.

Competitive Landscape

Brazil EdTech competitive landscape is commercially stratified between large private education conglomerates, pure EdTech platforms, corporate software providers, and international players. Brazil's most commercially distinctive competitive dynamic is the private university group's vertical integration of EdTech.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

|

Cogna, Kroton, Saber, Somos |

Market Leader |

Cogna Educação is acting as a major player in both digital higher education and K-12 educational technology with its brands like Cogna, Kroton, Saber, and Somos. |

|

|

Duolingo |

Market Leader |

Duolingo plays a significant role in the Brazilian EdTech landscape by acting as a widely accessible, gamified entry point for language learning. |

|

|

HardWork Medicina, Grupo Q |

Strong Challenger |

YDUQS is a leading Brazilian higher education group and a major player in EdTech, serving students through a hybrid model of on-campus and distance learning. |

|

|

Hotmart |

Strong Challenger |

Hotmart is a cornerstone of the Brazilian EdTech sector, acting as a leading "business-in-a-box" platform that enables independent creators to produce, manage, and sell digital educational products. |

Brazil EdTech competitive landscape is being reshaped through consolidation. The creator economy's disruption through Hotmart's marketplace model is the most commercially novel competitive force, with independent creators capturing supplementary education revenue that institutional EdTech previously controlled above the formal curriculum system.

Key Company Profiles

Cogna Educação

Cogna Educação is one of Brazil’s largest education companies and a leading participant in the country's EdTech market. The company operates across K-12 education, higher education, professional training, digital learning, and educational content solutions. Through its portfolio of educational institutions and digital platforms, Cogna serves millions of students nationwide, supporting both in-person and distance education (EaD) models.

- Key Brands: Cogna, Kroton, Saber, Somos.

- Recent Developments: In June 2025, IFC invested in Cogna Educação S.A. to accelerate the digital transformation of Kroton’s undergraduate and postgraduate operations over the next three years. The funding aims to broaden access to affordable and high-quality education across Brazil.

- Strategic Focus: Expanding digital and distance education (EaD) offerings through investments in online learning platforms, learning management systems, and data-driven educational technologies.

YDUQS

YDUQS is one of Brazil’s leading higher education groups and a prominent participant in the country's EdTech market. The company operates a broad portfolio of universities, colleges, and professional education brands, serving students through both on-campus and distance learning (EaD) formats. YDUQS has expanded its digital education presence through online degree programs, virtual learning environments, and technology-enabled teaching solutions.

- Key Brands: HardWork Medicina, Grupo Q.

- Recent Developments: In April 2026, YDUQS modernized its operations by deploying AI-based solutions across its educational centers. In collaboration with CI&T, the company developed the “Polos” project to digitalize processes, enhance operational efficiency, and improve the experience of both students and staff.

- Strategic Focus: Accelerating the digital transformation of higher education through AI-powered learning solutions, virtual learning environments, and data-driven student engagement tools.

Market Concentration Analysis

Brazil EdTech market is moderately concentrated at the higher education EaD segment and highly fragmented in K-12 supplementary, concurso preparation, and creator economy segments. The most commercially concentrated single vertical is EaD higher education. Market concentration is evolving through private equity-backed consolidation, creating above-organic revenue growth through the acquisition of fragmented direct-to-school competitive sales.

Investment & Growth Opportunities

Highest Growth Segments

Preschool digital learning (~12.2% CAGR), corporate EdTech and professional upskilling (~13-15% CAGR through digital transformation skills gap), AI tutoring and preparation tech (~14-16% CAGR from emerging technology base), creator economy digital course marketplace (~13-15% CAGR), Northeast and North public school B2G EdTech (~12-14% CAGR through government digital school program expansion), and preparation platform (~10-12% CAGR through Brazil's growing civil service examination culture) represent Brazil's highest-growth EdTech investment vectors through 2034.

Investment Themes

- AI personalized learning for Brazil's ENEM and vestibular preparation market: The ENEM preparation market's candidates' spending on preparation platforms creates an addressable annual market for AI-personalized examination preparation. Investment in AI essay correction, adaptive mock examination, and weakness-diagnosis personalized study plan creates the most commercially differentiated above-video-lecture EdTech product for Brazil's most commercially intense examination preparation segment.

- EaD expansion to technical and vocational education: Brazil's technical education students have historically been limited to in-person delivery. Receiving MEC's progressive EaD authorization creates the most commercially underpenetrated single EdTech expansion opportunity.

Future Market Outlook (2026-2034)

Brazil EdTech market is projected to grow from USD 6.04 Billion in 2025 to USD 15.60 Billion by 2034, delivering an 11.12% CAGR over the forecast period. The market's anchor value of USD 10.23 Billion in 2030 represents Brazil EdTech industry at a structural maturity inflection. Public school digital integration reaching above-50% penetration nationally, AI personalized learning moving from premium to mainstream, and EaD distance learning normalizing across all education levels from preschool through postgraduate.

Three structural forces define Brazil EdTech market through 2034: government universal digital education investment creating a guaranteed public sector EdTech market, EaD's enrollment trajectory creating the largest single-country distance learning system, and AI personalization creating premium product tier conversion.

Research Methodology

Primary Research

Primary research comprised structured interviews with Brazil EdTech industry stakeholders, including chief executive officers, technology directors, academic directors, state education secretariat representatives, school technology directors, and student surveys from EdTech users across Southeast, Northeast, and South regions.

Secondary Research

Secondary research encompassed company annual reports, Brazil EdTech investment data, Brazil e-learning market survey, 5G deployment progress report, Hotmart creator economy annual report. Over 45 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using the education enrollment model: Brazil's student population by level multiplied by EdTech penetration rate by level and segment-specific average revenue per user in BRL converted to USD at the IMF exchange rate forecast. Penetration rate growth projections from EaD enrollment trend, digital adoption data, and EdTech investment round data.

Brazil EdTech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Preschool, K-12, Higher Education, Others |

| Types Covered | Hardware, Software, Content |

| Deployment Modes Covered | Cloud-based, On-premises |

| End Users Covered | Individual Learners, Institutes, Enterprises |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Cogna Educação, Duolingo, YDUQS, Hotmart, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil EdTech market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil EdTech market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil EdTech industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil EdTech Market Report

The Brazil EdTech market reached USD 6.04 Billion in 2025, driven by rising internet and smartphone penetration, increasing adoption of distance education (EaD), and growing demand for flexible digital learning solutions across K-12, higher education, and professional training. Government initiatives supporting educational digitalization and expanding access to online learning are further accelerating market growth.

The Brazil EdTech market grows at 11.12% CAGR during 2026-2034, reaching USD 15.60 Billion by 2034. The overall growth is sustained by government digital education investment, EaD distance learning expansion, AI personalized learning adoption, and creator economy EdTech marketplace growth.

K-12 leads at 41.8% through Brazil's K-12 students in schools, creating the most commercially volume-intensive single-sector EdTech procurement base.

Software leads at 46.3% through LMS, AI adaptive learning, and school ERP's recurring subscription model, creating the most commercially predictable above-one-time revenue structure.

Southeast Brazil leads at 42.6% through Brazil's GDP, creating the most commercially premium per-student EdTech spending geography, Brazil's EdTech startup companies headquartered in São Paulo, and the Rio de Janeiro private education sector.

Leading companies include Cogna Educação, Duolingo, YDUQS, and Hotmart, among others.

The Brazil EdTech market is projected to reach approximately USD 10.23 Billion by 2030, with EaD higher education enrollment growth creating above-current LMS subscription concentration, AI ENEM preparation and automated essay correction becoming standard platform features above current premium differentiation, and creator economy EdTech.

Three priority investment opportunities: AI-powered ENEM and vestibular preparation platform with automated essay correction and adaptive mock examination, creating the most commercially premium above-video-content examination preparation product for Brazil's annual ENEM candidates, B2G public school EdTech, and EaD technical and vocational education platform.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)