Brazil Furniture Market Size, Share, Trends and Forecast by Material, Application, Distribution Channel, and Region, 2026-2034

Brazil Furniture Market Size, Share, Trends & Forecast (2026-2034)

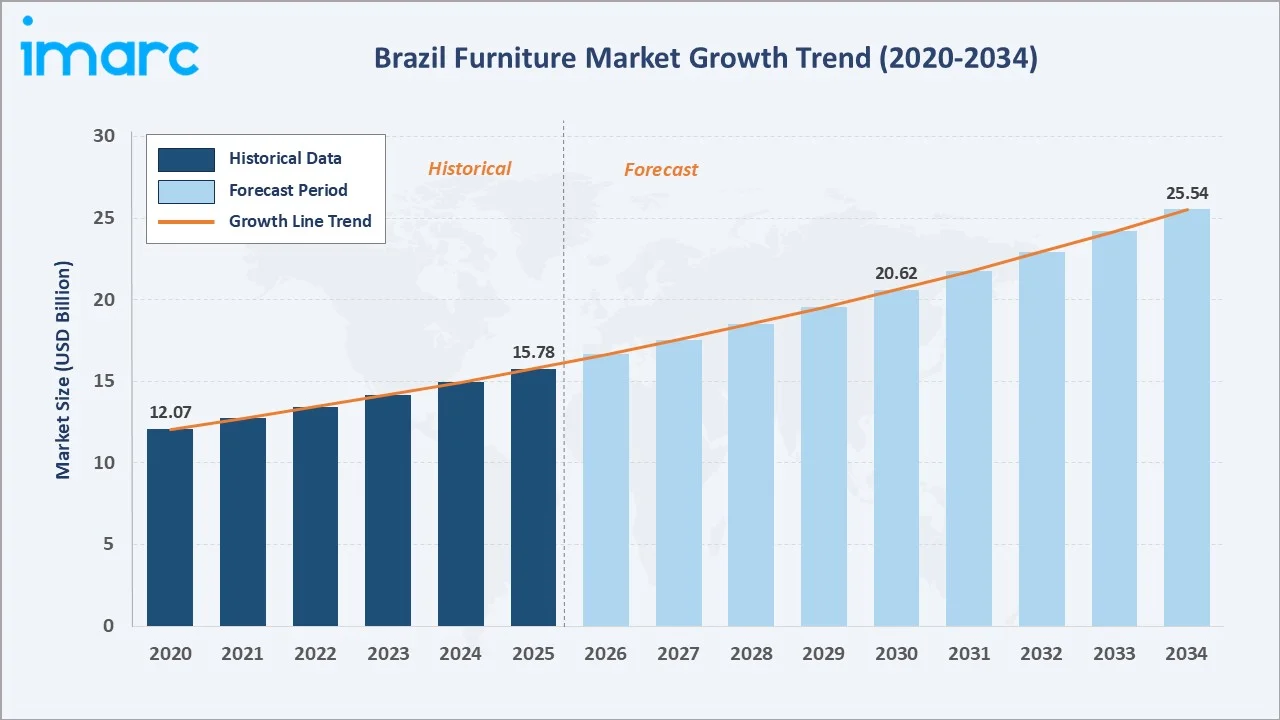

The Brazil furniture market size reached USD 15.78 Billion in 2025 and is projected to reach USD 25.54 Billion by 2034, exhibiting a CAGR of 5.50% during 2026-2034. Rising urbanization and government-backed housing programs, robust growth in middle-class disposable income, and expanding e-commerce furniture retail channels are the primary forces driving Brazil furniture market growth.

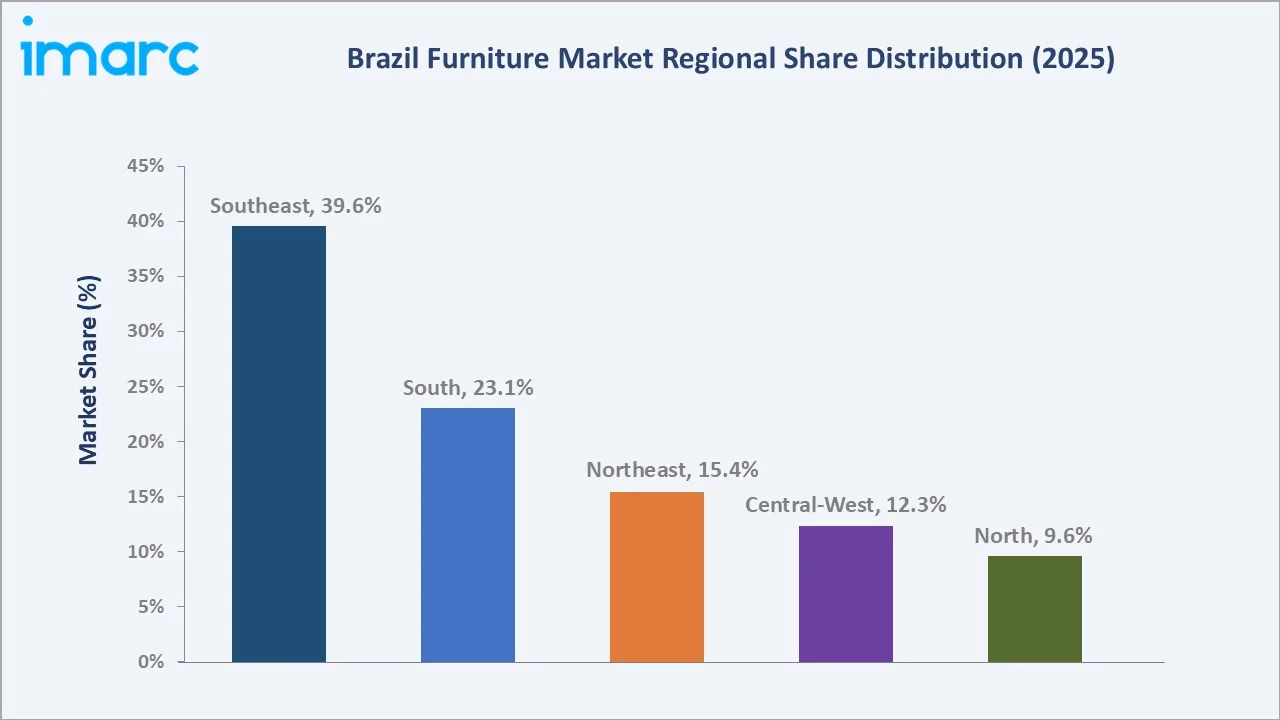

Wood dominates the material mix at 54.2% in 2025, while Home Furniture leads the application segment at 61.7%. The Southeast region commands a dominant 39.6% regional share in 2025, reflecting São Paulo and Rio de Janeiro's unparalleled consumer spending power and retail infrastructure depth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.78 Billion |

|

Forecast Market Size (2034) |

USD 25.54 Billion |

|

CAGR (2026-2034) |

5.50% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (39.6% share, 2025) |

|

Second Largest Region |

South (23.1% share, 2025) |

|

Leading Material Type |

Wood (54.2%, 2025) |

|

Leading Application |

Home Furniture (61.7%, 2025) |

The Brazil furniture market growth trajectory from 2020 through 2034, with historical expansion to USD 15.78 Billion in 2025, reflects consistent urbanization and housing-driven demand, while the forecast to USD 25.54 Billion captures accelerating middle-class expenditure, e-commerce adoption, and government housing stimulus effects.

To get more information on this market, Request Sample

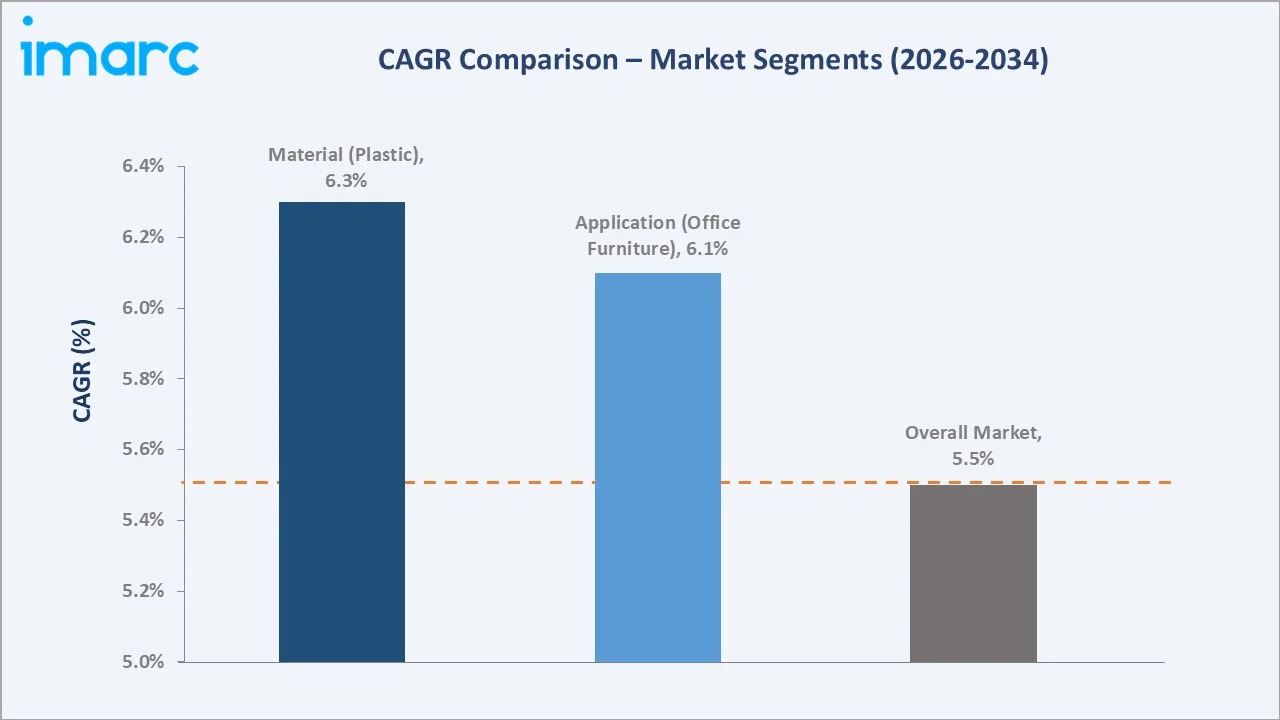

The CAGR trajectories across key material, application, and regional sub-segments, with Plastic at ~6.3% CAGR and Office Furniture at ~6.1% CAGR, represent the fastest-growing categories within the Brazil furniture industry through 2034.

Executive Summary

The Brazil furniture market is on a sustained growth trajectory from USD 15.78 Billion in 2025 to USD 25.54 Billion by 2034. Furniture, encompassing chairs, tables, sofas, beds, and storage units, serves essential residential, commercial, and hospitality functions supported by non-discretionary demand dynamics across Brazil's diverse economic regions.

Wood dominates material type at 54.2% in 2025, owing to Brazil's abundant domestic timber resources and strong consumer preference for natural aesthetics. Metal (18.6%) offers structural durability for commercial and outdoor applications. Plastic (14.3%) serves price-sensitive segments and grows fastest at ~6.3% CAGR through 2034.

Home Furniture leads application at 61.7% in 2025, driven by urbanization, housing program completions, and rising aspirational consumption. Office Furniture (18.9%) benefits from hybrid work infrastructure investment.

The Southeast dominates regionally at 39.6%, anchored by São Paulo, the largest consumer economy in Latin America.

Key Market Insights

|

Insight |

Data |

|

Largest Material Type |

Wood – 54.2% share (2025) |

|

Leading Application |

Home Furniture – 61.7% share (2025) |

|

Leading Region |

Southeast – 39.6% share (2025) |

|

Second Largest Region |

South – 23.1% share (2025) |

|

Top Companies |

Artesano, Móveis Dalla Costa LTDA, CENTURY, RUA MADEIRA, Bossa Furniture, Duoma Brazilian Furniture |

Key Analytical Observations Expanding on the Above Data:

- Wood, with 54.2% in 2025, dominates because Brazil is among the world's top timber producers. Domestic supply chains deliver competitive raw material costs, while consumer preference for natural wood aesthetics remains deeply rooted in Brazilian design culture across all income segments.

- Home Furniture, at 61.7% in 2025, leads because government housing programs have delivered millions of new residential units. First-time homeowners represent a structurally large pool of first-time furniture buyers requiring complete household furnishing sets at all price points.

- The Southeast's 39.6% dominance reflects São Paulo's position as the largest retail and consumer market in Latin America. The state concentrates Brazil's highest household incomes, the densest furniture retail network, and the majority of domestic furniture manufacturing capacity.

Brazil Furniture Market Overview

Furniture encompasses all movable objects designed to support human activities, seating, storage, sleeping, and work surfaces, manufactured from wood, metal, plastic, fabric, and composite materials. The Brazil furniture industry spans timber harvesting, panel board manufacturing, component fabrication, finished furniture production, surface finishing, logistics distribution, and multi-channel retail across five geographic regions.

The domestic ecosystem integrates certified timber suppliers, medium-density fiberboard (MDF) and particleboard mills, furniture manufacturers concentrated in the Bento Gonçalves cluster, fabric and foam upholstery suppliers, and a diverse retail network of specialty stores, large-format furniture chains, hypermarkets, and rapidly growing online platforms serving consumers across Brazil's 215-million-person population.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

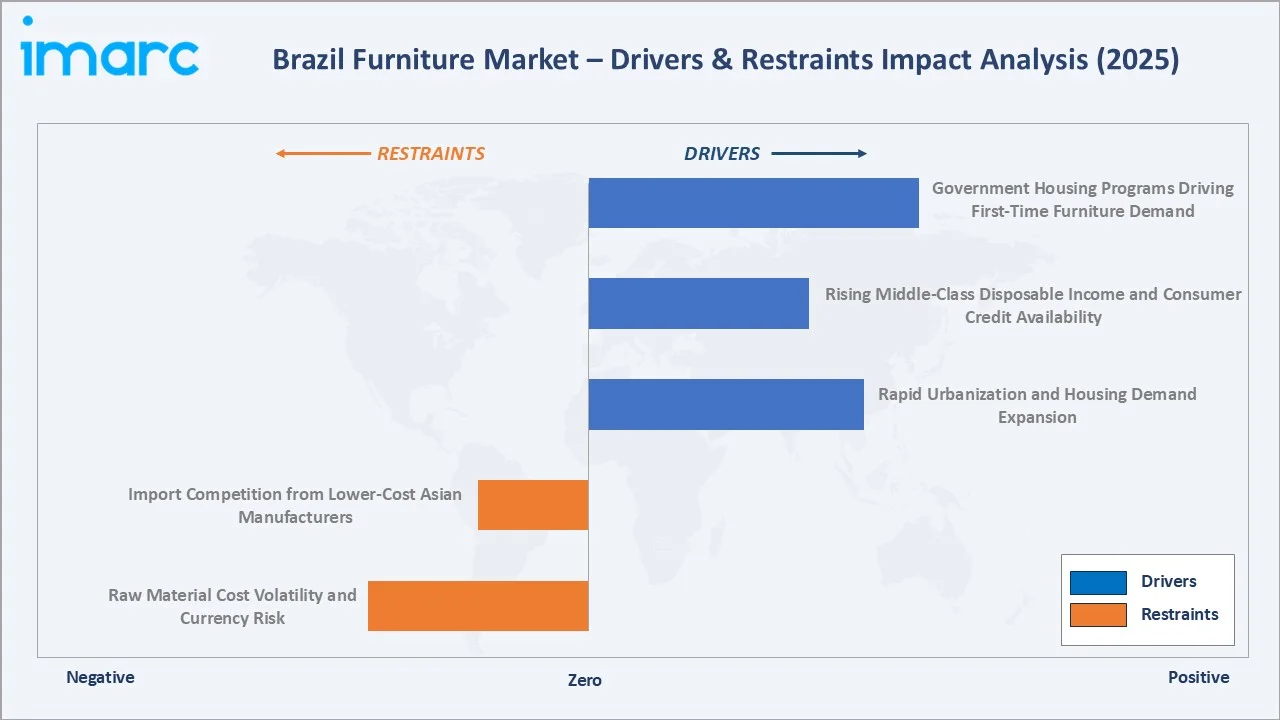

- Rapid Urbanization and Housing Demand Expansion: Brazil's urban population exceeds 87% of the national total, with continued urban migration, household formation among millennials, and a structural housing deficit estimated at 8.5 million units generating sustained furniture procurement demand. New household formation directly translates into furniture purchasing across all income segments.

- Rising Middle-Class Disposable Income and Consumer Credit Availability: Brazil's middle class, representing approximately 50% of the population, has gained greater access to consumer credit through installment financing. Retail credit availability enables furniture purchases across income brackets, directly expanding the addressable market for quality residential and office furniture segments nationwide.

- Government Housing Programs Driving First-Time Furniture Demand: The Brazilian federal government's Minha Casa Minha Vida (MCMV) program targets delivery of 2 million housing units through 2026 for low-income families. Each delivered unit creates immediate demand for complete household furniture sets, representing a structurally significant captive demand channel for value-segment furniture manufacturers and retailers.

Market Restraints

- Raw Material Cost Volatility and Currency Risk: Brazilian furniture manufacturers face dual raw material cost risks: domestic timber supply disruptions from deforestation regulation and wildfire events and imported component price volatility amplified by BRL/USD exchange rate fluctuations. Currency depreciation increases costs for metal hardware, foam chemicals, and synthetic textiles, compressing manufacturer margins significantly.

- Import Competition from Lower-Cost Asian Manufacturers: Chinese and Vietnamese furniture exporters benefit from significant labor cost advantages and automated manufacturing scale. Imported ready-to-assemble furniture, particularly in metal and plastic categories, competes aggressively on price in Brazil's value retail segment, limiting domestic manufacturers' pricing power in commodity product ranges.

Market Opportunities

- E-Commerce and Digital-First Furniture Retail Expansion: The continued growth of e-commerce and digital retail platforms is transforming furniture purchasing patterns and expanding consumer access to branded home furnishing products. Online sales channels are helping furniture companies reach customers beyond major urban centers, reducing geographic barriers and broadening the addressable market across emerging regional areas.

- Smart Furniture and Ergonomic Workspace Products: Brazil's hybrid work adoption following the pandemic has created sustained demand for home office furniture, ergonomic chairs, height-adjustable desks, and integrated storage solutions. The home office furniture sub-segment is growing, presenting a premium-priced opportunity for domestic and international brands targeting urban professionals.

Market Challenges

- Macroeconomic Instability and Consumer Confidence Cycles: Brazil's furniture market is highly sensitive to GDP growth cycles, inflation, and interest rate movements. High Selic benchmark rates increase credit costs, reducing installment plan attractiveness and deferring large furniture purchases among middle-income households, creating demand cyclicality that challenges inventory planning for manufacturers and retailers alike.

- Deforestation Regulation and Certified Timber Supply Constraints: Brazil's Forest Code and IBAMA enforcement increasingly restrict timber sourcing from non-certified origins. Certified wood supply commands price premiums above non-certified equivalents, elevating input costs for manufacturers targeting export markets or ESG-aligned retail channels, while creating compliance complexity for the fragmented SME manufacturer base.

Emerging Market Trends

1. E-Commerce Disruption Transforming Furniture Retail Distribution

Online furniture retail in Brazil is growing significantly. D2C furniture brands bypass traditional retail margins, enabling competitive pricing while accessing digital-native younger households. Augmented reality room visualization tools are reducing purchase hesitation for online shoppers and increasing average order values by encouraging complete room set purchases.

2. Sustainable Materials and Certified Timber Gaining Specification Momentum

Consumer and regulatory pressure is driving adoption of FSC-certified wood, recycled MDF panels, and water-based finishes. Premium furniture brands increasingly use sustainability certifications as competitive differentiators, particularly in export-oriented production and in urban consumer segments with higher environmental awareness and willingness to pay premium prices.

3. Modular and Space-Saving Furniture for Urban Apartment Living

Brazil's urbanization is concentrated in high-density apartment markets where average unit sizes are shrinking. Modular furniture systems, multifunctional sofas, wall beds, extendable dining tables, and convertible home office units, are gaining share against traditional fixed-dimension furniture in major metropolitan markets including São Paulo and Rio de Janeiro.

4. Foreign Brand Expansion and Premium Segment Development

International brands including IKEA, which entered Brazil, and European premium furniture labels are expanding into Brazil's growing upper-middle-class segment. Foreign brand entry raises the overall quality benchmark, stimulates category aspiration, and drives domestic manufacturers to upgrade product design, quality control, and retail presentation standards.

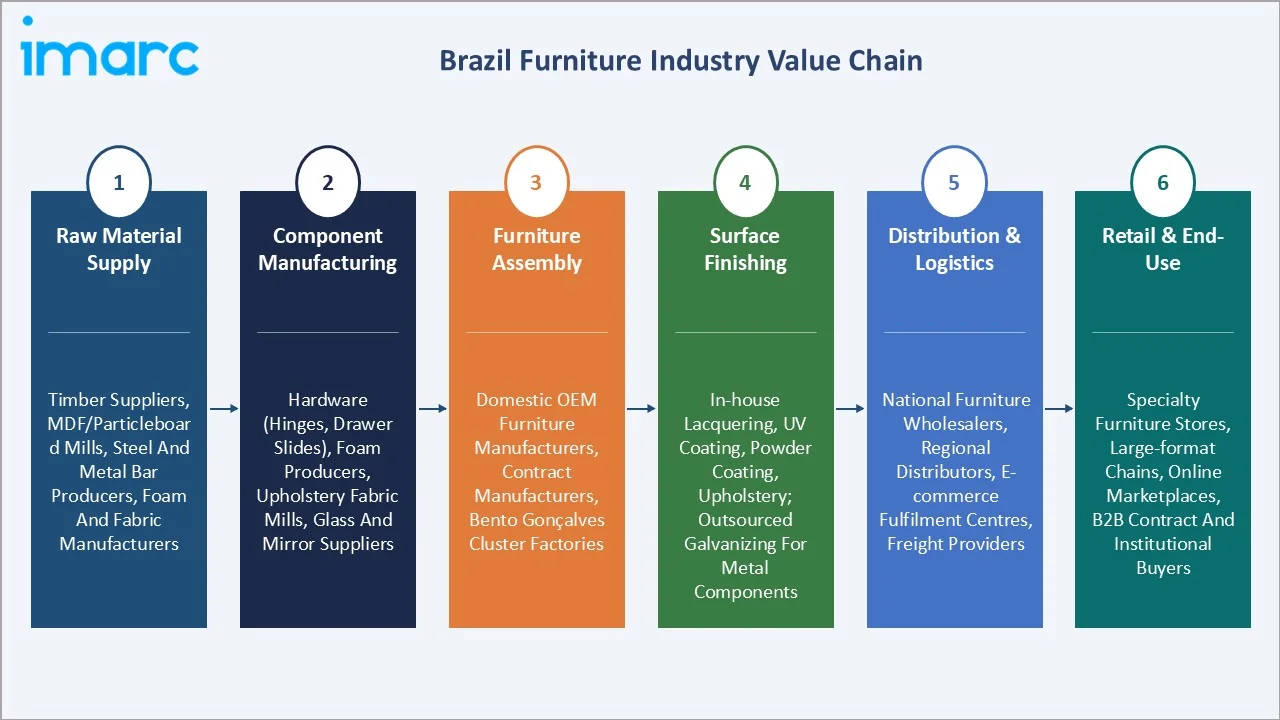

Industry Value Chain Analysis

The Brazil furniture value chain spans six stages from raw material input through end-use delivery. Manufacturing assembly and surface finishing capture the highest value-added margins, while distribution and retail logistics generate significant working capital requirements favouring well-capitalised mid-to-large producers over artisanal SME manufacturers.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Timber suppliers, MDF/particleboard mills, steel and metal bar producers, foam and fabric manufacturers |

|

Component Manufacturing |

Hardware (hinges, drawer slides), foam producers, upholstery fabric mills, glass and mirror suppliers |

|

Furniture Assembly |

Domestic OEM furniture manufacturers, contract manufacturers, Bento Gonçalves cluster factories |

|

Surface Finishing |

In-house lacquering, UV coating, powder coating, upholstery; outsourced galvanizing for metal components |

|

Distribution & Logistics |

National furniture wholesalers, regional distributors, e-commerce fulfilment centres, freight providers |

|

Retail & End-Use |

Specialty furniture stores, large-format chains, online marketplaces, B2B contract and institutional buyers |

Integrated furniture manufacturers with captive panel board procurement arrangements and in-house surface finishing achieve lower material cost bases than pure assemblers reliant on spot-market inputs. Regional cluster concentration reduces logistics costs and enables rapid supply-chain responsiveness, providing a structural cost advantage over geographically dispersed production models.

Technology Landscape in the Brazil Furniture Industry

Manufacturing Automation: CNC Machining and Robotic Assembly

Brazil's leading furniture manufacturers are investing in CNC routing, edge-banding automation, and robotic assembly lines. CNC machining enables mass customization — producing non-standard dimensions and shapes at near-standard production costs — addressing growing demand for fitted furniture in Brazilian urban apartments with non-standard floor plans and space constraints.

Digital Design and Augmented Reality in Retail

AR-powered room visualization, available on major furniture retail platforms' mobile apps, allows consumers to preview furniture placement in their actual rooms before purchasing. This technology reduces return rates, increases average order values by encouraging complete room set purchases, and shortens the purchase decision cycle for high-involvement furniture items.

Sustainable Material Technology: Eucalyptus and Recycled Content Panels

Brazil's dominant use of Eucalyptus-derived MDF and particleboard panels, driven by large-scale plantation forestry operations, provides a renewable, fast-growing timber input that reduces dependence on native forest timber. Recycled content panels incorporating post-industrial wood waste are gaining specification in environmentally certified furniture ranges targeting export and premium domestic markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

Wood |

54.2% |

2025 |

|

Application |

Home Furniture |

61.7% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Southeast |

39.6% |

2025 |

By Material

Wood commands a 54.2% majority share in 2025, reflecting Brazil's cost-competitive timber supply, strong artisanal and industrial woodworking tradition, and deeply rooted consumer aesthetic preference for natural materials across residential and commercial settings. The Bento Gonçalves manufacturing cluster produces the majority of Brazil's wood for both domestic consumption and export markets.

To access detailed market analysis, Request Sample

Metal at 18.6% in 2025 serves commercial, institutional, and outdoor applications where structural durability supersedes aesthetic preference. Growing B2B demand from data centres, coworking spaces, and healthcare facilities creates sustained procurement for metal shelving, racking, and institutional seating.

By Application

Home Furniture dominates the application mix at 61.7% in 2025, supported by government housing programme deliveries, household formation among Brazil's large young adult demographic, and middle-class upgrades to quality residential furniture. The residential sector benefits from instalment financing penetration, enabling consumers to purchase complete bedroom and living room sets through credit schemes across all income brackets.

Office Furniture (18.9%) benefits from hybrid work infrastructure investment, coworking space expansion, and corporate office refurbishment cycles across Brazil's major metropolitan areas. Hospitality Furniture (11.6%) is supported by Brazil's hotel construction pipeline and the expansion of boutique hotel and short-stay accommodation.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

39.6% |

Largest consumer economy; highest household incomes; dense retail network; corporate office demand |

|

South |

23.1% |

Bento Gonçalves manufacturer base; strong local consumption; European design heritage; export orientation |

|

Northeast |

15.4% |

MCMV housing programme deliveries; growing retail expansion; rising first-time furniture buyer base |

|

Central-West |

12.3% |

Agribusiness wealth driving residential upgrades; government and corporate office sector in Brasília |

|

North |

9.6% |

Urban housing growth; industrial investment; infrastructure development; growing middle-class emergence |

The Southeast's 39.6% market dominance in 2025 is driven by Brazil's largest and wealthiest consumer concentration. The region's dense specialty furniture retail infrastructure provides the distribution depth required to capture demand across all price tiers, from value-oriented mass-market products to ultra-premium designer pieces from international and domestic premium brands. São Paulo's established furniture retail corridors anchor this regional leadership.

The South (23.1%), home to Brazil's largest furniture manufacturing cluster in Bento Gonçalves and Serra Gaúcha, combines significant manufacturing with strong local consumption. The Northeast (15.4%) is the fastest-growing regional market, driven by MCMV housing programme roll-outs creating a sustained wave of first-time furniture buyers across Fortaleza, Recife, and Salvador. The Central-West and North regions are emerging demand centres supported by income growth and infrastructure development investment.

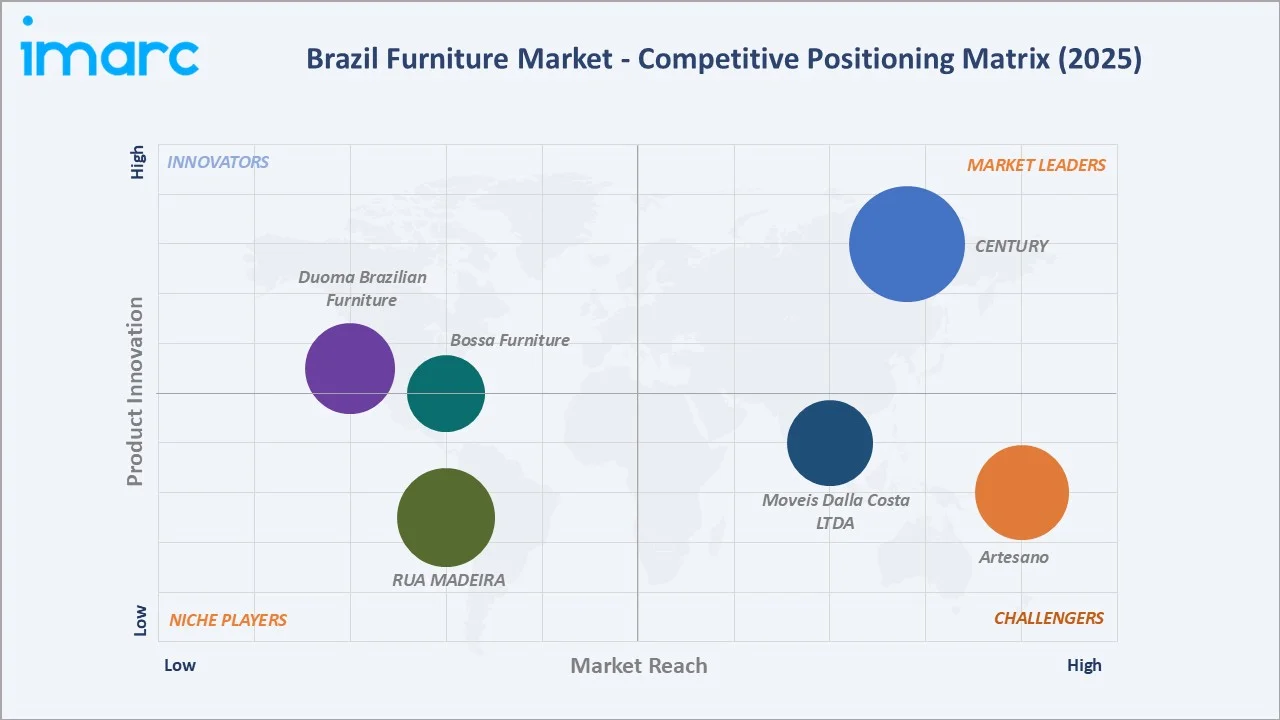

Competitive Landscape

The Brazil furniture market is moderately fragmented, with regional leaders holding strong positions in home states while national chains and a growing number of international entrants compete across geographies.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Artesano |

Dressing table, Chests of drawers, Bedside Tables, Desks, Racks, Sideboards |

Challenger |

Premium crafted wood; design-led; export orientation |

|

Móveis Dalla Costa LTDA |

Desk, Bookcase, Chest of drawers, Dining Tables, Chairs, Sideboard, Counter, Closet |

Challenger |

South region leader; residential; mid-premium positioning |

|

CENTURY |

Sofas, Armchairs, Chairs and Stools, Ottomans and Benches, Coffee and Side Tables, Dining Tables, Beds, Bedside tables |

Leader |

Full living & bedroom range; premium upholstery focus; strong domestic retail presence |

|

RUA MADEIRA |

Armchairs, Chairs & Stools Benches, Tables & Desks, Coffee & Side Tables |

Niche |

Contemporary design segment; DTC e-commerce focus; urban lifestyle positioning |

|

Bossa Furniture |

Table, Chairs and Stools, Storage |

Emerging |

Premium gallery specializing in vintage and contemporary collectible Brazilian design |

|

Duoma Brazilian Furniture |

Sofas, Armchairs, Benches |

Emerging |

Upholstered seating specialist; Brazilian craftsmanship heritage; regional market focus |

Key players include Artesano, Móveis Dalla Costa LTDA, CENTURY, RUA MADEIRA, Bossa Furniture, Duoma Brazilian Furniture, and others.

Key Company Profiles

CENTURY

Century is one of Brazil's largest and most recognized upholstered furniture brands. With over two decades of operating history, the company produces and distributes its products across all Brazilian states and in more than 15 countries across Latin America and the United States.

- Product Portfolio: Sofas, armchairs, chairs and stools, ottomans and benches, coffee and side tables, dining tables, bedside tables, and others.

- Recent Developments: In July 2022, Century Brazil partnered with Casa de Valentina to organize a roadshow initiative aimed at strengthening brand visibility and expanding engagement with architects, interior designers, and premium furniture consumers across key regional markets. The collaboration highlights the growing importance of experiential marketing and designer-focused outreach strategies in Brazil’s premium home décor and furniture industry.

- Strategic Focus: Century's strategy centres on design-led premiumisation of the upholstered seating segment, combining in-house design capability with mass manufacturing scale to deliver exclusive, customisable comfort products. The company targets Brazil's residential market through its Century Select retailer and architect partner programme, while expanding its international distribution footprint across Latin America and the United States.

Artesano

Artesano produces functional, accessible, and design-led furniture for residential environments, distributed nationally through e-commerce platforms and retail partners, with active exports to Colombia, Paraguay, the United States, and Bolivia.

- Product Portfolio: Dressing table, chests of drawers, bedside tables, desks, racks, sideboards, and others.

- Strategic Focus: Artesano's strategy is centred on delivering design-led, accessible furniture through scalable serialised production lines that combine artisanal heritage with modern manufacturing technology.

Móveis Dalla Costa LTDA

Móveis Dalla Costa is a Brazilian furniture manufacturer headquartered in Bento Gonçalves, Rio Grande do Sul. One of Brazil's pioneering companies in the adoption of MDF as a primary raw material, it operates a manufacturing facility and serves the national retail market through a broad network of dealers, distributors, and online marketplaces including Amazon Brazil and Mercado Livre.

- Product Portfolio: Desk, bookcase, chest of drawers, dining tables, chairs, sideboard, counter, closet, and others.

- Strategic Focus: Dalla Costa's strategy leverages its position as an MDF pioneer and Bento Gonçalves cluster manufacturer to deliver quality mid-market residential furniture at competitive price points. The company focuses on bedroom and home entertainment categories, targeting Brazil's expanding middle-class consumer base through nationwide retail and online distribution with export capabilities to international markets.

Market Concentration Analysis

The Brazil furniture market is highly fragmented at the national level, with no single company holding more than 3–5% of total market revenue. The industry comprises various furniture manufacturers, the vast majority of which are small and medium enterprises concentrated in regional clusters, serving distinct geographic and price-tier demand bases.

Consolidation at the brand and retail level is more advanced. National furniture retail chains aggregate demand across fragmented manufacturer supply bases, while e-commerce platforms are vertically integrating into private-label manufacturing. Private equity interest in consolidating Brazil's premium furniture manufacturing segment is growing, driven by attractive brand economics, export market potential, and recurring residential upgrade demand cycles.

Investment & Growth Opportunities

Fastest-Growing Segments

Plastic at ~6.3% CAGR through 2034 is the highest-growth material segment, driven by outdoor living, contract hospitality, and children's furniture applications. Office Furniture at ~6.1% CAGR represents the broadest-based B2B growth opportunity, supported by corporate workspace investment and the persistent demand for ergonomic home office solutions among Brazil's hybrid workforce.

Emerging Markets

The Northeast region at an estimated ~6.5% regional CAGR is the fastest-growing Brazilian furniture market through 2034. Government MCMV housing deliveries in Fortaleza, Recife, Salvador, and Natal are generating sustained waves of first-time furniture buyers. The region's growing middle class and expanding retail infrastructure create demand that currently significantly exceeds locally available supply, presenting logistics and distribution investment opportunities.

Venture & Investment Trends

Venture capital and private equity investment in Brazilian furniture e-commerce reached record levels in 2023–2024, with platforms attracting growth capital for logistics infrastructure and private-label product development. International furniture brands' Brazil market entry is catalysing domestic investment in retail modernisation, brand development, and digital channel capability across the incumbent competitive set, raising overall market sophistication.

Future Market Outlook (2026-2034)

The Brazil furniture market is forecast to expand from USD 15.78 Billion in 2025 to USD 25.54 Billion by 2034 at a CAGR of 5.50%, adding USD 9.76 Billion in incremental annual market value over the forecast period. This consistent, sustained growth reflects the market's housing-linked, consumer-spending-driven demand characteristics and Brazil's favourable demographic profile.

Three structural forces will most significantly shape the Brazil furniture industry landscape through 2034. First, the continued execution of MCMV housing programme deliveries will sustain first-time furniture buyer demand in the Northeast and North regions. Second, rising e-commerce penetration will expand the effective retail geography of premium furniture brands into previously underserved Tier 2 and Tier 3 cities nationwide.

Third, the entry and expansion of international furniture brands will elevate consumer expectations, accelerate domestic manufacturers' design and quality investment, and develop the premium segment which currently represents a smaller share of total market revenue than comparable economies at Brazil's income level. Collectively, these forces support the CAGR of 5.50% projected through 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Brazil furniture industry stakeholders, including senior commercial managers at domestic furniture manufacturers, retail chain buyers, e-commerce platform executives, interior designers, and industry association representatives from MOVERGS (Gaúcha Furniture Industry Association) and ABIMÓVEL (Brazilian Furniture Industry Association). Primary data validated market sizing, segment shares, and technology adoption timelines across regional markets.

Secondary Research

Key secondary sources include ABIMÓVEL Brazilian Furniture Industry Reports, IBGE (Brazilian Institute of Geography and Statistics) consumer expenditure surveys and housing construction data, Banco Central do Brasil consumer credit statistics, Brazilian Ministry of Economy trade data for furniture import and export flows, MOVERGS cluster performance reports, and industry publications including Móbile Fornecedores and Revista da Madeira.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, urbanisation indices, consumer expenditure data, housing construction starts, and historical market evolution patterns. Scenario analysis encompassing base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty in Brazil's historically volatile economic environment.

Brazil Furniture Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Materials Covered | Wood, Metal, Plastic, Others |

| Applications Covered | Home Furniture, Office Furniture, Hospitality Furniture, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Artesano, Móveis Dalla Costa LTDA, CENTURY, RUA MADEIRA, Bossa Furniture, Duoma Brazilian Furniture, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil furniture market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil furniture market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil furniture industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Furniture Market Report

The Brazil furniture market reached USD 15.78 Billion in 2025, reflecting sustained demand from government housing programmes, rising middle-class consumption, and growing e-commerce furniture retail penetration across all five Brazilian regions.

The market is projected to reach USD 25.54 Billion by 2034, growing at a CAGR of 5.50% during 2026-2034, driven by MCMV housing programme deliveries, e-commerce expansion, rising middle-class incomes, and international brand market entry stimulating category development.

Wood leads with a 54.2% material share in 2025, owing to Brazil's abundant domestic timber supply, competitive pricing, and strong consumer aesthetic preference for natural wood materials across residential and commercial furniture categories nationwide.

Home furniture leads at 61.7% in 2025, representing the largest demand segment supported by residential housing programme completions, household formation, and middle-class aspirational consumption driving continuous upgrade purchasing in the residential category.

The Southeast region commands a dominant 39.6% market share in 2025, anchored by São Paulo — the largest consumer economy in Latin America — where the highest household incomes, densest retail network, and majority of domestic manufacturing capacity converge.

Plastic is the fastest-growing material at ~6.3% CAGR through 2034, driven by outdoor living furniture, contract hospitality applications, and children's furniture where durability, cleanability, and price competitiveness are primary purchasing criteria.

Leading companies include Artesano, Móveis Dalla Costa LTDA, CENTURY, RUA MADEIRA, Bossa Furniture, Duoma Brazilian Furniture, and others.

Key applications include residential home furnishing (living rooms, bedrooms, dining rooms, kitchens), corporate and government office environments, hospitality and hotel fit-outs, healthcare and educational institutional procurement, and outdoor and leisure furniture.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade