Brazil Higher Education Market Size, Share, Trends and Forecast by Component, Deployment Mode, Course Type, Learning Type, End User, and Region, 2026-2034

Brazil Higher Education Market Size, Share, Trends & Forecast (2026-2034)

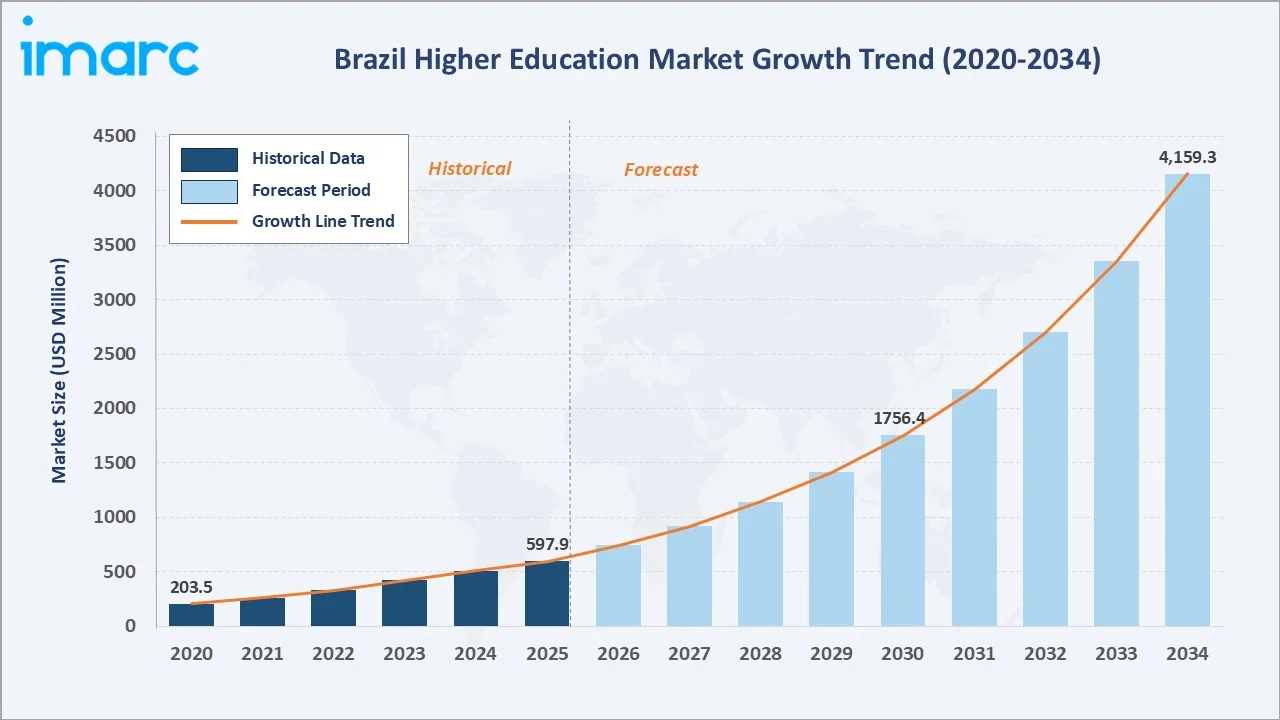

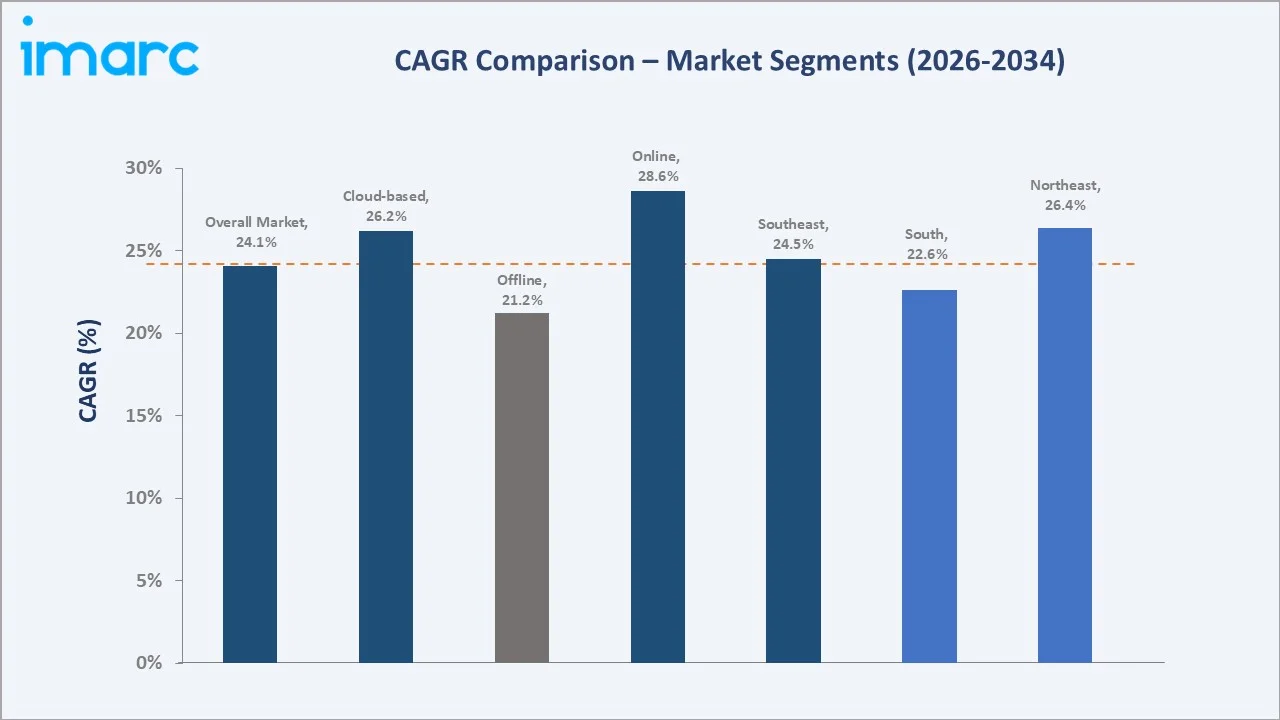

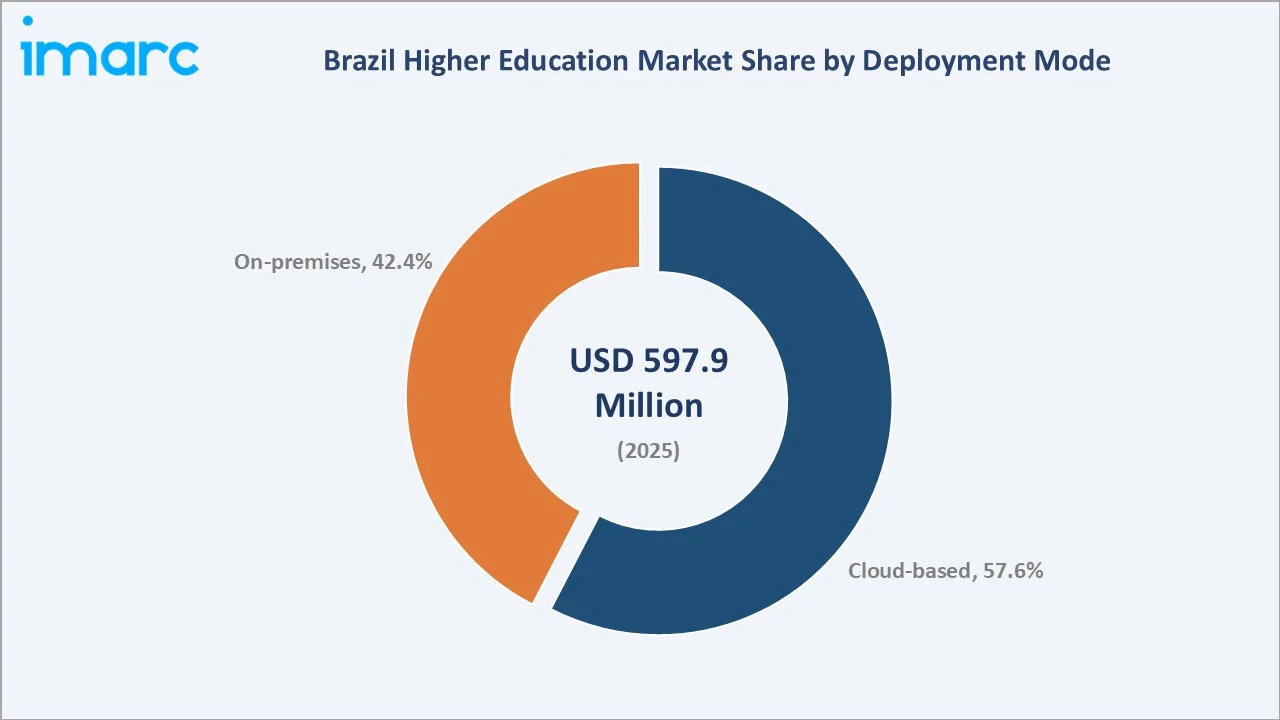

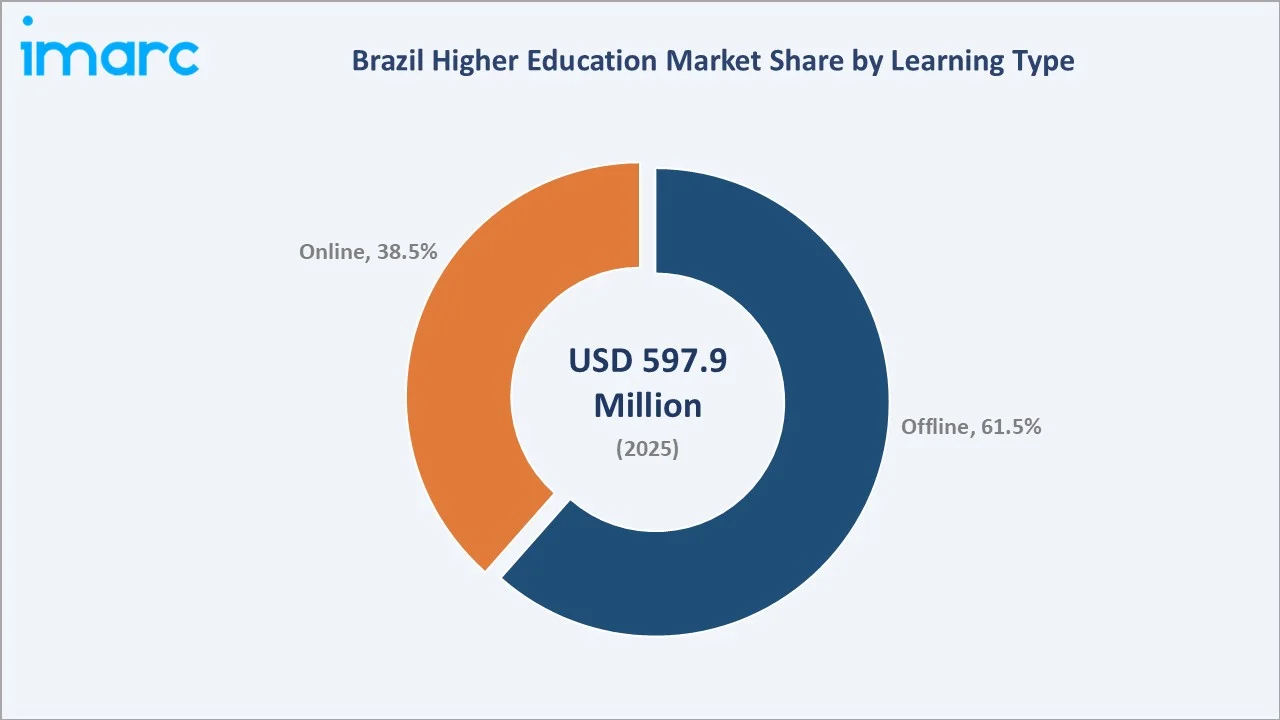

The Brazil higher education market size was valued at USD 597.9 Million in 2025 and is projected to reach USD 4,159.3 Million by 2034, exhibiting a CAGR of 24.05% during 2026-2034. Rising digital learning adoption, expanding private university enrollment, government investment in distance education, and growing demand for cloud-based campus solutions are driving market growth. Cloud-based deployment leads with a 57.6% share in 2025, while Offline learning dominates at 61.5%. The Southeast accounts for 46.3% of national revenue, anchored by São Paulo and Rio de Janeiro education hubs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 597.9 Million |

|

Forecast Market Size (2034) |

USD 4,159.3 Million |

|

CAGR (2026-2034) |

24.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (46.3% share, 2025) |

|

Fastest Growing Region |

Northeast |

|

Leading Deployment Mode |

Cloud-based (57.6%, 2025) |

|

Leading Learning Type |

Offline (61.5%, 2025) |

The chart below illustrates the rapid expansion of the Brazil higher education market between 2020 and 2034, highlighting strong post-pandemic digital adoption and accelerating EdTech investment.

To get more information on this market, Request Sample

CAGR analysis identifies cloud-based deployment and online learning as the fastest-growing segments, supported by digital infrastructure expansion and rising distance education demand through 2034.

Executive Summary

The Brazil higher education market is undergoing rapid transformation driven by digitalization, expanding private enrollment, and rising EdTech adoption. Valued at USD 597.9 Million in 2025, the market is projected to reach USD 4,159.3 Million by 2034 at a CAGR of 24.05%. The shift toward hybrid learning, regulatory liberalization of distance education, and rising investment in campus management platforms are reshaping institutional priorities.

Cloud-based solutions captured a 57.6% share in 2025, driven by universities adopting scalable, cost-efficient infrastructure. Offline learning still leads with 61.5%, though online learning is expanding at a strong double-digit pace. Key trends include AI-powered analytics, mobile-first platforms, and adaptive learning tailored to Brazil’s diverse student base.

The Southeast region commands 46.3% of national revenue in 2025, supported by mature universities in São Paulo and Rio de Janeiro. The South follows at 19.4%, while the Northeast at 16.2% represents the fastest-growing region, fuelled by federal investment, Tier-2 city expansion, and aggressive online program rollouts by Cogna, YDUQS, and Vitru.

Key Market Insights

|

Insight |

Data |

|

Largest Deployment Mode |

Cloud-based - 57.6% share (2025) |

|

Second Deployment Segment |

On-premises - 42.4% share (2025) |

|

Largest Learning Type |

Offline - 61.5% share (2025) |

|

Fastest Growing Learning Type |

Online - 38.5% share (2025) |

|

Leading Region |

Southeast - 46.3% (2025) |

|

Top Companies |

Cogna Educação, YDUQS, Ânima Educação, Cruzeiro do Sul Educacional SA, and Vitru Education |

Key Analytical Observations Supporting the Above Figures Include the Following:

- Cloud-based deployment captured 57.6% in 2025, driven by universities shifting to scalable SaaS platforms that enhance flexibility and reduce infrastructure costs.

- On-premises deployment held 42.4% in 2025, sustained by federal universities and large private institutions with strict data sovereignty rules and existing IT investments.

- Offline learning's 61.5% share in 2025 reflects cultural preference for in-person classrooms, particularly for engineering, law, and medicine programs requiring hands-on practice.

- Online learning at 38.5% in 2025 is expanding rapidly, supported by Ministry of Education (Brazil) regulations, with recent estimates indicating over 5 million students enrolled in distance undergraduate programs in Brazil.

- Southeast's 46.3% dominance in 2025 reflects São Paulo and Rio hosting Brazil's largest universities, including USP, UNICAMP, and major private operators headquartered there.

- Cogna and YDUQS together serve over 3.0 million students in 2025, representing a significant presence in Brazil’s private higher education market.

Brazil Higher Education Market Overview

Brazil higher education refers to post-secondary academic and vocational programs delivered by public and private institutions, increasingly powered by digital technology platforms. The ecosystem covers content creators, university operators, EdTech vendors, regulators (MEC, INEP), accreditation bodies, and student financing programs such as FIES and ProUni.

Brazilian higher education spans state and federal universities, community colleges, and private institutions, supported by a fast-growing layer of online learning, AI-driven analytics, and student information systems. Macroeconomic drivers include white-collar employment growth, urbanization, and expanding middle-class enrollment.

Market Dynamics

To evaluate market opportunities, Request Sample

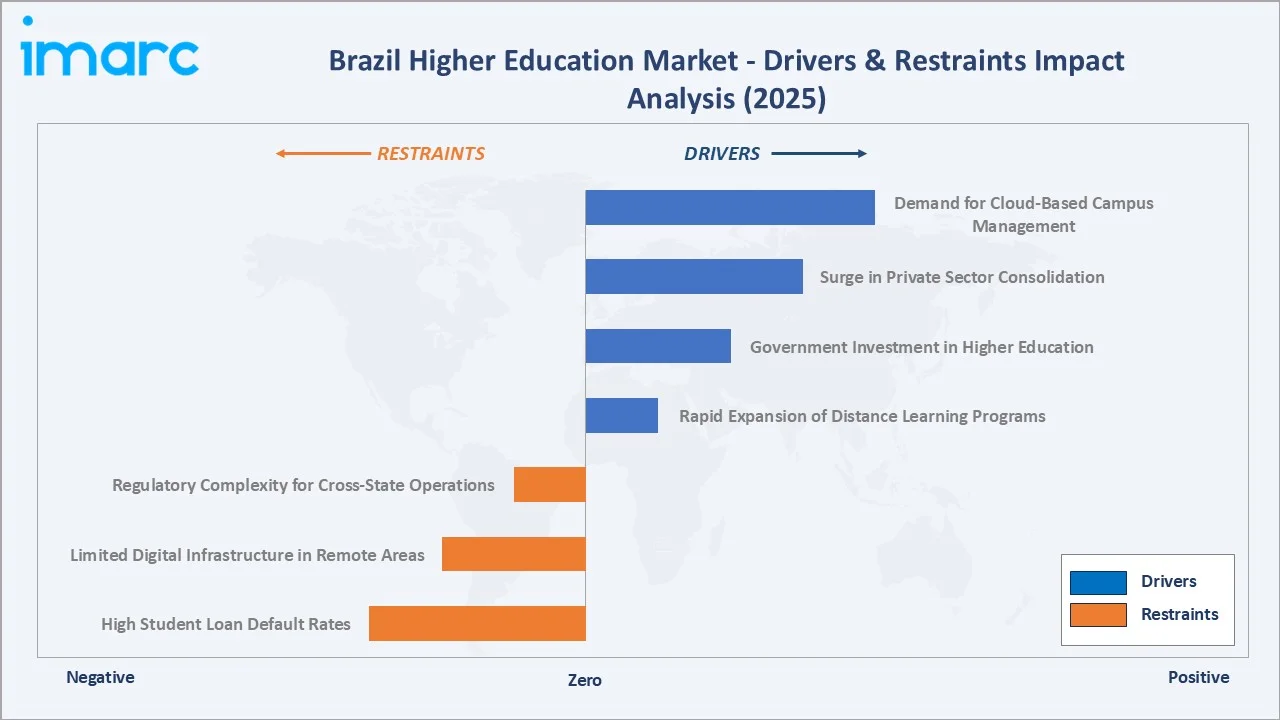

Market Drivers

- Rapid Expansion of Distance Learning Programs: Brazil's online undergraduate enrollment crossed 4.9 million students in 2024, supported by relaxed MEC regulations, fueling demand for cloud-based campus systems across institutions.

- Government Investment in Higher Education: Federal programs such as FIES and Future-se support access and modernization in higher education, alongside ongoing public digital education initiatives.

- Surge in Private Sector Consolidation: Private institutions account for 75% of total Brazilian higher education enrollment in 2023 with consolidators like Cogna and YDUQS investing heavily in centralized academic systems.

- Demand for Cloud-Based Campus Management: Universities are increasingly adopting cloud-based SIS and LMS platforms to improve scalability, reduce upfront IT infrastructure costs, and support hybrid learning models across Brazil.

Market Restraints

- High Student Loan Default Rates: Default rates on FIES loans reached over 40% by 2025, restricting new disbursements and limiting affordability for low-income students seeking access to private programs.

- Limited Digital Infrastructure in Remote Areas: Brazil’s internet penetration exceeds 90% overall, but rural access remains lower, highlighting persistent regional gaps that hinder online education adoption in underserved areas.

- Regulatory Complexity for Cross-State Operations: Brazil’s higher education expansion is constrained by centralized approval systems, with program accreditation and regulatory compliance often taking extended timelines, delaying institutional scaling and new course launches.

Market Opportunities

- AI-Powered Personalized Learning at Scale: AI-enabled learning platforms are gaining traction in Brazil, improving personalization and engagement, though adoption depends on infrastructure and teacher readiness rather than large-scale quantified deployment.

- EdTech Investment Boom in Latin America: Latin America’s EdTech sector has seen strong growth and global recognition, with Brazilian firms among top global players, reflecting rising investor interest in digital education solutions.

- Microcredentials and Industry Partnerships: Higher education in Latin America is expanding into short-cycle and professional programs, supported by industry collaboration and demand for flexible, job-oriented skills development among working adults.

Market Challenges

- Faculty Digital Skills Gap: Brazilian universities face uneven faculty readiness for digital teaching, with gaps in advanced LMS and online pedagogy skills slowing effective rollout and quality of distance education programs.

- Data Privacy and LGPD Compliance: Brazil’s Lei Geral de Proteção de Dados imposes strict data governance rules, increasing compliance costs and complicating cloud adoption for higher education institutions handling sensitive student data.

- Intense Pricing Competition Online: Expansion of distance learning in Brazil has intensified price competition, with significantly lower online tuition fees pressuring margins and forcing institutions to optimize costs and scale operations efficiently.

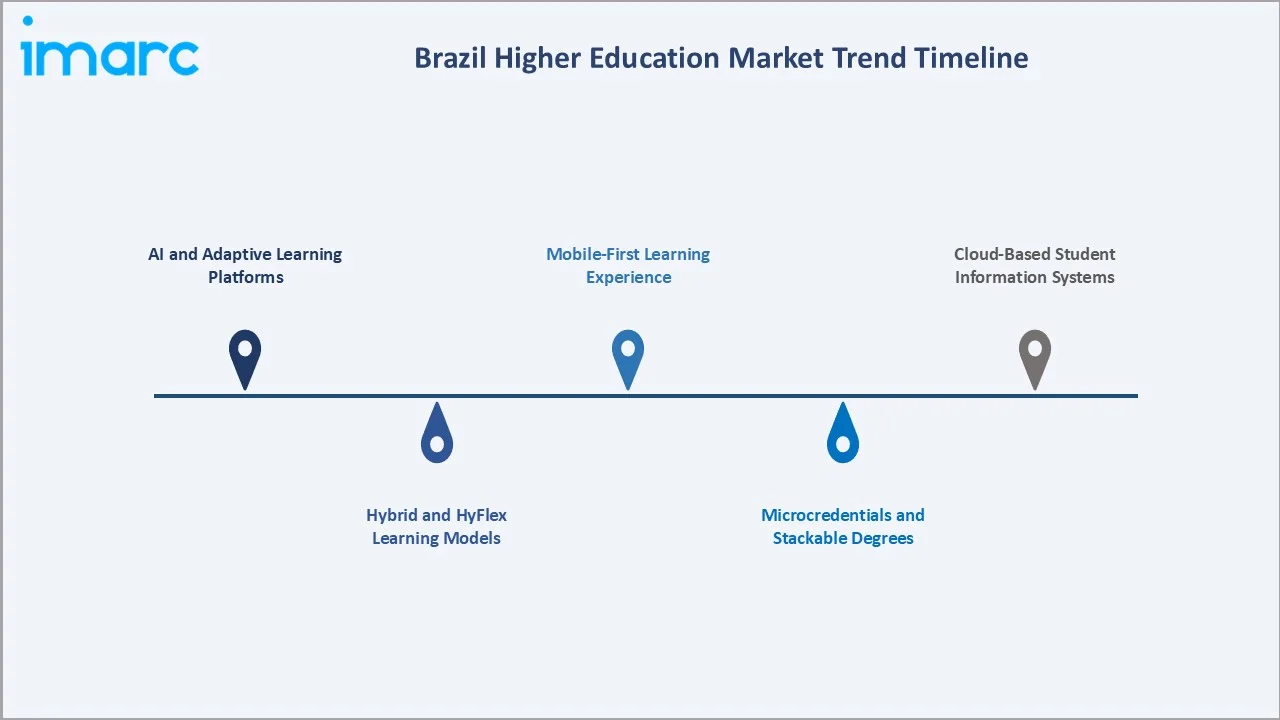

Emerging Market Trends

1. AI and Adaptive Learning Platforms

Brazilian universities are increasingly integrating AI-driven tools such as chatbots, adaptive learning systems, and predictive analytics to enhance student engagement, personalize learning paths, and support retention strategies across digital education platforms.

2. Hybrid and HyFlex Learning Models

Hybrid learning combining online and in-person delivery has become mainstream in Brazil, supported by regulatory flexibility and growing student demand for accessible, flexible, and scalable higher education formats post-pandemic.

3. Microcredentials and Stackable Degrees

Education groups like Cogna Educação and Ânima Educação are expanding short-term, industry-aligned certification programs, enabling universities to attract working professionals seeking flexible and career-focused upskilling options.

4. Mobile-First Learning Experience

Widespread smartphone usage, institutions are prioritizing mobile-optimized platforms, enabling students to access coursework, assessments, and academic services through apps and low-bandwidth solutions, improving accessibility across diverse socio-economic segments.

5. Cloud-Based Student Information Systems

Brazilian universities are adopting cloud-based student information and campus management systems to improve scalability, reduce IT costs, and enhance data analytics, while aligning with compliance requirements under Lei Geral de Proteção de Dados.

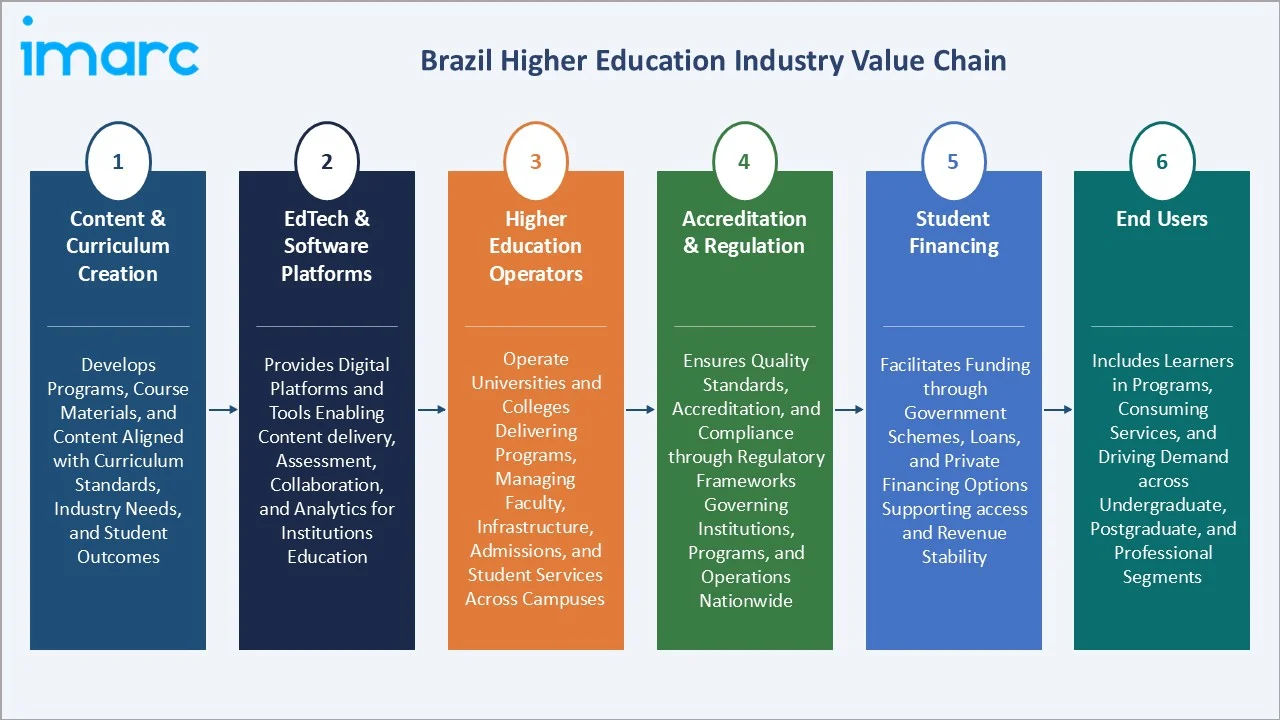

Industry Value Chain Analysis

The Brazil higher education value chain spans content creation, technology platforms, accreditation, institutional delivery, and graduate outcomes, each layer adding value through specialization, regulatory compliance, and student-centric service models.

|

Stage |

Key Players / Examples |

|

Content & Curriculum Creation |

Develops programs course materials, and content aligned with curriculum standards, industry needs, and student outcomes. |

|

EdTech & Software Platforms |

Provides digital platforms and tools enabling content delivery, assessment, collaboration, and analytics for institutions education. |

|

Higher Education Operators |

Operate universities and colleges delivering programs, managing faculty, infrastructure, admissions, and student services across campuses. |

|

Accreditation & Regulation |

Ensures quality standards, accreditation, and compliance through regulatory frameworks governing institutions, programs, and operations nationwide. |

|

Student Financing |

Facilitates funding through government schemes, loans, and private financing options supporting access and revenue stability. |

|

End Users |

Includes learners in programs, consuming services, and driving demand across undergraduate, postgraduate, and professional segments. |

Tier-1 operators integrate content, platforms, and delivery to capture maximum value, while specialist EdTech vendors compete for software contracts. Smaller institutions increasingly outsource technology to focus on academic differentiation.

Technology Landscape in the Brazil Higher Education Industry

AI-Powered Student Analytics and Adaptive Learning

Brazilian universities are adopting AI tools to analyze student performance, engagement, and progression, enabling personalized learning paths and early identification of at-risk students to support retention and academic success.

Cloud-Based Learning Management Systems

Cloud-based LMS platforms such as Moodle, Blackboard Learn, and Canvas are widely used, enabling scalable content delivery, mobile access, and integrated assessments across Brazilian higher education institutions.

Smart Campus and Digital Identity Solutions

Brazilian institutions are gradually implementing smart campus solutions, including digital identification, automated attendance, and connected systems to enhance operational efficiency, campus security, and administrative processes.

LGPD Compliance and Data Security Platforms

LGPD-driven demand for data security and compliance platforms is rising, with universities adopting encryption, role-based access, and consent management tools to safeguard student data and meet ANPD audit requirements.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | 🔒 | 🔒 | 2025 |

| Deployment Mode | Cloud-based | 57.6% | 2025 |

| Course Type | 🔒 | 🔒 | 2025 |

| Learning Type | Offline | 61.5% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Southeast | 46.3% | 2025 |

By Deployment Mode

Cloud-based deployment commands a 57.6% share in 2025, driven by demand for scalability and cost efficiency. Brazilian universities are increasingly adopting cloud-based SIS and LMS platforms to support digital learning, remote access, and data-driven academic management.

To access detailed market analysis, Request Sample

On-premises deployment retains 42.4% in 2025, supported by public universities and institutions relying on legacy IT systems. Data control, integration needs, and gradual digital transition continue to sustain on-premises infrastructure alongside growing cloud adoption trends.

By Learning Type

Offline learning leads with 61.5% in 2025, anchored by traditional in-person undergraduate programs in engineering, law, medicine, and the sciences, where laboratory access and faculty interaction remain core to academic outcomes and accreditation.

Online learning holds 38.5% in 2025 and is the fastest-growing segment. With 4.9 million distance learners enrolled, online programs are projected to surpass offline, supported by Vitru, Cogna, and YDUQS scaling national networks.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

46.3% |

São Paulo and Rio host top universities; high private enrollment; mature EdTech ecosystem |

|

South |

19.4% |

Strong public universities; industrial workforce; high digital infrastructure penetration in Rio Grande do Sul |

|

Northeast |

16.2% |

Fastest-growing region; federal investment; rising distance learning enrollment in Bahia, Pernambuco |

|

Central-West |

10.1% |

Brasilia public sector demand; agribusiness-driven workforce upskilling needs across Mato Grosso, Goias |

|

North |

8.0% |

Government-led access programs; growing distance learning adoption in Para and Amazonas regions |

The Southeast commands 46.3% of national revenue in 2025, driven by its concentration of leading universities, large student populations, and strong private sector presence, making it Brazil’s primary hub for higher education institutions and EdTech activity.

The South contributes 19.4% in 2025, supported by strong university networks and regional economic activity. The Northeast at 16.2% is expanding due to increased access and distance learning growth, while Central West and North together represent 18.1% in 2025, driven by government initiatives, improving connectivity, and rising adoption of flexible higher education programs.

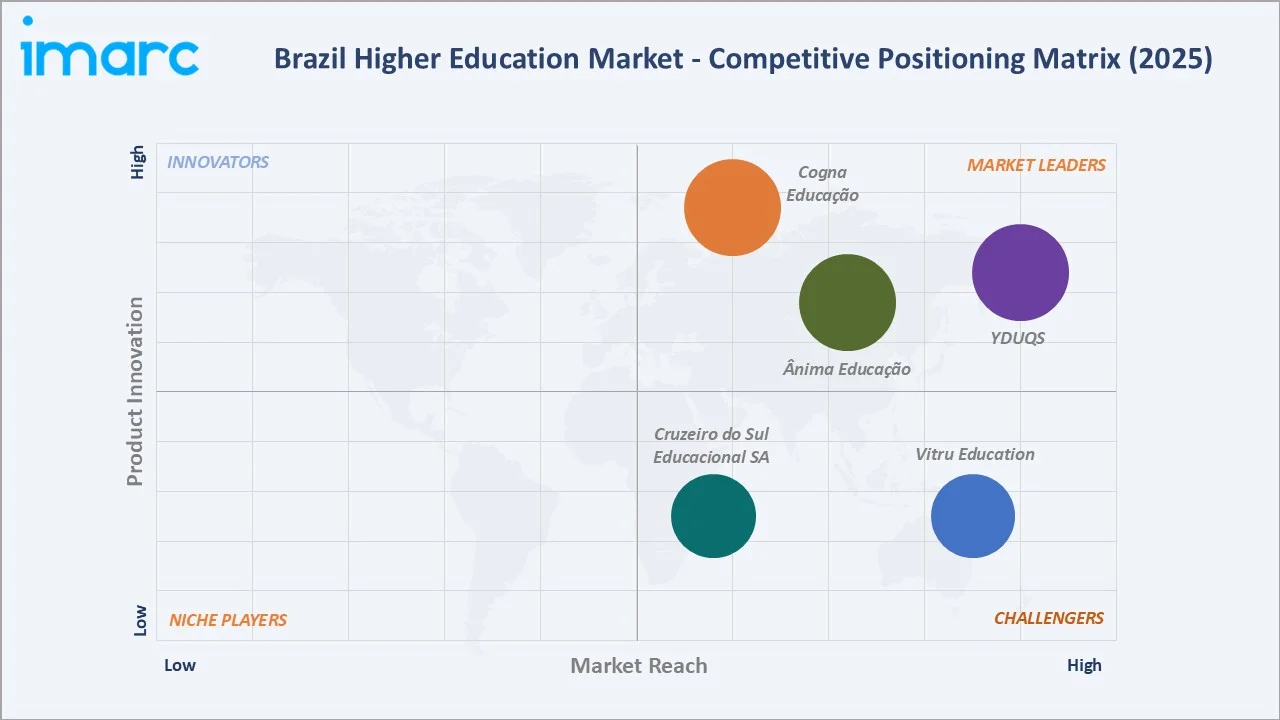

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Cogna Educação |

Kroton |

Leader |

Largest scale, distance learning network, K-12 + higher ed |

|

YDUQS |

Estacio / Ibmec / IDOMED |

Leader |

Premium brands, medical schools, professional education |

|

Ânima Educação |

UniBH / UNA / Unimonte |

Leader |

Premium positioning, medical education, Inspirali platform |

|

Cruzeiro do Sul Educacional SA |

Cruzeiro do Sul / UNICID / UNIFRAN |

Challenger |

Multi-state network, balanced online and on-campus mix |

|

Vitru Education |

Uniasselvi / UniCesumar |

Challenger |

Distance learning leader, low-cost online programs |

The Brazil higher education market combines large higher education operators with global EdTech vendors. Cogna Educação is Brazil’s leading private education group, serving over 1.2 million higher education students and more than 2.5 million learners overall, with nationwide presence across campuses and distance-learning centers.

Key Company Profiles

Cogna Educação

Cogna Educação, headquartered in Belo Horizonte, is one of Brazil’s largest private education groups, serving over one million students across higher education and K-12 segments. The company reported net revenue of around R$ 6,422.4 million in 2024, driven by its Kroton and Anhanguera brands.

- Product & Service Portfolio: Cogna operates across higher education (Kroton, Anhanguera), K-12 solutions (Vasta Educação), and content/publishing (Saber), offering undergraduate, distance learning, digital education platforms, and learning systems for schools.

- Recent Developments: Cogna Educação S.A. surged over 200% in 2025, the strongest gain on Brazil’s Ibovespa, and added ~13% in 2026, driven by its return to profitability in 2024 after restructuring. The turnaround was supported by cost optimization, campus closures, and debt reduction, alongside a continued shift toward digital education. Institutional investors such as XP Asset Management and Inter Asset have increased exposure, citing improving earnings outlook and attractive valuations.

- Strategic Focus: Cogna prioritizes distance learning expansion, EdTech platform integration, and operational efficiency through centralized academic and administrative systems.

YDUQS

YDUQS, headquartered in Rio de Janeiro, is one of Brazil’s leading private higher education groups, serving over one million students across on-campus and distance learning formats. The company reported net revenue of R$ 5.4 billion in 2024, supported by strong growth in digital and medical education segments.

- Product & Service Portfolio: YDUQS operates higher education and professional learning platforms including Estácio (undergraduate and EAD), Ibmec (business education), Idomed (medical schools), Damásio (legal education), Wyden (regional institutions), and Qconcursos (digital test preparation).

- Recent Developments: YDUQS Participações S.A. continues expanding its Idomed medical education network, which reached 17+ medical schools across Brazil by 2025, alongside ongoing seat additions and regional expansion. The company is also accelerating digital transformation, deploying 100+ AI and data-driven initiatives to improve operational efficiency and student engagement, including faster document processing and retention-focused analytics.

- Strategic Focus: YDUQS focuses on premium professional education, medical school expansion, and digital transformation across its Estácio undergraduate base.

Ânima Educação

Ânima Educação, headquartered in São Paulo, is a leading Brazilian private higher education group focused on premium institutions and medical education. The company serves ~350,000–380,000 students and reported net revenue of R$ 4,023.7 million in 2025, driven by high-value programs and its Inspirali platform.

- Product & Service Portfolio: Ânima operates premium universities (UniBH, UNA, São Judas, Universidade Anhembi Morumbi), the Inspirali medical education platform, and other academic brands, offering undergraduate, postgraduate, and medical programs across on-campus and digital formats.

- Recent Developments: Ânima Educação strengthened its Smart Campus and hybrid education model across 2025, focusing on flexible, technology-enabled learning formats. The initiative integrates digital tools, blended (on-campus + online) delivery, and employability-driven curricula, supporting scalability and improved student outcomes as part of its growth strategy.

- Strategic Focus: Ânima prioritizes premium education, expansion of its Inspirali medical platform, debt reduction, and selective investment in high-margin academic and healthcare-focused programs.

Market Concentration Analysis

The Brazilian higher education market is moderately concentrated at the top, with the Five largest operators - Cogna Educação, YDUQS, Ânima Educação, Cruzeiro do Sul Educacional SA, and Vitru Education - accounting for approximately 35-40% of total private enrollment in 2025, supported by national reach and scale advantages.

Fragmentation persists at the regional and local levels, with thousands of independent and Catholic universities competing for niche academic segments and state-specific demand. This bifurcated structure mirrors mature private education markets seen in the United States and Mexico.

Consolidation in Brazil’s higher education sector continues through strategic M&A and restructuring. Vitru Educação completed the acquisition of UniCesumar in 2023 to expand scale in distance learning, while Cogna Educação S.A. and YDUQS Participações S.A. explored merger discussions without a finalized deal. Meanwhile, Ânima Educação S.A. has pursued portfolio optimization and deleveraging. These developments reflect a broader industry shift toward scale, efficiency, and profitability.

Investment & Growth Opportunities

Fastest-Growing Segments

Online learning remains the fastest-growing segment in Brazil, driven by strong enrollment in distance education programs (EAD), which already account for a significant share of new admissions (as per INEP). Growth is supported by demand in business, IT, and education fields. Cloud-based solutions are rapidly replacing on-premise systems due to SaaS LMS adoption and digital campus initiatives.

Emerging Market Expansion

The Northeast region is a key growth area, supported by government access programs and increasing demand from Tier-2 and Tier-3 cities. States such as Bahia and Pernambuco are expanding higher education participation, driven by urbanization and affordability-focused private institutions.

Venture & Strategic Investment Trends

Brazil’s EdTech sector has attracted strong investor interest, with funding flowing into AI-based learning platforms, digital credentials, and student financing solutions. Major investors such as SoftBank and Advent International have been active in education and EdTech-related investments.

Future Market Outlook (2026-2034)

The Brazil higher education market is projected to expand from USD 597.9 Million in 2025 to USD 4,159.3 Million by 2034 at a CAGR of 24.05%, representing growth of more than USD 3.5 billion driven by digital adoption and online enrollment.

Three transformational trends will reshape Brazilian higher education through 2034. AI-powered personalized learning will scale across institutions; cloud-native campus platforms will become standard; and microcredentials will redefine how Brazilians acquire industry-aligned skills throughout adult careers.

By 2034, Brazilian higher education is expected to evolve into a digitally enabled, hybrid-first, learner-centric system. Operators investing in AI, mobile learning, and cloud infrastructure are likely to capture disproportionate value as enrollment, programs, and revenue continue migrating online.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024-2025 with university CIOs, MEC officials, EdTech executives, and senior leaders at Cogna, YDUQS, Ânima, Cruzeiro do Sul, and Vitru, supplemented by student panel surveys.

Secondary Research

Secondary sources include MEC and INEP institutional census data, company annual reports (Cogna, YDUQS, Ânima, Cruzeiro do Sul, Vitru), CAPES research databases, S&P and Fitch credit reports, World Bank education data, and Brazilian higher education trade publications.

Forecasting Models

Market estimates and forecasts were built using top-down and bottom-up models, integrating GDP growth, working-age population trends, FIES disbursement data, and EdTech adoption curves under base, optimistic, and conservative scenarios through 2034.

Brazil Higher Education Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Modes Covered | On-Premises, Cloud-Based |

| Course Types Covered | Arts, Economics, Engineering, Law, Science, Others |

| Learning Types Covered | Online, Offline |

| End Users Covered | State Universities, Community Colleges, Private Colleges |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Cogna Educação, YDUQS, Ânima Educação, Cruzeiro do Sul Educacional SA, Vitru Education, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil higher education market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil higher education market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil higher education industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Higher Education Market Report

The Brazil higher education market was valued at USD 597.9 Million in 2025, driven by digital learning adoption, expanding private enrollment, and rising EdTech investment.

The market is projected to reach USD 4,159.3 Million by 2034, growing at a CAGR of 24.05% during 2026-2034, supported by online learning expansion.

Cloud-based deployment leads with a 57.6% share in 2025, driven by universities migrating to scalable SaaS platforms that lower IT costs and support hybrid learning.

Offline learning leads with a 61.5% share in 2025, anchored by traditional in-person undergraduate programs in engineering, law, medicine, and the natural sciences.

The Southeast leads with a 46.3% share in 2025, anchored by São Paulo and Rio de Janeiro hosting top universities, EdTech firms, and the largest private operators.

Key drivers include distance learning expansion, FIES financing, private sector consolidation, cloud platform adoption, AI-powered analytics, and government investment in tertiary access programs.

The Northeast is the fastest-growing region, fueled by federal investment, distance learning enrollment growth, and Tier-2 city expansion in Bahia and Pernambuco.

Leading companies include Cogna Educação, YDUQS, Ânima Educação, Cruzeiro do Sul Educacional SA, and Vitru Education, alongside major EdTech vendors.

Online learning holds 38.5% in 2025 and is the fastest-growing segment, supported by relaxed MEC regulations and over 4.3 million enrolled distance learners.

Cloud adoption is driven by lower IT costs, scalability, integration with mobile learning, support for hybrid models, and improved analytics for student outcomes.

AI tutors, cloud LMS, mobile-first platforms, and student analytics are improving retention, scaling personalized learning, and enabling data-driven academic decisions across institutions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)