Brazil Power Market Size, Share, Trends and Forecast by Generation Source, and Region 2026-2034

Brazil Power Market Size, Share, Trends & Forecast (2026-2034)

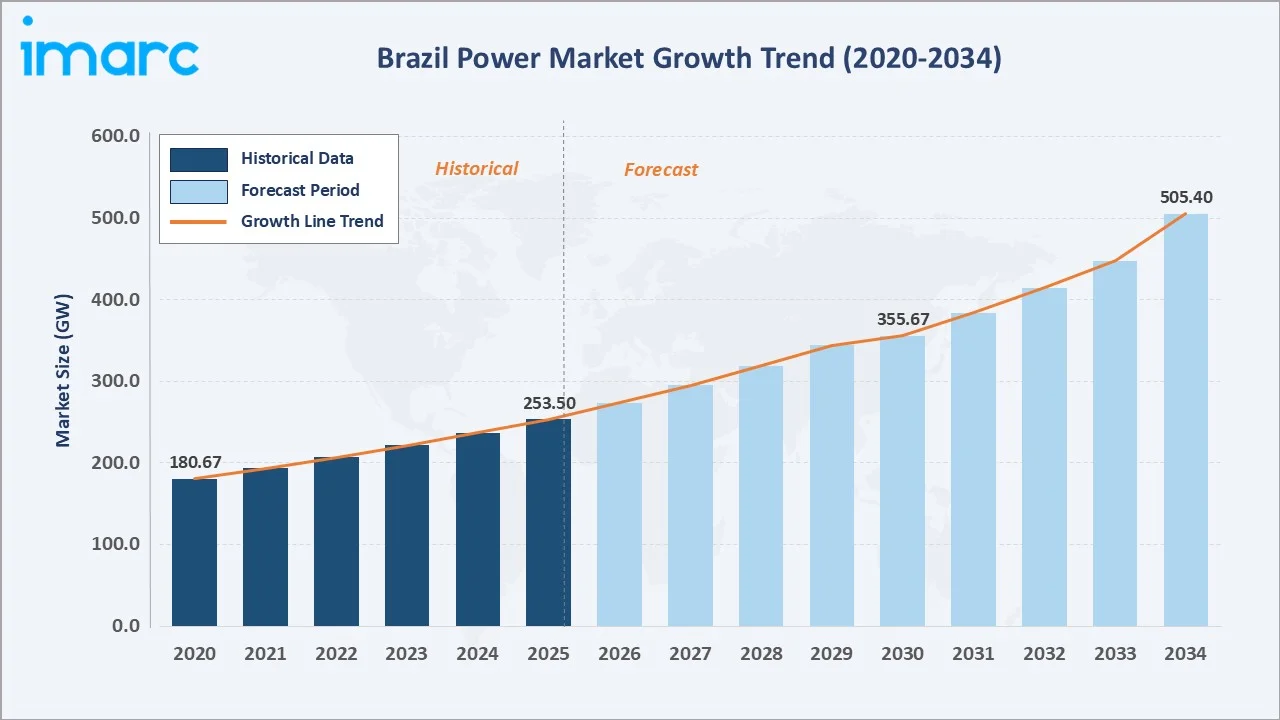

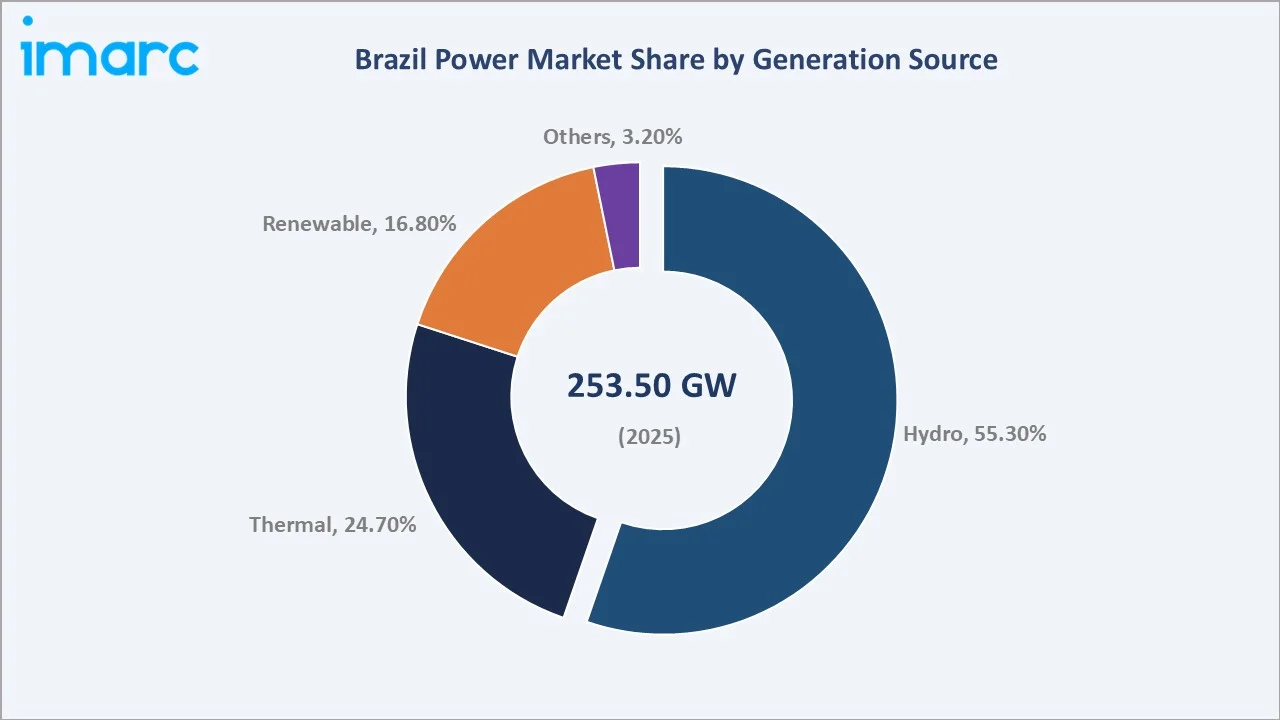

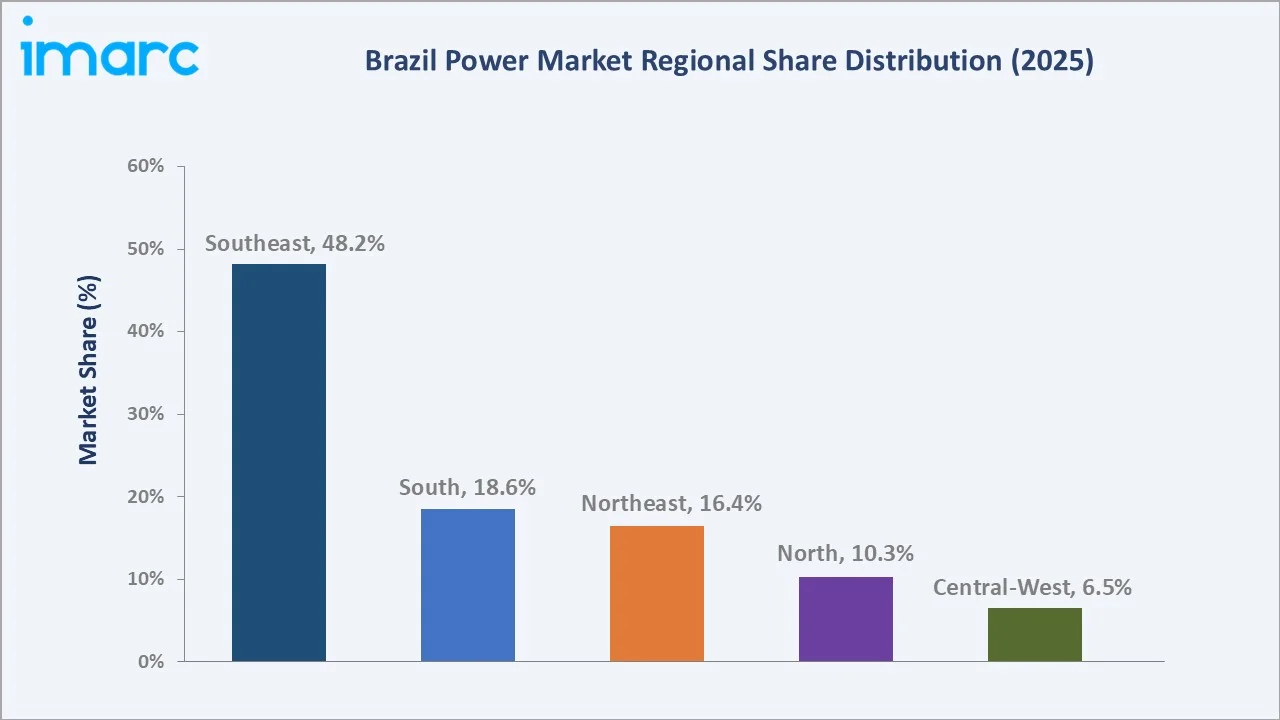

The Brazil power market reached an installed capacity of 253.50 GW in 2025 and is projected to reach 505.40 GW by 2034, expanding at a CAGR of 7.01% during the forecast period (2026-2034). Growth is driven by Brazil’s world-leading renewable energy expansion, with Brazil topped the G20 countries in renewable electricity, with renewables accounting for 89% of its energy supply in 2023, the landmark Eletrobrás privatization, rising industrial electricity demand, and the government’s net-zero 2050 pathway. Hydropower dominates at 55.3% of current installed capacity. The Southeast holds the largest regional share at 48.2%.

Market Snapshot

|

Metric |

Value |

|

Installed Capacity (2025) |

253.50 GW |

|

Forecast Installed Capacity (2034) |

505.40 GW |

|

CAGR (2026-2034) |

7.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Southeast (48.2% of installed capacity, 2025) |

|

Fastest Growing Region |

Northeast (CAGR ~9.8%, wind & solar, 2026-2034) |

To get more information on this market, Request Sample

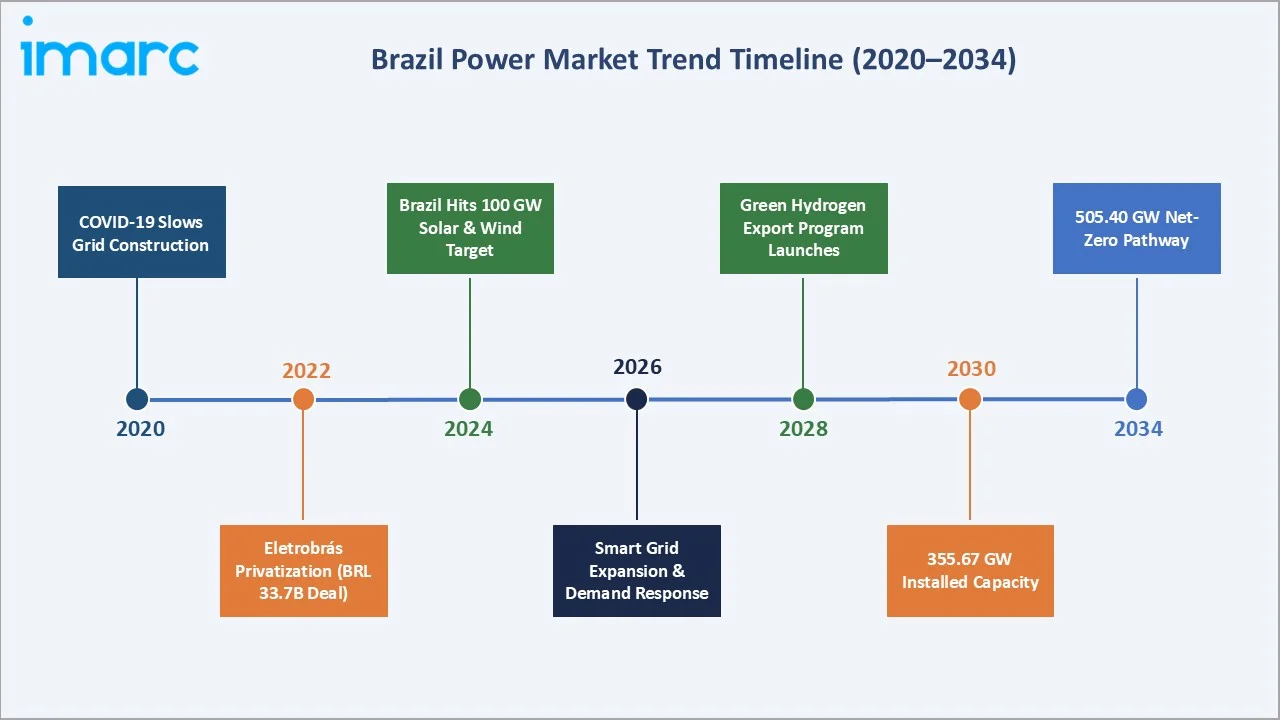

The Brazil’s installed power capacity grew from 180.67 GW in 2020 to 253.50 GW in 2025, driven by record renewable auctions, grid expansion, and industrial demand recovery post-COVID-19. By 2030, capacity is forecast to reach 355.67 GW and to 505.40 GW by 2034.

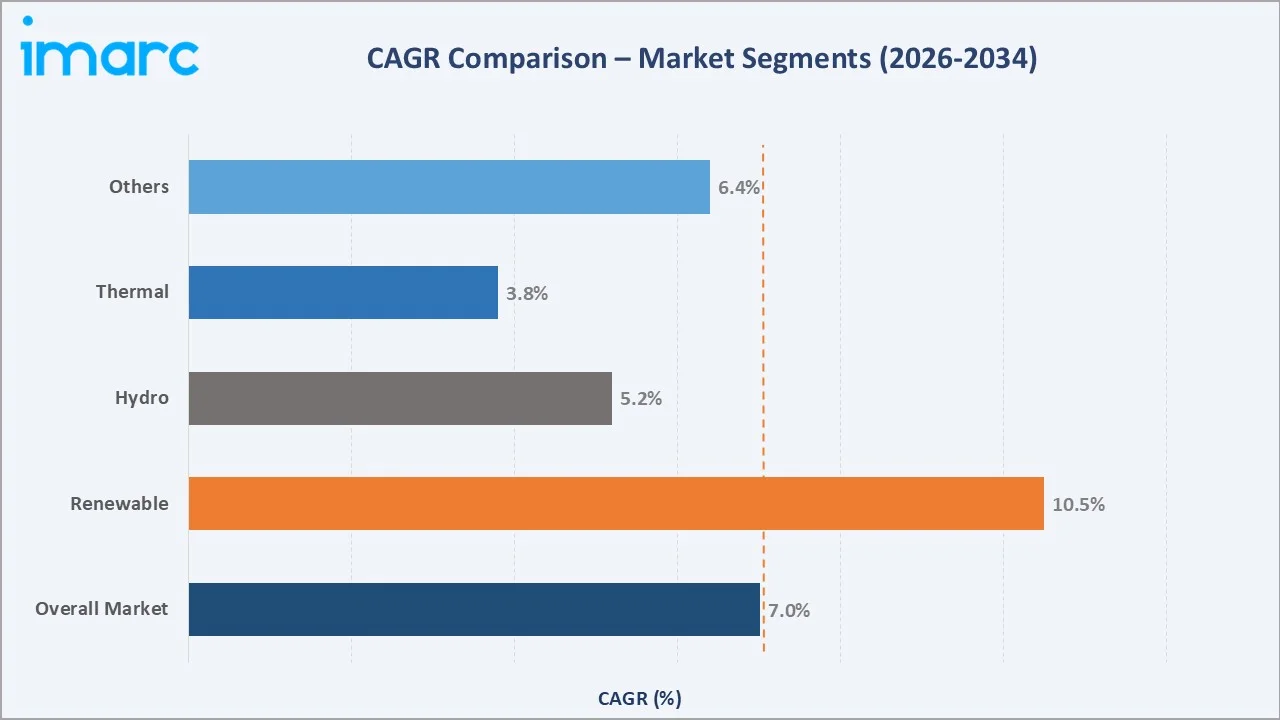

The CAGR across generation source segments, with renewable energy leads at ~10.5% CAGR, reflects Brazil’s structural energy transition as solar and wind replace thermal baseload. Hydro at ~5.2% CAGR benefits from incremental small hydro plant additions. Thermal at ~3.8% CAGR grows more slowly as gas-fired peakers complement intermittent renewables rather than expand baseload thermal capacity through 2034.

Executive Summary

The Brazil power market is one of Latin America’s most dynamic energy systems, anchored by the world’s largest renewable energy base relative to total installed capacity in a major economy. From 180.67 GW in 2020, installed capacity reached 253.50 GW in 2025, driven by aggressive wind and solar additions, the commissioning of new hydropower projects, and the ongoing capacity expansion programs of Brazil’s major generators. The forecast trajectory to 505.40 GW by 2034 reflects the convergence of three powerful structural forces: Brazil’s net-zero 2050 commitment requiring a near-doubling of clean energy capacity; the structural under-electrification of the North and Centre-West regions requiring grid expansion; and the once-in-a-generation growth of solar distributed generation driven by ANEEL Resolution 482, enabling small and medium consumers to install rooftop solar systems.

Hydropower at 55.3% of installed capacity (2025) remains the backbone of Brazil’s electricity system, with iconic assets. Thermal power at 24.7% serves as critical drought-year backup and seasonal peaking capacity. Renewable sources at 16.8% are growing explosively and will overtake thermal as the second-largest generation source by approximately 2029.

The Southeast region’s 48.2% capacity dominance reflects the concentration of Brazil’s industrial, commercial, and population centers in São Paulo and Rio de Janeiro states. However, the Northeast at 16.4% (2025) is the fastest-growing region at ~9.8% CAGR, driven by the world-class wind resources and the highest solar irradiance in Brazil.

Key Market Insights

|

Insight |

Data |

|

Dominant Generation Source |

Hydro – 55.3% of installed capacity (2025) |

|

Largest Region |

Southeast – 48.2% of national capacity (2025) |

|

Fastest Growing Region |

Northeast – CAGR ~9.8%, driven by wind & solar (2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Hydro dominates at 55.3% (2025): Brazil operates the world’s second-largest hydroelectric system, Itaipu Hydroelectric Dam. Belo Monte is the largest 100% Brazilian hydropower plant with a capacity of 11,233 MW and is ranked as the third largest hydropower plant in the world.

- Southeast leads at 48.2% (2025): São Paulo state alone consumes approximately 30% of Brazil’s total electricity. The Southeast’s grid interconnects Brazil’s most complex transmission topology, including the 800 kV HVDC links from Belo Monte and Itaipu that carry power to São Paulo and Rio de Janeiro distribution grids.

- Northeast fastest growing at ~9.8% CAGR: The Brazilian Northeast country’s installed wind capacity and is the primary site of new solar utility-scale auctions, driving the market growth.

Brazil Power Market Overview

The Brazil power market encompasses the generation, transmission, distribution, and commercialization of electricity across Brazil’s national interconnected system (SIN) and isolated systems. The SIN serves 98% of the electricity market in Brazil. The power sector’s market structure combines free market energy trading (ACL) through the CCEE (Energy Trading Chamber) with regulated market concessions, creating a dual-market architecture that accommodates both large industrial consumers and regulated tariff households.

Applications span residential, commercial, industrial, and public services, including agriculture and transport. Brazil’s electricity matrix is structurally unique globally, achieving 88% renewable energy generation in 2024 primarily through hydropower supplemented by an expanding base of wind and solar. Macroeconomic influences include Brazil’s GDP growth trajectory, the electrification of transport and industrial processes under decarbonization mandates, and the government’s Ecological Transformation Plan linking energy investment to Brazil’s Nationally Determined Contribution (NDC) under the Paris Agreement.

Market Dynamics

To evaluate market opportunities, Request Sample

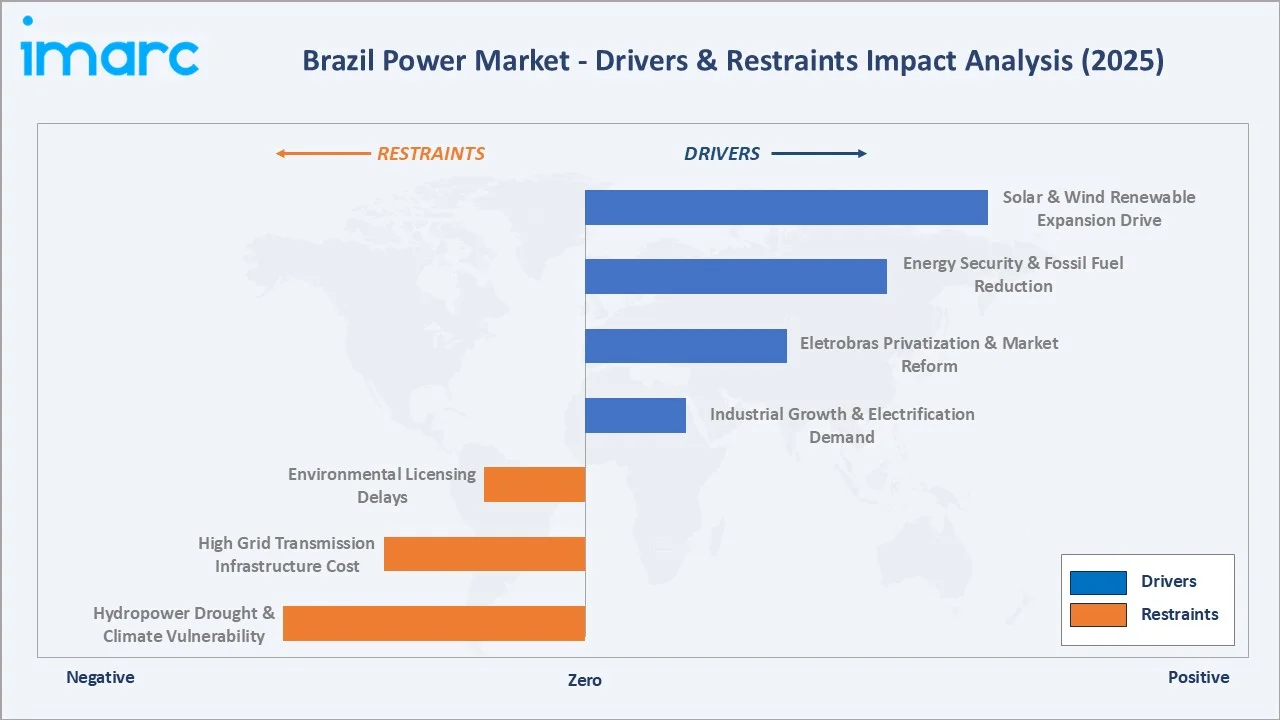

Market Drivers

- Solar and Wind Renewable Expansion: Brazil exceeded its 2030 goal of achieving 84% renewable electricity. According to the 2022-2031 Ten-Year Energy Expansion Plan (PDE) by the Energy Research Office (EPE), the country aims to reach 47 GW of solar power and 31 GW of wind power by 2030.

- Eletrobrás Privatization and Market Reform: The 2022 Eletrobrás privatization unlocked Brazil’s largest-ever energy investment program, with the company committing BRL29.3bn (US$5.7bn) in sales. The privatization also created new competitive dynamics as Eletrobrás’s former monopoly assets now operate under private-sector efficiency mandates, improving dispatch optimization and encouraging new renewable capacity additions through competitive auctions.

- Industrial Growth and Electrification: Brazil's industry electricity data was reported at 20,107.308 TOE th in 2024. The expansion of Petrobras’s offshore oil production creates significant offshore electrification opportunity, while the nascent EV market is beginning to add new flexible demand segments to the power grid.

Market Restraints

- Hydropower Vulnerability to Climate Change: Over 77% of total electricity demand is supplied by hydropower in Brazil, which creates systemic exposure to drought years. Climate models project increasing drought frequency in Southeast Brazil’s critical river basins, creating a structural reliability risk that can only be addressed by diversifying the generation matrix toward non-hydro renewables and battery storage.

- Environmental Licensing Complexity: Brazil’s IBAMA environmental licensing process requires extensive impact assessments, indigenous community consultations, and biodiversity studies for new power projects, particularly in Amazonian and Cerrado biomes.

Market Opportunities

- Green Hydrogen Production and Export: Brazil's green hydrogen production leverages the country's significant renewable energy potential, with current projects totaling 99 GW of solar and 25 GW of wind capacity. In the federal government auction held in October 2022, set to begin supply in 2027, wind and solar energy were priced at BRL 175 ($34.72)/MWh and BRL 171/MWh, respectively.

- Offshore Wind Development: Brazil’s 8,500 km coastline and offshore wind resources represent high technically exploitable offshore wind potential. Companies in Brazil have registered interest in Brazilian offshore wind concessions, representing a potential new energy investment wave.

Market Challenges

- Regulatory Tariff Complexity and Sector Debt: Brazil’s electricity sector carries billions in sector liability, accumulated through cross-subsidies, stranded hydro contracts, and emergency thermal dispatch costs, which is gradually recovered through consumer tariff surcharges.

- Land Use Conflict and Indigenous Rights: Large-scale renewable energy development in Brazil’s interior increasingly conflicts with indigenous land demarcation areas, quilombola communities, and traditional communities protected under Brazil’s Constitution and ILO Convention 169.

Emerging Market Trends

1. Distributed Solar Generation Revolution

Brazil’s distributed solar market, accelerated by ANEEL Resolution 482 and its successor Resolution 1000, enabling net metering and shared generation, became the world’s fastest-growing residential solar market. Brazil's solar installed capacity reached 50 GW.

2. Offshore Wind Sector Emergence

Brazil’s offshore wind regulatory framework is triggering the first wave of Brazilian offshore wind investment. The first Brazilian offshore wind auction is expected, with projects targeting the highly consistent southeastern coast off Rio de Janeiro and the Northeast’s Ceará coast.

3. Green Hydrogen and Power-to-X Industries

Brazil’s ecological transformation plan designates green hydrogen as a strategic export sector. The projects will require highly dedicated renewable generation capacity, creating a new category of “hydrogen-linked” renewable energy procurement contracts that are transforming Northeast Brazil’s electricity market dynamics.

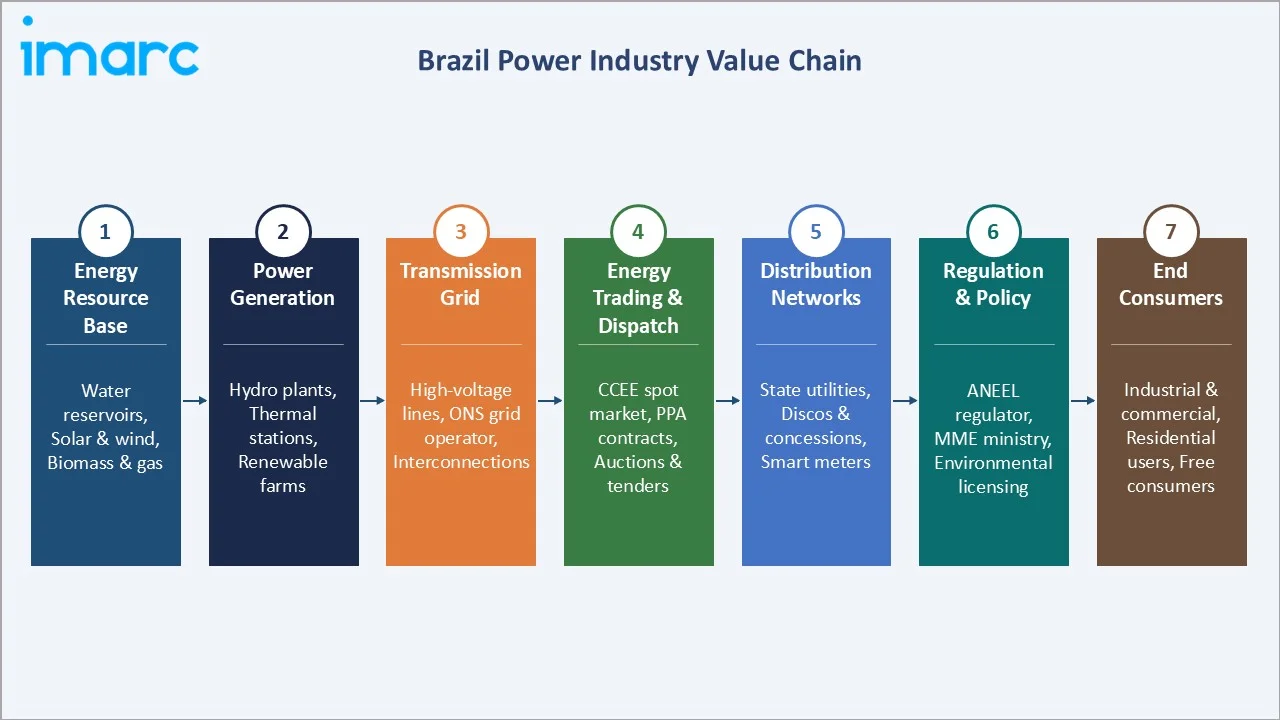

Industry Value Chain Analysis

The Brazil power value chain spans primary energy resource extraction or harvesting through large-scale power generation, high-voltage transmission across the national grid, regional distribution to end users, and the energy commercialization layer that mediates market pricing between generators, traders, and consumers.

|

Stage |

Key Participants |

|

Primary Energy Resources |

Water resources, wind corridors (Northeast), solar irradiance (all regions), natural gas, sugarcane biomass |

|

High-Voltage Transmission |

ONS (National Grid Operator); Eletrobras; Taesa |

|

Distribution Networks |

Neoenergia (Iberdrola), CEMIG Distribuição, COPEL Distribuição, Equatorial Energia |

|

Energy Trading & Commercialization |

Free market traders; long-term PPAs; distributed generation marketplace |

|

End-Use Consumers |

Industrial sector, residential, commercial, rural & public services |

The generation stage captures the highest revenue in the value chain. Distribution utilities are the largest single point of consumer interaction. WEG, Brazil’s homegrown electrical equipment manufacturer, uniquely occupies the equipment OEM layer, supplying transformers, motors, and switchgear to both domestic utilities and the global market.

Technology Landscape in the Brazil Power Industry

Hydropower Modernization and Efficiency Enhancement

Brazil’s aging hydropower fleet, with many plants commissioned in the 1970s–1990s, is undergoing systematic turbine replacement programs that increase generation efficiency by 5–10% without new environmental licensing. In January 2025, Omexom Brazil signed an engineering, procurement, and construction (EPC) contract with the Capim Branco Energia Consortium (CCBE) to undertake a major modernization of the Amador Aguiar I and II hydroelectric power plants.

Onshore and Offshore Wind Technology

Brazil’s onshore wind market has driven significant turbine technology advancement, with average hub heights. Brazil, with its nearly 7,500 km coastline and abundant offshore wind resources that offer capacity factors exceeding 60%, has the potential to emerge as a global leader in offshore wind energy. The rising interest in offshore wind resulted in a significant increase in environmental license applications, with over 176 GW of requests, averaging 2.7 GW per project.

Solar PV and Bifacial Module Technology

Brazil’s solar market, with installed capacity recently reached 50 GW in 2024, transitioned to primarily bifacial modules, achieving efficiency, with utility-scale LCOEs, making solar competitive with all conventional generation on an unsubsidised basis.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Generation Source | Hydro | 55.3% |

2025 |

| Region | Southeast | 48.2% |

2025 |

By Generation Source

To access detailed market analysis, Request Sample

Hydropower dominates at 55.3% of installed capacity (2025). Brazil's energy regulator evaluates more than 140 hydroelectric plants nationwide, considering various factors to assess their operational quality. The sheer scale of Brazil’s hydroelectric base creates a low-cost generation foundation that enables the power system to achieve clean energy generation in average hydrological years.

Thermal power at 24.7% provides essential drought-year backup capacity. Gas-fired thermal and biomass/biogas from sugarcane ethanol processing together form a flexible thermal layer that can be dispatched quickly when hydro reservoirs drop below critical thresholds. Renewable sources at 16.8%, comprising wind, solar utility-scale, and biomass, represent the fastest-growing generation category.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Southeast |

48.2% |

São Paulo & Rio industrial electricity demand; Itaipu + large hydro plants; data centre growth in São Paulo corridor; EV charging infrastructure |

|

South |

18.6% |

Itaipu Binacional subtropical wind resources; industrial agribusiness energy demand in Paraná & Rio Grande do Sul |

|

Northeast |

16.4% |

World-class wind resources; highest solar irradiance in Brazil; offshore wind potential; green hydrogen export corridor |

|

North |

10.3% |

Amazon hydropower; isolated system electrification; mineral industry electricity demand |

|

Central-West |

6.5% |

Agribusiness electricity demand; biomass/biogas from sugarcane; distributed solar generation growth; new capital infrastructure |

The Southeast’s 48.2% capacity dominance (2025) reflects the concentration of Brazil’s economic activity in this region. The region hosts Brazil’s largest industrial free market electricity consumers and the expanding data centre cluster in Tamboretê (Campinas metropolitan area).

The Northeast at 16.4% (2025) is the most dynamic growth region. The region’s wind resources achieve capacity factors of 50–60%, far exceeding the global average of 25–35% for onshore wind. The North’s 10.3% share (2025) is dominated by Amazonian hydropower but also encompasses isolated systems in remote communities served by diesel generators.

Competitive Landscape

The Brazil power market is moderately concentrated at the generation level and moderately fragmented at the distribution level. Eletrobras post-privatisation controls approximately 27–30% of national generation capacity and 40%+ of transmission line length, creating a structurally dominant market position.

|

Company Name |

Key Divisions |

Market Position |

Core Strength |

|

Eletrobras |

Energy Comercialization, Energy Generation, and Energy Transmission |

Dominant Market Leader |

Brazil’s one of the largest power company post-privatisation, largest transmission network operator |

|

ENGIE Group |

Hydroelectric Plants, Solar Plants, Wind Plants, Biomass Plants |

Market Leader |

Brazil’s largest private-sector power generator; 100% renewable ambition |

|

Neoenergia |

Wind, Hydro and Solar Energy Generation, Power Distribution and Transmission |

Strong Challenger |

Prominent distribution utility by number of consumers, Iberdrola’s primary Brazil platform |

|

CEMIG |

Wind Power Plants, Photovoltaic Plants, Hydroelectric Power Plants |

Established |

Minas Gerais state utility, CEMIG GT transmission and CEMIG GT renewable pipeline |

|

Eneva |

Power Energy, On-Grid, Off-Grid, and Energy Solutions |

Specialist |

Brazil’s leading gas-fired thermal generator, crucial grid backup for drought years; unique gas supply chain integration |

|

Casa dos Ventos |

Free Energy, Energy Supply Contracts, Energy Self-production |

Renewable Specialist |

Brazil’s largest independent wind power developer |

The next five generators collectively hold approximately 35–38% of generation capacity, with independent power producers and distributed generators. Distribution is organised by state concession areas, with major distribution groups collectively serving Brazil’s electricity consumers.

Key Company Profiles

Eletrobras

Eletrobras is Brazil’s largest power company and was privatised in June 2022.

- Portfolio: Energy Commercialization, Energy Generation, and Energy Transmission.

- Recent Developments: In June 2025, Hitachi Energy extended its service contract with Eletrobras for the Rio Madeira high-voltage direct current (HVDC) system.

- Strategic Focus: Generation efficiency and capacity expansion; transmission network modernisation; new renewable auctions; international energy export via new HVDC corridors to Argentina and Uruguay.

ENGIE Group

Engie is the largest private-sector power generator in Brazil by installed capacity. The company operates a diversified portfolio encompassing hydropower, wind, solar, and biomass plants.

- Portfolio: Hydroelectric Plants, Solar Plants, Wind Plants, Biomass Plants.

- Recent Developments: In March 2026, ENGIE awarded the concessions to build and operate 143 kilometers of transmission lines and 5 synchronous condenser units at the latest Brazilian Electric Energy Agency (ANEEL) auction.

- Strategic Focus: 100% renewable portfolio by 2030 (divesting remaining gas assets); green hydrogen production as long-term strategic business; Northeast wind & solar expansion; ENGIE group synergies for offshore wind development in Brazilian waters.

Neoenergia

Neoenergia is the primary vehicle for Spanish utility Iberdrola’s Brazilian operations and is the country’s largest distribution utility by number of consumer connections.

- Portfolio: Wind, Hydro and Solar Energy Generation, Power distribution and transmission.

- Recent Developments: In November 2025, Neoenergia, in collaboration with the Governments of Brazil and Pernambuco, officially launched the construction of the Noronha Verde Solar Plant at an event in Belém (Pará), with an investment of R$350 million.

- Strategic Focus: Smart grid investment as distribution regulatory return driver; offshore wind as next generation growth platform; Iberdrola technology transfer for BESS integration; green hydrogen upstream supply through Northeast renewable PPA portfolio; Latin America’s largest utility-scale solar pipeline.

Eneva

Eneva is Brazil’s leading thermal power generator and a unique integrated energy company that combines natural gas E&P (exploration and production) with gas-to-power generation in an integrated business model.

- Portfolio: Power Energy, On-Grid, Off-Grid, and Energy Solutions.

- Recent Developments: In October 2024, Eneva launched a share offer to raise around 4.2 billion reais ($774 million) to help fund power generation projects, natural gas exploration and possible M&A activity.

- Strategic Focus: Gas supply security through integrated E&P + power model; Northeast grid reliability insurance as strategic market position; expansion into LNG import capacity to supplement domestic gas production for peak dispatch; diversification into green hydrogen using existing thermal infrastructure platforms.

Market Concentration Analysis

The Brazil power generation market exhibits moderate concentration. Eletrobras at approximately 27–30% of national generation capacity occupies a structurally dominant position, the legacy of its 60-year history as Brazil’s state-owned national power company. The top five generation groups collectively account for approximately 55–60% of total installed generation capacity, with the remaining 40–45% distributed among independent power producers and distributed generators.

Distribution is structured around state concession monopolies, with the largest groups each holding geographically defined distribution territories. This regulated monopoly structure creates moderate concentration in distribution by design. M&A activity has intensified since the Eletrobras privatisation created a template for further energy sector privatisations. State government-owned utilities are at various stages of partial privatisation, creating consolidation opportunities.

Investment & Growth Opportunities

Fastest Growing Segments

Non-hydro renewables (CAGR ~15.2%), energy storage, and offshore wind represent the three highest-growth investment vectors. Brazil’s solar distributed generation market, the world’s fastest-growing prosumer market in 2023–2024, is generating high investments in cumulative private investment that does not appear in traditional capacity auction statistics.

Emerging Markets Within Brazil

The North region’s isolated system electrification, the Northeast’s green hydrogen industrial corridor, the Centre-West’s agribusiness energy autonomy drive, and the offshore wind frontier along Brazil’s 8,500 km coastline each represent distinct multi-billion-real investment frontiers that have received limited investor attention relative to the Southeast’s established market.

Venture and Institutional Investment Trends

BNDES, Brazil’s national development bank, committed investments in green financing for energy projects, including green hydrogen, distributed solar, and offshore wind. International institutional investors have all made significant Brazil renewable energy platform investments since 2020.

- Key investment themes: Offshore wind development rights, green hydrogen electrolysis & ammonia export, large-scale BESS, EV charging infrastructure powered by renewables, and agrivoltaics in agricultural heartland states.

- Government incentives: REIDI (infrastructure income tax exemption), BNDES Finame green equipment financing, ANEEL accelerated permitting for strategic projects, and PIS/COFINS exemptions for renewable energy equipment manufacturing under the new industrial policy frame.

Future Market Outlook (2026-2034)

The Brazil power market is positioned for sustained, strong-growth expansion through 2034. From 253.50 GW in 2025, installed capacity is forecast to reach 505.40 GW by 2034, a near-doubling of the national energy infrastructure, representing an absolute capacity addition of 251.9 GW. This expansion is structurally driven by three interlinked imperatives: Brazil’s net-zero 2050 commitment requiring clean energy capacity to grow at twice the rate of demand; the new industrial economy being built around green hydrogen and green steel that requires dedicated large-scale renewable generation supply; and the electrification of transport, heating, and industrial processes that will increase electricity demand.

Between 2026 and 2030, the defining transformation will be the crossover of non-hydro renewables (wind + solar) surpassing thermal power as Brazil’s second-largest generation source, and by approximately 2030–2031, approaching hydro’s absolute installed capacity for the first time. The 2030–2034 period will be defined by Brazil’s emergence as a global green energy exporter, a structural transformation with no precedent in the country’s economic history. Green hydrogen pipelines and liquid ammonia terminals in Ceará and Piauí will be operational, exporting to European and Asian markets under multi-decade off-take agreements.

Research Methodology

Primary Research

Primary research encompassed structured interviews with 120+ industry stakeholders in 2025, including generation company executives, ANEEL regulatory officers, ONS grid operations staff, distribution utility investment directors, energy traders, and independent power project developers. Geographic coverage spanned São Paulo, Rio de Janeiro, Brasília, Recife, and Fortaleza. Primary insights validated capacity projections, auction pipeline assessments, and regional market dynamics.

Secondary Research

Secondary research encompassed ANEEL installed capacity statistics, ONS system operation data, EPE (Energy Research Company) Decennial Energy Plan (PDE 2032), CCEE energy trading data, BNDES project financing approvals, IBGE economic statistics, company annual reports, B3 investor presentations, and IRENA renewable energy data. Over 240 secondary sources were reviewed.

Forecasting Models

Capacity forecasts were developed using a bottom-up project pipeline aggregation validated against top-down. Key inputs include ANEEL auction schedules, BNDES green financing commitments, renewable LCOE trajectories, government electrification targets, and climate scenario analysis for hydrological risk adjustment. Three-scenario modelling was applied across 2026–2034.

Brazil Power Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Generation Sources Covered | Thermal, Hydro, Renewable, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Companies Covered | Eletrobras, ENGIE Group, Neoenergia, CEMIG, Eneva, Casa dos Ventos, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Brazil power market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Brazil power market.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Brazil power industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Brazil Power Market Report

The Brazil power market had an installed capacity of 253.50 GW in 2025, projected to reach 505.40 GW by 2034, growing at a CAGR of 7.01%.

Hydropower dominates with 55.3% of installed capacity (2025), encompassing 140+ GW of river-based generation including Itaipu, Belo Monte, and Tucuruí.

The Southeast region leads with 48.2% of national installed capacity (2025), reflecting São Paulo and Rio de Janeiro’s concentration of industrial and residential electricity demand.

Renewables are the fastest growing at ~10.5% CAGR, with Brazil adding 50 GW in 2024 alone.

Key companies include Eletrobras, ENGIE Group, Neoenergia, CEMIG, Eneva, and Casa dos Ventos.

Eletrobrás was privatized in June 2022, the largest energy privatization in history, mandating new investment and new capacity auction commitments.

Brazil is diversifying through wind and solar, battery storage auctions, and thermal emergency contracts that activate during drought years when hydro reservoirs fall below critical thresholds.

Key trends include distributed solar revolution (50 GW by 2024), free energy market expansion to SMEs, offshore wind sector emergence, green hydrogen export corridor development, and battery storage integration.

Brazil’s 8,500 km coastline holds exploitable offshore wind potential. ANEEL published the regulatory framework in 2023, with first commercial auctions.

Top opportunities include offshore wind development rights, green hydrogen & ammonia export infrastructure, large-scale BESS, EV charging powered by renewables, and agrivoltaics in agricultural heartland states.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade