Bunker Fuel Market Size, Share, Trends and Forecast by Fuel Type, Vessel Type, Seller, and Region, 2026-2034

Global Bunker Fuel Market Size, Share, Trends & Forecast (2026-2034)

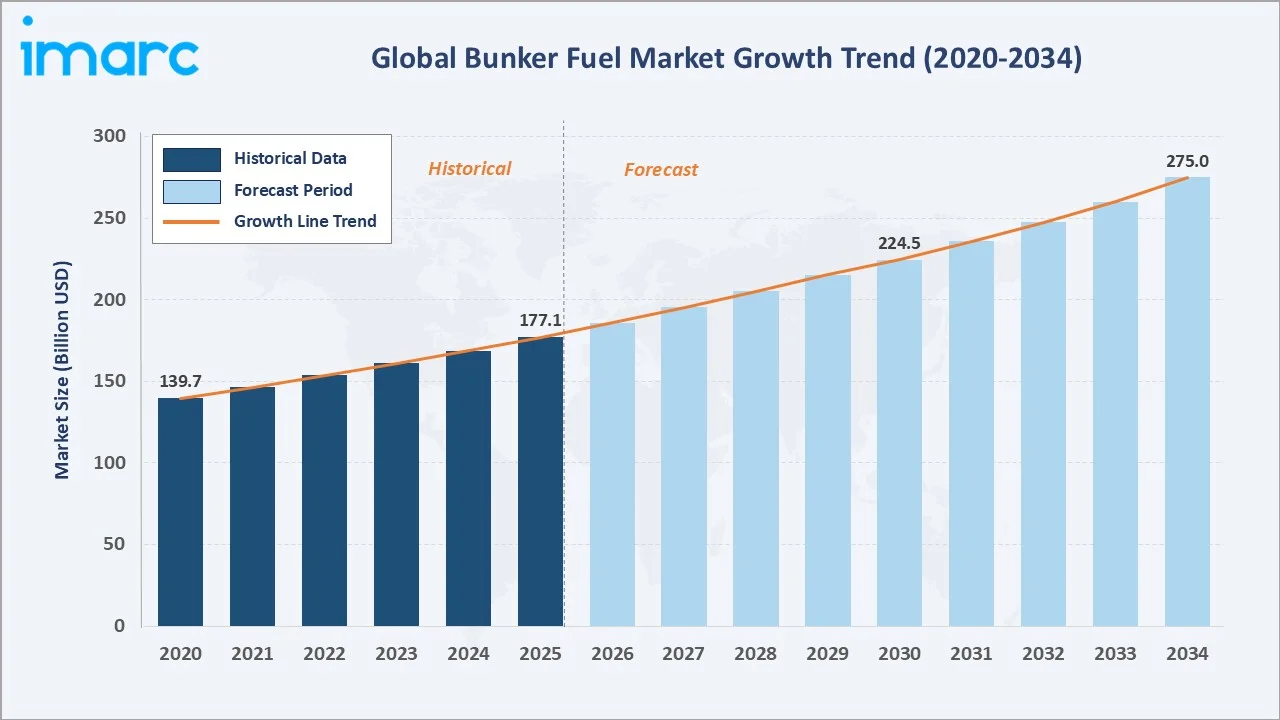

The global bunker fuel market size reached USD 177.1 Billion in 2025 and is projected to reach USD 275.0 Billion by 2034, exhibiting a CAGR of 4.86% during 2026-2034. Expanding global maritime trade volumes, IMO 2020 sulphur cap compliance driving VLSFO demand, and growing LNG bunkering infrastructure are the primary growth drivers.

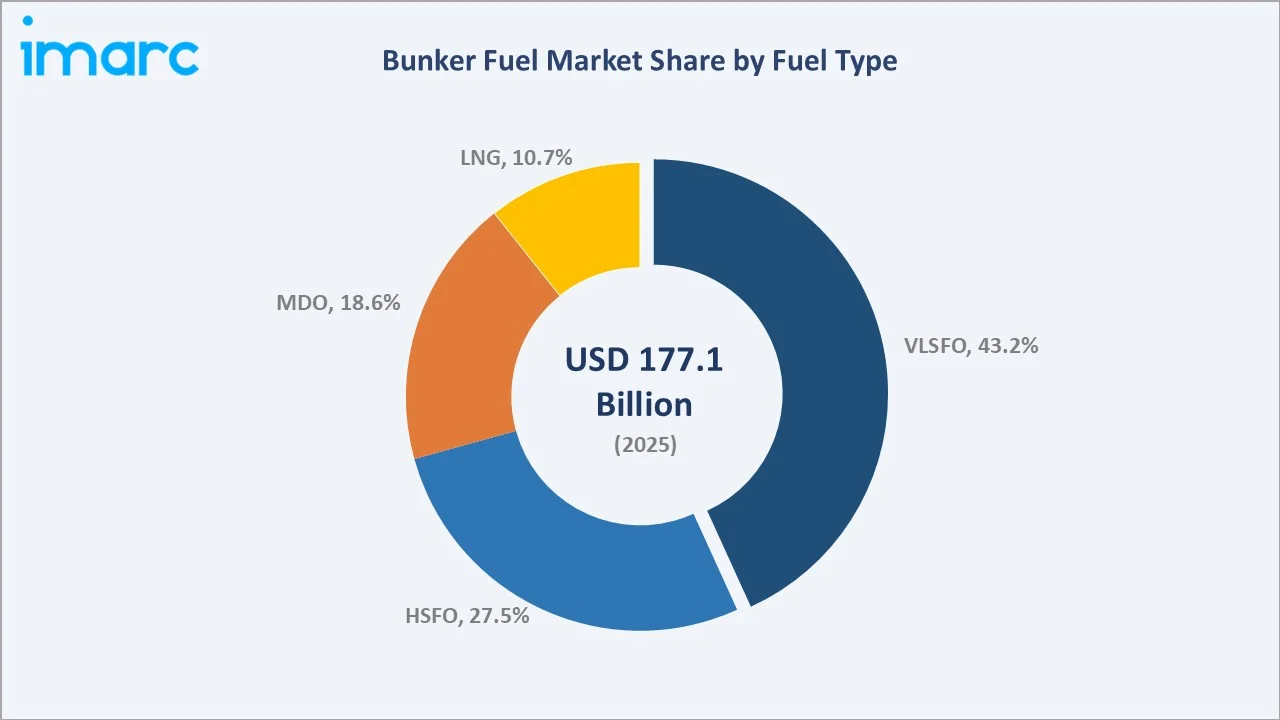

Very Low Sulfur Fuel Oil (VLSFO) dominates fuel type at 43.2% in 2025, driven by regulatory compliance mandates.

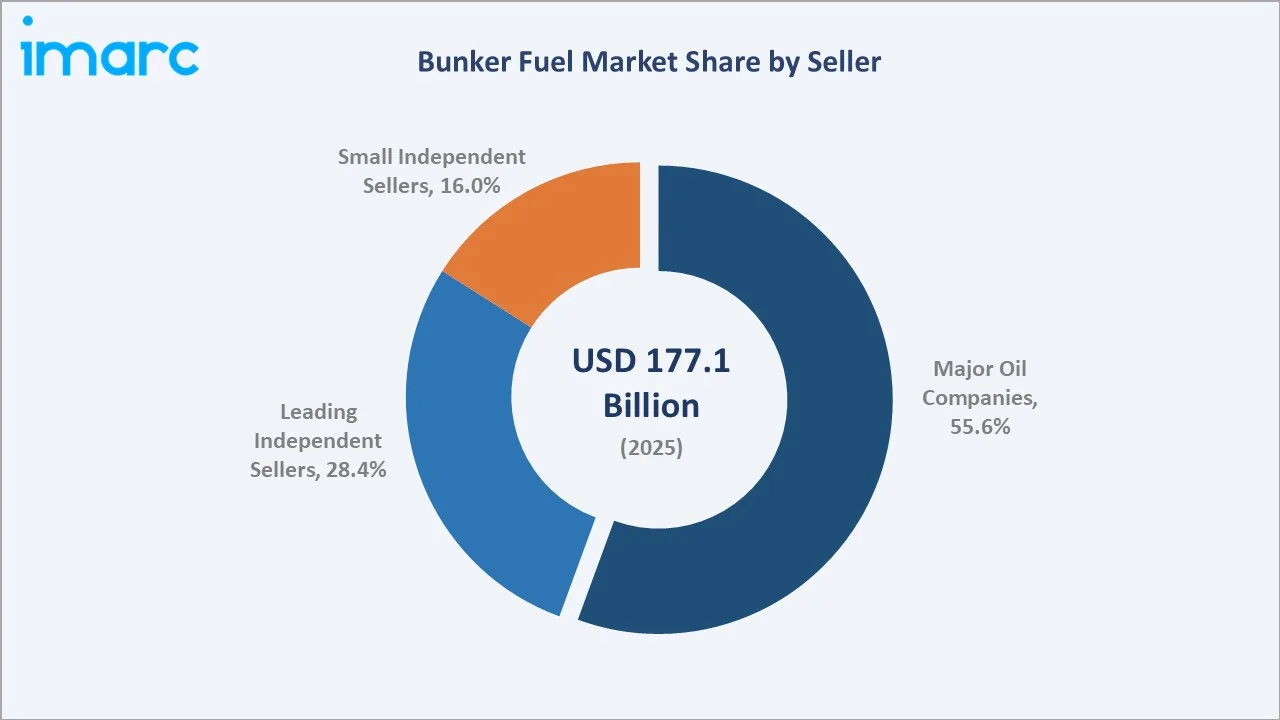

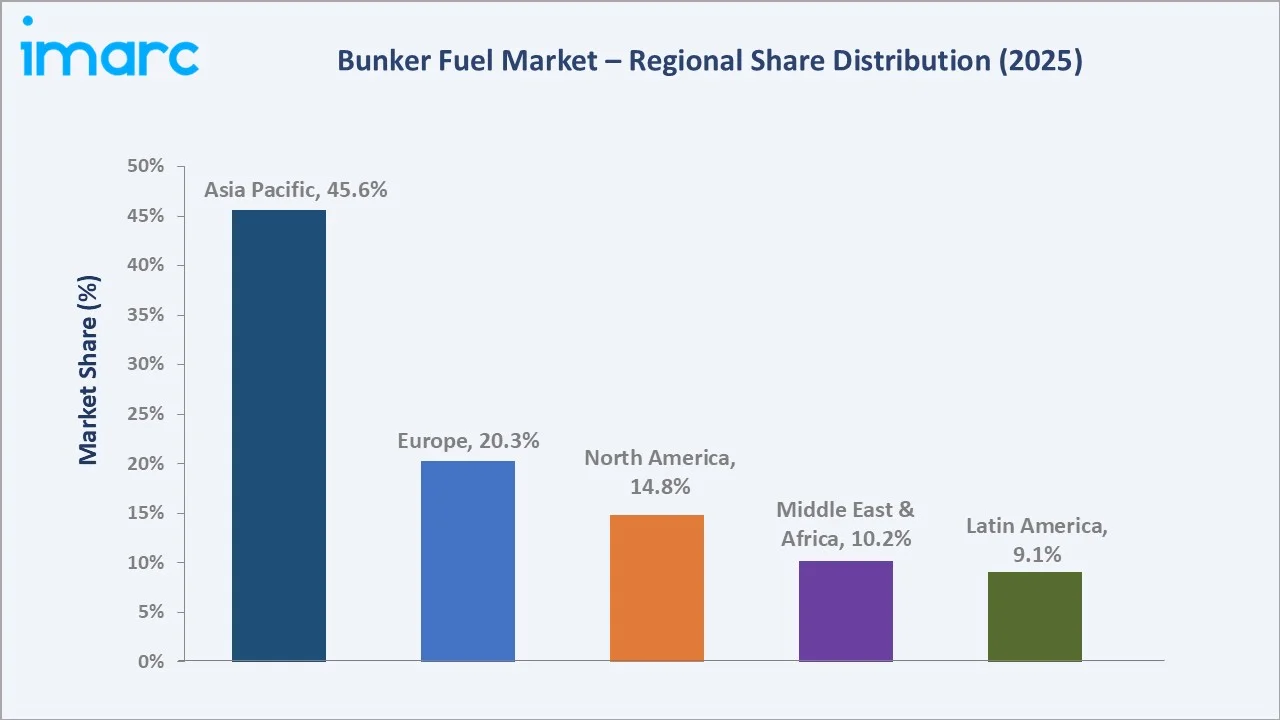

Major Oil Companies hold a commanding 55.6% seller share in 2025. Asia Pacific commands a 45.6% regional share in 2025, anchored by Singapore and Shanghai as the world's leading bunkering hubs.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 177.1 Billion |

|

Forecast Market Size (2034) |

USD 275.0 Billion |

|

CAGR (2026-2034) |

4.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (45.6% share, 2025) |

|

Second Largest Region |

Europe (20.3% share, 2025) |

|

Leading Seller |

Major Oil Companies (55.6%, 2025) |

|

Leading Fuel Type |

Very Low Sulfur Fuel Oil – VLSFO (43.2%, 2025) |

The bunker fuel market growth trajectory from 2020 through 2034, expanding from USD 139.7 Billion to USD 275.0 Billion, reflects the non-discretionary nature of marine fuel demand. Rising seaborne trade volumes and decarbonization-driven fuel transitions underpin sustained market expansion through the forecast period.

To get more information on this market, Request Sample

The CAGR trajectories across key fuel type, seller, and regional sub-segments, with LNG bunkering at ~9.2% CAGR and Middle East & Africa at ~5.9% CAGR, represent the fastest-growing categories within the global bunker fuel industry through 2034.

Executive Summary

The global bunker fuel market is on a sustained growth trajectory from USD 177.1 Billion in 2025 to USD 275.0 Billion by 2034. Bunker fuel, the primary energy source for commercial shipping including container vessels, bulk carriers, tankers, and cruise ships, benefits from the essential and non-discretionary nature of maritime trade.

VLSFO dominates fuel type at 43.2% in 2025, reflecting mandatory compliance with IMO 2020 sulphur cap regulations. High Sulfur Fuel Oil (HSFO) at 27.5% is retained by scrubber-equipped vessels benefiting from its price differential. Marine Diesel Oil (MDO) at 18.6% serves smaller vessels and port operations. LNG at 10.7% is the fastest-growing segment, driven by newbuild fleet specifications.

Major Oil Companies dominate the seller landscape at 55.6% in 2025, reflecting integrated supply chain advantages of global energy majors. Leading Independent Sellers at 28.4% compete on regional expertise and pricing flexibility.

Asia Pacific commands 45.6%, underpinned by Singapore as the world's largest bunkering port handling over 50 million tonnes annually.

Key Market Insights

|

Insight |

Data |

|

Largest Seller Category |

Major Oil Companies – 55.6% share (2025) |

|

Leading Fuel Type |

VLSFO – 43.2% share (2025) |

|

Leading Region |

Asia Pacific – 45.6% share (2025) |

|

Second Largest Region |

Europe – 20.3% share (2025) |

|

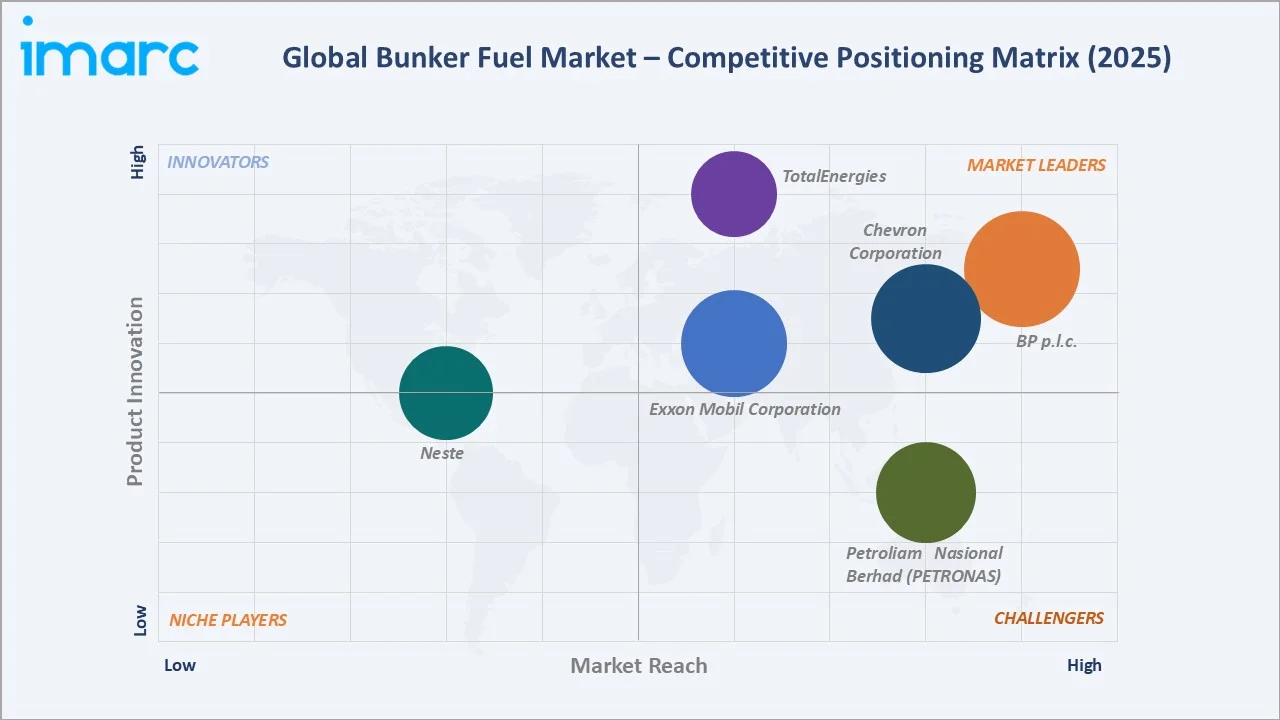

Top Companies |

BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, Neste, Petroliam Nasional Berhad (PETRONAS), TotalEnergies |

Key Analytical Observations Expanding On The Above Data:

- VLSFO, commanding 43.2% in 2025, dominates because IMO 2020 mandated a 0.5% global sulphur cap on marine fuels, forcing most of the fleet to transition from HSFO. Its compliance profile and widespread port availability make it the default fuel for commercial vessels globally.

- Major Oil Companies, with 55.6% seller share in 2025, dominate because integrated energy majors provide consistent quality, regulatory compliance documentation, credit facilities, and global port coverage that independent sellers cannot match at scale.

- Asia Pacific's 45.6% dominance in 2025 reflects Singapore's position as the world's largest bunkering port combined with China's Zhoushan hub expansion and the high intra-Asia maritime traffic density along major east-west trade routes.

- Europe's 20.3% share reflects Rotterdam's position as the largest European bunkering hub and the region's advanced LNG bunkering infrastructure, supporting the transition toward greener marine fuels under EU regulatory pressure.

Global Bunker Fuel Market Overview

Bunker fuel refers to marine fuel oil used by ships and large vessels for propulsion and auxiliary power generation. The market spans residual fuel oils (HSFO, VLSFO) and distillate fuels (MGO, MDO) through to alternative fuels including LNG, methanol, and ammonia. Global supply chain integration connects crude oil producers, refiners, blenders, traders, terminal operators, port bunkering companies, and end-use shipping companies.

The global ecosystem is anchored by four major bunkering hubs—Singapore, Rotterdam, Fujairah, and Houston—which collectively account for approximately 40% of global bunker fuel volumes. IMO 2020 sulphur regulations, IMO 2050 GHG reduction targets, and EU FuelEU Maritime regulation are driving structural transformation across fuel types, vessel designs, and port infrastructure throughout the forecast period.

Market Dynamics

To evaluate market opportunities, Request Sample

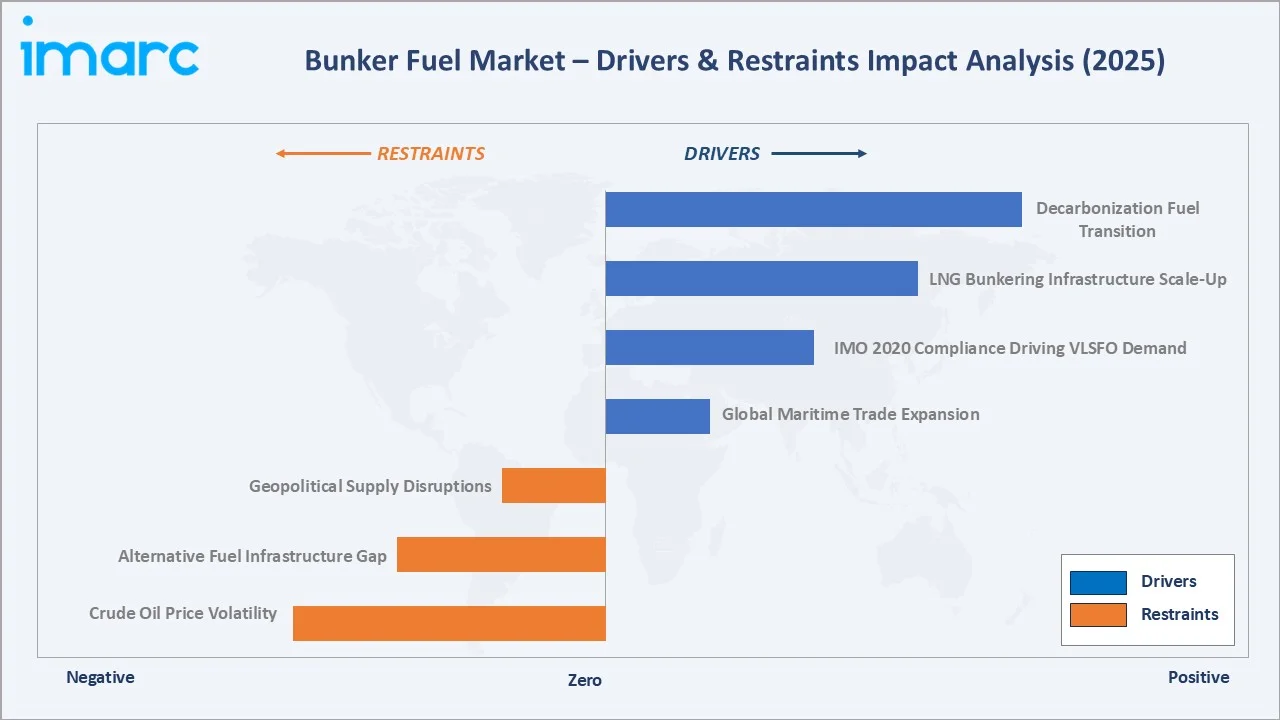

Market Drivers

- Global Maritime Trade Expansion: The International Maritime Organization estimates global seaborne trade exceeded 11 billion tonnes in 2022, with container throughput at major ports recovering to record levels post-pandemic. Rising consumer goods demand, raw material flows, and energy commodity trade are driving sustained vessel activity and corresponding bunker fuel consumption across major shipping lanes.

- IMO 2020 Compliance Driving VLSFO Demand: The IMO 2020 global 0.5% sulphur cap effective January 2020 structurally shifted demand from HSFO to VLSFO across the global fleet. With approximately 95,000 commercial vessels requiring compliant fuel and limited scrubber retrofitting at approximately 5,000 vessels, VLSFO demand is structurally embedded as the primary fuel type through the forecast period.

- LNG Bunkering Infrastructure Scale-Up: Global LNG bunkering infrastructure is expanding steadily in response to rising demand for cleaner marine fuels, with a growing number of LNG-fueled vessels entering the global fleet. Investments in bunkering terminals across major maritime hubs and emerging ports are enhancing fuel availability and supporting wider adoption among shipping operators. As key ports continue to strengthen their LNG supply capabilities, these developments are collectively driving sustained growth in the LNG bunkering market, with strong long-term expansion anticipated.

Market Restraints

- Crude Oil Price Volatility: Bunker fuel prices are directly correlated with crude oil benchmark movements, with Rotterdam VLSFO price ranging from USD 350-750 per tonne in 2020-2024. Price volatility creates hedging challenges for ship operators and introduces working capital risk for bunker fuel traders, potentially contracting trading margins in high-volatility periods.

- Alternative Fuel Infrastructure Gap: Despite growing LNG, methanol, and ammonia bunkering interest, infrastructure remains concentrated at fewer than 50 ports globally. The limited availability of alternative fuel bunkering creates range anxiety for operators considering fleet transitions, slowing adoption velocity outside primary hub ports.

Market Opportunities

- Decarbonization Fuel Transition: IMO 2050 net-zero GHG targets and EU FuelEU Maritime requirements are creating demand for bio-LNG, green methanol, and ammonia bunker fuels. Bio-blended marine fuel programs combining VLSFO or MGO with hydrotreated vegetable oil represent growing premium revenue pools, with alternative fuel bunkering market increasing during the forecast period.

- Digital Bunkering Platform Adoption: Digital platforms integrating real-time fuel pricing, quality verification, and logistics coordination are emerging as competitive differentiators. These bunkering solutions are improving transaction transparency, reducing fuel quality disputes, and enabling data-driven procurement optimization for large fleet operators.

Market Challenges

- Geopolitical Supply Disruptions: Conflicts in the Red Sea and Black Sea regions have altered shipping routes, increasing voyage distances and fuel consumption per journey, while creating pricing volatility and supply security concerns for operators relying on established bunkering corridors.

- Regulatory Complexity and Compliance Costs: Simultaneous compliance requirements across IMO 2020 sulphur limits, GHG Carbon Intensity Indicators, EU ETS carbon costs from 2024, and FuelEU Maritime requirements from 2025 create multi-layered compliance costs for operators managing fuel procurement.

Emerging Market Trends

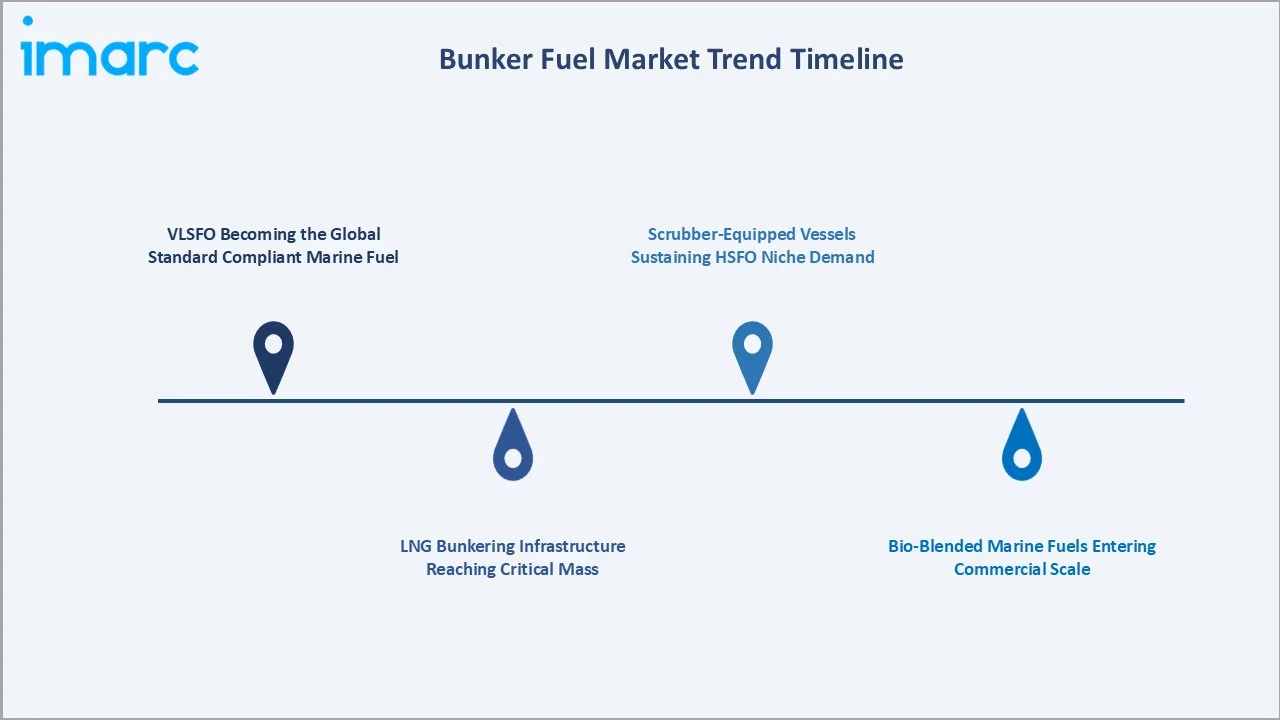

1. VLSFO Becoming the Global Standard Compliant Marine Fuel

Post-IMO 2020 implementation, VLSFO has established itself as the global baseline marine fuel standard. Port infrastructure at all major bunkering hubs has expanded VLSFO storage capacity, and major oil companies have optimized their refinery configurations to maximize VLSFO yield. VLSFO's 43.2% market share in 2025 is expected to remain dominant through 2034 as alternative fuels gradually increase their share.

2. LNG Bunkering Infrastructure Reaching Critical Mass

Global LNG-fueled vessel orderbook reached 500+ ships by 2024, driven by major container and cruise fleet programs. LNG bunkering terminal investments at Singapore, Rotterdam, and new South Korean and Chinese LNG bunkering facilities are enabling broader LNG adoption, supporting the segment's growth through 2034.

3. Bio-Blended Marine Fuels Entering Commercial Scale

Bio-blended marine fuel programs combining VLSFO or MGO with hydrotreated vegetable oil (HVO) and FAME blends are scaling commercially. Regulatory momentum in European ports supporting marine bio-blends toward renewable energy targets is creating policy support for bio-bunker commercialization across key port hubs.

4. Scrubber-Equipped Vessels Sustaining HSFO Niche Demand

Approximately 5,000 vessels globally have installed exhaust gas cleaning scrubbers, enabling continued HSFO consumption at a significant price discount to VLSFO, typically USD 100-150 per tonne.

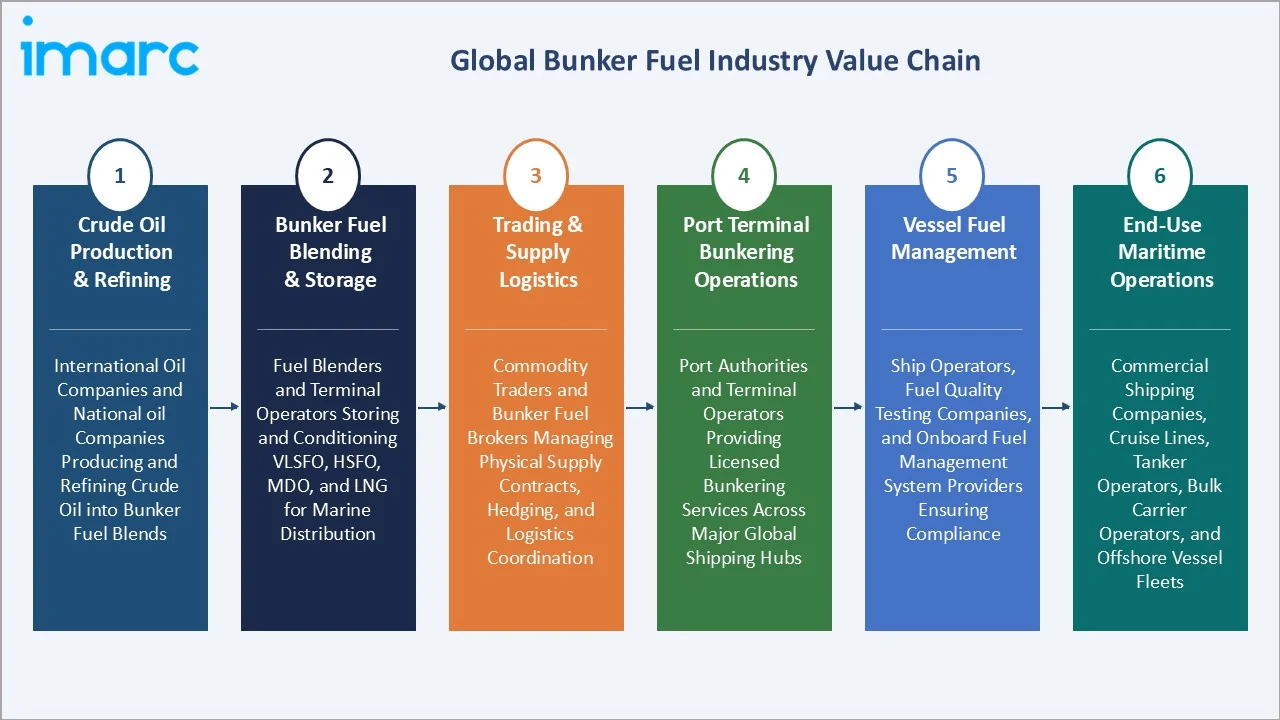

Industry Value Chain Analysis

The bunker fuel value chain spans six stages from crude oil production through end-use vessel operations. Trading and port terminal bunkering stages capture the highest commercial margins; while blending and quality assurance generate value-add premiums in the post-IMO 2020 compliant fuel environment. Vertical integration across production and distribution confers cost and quality advantages.

|

Stage |

Description |

|

Crude Oil Production & Refining |

International oil companies and national oil companies producing and refining crude oil into bunker fuel blends |

|

Bunker Fuel Blending & Storage |

Fuel blenders and terminal operators storing and conditioning VLSFO, HSFO, MDO, and LNG for marine distribution |

|

Trading & Supply Logistics |

Commodity traders and bunker fuel brokers managing physical supply contracts, hedging, and logistics coordination |

|

Port Terminal Bunkering Operations |

Port authorities and terminal operators providing licensed bunkering services across major global shipping hubs |

|

Vessel Fuel Management |

Ship operators, fuel quality testing companies, and onboard fuel management system providers ensuring compliance |

|

End-Use Maritime Operations |

Commercial shipping companies, cruise lines, tanker operators, bulk carrier operators, and offshore vessel fleets |

Integrated participants with captive refinery production, terminal storage, and direct vessel supply capabilities achieve cost and quality advantages over traders relying on spot market fuel procurement. This vertical integration is a significant competitive advantage in the premium VLSFO and LNG bunkering market segments.

Technology Landscape in the Bunker Fuel Industry

Fuel Blending and Quality Optimization Technology

Advanced refinery blending configurations are enabling precise VLSFO formulation to meet ISO 8217 viscosity, stability, and compatibility specifications. Near-infrared spectroscopy and inline blending control systems are reducing quality variation in VLSFO production, minimizing the risk of incompatible fuel blending incidents that cause costly vessel engine failures.

Exhaust Gas Cleaning Scrubber Technology

Open-loop and closed-loop exhaust gas cleaning systems enabling HSFO combustion within an IMO 2020-compliant framework represent a USD 3-5 million per vessel capital investment. Hybrid scrubber technology allowing switching between open and closed loop modes based on port regulations is gaining adoption, with approximately 5,000 vessels globally equipped with operational scrubbers as of 2024.

Digital Bunkering and Fuel Management Systems

Mass Flow Meter bunkering systems mandated at Singapore since 2014 are being adopted at additional major ports, improving measurement accuracy and reducing fuel quantity disputes. Digital platforms integrating mass flow meter data, fuel quality certificates, and delivery documentation are creating auditable chain-of-custody records that reduce fraud and quality management costs.

LNG Bunkering Transfer Technology

Ship-to-ship, truck-to-ship, and pipeline-to-ship LNG transfer technologies are expanding LNG bunkering accessibility beyond dedicated LNG bunkering vessels. Cryogenic flexible hose systems and standardized LNG manifold connections are reducing bunkering time and safety risks, supporting broader LNG fleet adoption across vessel categories.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Fuel Type | Very Low Sulfur Fuel Oil (VLSFO) | 43.2% | 2025 |

| Vessel Type | Containers | 40.0% | 2025 |

| Seller | Major Oil Companies | 55.6% | 2025 |

| Region | Asia Pacific | 45.6% | 2025 |

By Seller

Major oil companies command a 55.6% majority share in 2025, reflecting the integrated supply chain advantages of global energy majors providing VLSFO, HSFO, MDO, and LNG across their extensive port networks. Their global reach, quality assurance systems, credit facilities, and regulatory compliance capabilities justify their market leadership position.

To access detailed market analysis, Request Sample

Leading independent sellers at 28.4% in 2025 compete through regional expertise, flexible pricing structures, and value-added services including fuel quality testing and logistics coordination, serving regional customers with responsive local presence.

Small independent sellers at 16.0% operate in niche geographic markets and specialized fuel segments, serving port-specific demand where global majors do not maintain a direct presence.

By Fuel Type

VLSFO leads at 43.2% in 2025, established as the global standard compliant marine fuel following IMO 2020 sulphur cap implementation. Extensive port infrastructure investment in VLSFO storage capacity and the cost-prohibitiveness of scrubber retrofitting for most of the global fleet ensure VLSFO's continued dominance through the forecast period.

HSFO at 27.5% in 2025 is sustained by scrubber-equipped vessels benefiting from a significant price differential versus VLSFO. MDO at 18.6% serves smaller coastal vessels and port operations.

LNG at 10.7% is the fastest-growing segment at approximately 9.2% CAGR through 2034, driven by newbuild vessel specifications and expanding LNG bunkering infrastructure across key global ports.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

45.6% |

Singapore & Shanghai bunkering hubs; high maritime traffic; port infrastructure expansion; growing LNG bunkering |

|

Europe |

20.3% |

Rotterdam, Antwerp, Gibraltar hubs; IMO compliance-driven VLSFO demand; LNG bunkering growth; EU decarbonization regulation |

|

North America |

14.8% |

US Gulf Coast LNG export fleet bunkering; Houston and New York hubs; fleet modernization programs |

|

Middle East & Africa |

10.2% |

Fujairah strategic bunkering hub; Sub-Saharan African port expansion; growing offshore activity |

|

Latin America |

9.1% |

Panama Canal transit fueling; Santos hubs; offshore support vessel fuel demand |

Asia Pacific's 45.6% market dominance in 2025 is driven by Singapore's position as the world's largest bunkering port handling over 50 million tonnes annually and China's Zhoushan-Ningbo bunkering hub, the world's second largest by volume. Japan, South Korea, and emerging Southeast Asian ports contribute meaningfully to regional demand growth.

Europe's 20.3% share reflects Rotterdam's dominance as Europe's primary bunkering hub and the region's advanced LNG bunkering infrastructure. EU ETS carbon pricing effective for the maritime sector from 2024 is accelerating VLSFO and LNG adoption, with Rotterdam already operating multiple LNG bunkering vessels and methanol bunkering pilots at major North Sea ports.

Competitive Landscape

The global bunker fuel market is moderately consolidated, with major integrated oil companies holding leading positions in their home markets while competing globally. Asia Pacific bunkering is served by global majors and regional specialists, while North American and European markets have established competitive ecosystems with distinct dynamics and fuel transition trajectories.

|

Company Name |

Key Products |

Position |

Global Strategic Focus |

|

BP p.l.c. |

Marine Fuels, NGL, LNG |

Leader |

Global integrated energy; extensive bunkering network across 100+ ports; IMO 2020 compliant fuels |

|

Chevron Corporation |

High sulphur fuel oil (HSFO), Very low sulphur fuel oil (VLSFO), Marine gas oil (MGO) |

Leader |

US energy major; Pacific Rim bunkering strength; advanced lubricants differentiation |

|

Exxon Mobil Corporation |

Marine fuel oils |

Leader |

Global integrated oil major; low-sulfur fuel transition leader; digital fuel management tools |

|

Neste |

Marine Fuel |

Emerging |

Finland-based; renewable fuels pioneer; HVO-based marine biofuel leader; decarbonization positioned |

|

Petroliam Nasional Berhad (PETRONAS) |

LNG Bunker, Marine Fuel |

Challenger |

Malaysia national oil company; Singapore hub strength; Asia Pacific VLSFO supply scale |

|

TotalEnergies |

Marine fuels, LNG, biofuels |

Leader |

120+ port presence; LNG bunkering infrastructure investment; bio-blended fuel pioneer |

Key players include BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, Neste, Petroliam Nasional Berhad (PETRONAS), TotalEnergies, and others.

Key Company Profiles

BP p.l.c.

BP Marine is a leading global bunker fuel supplier with operations across major international ports including Rotterdam, Singapore, Fujairah, and Houston. BP provides an extensive range of IMO 2020-compliant marine fuels with advanced quality documentation and credit facilities for fleet operators managing large fuel procurement budgets.

- Product Portfolio: Marine Fuels, NGL, LNG, and others

- Recent Developments: In December 2021, BP successfully collaborated with Maersk Tankers to conduct marine biofuel trials, demonstrating the viability of biofuel-blended marine fuels as a scalable, lower-carbon solution for the shipping industry. The trials validated the use of biofuels as a “drop-in” alternative, requiring no engine modifications while maintaining operational performance and reliability across vessel systems.

- Strategic Focus: BP's marine fuel strategy focuses on quality assurance leadership, digital bunkering solutions, and expanding low-carbon fuel options including LNG and biofuels, targeting fleet operators with sustainability mandates and decarbonization targets.

TotalEnergies

TotalEnergies operates at over 120 ports globally, providing one of the broadest marine fuel product ranges including VLSFO, LNG, and biofuels. The company is a pioneer in bio-blended marine fuels and LNG bunkering investments across European and Asian port networks, positioning for EU FuelEU Maritime requirements.

- Product Portfolio: Marine fuels, LNG, biofuels, and others

- Recent Developments: In July 2025, TotalEnergies entered a strategic 50:50 joint venture with CMA CGM to develop and operate an LNG bunkering logistics solution, reinforcing its position in the marine fuels value chain and supporting the decarbonization of maritime transport. The partnership will deliver an integrated LNG supply service in the Amsterdam–Rotterdam–Antwerp (ARA) region.

- Strategic Focus: TotalEnergies differentiates through LNG bunkering infrastructure investment and bio-blended marine fuel commercialization, positioning for EU FuelEU Maritime regulation requirements and IMO GHG reduction mandates shaping demand through 2034.

Exxon Mobil Corporation

ExxonMobil provides post-IMO 2020-compliant marine fuels including VLSFO, MDO, and advanced marine cylinder oils across its global marine fuel supply network. The company has developed an engineered marine fuels range specifically designed to meet evolving regulatory and operational requirements for modern two-stroke engine fleets.

- Product Portfolio: Marine fuel oils

- Recent Developments: In October 2025, ExxonMobil announced its entry into the LNG marine bunkering market, chartering two LNG bunker vessels, to deliver LNG and bio-LNG fuel solutions for the maritime sector. The vessels will form the foundation of its LNG supply capabilities, while complementary logistics solutions are being developed to enable early market access ahead of vessel deliveries.

- Strategic Focus: ExxonMobil's marine fuel strategy focuses on technical fuel quality differentiation, advanced lubricants supply, and digital fuel management services targeting premium fleet operator segments across major global bunkering hubs.

Market Concentration Analysis

The global bunker fuel market is moderately concentrated at the seller level, with Major Oil Companies collectively holding 55.6% of supply in 2025. The five largest integrated oil majors collectively supply an estimated 35-40% of global bunker volumes through their integrated refinery-to-port distribution networks, conferring significant scale and quality assurance advantages.

Independent sellers including large-scale independent distributors and bunker holding companies hold the 28.4% Leading Independent share through regional expertise and flexible pricing. Market consolidation is occurring through digital platform integration and sustainability-driven mergers as fuel transition investments favour well-capitalised players with infrastructure scale.

Investment & Growth Opportunities

Fastest-Growing Segments

LNG bunkering at ~9.2% CAGR through 2034 is the highest-growth fuel type segment, driven by newbuild LNG-fueled vessel deliveries and expanding port LNG infrastructure. Middle East & Africa at ~5.9% CAGR represents the fastest-growing regional opportunity, anchored by Fujairah's growing role as an east-west trade bunkering hub and African offshore vessel demand.

Emerging Markets

Southeast Asia, particularly Vietnam and Indonesia, represents emerging bunkering hub investment opportunities as regional manufacturing and trade volumes expand. West African ports are attracting bunker fuel investment as offshore oil and gas operations expand vessel traffic, creating incremental demand for compliant marine fuels beyond existing hub capacity.

Venture & Investment Trends

Private equity investment in digital bunkering platforms, bio-marine fuel blending facilities, and LNG bunkering vessels is accelerating. Green ammonia and methanol fuel production facilities serving the maritime sector are attracting infrastructure investment from energy transition funds, with first commercial scale methanol bunkering operations expected at Rotterdam and Singapore during the forecast period.

Future Market Outlook (2026-2034)

The global bunker fuel market is forecast to expand from USD 177.1 Billion in 2025 to USD 275.0 Billion by 2034 at a CAGR of 4.86%, adding USD 97.9 Billion in incremental annual market value over the forecast period. This sustained growth reflects structurally growing maritime trade volumes and the expanding per-tonne value of compliant and alternative marine fuels.

Three transformative forces will reshape the market through 2034: progressive decarbonization mandates requiring greener fuel procurement, expanding LNG and bio-fuel infrastructure enabling practical fleet transitions, and digital bunkering platforms improving supply chain efficiency. VLSFO will remain dominant but gradually cede share to LNG, methanol, and ammonia as port infrastructure reaches critical mass globally.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews with bunker fuel market stakeholders including senior commercial managers at oil majors, independent fuel suppliers, port terminal operators, shipping company fuel procurement directors, and IMO regulatory affairs specialists. Primary data validated market sizing, seller and fuel type segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include IMO Marine Environment Protection Committee reports, IBIA annual reviews, Singapore MPA bunkering statistics, Port of Rotterdam bunker fuel delivery reports, IEA Oil Market Reports (2020-2024), DNV Alternative Fuels Insight database, and trade publications including Bunkerspot, Manifold Times, and Ship & Bunker.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating global seaborne trade volume indices, fleet size and fuel consumption data, regulatory compliance adoption curves, and alternative fuel infrastructure development timelines. Scenario analysis across base, optimistic, and conservative cases accounted for crude oil price volatility and regulatory implementation risk.

Bunker Fuel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Bunker Fuel Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fuel Types Covered | High Sulfur Fuel Oil (HSFO), Very Low Sulfur Fuel Oil (VLSFO), Marine Diesel Oil (MDO), Liquefied Natural Gas (LNG) |

| Vessel Types Covered | Containers, Tankers, General Cargo, Bulk Carrier, Others |

| Sellers Covered | Major Oil Companies, Leading Independent Sellers, Small Independent Sellers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, Neste, Petroliam Nasional Berhad (PETRONAS), TotalEnergies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the bunker fuel market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global bunker fuel market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the bunker fuel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Bunker Fuel Market Report

The global bunker fuel market reached USD 177.1 Billion in 2025, reflecting steady demand growth from expanding global maritime trade, IMO 2020 fuel transition completion, and recovering post-pandemic shipping volumes across all major vessel categories.

The market is projected to reach USD 275.0 Billion by 2034, growing at a CAGR of 4.86% during 2026-2034, driven by seaborne trade volume growth, LNG bunkering infrastructure expansion, and decarbonization-driven premium fuel adoption.

Major Oil Companies lead with a 55.6% seller share in 2025, with global integrated energy majors providing integrated supply chain coverage, quality assurance, and credit facilities across 700+ ports globally.

VLSFO leads at 43.2% in 2025, established as the global standard compliant marine fuel following IMO 2020's 0.5% sulphur cap, with widespread VLSFO storage infrastructure at all major bunkering ports supporting fleet compliance.

Asia Pacific commands a 45.6% market share in 2025, driven by Singapore's position as the world's largest bunkering port handling over 50 million tonnes annually, combined with China's expanding Zhoushan-Ningbo hub.

LNG is the fastest-growing fuel type at approximately 9.2% CAGR through 2034, driven by growing LNG-fueled vessel orderbook deliveries, expanding LNG bunkering terminal infrastructure, and shipping company decarbonization commitments.

Leading companies include BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, Neste, Petroliam Nasional Berhad (PETRONAS), TotalEnergies, and others.

Primary applications include propulsion and auxiliary power for container vessels, crude oil and product tankers, bulk carriers, general cargo ships, cruise ships, offshore supply vessels, and military naval vessels across international and coastal shipping routes.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade