Bronchodilators Market Size, Share, Trends and Forecast by Indication, Drug Type, Route of Administration, and Region 2026-2034

Bronchodilators Market Size, Share, Trends & Forecast (2026-2034)

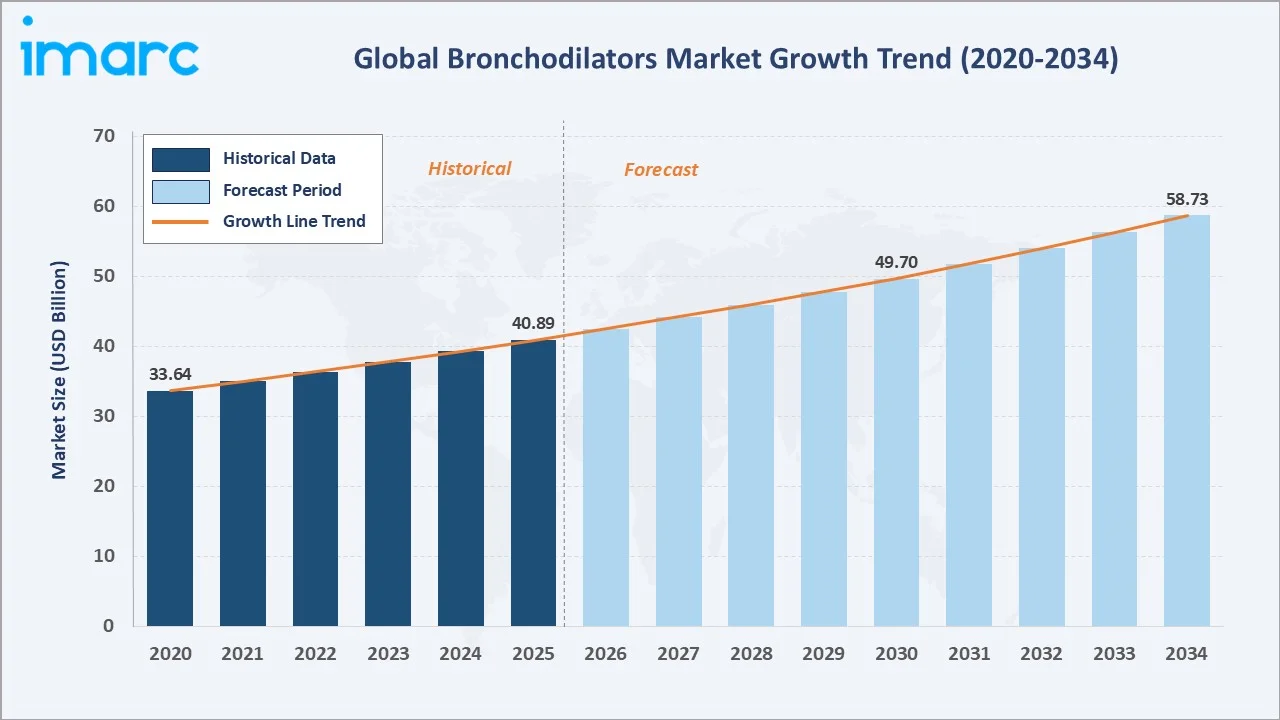

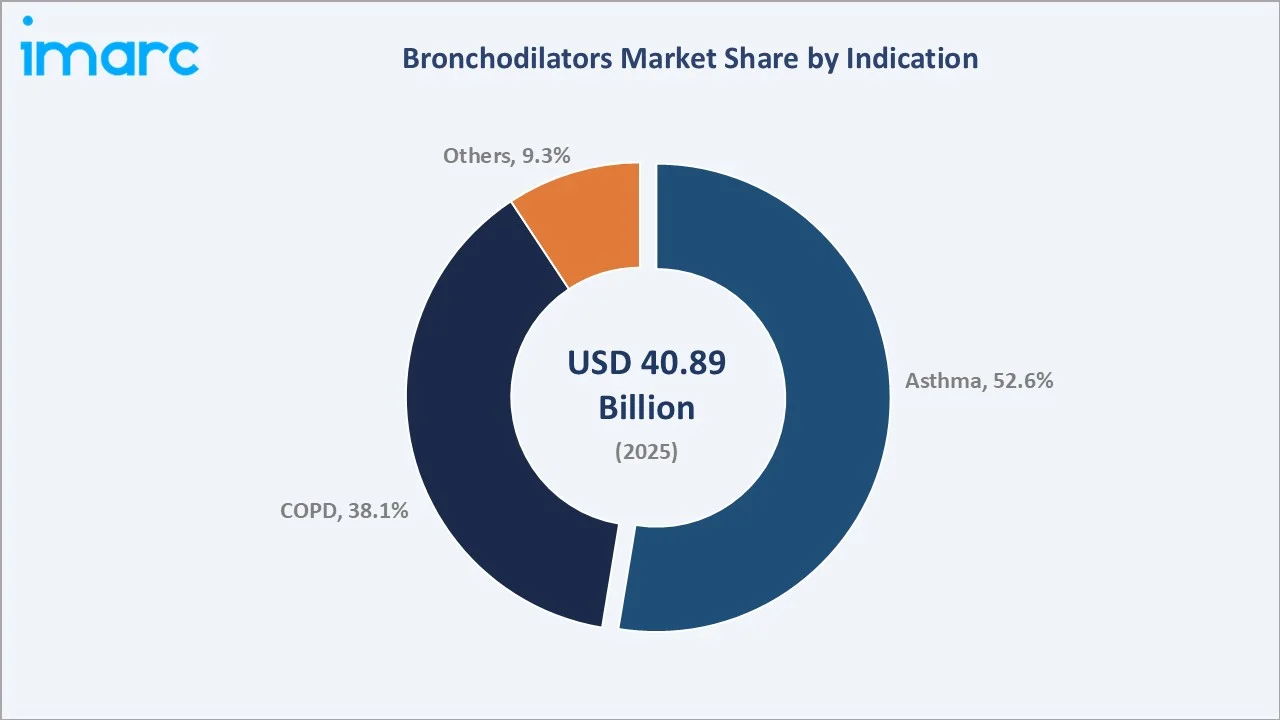

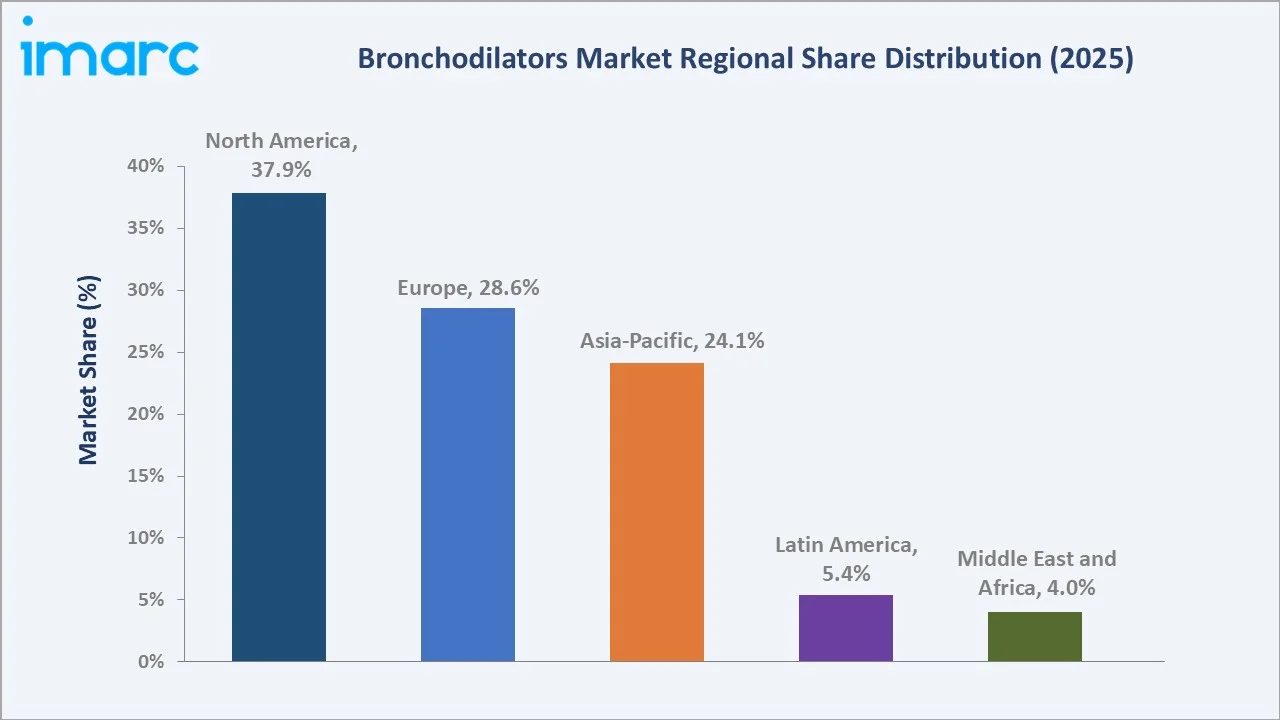

The global bronchodilators market reached USD 40.89 Billion in 2025 and is projected to reach USD 58.73 Billion by 2034, growing at a CAGR of 3.98% during 2026-2034. The market is driven by the rising prevalence of respiratory diseases such as asthma and chronic obstructive pulmonary disease (COPD), alongside growing awareness and adoption of inhalation therapies and increasing healthcare expenditure worldwide. In 2023, around 363 million individuals worldwide were affected by asthma, resulting in approximately 442,000 fatalities. This high prevalence and significant mortality burden are fueling the demand for bronchodilators, as these medications are essential for managing asthma symptoms, improving respiratory function, and preventing severe exacerbations. Asthma dominates at 52.6%. Inhaler leads the route of administration at 61.8%. North America commands 37.9% of the global market share.

Market Snapshot

| Metric | Value |

|---|---|

| Forecast Market Size (2034) | USD 30.67 Billion |

| CAGR (2026-2034) | 7.41% |

| Base Year | 2025 |

| Market Size (2025) | USD 40.89 Billion |

| Forecast Market Size (2034) | USD 58.73 Billion |

| CAGR (2026-2034) | 3.98% |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Dominant Indication | Asthma (52.6%, 2025) |

| Dominant Route of Administration | Inhaler (61.8%, 2025) |

| Leading Region | North America (37.9%, 2025) |

The market expanded from USD 33.64 Billion in 2020 to USD 40.89 Billion in 2025, anchored at USD 49.70 Billion in 2030, and forecast to reach USD 58.73 Billion by 2034. COVID-19 created meaningful demand disruptions in bronchodilators. COVID-19 respiratory symptom overlaps with asthma and COPD exacerbations increased acute bronchodilator utilization. At the same time, pandemic telemedicine adoption improved COPD management, respiratory condition monitoring, and access to inhaler adherence coaching, creating durable improvements in long-acting bronchodilator compliance rates among previously undertreated patients.

To get more information on this market, Request Sample

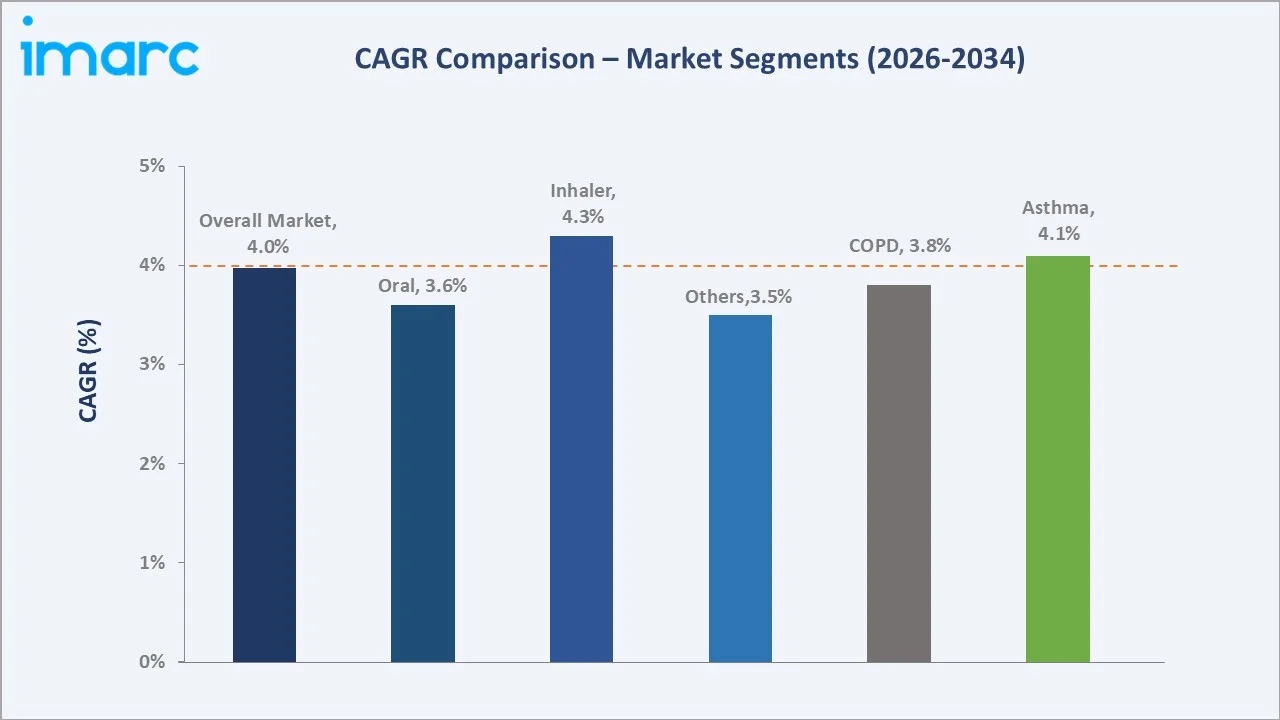

Inhaler route grows fastest at ~4.3% CAGR as the DPI platform patient experience advantages over conventional DPI and pMDI alternatives. Asthma indication grows at ~4.1% CAGR through the MART (Maintenance and Reliever Therapy) protocol adoption and growing awareness in the Asia Pacific markets, where undertreatment historically limited market development.

Executive Summary

The global bronchodilators market reached USD 40.89 Billion in 2025, representing the intersection of two converging healthcare priorities: the management of chronic respiratory diseases and the pharmaceutical industry's largest non-oncology branded drug category by revenue among chronic disease specialty medicines. Bronchodilators encompass the full spectrum of inhaled and systemic airway smooth muscle relaxants. The market is projected to reach USD 58.73 Billion by 2034.

Asthma, accounting for 52.6%, leads by indication due to rising asthma cases and increased adoption of bronchodilators. Inhaler at 61.8% dominates administration routes as the global standard of care for respiratory drug delivery, providing superior lung deposition, lower systemic absorption, and faster onset versus oral bronchodilators, with dry powder inhalers (DPIs) and pressurized metered-dose inhalers (pMDIs) serving distinct patient and prescriber preference segments. North America, at 37.9%, leads globally through US premium pricing for branded bronchodilators and the highest specialist respiratory prescription compliance rates globally.

Key Market Insights

| Insight | Data |

|---|---|

| Dominant Indication | Asthma – 52.6% share (2025) |

| Dominant Route of Administration | Inhaler – 61.8% market share (2025) |

| Leading Region | North America – 37.9% market share (2025) |

| Market Opportunity | Triple therapy for COPD; MART protocol smart inhalers; biologic add-on for severe asthma; Asia-Pacific air pollution-driven demand; biosimilar and generic inhaler growth |

Key Analytical Observations Supporting The Above Data:

- Asthma at 52.6%: The asthma segment dominates the market due to its high global prevalence, chronic nature, and the need for ongoing symptom management. Patients rely heavily on short-acting and long-acting bronchodilators to control airway constriction, prevent attacks, and improve quality of life, making asthma the leading therapeutic area driving market demand.

- Inhaler at 61.8%: Inhalers lead the market as the preferred delivery method because they provide rapid, targeted relief directly to the lungs, improve drug efficacy, and minimize systemic side effects. Their convenience, portability, and ease of use for both acute asthma attacks and chronic management make them the dominant choice among patients and healthcare providers.

- North America at 37.9%: North America dominates the market due to a high prevalence of respiratory diseases, well-established healthcare infrastructure, and strong patient awareness of asthma and COPD management. Additionally, widespread access to advanced inhalation devices and higher healthcare spending support sustained market leadership in the region.

Bronchodilators Market Overview

The global bronchodilators market encompasses all pharmacological agents that act to relax or dilate the airways (bronchi and bronchioles) by reducing smooth muscle contraction, reducing airway inflammation, or blocking bronchoconstriction signals.

The ecosystem integrates pharmaceutical manufacturers, drug delivery device companies, specialty distributors, pulmonologists and respiratory physicians, primary care prescribers managing chronic respiratory conditions, hospital emergency departments, payers, and digital health adherence platforms. Macroeconomic factors include rising healthcare expenditure, increasing government investment in respiratory disease management, and growing urbanization that contributes to higher pollution-related respiratory conditions.

Market Dynamics

To evaluate market opportunities, Request Sample

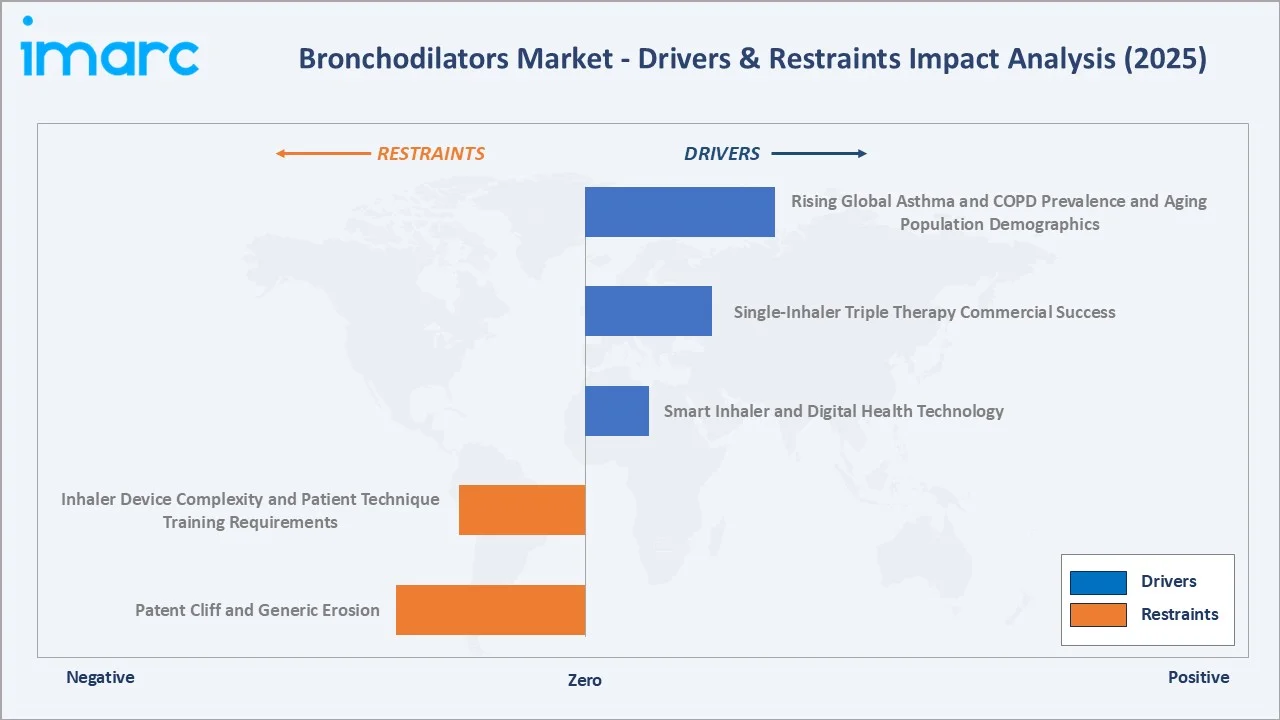

Market Drivers

- Rising Global Asthma and COPD Prevalence and Aging Population Demographics: Asthma affected 363 million people in 2023, COPD affects 4% of the total world’s population, and 3.2 million people die of it annually. This increasing global prevalence of asthma and COPD is a major driver of the bronchodilators market, as more patients require ongoing treatment to manage chronic respiratory symptoms and prevent exacerbations. By 2030, 1 in 6 people globally will be aged 60 years or over, and by 2050, the world’s population of people aged 60 years and older will be 2.1 billion. This rising aging population further amplifies this demand, since older individuals are more susceptible to respiratory diseases and often require long-term medication. Combined, these trends expand the patient pool, increase prescription volumes, and encourage the development and adoption of both short-acting and long-acting bronchodilator therapies, sustaining robust market growth worldwide.

- Single-Inhaler Triple Therapy Commercial Success: The commercial success of Single-Inhaler Triple Therapy (SITT) offers patients a convenient, all-in-one solution. This simplification improves patient adherence, reduces treatment complexity, and enhances clinical outcomes for asthma and COPD management. In May 2026, Chiesi announced that the U.S. Food and Drug Administration (FDA) approved its single-inhaler triple therapy (beclomethasone dipropionate/formoterol fumarate/glycopyrrolate; BDP/FF/G) for the long-term maintenance treatment of asthma in adult patients. Strong adoption of SITT by healthcare providers and patients has expanded prescription volumes, stimulated innovation in inhaler devices, and reinforced overall market growth in the bronchodilator segment.

- Smart Inhaler and Digital Health Technology: Smart inhalers and digital health technologies are improving medication adherence and enabling real-time monitoring of patient usage patterns. These devices track inhalation technique, remind patients to take doses, and transmit data to healthcare providers for personalized treatment adjustments. Enhanced patient engagement, reduced exacerbations, and better disease management outcomes increase demand for technologically advanced bronchodilator solutions, fueling overall market growth.

Market Restraints

- Patent Cliff and Generic Erosion: The patent cliff and generic erosion allow cheaper generic versions of branded drugs to enter the market, reducing revenue for original manufacturers. As patents expire, competition intensifies, leading to price reductions and margin pressure. This dynamic limits incentives for innovation, slows new product launches, and creates pricing pressures that collectively hamper overall market growth despite rising disease prevalence.

- Inhaler Device Complexity and Patient Technique Training Requirements: Inhaler device complexity and the need for proper patient technique are limiting the market by increasing the risk of incorrect usage, which can reduce drug efficacy and treatment outcomes. Patients often require training and repeated guidance to use devices correctly, creating barriers to adoption. These challenges lead to lower adherence, higher chances of exacerbations, and reluctance among healthcare providers to prescribe certain devices, collectively restraining market growth.

Market Opportunities

- MART Maintenance and Reliever Therapy Protocol: The MART (Maintenance and Reliever Therapy) protocol combines maintenance and quick-relief treatment into a single inhaler, simplifying asthma management. This approach improves patient adherence, reduces the frequency of exacerbations, and enhances overall treatment effectiveness. Growing adoption of MART therapy encourages the development of innovative inhaler formulations, driving prescription volumes and expanding market potential for bronchodilator therapies globally.

- Asia Pacific Untreated COPD and Asthma Population: The large untreated COPD and asthma population in the Asia Pacific region represents a significant growth opportunity for the bronchodilators market. Limited access to healthcare, low disease awareness, and underdiagnosis in many countries create a substantial patient pool for new treatments. Expanding healthcare infrastructure, increasing government initiatives, and rising patient awareness are expected to drive adoption of bronchodilator therapies, boosting market penetration and long-term growth in the region.

Market Challenges

- Environmental Sustainability Regulatory Pressure on pMDI HFC Propellants Creating Device Technology Transition Requirement: Environmental regulations targeting HFC propellants in pressurized metered-dose inhalers (pMDIs) are forcing manufacturers to transition to eco-friendly alternatives. This shift requires substantial investment in new device technologies, redesigning inhalers, and regulatory approvals. The added costs, longer development timelines, and potential supply disruptions create barriers for companies, slowing market growth while balancing environmental compliance with patient access.

- Biologic Monoclonal Antibody Competition for Severe Asthma Market Share Creating Treatment Tier Competition: The emergence of biologic monoclonal antibodies for severe asthma is introducing high-efficacy alternatives that target specific inflammatory pathways. These therapies compete for the same patient segment, particularly those with severe or uncontrolled asthma, reducing reliance on traditional bronchodilators. As a result, market share pressure increases, prompting manufacturers to innovate or reposition products, while overall growth in conventional bronchodilator usage faces constraints.

Emerging Market Trends

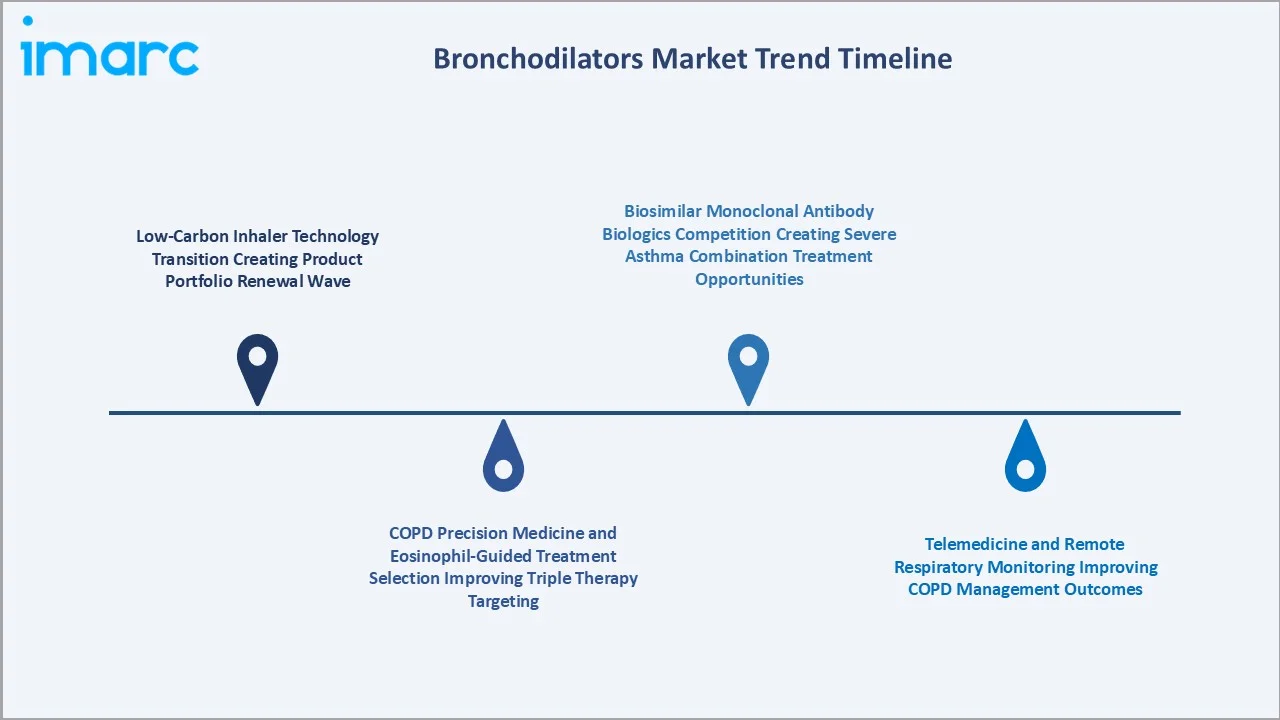

1. Low-Carbon Inhaler Technology Transition Creating Product Portfolio Renewal Wave

The shift toward low-carbon inhaler technology is prompting manufacturers to innovate environmentally friendly devices. This transition encourages the development of new propellant-free or reduced-emission inhalers, leading to product portfolio renewal. It aligns with global sustainability initiatives, enhances brand reputation, and attracts environmentally conscious patients, creating growth opportunities while modernizing the market landscape. In December 2025, Chiesi submitted its first carbon-minimal pressurized metered-dose inhaler (pMDI) portfolio for beclometasone (100 mcg and 200 mcg) to the UK Medicines and Healthcare products Regulatory Agency (MHRA).

2. COPD Precision Medicine and Eosinophil-Guided Treatment Selection Improving Triple Therapy Targeting

COPD precision medicine and eosinophil-guided treatment selection are enabling more personalized therapy. By identifying patients with higher eosinophil counts, clinicians can better target triple therapy combinations, optimizing efficacy and minimizing unnecessary medication. This precision approach improves clinical outcomes, enhances patient adherence, and drives adoption of advanced bronchodilator therapies, supporting market growth through tailored treatment strategies.

3. Telemedicine and Remote Respiratory Monitoring Improving COPD Management Outcomes

Telemedicine and remote respiratory monitoring enable continuous patient oversight and timely intervention for COPD management. Digital platforms allow healthcare providers to track lung function, inhaler usage, and symptom progression remotely, improving adherence and reducing hospitalizations. This technology enhances patient engagement, optimizes treatment outcomes, and increases demand for connected bronchodilator devices, fostering growth in the market. In October 2025, electronRx launched its pDx app, designed to enable clinicians to remotely evaluate cardiopulmonary function, monitor disease progression, and tailor treatment plans for conditions such as asthma, COPD, interstitial lung disease, and pulmonary hypertension.

4. Biosimilar Monoclonal Antibody Biologics Competition Creating Severe Asthma Combination Treatment Opportunities

The entry of biosimilar monoclonal antibody biologics enables cost-effective combination therapies for severe asthma. These biosimilars allow clinicians to pair targeted biologics with traditional bronchodilators, enhancing treatment efficacy while expanding patient access. This trend encourages innovation in therapy regimens, supports broader adoption of triple and combination treatments, and drives growth in the severe asthma segment.

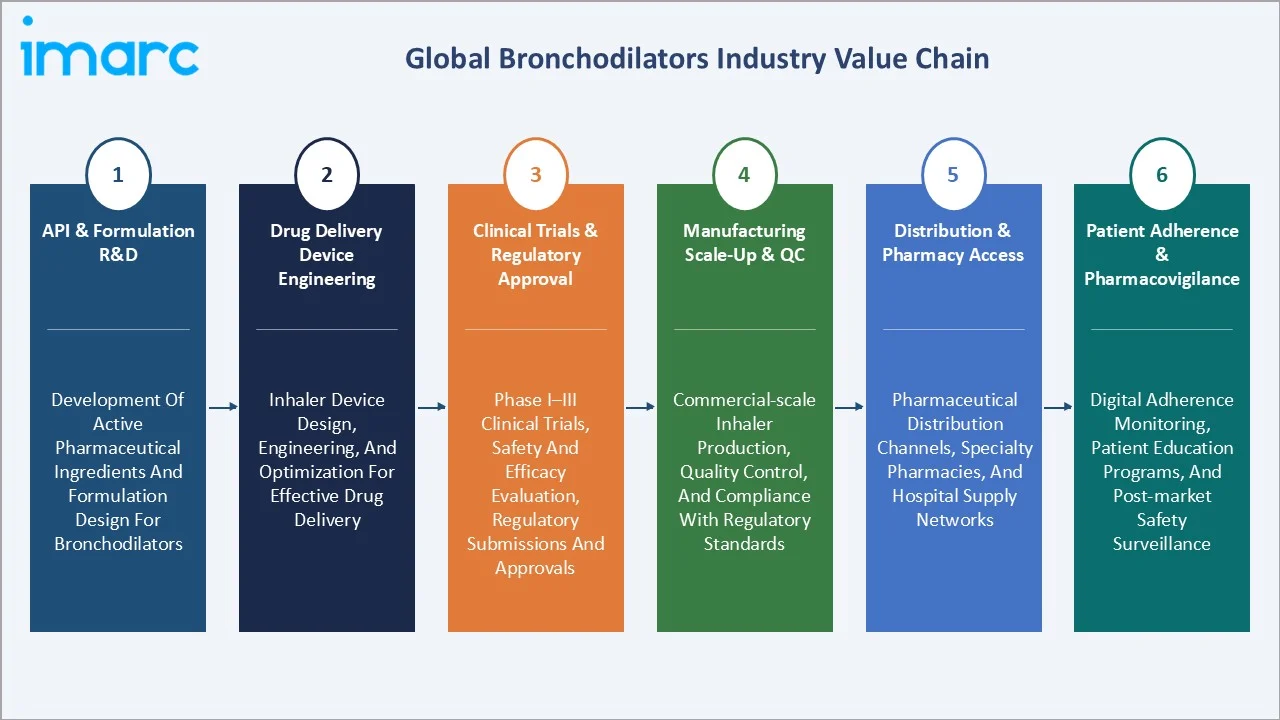

Industry Value Chain Analysis

The bronchodilators value chain integrates API and formulation R&D, drug delivery device engineering, clinical trials and regulatory approval, manufacturing scale-up and quality control, distribution and pharmacy access, and patient adherence and pharmacovigilance.

| Stage | Key Participants |

|---|---|

| API & Formulation R&D | Development of active pharmaceutical ingredients and formulation design for bronchodilators |

| Drug Delivery Device Engineering | Inhaler device design, engineering, and optimization for effective drug delivery |

| Clinical Trials & Regulatory Approval | Phase I–III clinical trials, safety and efficacy evaluation, regulatory submissions and approvals |

| Manufacturing Scale-Up & QC | Commercial-scale inhaler production, quality control, and compliance with regulatory standards |

| Distribution & Pharmacy Access | Pharmaceutical distribution channels, specialty pharmacies, and hospital supply networks |

| Patient Adherence & Pharmacovigilance | Digital adherence monitoring, patient education programs, and post-market safety surveillance |

The patient adherence and pharmacovigilance tier represents the value chain's highest strategic importance for long-term commercial success. Bronchodilator market revenue is directly proportional to patient medication adherence rates, and the chronic nature of asthma and COPD creates multi-decade patient-treatment relationships that compound the value of adherence improvement.

Technology Landscape in the Bronchodilators Industry

Pressurized Metered-Dose Inhaler Technology

Pressurized metered-dose inhaler (pMDI) technology is providing precise, consistent dosing directly to the lungs. Innovations in pMDI design, such as low-carbon propellants, improved actuator mechanisms, and dose counters, enhance drug delivery efficiency and patient adherence. In May 2025, AstraZeneca’s Trixeo Aerosphere (budesonide/glycopyrronium/formoterol fumarate or BGF), previously approved for adult COPD treatment, received UK approval featuring a next-generation pMDI propellant with near-zero global warming potential. This marks the first pMDI-delivered medication using a propellant that reduces GWP by 99.9% compared to conventional pMDI propellants. These advancements support the development of combination therapies, enable integration with smart inhaler systems, and drive overall technological evolution in the bronchodilator market.

Dry Powder Inhaler Technology

Dry powder inhaler (DPI) technology offers a propellant-free, breath-actuated delivery system that enhances patient convenience and adherence. Innovations in DPI design, such as improved powder formulation, flow control mechanisms, and multi-dose capsules, increase drug deposition efficiency and dosing accuracy. This technology supports combination therapies, reduces environmental impact compared to pMDIs, and drives the adoption of next-generation inhalers, strengthening the overall technological landscape in bronchodilator treatment.

Fixed-Dose Combination and Triple Therapy Formulation

Fixed-dose combination (FDC) and triple therapy formulations are integrating multiple active ingredients, such as LABA, LAMA, and ICS, into a single inhaler. This innovation simplifies treatment regimens, improves patient adherence, and enhances clinical outcomes. Advanced formulation techniques ensure optimal drug stability, delivery efficiency, and compatibility within a single device, driving the development of next-generation inhalers and strengthening technological advancement in the bronchodilator market.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Indication | Asthma | 52.6% | 2025 |

| Drug Type | 🔒 | 🔒 | 2025 |

| Route of Administration | Inhaler | 61.8% | 2025 |

| Region | North America | 37.9% | 2025 |

By Indication

Asthma leads at 52.6% market share (2025). The asthma segment dominates due to the high global prevalence of asthma and its chronic nature, which requires continuous management. Patients rely heavily on both short-acting and long-acting bronchodilators to control symptoms, prevent exacerbations, and maintain lung function. This persistent demand for effective asthma therapies drives significant prescription volumes, making asthma the leading therapeutic area in the bronchodilators market.

To access detailed market analysis, Request Sample

COPD, at 38.1%, as patients require ongoing treatment to manage persistent airflow limitation and reduce exacerbations. The chronic and progressive nature of COPD ensures sustained use of long-acting and combination bronchodilator therapies, fueling market growth globally. Others at 9.3% includes bronchiectasis, cystic fibrosis, exercise-induced bronchoconstriction, and other obstructive airway conditions.

By Route of Administration

Inhaler leads at 61.8% market share (2025). Inhaler encompasses pMDI (pressurized metered dose inhaler), DPI (dry powder inhaler), SMI (Soft Mist Inhaler), and nebuliser solutions. The inhaler route's clinical superiority for chronic asthma and COPD management is institutionalised in guidelines recommending inhaled bronchodilators as first-line therapy for all patients capable of using an inhaler device.

Oral at 25.6% includes theophylline, oral salbutamol tablets, oral bambuterol, and oral montelukast leukotriene antagonist. Injection at 12.6% includes IV aminophylline, subcutaneous terbutaline, IV/IM adrenaline, and IV magnesium sulfate for acute hospital bronchospasm management and severe asthma/COPD exacerbation treatment.

Regional Market Insights

| Region | Share (2025) | Key Bronchodilators Market Drivers & Characteristics |

|---|---|---|

| North America | 37.9% | Driven by high healthcare expenditure, established respiratory care infrastructure, and widespread adoption of inhaler therapies. |

| Europe | 28.6% | Driven by strong asthma and COPD prevalence, well-developed healthcare systems, and high awareness of respiratory treatments. |

| Asia-Pacific | 24.1% | Supported by rising asthma and COPD incidence, expanding healthcare access, and increasing urban pollution levels. |

| Latin America | 5.4% | Latin America’s market reflects growing respiratory disease prevalence in urban populations and improving access to inhalation therapies. |

| Middle East and Africa | 4.0% | The MEA represent a smaller market by revenue but faces high asthma triggers and environmental factors, creating potential for market expansion. |

North America, at 37.9%, leads through US premium branded bronchodilator pricing and the highest specialist respiratory prescription compliance globally. Europe, at 28.6%, reflects EMA centralised approval, European national health service formulary coverage, and growing environmental inhaler policy driving DPI adoption above the global average.

Asia Pacific, at 24.1%, is the fastest-growing region through China and India's asthma awareness improvement, and Japan and Australia's high-compliance premium markets. Latin America, at 5.4%, reflects Brazil's coverage of essential bronchodilators and a growing generic market. MEA, at 4.0%, encompasses GCC premium access and Africa WHO Essential Medicine access programmes.

Competitive Landscape

The global bronchodilators market is concentrated among three primary pharmaceutical companies, GSK plc, AstraZeneca, and Boehringer Ingelheim International GmbH, collectively accounting for approximately 50-60% of total market revenue through their dominant positions in branded products. This concentration reflects the historical regulatory exclusivity periods and complex device IP that protected products through their commercial peak years, enabling sustained revenue at premium pricing.

| Company Name | Key Products | Market Position | Core Strength |

|---|---|---|---|

| GSK plc | ADVAIR DISKUS, ADVAIR HFA, ANORO ELLIPTA, BREO ELLIPTA, INCRUSE ELLIPTA, TRELEGY ELLIPTA | Market Leader | GSK plc holds a leading position in the bronchodilators market, with experience in respiratory medicine, a strong portfolio of inhaled medicines, and continuous R&D innovation for asthma and COPD treatments. |

| AstraZeneca | SYMBICORT, BEVESPI AEROSPHERE, BREZTRI AEROSPHERE | Market Leader | AstraZeneca holds a leading, innovative role in the bronchodilator and respiratory market, with a focus on treating asthma and Chronic Obstructive Pulmonary Disease (COPD) through inhaled combinations and advanced inhaler technologies. |

| Boehringer Ingelheim International GmbH | Spiriva Respimat, Striverdi Respimat, Combivent Respimat | Market Leader | Boehringer Ingelheim International GmbH focuses on developing and marketing innovative treatments for Chronic Obstructive Pulmonary Disease (COPD) and asthma, with a strong focus on enhancing the quality of life through advanced delivery devices. |

| Teva Pharmaceutical Industries Ltd. | Albuterol Sulfate HFA Inhalation Aerosol | Strong Challenger | Teva Pharmaceutical Industries Ltd.'s market position is driven by a combination of established generic products and specialty respiratory medicines. |

| Novartis AG | Ultibro Breezhaler, Seebri Breezhaler, Enerzair Breezhaler | Strong Challenger | Novartis AG focuses on innovative, long-acting treatments for Chronic Obstructive Pulmonary Disease (COPD) and asthma. |

The competitive dynamics are progressively shaped by platform competition between inhaler device architectures. Platform ownership creates switching barrier economics. Once a COPD patient and their pulmonologist select a device platform, subsequent line additions prefer the familiar device, creating commercial inertia that benefits incumbent platform holders.

Key Company Profiles

GSK plc

GSK plc is a leading global biopharmaceutical company with a strong focus on respiratory medicines, particularly bronchodilator therapies for asthma and COPD. The company has a long heritage in developing and commercializing inhaled respiratory treatments and remains one of the dominant players in the bronchodilators market.

- Key Products: ADVAIR DISKUS, ADVAIR HFA, ANORO ELLIPTA, BREO ELLIPTA, INCRUSE ELLIPTA, TRELEGY ELLIPTA.

- Recent Developments: In October 2025, GSK plc announced positive results from its Phase III clinical program for a next-generation Ventolin (salbutamol) metered-dose inhaler (MDI). The study confirmed that the salbutamol MDI using the innovative low-carbon propellant HFA-152a is therapeutically equivalent and demonstrates a safety profile comparable to the current MDI formulation containing HFA-134a.

- Strategic Focus: Developing innovative inhaler technologies, including low-carbon propellants and single-inhaler combination therapies, to enhance treatment efficacy, patient adherence, and environmental sustainability.

AstraZeneca

AstraZeneca is a leading global biopharmaceutical company with a strong foothold in the bronchodilators market, driven by a focus on advanced inhaled therapies for COPD and asthma management. Through robust R&D investment, global regulatory approvals, and strategic market launches, AstraZeneca continues to expand its presence and competitiveness in the global bronchodilators market.

- Key Products: SYMBICORT, BEVESPI AEROSPHERE, BREZTRI AEROSPHERE.

- Recent Developments: In April 2026, AstraZeneca’s Breztri Aerosphere (budesonide/glycopyrrolate/formoterol fumarate or BGF 320/36/9.6 μg), a fixed-dose triple-combination therapy, was approved in the US for maintenance treatment of asthma in adults and children aged 12 and older.

- Strategic Focus: Expanding global access to advanced COPD and asthma therapies through next-generation inhaler innovations and precision combination treatments.

Market Concentration Analysis

The bronchodilators market is moderately concentrated at the branded originator level; GSK plc, AstraZeneca, and Boehringer Ingelheim International GmbH together hold approximately 50-60% of total market revenue through their dominant positions in the market. The market's concentration is lower than analogous branded pharmaceutical categories because of the significant generic and affordable brand presence.

Market concentration patterns differ significantly by geography: US branded market concentration is highest with GSK and AstraZeneca holding approximately 55-60% of US branded inhaler revenue, European generic prescribing policies create a more fragmented market share, with Boehringer Ingelheim's Spiriva more dominant in COPD, and India's market is effectively Cipla-dominated. Market concentration is declining through the forecast period as generic competition increases across all major markets.

Investment & Growth Opportunities

Highest Growth Segments

Inhaler route (~4.3% CAGR), asthma indication (~4.1% CAGR), triple therapy ICS/LABA/LAMA (~15-20% CAGR from growing base), smart inhaler/digital health (~20-25% CAGR from small base), biologic add-on for severe asthma (~12-15% CAGR complementing bronchodilator market), and Asia Pacific bronchodilators (~5% regional CAGR from COPD treatment gap closure) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Low-carbon inhaler reformulation represents both a regulatory requirement and a commercial opportunity. Companies that complete low-carbon reformulations early benefit from preferential formulary listing and physician environmental prescribing preference that translates to above-average share retention versus non-low-carbon branded and generic alternatives.

Investment Themes

- Triple therapy market penetration programme for eligible COPD patients: The COPD triple therapy market has a long commercial runway because only 20-30% of COPD Group E patients with eosinophil counts above 100 cells/mcL have been converted from dual therapy to triple therapy as of 2025. Each 5% improvement in triple therapy conversion rate among eligible dual-therapy COPD patients generates approximately USD 500 Million-1 Billion in incremental annual triple therapy revenue.

- Smart inhaler ecosystem development for COPD remote monitoring and clinical trial digital endpoint market: The regulatory acceptance of connected inhaler data as a digital clinical trial endpoint and the health economics evidence for remote COPD monitoring reducing hospitalisation create a commercial framework for smart inhaler ecosystem investment above drug product alone.

Future Market Outlook (2026-2034)

The global bronchodilators market is projected to grow from USD 40.89 Billion in 2025 to USD 58.73 Billion by 2034, delivering a 3.98% CAGR over the forecast period. The market's anchor value of USD 49.70 Billion in 2030 represents a bronchodilators industry at its most complex structural transition - triple therapy is becoming the standard of care for symptomatic COPD, low-carbon inhaler reformulation is creating product portfolio renewal across the pMDI category, and biologic add-on therapies are establishing a premium treatment tier above traditional bronchodilators for severe eosinophilic asthma that lifts average per-patient pharmaceutical expenditure while complementing bronchodilator controller revenue.

Three structural forces define the bronchodilators market growth through 2034 with confidence. The epidemiological inevitability of asthma and COPD prevalence growing with aging populations, urbanisation, and air pollution creates structural demand growth independent of clinical innovation or pricing dynamics. The clinical innovation pipeline. The generic access expansion for affordable inhaler availability in Asia Pacific, LATAM, and MEA markets through domestic generic manufacturers progressively closes the diagnosis-treatment gap in the world's highest-burden markets, expanding total patient treatment volume that sustains aggregate market revenue even as per-unit branded pricing erodes.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Global Respiratory Medical Directors; Regulatory Affairs Directors; Hospital Respiratory Pharmacists; Payer and HTA Medical Directors; Digital health adherence platform executives; and emerging market respiratory medicine representatives.

Secondary Research

Secondary research encompassed European Public Assessment Reports for all marketed bronchodilator approvals; Global Strategy for Asthma Management and Prevention; Global Strategy for Prevention, Diagnosis and Management of COPD; WHO Global Asthma Report; World Air Quality Report 2024; individual company annual reports and investor presentations; IQVIA market data for bronchodilator prescription volume and value; and FDA Adverse Event Reporting System for inhaled bronchodilator safety signal monitoring. Over 70 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up product-level modelling: (i) branded originator products; (ii) generic segment; (iii) emerging market volume growth modelling from China and India COPD treatment rate improvement trajectories calibrated against COPD Action Plan implementation data. Market CAGR validated against consensus forecasts from IQVIA Global Market Forecasts, respiratory disease model, and respiratory pipeline revenue projections.

Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Indication, Drug Type, Route of Administration, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | GSK plc, AstraZeneca, Boehringer Ingelheim International GmbH, Teva Pharmaceutical Industries Ltd., Novartis AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Bronchodilators Market Report

The global bronchodilators market reached USD 40.89 Billion in 2025, driven by fixed-dose combination inhalers for asthma and COPD, LAMA bronchodilators for COPD, growing single-inhaler triple therapy, and expanding generic bronchodilator access in the Asia Pacific and emerging markets.

The market grows at 3.98% CAGR during 2026-2034, reaching USD 58.73 Billion by 2034. Growth reflects triple therapy expansion, Asia Pacific COPD treatment gap closure, creating volume growth, smart inhaler digital health premium segment creation, low-carbon pMDI reformulation providing product renewal commercial opportunities, and biologic add-on severe asthma market lifting per-patient asthma treatment revenue.

Asthma leads at 52.6% through fixed-dose combination commercial dominance. Asthma also grows fastest at ~4.1% CAGR through the MART protocol, biologic combination therapy for severe asthma, and guideline step therapy implementation in the Asia Pacific and Latin American markets.

Inhaler leads at 61.8% as the guideline-recommended standard of care for respiratory drug delivery, providing superior lung deposition, faster onset, and lower systemic exposure versus oral or injection alternatives. Inhaler also grows fastest at ~4.3% CAGR through DPI adoption driven by environmental inhaler policy and smart inhaler digital health premium products.

North America leads at 37.9% through US premium branded bronchodilator pricing, high COPD disease burden, and specialist respiratory prescribing compliance with guidelines.

Leading companies include GSK plc, AstraZeneca, Boehringer Ingelheim International GmbH, Teva Pharmaceutical Industries Ltd., and Novartis AG, among others.

The market is projected to reach approximately USD 49.70 Billion by 2030, with triple therapies growth and low-carbon inhaler reformulations beginning commercial launches in the emerging markets.

Smart inhaler platforms combine electronic sensors within or attached to inhaler devices to record data, time, GPS location, and inhalation technique data automatically for patient and physician review.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)