Bubble Tea Market Size, Share, Trends and Forecast by Base Ingredients, Flavor, Component, and Region, 2026-2034

Global Bubble Tea Market Size, Share, Trends & Forecast (2026-2034)

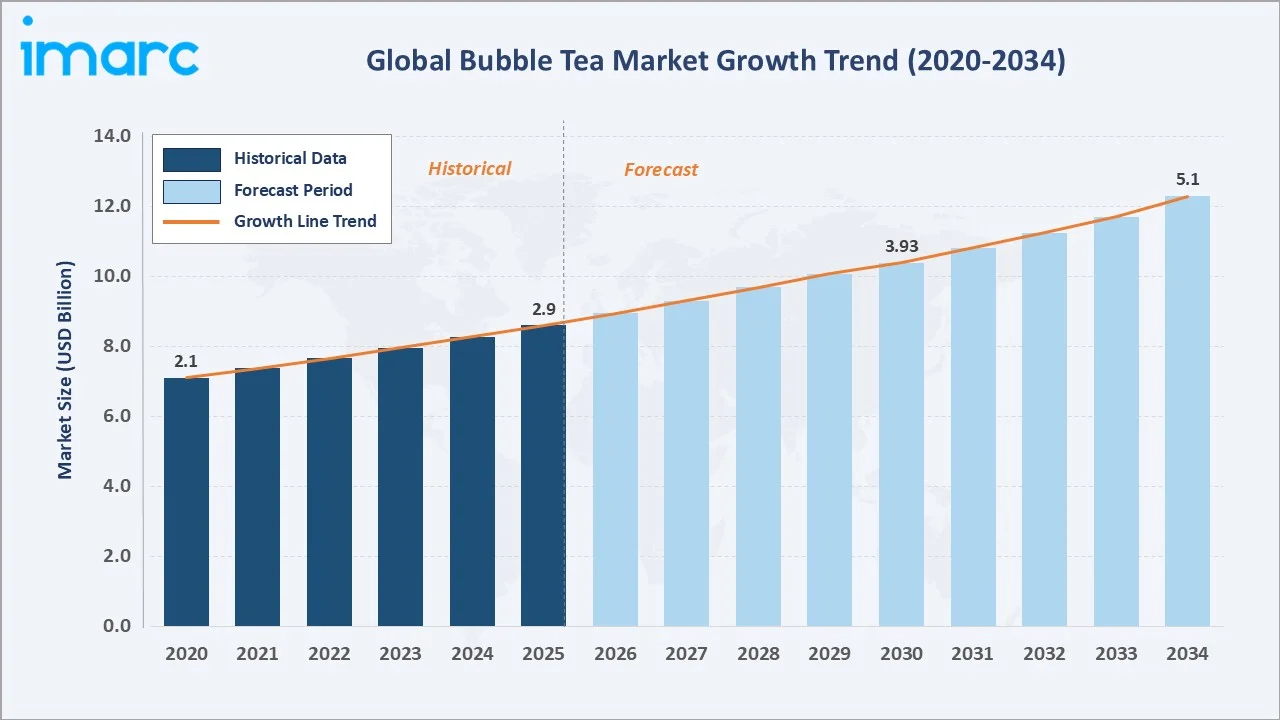

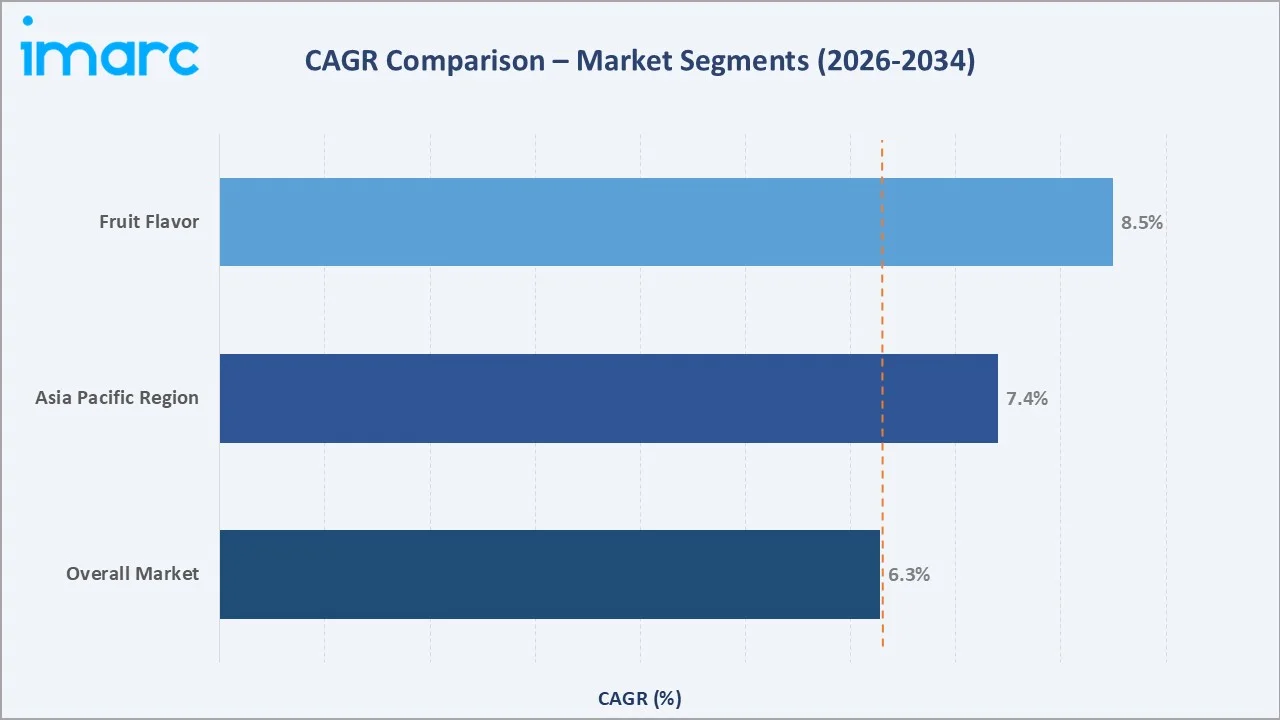

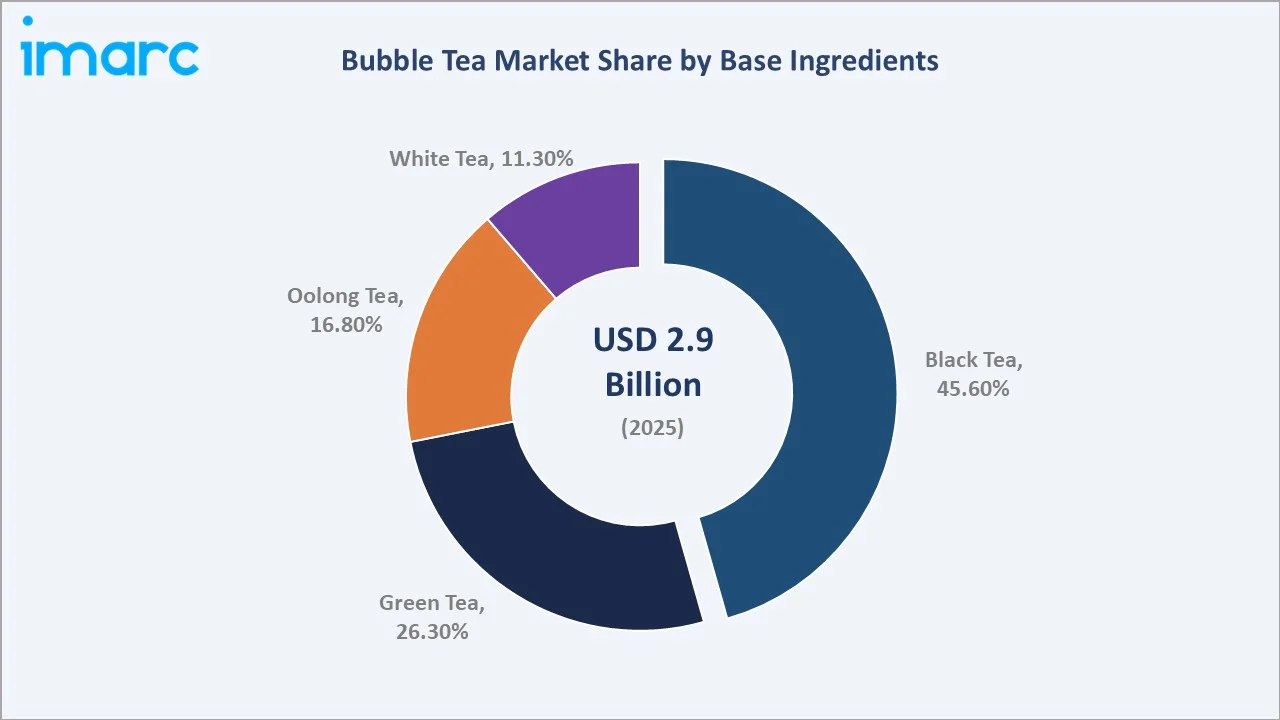

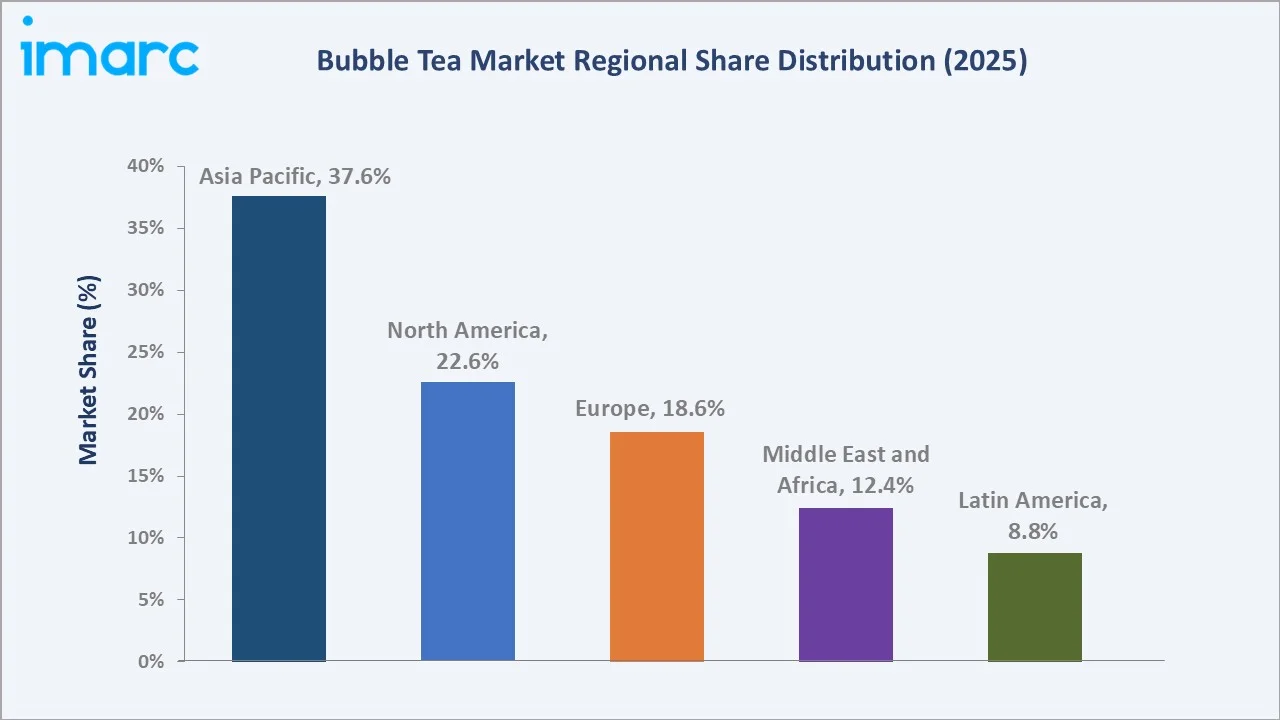

The global bubble tea market reached a value of USD 2.9 Billion in 2025 and is projected to reach USD 5.1 Billion by 2034, exhibiting a CAGR of 6.28% during the forecast period (2026-2034). Market growth is powered by rising global popularity among Gen-Z and millennial consumers, rapid franchise expansion across Asia Pacific, North America, and Europe, and the strong influence of social media in driving product discovery and demand for innovative flavors. Asia Pacific dominates with a 37.6% revenue share in 2025, reflecting the beverage's Taiwanese origins and deep cultural embedding across China, Thailand, South Korea, and Southeast Asia. Fruit flavor leads the flavor segment at 38.3% (2025), while black tea holds the largest base ingredient share at 45.6%. The market is forecast to reach USD 3.9 Billion by 2030.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.9 Billion |

|

Forecast Market Size (2034) |

USD 5.1 Billion |

|

CAGR (2026-2034) |

6.28% |

|

Largest Region |

Asia Pacific (37.6%, 2025) |

|

Fastest Growing Region |

Middle East & Africa (~9.2% CAGR) |

|

Leading Base Ingredient |

Black Tea (45.6%, 2025) |

|

Leading Flavor |

Fruit Flavor (38.3%, 2025) |

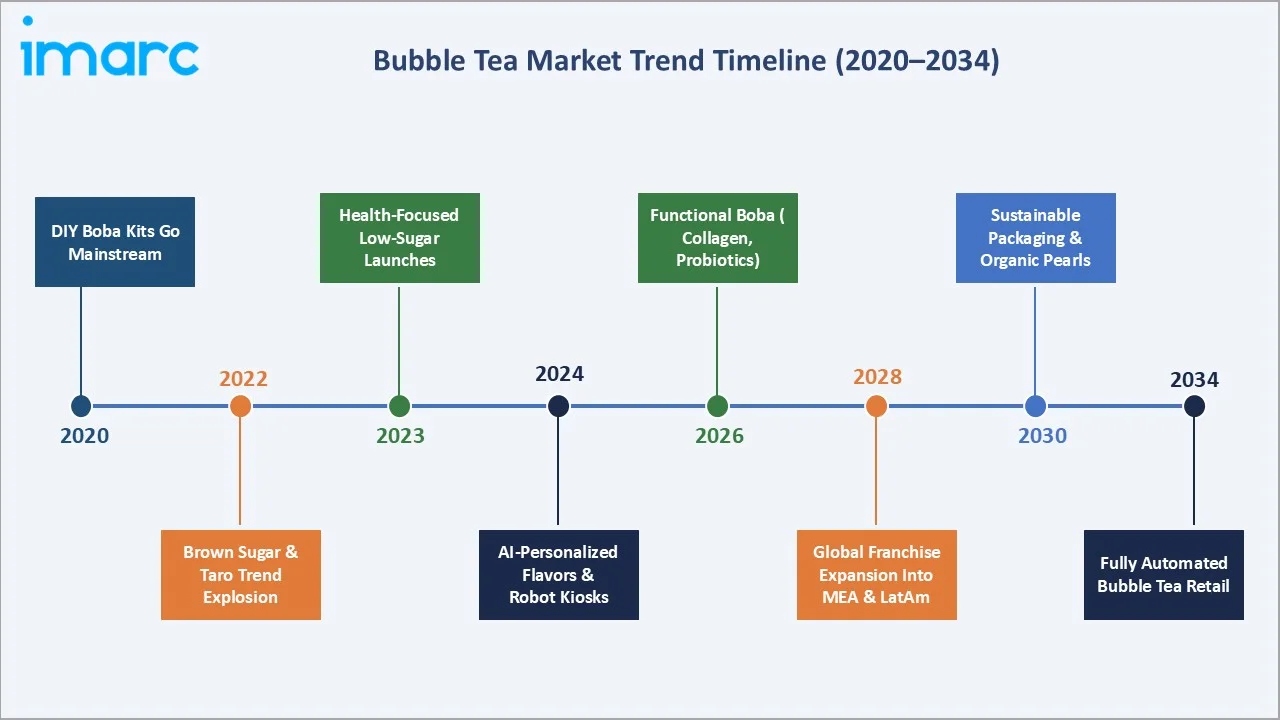

The market's growth from USD 2.1 Billion in 2020 to USD 2.9 Billion in 2025 reflects robust resilience through the pandemic period, driven by e-commerce channel adaptation and the explosion of DIY bubble tea kit sales. The forecast addition of USD 2.2 Billion through 2034 represents a near-doubling of market value, anchored by franchise network expansion into underpenetrated markets and ongoing product premiumization.

To get more information on this market, Request Sample

The 6.28% CAGR through 2034 positions bubble tea as one of the beverage sector's fastest-growing categories globally. The social-media-driven virality of visually distinctive drinks, combined with the beverage's deep customization capability, creates durable consumer loyalty and repeat purchase behavior that sustains above-average category growth.

Executive Summary

The global bubble tea market stood at USD 2.9 Billion in 2025, propelled by accelerating franchise network expansion, social media-driven consumer demand among younger demographics, and the mainstreaming of Asian tea culture across Western markets. The market is projected to reach USD 5.1 Billion by 2034 at a CAGR of 6.28%, passing USD 3.9 Billion by 2030. Asia Pacific commands a 37.6% revenue share (2025), anchored by China's booming domestic tea culture, with Sichuan province alone reporting comprehensive tea output value exceeding 120 billion yuan in 2023, alongside strong markets in Thailand, South Korea, and Taiwan.

By base ingredient, black tea leads at 45.6% (2025), valued for its rich flavor, robust taste profile, and high versatility for flavor combination. Green tea (26.3%) is the second-largest segment, benefiting from health-positioning and growing adoption among wellness-conscious consumers. By flavor, fruit flavor dominates at 38.3% (2025), driven by the visual appeal and social media shareability of vibrant fruit-infused beverages.

North America (22.6%), Europe (18.6%), the Middle East and Africa (12.4%), and Latin America (8.8%) complete the regional landscape. Key growth trends include the rapid rise of healthier low-sugar and organic formulations, the expansion of ready-to-drink bottled boba in retail, and the growth of DIY bubble tea kits through e-commerce platforms. BUBLUV, Inc. launched the first ready-to-drink boba alternative with less than 1g of sugar and 50 calories per bottle, exemplifying the market's health-oriented product innovation trajectory.

Key Market Insights

|

Insight |

Data |

|

Largest Base Ingredient |

Black Tea – 45.6% (2025) |

|

Largest Flavor Segment |

Fruit Flavor – 38.3% (2025) |

|

Leading Region |

Asia Pacific – 37.6% (2025) |

|

Fastest Growing Region |

Middle East & Africa (~9.2% CAGR) |

|

Top Companies |

Gong Cha, Tiger Sugar, CoCo Fresh, TP Tea, Chatime, Kung Fu Tea |

|

Key Opportunity |

RTD bottled boba & retail expansion – USD 1.5B+ addressable by 2034 |

Key Analytical Observations Supporting the Data Points Above:

- Black tea’s 45.6% share (2025) reflects its status as the classic bubble tea base – its bold flavor, worldwide availability, and compatibility with diverse toppings and syrups make it the default consumer and operator choice across all markets.

- Fruit flavor’s 38.3% lead (2025) is driven by the visual appeal and Instagram-shareability of colorful, layered fruit tea drinks that dominate social media platforms. Taro, mango, strawberry, and lychee are among the highest-velocity flavors globally.

- Asia Pacific’s 37.6% share reflects the beverage's deep cultural roots in Taiwan, its rapid QSR-style franchise proliferation across China, and growing adoption in India, Indonesia, Vietnam, and Thailand where tea consumption is embedded in daily lifestyle.

Global Bubble Tea Market Overview

Bubble tea, also known as boba, pearl milk tea, or tapioca tea is a Taiwanese-origin cold tea beverage typically consisting of a tea base, milk or non-dairy creamer, flavored syrup, and chewy tapioca pearls or other toppings including popping boba, jelly, and pudding. Originating in Taichung, Taiwan in the 1980s, the beverage has evolved into a globally recognized multi-billion dollar industry spanning franchise chains, independent cafes, ready-to-drink retail products, and at-home preparation kits. Tea imports into the United States reached USD 578.58 Million in 2024, nearly quadrupling from values three decades earlier, reflecting the deep mainstreaming of tea-based beverages in non-traditional markets.

Market Dynamics

To evaluate market opportunities, Request Sample

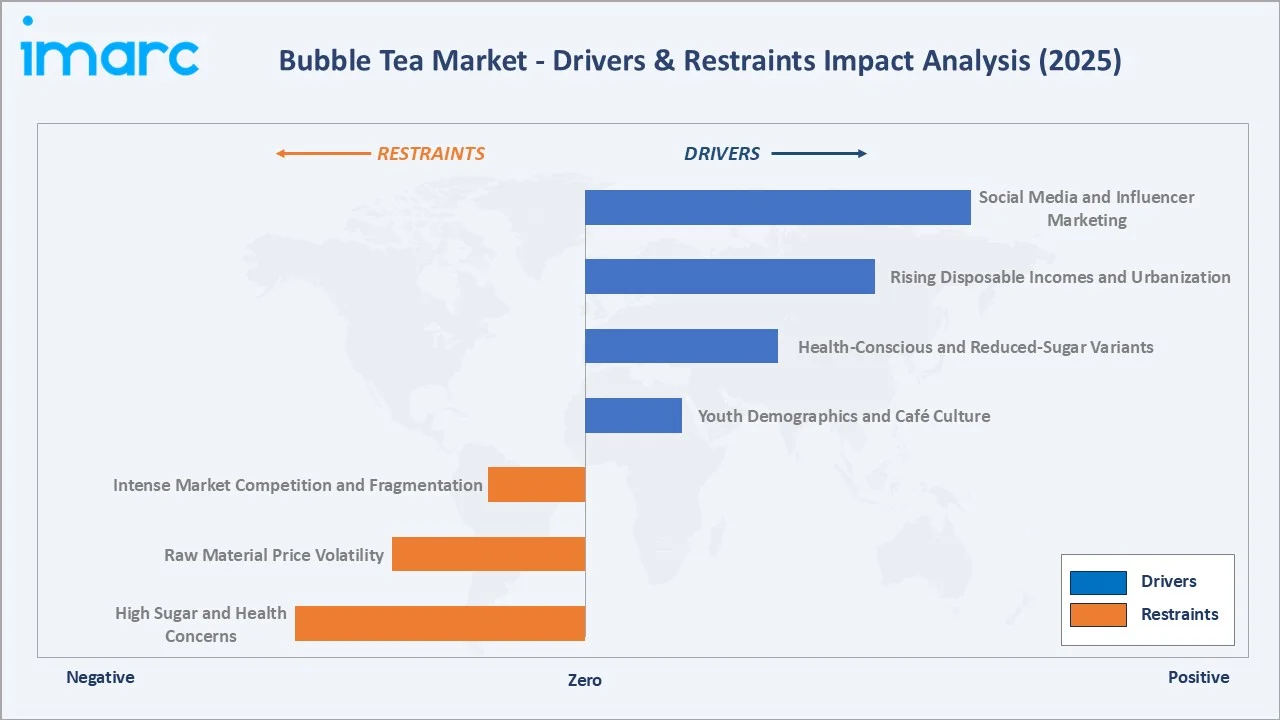

Market Drivers

- Social Media and Influencer Marketing: Visual platforms including Instagram, TikTok, and YouTube are primary demand catalysts, driving product discovery and purchase intent particularly among Gen-Z consumers. CoCo Fresh Tea & Juice's October 2023 collaboration with Blizzard Entertainment for Diablo IV-themed drinks exemplifies how pop-culture partnerships translate social media engagement directly into outlet traffic and sales lift.

- Rising Disposable Incomes and Urbanization: Growing middle-class populations in Asia, the Middle East, and Latin America are increasing expenditure on premium beverages and café-culture experiences. Over 159 million Americans drink tea daily, and U.S. retail and food services sales reached USD 724.6 Billion in November 2024, a 3.8% year-on-year increase, reflecting the broad base for premium beverage growth.

- Health-Conscious and Reduced-Sugar Variants: Growing consumer demand for low-sugar, organic, and plant-based formulations is expanding the addressable market. BUBLUV Inc.'s RTD boba alternative, featuring under 1g sugar and 50 calories per 9.5oz bottle, brewed with loose-leaf tea and natural sweeteners demonstrates how health-led product innovation is converting health-conscious consumers who previously avoided traditional bubble tea.

- Youth Demographics and Café Culture: Gen-Z and millennial consumers globally are driving the café culture phenomenon, with bubble tea shops becoming social gathering destinations. New Zealand's Avalanche DIY bubble tea kits, featuring taro, brown sugar, and strawberry flavors went viral on TikTok, reflecting how the beverage has become a participatory, shareable cultural experience. These drivers reinforce a self-sustaining growth cycle social media virality drives outlet trial, franchise expansion increases accessibility, product innovation retains health-conscious segments, and café culture embeds bubble tea as a lifestyle beverage rather than an occasional treat.

Market Restraints

- High Sugar and Health Concerns: Traditional bubble tea formulations contain high caloric content, with standard drinks exceeding 400 calories and 30–60g of added sugar. Growing consumer awareness of health risks associated with high sugar intake is prompting purchase frequency reduction among health-conscious demographics.

- Raw Material Price Volatility: Tapioca pearls are derived from cassava starch, and tea leaves are subject to agricultural weather variability. Price disruptions in these key inputs, driven by El Nino weather patterns and supply chain disruptions can compress operator margins, particularly for small and independent outlets.

- Intense Market Competition and Fragmentation: The bubble tea market combines large international franchise chains with thousands of independent local operators, creating intense price competition at the outlet level and high churn among smaller brands. Consumer loyalty in many markets is driven by location convenience rather than brand attachment.

Market Opportunities

- Ready-to-Drink Bottled Boba Retail Expansion: The retail-shelf RTD bubble tea segment is nascent but rapidly growing, offering brands the opportunity to distribute beyond physical outlet locations into supermarkets, convenience stores, and online retail. In the Mid-Atlantic, BUBLUV® Bubble Tea now has 133 Giant Food locations. The unique beverage is now easily accessible to citizens of Delaware, Maryland, and Virginia thanks to this expansion in 2026.

- Emerging Market Penetration: The Middle East, India, Southeast Asia, and Eastern Europe represent underserved but high-growth opportunity markets. India's bubble tea market is expected to grow at approximately 4-5% annually in the coming years, driven by rapid café culture adoption among urban youth. GCC markets including UAE and Saudi Arabia are experiencing rapid outlet expansion backed by mall-driven food and beverage consumption.

- Plant-Based and Functional Ingredient Innovation: Plant-based milk alternatives including oat milk, almond milk, and soy milk are gaining traction as bubble tea bases. Functional additions including collagen, probiotics, and adaptogens are creating new premium positioning opportunities targeting wellness-oriented consumers willing to pay significant price premiums.

Market Challenges

- Standardization vs. Customization Balance: The bubble tea category's strength, unlimited customization, also creates quality consistency challenges as franchise networks scale. Maintaining product quality and brand experience across thousands of franchise outlets in diverse geographies requires significant training, supply chain, and quality management investment.

- Perishability and Cold Chain Requirements: Fresh bubble tea has a short shelf life, requiring same-day preparation. The expansion of delivery and take-out channels creates texture and quality degradation challenges for tapioca pearls over extended delivery times, limiting the viability of long-distance delivery economics.

- Regulatory and Labeling Compliance: Evolving sugar content labeling regulations across the EU, Singapore, and UK markets are requiring operators to reformulate or disclose high-sugar content, creating compliance costs and potential demand impact in health-regulation-progressive markets.

Emerging Market Trends

The global bubble tea market is being reshaped by five converging trends that are redefining product innovation, distribution models, and competitive dynamics across all geographies through 2034.

1. Social Media Virality and Influencer-Driven Demand

TikTok, Instagram, and YouTube are the primary awareness and demand-generation channels for bubble tea globally. Visually striking beverages, layered fruit teas, cheese foam drinks, brown sugar tiger-stripe lattes generate organic user-generated content that functions as earned media at massive scale. New Zealand's Avalanche DIY bubble tea kits went viral through a single TikTok post, driving national retail distribution. Brand collaborations with gaming, anime, and K-pop properties are accelerating cultural embeddedness among Gen-Z audiences globally.

2. Health-Oriented Reformulation and Low-Sugar Innovation

The shift toward reduced-sugar, organic, and functional beverage formulations is reshaping bubble tea product development. BUBLUV's RTD boba featuring under 1g of sugar and 50 calories demonstrates the commercial viability of the health-positioned category. Bubble tea shops across Singapore, UK, and Australia are offering customizable sugar levels, vegan milk alternatives, and fresh-fruit options. This trend is expanding the addressable demographic from primarily indulgence-driven consumers to include health-conscious daily users.

3. Plant-Based and Functional Ingredient Trends

Oat milk, almond milk, coconut milk, and soy-based bubble tea variants are gaining mainstream acceptance globally, driven by the broader plant-based beverage trend. Functional ingredient additions including collagen peptides, prebiotic fiber, adaptogens (ashwagandha, lion's mane), and vitamin fortification are positioning premium bubble tea as a functional wellness beverage, unlocking new price tiers and consumer segments.

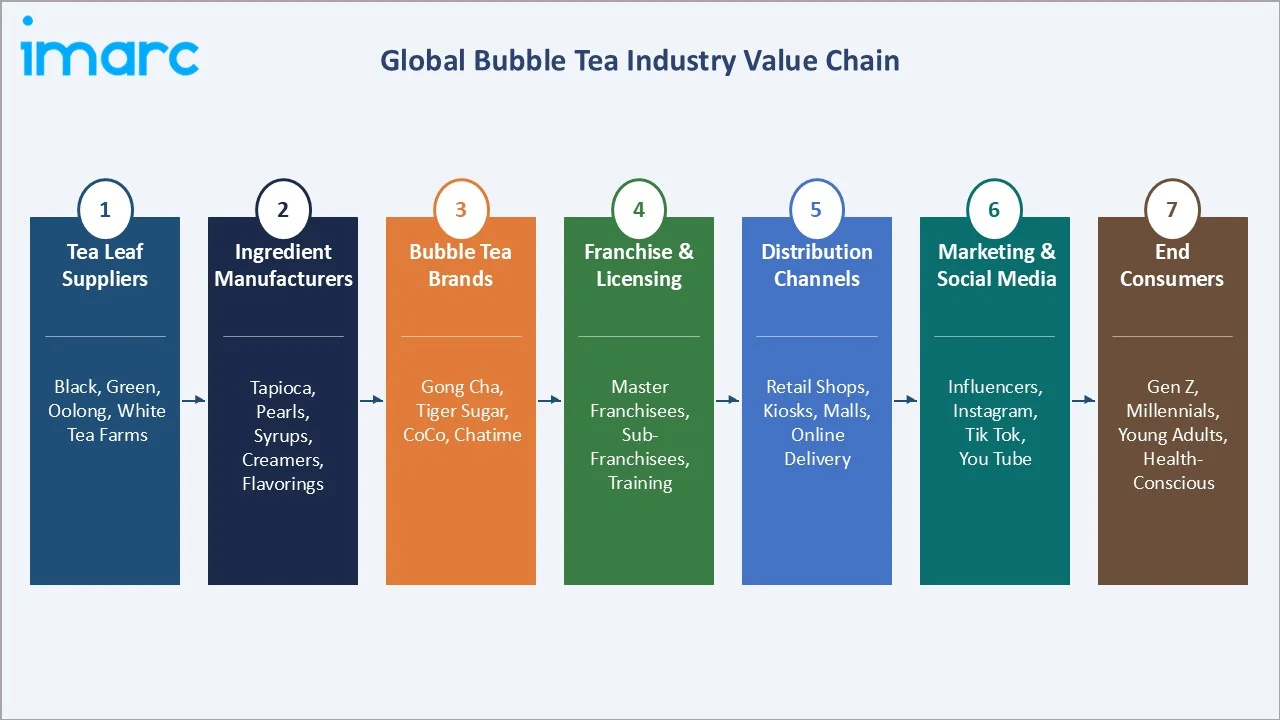

Industry Value Chain Analysis

The bubble tea industry value chain encompasses seven interconnected stages from raw material sourcing through to end consumer delivery. Each stage requires specialized expertise and quality management to ensure the sensory and visual experience that defines premium bubble tea consumption.

|

Stage |

Key Activities |

Representative Players |

|

Raw Material Sourcing |

Tea leaf procurement, tapioca starch sourcing, fruit puree, milk supply |

Taiwan tea gardens, Asian cassava farms, fruit processors |

|

Processing & Ingredients |

Tea blending, tapioca pearl manufacturing, syrup production, powder mixing |

Kung Fu Tea ingredients, St. Dreux Boba, POSSMEI |

|

Franchise & Brand Operations |

Franchise licensing, brand standards, marketing, menu innovation |

Gong Cha, CoCo Fresh, Tiger Sugar, Chatime, TP Tea |

|

Outlet Operations |

In-store preparation, quality control, customer experience, barista training |

Franchise outlets, independent cafes, cloud kitchen ops |

|

RTD & Packaging |

Bottling, packaging design, shelf-life optimization, retail distribution |

BUBLUV, Boba Bam, Steap Tea Bar (RTD brands) |

|

Distribution & Delivery |

3PL logistics, food delivery aggregators, e-commerce channel |

Grab, Uber Eats, Amazon, Instacart, direct delivery |

|

End Consumers |

In-store, delivery, retail, DIY kit consumption |

Gen-Z, millennials, café culture consumers globally |

The franchise and brand operations stage is the primary value creation point, it is where product formulation, consumer experience design, and brand equity are built. Leading franchise operators including Gong Cha and Tiger Sugar invest heavily in proprietary recipe development, outlet design aesthetics, and staff training to create premium, Instagrammable product experiences that command price premiums of 20–40% over commodity bubble tea competitors.

Technology Landscape in the Bubble Tea Industry

Automated Preparation Equipment

Precision bubble tea preparation machines controlling shake time, ice content, sugar level, and ingredient dispensing are standardizing product quality across large franchise networks. Automated tapioca pearl cooking and dispensing systems are reducing labor requirements and improving consistency. These technologies enable faster throughput during peak periods and reduce training requirements for new staff, supporting rapid franchise expansion.

Digital Ordering and Loyalty Technology

Mobile ordering apps, digital loyalty programs, and CRM platforms are central to customer retention strategies for major bubble tea chains. Gong Cha, CoCo Fresh, and Chatime all operate sophisticated mobile apps enabling pre-ordering, loyalty point accumulation, and personalized flavor recommendations. AI-powered recommendation engines are analyzing purchase history to suggest new flavor combinations and drive average transaction value uplift.

Food Delivery Platform Integration

Third-party delivery platform integration, including Grab, Uber Eats, DoorDash, and Meituan in key markets has significantly expanded bubble tea outlet effective trade areas. Delivery now represents 25–40% of revenues for urban bubble tea outlets in major markets. Real-time order management systems integrated with delivery platforms are optimizing preparation workflows and minimizing delivery wait times.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Base Ingredients |

Black Tea |

45.6% |

2025 |

|

Flavor |

Fruit Flavor |

38.3% |

2025 |

|

Component |

Liquid |

🔒 |

2025 |

|

Region |

Asia Pacific |

37.6% |

2025 |

By Base Ingredients

The bubble tea market is segmented by four primary tea base types, each with distinct flavor profiles, consumer positioning, and growth characteristics:

To access detailed market analysis, Request Sample

Black tea’s 45.6% dominance reflects its role as the foundational bubble tea base since the category's inception. However, green tea’s 26.3% share is being amplified by the matcha phenomenon, premium matcha latte bubble tea drinks have become one of the most viral and highest-margin menu items across all major franchise chains globally.

By Flavor

Fruit flavor leads the flavor segmentation at 38.3% (2025), surpassing original flavor (26.2%), reflecting the growing consumer preference for vibrant, visually striking, and refreshing fruit-infused tea beverages. Coffee flavor at 17.2% reflects the crossover appeal between bubble tea and coffee culture, particularly popular in North America and Europe.

The fruit flavor category’s leadership (38.3%, 2025) is particularly pronounced in Asia Pacific, where seasonal and regional fruit varieties, including durian, longan, and pandan – create high-engagement limited edition products.

Regional Market Insights

The global bubble tea market exhibits distinct regional dynamics in terms of consumer preference, price sensitivity, outlet density, and growth trajectory. Asia Pacific leads in both revenue share and market maturity, while the Middle East, Africa, and Latin America represent the highest-growth frontier opportunities.

Asia Pacific’s 37.6% market share (2025) is underpinned by Taiwan's role as the category's birthplace and ongoing innovation hub, North America’s 22.6% reflects the extraordinary growth of the Asian-American community's cultural influence on mainstream U.S. food and beverage trends, combined with the aggressive expansion of Taiwanese and Hong Kong bubble tea franchise brands in major metropolitan areas.

Competitive Landscape

The global bubble tea competitive landscape combines large international franchise chains with thousands of independent local operators. The top five franchise networks including Gong Cha, Tiger Sugar, CoCo Fresh Tea & Juice, Chatime, and TP Tea, collectively operate thousands of outlets globally as of 2025, representing approximately 25–30% of total bubble tea outlet count but a significantly higher share of branded, premium-tier revenues. For instance, the most popular bubble tea brand in the world, Gong Cha, has over 240 stores in 23 states, Washington, D.C., and Puerto Rico in addition to approximately 2,200 sites in 30 foreign markets.

|

Company |

Key Brand(s) |

Market Position |

Primary Strategy |

|

Gong Cha |

Gong Cha |

Global Leader – Premium Franchise |

International franchise expansion, digital loyalty app, premium tea sourcing |

|

Tiger Sugar |

Tiger Sugar |

Leader – Viral/Premium |

Brown sugar tiger stripe aesthetic, social media virality, limited editions |

|

CoCo Fresh Tea & Juice |

CoCo |

Leader – Asia Pacific |

Brand collaborations (Blizzard 2023), Asia dominance, rapid new market entry |

|

TP Tea |

TP Tea |

Leader – Taiwan Origin |

Heritage positioning, tea quality focus, Asia Pacific and North America |

|

Chatime |

Chatime |

Leader – Global Scale |

Significant global outlet count, broad menu, middle-market positioning |

|

Kung Fu Tea |

Kung Fu Tea |

Leader – USA |

U.S. market leader, franchise growth, customization focus |

|

Lollicup |

Lollicup |

Established – USA |

B2B supply, franchise, affordable positioning in North America |

|

Boba Guys |

Boba Guys |

Challenger – Premium USA |

Artisanal quality, clean ingredients, premium San Francisco origin |

|

Quickly |

Quickly |

Established – Asia/USA |

Legacy brand, broad menu, value positioning across Taiwan and USA |

|

Sharetea |

Sharetea |

Established – Global |

Taiwan heritage, global franchise, diverse menu depth |

The companies covered in the report includes Gong Cha, Tiger Sugar, CoCo Fresh Tea & Juice, TP Tea, Chatime, Kung Fu Tea, Lollicup, Boba Guys, Quickly, and Sharetea.

Gong Cha

Gong Cha is one of the world's largest premium bubble tea franchise chains, with over 2,200 outlets across 30+ countries as of 2025. Founded in Kaohsiung, Taiwan in 2006, the brand has built a premium positioning around Taiwanese tea heritage and consistent quality.

- Product Portfolio: Classic milk teas, fruit teas, yakult-based drinks, brown sugar series, seasonal specials, and cheese foam teas across all regional menus.

- Recent Developments: Launched the Gong Cha 2.0 program, which combines a modernised store design with two essential technologies, Super Wu beverage automation and self-order kiosks to boost throughput, streamline operations, and save labour costs without sacrificing quality or hospitality.

- Strategic Focus: Premium franchise model growth, tea quality sourcing and transparency, digital customer engagement, and emerging market entry.

CoCo Fresh Tea & Juice

CoCo Fresh Tea & Juice is one of Asia's largest bubble tea chains with over 5,000 outlets across continents. Its 2023 collaboration with Blizzard Entertainment for Diablo IV-themed drinks demonstrated the brand's capability to execute high-profile IP partnerships.

- Product Portfolio: Classic milk teas, fresh fruit teas, signature CoCo series, seasonal and collaboration special editions, coffee-tea hybrids.

- Recent Developments: Diablo IV brand collaboration (October 2023) with exclusive flavors and in-game benefits; expanded SEA and Middle East franchise network throughout 2024.

- Strategic Focus: Brand partnership innovation, Asia Pacific dominance, international franchise acceleration, and product novelty-driven traffic generation.

Chatime

Chatime is among the world's prominent bubble tea franchise networks by total outlet count, with presence in over 50 countries. The brand targets the middle-market consumer segment with a broad menu and accessible price points.

- Product Portfolio: Pearl milk tea, fruit teas, yogurt-based drinks, taro series, seasonal offerings, and customizable sugar/ice level beverages.

- Recent Developments: Expanded franchise presence in Latin America and Eastern Europe in 2024; launched plant-based milk alternatives across key Western markets.

- Strategic Focus: Global scale, accessible pricing, broad menu diversity, and franchise model standardization for rapid geographic expansion.

Kung Fu Tea

Kung Fu Tea is the leading bubble tea chain in the United States, with over 350 locations across North America as of 2025. Founded by Taiwanese entrepreneurs in Queens, New York in 2010, the brand has become synonymous with authentic bubble tea in the U.S. market.

- Product Portfolio: Classic milk teas, fresh teas, slush, smoothies, signature Kung Fu milk tea, brown sugar series, and seasonal specials.

- Recent Developments: Continued U.S. franchise expansion targeting Midwest and Sun Belt markets; enhanced mobile ordering and loyalty rewards ecosystem in 2024.

- Strategic Focus: U.S. market leadership, franchise growth into underserved U.S. geographies, digital ordering investment, and menu innovation.

Market Concentration Analysis

The global bubble tea market is structurally fragmented at the outlet level, the vast majority operated by independent local businesses or small regional chains.

In mature markets including Taiwan, China, and the United States, market concentration at the branded franchise tier is higher, with franchise chains representing 40–50% of revenue in urban premium segments. In emerging markets including India, Eastern Europe, and Sub-Saharan Africa, independent operators and regional chains dominate, creating significant white space for international franchise entry at premium price tiers.

Consolidation at the franchise and brand tier is expected to accelerate through 2034, as private equity investment in premium bubble tea franchise networks increases and smaller regional chains seek brand and operational support through acquisition or licensing partnerships. The market is expected to see significant brand acquisitions or franchise licensing deals annually through 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Ready-to-drink bottled bubble tea plant-based and functional ingredient formulations and e-commerce DIY bubble tea kit sales represent the highest-growth investment vectors through 2034. These segments collectively address a total addressable market exceeding USD 1.5 Billion by 2034.

Emerging Market Expansion

The Middle East and Africa region's estimated 9.2% CAGR represents the highest regional growth opportunity. UAE, Saudi Arabia, and Egypt are experiencing rapid bubble tea outlet expansion backed by young populations and mall-centric F&B consumption culture. India's bubble tea market is growing consistently, with Tier-1 and Tier-2 cities providing high-growth franchise opportunities for international brands.

Technology and Innovation Investment Trends

- Bubble tea equipment and automation manufacturers supplying precision preparation machines and automated pearl cooking systems are experiencing strong B2B demand growth from rapid franchise network expansion.

- DIY bubble tea kit brands and subscription services are capturing the at-home preparation market, with e-commerce-first brands including Boba Bam and Tea Drops attracting consumer goods investment.

- Social commerce and influencer marketing platforms are emerging as critical distribution and awareness channels, with brands investing in dedicated creator partnership programs and viral product development pipelines.

Future Market Outlook (2026-2034)

The global bubble tea market is poised for sustained, consumer-driven growth through 2034, anchored by demographic demand expansion among Gen-Z and millennial consumers, ongoing franchise network penetration into underdeveloped markets, and product category evolution toward health-conscious and functional formulations.

Product innovation will be the primary competitive battleground. Brands that successfully navigate the tension between indulgent, visually spectacular products that generate social media virality and health-conscious, clean-ingredient formulations that satisfy growing wellness demand will capture the widest demographic range. The emergence of functional bubble tea, incorporating adaptogens, probiotics, collagen, and nootropics, represents the highest premium opportunity of the next decade.

By 2034, the bubble tea category is expected to be firmly established as a mainstream global beverage category in all major consumer markets, with branded international franchise chains representing a larger share of total outlet count as consolidation accelerates.

Research Methodology

Primary Research

Primary research for this report included structured interviews and surveys conducted with over 150 industry participants in 2024–2025, comprising bubble tea franchise operators, ingredient and equipment suppliers, retail buyers, food service distributors, and end consumers across Asia Pacific, North America, Europe, and the Middle East.

Secondary Research

Secondary research encompassed a comprehensive review of company press releases, franchise disclosure documents, trade publications (QSR Magazine, Food Business News, Nation's Restaurant News), industry databases (Euromonitor, Mintel), and publicly available market data including government trade statistics and tea industry association reports. Over 250 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of bottom-up outlet count and average revenue per outlet modeling, combined with top-down consumer expenditure analysis incorporating tea consumption data, café culture penetration rates, and social media trend analytics.

Bubble Tea Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Base Ingredients Covered | Black Tea, Green Tea, Oolong Tea, White Tea |

| Flavors Covered | Original Flavor, Coffee Flavor, Fruit Flavor, Chocolate Flavor, Others |

| Components Covered | Flavor, Creamer, Sweetener, Liquid, Tapioca Pearls, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Gong Cha, Tiger Sugar, CoCo Fresh Tea & Juice, TP Tea, Chatime, Kung Fu Tea, Lollicup, Boba Guys, Quickly, Sharetea, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the bubble tea market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global bubble tea market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the bubble tea industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Bubble Tea Market Report

The market is forecast to grow at a CAGR of 6.28% during 2026-2034, driven by franchise expansion, social media influence, product innovation, and rising disposable incomes globally.

Asia Pacific is the leading region with a 37.6% share in 2025, anchored by Taiwan's origin position, China's massive domestic market, and broad adoption across Southeast Asia.

The Middle East and Africa is the fastest-growing region at an estimated 9.2% CAGR, driven by young urban populations, mall culture, and expanding international franchise entry in GCC markets.

Key drivers include social media and influencer marketing, rapid franchise network expansion, rising disposable incomes and urbanization, health-conscious product innovation, and youth café culture adoption globally.

Black tea leads with a 45.6% share in 2025, valued for its rich flavor, versatility for flavor pairing, and role as the classic foundational bubble tea base since the category's origin.

Fruit flavor leads with a 38.3% share in 2025, driven by its vibrant visual appeal, social media shareability, and the popularity of taro, mango, strawberry, and passion fruit variants globally.

Leading companies include Gong Cha, Tiger Sugar, CoCo Fresh Tea & Juice, TP Tea, Chatime, Kung Fu Tea, Lollicup, Boba Guys, Quickly, and Sharetea.

The global bubble tea market is projected to reach USD 3.9 Billion by 2030, reflecting steady compound growth from the 2025 base at the market's 6.28% CAGR.

High-growth opportunities include RTD bottled boba retail expansion, DIY bubble tea kit e-commerce, plant-based and functional formulations, emerging market franchise entry (India, GCC, Eastern Europe), and digital loyalty technology platforms.

Key challenges include high sugar health concerns driving reformulation pressure, raw material price volatility (tapioca, tea), intense competition and outlet fragmentation, delivery quality degradation of tapioca pearls, and evolving sugar labeling regulations across EU and Asian markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade